Management Accounting Report: Analysis of Smart Looks Ltd

VerifiedAdded on 2019/12/28

|23

|7362

|191

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles as applied to Smart Looks Ltd, a clothing retailer. It begins by classifying costs into fixed, variable, and semi-variable categories, followed by a discussion of total cost computation and inventory costing methods like FIFO, LIFO, and average cost. The report then delves into costing analysis, including a graphical presentation of cost structures and the cost of goods sold performance. Furthermore, it examines performance indicators useful for measuring company performance and discusses methods for reducing costs and managing quality. Budgeting is addressed with an emphasis on sales and cash budgets, along with a comparison of budgeted and actual profits, and the application of marginal costing for a new product line. The report concludes with an overall assessment of the company's financial performance and recommendations for improvement.

Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Classifying the cost................................................................................................................3

1.2 Computation of total cost.......................................................................................................4

1.3 Inventory costing methods.....................................................................................................5

1.4 Costing analysis.....................................................................................................................6

TASK 2............................................................................................................................................6

2.1 Cost of goods sold performance............................................................................................6

2.2 Performance indicators helpful in measuring performance of the company.........................7

2.3 Reduction in cost and managing the quality..........................................................................7

TASK 3............................................................................................................................................8

3.1 Budget and its significance....................................................................................................8

3.2 Methods for preparing budgets..............................................................................................9

3.3 Budget for the three months to 30 June...............................................................................11

Sales budget: It is an important for any business. Without budgeting company can't take record

of progress and or performance improvement. First step for company while creating while

budgeting is creating sales budget A sales budget estimates sales in unit as well as estimates

profit in each sale. Organization carefully analyses economic condition, marketing condition,

production capacity and selling expenses while preparing sales budget...................................11

3.4 Cash budget..........................................................................................................................13

TASK 4..........................................................................................................................................14

4.1 Marginal costing methods and price determination for new product line...........................14

4.2 Comparison of budgeted and actual profit for Smart Looks Ltd.........................................14

4.3 Budgetary report..................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

1

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

TASK 1............................................................................................................................................3

1.1 Classifying the cost................................................................................................................3

1.2 Computation of total cost.......................................................................................................4

1.3 Inventory costing methods.....................................................................................................5

1.4 Costing analysis.....................................................................................................................6

TASK 2............................................................................................................................................6

2.1 Cost of goods sold performance............................................................................................6

2.2 Performance indicators helpful in measuring performance of the company.........................7

2.3 Reduction in cost and managing the quality..........................................................................7

TASK 3............................................................................................................................................8

3.1 Budget and its significance....................................................................................................8

3.2 Methods for preparing budgets..............................................................................................9

3.3 Budget for the three months to 30 June...............................................................................11

Sales budget: It is an important for any business. Without budgeting company can't take record

of progress and or performance improvement. First step for company while creating while

budgeting is creating sales budget A sales budget estimates sales in unit as well as estimates

profit in each sale. Organization carefully analyses economic condition, marketing condition,

production capacity and selling expenses while preparing sales budget...................................11

3.4 Cash budget..........................................................................................................................13

TASK 4..........................................................................................................................................14

4.1 Marginal costing methods and price determination for new product line...........................14

4.2 Comparison of budgeted and actual profit for Smart Looks Ltd.........................................14

4.3 Budgetary report..................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

1

INTRODUCTION

Management accounting is multidisciplinary approach that is useful for managing all

business operations and enhancing efficiencies by using decision making tools. It is helpful to

improve quality services and preparing strategies to gain competitive advantages. The present

report is based on understanding different management accounting tools as costing and

budgeting for forecasting and decision making process for Smart Looks Ltd. It is clothing retailer

manufacturing company of UK that makes clothes for different retailers. In this regard, several

costing methods and budgeting for purchasing and selling goods are to be obtained. Along with

this, differences between actual and standard performance of organization is also to be

determined that is interrelated with productivity and profitability of organization.

