Financial Resources Management: Smart Resort Ltd. Case Analysis

VerifiedAdded on 2023/06/16

|13

|3050

|161

Report

AI Summary

This report provides an analysis of financial resource management within the hospitality industry, focusing on the application of Generally Accepted Accounting Principles (GAAP) and the interpretation of financial statements. It identifies key users of financial statements, such as investors, governments, employees, management, competitors, and customers, highlighting their specific interests. The report discusses the significance of income statements, balance sheets, and cash flow statements for loan and trade creditors in assessing a company's financial health. It also examines the components of financial statements in annual reports, including balance sheets, income statements, statements of changes in equity, and cash flow statements, emphasizing the concept of financial reporting and its importance for external stakeholders. Furthermore, the report includes a financial analysis of Smart Resort Ltd., calculating and interpreting various financial ratios to evaluate the company's performance. The analysis covers net profit margin, return on equity, return on assets, current ratio, quick ratio, debt-to-equity ratio, times interest earned ratio, inventory turnover ratio, and accounts receivable turnover ratio, providing insights into the company's profitability, liquidity, and solvency. The report concludes with an overall assessment of Smart Resort Ltd.'s financial performance based on the calculated ratios and trends.

Managing Financial Resources in the

Hospitality Industry

Hospitality Industry

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Generally accepted accounting principle.....................................................................................1

Discussing about the statements of income, financial position and cash flows and which of

them is most interest to loan creditor and trade creditor..............................................................2

Components in the financial statements in annual report and concept of financial reporting. ...3

Interpreting financial statements of Smart resort ltd....................................................................5

CONCLUSION................................................................................................................................7

REFERENCE...................................................................................................................................8

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Generally accepted accounting principle.....................................................................................1

Discussing about the statements of income, financial position and cash flows and which of

them is most interest to loan creditor and trade creditor..............................................................2

Components in the financial statements in annual report and concept of financial reporting. ...3

Interpreting financial statements of Smart resort ltd....................................................................5

CONCLUSION................................................................................................................................7

REFERENCE...................................................................................................................................8

INTRODUCTION

Managing financial resources is important thing which every organisation should have done

properly. If company will manage its financial resources properly than they can easily achieve

their objectives. This report will discuss about accounting principles and also will identify users

of financial statement. Further it will evaluate loan creditor and trade creditor needs for financial

statement. It will also discuss financial statement components in the annual report and also

financial ratios.

MAIN BODY

Generally accepted accounting principle

GAAP or the accounting principles are the set of rules and standards of the financial reports or

statements. The purpose of this principle is to make sure that financial reports and statements are

transparent and it also helps in maintaining consistency from one company to other. Although

gaap provides transparency and its the principle but they does not take guarantee that the

financial statements of the company is free from omissions or mistakes which can even mislead

their investors (Plaskova and et.al., 2020). GAAP is not the government regulated function but it

came into existence because of the mixed efforts of the business. There are components in

GAAP which helps in consistent accounting so that investors can evaluate the financial position

of the company.

Users of financial statements-

investors: they require financial statements in order to take their investment related decisions. As

they will become business owners so that is why they needed financial statements.

Governments: they are interested in financial statements in order to check that the organisation

has paid the tax which is expected from them or not.

Employees: company provide information of financial reports to their employees and also

explain its elements. Employees are interested in the reports because this report will give them

information about company's profitability and if company will make good profit than salary of

employees will also increase.

Management: financial reports are required by the management of the company because

company wanted to know about the profitability and calculate cash flow of every month

1

Managing financial resources is important thing which every organisation should have done

properly. If company will manage its financial resources properly than they can easily achieve

their objectives. This report will discuss about accounting principles and also will identify users

of financial statement. Further it will evaluate loan creditor and trade creditor needs for financial

statement. It will also discuss financial statement components in the annual report and also

financial ratios.

