Managerial Accounting: SleepEase Ltd's Costing and Performance

VerifiedAdded on 2020/07/22

|11

|3161

|57

Report

AI Summary

This report provides a comprehensive analysis of SleepEase Ltd's managerial accounting practices. It begins with an introduction to management accounting and its importance in business decision-making, followed by a detailed comparison of marginal and absorption costing methods, including their advantages and disadvantages. The report then presents profit and loss statements for 2015 and 2016 using both costing methods, along with interpretations of the financial results. The core of the report examines the decision of whether or not to award a bonus to Mr. Spenser, the sales manager, based on his performance and the company's financial outcomes, considering the requirements of the Bonus Act of 1965. It presents arguments for and against the bonus, providing insights into the complexities of performance evaluation and incentive structures within the company. The report concludes with a summary of the findings and their implications for SleepEase Ltd.

MANAGERIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................3

TASK 3............................................................................................................................................5

TASK 4............................................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

.........................................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................3

TASK 3............................................................................................................................................5

TASK 4............................................................................................................................................6

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

.........................................................................................................................................................9

INTRODUCTION

Management accounting is of utmost importance for administration of business

organisation. This form of accounting provides various reports to administration. Such reports

are helpful in decision making of business concern. There are two approaches followed by an

organisation i.e. Marginal costing and absorption costing. These approaches are very necessary

in decision making of inventory valuation and pricing. Every company spend massive amount of

time in deciding pricing of products and services being offered to customers. If prices are

appropriate as per quality, customers will be attracted towards products and vice-versa.

SleepEase Ltd. is one of the British well known manufacturer of mattresses. They provide

variety of mattresses to customers. They produces specialised bed named Max-ease. It is one of

the product designed to ease back pains for orthopaedic patients. The company SleepEase uses

performance management tool balanced scorecard to evaluate different aspects of their

businesses.

TASK 1

Marginal and Absorption costing

There are two methods by which organisation can value its inventory i.e. Absorption and

marginal costing method. These are the approaches that SleepEase uses to deal with fixed

overheads of production. This is based on the fact that whether to use fixed overheads in decision

making of administration i.e. inventory valuation and pricing of product and offerings. The main

difference between two methods is how they are using fixed overheads in costing techniques.

The elaboration of both techniques of costing are as follows-

Marginal costing- Such method of costing can be defined as variable costing. To make

right decision of production, both fixed and variable cost are computed. The marginal cost is one

the main consideration under such approach. This also determines impact on profitability for

change in output. under such costing technique, fixed overheads cost are not distributed to

products and offerings. when an additional unit of a product and offerings is manufactured, the

additional cost incurred will be termed as marginal cost. fixed cost remain same and unaffected.

More fixed cost are not incurred when the output is increased. The marginal cost is generally

variable cost of production that involves direct material, direct labour, direct expenses and

variable overheads. This shows the impact of variable cost on volume of production/output. This

1

Management accounting is of utmost importance for administration of business

organisation. This form of accounting provides various reports to administration. Such reports

are helpful in decision making of business concern. There are two approaches followed by an

organisation i.e. Marginal costing and absorption costing. These approaches are very necessary

in decision making of inventory valuation and pricing. Every company spend massive amount of

time in deciding pricing of products and services being offered to customers. If prices are

appropriate as per quality, customers will be attracted towards products and vice-versa.

SleepEase Ltd. is one of the British well known manufacturer of mattresses. They provide

variety of mattresses to customers. They produces specialised bed named Max-ease. It is one of

the product designed to ease back pains for orthopaedic patients. The company SleepEase uses

performance management tool balanced scorecard to evaluate different aspects of their

businesses.

TASK 1

Marginal and Absorption costing

There are two methods by which organisation can value its inventory i.e. Absorption and

marginal costing method. These are the approaches that SleepEase uses to deal with fixed

overheads of production. This is based on the fact that whether to use fixed overheads in decision

making of administration i.e. inventory valuation and pricing of product and offerings. The main

difference between two methods is how they are using fixed overheads in costing techniques.

The elaboration of both techniques of costing are as follows-

Marginal costing- Such method of costing can be defined as variable costing. To make

right decision of production, both fixed and variable cost are computed. The marginal cost is one

the main consideration under such approach. This also determines impact on profitability for

change in output. under such costing technique, fixed overheads cost are not distributed to

products and offerings. when an additional unit of a product and offerings is manufactured, the

additional cost incurred will be termed as marginal cost. fixed cost remain same and unaffected.

More fixed cost are not incurred when the output is increased. The marginal cost is generally

variable cost of production that involves direct material, direct labour, direct expenses and

variable overheads. This shows the impact of variable cost on volume of production/output. This

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

technique is also known as variable or direct costing method. This can be referred as changes in

total cost of production by producing one additional unit of output. Fixed cost are of less

importance than variable cost of production. It overall contributes to changes occurring because

of variable cost of production. It is one of the accounting system in which marginal cost are

charged to products and offerings while fixed cost is called as periodic cost. Fixed cost are

written off against contribution. Marginal costing are of utmost importance for taking

appropriate decision regarding pricing decisions of SleepEase Ltd. A firm is more concerned

about additional cost required in extra unit of output (Salehi, Rostami and Mogadam, 2010).

Contribution concept in marginal costing is also important in decision making aspect of business.

