Financial Management, Crisis, and SME Analysis in Slovakia

VerifiedAdded on 2022/02/24

|34

|7595

|25

Report

AI Summary

This report delves into the critical aspects of financial management within small and medium-sized enterprises (SMEs), particularly in the context of the Slovakian economy and the impact of financial crises. It begins by emphasizing the importance of financial management and planning for business sustainability and growth, including effective fund allocation and financial decision-making. The report then provides an overview of SMEs in Slovakia, highlighting their significance in the national economy and their vulnerability to economic downturns. A key focus is the role of financial management in helping SMEs navigate challenges such as limited resources and external financial constraints. The report offers practical tips for SMEs to manage finances during a crisis, including cash flow management, financial ratio analysis, and strategic planning. It also includes a case study of a company's financial performance and the application of financial ratios, providing a comprehensive analysis of how SMEs can improve their financial health and resilience in a challenging economic environment. Finally, the report includes an abstract, keywords, and a bibliography.

Contents

1. THE IMPORTANCE OF FINANCIAL MANAGEMENT...................................................................................1

2. SMALL AND MEDIUM SIZED ENTERPRISES AND THEIR IMPORTANCE IN SLOVAK ECONOMICS..............2

3.ROLE OF FINANCIAL MANAGEMENT IN SMALL AND MEDIUM SIZED ENTERPRISES.................................4

4. Tips for small and medium-sized financial management of the financial crisis in Slovakia during

Enterprise use..............................................................................................................................................5

5.CONCLUSION........................................................................................................................................6

6.REFERENCES.........................................................................................................................................7

2. The cash flow statement shows the company's..................................................................................7

PARTS OF THE CASH FLOW STATEMENT..................................................................................................8

CLASSIFICATIONS OF CASH RECEIPTS AND PAYMENTS............................................................................9

Cash from Investing.............................................................................................................................9

Cash from Operations..........................................................................................................................9

Methods of Preparing the Cash Flow Statement.................................................................................9

Direct Method...................................................................................................................................10

Indirect Method.................................................................................................................................10

FINANCING AND INVESTING SECTIONS.................................................................................................10

Cash Flows from Investing.................................................................................................................10

Cash Flows from Financing................................................................................................................11

BIBLIOGRAPHY.......................................................................................................................................11

Compute at least 13 key ratios to enable you to assess the financial performance of Healthy Snack

Corporation. Round all ratios to the nearest 1 decimal based on 360 working days.................................12

1. THE IMPORTANCE OF FINANCIAL MANAGEMENT

The financial industry is the lifeblood of an organization. It is a business concern that needs to be

met. Concerns of each business and economic concern for their smooth running financially and

maintaining an adequate amount to achieve the goals of economic concern must be careful to

maintain business. The financial goals of the economy with the help of effective management

can be achieved. Our situation at any time, financially important from which can not be ignored

1. THE IMPORTANCE OF FINANCIAL MANAGEMENT...................................................................................1

2. SMALL AND MEDIUM SIZED ENTERPRISES AND THEIR IMPORTANCE IN SLOVAK ECONOMICS..............2

3.ROLE OF FINANCIAL MANAGEMENT IN SMALL AND MEDIUM SIZED ENTERPRISES.................................4

4. Tips for small and medium-sized financial management of the financial crisis in Slovakia during

Enterprise use..............................................................................................................................................5

5.CONCLUSION........................................................................................................................................6

6.REFERENCES.........................................................................................................................................7

2. The cash flow statement shows the company's..................................................................................7

PARTS OF THE CASH FLOW STATEMENT..................................................................................................8

CLASSIFICATIONS OF CASH RECEIPTS AND PAYMENTS............................................................................9

Cash from Investing.............................................................................................................................9

Cash from Operations..........................................................................................................................9

Methods of Preparing the Cash Flow Statement.................................................................................9

Direct Method...................................................................................................................................10

Indirect Method.................................................................................................................................10

FINANCING AND INVESTING SECTIONS.................................................................................................10

Cash Flows from Investing.................................................................................................................10

Cash Flows from Financing................................................................................................................11

BIBLIOGRAPHY.......................................................................................................................................11

Compute at least 13 key ratios to enable you to assess the financial performance of Healthy Snack

Corporation. Round all ratios to the nearest 1 decimal based on 360 working days.................................12

1. THE IMPORTANCE OF FINANCIAL MANAGEMENT

The financial industry is the lifeblood of an organization. It is a business concern that needs to be

met. Concerns of each business and economic concern for their smooth running financially and

maintaining an adequate amount to achieve the goals of economic concern must be careful to

maintain business. The financial goals of the economy with the help of effective management

can be achieved. Our situation at any time, financially important from which can not be ignored

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

First of all, the importance of financial management and financial planning. Financial

management services will help determine the financial needs of the concerns and concerns of

financial planning. Financial planning, business promotion helps to be part of business concerns.

Second, we can learn the proper use of funds. The proper use of funds and the allocation of

economic anxiety helps to improve operational efficiency. When using financial management

programs that are required to provide funds, reduce the city's expenses and the ability to increase

the value of the company, they can prevent a large amount of debt from others.

After that, the importance of financial management, you can learn how to make financial

decisions. Sound financial management for business concerns helps to use financial decisions.

Fear of financial decisions that will affect the entire business cycle. Such as marketing,

production, personnel with various department activities because of direct relationships

Finally, improving profits, the importance of financial management The edge of the greatest

concern of the purely economic worries of the fund depends on the efficient and appropriate use.

Financial management, such as budget control, profit ratio analysis and cost audit, strong

financial control from concerns with the help of devices that help improve profitability positions.

Now, in financial management it is popularly known as the financial position of a business or

corporate finance. Economic concerns or important business sectors of financial management

that cannot work without

Abstract: This article plays an important role for small and medium-sized entrepreneurs with the

size of the company's financial management regarding the effects of the global financial and

economic crisis. Will focus on small and medium-sized enterprises (SMEs) Slovakia after the

global financial and economic crisis. In this article, I focus on defining small and medium

enterprises Various methods have been introduced to improve small and medium-sized

enterprises. Keywords: small and medium enterprises (SMEs), global financial and economic

crisis, financial management.