TASK 1

1.1 Classifying the cost A

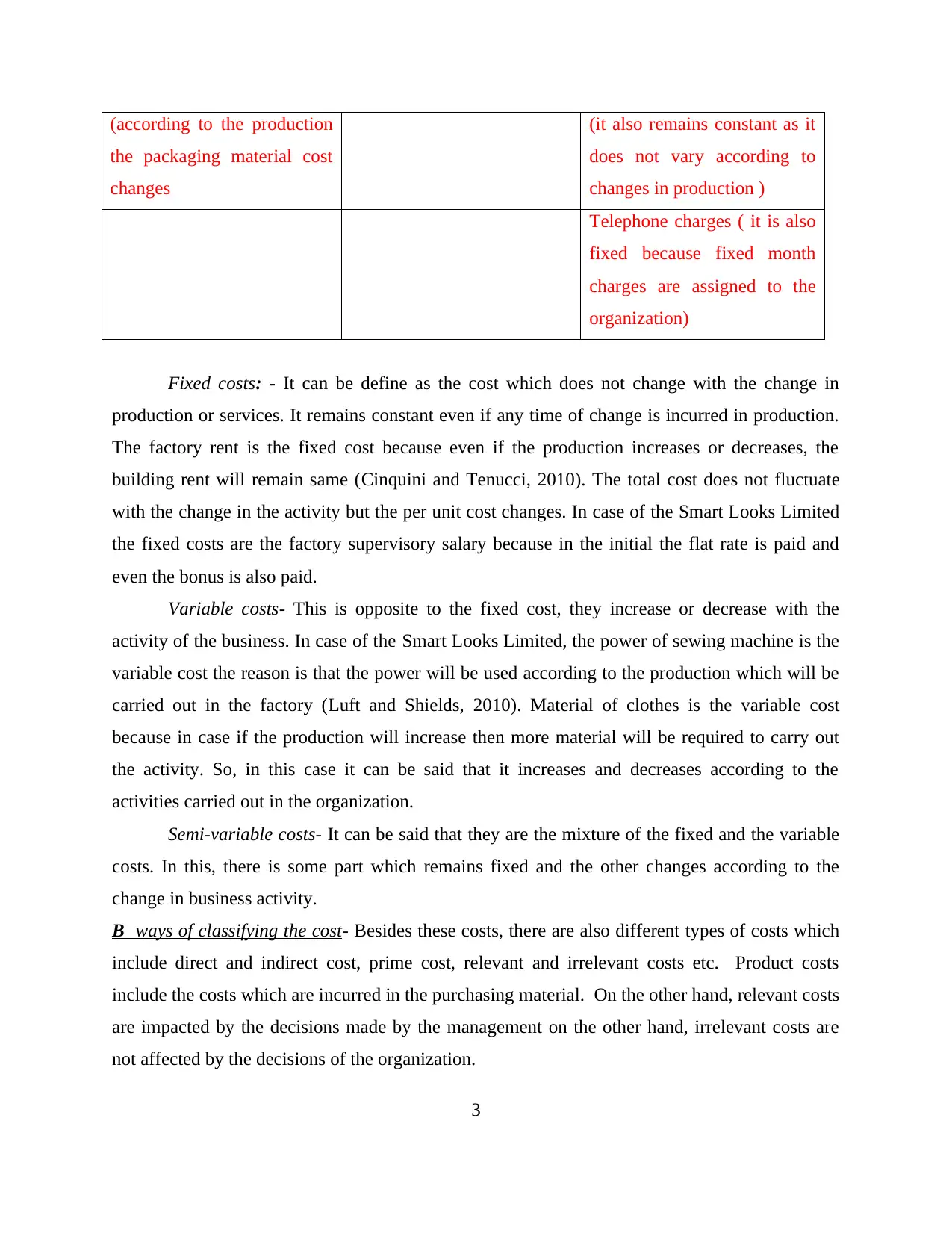

Cost can be defined as the value which is attached with anything. Further, the word cost

is used in many different contexts. Cost of the products and services are included by included

resources, time and the risk which is occurred in producing goods as well as services

(Weißenberger and Angelkort, 2011). Besides this, the nature of the cost is also different from

others which are the main basis for differentiation. Costs are of different types one is the fixed

cost, variable and the semi-variable costs.

Variable cost Semi-variable cost Fixed cost

Power for sewing machine

(power changes with the

production)

Deliver delivers pay

(sometimes it is fixed and if

the deliver is more than the

cost increases)

Factory rent

(according to the contract it is

fixed)

Material for clothes

(according to the increase or

decrease of demand and the

cost changes)

Factory heating

( it is fixed at one point of

time, but if the production

increases or decreases it

changes)

Factory supervisor wages

(according to the agreement it

is fixed)

Packaging material Office rates

2

Management accounting is multidisciplinary approach that is useful for managing all

business operations and enhancing efficiencies by using decision making tools. It is helpful to

improve quality services and preparing strategies to gain competitive advantages. The present

report is based on understanding different management accounting tools as costing and

budgeting for forecasting and decision making process for Smart Looks Ltd. It is clothing retailer

manufacturing company of UK that makes clothes for different retailers. In this regard, several

costing methods and budgeting for purchasing and selling goods are to be obtained. Along with

this, differences between actual and standard performance of organization is also to be

determined that is interrelated with productivity and profitability of organization.

TASK 1

1.1 Classifying the cost A

Cost can be defined as the value which is attached with anything. Further, the word cost

is used in many different contexts. Cost of the products and services are included by included

resources, time and the risk which is occurred in producing goods as well as services

(Weißenberger and Angelkort, 2011). Besides this, the nature of the cost is also different from

others which are the main basis for differentiation. Costs are of different types one is the fixed

cost, variable and the semi-variable costs.

Variable cost Semi-variable cost Fixed cost

Power for sewing machine

(power changes with the

production)

Deliver delivers pay

(sometimes it is fixed and if

the deliver is more than the

cost increases)

Factory rent

(according to the contract it is

fixed)

Material for clothes

(according to the increase or

decrease of demand and the

cost changes)

Factory heating

( it is fixed at one point of

time, but if the production

increases or decreases it

changes)

Factory supervisor wages

(according to the agreement it

is fixed)

Packaging material Office rates

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(according to the production

the packaging material cost

changes

(it also remains constant as it

does not vary according to

changes in production )

Telephone charges ( it is also

fixed because fixed month

charges are assigned to the

organization)

Fixed costs: - It can be define as the cost which does not change with the change in

production or services. It remains constant even if any time of change is incurred in production.

The factory rent is the fixed cost because even if the production increases or decreases, the

building rent will remain same (Cinquini and Tenucci, 2010). The total cost does not fluctuate

with the change in the activity but the per unit cost changes. In case of the Smart Looks Limited

the fixed costs are the factory supervisory salary because in the initial the flat rate is paid and

even the bonus is also paid.

Variable costs- This is opposite to the fixed cost, they increase or decrease with the

activity of the business. In case of the Smart Looks Limited, the power of sewing machine is the

variable cost the reason is that the power will be used according to the production which will be

carried out in the factory (Luft and Shields, 2010). Material of clothes is the variable cost

because in case if the production will increase then more material will be required to carry out

the activity. So, in this case it can be said that it increases and decreases according to the

activities carried out in the organization.

Semi-variable costs- It can be said that they are the mixture of the fixed and the variable

costs. In this, there is some part which remains fixed and the other changes according to the

change in business activity.

B ways of classifying the cost- Besides these costs, there are also different types of costs which

include direct and indirect cost, prime cost, relevant and irrelevant costs etc. Product costs

include the costs which are incurred in the purchasing material. On the other hand, relevant costs

are impacted by the decisions made by the management on the other hand, irrelevant costs are

not affected by the decisions of the organization.

3

the packaging material cost

changes

(it also remains constant as it

does not vary according to

changes in production )

Telephone charges ( it is also

fixed because fixed month

charges are assigned to the

organization)

Fixed costs: - It can be define as the cost which does not change with the change in

production or services. It remains constant even if any time of change is incurred in production.

The factory rent is the fixed cost because even if the production increases or decreases, the

building rent will remain same (Cinquini and Tenucci, 2010). The total cost does not fluctuate

with the change in the activity but the per unit cost changes. In case of the Smart Looks Limited

the fixed costs are the factory supervisory salary because in the initial the flat rate is paid and

even the bonus is also paid.

