Smith Group Plc Financial Analysis: Profitability and Liquidity Ratios

VerifiedAdded on 2022/01/07

|15

|3796

|33

Report

AI Summary

This report provides a comprehensive financial analysis of Smith Group Plc, a multinational enterprise with diverse business segments. The analysis includes a detailed examination of the company's financial performance over two years, focusing on key metrics such as revenue, operating profit, and net profit. The report employs various financial ratios, including profitability, liquidity, capital structure, and asset efficiency ratios, to assess Smith Group Plc's performance relative to its competitor, Emerson Electric Co. Furthermore, the report delves into project appraisal, specifically evaluating the potential investment in new catheter manufacturing equipment using Net Present Value (NPV), Internal Rate of Return (IRR), and Discounted Payback Period methods, considering factors such as sunk costs, depreciation, and working capital. The report concludes with a discussion of the limitations of ratio analysis and the overall financial health of Smith Group Plc.

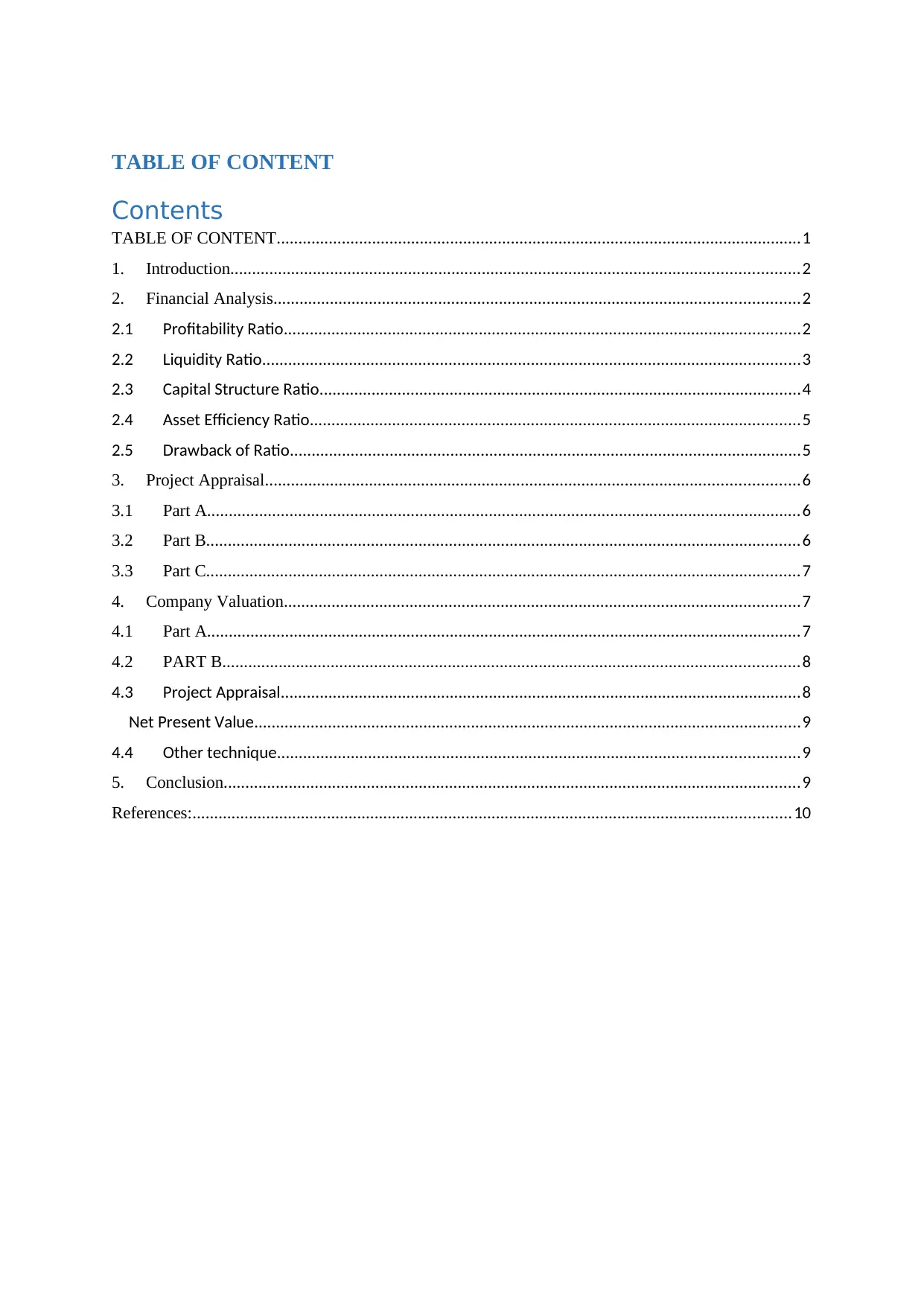

TABLE OF CONTENT

Contents

TABLE OF CONTENT.........................................................................................................................1

1. Introduction...................................................................................................................................2

2. Financial Analysis.........................................................................................................................2

2.1 Profitability Ratio.......................................................................................................................2

2.2 Liquidity Ratio............................................................................................................................3

2.3 Capital Structure Ratio...............................................................................................................4

2.4 Asset Efficiency Ratio.................................................................................................................5

2.5 Drawback of Ratio......................................................................................................................5

3. Project Appraisal...........................................................................................................................6

3.1 Part A.........................................................................................................................................6

3.2 Part B.........................................................................................................................................6

3.3 Part C.........................................................................................................................................7

4. Company Valuation.......................................................................................................................7

4.1 Part A.........................................................................................................................................7

4.2 PART B.....................................................................................................................................8

4.3 Project Appraisal........................................................................................................................8

Net Present Value..............................................................................................................................9

4.4 Other technique........................................................................................................................9

5. Conclusion.....................................................................................................................................9

References:..........................................................................................................................................10

Contents

TABLE OF CONTENT.........................................................................................................................1

1. Introduction...................................................................................................................................2

2. Financial Analysis.........................................................................................................................2

2.1 Profitability Ratio.......................................................................................................................2

2.2 Liquidity Ratio............................................................................................................................3

2.3 Capital Structure Ratio...............................................................................................................4

2.4 Asset Efficiency Ratio.................................................................................................................5

2.5 Drawback of Ratio......................................................................................................................5

3. Project Appraisal...........................................................................................................................6

3.1 Part A.........................................................................................................................................6

3.2 Part B.........................................................................................................................................6

3.3 Part C.........................................................................................................................................7

4. Company Valuation.......................................................................................................................7

4.1 Part A.........................................................................................................................................7

4.2 PART B.....................................................................................................................................8

4.3 Project Appraisal........................................................................................................................8

Net Present Value..............................................................................................................................9

4.4 Other technique........................................................................................................................9

5. Conclusion.....................................................................................................................................9

References:..........................................................................................................................................10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