The main advantages and disadvantages of marginal costing techniques are as follows-

Advantages

Marginal costing technique of inventory valuation is one of the easier and simpler

method.

The fixed cost are not considered hence it helps in avoiding complicated statement.

The issue with under absorption and over absorption will not arise.

Contribution details will provide benefits in decision making aspects of SleepEase.

Disadvantages

The total cost cannot be segregated easily into different variable and fixed costs.

It is not easy to determine the variability degree of semi variable cost incurred in

production of products and offerings.

Tax authorities are not accepting such statements which excludes fixed manufacturing

overheads.

The administration cannot take quality decision based on contribution aspect of

production.

Absorption costing- Absorption costing is one of the cost technique where both fixed

and variable cost are considered. Here cost are grouped into centres to find out total cost of

production. Both fixed and variable cost are of equal importance in such technique of costing.

Hence also termed as full absorption costing. Various expenses in production of products and

offerings are grouped under different overheads such as production, distribution, selling and

distribution overhead. Such techniques of costing is basically used for the purpose of reporting.

The overall cost of production are affected by involvement of fixed manufacturing overheads. It

2

total cost of production by producing one additional unit of output. Fixed cost are of less

importance than variable cost of production. It overall contributes to changes occurring because

of variable cost of production. It is one of the accounting system in which marginal cost are

charged to products and offerings while fixed cost is called as periodic cost. Fixed cost are

written off against contribution. Marginal costing are of utmost importance for taking

appropriate decision regarding pricing decisions of SleepEase Ltd. A firm is more concerned

about additional cost required in extra unit of output (Salehi, Rostami and Mogadam, 2010).

Contribution concept in marginal costing is also important in decision making aspect of business.

The main advantages and disadvantages of marginal costing techniques are as follows-

Advantages

Marginal costing technique of inventory valuation is one of the easier and simpler

method.

The fixed cost are not considered hence it helps in avoiding complicated statement.

The issue with under absorption and over absorption will not arise.

Contribution details will provide benefits in decision making aspects of SleepEase.

Disadvantages

The total cost cannot be segregated easily into different variable and fixed costs.

It is not easy to determine the variability degree of semi variable cost incurred in

production of products and offerings.

Tax authorities are not accepting such statements which excludes fixed manufacturing

overheads.

The administration cannot take quality decision based on contribution aspect of

production.

Absorption costing- Absorption costing is one of the cost technique where both fixed

and variable cost are considered. Here cost are grouped into centres to find out total cost of

production. Both fixed and variable cost are of equal importance in such technique of costing.

Hence also termed as full absorption costing. Various expenses in production of products and

offerings are grouped under different overheads such as production, distribution, selling and

distribution overhead. Such techniques of costing is basically used for the purpose of reporting.

The overall cost of production are affected by involvement of fixed manufacturing overheads. It

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is one of the best way used in small businesses. Thus, organisation uses such methods to find

effect on profitability (McVay, et. al., 2012). Also it is to be noticed that fixed cost are being

incurred for production of goods and offerings hence their their inclusion in valuation of closing

stock is justifiable. It is also right to match up cost with the revenues (Maher, Stickney and Weil,

2012). It overall contribute to fix the price above cost of production. The main advantages and

disadvantages are as follows-

Advantages

It helps in product cost determination and hence frame a suitable policy of pricing.

All cost should be charged in determining total cost of production

This helps in correct analyses of profit, thus an important technique of costing.

It eliminates separation of fixed and variable cost and calculations became more easy.

Disadvantages

It create difficulty in cost controlling element. Also comparison done by an organisation

based on different levels of output are not easy.

It is not helpful for administration in managerial decisions.

fixed cost inclusion in computation of total cost of production is not justifiable.

preparation of flexible budgets are also not easy to be done.