1. INTRODUCTION

Many of the worst economists in the 1930s since the Great Depression, 2007 to consider the

current financial and economic crisis. This economic crisis began as a sub-prime US crisis. But

management services will help determine the financial needs of the concerns and concerns of

financial planning. Financial planning, business promotion helps to be part of business concerns.

Second, we can learn the proper use of funds. The proper use of funds and the allocation of

economic anxiety helps to improve operational efficiency. When using financial management

programs that are required to provide funds, reduce the city's expenses and the ability to increase

the value of the company, they can prevent a large amount of debt from others.

After that, the importance of financial management, you can learn how to make financial

decisions. Sound financial management for business concerns helps to use financial decisions.

Fear of financial decisions that will affect the entire business cycle. Such as marketing,

production, personnel with various department activities because of direct relationships

Finally, improving profits, the importance of financial management The edge of the greatest

concern of the purely economic worries of the fund depends on the efficient and appropriate use.

Financial management, such as budget control, profit ratio analysis and cost audit, strong

financial control from concerns with the help of devices that help improve profitability positions.

Now, in financial management it is popularly known as the financial position of a business or

corporate finance. Economic concerns or important business sectors of financial management

that cannot work without

Abstract: This article plays an important role for small and medium-sized entrepreneurs with the

size of the company's financial management regarding the effects of the global financial and

economic crisis. Will focus on small and medium-sized enterprises (SMEs) Slovakia after the

global financial and economic crisis. In this article, I focus on defining small and medium

enterprises Various methods have been introduced to improve small and medium-sized

enterprises. Keywords: small and medium enterprises (SMEs), global financial and economic

crisis, financial management.

1. INTRODUCTION

Many of the worst economists in the 1930s since the Great Depression, 2007 to consider the

current financial and economic crisis. This economic crisis began as a sub-prime US crisis. But

quickly, after the global financial crisis, non-financial companies in the economic environment

have a negative impact, becoming a global economic crisis. Many organizations in a changing

environment to consider their position and to survive the crisis will be forced to accept unpopular

measures. The dilemma for products and services, lower prices, pressure on lower sales demand

to reduce unemployment and an increase in external funding is a proposal that limits small and

medium-sized companies to manage to survive that time. Importantly, this took the process to

use small and medium-sized companies than large companies that were more flexible and able to

respond faster. But their needs, products / services, logistics networks and changes in the

financial sector and are more important to suffer from the economic crisis faster than large

businesses In order to survive the environment crisis of small and medium-sized business

management, in order to overcome the negative changes, flexibility and innovation, new

conditions must be ready to adjust..