Variable costs- This is opposite to the fixed cost, they increase or decrease with the

activity of the business. In case of the Smart Looks Limited, the power of sewing machine is the

variable cost the reason is that the power will be used according to the production which will be

carried out in the factory (Luft and Shields, 2010). Material of clothes is the variable cost

because in case if the production will increase then more material will be required to carry out

the activity. So, in this case it can be said that it increases and decreases according to the

activities carried out in the organization.

Semi-variable costs- It can be said that they are the mixture of the fixed and the variable

costs. In this, there is some part which remains fixed and the other changes according to the

change in business activity.

B ways of classifying the cost- Besides these costs, there are also different types of costs which

include direct and indirect cost, prime cost, relevant and irrelevant costs etc. Product costs

include the costs which are incurred in the purchasing material. On the other hand, relevant costs

are impacted by the decisions made by the management on the other hand, irrelevant costs are

not affected by the decisions of the organization.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

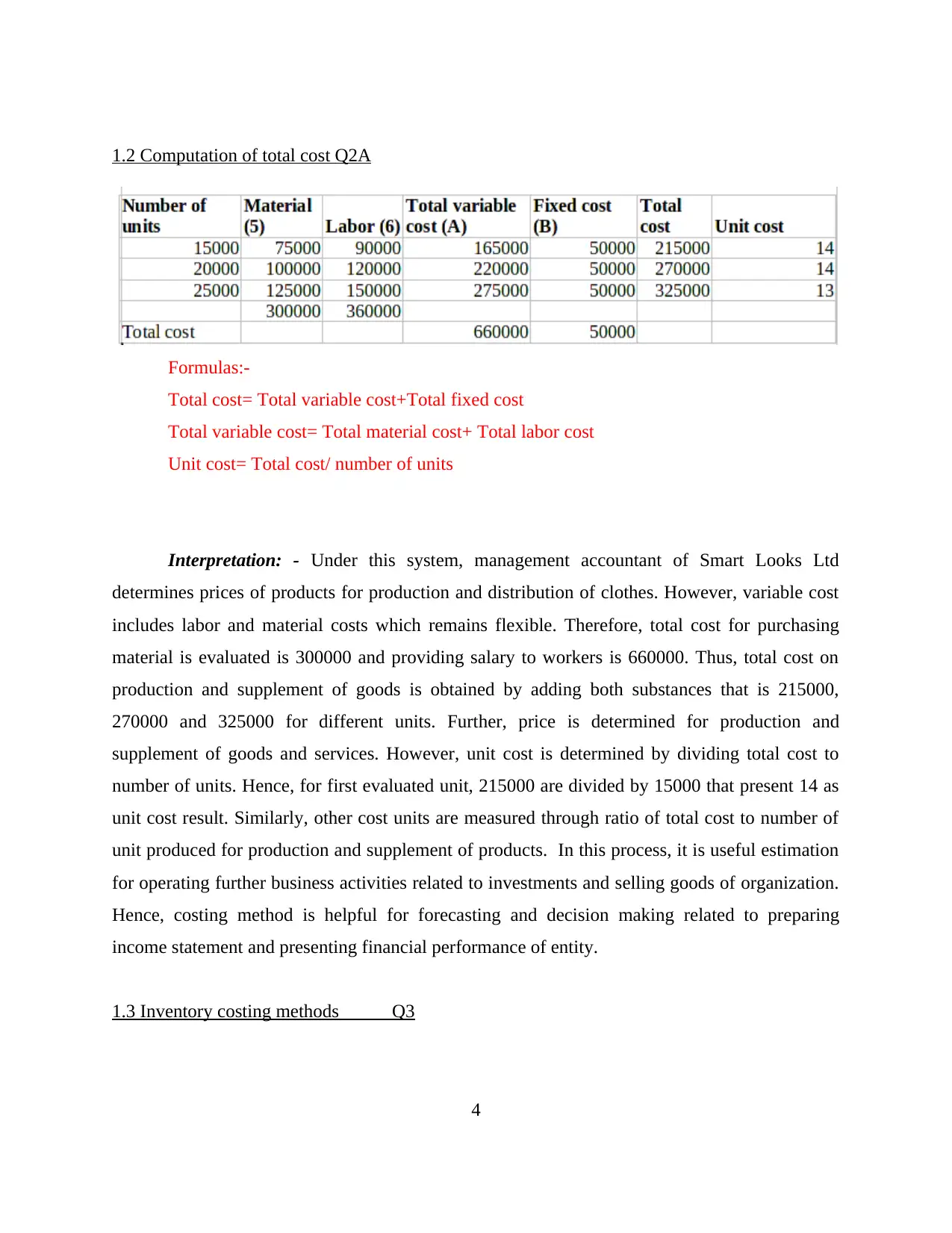

1.2 Computation of total cost Q2A

Formulas:-

Total cost= Total variable cost+Total fixed cost

Total variable cost= Total material cost+ Total labor cost

Unit cost= Total cost/ number of units

Interpretation: - Under this system, management accountant of Smart Looks Ltd

determines prices of products for production and distribution of clothes. However, variable cost

includes labor and material costs which remains flexible. Therefore, total cost for purchasing

material is evaluated is 300000 and providing salary to workers is 660000. Thus, total cost on

production and supplement of goods is obtained by adding both substances that is 215000,

270000 and 325000 for different units. Further, price is determined for production and

supplement of goods and services. However, unit cost is determined by dividing total cost to

number of units. Hence, for first evaluated unit, 215000 are divided by 15000 that present 14 as

unit cost result. Similarly, other cost units are measured through ratio of total cost to number of

unit produced for production and supplement of products. In this process, it is useful estimation

for operating further business activities related to investments and selling goods of organization.

Hence, costing method is helpful for forecasting and decision making related to preparing

income statement and presenting financial performance of entity.