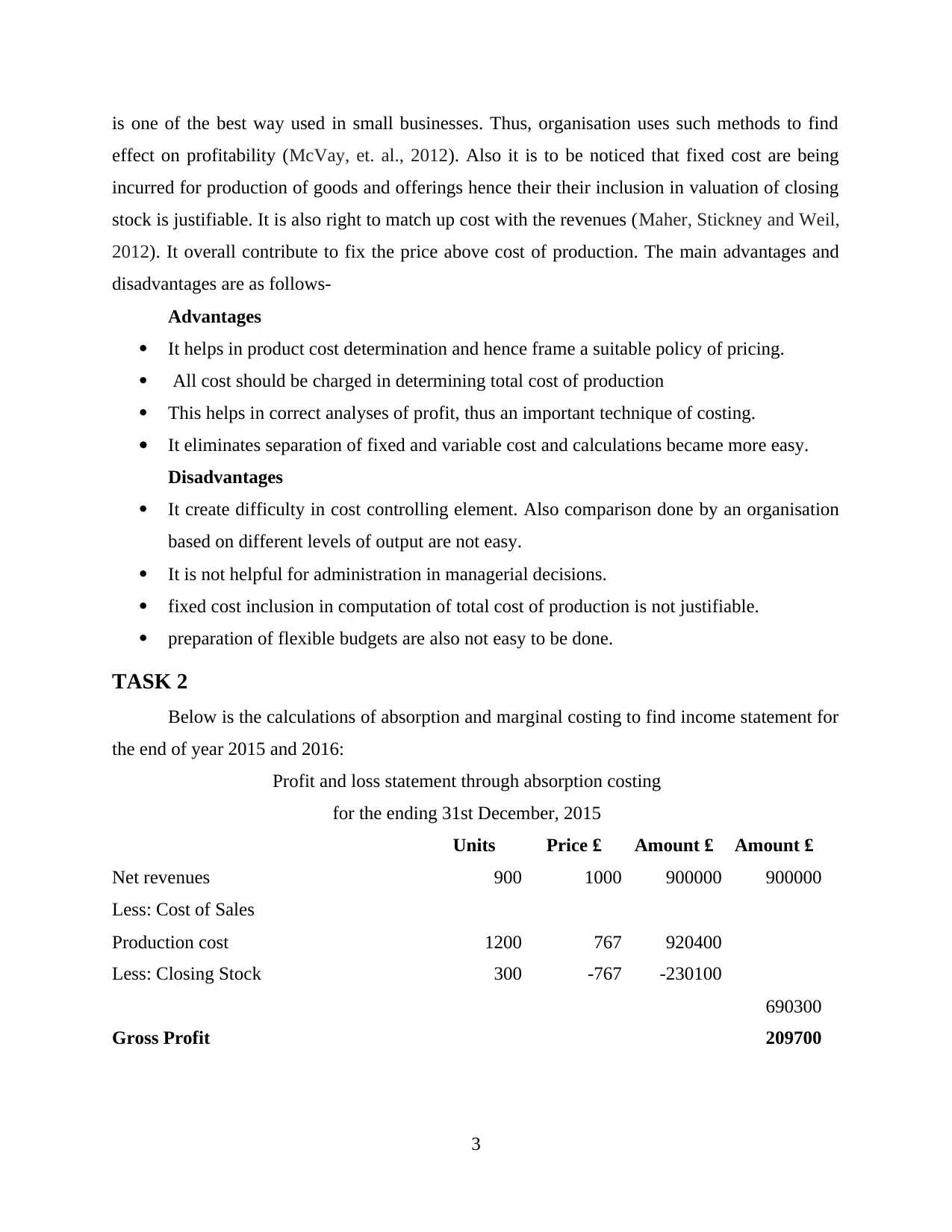

TASK 2

Below is the calculations of absorption and marginal costing to find income statement for

the end of year 2015 and 2016:

Profit and loss statement through absorption costing

for the ending 31st December, 2015

Units Price ₤ Amount ₤ Amount ₤

Net revenues 900 1000 900000 900000

Less: Cost of Sales

Production cost 1200 767 920400

Less: Closing Stock 300 -767 -230100

690300

Gross Profit 209700

3

effect on profitability (McVay, et. al., 2012). Also it is to be noticed that fixed cost are being

incurred for production of goods and offerings hence their their inclusion in valuation of closing

stock is justifiable. It is also right to match up cost with the revenues (Maher, Stickney and Weil,

2012). It overall contribute to fix the price above cost of production. The main advantages and

disadvantages are as follows-

Advantages

It helps in product cost determination and hence frame a suitable policy of pricing.

All cost should be charged in determining total cost of production

This helps in correct analyses of profit, thus an important technique of costing.

It eliminates separation of fixed and variable cost and calculations became more easy.

Disadvantages

It create difficulty in cost controlling element. Also comparison done by an organisation

based on different levels of output are not easy.

It is not helpful for administration in managerial decisions.

fixed cost inclusion in computation of total cost of production is not justifiable.

preparation of flexible budgets are also not easy to be done.

TASK 2

Below is the calculations of absorption and marginal costing to find income statement for

the end of year 2015 and 2016:

Profit and loss statement through absorption costing

for the ending 31st December, 2015

Units Price ₤ Amount ₤ Amount ₤

Net revenues 900 1000 900000 900000

Less: Cost of Sales

Production cost 1200 767 920400

Less: Closing Stock 300 -767 -230100

690300

Gross Profit 209700

3

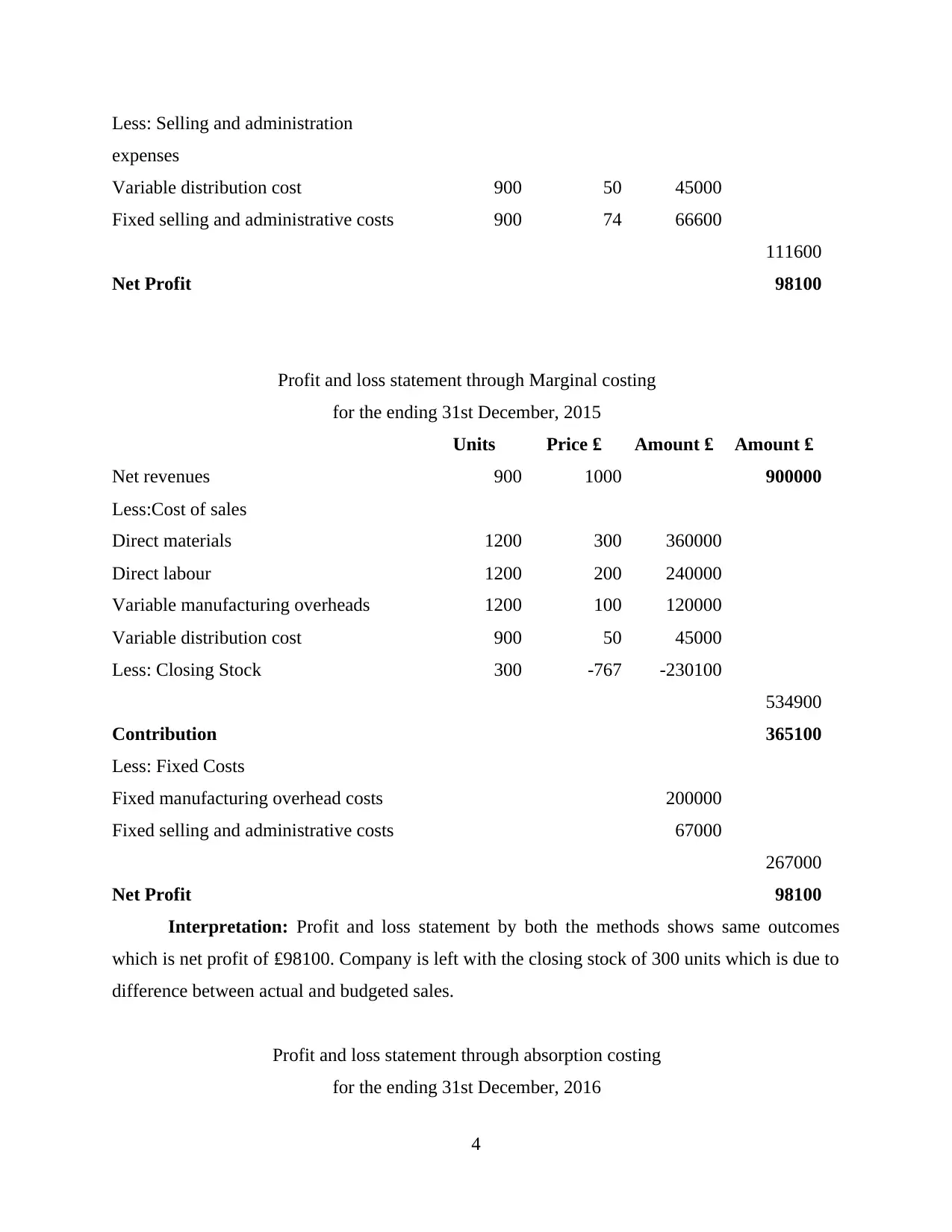

Less: Selling and administration

expenses

Variable distribution cost 900 50 45000

Fixed selling and administrative costs 900 74 66600

111600

Net Profit 98100

Profit and loss statement through Marginal costing

for the ending 31st December, 2015

Units Price ₤ Amount ₤ Amount ₤

Net revenues 900 1000 900000

Less:Cost of sales

Direct materials 1200 300 360000

Direct labour 1200 200 240000

Variable manufacturing overheads 1200 100 120000

Variable distribution cost 900 50 45000

Less: Closing Stock 300 -767 -230100

534900

Contribution 365100

Less: Fixed Costs

Fixed manufacturing overhead costs 200000

Fixed selling and administrative costs 67000

267000

Net Profit 98100

Interpretation: Profit and loss statement by both the methods shows same outcomes

which is net profit of ₤98100. Company is left with the closing stock of 300 units which is due to

difference between actual and budgeted sales.

Profit and loss statement through absorption costing

for the ending 31st December, 2016

4

expenses

Variable distribution cost 900 50 45000

Fixed selling and administrative costs 900 74 66600

111600

Net Profit 98100

Profit and loss statement through Marginal costing

for the ending 31st December, 2015

Units Price ₤ Amount ₤ Amount ₤

Net revenues 900 1000 900000

Less:Cost of sales

Direct materials 1200 300 360000

Direct labour 1200 200 240000

Variable manufacturing overheads 1200 100 120000

Variable distribution cost 900 50 45000

Less: Closing Stock 300 -767 -230100

534900

Contribution 365100

Less: Fixed Costs

Fixed manufacturing overhead costs 200000

Fixed selling and administrative costs 67000

267000

Net Profit 98100

Interpretation: Profit and loss statement by both the methods shows same outcomes

which is net profit of ₤98100. Company is left with the closing stock of 300 units which is due to

difference between actual and budgeted sales.