2. SMALL AND MEDIUM SIZED ENTERPRISES AND THEIR

IMPORTANCE IN SLOVAK ECONOMICS

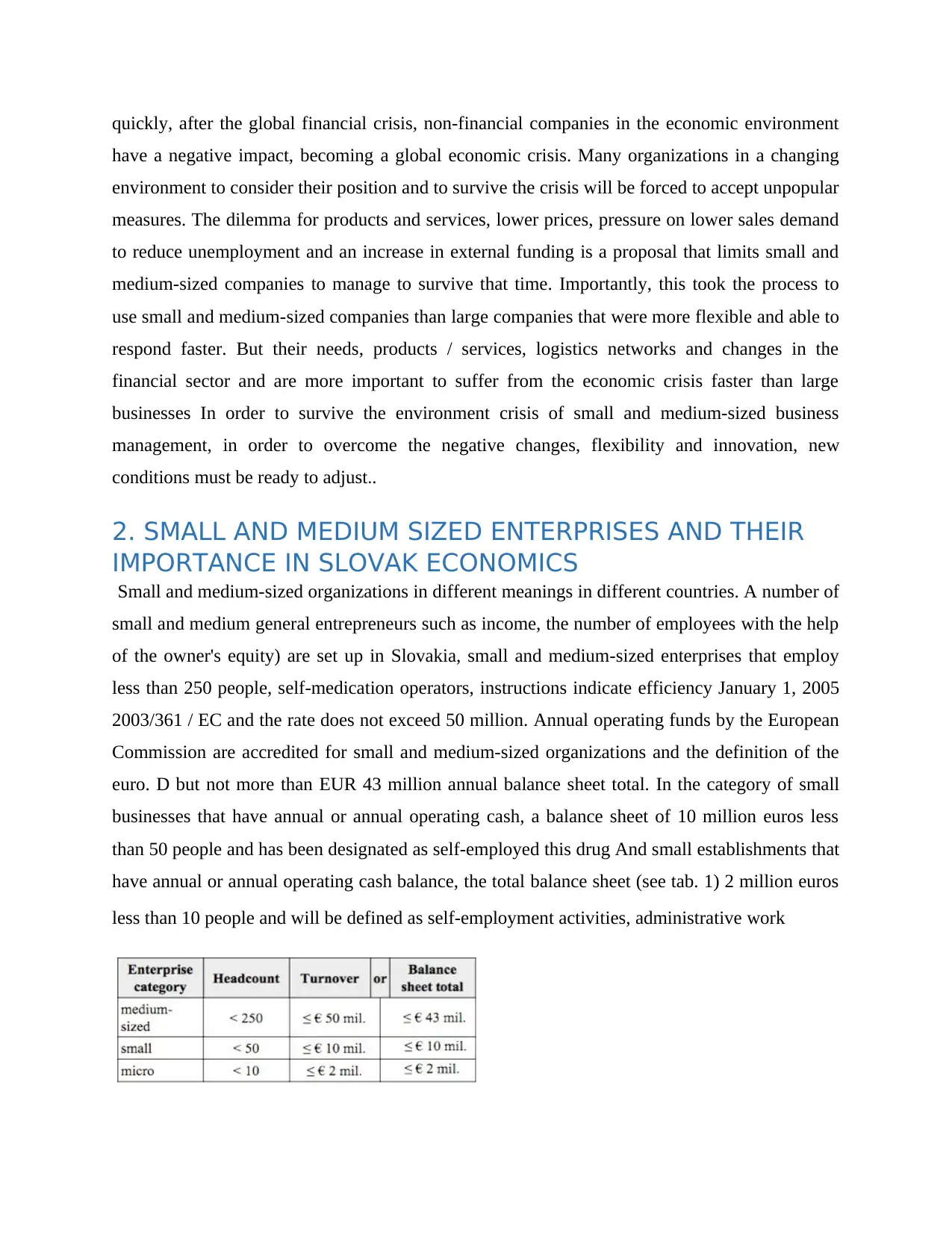

Small and medium-sized organizations in different meanings in different countries. A number of

small and medium general entrepreneurs such as income, the number of employees with the help

of the owner's equity) are set up in Slovakia, small and medium-sized enterprises that employ

less than 250 people, self-medication operators, instructions indicate efficiency January 1, 2005

2003/361 / EC and the rate does not exceed 50 million. Annual operating funds by the European

Commission are accredited for small and medium-sized organizations and the definition of the

euro. D but not more than EUR 43 million annual balance sheet total. In the category of small

businesses that have annual or annual operating cash, a balance sheet of 10 million euros less

than 50 people and has been designated as self-employed this drug And small establishments that

have annual or annual operating cash balance, the total balance sheet (see tab. 1) 2 million euros

less than 10 people and will be defined as self-employment activities, administrative work

have a negative impact, becoming a global economic crisis. Many organizations in a changing

environment to consider their position and to survive the crisis will be forced to accept unpopular

measures. The dilemma for products and services, lower prices, pressure on lower sales demand

to reduce unemployment and an increase in external funding is a proposal that limits small and

medium-sized companies to manage to survive that time. Importantly, this took the process to

use small and medium-sized companies than large companies that were more flexible and able to

respond faster. But their needs, products / services, logistics networks and changes in the

financial sector and are more important to suffer from the economic crisis faster than large

businesses In order to survive the environment crisis of small and medium-sized business

management, in order to overcome the negative changes, flexibility and innovation, new

conditions must be ready to adjust..

2. SMALL AND MEDIUM SIZED ENTERPRISES AND THEIR

IMPORTANCE IN SLOVAK ECONOMICS

Small and medium-sized organizations in different meanings in different countries. A number of

small and medium general entrepreneurs such as income, the number of employees with the help

of the owner's equity) are set up in Slovakia, small and medium-sized enterprises that employ

less than 250 people, self-medication operators, instructions indicate efficiency January 1, 2005

2003/361 / EC and the rate does not exceed 50 million. Annual operating funds by the European

Commission are accredited for small and medium-sized organizations and the definition of the

euro. D but not more than EUR 43 million annual balance sheet total. In the category of small

businesses that have annual or annual operating cash, a balance sheet of 10 million euros less

than 50 people and has been designated as self-employed this drug And small establishments that

have annual or annual operating cash balance, the total balance sheet (see tab. 1) 2 million euros

less than 10 people and will be defined as self-employment activities, administrative work

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Tab. 1. SME definition per European Comission

