Taxation Laws: Deductions, Concessions, and Capital Gains Analysis

VerifiedAdded on 2021/05/31

|16

|3482

|89

Report

AI Summary

This report is a comprehensive analysis of Australian taxation laws, specifically focusing on deductions, capital gains tax (CGT), and small business concessions. The report examines various scenarios and provides detailed answers to questions regarding allowable deductions for expenses such as repairs, depreciation of assets, and car expenses, referencing relevant sections of the ITAA 1997. It also addresses non-allowable deductions, including those related to capital expenses and fines. Furthermore, the report delves into CGT, covering the treatment of collectibles, personal use assets, and CGT assets like shares. The second part of the report provides an overview of small business concessions, including their types, eligibility criteria, objectives, and historical context, concluding with a discussion on the effectiveness of these methods and recommendations. The report uses case studies to illustrate the application of tax laws and provides a clear understanding of complex tax principles.

Running head: TAXATION LAWS

Taxation Laws

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Laws

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAWS

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to C:..........................................................................................................................4

Answer to D:..........................................................................................................................4

Answer to E:...........................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................5

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................6

Answer to E:...........................................................................................................................6

Answer to question 3:.................................................................................................................7

Answer to A:..........................................................................................................................7

Answer to B:..........................................................................................................................7

Answer to C:..........................................................................................................................8

Answer to D:..........................................................................................................................8

Answer to E:...........................................................................................................................9

Part B: Small Business Concessions:.......................................................................................10

Introduction:.............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................3

Answer to A:..........................................................................................................................3

Answer to B:..........................................................................................................................3

Answer to C:..........................................................................................................................4

Answer to D:..........................................................................................................................4

Answer to E:...........................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer to A:..........................................................................................................................5

Answer to B:..........................................................................................................................5

Answer to C:..........................................................................................................................6

Answer to D:..........................................................................................................................6

Answer to E:...........................................................................................................................6

Answer to question 3:.................................................................................................................7

Answer to A:..........................................................................................................................7

Answer to B:..........................................................................................................................7

Answer to C:..........................................................................................................................8

Answer to D:..........................................................................................................................8

Answer to E:...........................................................................................................................9

Part B: Small Business Concessions:.......................................................................................10

Introduction:.............................................................................................................................10

2TAXATION LAWS

Types of small Business Concessions:.....................................................................................10

Criteria for meeting the eligibility of concessions:..................................................................10

Objectives of the small business Concessions:........................................................................11

History of measuring tax for small business:...........................................................................11

Current amendments that are made to the small business concessions:..................................11

Effectiveness of the methods:..................................................................................................13

Recommendations:...................................................................................................................13

Conclusion:..............................................................................................................................13

Reference List:.........................................................................................................................14

Types of small Business Concessions:.....................................................................................10

Criteria for meeting the eligibility of concessions:..................................................................10

Objectives of the small business Concessions:........................................................................11

History of measuring tax for small business:...........................................................................11

Current amendments that are made to the small business concessions:..................................11

Effectiveness of the methods:..................................................................................................13

Recommendations:...................................................................................................................13

Conclusion:..............................................................................................................................13

Reference List:.........................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAWS

Answer to question 1:

Answer to A:

As defined under “section 25-10 of the ITAA 1997” a person is entitled to claim an

allowable deduction for expense relating to repairs performed on the premises and any

deprecating asset which is solely held for the deriving assessable income. Nevertheless, the

provision of this section prohibits a person from any deductions relating to expenses that are

solely capital in nature (Woellner et al., 2016). Bhavraj reports an expense on repainting the

building of the restaurant to reflect Indian theme. Denoting the judgement in “W Thomas and

Co Pty Ltd v FCT (1965)” cost of repairing and painting the initially acquired is not allowed

for deductions since it is a capital expense. The cost of repainting the restaurant building

reflects an initial repair which is non-allowable capital expenditure.