MAIN BODY

Generally accepted accounting principle

GAAP or the accounting principles are the set of rules and standards of the financial reports or

statements. The purpose of this principle is to make sure that financial reports and statements are

transparent and it also helps in maintaining consistency from one company to other. Although

gaap provides transparency and its the principle but they does not take guarantee that the

financial statements of the company is free from omissions or mistakes which can even mislead

their investors (Plaskova and et.al., 2020). GAAP is not the government regulated function but it

came into existence because of the mixed efforts of the business. There are components in

GAAP which helps in consistent accounting so that investors can evaluate the financial position

of the company.

Users of financial statements-

investors: they require financial statements in order to take their investment related decisions. As

they will become business owners so that is why they needed financial statements.

Governments: they are interested in financial statements in order to check that the organisation

has paid the tax which is expected from them or not.

Employees: company provide information of financial reports to their employees and also

explain its elements. Employees are interested in the reports because this report will give them

information about company's profitability and if company will make good profit than salary of

employees will also increase.

Management: financial reports are required by the management of the company because

company wanted to know about the profitability and calculate cash flow of every month

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(SOLOMON and NWAFOR, 2018). Company takes financial decisions by using the financial

statements.

Competitors: competitors are interested in the financial statements of company in order to know

their competitive strategy. If competitor wanted to attain competitive advantage than it is

important to know their competitive strategy.

Customers: for the customer it is important to access that from which company they need to

purchase. They check financial reports of the company in order to find out their financial ability

so that they can decide that they want to be with with for longer time or not.

Financial accounting records, reports and summarize the financial transactions which is used by

the management of the company for making various decisions. Financial statements which

consists of income statements, balance sheet etc. helps company in determining its financial

position and liquidity (Azami, 2018). For taking important decisions financial reports or

statements are required because by determining those statements only important decision can

take place. As financial statements consists of important information which require every

organisation in order to take decisions or making various strategies.

Discussing about the statements of income, financial position and cash flows and which of them

is most interest to loan creditor and trade creditor.

With the help of financial statements creditors can get knowledge about the financial health of

the company. Financial statements provides various information like income, profit, debt

obligations, expenses etc. creditors use the financial statements of the company to check that

business have the capabilities to pay debt or not. If any business reaches to the financial

institution for loan than it is important to provide financial statements to their creditor (Wei,

2018). Financial institution or loan creditor will analyse or study financial statements carefully

before they grant loan to the company.

Three statements which are used by loan creditor and trade creditor are as follows:

Income statement-

income statement is the first thing which is considered by the trade creditor or loan creditor.

Before granting any loan to the company, loan creditor checks the income statement of the

company. With the help of income statement, creditors can check the business performance of

the company with the time period. As the element which is there at the top of income statement

is important and it is considered before granting loan. With the help of this statement, gross

2

statements.

Competitors: competitors are interested in the financial statements of company in order to know

their competitive strategy. If competitor wanted to attain competitive advantage than it is

important to know their competitive strategy.

Customers: for the customer it is important to access that from which company they need to

purchase. They check financial reports of the company in order to find out their financial ability

so that they can decide that they want to be with with for longer time or not.

Financial accounting records, reports and summarize the financial transactions which is used by

the management of the company for making various decisions. Financial statements which

consists of income statements, balance sheet etc. helps company in determining its financial

position and liquidity (Azami, 2018). For taking important decisions financial reports or

statements are required because by determining those statements only important decision can

take place. As financial statements consists of important information which require every

organisation in order to take decisions or making various strategies.

Discussing about the statements of income, financial position and cash flows and which of them

is most interest to loan creditor and trade creditor.

With the help of financial statements creditors can get knowledge about the financial health of

the company. Financial statements provides various information like income, profit, debt

obligations, expenses etc. creditors use the financial statements of the company to check that

business have the capabilities to pay debt or not. If any business reaches to the financial

institution for loan than it is important to provide financial statements to their creditor (Wei,

2018). Financial institution or loan creditor will analyse or study financial statements carefully

before they grant loan to the company.

Three statements which are used by loan creditor and trade creditor are as follows:

Income statement-

income statement is the first thing which is considered by the trade creditor or loan creditor.