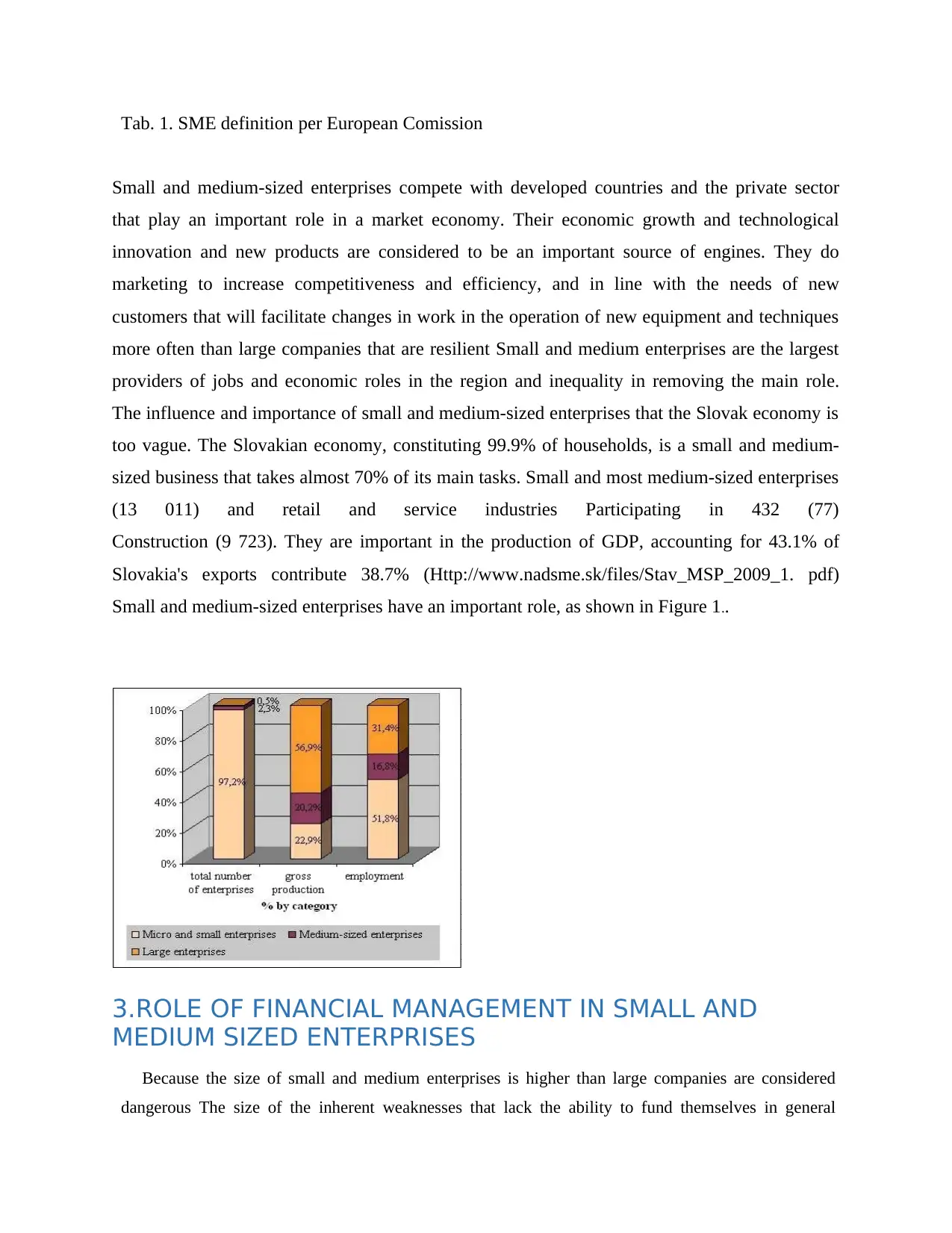

Small and medium-sized enterprises compete with developed countries and the private sector

that play an important role in a market economy. Their economic growth and technological

innovation and new products are considered to be an important source of engines. They do

marketing to increase competitiveness and efficiency, and in line with the needs of new

customers that will facilitate changes in work in the operation of new equipment and techniques

more often than large companies that are resilient Small and medium enterprises are the largest

providers of jobs and economic roles in the region and inequality in removing the main role.

The influence and importance of small and medium-sized enterprises that the Slovak economy is

too vague. The Slovakian economy, constituting 99.9% of households, is a small and medium-

sized business that takes almost 70% of its main tasks. Small and most medium-sized enterprises

(13 011) and retail and service industries Participating in 432 (77)

Construction (9 723). They are important in the production of GDP, accounting for 43.1% of

Slovakia's exports contribute 38.7% (Http://www.nadsme.sk/files/Stav_MSP_2009_1. pdf)

Small and medium-sized enterprises have an important role, as shown in Figure 1..

3.ROLE OF FINANCIAL MANAGEMENT IN SMALL AND

MEDIUM SIZED ENTERPRISES

Because the size of small and medium enterprises is higher than large companies are considered

dangerous The size of the inherent weaknesses that lack the ability to fund themselves in general

Small and medium-sized enterprises compete with developed countries and the private sector

that play an important role in a market economy. Their economic growth and technological

innovation and new products are considered to be an important source of engines. They do

marketing to increase competitiveness and efficiency, and in line with the needs of new

customers that will facilitate changes in work in the operation of new equipment and techniques

more often than large companies that are resilient Small and medium enterprises are the largest

providers of jobs and economic roles in the region and inequality in removing the main role.

The influence and importance of small and medium-sized enterprises that the Slovak economy is

too vague. The Slovakian economy, constituting 99.9% of households, is a small and medium-

sized business that takes almost 70% of its main tasks. Small and most medium-sized enterprises

(13 011) and retail and service industries Participating in 432 (77)

Construction (9 723). They are important in the production of GDP, accounting for 43.1% of

Slovakia's exports contribute 38.7% (Http://www.nadsme.sk/files/Stav_MSP_2009_1. pdf)

Small and medium-sized enterprises have an important role, as shown in Figure 1..

3.ROLE OF FINANCIAL MANAGEMENT IN SMALL AND

MEDIUM SIZED ENTERPRISES

Because the size of small and medium enterprises is higher than large companies are considered

dangerous The size of the inherent weaknesses that lack the ability to fund themselves in general

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

because the base is a small client Therefore, the lack of collateral or credit history or leaving businesses

and small and medium enterprises more often than large companies are often bankrupt. Small and

medium-sized businesses that will help survive in a highly competitive, ever-changing environment are

key tools for effective financial management. Overall, the company's management into the financial

process subsystem (Financial planning, the financial decision-making process of the financial team and

financial analysis and public awareness) in the management and control of shareholders, the value

attached to the focus on the goals of financial management Can be set up. Financial management in the

main work needed to efficiently allocate financial and get money for The plan, profit sharing, the

Company's financial management for companies of any size and type is important (Fetisovova et al.,

2004), while the owners of small and medium enterprises is crucial, especially. Based on our research,

we have more than half of small and medium-sized entrepreneurs on both sides of the crisis having a

negative impact on the discovery of most companies, as their movements have a major influence. In the

crisis at the beginning of 2009, more than 50% of companies felt the impact, felt their limited income

and external financial liabilities decreased significantly, especially at Especially in the financial notes.

Some people feel pressure from falling prices. The problem with debt repayment from investing in

the lower back. Some companies have become insolvent and the current shares of account

owners or credit cards are used for this solution to increase It licensed a small new company

and the bank to make loans has become very difficult. EXIM Bank and through the micro

credit program SZRB (Slovakia guarantee and development), the only restriction was able to

get money. Grants for small and medium-sized enterprises..