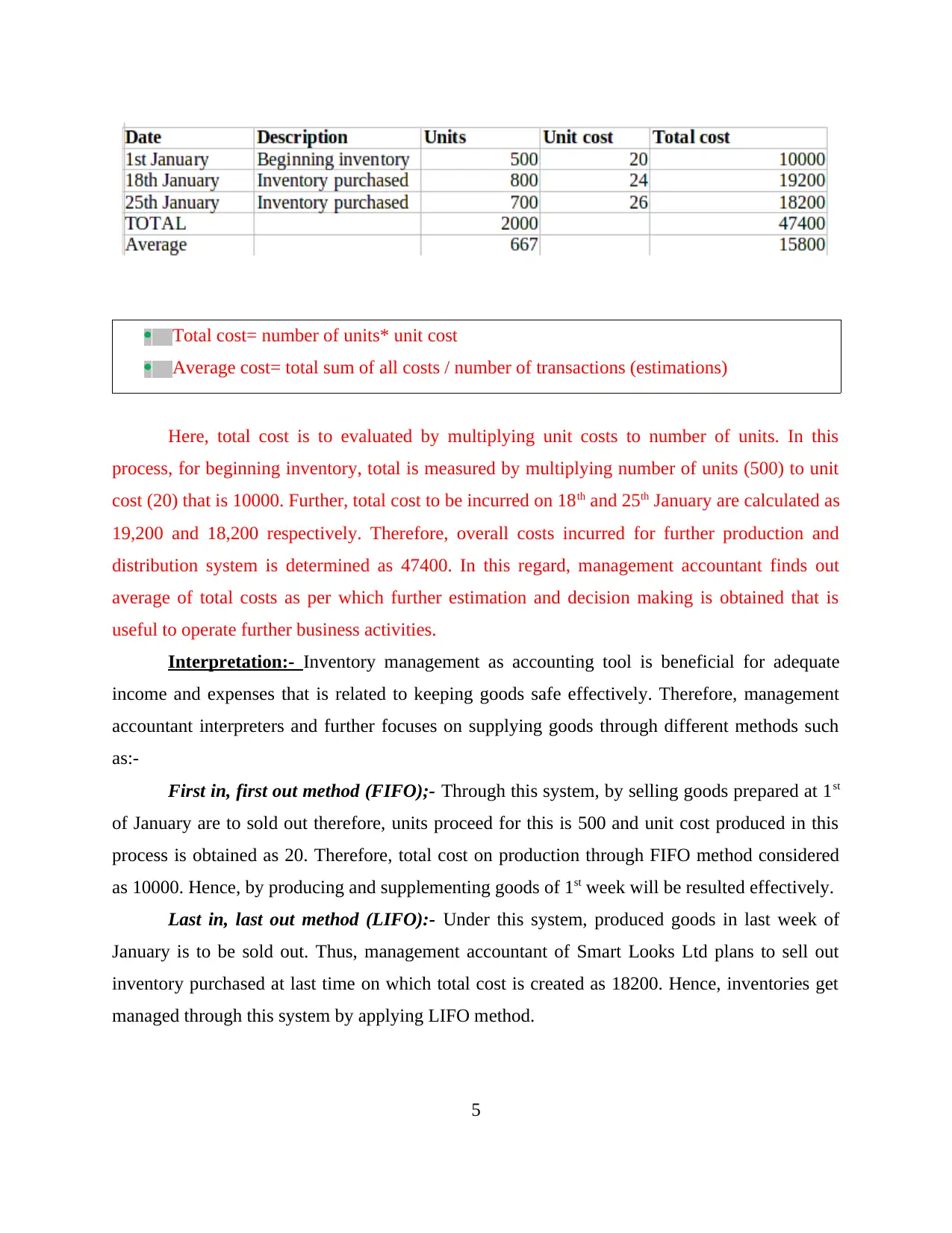

1.3 Inventory costing methods Q3

4

Formulas:-

Total cost= Total variable cost+Total fixed cost

Total variable cost= Total material cost+ Total labor cost

Unit cost= Total cost/ number of units

Interpretation: - Under this system, management accountant of Smart Looks Ltd

determines prices of products for production and distribution of clothes. However, variable cost

includes labor and material costs which remains flexible. Therefore, total cost for purchasing

material is evaluated is 300000 and providing salary to workers is 660000. Thus, total cost on

production and supplement of goods is obtained by adding both substances that is 215000,

270000 and 325000 for different units. Further, price is determined for production and

supplement of goods and services. However, unit cost is determined by dividing total cost to

number of units. Hence, for first evaluated unit, 215000 are divided by 15000 that present 14 as

unit cost result. Similarly, other cost units are measured through ratio of total cost to number of

unit produced for production and supplement of products. In this process, it is useful estimation

for operating further business activities related to investments and selling goods of organization.

Hence, costing method is helpful for forecasting and decision making related to preparing

income statement and presenting financial performance of entity.

1.3 Inventory costing methods Q3

4

Total cost= number of units* unit cost

Average cost= total sum of all costs / number of transactions (estimations)

Here, total cost is to evaluated by multiplying unit costs to number of units. In this

process, for beginning inventory, total is measured by multiplying number of units (500) to unit

cost (20) that is 10000. Further, total cost to be incurred on 18th and 25th January are calculated as

19,200 and 18,200 respectively. Therefore, overall costs incurred for further production and

distribution system is determined as 47400. In this regard, management accountant finds out

average of total costs as per which further estimation and decision making is obtained that is

useful to operate further business activities.

Interpretation:- Inventory management as accounting tool is beneficial for adequate

income and expenses that is related to keeping goods safe effectively. Therefore, management

accountant interpreters and further focuses on supplying goods through different methods such

as:-

First in, first out method (FIFO);- Through this system, by selling goods prepared at 1st

of January are to sold out therefore, units proceed for this is 500 and unit cost produced in this

process is obtained as 20. Therefore, total cost on production through FIFO method considered

as 10000. Hence, by producing and supplementing goods of 1st week will be resulted effectively.

Last in, last out method (LIFO):- Under this system, produced goods in last week of

January is to be sold out. Thus, management accountant of Smart Looks Ltd plans to sell out

inventory purchased at last time on which total cost is created as 18200. Hence, inventories get

managed through this system by applying LIFO method.