Answer to B:

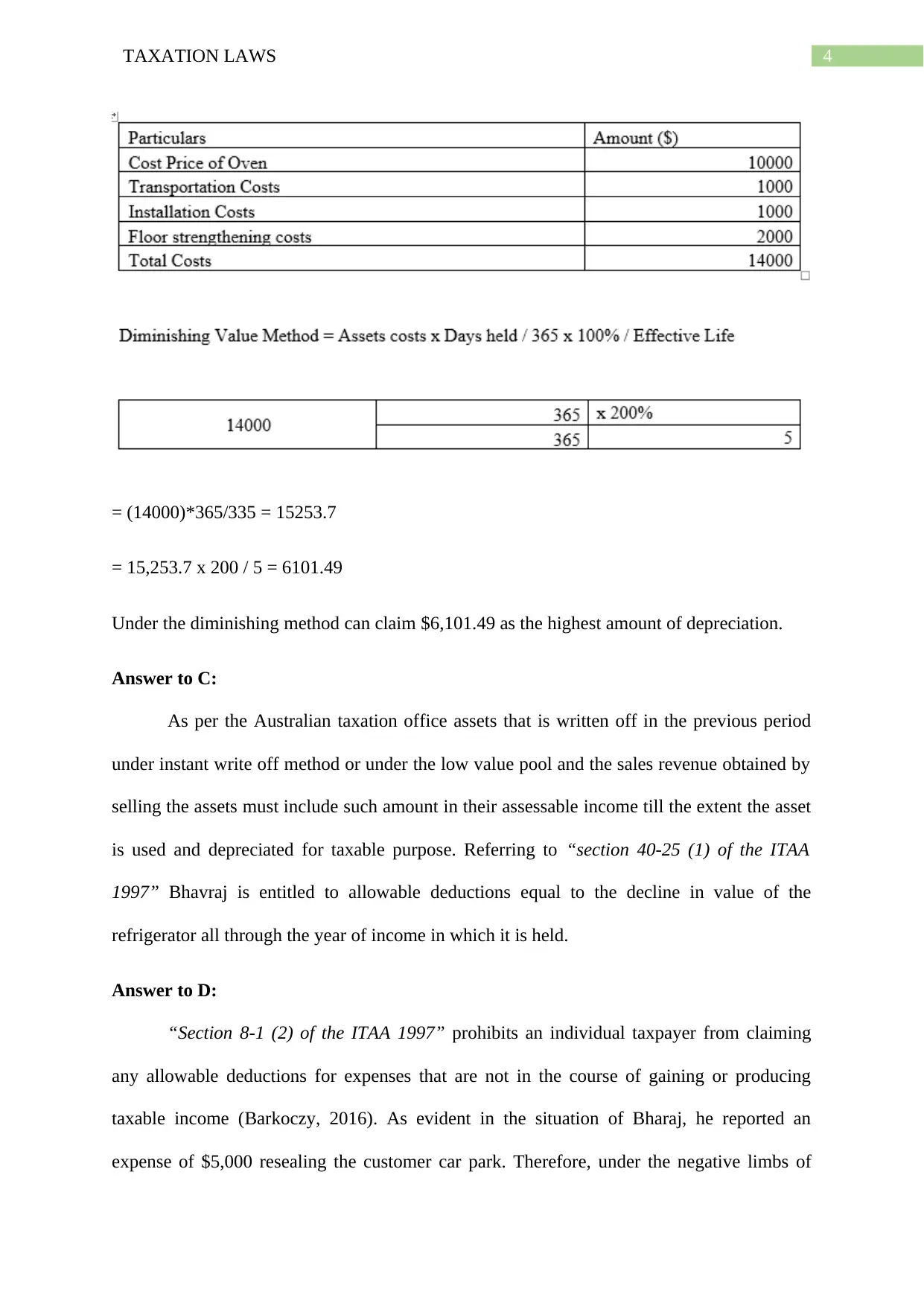

Referring to “division 40-25(1)” an individual entity is entitled to claim a sum that is

equal to the decline in the value of the asset during the year in which it is held (Anderson et

al., 2016). Bhavraj reported expense on purchase of new oven that costs $10,000 with

additional expenses of $1,000 each for transportation and installation. Based on rules of

simpler depreciation for small entity a person can immediately write off or subtract the entire

cost of asset in the year of purchase given the asset costs is less than $20,000. The

transportation costs and installation costs forms the cost of assets. Bhavraj can write-off the

cost of assets as it is less than $20,000.

Answer to question 1:

Answer to A:

As defined under “section 25-10 of the ITAA 1997” a person is entitled to claim an

allowable deduction for expense relating to repairs performed on the premises and any

deprecating asset which is solely held for the deriving assessable income. Nevertheless, the

provision of this section prohibits a person from any deductions relating to expenses that are

solely capital in nature (Woellner et al., 2016). Bhavraj reports an expense on repainting the

building of the restaurant to reflect Indian theme. Denoting the judgement in “W Thomas and

Co Pty Ltd v FCT (1965)” cost of repairing and painting the initially acquired is not allowed

for deductions since it is a capital expense. The cost of repainting the restaurant building

reflects an initial repair which is non-allowable capital expenditure.