Before granting any loan to the company, loan creditor checks the income statement of the

company. With the help of income statement, creditors can check the business performance of

the company with the time period. As the element which is there at the top of income statement

is important and it is considered before granting loan. With the help of this statement, gross

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit can be easily calculated by deducting cost of goods sold. With the help of income

statement, lenders comes to know about the revenues and expenses of company.

Balance sheet-

balance sheet shows the assets and liabilities of the business. It is the common saying that the

assets and liabilities of the business should have equal. At the asset side of the balance sheet

cash balance can be seen. There can be also seen adjustments in the balance sheet which can

help trade creditors or loan creditors in making various decisions. Net income can be also seen

in the balance sheet which is flow within the income statement (Сосновська and Житар, 2018).

With the help of balance sheet investor or creditor can determine that they should have invest in

the business or not. As balance sheet draws the clear picture of the company in front of trade

creditors and loan creditors. Balance sheet is made with three sections which are assets,

liabilities and shareholders equity.

Cash flow statement-

this statement is also used by the company which shows cash related adjustments. Basically this

statement shows the changes in the cash within the period. It will also shows the ending and the

beginning balance of the cash. By seeing the cash flow statement also trade creditors can decide

that they should give or lend money to the business or not. As it will show changes in cash in

terms of increase or decrease in the cash.

Components in the financial statements in annual report and concept of financial reporting.

Financial statements-

financial statements are the formal reports which shows all the financial activities and also the

financial position of the business (Components of Financial Statements., 2020). The components

which comes under financial statements are balance sheet, income statement, cash flow

statement and statement of changes in equity.

Balance sheet-

it is the financial statement which is used to see the financial position of the company. It exactly

shows company's financial position. On the one side it shows assets of the business and on the

other side it shows liabilities of the business. In short balance sheet is used to check the amount

of money business is actually holding. Balance sheet have three elements which are assets,

owners equity and liabilities (van Der Graaf, 2018). Asset side include current and fixed assets

3

statement, lenders comes to know about the revenues and expenses of company.

Balance sheet-

balance sheet shows the assets and liabilities of the business. It is the common saying that the

assets and liabilities of the business should have equal. At the asset side of the balance sheet

cash balance can be seen. There can be also seen adjustments in the balance sheet which can

help trade creditors or loan creditors in making various decisions. Net income can be also seen

in the balance sheet which is flow within the income statement (Сосновська and Житар, 2018).

With the help of balance sheet investor or creditor can determine that they should have invest in

the business or not. As balance sheet draws the clear picture of the company in front of trade

creditors and loan creditors. Balance sheet is made with three sections which are assets,

liabilities and shareholders equity.

Cash flow statement-

this statement is also used by the company which shows cash related adjustments. Basically this

statement shows the changes in the cash within the period. It will also shows the ending and the

beginning balance of the cash. By seeing the cash flow statement also trade creditors can decide

that they should give or lend money to the business or not. As it will show changes in cash in

terms of increase or decrease in the cash.

Components in the financial statements in annual report and concept of financial reporting.

Financial statements-

financial statements are the formal reports which shows all the financial activities and also the

financial position of the business (Components of Financial Statements., 2020). The components

which comes under financial statements are balance sheet, income statement, cash flow

statement and statement of changes in equity.

Balance sheet-

it is the financial statement which is used to see the financial position of the company. It exactly

shows company's financial position. On the one side it shows assets of the business and on the

other side it shows liabilities of the business. In short balance sheet is used to check the amount

of money business is actually holding. Balance sheet have three elements which are assets,

owners equity and liabilities (van Der Graaf, 2018). Asset side include current and fixed assets

3

of the company which are plant and machinery, buildings etc. and liability side involves non

current liability and current liability, which is trade payables, creditors etc.

income statement-

this statement represents the financial performance of the company. By reviewing this report and

individual can come to know about the financial performance of any company. It includes

revenue and expenses. It also comprises of the losses or gains of the business. More revenue

over the expense is the profit condition for the business and if the expenses are more than the

revenue will show the loss of the business.