5

Average cost= total sum of all costs / number of transactions (estimations)

Here, total cost is to evaluated by multiplying unit costs to number of units. In this

process, for beginning inventory, total is measured by multiplying number of units (500) to unit

cost (20) that is 10000. Further, total cost to be incurred on 18th and 25th January are calculated as

19,200 and 18,200 respectively. Therefore, overall costs incurred for further production and

distribution system is determined as 47400. In this regard, management accountant finds out

average of total costs as per which further estimation and decision making is obtained that is

useful to operate further business activities.

Interpretation:- Inventory management as accounting tool is beneficial for adequate

income and expenses that is related to keeping goods safe effectively. Therefore, management

accountant interpreters and further focuses on supplying goods through different methods such

as:-

First in, first out method (FIFO);- Through this system, by selling goods prepared at 1st

of January are to sold out therefore, units proceed for this is 500 and unit cost produced in this

process is obtained as 20. Therefore, total cost on production through FIFO method considered

as 10000. Hence, by producing and supplementing goods of 1st week will be resulted effectively.

Last in, last out method (LIFO):- Under this system, produced goods in last week of

January is to be sold out. Thus, management accountant of Smart Looks Ltd plans to sell out

inventory purchased at last time on which total cost is created as 18200. Hence, inventories get

managed through this system by applying LIFO method.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Average cost method:- In this method, management accountant of Smart Looks Ltd

determines average as dividing sum total of costs to number of variables. In this process, total

cost on production and distribution system is considered as 47400. Thus, it is divided by 3 that

evaluate average of costs that is calculated as 15800. Hence, by using average cost method, it is

analyzed that through effective forecasting for production and distribution of goods can be

implemented that impacts on further business activities as well production and distribution of

goods.

Thus, by using above mentioned methods, different forecasting and decision making can

be done effectively that affects productivity and profit earning capacity. It is useful for

determining price of products and preparing income statement to present economic position of

organization at high level.

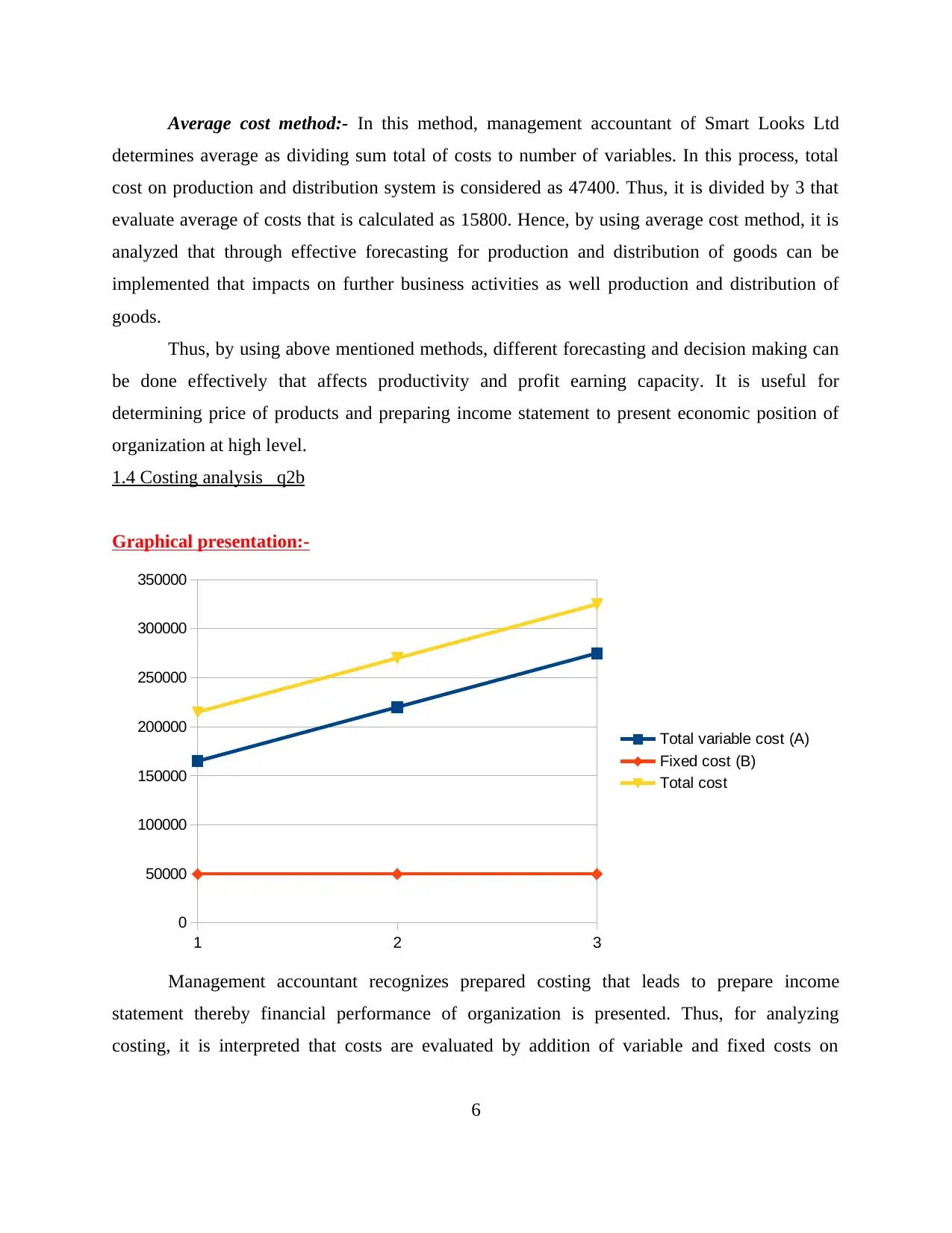

1.4 Costing analysis q2b

Graphical presentation:-

Management accountant recognizes prepared costing that leads to prepare income

statement thereby financial performance of organization is presented. Thus, for analyzing

costing, it is interpreted that costs are evaluated by addition of variable and fixed costs on

6

1 2 3

0

50000

100000

150000

200000

250000

300000

350000

Total variable cost (A)

Fixed cost (B)

Total cost

determines average as dividing sum total of costs to number of variables. In this process, total

cost on production and distribution system is considered as 47400. Thus, it is divided by 3 that

evaluate average of costs that is calculated as 15800. Hence, by using average cost method, it is

analyzed that through effective forecasting for production and distribution of goods can be

implemented that impacts on further business activities as well production and distribution of

goods.