Answer to B:

Referring to “division 40-25(1)” an individual entity is entitled to claim a sum that is

equal to the decline in the value of the asset during the year in which it is held (Anderson et

al., 2016). Bhavraj reported expense on purchase of new oven that costs $10,000 with

additional expenses of $1,000 each for transportation and installation. Based on rules of

simpler depreciation for small entity a person can immediately write off or subtract the entire

cost of asset in the year of purchase given the asset costs is less than $20,000. The

transportation costs and installation costs forms the cost of assets. Bhavraj can write-off the

cost of assets as it is less than $20,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAWS

= (14000)*365/335 = 15253.7

= 15,253.7 x 200 / 5 = 6101.49

Under the diminishing method can claim $6,101.49 as the highest amount of depreciation.

Answer to C:

As per the Australian taxation office assets that is written off in the previous period

under instant write off method or under the low value pool and the sales revenue obtained by

selling the assets must include such amount in their assessable income till the extent the asset

is used and depreciated for taxable purpose. Referring to “section 40-25 (1) of the ITAA

1997” Bhavraj is entitled to allowable deductions equal to the decline in value of the

refrigerator all through the year of income in which it is held.

Answer to D:

“Section 8-1 (2) of the ITAA 1997” prohibits an individual taxpayer from claiming

any allowable deductions for expenses that are not in the course of gaining or producing

taxable income (Barkoczy, 2016). As evident in the situation of Bharaj, he reported an

expense of $5,000 resealing the customer car park. Therefore, under the negative limbs of

= (14000)*365/335 = 15253.7

= 15,253.7 x 200 / 5 = 6101.49

Under the diminishing method can claim $6,101.49 as the highest amount of depreciation.

Answer to C:

As per the Australian taxation office assets that is written off in the previous period

under instant write off method or under the low value pool and the sales revenue obtained by

selling the assets must include such amount in their assessable income till the extent the asset

is used and depreciated for taxable purpose. Referring to “section 40-25 (1) of the ITAA

1997” Bhavraj is entitled to allowable deductions equal to the decline in value of the

refrigerator all through the year of income in which it is held.

Answer to D:

“Section 8-1 (2) of the ITAA 1997” prohibits an individual taxpayer from claiming

any allowable deductions for expenses that are not in the course of gaining or producing

taxable income (Barkoczy, 2016). As evident in the situation of Bharaj, he reported an

expense of $5,000 resealing the customer car park. Therefore, under the negative limbs of

5TAXATION LAWS

section 8-1 (2) of the ITAA 1997 the expenses are neither relevant nor incidental in

derivation of Bhavraj assessable income hence no deductions will be allowed for cost of

resealing the customer car park.

Answer to E:

As defined by the Australian Taxation Office car refers to the motor vehicle which is

created to carry weight of lower than one tonne (Tan et al., 2016). While working the

depreciation a person can use the cents per kilo metre method or the log book method for

claiming the deductions. Similarly Bhavraj can claim deductions for the cost of running the

car as the car was solely used for business purpose.

Answer to question 2:

Answer to A:

As defined under the “ATO ID 2004/489” expenses that are incurred for long service

leave contribution made to the worker by the employee would be allowed for deductions

under “section 8-1 of the ITAA 1997” (Long et al., 2016). As evident in the situation of Raj

the payment that is made by him into his employee long service leave shall be considered as

the allowable deductions under “section 8-1 of the ITAA 1997”. The reason for being held

deductible is because it is incurred in the course of gaining taxable income.

Answer to B:

As defined under “Section 26-5 of the ITAA 1997” a person is prohibited from

claiming any deductions in respect of fines or penalties which is imposed in the form of

breach of Australian law (Cao et al., 2015). This consists of the fines relating to parking that

is occurred while travelling in the course of work. Evidently in the situation of Raj the

parking fines that was incurred by his employee would not be allowed as deductions since it

section 8-1 (2) of the ITAA 1997 the expenses are neither relevant nor incidental in

derivation of Bhavraj assessable income hence no deductions will be allowed for cost of

resealing the customer car park.

Answer to E:

As defined by the Australian Taxation Office car refers to the motor vehicle which is

created to carry weight of lower than one tonne (Tan et al., 2016). While working the

depreciation a person can use the cents per kilo metre method or the log book method for

claiming the deductions. Similarly Bhavraj can claim deductions for the cost of running the

car as the car was solely used for business purpose.