Statements of changes in equity-

this is one of the important financial statement which represents the changes in the equity

shareholders investment in the company. It further shows any changes in the reserves and capital

equitable to the equity holders of the business over the time period. So it is important to adjust

the increase or decrease of the year (Sova and et.al., 2021). This statement represents the

transaction of the shareholders which involves retained earnings, paid in capital and capital

stock. This statement also states changes in equity, reserves and share capital.

Cash flow statement-

this statement represents any changes in the financial position of the company by viewing the

changes in cash of the company. The main objective of preparing the cash flow statement is that

to give supplement to the financial position and income statement as these two statements do not

provide sufficient information in regards of the cash balance. Shareholders gets help from cash

flow statement n order to understand cash utilization and cash sources. Cash flow have three

major sections which are cash flow from operating activities, cash flow from investing activities

and the cash flow from finance. Cash flow operating activities begins with the operating profit

and do reconsilation of operating profits. Whereas investing activities comprises of purchase of

long term assets and also the sale of long term assets. It further involves the information which is

related to the investments. Cash flow from finance shows changes in the equity capital. It also

contain dividends of shareholders (Sukharev, 2019). Investors view this statement before taking

their investment decisions.

Financial reporting-

financial reports gives the financial results of the company which are released by the company

for the public and stakeholders. Financial reporting consists of the components which are cash

4

current liability and current liability, which is trade payables, creditors etc.

income statement-

this statement represents the financial performance of the company. By reviewing this report and

individual can come to know about the financial performance of any company. It includes

revenue and expenses. It also comprises of the losses or gains of the business. More revenue

over the expense is the profit condition for the business and if the expenses are more than the

revenue will show the loss of the business.

Statements of changes in equity-

this is one of the important financial statement which represents the changes in the equity

shareholders investment in the company. It further shows any changes in the reserves and capital

equitable to the equity holders of the business over the time period. So it is important to adjust

the increase or decrease of the year (Sova and et.al., 2021). This statement represents the

transaction of the shareholders which involves retained earnings, paid in capital and capital

stock. This statement also states changes in equity, reserves and share capital.

Cash flow statement-

this statement represents any changes in the financial position of the company by viewing the

changes in cash of the company. The main objective of preparing the cash flow statement is that

to give supplement to the financial position and income statement as these two statements do not

provide sufficient information in regards of the cash balance. Shareholders gets help from cash

flow statement n order to understand cash utilization and cash sources. Cash flow have three

major sections which are cash flow from operating activities, cash flow from investing activities

and the cash flow from finance. Cash flow operating activities begins with the operating profit

and do reconsilation of operating profits. Whereas investing activities comprises of purchase of

long term assets and also the sale of long term assets. It further involves the information which is

related to the investments. Cash flow from finance shows changes in the equity capital. It also

contain dividends of shareholders (Sukharev, 2019). Investors view this statement before taking

their investment decisions.

Financial reporting-

financial reports gives the financial results of the company which are released by the company

for the public and stakeholders. Financial reporting consists of the components which are cash

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

flows, income statements and balance sheet. It is the annual reports which is released by the

company so tat their external users can use it.

In simple language financial reporting is the system when enterprise communicate the financial

information to the external users which includes public, government, consumers, investors etc.

this information is important to communicate to the external or internal users so that they can

decide that they want to invest in the company or not. While creditors can also decide by

reviewing the statements that they want to lend money to the business or not (Borisova,

Samoshkina, Rybina and Shumkova, 2020).