Thus, by using above mentioned methods, different forecasting and decision making can

be done effectively that affects productivity and profit earning capacity. It is useful for

determining price of products and preparing income statement to present economic position of

organization at high level.

1.4 Costing analysis q2b

Graphical presentation:-

Management accountant recognizes prepared costing that leads to prepare income

statement thereby financial performance of organization is presented. Thus, for analyzing

costing, it is interpreted that costs are evaluated by addition of variable and fixed costs on

6

1 2 3

0

50000

100000

150000

200000

250000

300000

350000

Total variable cost (A)

Fixed cost (B)

Total cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

incurring expenditures to operate business activities. It is evaluated that material costs for each

unit are different such as 75000, 100000 and 125000. Similarly, costs incurred on labor are

considered as 90000, 120000 and 1500000. In respect to this, total material and labor costs are

obtained as 300000 and 360000 that are presented as variable costs which are flexible. For each

production and manufacturing process, these costs are different. On the other hand, fixed costs

are incurred as 50000 for each unit that presents that organization incurred fixed expenses on

some expenditure are termed as fixed costs. Further, total costs for each unit are created as

215000, 270000 and 325000. On the basis of this cost calculation, several ideas are created for

operating further business activities as production and supplement of Smart Looks Ltd products.

TASK 2

2.1 Cost of goods sold performance Q4

To

Board Of Director

Smart Looks Ltd

In this process, cost of goods sold are presented that is valuable for forecasting and

decision making related to production and distribution of goods. However, performance of cost

of goods sold is presented through this process that affects price determination and economic

position of Smart Looks Ltd. In addition to this, selling price is evaluated that is interrelated

with increasing business performance and making decisions for further implementation at high

level. Through this process system, management accountant recognizes all costs and prices for

further investments and incurring expenses. However, total costs incurred for producing goods

is measured as 47400 therefore, expansion and of organization and decision making can be

created at large scale. It impacts on productivity and profitability of firm. In addition to this,

cost of goods sold are determined as well forecast through different methods as first in, first out

(FIFO), LIFO and average method. It is helpful for decision making process and implementing

strategies for further business operations as well remains impacted for cost effectiveness.

Therefore, cost of goods sold performance evaluation is useful for planning procedure and

further decisions that affects productivity and profitability at high level. Including this,

management accountant of Smart Looks prepares this strategies and planning procedures to

7

unit are different such as 75000, 100000 and 125000. Similarly, costs incurred on labor are

considered as 90000, 120000 and 1500000. In respect to this, total material and labor costs are

obtained as 300000 and 360000 that are presented as variable costs which are flexible. For each

production and manufacturing process, these costs are different. On the other hand, fixed costs

are incurred as 50000 for each unit that presents that organization incurred fixed expenses on

some expenditure are termed as fixed costs. Further, total costs for each unit are created as

215000, 270000 and 325000. On the basis of this cost calculation, several ideas are created for

operating further business activities as production and supplement of Smart Looks Ltd products.

TASK 2

2.1 Cost of goods sold performance Q4

To

Board Of Director

Smart Looks Ltd

In this process, cost of goods sold are presented that is valuable for forecasting and

decision making related to production and distribution of goods. However, performance of cost

of goods sold is presented through this process that affects price determination and economic

position of Smart Looks Ltd. In addition to this, selling price is evaluated that is interrelated

with increasing business performance and making decisions for further implementation at high

level. Through this process system, management accountant recognizes all costs and prices for

further investments and incurring expenses. However, total costs incurred for producing goods

is measured as 47400 therefore, expansion and of organization and decision making can be

created at large scale. It impacts on productivity and profitability of firm. In addition to this,

cost of goods sold are determined as well forecast through different methods as first in, first out

(FIFO), LIFO and average method. It is helpful for decision making process and implementing

strategies for further business operations as well remains impacted for cost effectiveness.

Therefore, cost of goods sold performance evaluation is useful for planning procedure and

further decisions that affects productivity and profitability at high level. Including this,

management accountant of Smart Looks prepares this strategies and planning procedures to

7

operate business activities in future time.

2.2 Q5 A Performance indicators helpful in measuring performance of the company

There are several performance indicators of the organization which can help in deciding

the performance of the company. For gaining the customer experience, the Smart Looks Limited

is required to provide good quality product to the customers so that their customer experience

can be enhanced. Besides this, another factor is the services, through effective services; the

customer will gain huge experience (Vaivio and Sirén, 2010). The performance indicator is

basically the profitability of the Smart Looks Limited which can help in identifying the customer

good experience. For Supplier and product quality the two success factors are the materials

which are purchased from the suppliers. If the materials are good then the Smart Looks Limited

can provide quality products to the customers.

Further, the operational efficiency can be attained by determining the price determination

strategies. This will help in attaining the operational efficiency. The two critical success factor

for the cost reduction and profitability increase is the less expense incurred on the production

process (Giovannoni, Maraghini and Riccaboni, 2011). This will help in reducing the cost of the

product and due to this reason the profitability of the Smart Looks Limited can be increased. The

performance indicator which can be used for analyzing the profitability is the balance sheet as

through this they can effectively identify the profits which are earned by the organization (Vaivio

and Sirén, 2010). On the other hand, cash flow statements are also the performance indicator

which can aid in identifying the profitability of the firm. For reducing maintenance spending the

two critical success factors are the repeatedly carrying out the serving of the machines and

training the employees to use the machines. The key performance indicators which can be used

for measuring the performance are the less expense in the profit and loss sheet.

5A (1) Reduction in cost

There are several techniques which can be applied by the Smart Looks Limited to reduce

the cost of the production which is carried out in the Smart Looks Limited. The main techniques

are the target costing it basically helps to design the product and further estimated cost price is

determined which helps in reducing the cost of the product (DRURY, 2013). The other technique

is the kaizan cost which is the process that assists in reducing the cost at the time of

8

2.2 Q5 A Performance indicators helpful in measuring performance of the company

There are several performance indicators of the organization which can help in deciding

the performance of the company. For gaining the customer experience, the Smart Looks Limited

is required to provide good quality product to the customers so that their customer experience

can be enhanced. Besides this, another factor is the services, through effective services; the

customer will gain huge experience (Vaivio and Sirén, 2010). The performance indicator is

basically the profitability of the Smart Looks Limited which can help in identifying the customer

good experience. For Supplier and product quality the two success factors are the materials

which are purchased from the suppliers. If the materials are good then the Smart Looks Limited

can provide quality products to the customers.