4. Tips for small and medium-sized financial management

of the financial crisis in Slovakia during Enterprise use

In the current economic literature on the financial crisis and the global economy, the

financial management of companies in best practices in discussions from our research

we have for small and medium-sized entrepreneurs received. Under financial

management tips

1. Small and medium-sized during the long-term crisis that will fill the aircraft and the

strategy and the shareholders of the company have the appropriate value attached to the

company, focusing on the main goal is important for the Ministry of Finance to

implement the strategy Created corporate strategy, economy, marketing and related

activities for choosing a company, therefore determining the scope and direction of the

financial strategy project Many are working strategies. This is an organization's strategy

and small and medium enterprises more often than large companies are often bankrupt. Small and

medium-sized businesses that will help survive in a highly competitive, ever-changing environment are

key tools for effective financial management. Overall, the company's management into the financial

process subsystem (Financial planning, the financial decision-making process of the financial team and

financial analysis and public awareness) in the management and control of shareholders, the value

attached to the focus on the goals of financial management Can be set up. Financial management in the

main work needed to efficiently allocate financial and get money for The plan, profit sharing, the

Company's financial management for companies of any size and type is important (Fetisovova et al.,

2004), while the owners of small and medium enterprises is crucial, especially. Based on our research,

we have more than half of small and medium-sized entrepreneurs on both sides of the crisis having a

negative impact on the discovery of most companies, as their movements have a major influence. In the

crisis at the beginning of 2009, more than 50% of companies felt the impact, felt their limited income

and external financial liabilities decreased significantly, especially at Especially in the financial notes.

Some people feel pressure from falling prices. The problem with debt repayment from investing in

the lower back. Some companies have become insolvent and the current shares of account

owners or credit cards are used for this solution to increase It licensed a small new company

and the bank to make loans has become very difficult. EXIM Bank and through the micro

credit program SZRB (Slovakia guarantee and development), the only restriction was able to

get money. Grants for small and medium-sized enterprises..

4. Tips for small and medium-sized financial management

of the financial crisis in Slovakia during Enterprise use

In the current economic literature on the financial crisis and the global economy, the

financial management of companies in best practices in discussions from our research

we have for small and medium-sized entrepreneurs received. Under financial

management tips

1. Small and medium-sized during the long-term crisis that will fill the aircraft and the

strategy and the shareholders of the company have the appropriate value attached to the

company, focusing on the main goal is important for the Ministry of Finance to

implement the strategy Created corporate strategy, economy, marketing and related

activities for choosing a company, therefore determining the scope and direction of the

financial strategy project Many are working strategies. This is an organization's strategy

for supporting and making strategic financial decisions. Increasing finances helps to

evaluate strategic options. Existing operations will help monitor and execute decisions.

these The operational decisions of the said appraisal and the company audit on cash

flow are expected to be important for the increase of

2. Dealing with the financial and economic crisis to be completely ready to small and

medium-sized enterprises to monitor the economic environment and major changes in

their environment, the need to recognize warning signs Comments on various rating

institutions and foreign banks and predictions, even if they have to pay attention to the

financial health of their suppliers, diversification of customer needs, analysis,

examination of the results. Important in the planning process, needs to be converted into

variables

3. Small and medium-sized cash flow management should be more focused in order to

survive the crisis, small and medium-sized enterprises will address the dissolved

materials and the need to have sufficient liquidity, this is a special collection. Of

agreements with customers, suppliers and assessing credit card businesses and checking

the financial health of customers, working with city management of rehabilitation can

be done by debt repayment The Slovakian government, which helps small and medium

enterprises to overcome the financial crisis, take measures to increase production

efficiency and reduce its impact on the ecosystem with the goal of achieving efficiency.

usage Innovative energy and higher transfer technology and support for small and

medium-sized enterprises, a financial program that has Small and medium-sized

lockout "In competition and economic growth through a program known as" operating

or requesting financial assistance through a program sponsored by the European Union;

For example, in the competition and innovation framework program or for research and

technology development in the seventh frame project (*** 2011) 1. The majority of

small and medium-sized entrepreneurs and the performance of their companies and to

assess financial status and use financial ratios. This is a ratio helping to analyze current

and past conditions and planning for the future. Is a starting point in order to anticipate

the future growth of non-financial indicators for auditing and analysis; For example,

customer satisfaction, employee satisfaction, retention of high quality staff and

innovation (Cerna 2010). These are the indicators and business advantages by pointing

evaluate strategic options. Existing operations will help monitor and execute decisions.

these The operational decisions of the said appraisal and the company audit on cash

flow are expected to be important for the increase of

2. Dealing with the financial and economic crisis to be completely ready to small and

medium-sized enterprises to monitor the economic environment and major changes in

their environment, the need to recognize warning signs Comments on various rating

institutions and foreign banks and predictions, even if they have to pay attention to the

financial health of their suppliers, diversification of customer needs, analysis,

examination of the results. Important in the planning process, needs to be converted into

variables

3. Small and medium-sized cash flow management should be more focused in order to

survive the crisis, small and medium-sized enterprises will address the dissolved

materials and the need to have sufficient liquidity, this is a special collection. Of

agreements with customers, suppliers and assessing credit card businesses and checking

the financial health of customers, working with city management of rehabilitation can

be done by debt repayment The Slovakian government, which helps small and medium

enterprises to overcome the financial crisis, take measures to increase production

efficiency and reduce its impact on the ecosystem with the goal of achieving efficiency.

usage Innovative energy and higher transfer technology and support for small and

medium-sized enterprises, a financial program that has Small and medium-sized

lockout "In competition and economic growth through a program known as" operating

or requesting financial assistance through a program sponsored by the European Union;

For example, in the competition and innovation framework program or for research and

technology development in the seventh frame project (*** 2011) 1. The majority of

small and medium-sized entrepreneurs and the performance of their companies and to

assess financial status and use financial ratios. This is a ratio helping to analyze current

and past conditions and planning for the future. Is a starting point in order to anticipate

the future growth of non-financial indicators for auditing and analysis; For example,

customer satisfaction, employee satisfaction, retention of high quality staff and

innovation (Cerna 2010). These are the indicators and business advantages by pointing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to new opportunities in the development of the company. Can help with long-term

predictions

The company will have to face a 2% drop in sales, access to liquidity, credit and others

during the financial crisis and are struggling for significant survival so this cost and

limit analysis will increase production value by Methods, unnecessary steps of disposal.