Profit and loss statement through absorption costing

for the ending 31st December, 2016

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

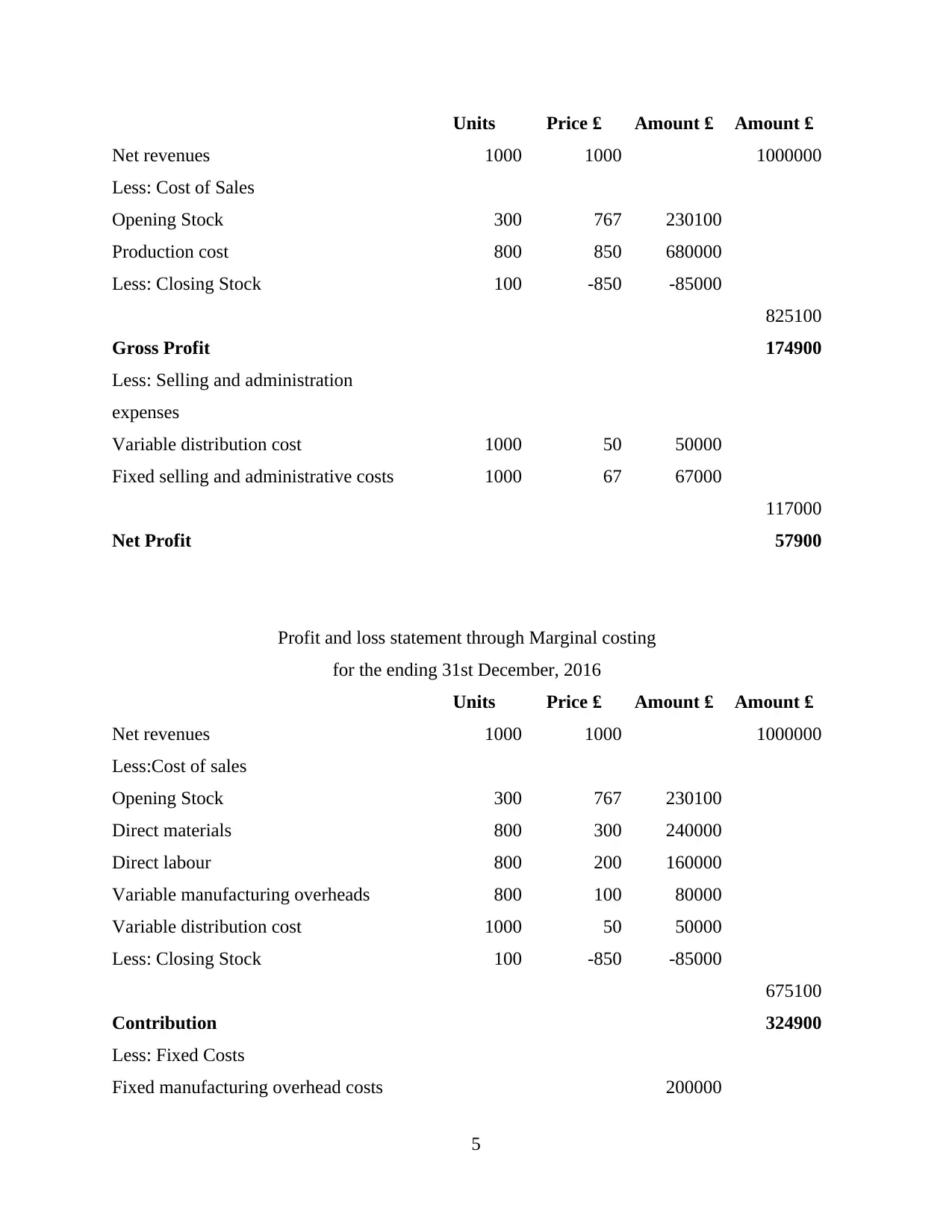

Units Price ₤ Amount ₤ Amount ₤

Net revenues 1000 1000 1000000

Less: Cost of Sales

Opening Stock 300 767 230100

Production cost 800 850 680000

Less: Closing Stock 100 -850 -85000

825100

Gross Profit 174900

Less: Selling and administration

expenses

Variable distribution cost 1000 50 50000

Fixed selling and administrative costs 1000 67 67000

117000

Net Profit 57900

Profit and loss statement through Marginal costing

for the ending 31st December, 2016

Units Price ₤ Amount ₤ Amount ₤

Net revenues 1000 1000 1000000

Less:Cost of sales

Opening Stock 300 767 230100

Direct materials 800 300 240000

Direct labour 800 200 160000

Variable manufacturing overheads 800 100 80000

Variable distribution cost 1000 50 50000

Less: Closing Stock 100 -850 -85000

675100

Contribution 324900

Less: Fixed Costs

Fixed manufacturing overhead costs 200000

5

Net revenues 1000 1000 1000000

Less: Cost of Sales

Opening Stock 300 767 230100

Production cost 800 850 680000

Less: Closing Stock 100 -850 -85000

825100

Gross Profit 174900

Less: Selling and administration

expenses

Variable distribution cost 1000 50 50000

Fixed selling and administrative costs 1000 67 67000

117000

Net Profit 57900

Profit and loss statement through Marginal costing

for the ending 31st December, 2016

Units Price ₤ Amount ₤ Amount ₤

Net revenues 1000 1000 1000000

Less:Cost of sales

Opening Stock 300 767 230100

Direct materials 800 300 240000

Direct labour 800 200 160000

Variable manufacturing overheads 800 100 80000

Variable distribution cost 1000 50 50000

Less: Closing Stock 100 -850 -85000

675100

Contribution 324900

Less: Fixed Costs

Fixed manufacturing overhead costs 200000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