Answer to question 2:

Answer to A:

As defined under the “ATO ID 2004/489” expenses that are incurred for long service

leave contribution made to the worker by the employee would be allowed for deductions

under “section 8-1 of the ITAA 1997” (Long et al., 2016). As evident in the situation of Raj

the payment that is made by him into his employee long service leave shall be considered as

the allowable deductions under “section 8-1 of the ITAA 1997”. The reason for being held

deductible is because it is incurred in the course of gaining taxable income.

Answer to B:

As defined under “Section 26-5 of the ITAA 1997” a person is prohibited from

claiming any deductions in respect of fines or penalties which is imposed in the form of

breach of Australian law (Cao et al., 2015). This consists of the fines relating to parking that

is occurred while travelling in the course of work. Evidently in the situation of Raj the

parking fines that was incurred by his employee would not be allowed as deductions since it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAWS

is a breach of Australian law. With respect to Section 26-5 of the ITAA 1997”, the parking

fines of $5,000 is a non-allowable deductions.

Answer to C:

An expenditure is allowed as deductions given the outgoings are held relevant and

incidental in the derivation of the assessable income of the taxpayer. Citing the reference of

“W Neville & Co v FCT” the court of law permitted the taxpayer from claiming allowable

deductions relating to the payment that was made for agreeing the managing director to

resignation (Saad, 2014). This is because the payment made was to increase the business

efficiency. Similarly, in the case of Raj the payment that is made the restaurant manager for

obtaining the resignation is an allowable deductions under “section 8-1 of the ITAA 1997”.

Answer to D:

As stated by the Australian Taxation Office an individual taxpayer can be entitled to

claim a permissible deduction for the expenses that is incurred in relation to the

superannuation payment of the employees. Raj would be allowed to claim an allowable

deductions for an amount of $45,000 relating to the contributions that is by him in the

employee superannuation fund.

Answer to E:

Losses or outgoings that are incurred during the preliminary stage of business or prior

to the commencement of income producing activities is not allowed as deductions under

“section 8-1 of the ITAA 1997”. Citing the case of “Softwood Pulp & Paper v Federal

Commissioner of Taxation (1976)” the taxpayer reported an expenses that was related to the

feasibility study with other cost to commence the production of the paper mill (Robin &

Barkoczy, 2018). The court of law held that the expenditure was in nature of preliminary and

non-deductible. As evident in the current case of Raj, the cost that was incurred for the

is a breach of Australian law. With respect to Section 26-5 of the ITAA 1997”, the parking

fines of $5,000 is a non-allowable deductions.

Answer to C:

An expenditure is allowed as deductions given the outgoings are held relevant and

incidental in the derivation of the assessable income of the taxpayer. Citing the reference of

“W Neville & Co v FCT” the court of law permitted the taxpayer from claiming allowable

deductions relating to the payment that was made for agreeing the managing director to

resignation (Saad, 2014). This is because the payment made was to increase the business

efficiency. Similarly, in the case of Raj the payment that is made the restaurant manager for

obtaining the resignation is an allowable deductions under “section 8-1 of the ITAA 1997”.

Answer to D:

As stated by the Australian Taxation Office an individual taxpayer can be entitled to

claim a permissible deduction for the expenses that is incurred in relation to the

superannuation payment of the employees. Raj would be allowed to claim an allowable

deductions for an amount of $45,000 relating to the contributions that is by him in the

employee superannuation fund.

Answer to E:

Losses or outgoings that are incurred during the preliminary stage of business or prior

to the commencement of income producing activities is not allowed as deductions under

“section 8-1 of the ITAA 1997”. Citing the case of “Softwood Pulp & Paper v Federal

Commissioner of Taxation (1976)” the taxpayer reported an expenses that was related to the

feasibility study with other cost to commence the production of the paper mill (Robin &

Barkoczy, 2018). The court of law held that the expenditure was in nature of preliminary and

non-deductible. As evident in the current case of Raj, the cost that was incurred for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAWS

feasibility study of would not be allowed as deductions since it is preliminary business costs

and non-deductible under “section 8-1 of the ITAA 1997”.

Answer to question 3:

Answer to A:

As defined under the “section 108-10 (2) of the ITAA 1997” collectibles represent any

form of artwork, antique or jewellery which is usually kept for an individual taxpayers

personal use and enjoyment (Murphy, & Higgins, 2016). As stated under “section 118-

10(1)” capital gains or loss from the collectibles should be disregarded in the first element

given the cost base of the collectibles is less than $500. Similarly, the present situation it is

noticed that the antique desk was purchased for $4,000 but was sold at a loss of 500 (i.e.