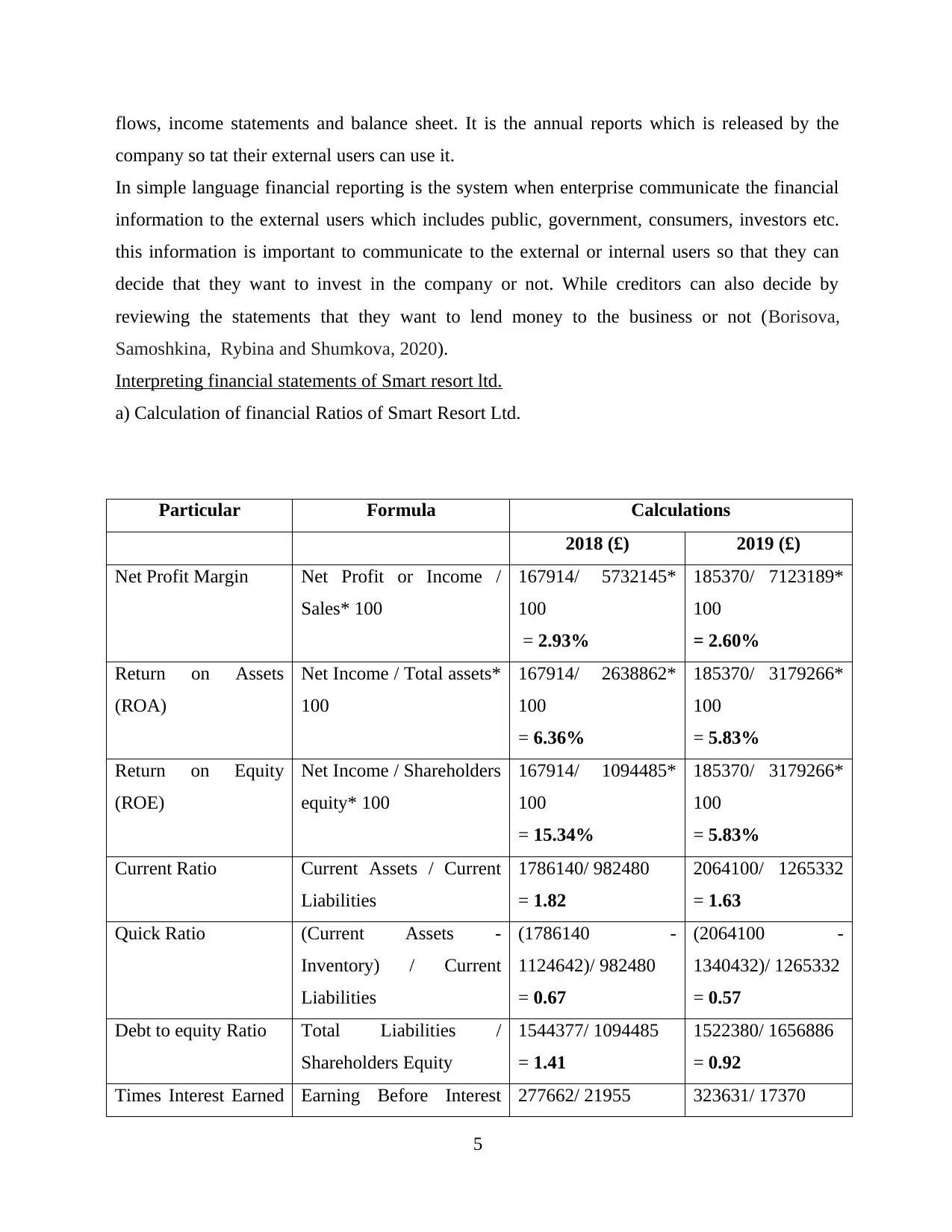

Interpreting financial statements of Smart resort ltd.

a) Calculation of financial Ratios of Smart Resort Ltd.

Particular Formula Calculations

2018 (£) 2019 (£)

Net Profit Margin Net Profit or Income /

Sales* 100

167914/ 5732145*

100

= 2.93%

185370/ 7123189*

100

= 2.60%

Return on Assets

(ROA)

Net Income / Total assets*

100

167914/ 2638862*

100

= 6.36%

185370/ 3179266*

100

= 5.83%

Return on Equity

(ROE)

Net Income / Shareholders

equity* 100

167914/ 1094485*

100

= 15.34%

185370/ 3179266*

100

= 5.83%

Current Ratio Current Assets / Current

Liabilities

1786140/ 982480

= 1.82

2064100/ 1265332

= 1.63

Quick Ratio (Current Assets -

Inventory) / Current

Liabilities

(1786140 -

1124642)/ 982480

= 0.67

(2064100 -

1340432)/ 1265332

= 0.57

Debt to equity Ratio Total Liabilities /

Shareholders Equity

1544377/ 1094485

= 1.41

1522380/ 1656886

= 0.92

Times Interest Earned Earning Before Interest 277662/ 21955 323631/ 17370

5

company so tat their external users can use it.