At the same time, high-quality products and services during the crisis, it is very

important to restrain this factor If this process is suffering, he will be separated from the

company. Successful progress towards product quality standards for quality

management systems, using standards and attitudes to meet customer needs and the

economy, there are ways to help No The competitiveness of entrepreneurs (Kucerova,

2008) and medium-sized enterprises and review distribution agreements, pricing,

payment and distribution Discharge can negotiate conditions, save materials and

products to reduce the number of their employees better, better working capital

management and strict..

5.CONCLUSION

Finally, the end of the year for Gross Domestic Product (GDP) in the Slovak Republic increased by

4.5%. This depends on the 2011 development. There is also a positive development in this year's GDP

forecast and There are still some other symptoms that the global financial and economic crisis has no

hope of withdrawing. Small and medium-sized enterprises that have survived their pre-crisis market

conditions, you need to recover and re-effectiveness The business environment can help manage the

changes in current and future tools that need to be used by the system. Our hope for paper will be useful

in this process..

6.REFERENCES

Cerna, L. (2010). Business etiquette and its implementation in industrial enterprises in

Slovak Republic, AlumniPress, ISBN 978-80-8096-110-7, Trnava

Fetisovova, E. et al. (2004). Finance of small and medium-sized enterprises, IURA EDITION,

ISBN 80-89047-87-4,

predictions

The company will have to face a 2% drop in sales, access to liquidity, credit and others

during the financial crisis and are struggling for significant survival so this cost and

limit analysis will increase production value by Methods, unnecessary steps of disposal.

At the same time, high-quality products and services during the crisis, it is very

important to restrain this factor If this process is suffering, he will be separated from the

company. Successful progress towards product quality standards for quality

management systems, using standards and attitudes to meet customer needs and the

economy, there are ways to help No The competitiveness of entrepreneurs (Kucerova,

2008) and medium-sized enterprises and review distribution agreements, pricing,

payment and distribution Discharge can negotiate conditions, save materials and

products to reduce the number of their employees better, better working capital

management and strict..

5.CONCLUSION

Finally, the end of the year for Gross Domestic Product (GDP) in the Slovak Republic increased by

4.5%. This depends on the 2011 development. There is also a positive development in this year's GDP

forecast and There are still some other symptoms that the global financial and economic crisis has no

hope of withdrawing. Small and medium-sized enterprises that have survived their pre-crisis market

conditions, you need to recover and re-effectiveness The business environment can help manage the

changes in current and future tools that need to be used by the system. Our hope for paper will be useful

in this process..

6.REFERENCES

Cerna, L. (2010). Business etiquette and its implementation in industrial enterprises in

Slovak Republic, AlumniPress, ISBN 978-80-8096-110-7, Trnava

Fetisovova, E. et al. (2004). Finance of small and medium-sized enterprises, IURA EDITION,

ISBN 80-89047-87-4,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Bratislava

Kucerova, M. (2008). Improvement in Quality management system, In: Intercathedra, No 24.

Poznan, ISSN 1640-3622, pp 49-50, 2008

*** (2010) http://www.nadsme.sk/files/Stav_MSP_2009_1.pdf,

accessed on 2010-12-14

*** (2011) http://www.euractiv.sk/podnikanie-v-eu/zoznam liniek/kriza-a-male-a-stredne-

podniky-000237, accessed on 2011-01-21

2. The cash flow statement shows the company's

The cash flow statement shows the company's source of cash and cash used for a specified period

of time regarding financial reporting methods. As the value of the above non-cash items are not

included This is the company's short-term and long-term potential, especially the ability to pay

bills and determine useful dates. Cash flow management for businesses and small businesses,

especially businesses, is one of the most important. Analysts at least a quarter of every day

recommend that you study cash flow statements. Therefore, during the specified period, it is

recorded in the operations of the company in a similar cash flow statement in the income

statement. The value of some non-cash items such as accounts in the income statement, cash

flow statements, both spaces have disappeared. . All of this can then be removed and the

company that issued today shows how much money actually happened. The company's cash flow

statement with cash flow and flow management shows how they operate. This is the company's

ability to pay off debt and financial growth will provide a sharp image. If it doesn't have enough

money on hand to pay the expenses that will go under, in accordance with the accounting

standards that are perfectly possible for the company to show profits. Known as outstanding

debt, with the amount of cash generated comparing "The ratio of operating cash flow generated"

to repay the loan and its interest, indicating the company's ability to provide services. A slight

decrease in the company's cash flow for the quarter that will make the loan repayments, its

ability to be affected, even if the company's net income is minimal, strengthening the level of

cash flow and in a position with Higher risk Earnings reports can be presented in contrast to

Kucerova, M. (2008). Improvement in Quality management system, In: Intercathedra, No 24.

Poznan, ISSN 1640-3622, pp 49-50, 2008

*** (2010) http://www.nadsme.sk/files/Stav_MSP_2009_1.pdf,

accessed on 2010-12-14

*** (2011) http://www.euractiv.sk/podnikanie-v-eu/zoznam liniek/kriza-a-male-a-stredne-

podniky-000237, accessed on 2011-01-21

2. The cash flow statement shows the company's

The cash flow statement shows the company's source of cash and cash used for a specified period

of time regarding financial reporting methods. As the value of the above non-cash items are not

included This is the company's short-term and long-term potential, especially the ability to pay

bills and determine useful dates. Cash flow management for businesses and small businesses,

especially businesses, is one of the most important. Analysts at least a quarter of every day

recommend that you study cash flow statements. Therefore, during the specified period, it is

recorded in the operations of the company in a similar cash flow statement in the income

statement. The value of some non-cash items such as accounts in the income statement, cash

flow statements, both spaces have disappeared. . All of this can then be removed and the

company that issued today shows how much money actually happened. The company's cash flow

statement with cash flow and flow management shows how they operate. This is the company's

ability to pay off debt and financial growth will provide a sharp image. If it doesn't have enough

money on hand to pay the expenses that will go under, in accordance with the accounting

standards that are perfectly possible for the company to show profits. Known as outstanding

debt, with the amount of cash generated comparing "The ratio of operating cash flow generated"

to repay the loan and its interest, indicating the company's ability to provide services. A slight

decrease in the company's cash flow for the quarter that will make the loan repayments, its

ability to be affected, even if the company's net income is minimal, strengthening the level of

cash flow and in a position with Higher risk Earnings reports can be presented in contrast to

many ways in which the company and the cash situation are few. We can manage. Despite the

implicit fraud, including the cash flow statement, telling the whole story, the company's cash?