$3500).

As defined under the “subsection 108-10 (1) of the ITAA 1997” while determining the

net amount of capital gains during the income year capital loss that are made from the

collectables can be used only to offset the capital gains made from collectibles (Blakelock &

King, 2017). A taxpayer is under obligation of disregarding the capital loss incurred from the

collectibles. The loss sustained from the sale of the antique desk is not permitted for offset as

there was no such instances of capital gains from the sale of collectibles. Raj under

“subsection 108-10 of the ITAA 1997” is required to disregard the loss sustained from the

disposal of antique desk.

Answer to B:

Personal use asset can be defined under “subdivision 108-C” as those assets that are

mainly kept or used for personal enjoyment and use but does not include land and buildings

(McDaniel, 2017). This usually comprises of the electrical goods, households items, Yacht

and furniture. Referring to “section 118-10 (3)” capital gains that are made from the sale of

feasibility study of would not be allowed as deductions since it is preliminary business costs

and non-deductible under “section 8-1 of the ITAA 1997”.

Answer to question 3:

Answer to A:

As defined under the “section 108-10 (2) of the ITAA 1997” collectibles represent any

form of artwork, antique or jewellery which is usually kept for an individual taxpayers

personal use and enjoyment (Murphy, & Higgins, 2016). As stated under “section 118-

10(1)” capital gains or loss from the collectibles should be disregarded in the first element

given the cost base of the collectibles is less than $500. Similarly, the present situation it is

noticed that the antique desk was purchased for $4,000 but was sold at a loss of 500 (i.e.

$3500).

As defined under the “subsection 108-10 (1) of the ITAA 1997” while determining the

net amount of capital gains during the income year capital loss that are made from the

collectables can be used only to offset the capital gains made from collectibles (Blakelock &

King, 2017). A taxpayer is under obligation of disregarding the capital loss incurred from the

collectibles. The loss sustained from the sale of the antique desk is not permitted for offset as

there was no such instances of capital gains from the sale of collectibles. Raj under

“subsection 108-10 of the ITAA 1997” is required to disregard the loss sustained from the

disposal of antique desk.

Answer to B:

Personal use asset can be defined under “subdivision 108-C” as those assets that are

mainly kept or used for personal enjoyment and use but does not include land and buildings

(McDaniel, 2017). This usually comprises of the electrical goods, households items, Yacht

and furniture. Referring to “section 118-10 (3)” capital gains that are made from the sale of

8TAXATION LAWS

the personal use assets should be disregarded if the cost base of the asset is $10,000 or less.

With respect to section “section 118-10 (3)” Raj is reports a capital gains on selling the

Yacht. However, Raj under the provision of “section 118-10 (3)” is required to disregard

such capital gains as the Yacht was acquired for $6,000 which is less than the prescribed cost

base of $6,000.

Answer to C:

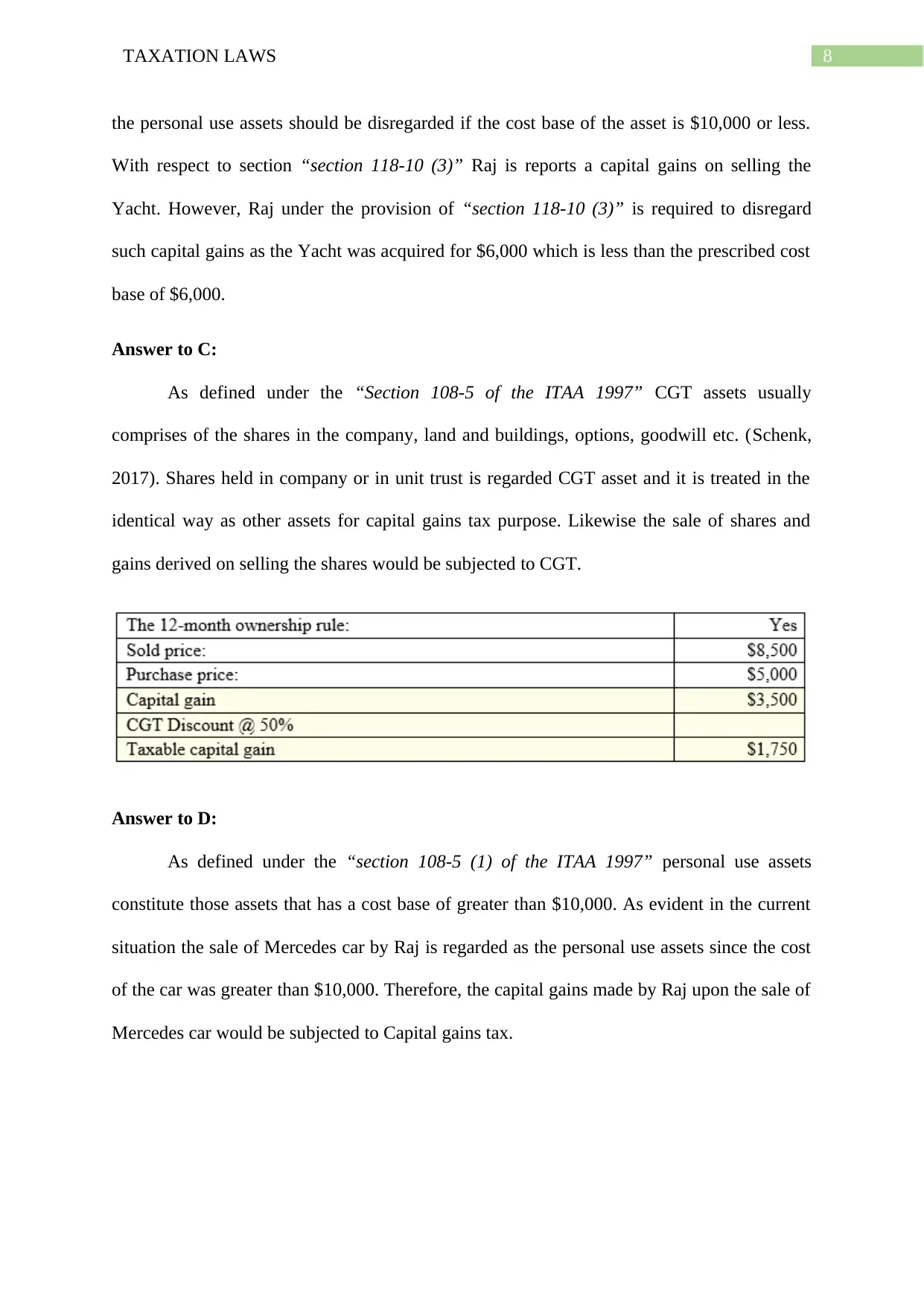

As defined under the “Section 108-5 of the ITAA 1997” CGT assets usually

comprises of the shares in the company, land and buildings, options, goodwill etc. (Schenk,

2017). Shares held in company or in unit trust is regarded CGT asset and it is treated in the

identical way as other assets for capital gains tax purpose. Likewise the sale of shares and

gains derived on selling the shares would be subjected to CGT.

Answer to D:

As defined under the “section 108-5 (1) of the ITAA 1997” personal use assets

constitute those assets that has a cost base of greater than $10,000. As evident in the current

situation the sale of Mercedes car by Raj is regarded as the personal use assets since the cost

of the car was greater than $10,000. Therefore, the capital gains made by Raj upon the sale of

Mercedes car would be subjected to Capital gains tax.

the personal use assets should be disregarded if the cost base of the asset is $10,000 or less.

With respect to section “section 118-10 (3)” Raj is reports a capital gains on selling the

Yacht. However, Raj under the provision of “section 118-10 (3)” is required to disregard

such capital gains as the Yacht was acquired for $6,000 which is less than the prescribed cost

base of $6,000.

Answer to C:

As defined under the “Section 108-5 of the ITAA 1997” CGT assets usually

comprises of the shares in the company, land and buildings, options, goodwill etc. (Schenk,

2017). Shares held in company or in unit trust is regarded CGT asset and it is treated in the

identical way as other assets for capital gains tax purpose. Likewise the sale of shares and

gains derived on selling the shares would be subjected to CGT.

Answer to D:

As defined under the “section 108-5 (1) of the ITAA 1997” personal use assets

constitute those assets that has a cost base of greater than $10,000. As evident in the current

situation the sale of Mercedes car by Raj is regarded as the personal use assets since the cost

of the car was greater than $10,000. Therefore, the capital gains made by Raj upon the sale of

Mercedes car would be subjected to Capital gains tax.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAWS

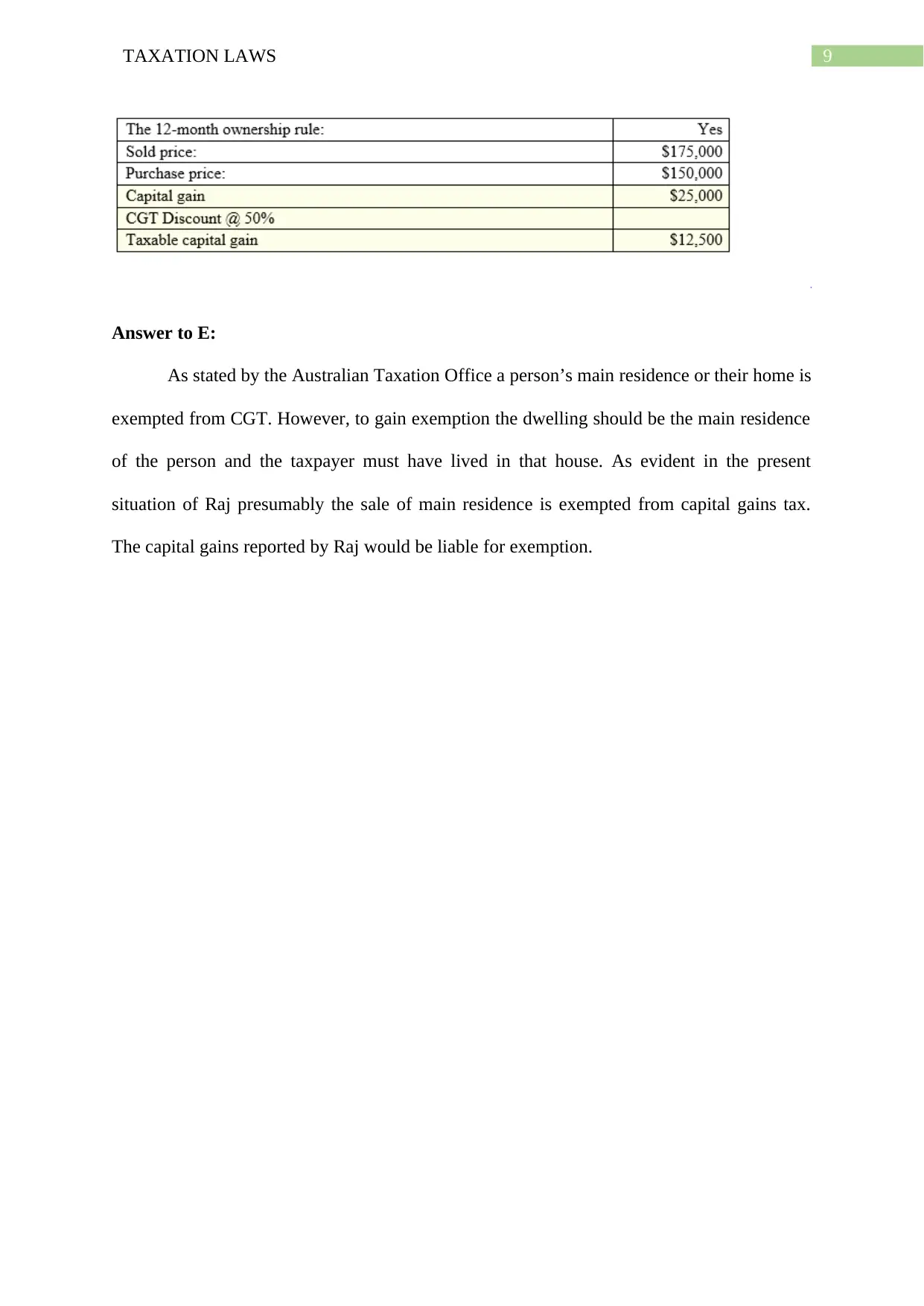

Answer to E:

As stated by the Australian Taxation Office a person’s main residence or their home is

exempted from CGT. However, to gain exemption the dwelling should be the main residence

of the person and the taxpayer must have lived in that house. As evident in the present

situation of Raj presumably the sale of main residence is exempted from capital gains tax.

The capital gains reported by Raj would be liable for exemption.

Answer to E:

As stated by the Australian Taxation Office a person’s main residence or their home is

exempted from CGT. However, to gain exemption the dwelling should be the main residence

of the person and the taxpayer must have lived in that house. As evident in the present

situation of Raj presumably the sale of main residence is exempted from capital gains tax.