In simple language financial reporting is the system when enterprise communicate the financial

information to the external users which includes public, government, consumers, investors etc.

this information is important to communicate to the external or internal users so that they can

decide that they want to invest in the company or not. While creditors can also decide by

reviewing the statements that they want to lend money to the business or not (Borisova,

Samoshkina, Rybina and Shumkova, 2020).

Interpreting financial statements of Smart resort ltd.

a) Calculation of financial Ratios of Smart Resort Ltd.

Particular Formula Calculations

2018 (£) 2019 (£)

Net Profit Margin Net Profit or Income /

Sales* 100

167914/ 5732145*

100

= 2.93%

185370/ 7123189*

100

= 2.60%

Return on Assets

(ROA)

Net Income / Total assets*

100

167914/ 2638862*

100

= 6.36%

185370/ 3179266*

100

= 5.83%

Return on Equity

(ROE)

Net Income / Shareholders

equity* 100

167914/ 1094485*

100

= 15.34%

185370/ 3179266*

100

= 5.83%

Current Ratio Current Assets / Current

Liabilities

1786140/ 982480

= 1.82

2064100/ 1265332

= 1.63

Quick Ratio (Current Assets -

Inventory) / Current

Liabilities

(1786140 -

1124642)/ 982480

= 0.67

(2064100 -

1340432)/ 1265332

= 0.57

Debt to equity Ratio Total Liabilities /

Shareholders Equity

1544377/ 1094485

= 1.41

1522380/ 1656886

= 0.92

Times Interest Earned Earning Before Interest 277662/ 21955 323631/ 17370

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(coverage) ratio and Tax (EBIT) / Interest

Expenses

= 12.65 = 18.63

Inventory Turnover

Ratio

Cost of Goods sold /

Inventory

4377690/ 1124642

= 3.89

5396923/ 1340432

= 4.03

Average collection

Period

365 days / Average

receivable collection

365 days/ 28.22

= 13 days

365 days/ 5.31

= 69 days

Accounts receivable

turnover

Sales / Accounts

receivable

5732145/ 203143

= 28.22

7123189/ 1340432

= 5.31

B. company performance

from the above calculation it can be interpreted that net income of the company has grown as £

18 million has increased in the year 2019 as compared to 2018. gross profit and operating profits

of the company has also rises in the year 2019 when compared with the year 2018. if we

properly see the above table then it can is said that current assets have also increased the

difference in the current asset in the year 2018 and 2019 is £ 278. it means that company can pay

their current liabilities easily because they are having the capacity to do so. Sales of the business

has also increased in 2019 as than 2018. so it can be said that if sales of the company has

increased than profit and revenue of the company has also increased (Korepanov and et.al.,

2020). So it can be said that Smart resort ltd is the profitable company. Whereas there is other

scenario also current liabilities of the company have also increased and this is the time when it

has seen that company have witness decline in their business.

Equity investment of the company has also increased which means that company is having more

capital which they can invest in expanding the business. Inventory turnover ratio in the year

2019 is 4% and in the year 2018 it was 3.8% which means that company is doing good. When

the inventory turnover ratio is high then it is good for the company because it means that they

are selling goods rapidly and fast. There is demand for the products of the company in the

market (Quaglia and Spendzharova, 2021). The accounts receivable turnover ratio of company

in year 2018 was 28.88 and in the year 2019 it was 5.3. the reason behind less receivable

turnover ratio can be inadequate collection process, low creditworthiness or bad credit policies

of the company. So it is important that smart resort ltd should have revise their credit policies so

that receivables can be collected at time.