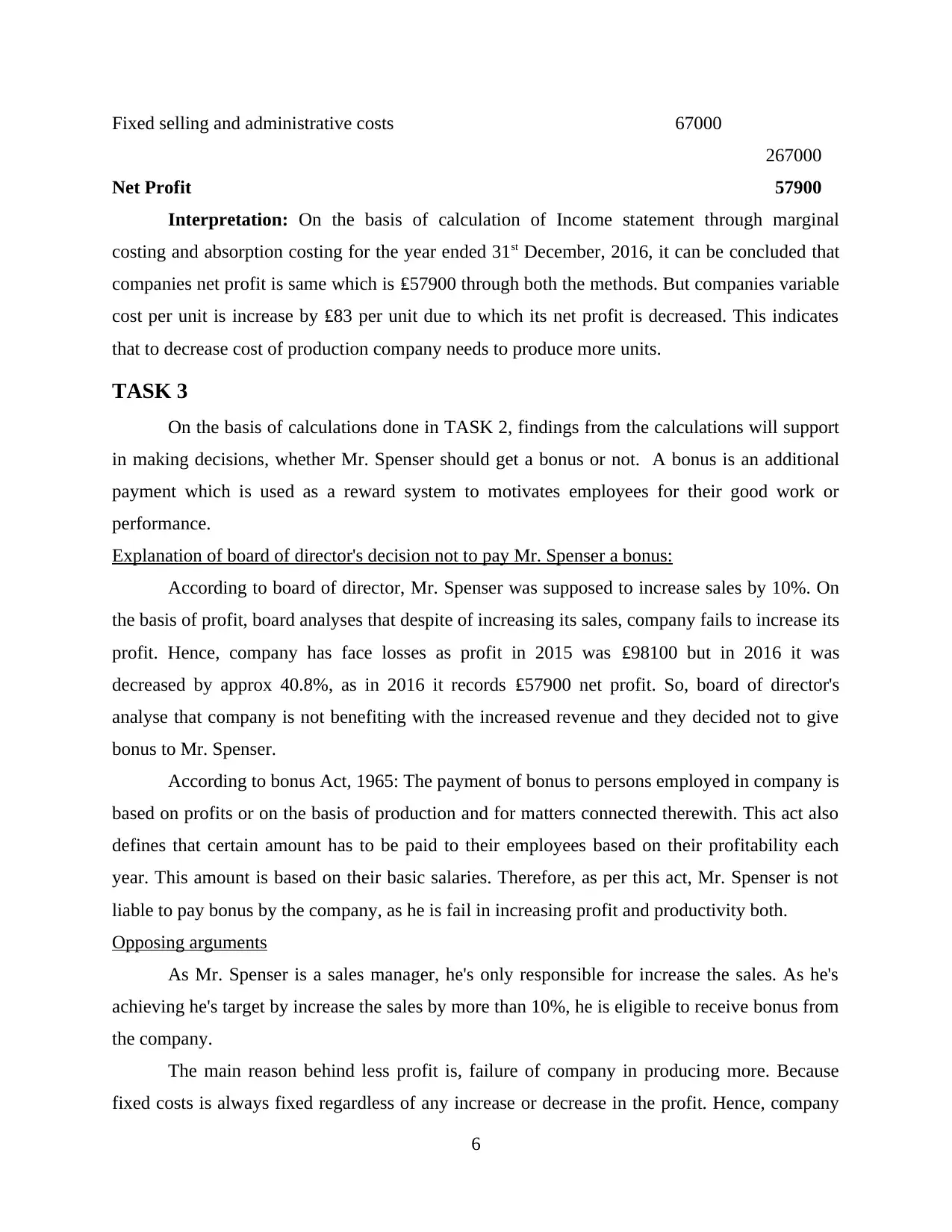

Fixed selling and administrative costs 67000

267000

Net Profit 57900

Interpretation: On the basis of calculation of Income statement through marginal

costing and absorption costing for the year ended 31st December, 2016, it can be concluded that

companies net profit is same which is ₤57900 through both the methods. But companies variable

cost per unit is increase by ₤83 per unit due to which its net profit is decreased. This indicates

that to decrease cost of production company needs to produce more units.

TASK 3

On the basis of calculations done in TASK 2, findings from the calculations will support

in making decisions, whether Mr. Spenser should get a bonus or not. A bonus is an additional

payment which is used as a reward system to motivates employees for their good work or

performance.

Explanation of board of director's decision not to pay Mr. Spenser a bonus:

According to board of director, Mr. Spenser was supposed to increase sales by 10%. On

the basis of profit, board analyses that despite of increasing its sales, company fails to increase its

profit. Hence, company has face losses as profit in 2015 was ₤98100 but in 2016 it was

decreased by approx 40.8%, as in 2016 it records ₤57900 net profit. So, board of director's

analyse that company is not benefiting with the increased revenue and they decided not to give

bonus to Mr. Spenser.

According to bonus Act, 1965: The payment of bonus to persons employed in company is

based on profits or on the basis of production and for matters connected therewith. This act also

defines that certain amount has to be paid to their employees based on their profitability each

year. This amount is based on their basic salaries. Therefore, as per this act, Mr. Spenser is not

liable to pay bonus by the company, as he is fail in increasing profit and productivity both.

Opposing arguments

As Mr. Spenser is a sales manager, he's only responsible for increase the sales. As he's

achieving he's target by increase the sales by more than 10%, he is eligible to receive bonus from

the company.

The main reason behind less profit is, failure of company in producing more. Because

fixed costs is always fixed regardless of any increase or decrease in the profit. Hence, company

6

267000

Net Profit 57900

Interpretation: On the basis of calculation of Income statement through marginal

costing and absorption costing for the year ended 31st December, 2016, it can be concluded that

companies net profit is same which is ₤57900 through both the methods. But companies variable

cost per unit is increase by ₤83 per unit due to which its net profit is decreased. This indicates

that to decrease cost of production company needs to produce more units.

TASK 3

On the basis of calculations done in TASK 2, findings from the calculations will support

in making decisions, whether Mr. Spenser should get a bonus or not. A bonus is an additional

payment which is used as a reward system to motivates employees for their good work or

performance.