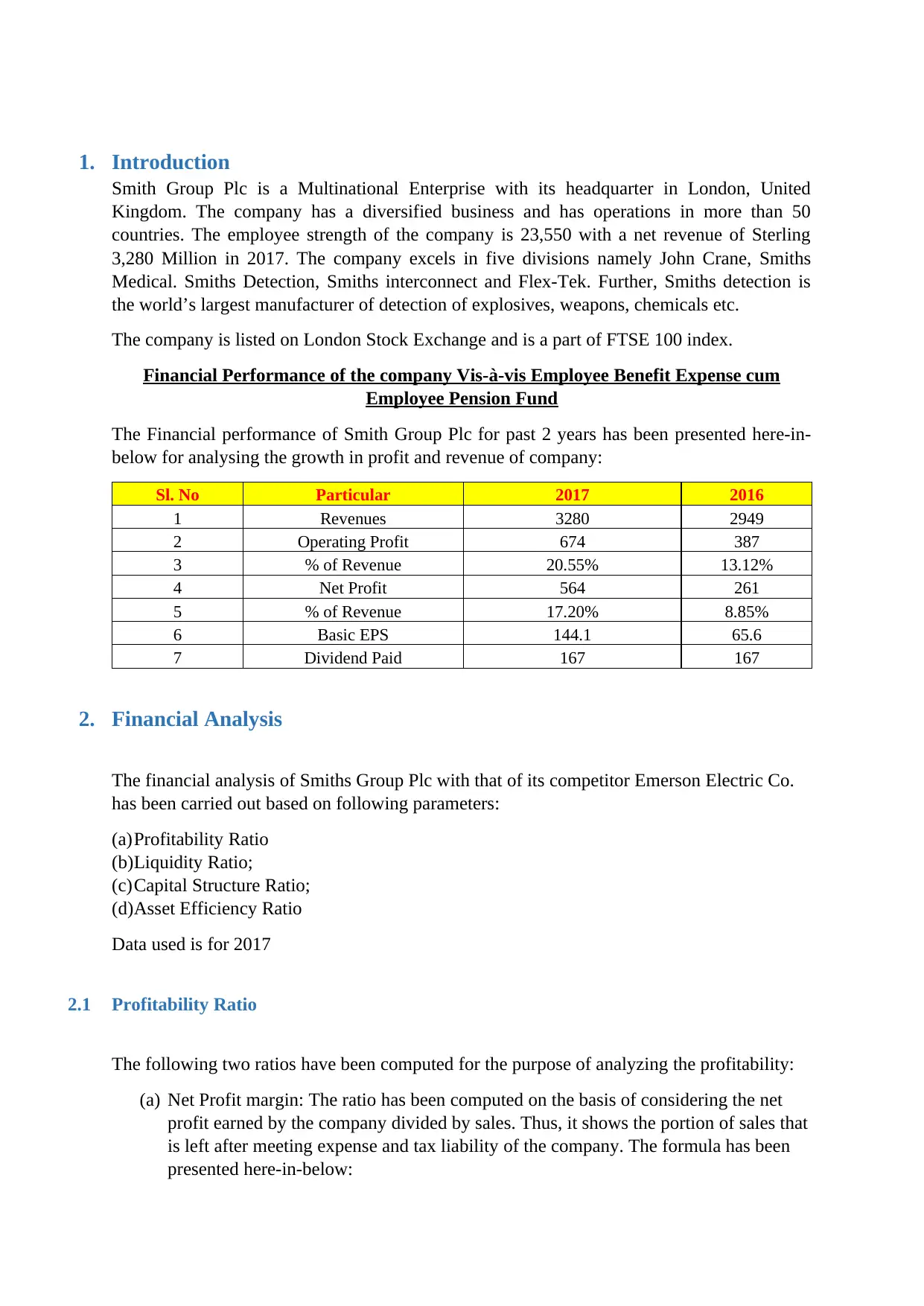

1. Introduction

Smith Group Plc is a Multinational Enterprise with its headquarter in London, United

Kingdom. The company has a diversified business and has operations in more than 50

countries. The employee strength of the company is 23,550 with a net revenue of Sterling

3,280 Million in 2017. The company excels in five divisions namely John Crane, Smiths

Medical. Smiths Detection, Smiths interconnect and Flex-Tek. Further, Smiths detection is

the world’s largest manufacturer of detection of explosives, weapons, chemicals etc.

The company is listed on London Stock Exchange and is a part of FTSE 100 index.

Financial Performance of the company Vis-à-vis Employee Benefit Expense cum

Employee Pension Fund

The Financial performance of Smith Group Plc for past 2 years has been presented here-in-

below for analysing the growth in profit and revenue of company:

Sl. No Particular 2017 2016

1 Revenues 3280 2949

2 Operating Profit 674 387

3 % of Revenue 20.55% 13.12%

4 Net Profit 564 261

5 % of Revenue 17.20% 8.85%

6 Basic EPS 144.1 65.6

7 Dividend Paid 167 167

2. Financial Analysis

The financial analysis of Smiths Group Plc with that of its competitor Emerson Electric Co.

has been carried out based on following parameters:

(a)Profitability Ratio

(b)Liquidity Ratio;

(c)Capital Structure Ratio;

(d)Asset Efficiency Ratio

Data used is for 2017

2.1 Profitability Ratio

The following two ratios have been computed for the purpose of analyzing the profitability:

(a) Net Profit margin: The ratio has been computed on the basis of considering the net

profit earned by the company divided by sales. Thus, it shows the portion of sales that

is left after meeting expense and tax liability of the company. The formula has been

presented here-in-below:

Smith Group Plc is a Multinational Enterprise with its headquarter in London, United

Kingdom. The company has a diversified business and has operations in more than 50

countries. The employee strength of the company is 23,550 with a net revenue of Sterling

3,280 Million in 2017. The company excels in five divisions namely John Crane, Smiths

Medical. Smiths Detection, Smiths interconnect and Flex-Tek. Further, Smiths detection is

the world’s largest manufacturer of detection of explosives, weapons, chemicals etc.