Further, the operational efficiency can be attained by determining the price determination

strategies. This will help in attaining the operational efficiency. The two critical success factor

for the cost reduction and profitability increase is the less expense incurred on the production

process (Giovannoni, Maraghini and Riccaboni, 2011). This will help in reducing the cost of the

product and due to this reason the profitability of the Smart Looks Limited can be increased. The

performance indicator which can be used for analyzing the profitability is the balance sheet as

through this they can effectively identify the profits which are earned by the organization (Vaivio

and Sirén, 2010). On the other hand, cash flow statements are also the performance indicator

which can aid in identifying the profitability of the firm. For reducing maintenance spending the

two critical success factors are the repeatedly carrying out the serving of the machines and

training the employees to use the machines. The key performance indicators which can be used

for measuring the performance are the less expense in the profit and loss sheet.

5A (1) Reduction in cost

There are several techniques which can be applied by the Smart Looks Limited to reduce

the cost of the production which is carried out in the Smart Looks Limited. The main techniques

are the target costing it basically helps to design the product and further estimated cost price is

determined which helps in reducing the cost of the product (DRURY, 2013). The other technique

is the kaizan cost which is the process that assists in reducing the cost at the time of

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manufacturing phrase. In this, the slow and gradual improvement is carried out so that they can

improve the performance of the manufacturing process. The cost can be reduced by focusing on

the material, labor, and overhead. In case of the outdated machinery, the cost of the product

increases which further increases the cost of the product. Due to this reason, to reduce the cost of

the product, proper machinery needs to be installed. Overhead can be considered as the

additional cost. With the use less material, the cost of the production can be reduced. Factors of

production has huge role in reducing the cost of the product. With the help of the new

machinery, the time will be consumed less so the cost will also be less. On the other hand, if the

labor rates are low they also it will directly affects the cost of production. So if this adopted in

the organization then the cost can be reduced.

5B (ii) Managing the quality

For increasing the quality of the products, Smart Looks Limited can use the total quality

management in which the process is involved in continuous improvement which aids the

organization in improving the quality of the product. On the other hand, business process re-

engineering is the process which redesigns the process for achieving the goals and objectives of

the organization. This is the whole process that focuses on reducing the costs as well as

improving the quality of the products (Pitkänen and Lukka, 2011). It has been witnessed that

through reducing the cost of the products it has been witnessed that the quality is not maintained

by the organization; due to this reason the quality degrades which affects the satisfaction of the

customers. But in the case of business process re-engineering it focuses on increasing the quality

and reducing the cost. Besides this, there are further tools and techniques which can be applied in

the Smart Looks Limited for improving the quality and reducing the cost in the organization

(Cinquini, and Tenucci, 2010). Further, it is important to enhance the quality because the

organization can gain customer satisfaction and experience when they are provided with good

quality products.

9

improve the performance of the manufacturing process. The cost can be reduced by focusing on

the material, labor, and overhead. In case of the outdated machinery, the cost of the product

increases which further increases the cost of the product. Due to this reason, to reduce the cost of

the product, proper machinery needs to be installed. Overhead can be considered as the

additional cost. With the use less material, the cost of the production can be reduced. Factors of

production has huge role in reducing the cost of the product. With the help of the new

machinery, the time will be consumed less so the cost will also be less. On the other hand, if the

labor rates are low they also it will directly affects the cost of production. So if this adopted in

the organization then the cost can be reduced.

5B (ii) Managing the quality

For increasing the quality of the products, Smart Looks Limited can use the total quality

management in which the process is involved in continuous improvement which aids the

organization in improving the quality of the product. On the other hand, business process re-

engineering is the process which redesigns the process for achieving the goals and objectives of

the organization. This is the whole process that focuses on reducing the costs as well as

improving the quality of the products (Pitkänen and Lukka, 2011). It has been witnessed that

through reducing the cost of the products it has been witnessed that the quality is not maintained

by the organization; due to this reason the quality degrades which affects the satisfaction of the

customers. But in the case of business process re-engineering it focuses on increasing the quality

and reducing the cost. Besides this, there are further tools and techniques which can be applied in

the Smart Looks Limited for improving the quality and reducing the cost in the organization

(Cinquini, and Tenucci, 2010). Further, it is important to enhance the quality because the

organization can gain customer satisfaction and experience when they are provided with good

quality products.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

3.1 Budget and its significance Q6 A

In order to do forecasting for the business operations that will be performed in the future

and to take decisions accordingly, making budget is the most appropriate approach. With the

help of this, present business performance in an actual manner is shown. Along with that, it also

tells about the different factors of organization like profit the firm is earning, its productivity,

customer dealing services and working culture of the firm. Under this system, it is the

responsibility of management accountant of Smart Looks Ltd. to make the budget prepared by

assessing the structure of organization in relation with various activities (Quattrone, 2016).

However, there are many ideas are through which productivity of company can be effectually

increased as well as higher profits can be gained. In addition to this, it will also help the

organization to expand at a large scale and gain various benefits out of the same. It can be said

that budget plays a significant role in creating balance between production and supplement of

goods. Further, budget proves to be highly effectual in maintaining the level of required

resources along with the fund that are needed to be attained to meet the objectives. Hence,

budget can be referred as a technique that helps in making prediction and decision making by

which the set targets can be attained within stipulated time period in a systematic manner

(Zimmerman and Yahya-Zadeh, 2011). Moreover, budget proves to be very helpful in

formulating business, competitive and marketing strategies of entity.

Preparing budget is highly essential for the organization and its importance can be

understood in a way that to assess the present and actual performance that business is rendering,

it plays a significant role. Along with that, it can be said that by the help of preparing budget,

Smart Looks Ltd. would be able to make optimum utilization of resources and funds invested.