Explanation of board of director's decision not to pay Mr. Spenser a bonus:

According to board of director, Mr. Spenser was supposed to increase sales by 10%. On

the basis of profit, board analyses that despite of increasing its sales, company fails to increase its

profit. Hence, company has face losses as profit in 2015 was ₤98100 but in 2016 it was

decreased by approx 40.8%, as in 2016 it records ₤57900 net profit. So, board of director's

analyse that company is not benefiting with the increased revenue and they decided not to give

bonus to Mr. Spenser.

According to bonus Act, 1965: The payment of bonus to persons employed in company is

based on profits or on the basis of production and for matters connected therewith. This act also

defines that certain amount has to be paid to their employees based on their profitability each

year. This amount is based on their basic salaries. Therefore, as per this act, Mr. Spenser is not

liable to pay bonus by the company, as he is fail in increasing profit and productivity both.

Opposing arguments

As Mr. Spenser is a sales manager, he's only responsible for increase the sales. As he's

achieving he's target by increase the sales by more than 10%, he is eligible to receive bonus from

the company.

The main reason behind less profit is, failure of company in producing more. Because

fixed costs is always fixed regardless of any increase or decrease in the profit. Hence, company

6

is only producing 800 units and remaining costs are same. It indicates that company is producing

800 units at same cost at which it was producing 1200 products.

After taking consideration of law, it is clear that Mr. Spenser is not eligible for bonus as

he was not able to increase production and profits of the company. But at the same time it can't

be neglected that he able to sell previous units, for which he's eligible to receive bonus. He

achieves sales of 1000 units in 2016 from 900 units in 2015. In the deal it is clearly mentioned

that, if he's able to increase sales by 10% than he's eligible for ₤10000 commission or bonus and

he achieved that target.

Hence, Mr. Spenser should receive bonus because he has fulfilled the terms offering by

company. He's not responsible for increase in the cost of production, as he's only a sales manager

not a finance and production manager and cost controlling factor is out of his sales domain.

TASK 4

Strategic importance of using Balanced scorecard in performance management

Every organisation wants to improve their performance. To effectively implement

corporate strategies, balanced scorecard is of utmost importance (Strategic importance of using

Balanced scorecard in performance management. 2017). SleepEase Ltd. should have to tighten

their belts for demanding high performance. The use of balanced scorecard gives many

advantages to firm. Many firm struggle with suitable performance management system. The

system that an organisation uses consist of annual employee evaluation which not reveal true

assessment of performance. Annual employee evaluation will not work as performance

management is an on-going process of conversation between manager and employees. Manager

should done timely evaluation of performance and set clear objectives and deliver feedback to

workers about their performance reviews. The Balanced scorecard is the set of financial and non-

financial measure that are meant to be assessed. It helps in making improvement in performance

and create value for an organisation. Large number of enterprises are using balanced scorecard to

analyse performance of different aspects of businesses. Major enterprises in US, Europe and

Asia are using tool of balanced scorecard.

Balanced scorecard is one of the tool of strategic planning developed by Kaplan and

Norton in 1996. organisation really exist to satisfy its stakeholders. It is based on four different

dimensional framework (Hall, 2010). Each of the dimension represent different stakeholders.

The four perspectives are Learning and Growth, Internal business processes, Customers and

7

800 units at same cost at which it was producing 1200 products.

After taking consideration of law, it is clear that Mr. Spenser is not eligible for bonus as

he was not able to increase production and profits of the company. But at the same time it can't

be neglected that he able to sell previous units, for which he's eligible to receive bonus. He

achieves sales of 1000 units in 2016 from 900 units in 2015. In the deal it is clearly mentioned

that, if he's able to increase sales by 10% than he's eligible for ₤10000 commission or bonus and

he achieved that target.

Hence, Mr. Spenser should receive bonus because he has fulfilled the terms offering by

company. He's not responsible for increase in the cost of production, as he's only a sales manager

not a finance and production manager and cost controlling factor is out of his sales domain.

TASK 4

Strategic importance of using Balanced scorecard in performance management

Every organisation wants to improve their performance. To effectively implement

corporate strategies, balanced scorecard is of utmost importance (Strategic importance of using

Balanced scorecard in performance management. 2017). SleepEase Ltd. should have to tighten

their belts for demanding high performance. The use of balanced scorecard gives many

advantages to firm. Many firm struggle with suitable performance management system. The

system that an organisation uses consist of annual employee evaluation which not reveal true

assessment of performance. Annual employee evaluation will not work as performance

management is an on-going process of conversation between manager and employees. Manager

should done timely evaluation of performance and set clear objectives and deliver feedback to

workers about their performance reviews. The Balanced scorecard is the set of financial and non-

financial measure that are meant to be assessed. It helps in making improvement in performance

and create value for an organisation. Large number of enterprises are using balanced scorecard to

analyse performance of different aspects of businesses. Major enterprises in US, Europe and

Asia are using tool of balanced scorecard.

Balanced scorecard is one of the tool of strategic planning developed by Kaplan and

Norton in 1996. organisation really exist to satisfy its stakeholders. It is based on four different

dimensional framework (Hall, 2010). Each of the dimension represent different stakeholders.

The four perspectives are Learning and Growth, Internal business processes, Customers and

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Finance. The finance perspectives are generally at the top and contains clear set of objectives.