The capital gains reported by Raj would be liable for exemption.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAWS

Part B: Small Business Concessions:

Introduction:

Small business forms the sizeable share of Australia. Small business contributes

greater $1.4 trillion in the form of revenue for the Australian government. Even after making

large amount of contributions they fail to get the large scale benefits then the large business

(Woellner et al., 2016). Owing to the increasing importance of small business a small

business tax system was bought into the action with the objective of providing the small

business an options of measuring the tax and simplifying the measures of tax by

simultaneously lowering the cost of compliance. The CGT concessions for small business

enables the taxpayers with the objective of lowering or removing the capital gains made on

definite assets.

Types of small Business Concessions:

Small business concessions are of four types namely;

a. 50% reduction in the active assets

b. Exemptions associated to retirement

c. 15 year exemptions

d. Exemptions of rollover

Criteria for meeting the eligibility of concessions:

For a small business taxpayer there are certain kinds of criteria that is required to be met

and these are as follows;

a. Fulfilling the test of Net Asset Value

b. Fulfilling the criteria of active asset

c. Where the assets are as shares in company or unit in the trust

Part B: Small Business Concessions:

Introduction:

Small business forms the sizeable share of Australia. Small business contributes

greater $1.4 trillion in the form of revenue for the Australian government. Even after making

large amount of contributions they fail to get the large scale benefits then the large business

(Woellner et al., 2016). Owing to the increasing importance of small business a small

business tax system was bought into the action with the objective of providing the small

business an options of measuring the tax and simplifying the measures of tax by

simultaneously lowering the cost of compliance. The CGT concessions for small business

enables the taxpayers with the objective of lowering or removing the capital gains made on

definite assets.

Types of small Business Concessions:

Small business concessions are of four types namely;

a. 50% reduction in the active assets

b. Exemptions associated to retirement

c. 15 year exemptions

d. Exemptions of rollover

Criteria for meeting the eligibility of concessions:

For a small business taxpayer there are certain kinds of criteria that is required to be met

and these are as follows;

a. Fulfilling the test of Net Asset Value

b. Fulfilling the criteria of active asset

c. Where the assets are as shares in company or unit in the trust

11TAXATION LAWS

Objectives of the small business Concessions:

The purpose of the small business concessions was to give the taxpayers with a new

platform of dealing with tax. The purpose of applying the simplified rules of business is to

lower down the cost of tax compliance cost for around 95% of the business (Anderson et al.,

2016). The actual small business concessions provide the business with the options of

collectively undertaking four sets of tax treatment. This comprises of the simplified

depreciations rules, accounting in cash for the purpose of income tax, simplified business

rules trading stock and the claiming tax deductions immediately for prepaid expenses. These

four types of concessions that are determined by the business was to give the small business

with the ability of increasing the simplicity of the business.

History of measuring tax for small business:

By gauging into the history of the business it reflects that there are additional

concessions for the business that comprised of CGT relief and GST relief for the purpose of

accounting based on the cash basis (Barkoczy, 2016). The small business concessions were

implemented on business that had the annual turnover was lower than $1 million every year,

even though the test of eligibility differed in respect of the additional related provision. Under

the traditional system it ignored the debtors and the credits with the taxation of work-in-

progress when it realised.

Current amendments that are made to the small business concessions:

The current amendments have been introduced by the small business which is

intended to achieve the simplifications and greater amount of fairness for the small business.

The recent amendments include the options of accounting for GST on the cash basis. Other

prominent changes are stated below;

Objectives of the small business Concessions:

The purpose of the small business concessions was to give the taxpayers with a new

platform of dealing with tax. The purpose of applying the simplified rules of business is to

lower down the cost of tax compliance cost for around 95% of the business (Anderson et al.,

2016). The actual small business concessions provide the business with the options of

collectively undertaking four sets of tax treatment. This comprises of the simplified

depreciations rules, accounting in cash for the purpose of income tax, simplified business

rules trading stock and the claiming tax deductions immediately for prepaid expenses. These

four types of concessions that are determined by the business was to give the small business

with the ability of increasing the simplicity of the business.

History of measuring tax for small business:

By gauging into the history of the business it reflects that there are additional

concessions for the business that comprised of CGT relief and GST relief for the purpose of

accounting based on the cash basis (Barkoczy, 2016). The small business concessions were

implemented on business that had the annual turnover was lower than $1 million every year,

even though the test of eligibility differed in respect of the additional related provision. Under

the traditional system it ignored the debtors and the credits with the taxation of work-in-

progress when it realised.

Current amendments that are made to the small business concessions:

The current amendments have been introduced by the small business which is

intended to achieve the simplifications and greater amount of fairness for the small business.

The recent amendments include the options of accounting for GST on the cash basis. Other

prominent changes are stated below;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.