Through this, company will gain higher profits in the market at reasonable cost as well as its

productivity would also get increased to a high extent in an efficient manner. Budget plays a

crucial role in maintaining proper balance between incurred expenses and gained revenue. Also,

it can be said that budget proves to be highly helpful in formulating the business and competitive

strategies with the help of which Smart Looks Ltd (DRURY, 2013). would gain a competitive

edge over others and stay in the market for longer span of time. Therefore, with all these, a

positive and healthy working environment will be created in the firm by which employees will

10

3.1 Budget and its significance Q6 A

In order to do forecasting for the business operations that will be performed in the future

and to take decisions accordingly, making budget is the most appropriate approach. With the

help of this, present business performance in an actual manner is shown. Along with that, it also

tells about the different factors of organization like profit the firm is earning, its productivity,

customer dealing services and working culture of the firm. Under this system, it is the

responsibility of management accountant of Smart Looks Ltd. to make the budget prepared by

assessing the structure of organization in relation with various activities (Quattrone, 2016).

However, there are many ideas are through which productivity of company can be effectually

increased as well as higher profits can be gained. In addition to this, it will also help the

organization to expand at a large scale and gain various benefits out of the same. It can be said

that budget plays a significant role in creating balance between production and supplement of

goods. Further, budget proves to be highly effectual in maintaining the level of required

resources along with the fund that are needed to be attained to meet the objectives. Hence,

budget can be referred as a technique that helps in making prediction and decision making by

which the set targets can be attained within stipulated time period in a systematic manner

(Zimmerman and Yahya-Zadeh, 2011). Moreover, budget proves to be very helpful in

formulating business, competitive and marketing strategies of entity.

Preparing budget is highly essential for the organization and its importance can be

understood in a way that to assess the present and actual performance that business is rendering,

it plays a significant role. Along with that, it can be said that by the help of preparing budget,

Smart Looks Ltd. would be able to make optimum utilization of resources and funds invested.

Through this, company will gain higher profits in the market at reasonable cost as well as its

productivity would also get increased to a high extent in an efficient manner. Budget plays a

crucial role in maintaining proper balance between incurred expenses and gained revenue. Also,

it can be said that budget proves to be highly helpful in formulating the business and competitive

strategies with the help of which Smart Looks Ltd (DRURY, 2013). would gain a competitive

edge over others and stay in the market for longer span of time. Therefore, with all these, a

positive and healthy working environment will be created in the firm by which employees will

10

render effective services and thus, maximum level of customer satisfaction would be attained. It

can be said that in order to manage the overall business operations by setting a particular budget,

employees would perform in a systematic and coordinated manner.

Therefore, on the basis of analyzing actual business performance through preparing

budget, company will come in position to generate different ideas for the purpose of operating

different business activities. Level of production and balance of distribution of goods, income

and expenditure made by business as well as rise in productivity and profits are some of the

factors that get directly affected by the budget that organization prepares for a year (Christ and

et.al., 2017). In addition to this, elements like demand for products and proper allocation of

resources as well as fund can be effectually done by Smart Looks Ltd. with the help of preparing

budget. Therefore, it can be said that with the help of setting budget in company, quality of

products and services can be improved as according to the same, operations will take place.

Q6 B.

There are a lot of purposes of preparing budgets for Smart Looks Ltd. among which the

major one is that the budgets play a significant role in setting the short term targets as well as

achieving the same within stipulated time period. Along with that, these budgets prove to be

highly helpful for monitoring the business performance. It is because; as per the budget set,

company reviews the performance time to time so as to assess that whether functions are being

carried out as per the decided budget or not (Bhimani and et.al., 2013). In case if the process is

not going as per the decided budget, corrective actions are taken on immediate basis. Apart from

that, there is one more purpose behind preparing the budget, that is, to have control on the

operations as well as on use of resources. In addition to this, these budgets help in keeping the

workforce and management motivated to attain the specified targets on time and thus, level of

their performance gets improved. It can be said that in Smart Looks Ltd., budgets will help in

monitoring the relationship between costs and revenues as well. Thus, company would come in

position to earn higher revenues at low cost by making effective utilization of the resources due

to having a limited budget (Christ and et.al., 2017). Last but not the least; budgets fulfill an

important purpose, that is, it helps in leading communication with the senior management which

creates a healthy working environment in the firm.

11

can be said that in order to manage the overall business operations by setting a particular budget,

employees would perform in a systematic and coordinated manner.

Therefore, on the basis of analyzing actual business performance through preparing

budget, company will come in position to generate different ideas for the purpose of operating

different business activities. Level of production and balance of distribution of goods, income

and expenditure made by business as well as rise in productivity and profits are some of the

factors that get directly affected by the budget that organization prepares for a year (Christ and

et.al., 2017). In addition to this, elements like demand for products and proper allocation of

resources as well as fund can be effectually done by Smart Looks Ltd. with the help of preparing

budget. Therefore, it can be said that with the help of setting budget in company, quality of

products and services can be improved as according to the same, operations will take place.

Q6 B.

There are a lot of purposes of preparing budgets for Smart Looks Ltd. among which the

major one is that the budgets play a significant role in setting the short term targets as well as

achieving the same within stipulated time period. Along with that, these budgets prove to be

highly helpful for monitoring the business performance. It is because; as per the budget set,

company reviews the performance time to time so as to assess that whether functions are being

carried out as per the decided budget or not (Bhimani and et.al., 2013). In case if the process is

not going as per the decided budget, corrective actions are taken on immediate basis. Apart from

that, there is one more purpose behind preparing the budget, that is, to have control on the

operations as well as on use of resources. In addition to this, these budgets help in keeping the

workforce and management motivated to attain the specified targets on time and thus, level of

their performance gets improved. It can be said that in Smart Looks Ltd., budgets will help in

monitoring the relationship between costs and revenues as well. Thus, company would come in

position to earn higher revenues at low cost by making effective utilization of the resources due

to having a limited budget (Christ and et.al., 2017). Last but not the least; budgets fulfill an

important purpose, that is, it helps in leading communication with the senior management which

creates a healthy working environment in the firm.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.