Customer perspectives always focuses on meeting customer needs. This will result in making

them loyal towards brand. SleepEase can able to drive sales based on the same perspective.

Operational perspectives is primarily based on smooth functioning of business organisation.

Finally people perspectives consist of set of goals that support operational perspective of

business. It is an important strategic planning and management tool that are used by firm to

improve communication processes of tasks that are to be attained, assigning of work to be done,

measuring and monitoring progress.

The balanced scorecard helps organisation like SleepEase Ltd. in many ways-

Overcoming challenges- SleepEase organisation can able to overcome challenges arise

during different course of time. It helps in effectively implementing strategies. It facilitates

advantage of performance measurement and rise of intangible asset of firm (Garrison, et. al.,

2010). It also encourage long term thinking of business concern. It is also one of the beneficial

tool for reducing barriers in operational activities of SleepEase Ltd.

Four perspectives- It consist of four different perspectives i.e. Financial, customers,

Internal business processes and learning and growth. This allows firm to have four viewpoints to

create a value for the firm. Therefore company able to gain higher customer satisfaction and

market share.

Competitive advantage- SleepEase Ltd. Can able to improve performance of business

by using balanced scorecard (Demski, 2013). This contributes to gain an edge over rivals. Hence,

they should implement such strategic tool in performance management system.

CONCLUSION

By this report, it has been concluded that managerial accounting is vital for taking

decisions in business. The accounting generally uses two approaches of valuation of inventory

i.e. marginal costing and absorption costing. These approaches helps with production and pricing

aspects of business concern. SleepEase is one of the British enterprise engaged in business of

mattresses. They produces specialised bed named Max-ease. It is the product designed to ease

back pains for orthopaedic patients. They also constantly need to review their performance.

performance is one of the important aspect of business organisation. Hence use of balanced

scorecard in implementing strategies in business will give an advantage to the firm.

8

Customer perspectives always focuses on meeting customer needs. This will result in making

them loyal towards brand. SleepEase can able to drive sales based on the same perspective.

Operational perspectives is primarily based on smooth functioning of business organisation.

Finally people perspectives consist of set of goals that support operational perspective of

business. It is an important strategic planning and management tool that are used by firm to

improve communication processes of tasks that are to be attained, assigning of work to be done,

measuring and monitoring progress.

The balanced scorecard helps organisation like SleepEase Ltd. in many ways-

Overcoming challenges- SleepEase organisation can able to overcome challenges arise

during different course of time. It helps in effectively implementing strategies. It facilitates

advantage of performance measurement and rise of intangible asset of firm (Garrison, et. al.,

2010). It also encourage long term thinking of business concern. It is also one of the beneficial

tool for reducing barriers in operational activities of SleepEase Ltd.

Four perspectives- It consist of four different perspectives i.e. Financial, customers,

Internal business processes and learning and growth. This allows firm to have four viewpoints to

create a value for the firm. Therefore company able to gain higher customer satisfaction and

market share.

Competitive advantage- SleepEase Ltd. Can able to improve performance of business

by using balanced scorecard (Demski, 2013). This contributes to gain an edge over rivals. Hence,

they should implement such strategic tool in performance management system.

CONCLUSION

By this report, it has been concluded that managerial accounting is vital for taking

decisions in business. The accounting generally uses two approaches of valuation of inventory

i.e. marginal costing and absorption costing. These approaches helps with production and pricing

aspects of business concern. SleepEase is one of the British enterprise engaged in business of

mattresses. They produces specialised bed named Max-ease. It is the product designed to ease

back pains for orthopaedic patients. They also constantly need to review their performance.

performance is one of the important aspect of business organisation. Hence use of balanced

scorecard in implementing strategies in business will give an advantage to the firm.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Demski, J., 2013. Managerial uses of accounting information. Springer Science & Business

Media.

Garrison, R.H., et. al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Hall, M., 2010. Accounting information and managerial work. Accounting, Organizations and

Society. 35(3). pp.301-315.

Maher, M.W., Stickney, C.P. and Weil, R.L., 2012. Managerial accounting: An introduction to

concepts, methods and uses. Cengage Learning.

McVay, S.E., et. al., 2012. Managerial ability and earnings quality. The Accounting

Review. 88(2). pp.463-498.

Salehi, M., Rostami, V. and Mogadam, A., 2010. Usefulness of accounting information system

in emerging economy: Empirical evidence of Iran. International Journal of Economics

and Finance. 2(2). p.186.

Online

9

Books and Journals

Demski, J., 2013. Managerial uses of accounting information. Springer Science & Business

Media.

Garrison, R.H., et. al., 2010. Managerial accounting. Issues in Accounting Education. 25(4).

pp.792-793.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Hall, M., 2010. Accounting information and managerial work. Accounting, Organizations and

Society. 35(3). pp.301-315.

Maher, M.W., Stickney, C.P. and Weil, R.L., 2012. Managerial accounting: An introduction to

concepts, methods and uses. Cengage Learning.

McVay, S.E., et. al., 2012. Managerial ability and earnings quality. The Accounting

Review. 88(2). pp.463-498.

Salehi, M., Rostami, V. and Mogadam, A., 2010. Usefulness of accounting information system

in emerging economy: Empirical evidence of Iran. International Journal of Economics

and Finance. 2(2). p.186.

Online

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.