Analysts in order to understand the overall health of the company's cash flow statements will be

closely monitored..

PARTS OF THE CASH FLOW STATEMENT

Statements of cash flows in operations, investments or financing their activities in accordance

with whether the diaspora distinguish cash and payments The cash flow statements in this same

business are divided into sections by three working areas:

• Expenses - day-to-day operations of cash generated from business operations

• Cash used for investing in assets in other businesses, equipment, or other funds from long-term

asset sales - cash from investing

• Finance - cash from funds, loans, and giving, receiving money or receiving This part also

includes joint expenses. (Although sometimes he listed below the operating cash.)

• Increased cash in cash from previous years - net increase or decrease is generally written and

lower cash is usually written in parentheses.

Although cash flow statements may vary slightly, they all present data in the four sections listed

here.

CLASSIFICATIONS OF CASH RECEIPTS AND

PAYMENTS

Money from the treasury

New companies came up with ideas. A man of a person or group that will freeze the seats of the

company. At first, the owner of the money By owner or corrosion "The funded owner is a new

company that has been formed." What kind of money for the company, general financial

activities classified as equivalent or long-term liabilities and financial activities as separate items

in the balance sheet will be used will

.

implicit fraud, including the cash flow statement, telling the whole story, the company's cash?

Analysts in order to understand the overall health of the company's cash flow statements will be

closely monitored..

PARTS OF THE CASH FLOW STATEMENT

Statements of cash flows in operations, investments or financing their activities in accordance

with whether the diaspora distinguish cash and payments The cash flow statements in this same

business are divided into sections by three working areas:

• Expenses - day-to-day operations of cash generated from business operations

• Cash used for investing in assets in other businesses, equipment, or other funds from long-term

asset sales - cash from investing

• Finance - cash from funds, loans, and giving, receiving money or receiving This part also

includes joint expenses. (Although sometimes he listed below the operating cash.)

• Increased cash in cash from previous years - net increase or decrease is generally written and

lower cash is usually written in parentheses.

Although cash flow statements may vary slightly, they all present data in the four sections listed

here.

CLASSIFICATIONS OF CASH RECEIPTS AND

PAYMENTS

Money from the treasury

New companies came up with ideas. A man of a person or group that will freeze the seats of the

company. At first, the owner of the money By owner or corrosion "The funded owner is a new

company that has been formed." What kind of money for the company, general financial

activities classified as equivalent or long-term liabilities and financial activities as separate items

in the balance sheet will be used will

.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash from Investing

Business owners, equipment, or managers must run their business or use the money to buy other

assets. In other words, they invest. Property, plant and equipment and purchase of other

production assets which are classified as investment activities Sometimes other businesses will

lend money to companies that don't have enough of their own cash. This is classified as an

investment activity. In general, long-term assets in the balance sheets are separate items, will be

classified as investment activities will be candidates.

Cash from Operations

Now the company can start doing business. This purchase and operation, the money to buy the

necessary equipment and other assets. This trade, rent or sale of services and supplies, business

expenses and other taxes to pay for everything starts. The workplace for the company that was

established and the associated cash flows will be classified as operating activities. Movement

regarding the statement in the income statement, the company's cash flow, in general, the part of

the applicant in operation.

Methods of Preparing the Cash Flow Statement

Changes in the financial status of the cash flow statements of November 1987, the Financial

Accounting Standards Board (FASB), rather than the state, requires businesses to use "Financial

Accounting Standards Statements" This is a direct and indirect statement. FASB encourages, but

does not need to use direct methods for reporting methods and preparing the next two methods.

Day-to-day operations of investments and financial sector involvement report both methods

regardless of the proposed methods being presented in the same way.

Direct Method

In addition, the operating method of the income statement is called the direct cash receipt and

payment method of the main level reports. Statement of the cash flow from the use of the method

of preparing beef Ngwe to calculate the money spent, and then began to record received

Therefore, despite the net profit, the impact on money expenses that are not received or

exempted because the value is zero..

Business owners, equipment, or managers must run their business or use the money to buy other

assets. In other words, they invest. Property, plant and equipment and purchase of other

production assets which are classified as investment activities Sometimes other businesses will

lend money to companies that don't have enough of their own cash. This is classified as an

investment activity. In general, long-term assets in the balance sheets are separate items, will be

classified as investment activities will be candidates.

Cash from Operations

Now the company can start doing business. This purchase and operation, the money to buy the

necessary equipment and other assets. This trade, rent or sale of services and supplies, business

expenses and other taxes to pay for everything starts. The workplace for the company that was

established and the associated cash flows will be classified as operating activities. Movement

regarding the statement in the income statement, the company's cash flow, in general, the part of

the applicant in operation.

Methods of Preparing the Cash Flow Statement

Changes in the financial status of the cash flow statements of November 1987, the Financial

Accounting Standards Board (FASB), rather than the state, requires businesses to use "Financial

Accounting Standards Statements" This is a direct and indirect statement. FASB encourages, but

does not need to use direct methods for reporting methods and preparing the next two methods.

Day-to-day operations of investments and financial sector involvement report both methods

regardless of the proposed methods being presented in the same way.

Direct Method

In addition, the operating method of the income statement is called the direct cash receipt and

payment method of the main level reports. Statement of the cash flow from the use of the method

of preparing beef Ngwe to calculate the money spent, and then began to record received

Therefore, despite the net profit, the impact on money expenses that are not received or

exempted because the value is zero..