The company is listed on London Stock Exchange and is a part of FTSE 100 index.

Financial Performance of the company Vis-à-vis Employee Benefit Expense cum

Employee Pension Fund

The Financial performance of Smith Group Plc for past 2 years has been presented here-in-

below for analysing the growth in profit and revenue of company:

Sl. No Particular 2017 2016

1 Revenues 3280 2949

2 Operating Profit 674 387

3 % of Revenue 20.55% 13.12%

4 Net Profit 564 261

5 % of Revenue 17.20% 8.85%

6 Basic EPS 144.1 65.6

7 Dividend Paid 167 167

2. Financial Analysis

The financial analysis of Smiths Group Plc with that of its competitor Emerson Electric Co.

has been carried out based on following parameters:

(a)Profitability Ratio

(b)Liquidity Ratio;

(c)Capital Structure Ratio;

(d)Asset Efficiency Ratio

Data used is for 2017

2.1 Profitability Ratio

The following two ratios have been computed for the purpose of analyzing the profitability:

(a) Net Profit margin: The ratio has been computed on the basis of considering the net

profit earned by the company divided by sales. Thus, it shows the portion of sales that

is left after meeting expense and tax liability of the company. The formula has been

presented here-in-below:

Net Profit Margin = (Net Profit / Sales)

Further, the higher the margin, the better the company is performing

Emerson Electric Co

Sl. No. Particulars Net Profit Sales

Rati

o

1

Net Profit

Ratio 15,18,000 1,52,64,000 9.94

Smith Group Plc.

l. No Particulars Net Sales Net Profit Ratio

1

Net profit

Ratio 32,80,000 5,62,000 17.13%

On the basis of above, it can be seen that Smith Group Plc is performing better

compared to Emerson Electric Co.

(b) Return on Capital Employed: The ratio has been computed on the basis of Earning

before Interest and Tax as divided by capital employed by the company. Further, the

higher the margin, the better the company is performing.

Emerson Electric Co

Sl. No. Particulars EBIT

Capital

Employed Ratio

1

Return On Capital

Employed 26,91,000 1,45,44,000 18.50%

Smith Group Plc.

Sl. No Particulars EBIT

Capital

Employed Ratio

1

Return on Capital

Employed 5,69,000 42,90,000 13.26%

On the basis of above, it can be seen that Return on Capital Employed is better for

Emerson Electric Co.

Further, the higher the margin, the better the company is performing

Emerson Electric Co

Sl. No. Particulars Net Profit Sales

Rati

o

1

Net Profit

Ratio 15,18,000 1,52,64,000 9.94

Smith Group Plc.

l. No Particulars Net Sales Net Profit Ratio

1

Net profit

Ratio 32,80,000 5,62,000 17.13%

On the basis of above, it can be seen that Smith Group Plc is performing better

compared to Emerson Electric Co.

(b) Return on Capital Employed: The ratio has been computed on the basis of Earning

before Interest and Tax as divided by capital employed by the company. Further, the

higher the margin, the better the company is performing.

Emerson Electric Co

Sl. No. Particulars EBIT

Capital

Employed Ratio

1

Return On Capital

Employed 26,91,000 1,45,44,000 18.50%

Smith Group Plc.

Sl. No Particulars EBIT

Capital

Employed Ratio

1

Return on Capital

Employed 5,69,000 42,90,000 13.26%

On the basis of above, it can be seen that Return on Capital Employed is better for