6

Expenses

= 12.65 = 18.63

Inventory Turnover

Ratio

Cost of Goods sold /

Inventory

4377690/ 1124642

= 3.89

5396923/ 1340432

= 4.03

Average collection

Period

365 days / Average

receivable collection

365 days/ 28.22

= 13 days

365 days/ 5.31

= 69 days

Accounts receivable

turnover

Sales / Accounts

receivable

5732145/ 203143

= 28.22

7123189/ 1340432

= 5.31

B. company performance

from the above calculation it can be interpreted that net income of the company has grown as £

18 million has increased in the year 2019 as compared to 2018. gross profit and operating profits

of the company has also rises in the year 2019 when compared with the year 2018. if we

properly see the above table then it can is said that current assets have also increased the

difference in the current asset in the year 2018 and 2019 is £ 278. it means that company can pay

their current liabilities easily because they are having the capacity to do so. Sales of the business

has also increased in 2019 as than 2018. so it can be said that if sales of the company has

increased than profit and revenue of the company has also increased (Korepanov and et.al.,

2020). So it can be said that Smart resort ltd is the profitable company. Whereas there is other

scenario also current liabilities of the company have also increased and this is the time when it

has seen that company have witness decline in their business.

Equity investment of the company has also increased which means that company is having more

capital which they can invest in expanding the business. Inventory turnover ratio in the year

2019 is 4% and in the year 2018 it was 3.8% which means that company is doing good. When

the inventory turnover ratio is high then it is good for the company because it means that they

are selling goods rapidly and fast. There is demand for the products of the company in the

market (Quaglia and Spendzharova, 2021). The accounts receivable turnover ratio of company

in year 2018 was 28.88 and in the year 2019 it was 5.3. the reason behind less receivable

turnover ratio can be inadequate collection process, low creditworthiness or bad credit policies

of the company. So it is important that smart resort ltd should have revise their credit policies so

that receivables can be collected at time.

6

Average collection period of the company was 13 days and it grows to 69 days. The growth is

bad for the company because normally low average collection period is preferred by the

company and not high collection period (van der Graaf, 2018). When the collection period is

low which means that company has the ability to collect their payments fast.

CONCLUSION

Through this report it can be concluded that GAAP has discussed in this report. There are

external and internal users of the financial statement which are customers, government,

investors, employee, owners, management, public, media etc. investors are interested in the

financial statements so that they can decide that they want to invest or not. Trade creditors are

interested to see financial reports so that they can take their decision of lending money to the

company or not. Report has also discussed about components of the financial statements in

detail which are income statement, balance sheet and cash flow. Report has also discussed in

detail about the company performance of smart resort ltd.

7

bad for the company because normally low average collection period is preferred by the

company and not high collection period (van der Graaf, 2018). When the collection period is

low which means that company has the ability to collect their payments fast.

CONCLUSION

Through this report it can be concluded that GAAP has discussed in this report. There are

external and internal users of the financial statement which are customers, government,

investors, employee, owners, management, public, media etc. investors are interested in the

financial statements so that they can decide that they want to invest or not. Trade creditors are

interested to see financial reports so that they can take their decision of lending money to the

company or not. Report has also discussed about components of the financial statements in

detail which are income statement, balance sheet and cash flow. Report has also discussed in

detail about the company performance of smart resort ltd.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCE

Books and Journals

Azami, Z., 2018. Review of the Performance of Marketing Media in Managing Financial

Markets (Case Study: Private banks).

Borisova, V., Samoshkina, I., Rybina, L. and Shumkova, O., 2020. Financial Mechanism for

Managing the Environmental Innovation Development of the Economy in

Ukraine. Journal of Environmental Management & Tourism. 11(7). pp.1617-1633.

Korepanov, G. and et.al., 2020. Managing the Financial Stability Potential of Crisis

Enterprises. International Journal of Advanced Research in Engineering and

Technology (IJARET). 11(4).

Plaskova, N.S. and et.al., 2020. Improving Information and Analytical and Methodological

Support for Managing the Structure of Financial Resources of the Organization. Talent

Development & Excellence. 12.