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Indirect Method

This method is the only way to reconcile the net operating income and focus on the flow of Tin

Ngwe. One default with net income is inserted again using this method and then to calculate the

change in Balance sheet items The most direct method to produce the same result is Ngwe flow.

Therefore, the value is a negative expense. Net income beginning with the indirect method is

equal to added value. However, whether it is a direct or indirect method, the cash flow statement

from operating activities Ngwe (three) at the end of the operating section in the header. This is

the most important thing to the cash flow of the advertising statement. The company will

maintain its business activities to generate enough cash flow from operations. The company will

not need to receive additional investment funds or borrow to survive the company. In the long-

term existence is in danger.

.

FINANCING AND INVESTING SECTIONS

The cash flows, in and out, resulting from financing and investing activities are listed in the same

way whether the direct or indirect method of presentation is employed.

Cash Flows from Investing

The cash flow statements shown below in respect of the main lines of this product are:

• Capital Expenses This is the amount of land, buildings and equipment and products that have a

long life means spending money. When increasing investment expenditure, it often means that

the company is expanding.

• Investment profits. Companies often spend some of their excess cash. Savings accounts or

money market funds can be invested in an effort to get better returns. This company has made

about showing that this investment figure is lost or lost.

• Business acquisition or sales These numbers are from the purchase or sale of the subsidiary's

business and sometimes more. Here, the company is made from the operating activities section

of cash flow, including the money that will appear if.

Cash Flows from Financing

This method is the only way to reconcile the net operating income and focus on the flow of Tin

Ngwe. One default with net income is inserted again using this method and then to calculate the

change in Balance sheet items The most direct method to produce the same result is Ngwe flow.

Therefore, the value is a negative expense. Net income beginning with the indirect method is

equal to added value. However, whether it is a direct or indirect method, the cash flow statement

from operating activities Ngwe (three) at the end of the operating section in the header. This is

the most important thing to the cash flow of the advertising statement. The company will

maintain its business activities to generate enough cash flow from operations. The company will

not need to receive additional investment funds or borrow to survive the company. In the long-

term existence is in danger.

.

FINANCING AND INVESTING SECTIONS

The cash flows, in and out, resulting from financing and investing activities are listed in the same

way whether the direct or indirect method of presentation is employed.

Cash Flows from Investing

The cash flow statements shown below in respect of the main lines of this product are:

• Capital Expenses This is the amount of land, buildings and equipment and products that have a

long life means spending money. When increasing investment expenditure, it often means that

the company is expanding.

• Investment profits. Companies often spend some of their excess cash. Savings accounts or

money market funds can be invested in an effort to get better returns. This company has made

about showing that this investment figure is lost or lost.

• Business acquisition or sales These numbers are from the purchase or sale of the subsidiary's

business and sometimes more. Here, the company is made from the operating activities section

of cash flow, including the money that will appear if.

Cash Flows from Financing

To pay the company $ in figures released during the time period: This cash flow statement

includes things such as main line items

• Common shares issued / road brokers are not financial companies, the activities of this new

show, the number of companies growing rapidly Usually a new stock will be blended and the

value of the current stock This practice But since the company's cash for expansion, the company

set up its own shares to repurchase will be in position, and when this will help increase the value

of existing shares

• Debt / Debt Settlement of the amount of the securities issuing company or borrowing money to

repay the loan before you the securities company to raise funds in the stock, there are ways to

choose the main issues.Cash flow statements with most companies, all prepared by publicly

traded companies, need to be submitted with the Securities and Exchange Commission as the

latest of the three basic financial statements. There are often different forms and other statements

of income statements or balance sheets for the majority of components contained in the report.

However, the company's income, regardless of the manufacturer, a woman in her will do to meet

short-term obligations to management methods and investors, savings and loans, and present the

views of those Company distributor.

.

BIBLIOGRAPHY

Brahmasrene, Tantatape, and C. David Strupeck, Donna Whitten. "Examining Preferences in

Cash Flow Statement Format." The CPA Journal. October 2004.

Hey-Cunningham, David. Financial Statements Demystified. Allen & Unwin, 2002.

O'Connor, Tricia. "The Formula for Determini.ng Cash Flow." Denver Business Journal. 2 June

2000.

Taulli, Tom. The Edgar Online Guide to Decoding Financial Statements. J. Ross Publishing,

2004.

"Ten Ways to Improve Small Business Cash Flow." Journal of Accountancy. March 2000.

includes things such as main line items

• Common shares issued / road brokers are not financial companies, the activities of this new

show, the number of companies growing rapidly Usually a new stock will be blended and the

value of the current stock This practice But since the company's cash for expansion, the company

set up its own shares to repurchase will be in position, and when this will help increase the value

of existing shares

• Debt / Debt Settlement of the amount of the securities issuing company or borrowing money to

repay the loan before you the securities company to raise funds in the stock, there are ways to

choose the main issues.Cash flow statements with most companies, all prepared by publicly

traded companies, need to be submitted with the Securities and Exchange Commission as the

latest of the three basic financial statements. There are often different forms and other statements

of income statements or balance sheets for the majority of components contained in the report.

However, the company's income, regardless of the manufacturer, a woman in her will do to meet

short-term obligations to management methods and investors, savings and loans, and present the

views of those Company distributor.

.

BIBLIOGRAPHY

Brahmasrene, Tantatape, and C. David Strupeck, Donna Whitten. "Examining Preferences in

Cash Flow Statement Format." The CPA Journal. October 2004.

Hey-Cunningham, David. Financial Statements Demystified. Allen & Unwin, 2002.

O'Connor, Tricia. "The Formula for Determini.ng Cash Flow." Denver Business Journal. 2 June

2000.

Taulli, Tom. The Edgar Online Guide to Decoding Financial Statements. J. Ross Publishing,

2004.

"Ten Ways to Improve Small Business Cash Flow." Journal of Accountancy. March 2000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 34

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.