Emerson Electric Co.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

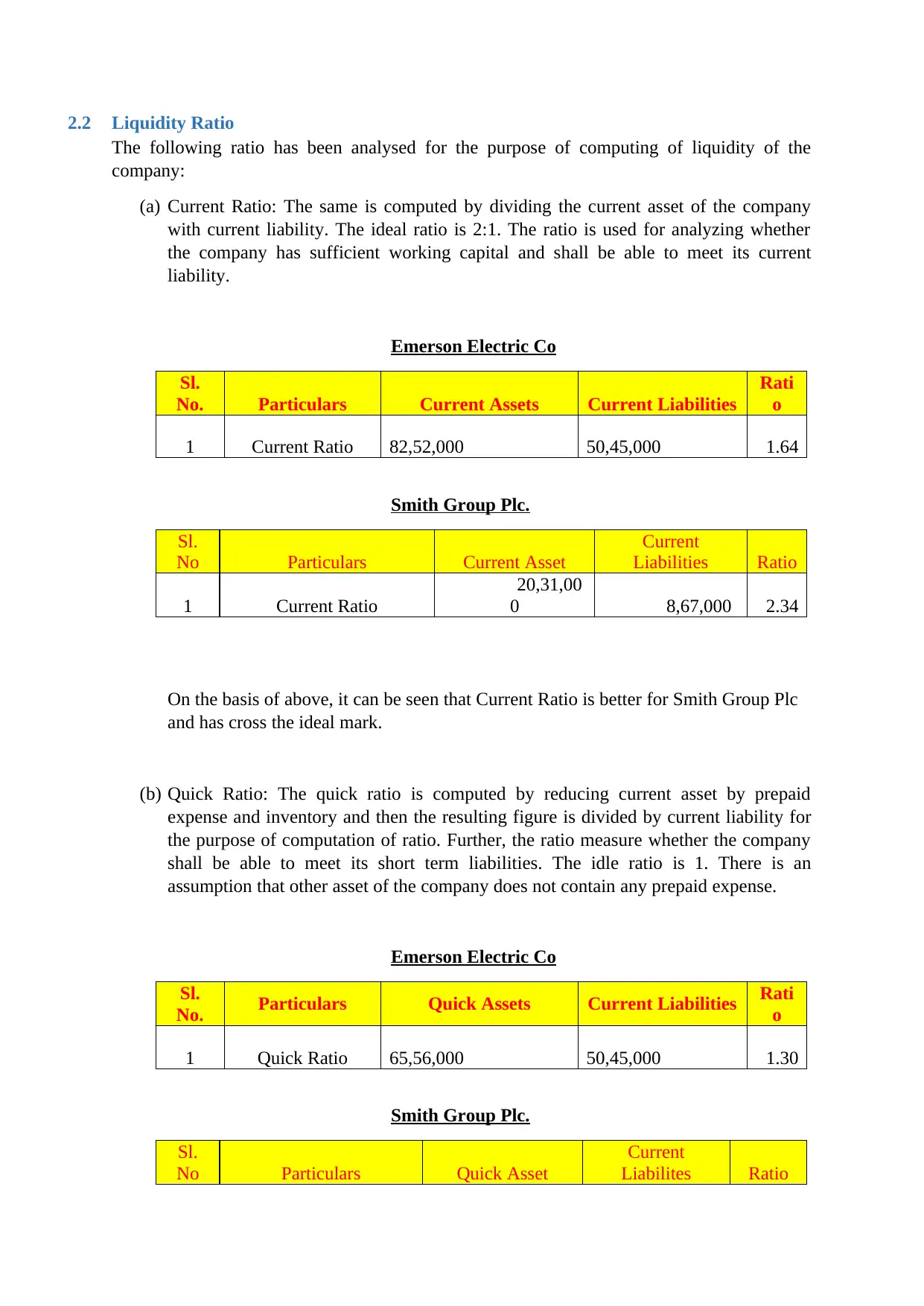

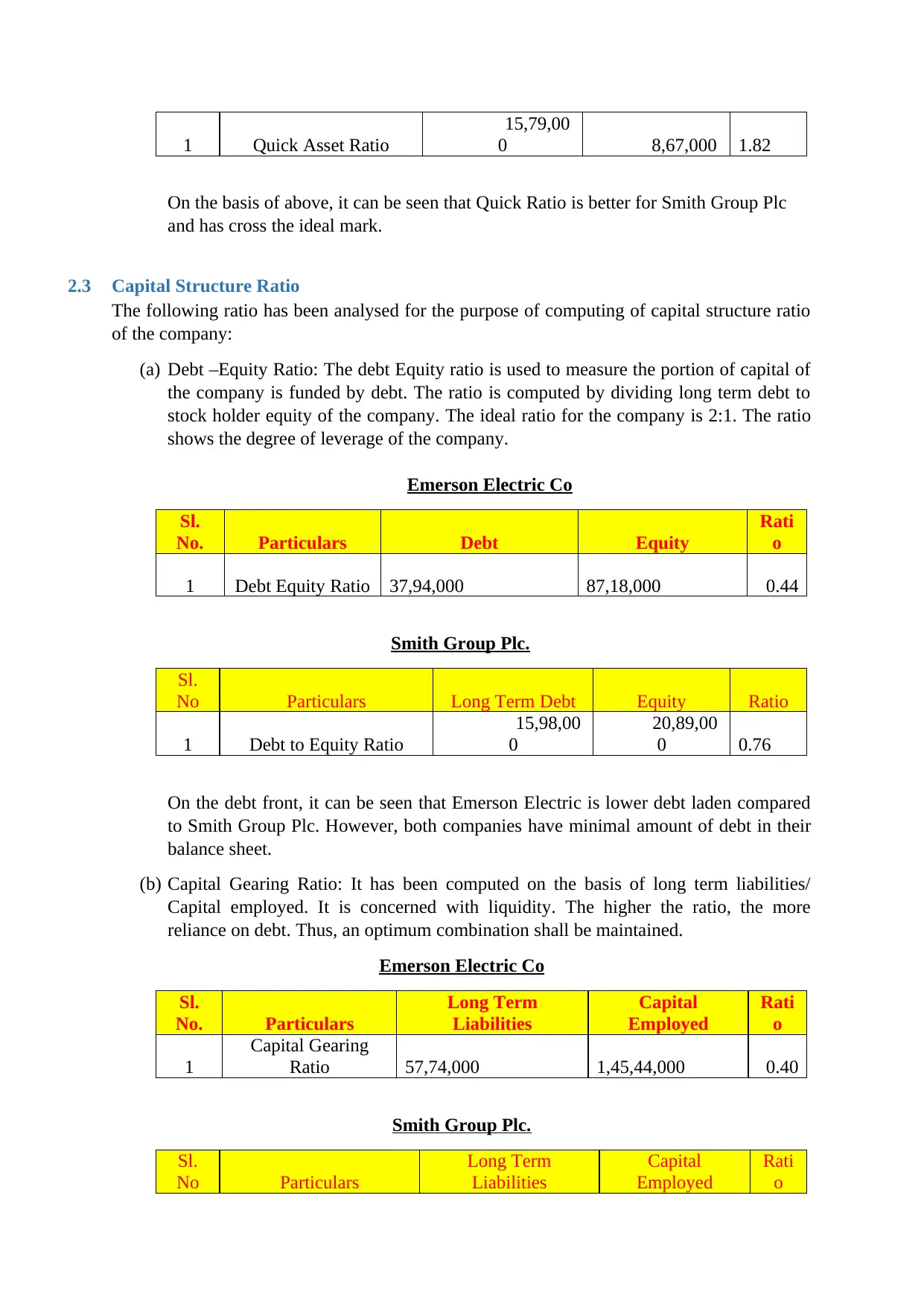

2.2 Liquidity Ratio

The following ratio has been analysed for the purpose of computing of liquidity of the

company:

(a) Current Ratio: The same is computed by dividing the current asset of the company

with current liability. The ideal ratio is 2:1. The ratio is used for analyzing whether

the company has sufficient working capital and shall be able to meet its current

liability.

Emerson Electric Co

Sl.

No. Particulars Current Assets Current Liabilities

Rati

o

1 Current Ratio 82,52,000 50,45,000 1.64

Smith Group Plc.

Sl.

No Particulars Current Asset

Current

Liabilities Ratio

1 Current Ratio

20,31,00

0 8,67,000 2.34

On the basis of above, it can be seen that Current Ratio is better for Smith Group Plc

and has cross the ideal mark.

(b) Quick Ratio: The quick ratio is computed by reducing current asset by prepaid

expense and inventory and then the resulting figure is divided by current liability for

the purpose of computation of ratio. Further, the ratio measure whether the company

shall be able to meet its short term liabilities. The idle ratio is 1. There is an

assumption that other asset of the company does not contain any prepaid expense.

Emerson Electric Co

Sl.

No. Particulars Quick Assets Current Liabilities Rati

o

1 Quick Ratio 65,56,000 50,45,000 1.30

Smith Group Plc.

Sl.