Quaglia, L. and Spendzharova, A., 2021. Regime complexity and managing financial data

streams: The orchestration of trade reporting for derivatives. Regulation &

Governance.

SOLOMON, E.D. and NWAFOR, S., 2018. STRATEGIES FOR MANAGING NON-

FINANCIAL RESOURCES FOR ENHANCED PEACEFUL LEARNING

ENVIRONMENT IN PUBLIC UNIVERSITIES IN RIVERS STATE,

NIGERIA. African Journal of Educational Research and Development (AJERD). 11,

p.1.

Sova, O.Y. and et.al., 2021. The mechanism for managing the financial and economic security

of an enterprise in the context of instability. Studies of Applied Economics. 39(6).

Sukharev, O.S., 2019. Managing the technological development structure: Risk and “interest

portfolio”. Upravlenets. 10(1). pp.2-15.

van Der Graaf, A., 2018. Managing financial risks: protecting the organisation (Doctoral

dissertation, Institut d'études politiques de paris-Sciences Po).

van der Graaf, A.E.A., 2018. Managing Financial Risks (Doctoral dissertation, Sciences Po).

Wei, S.J., 2018. Managing financial globalization: Insights from the recent literature (No.

w24330). National Bureau of Economic Research.

Сосновська, О.О. and Житар, М.О., 2018. Financial architecture as the base of financial safety

of the enterprise. Baltic Journal of Economic Studies. 4(4). pp.334-340.

Online

Components of Financial Statements., 2020. [Online]. Available through:

<https://www.wallstreetmojo.com/components-of-financial-statements/>

8

Books and Journals

Azami, Z., 2018. Review of the Performance of Marketing Media in Managing Financial

Markets (Case Study: Private banks).

Borisova, V., Samoshkina, I., Rybina, L. and Shumkova, O., 2020. Financial Mechanism for

Managing the Environmental Innovation Development of the Economy in

Ukraine. Journal of Environmental Management & Tourism. 11(7). pp.1617-1633.

Korepanov, G. and et.al., 2020. Managing the Financial Stability Potential of Crisis

Enterprises. International Journal of Advanced Research in Engineering and

Technology (IJARET). 11(4).

Plaskova, N.S. and et.al., 2020. Improving Information and Analytical and Methodological

Support for Managing the Structure of Financial Resources of the Organization. Talent

Development & Excellence. 12.

Quaglia, L. and Spendzharova, A., 2021. Regime complexity and managing financial data

streams: The orchestration of trade reporting for derivatives. Regulation &

Governance.

SOLOMON, E.D. and NWAFOR, S., 2018. STRATEGIES FOR MANAGING NON-

FINANCIAL RESOURCES FOR ENHANCED PEACEFUL LEARNING

ENVIRONMENT IN PUBLIC UNIVERSITIES IN RIVERS STATE,

NIGERIA. African Journal of Educational Research and Development (AJERD). 11,

p.1.

Sova, O.Y. and et.al., 2021. The mechanism for managing the financial and economic security

of an enterprise in the context of instability. Studies of Applied Economics. 39(6).

Sukharev, O.S., 2019. Managing the technological development structure: Risk and “interest

portfolio”. Upravlenets. 10(1). pp.2-15.

van Der Graaf, A., 2018. Managing financial risks: protecting the organisation (Doctoral

dissertation, Institut d'études politiques de paris-Sciences Po).

van der Graaf, A.E.A., 2018. Managing Financial Risks (Doctoral dissertation, Sciences Po).

Wei, S.J., 2018. Managing financial globalization: Insights from the recent literature (No.

w24330). National Bureau of Economic Research.

Сосновська, О.О. and Житар, М.О., 2018. Financial architecture as the base of financial safety

of the enterprise. Baltic Journal of Economic Studies. 4(4). pp.334-340.

Online

Components of Financial Statements., 2020. [Online]. Available through:

<https://www.wallstreetmojo.com/components-of-financial-statements/>

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.