No Particulars Quick Asset

Current

Liabilites Ratio

The following ratio has been analysed for the purpose of computing of liquidity of the

company:

(a) Current Ratio: The same is computed by dividing the current asset of the company

with current liability. The ideal ratio is 2:1. The ratio is used for analyzing whether

the company has sufficient working capital and shall be able to meet its current

liability.

Emerson Electric Co

Sl.

No. Particulars Current Assets Current Liabilities

Rati

o

1 Current Ratio 82,52,000 50,45,000 1.64

Smith Group Plc.

Sl.

No Particulars Current Asset

Current

Liabilities Ratio

1 Current Ratio

20,31,00

0 8,67,000 2.34

On the basis of above, it can be seen that Current Ratio is better for Smith Group Plc

and has cross the ideal mark.

(b) Quick Ratio: The quick ratio is computed by reducing current asset by prepaid

expense and inventory and then the resulting figure is divided by current liability for

the purpose of computation of ratio. Further, the ratio measure whether the company

shall be able to meet its short term liabilities. The idle ratio is 1. There is an

assumption that other asset of the company does not contain any prepaid expense.

Emerson Electric Co

Sl.

No. Particulars Quick Assets Current Liabilities Rati

o

1 Quick Ratio 65,56,000 50,45,000 1.30

Smith Group Plc.

Sl.

No Particulars Quick Asset

Current

Liabilites Ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 Quick Asset Ratio

15,79,00

0 8,67,000 1.82

On the basis of above, it can be seen that Quick Ratio is better for Smith Group Plc

and has cross the ideal mark.

2.3 Capital Structure Ratio

The following ratio has been analysed for the purpose of computing of capital structure ratio

of the company:

(a) Debt –Equity Ratio: The debt Equity ratio is used to measure the portion of capital of

the company is funded by debt. The ratio is computed by dividing long term debt to

stock holder equity of the company. The ideal ratio for the company is 2:1. The ratio

shows the degree of leverage of the company.

Emerson Electric Co

Sl.

No. Particulars Debt Equity

Rati

o

1 Debt Equity Ratio 37,94,000 87,18,000 0.44

Smith Group Plc.

Sl.

No Particulars Long Term Debt Equity Ratio

1 Debt to Equity Ratio

15,98,00

0

20,89,00

0 0.76

On the debt front, it can be seen that Emerson Electric is lower debt laden compared

to Smith Group Plc. However, both companies have minimal amount of debt in their

balance sheet.

(b) Capital Gearing Ratio: It has been computed on the basis of long term liabilities/

Capital employed. It is concerned with liquidity. The higher the ratio, the more

reliance on debt. Thus, an optimum combination shall be maintained.

Emerson Electric Co

Sl.

No. Particulars

Long Term

Liabilities

Capital

Employed

Rati

o

1

Capital Gearing

Ratio 57,74,000 1,45,44,000 0.40

Smith Group Plc.

Sl.

No Particulars

Long Term

Liabilities

Capital

Employed

Rati

o

15,79,00

0 8,67,000 1.82

On the basis of above, it can be seen that Quick Ratio is better for Smith Group Plc

and has cross the ideal mark.

2.3 Capital Structure Ratio

The following ratio has been analysed for the purpose of computing of capital structure ratio

of the company:

(a) Debt –Equity Ratio: The debt Equity ratio is used to measure the portion of capital of

the company is funded by debt. The ratio is computed by dividing long term debt to

stock holder equity of the company. The ideal ratio for the company is 2:1. The ratio

shows the degree of leverage of the company.

Emerson Electric Co

Sl.

No. Particulars Debt Equity

Rati

o

1 Debt Equity Ratio 37,94,000 87,18,000 0.44

Smith Group Plc.

Sl.

No Particulars Long Term Debt Equity Ratio

1 Debt to Equity Ratio

15,98,00

0

20,89,00

0 0.76

On the debt front, it can be seen that Emerson Electric is lower debt laden compared

to Smith Group Plc. However, both companies have minimal amount of debt in their

balance sheet.

(b) Capital Gearing Ratio: It has been computed on the basis of long term liabilities/

Capital employed. It is concerned with liquidity. The higher the ratio, the more

reliance on debt. Thus, an optimum combination shall be maintained.

Emerson Electric Co

Sl.

No. Particulars

Long Term

Liabilities

Capital

Employed

Rati

o

1

Capital Gearing

Ratio 57,74,000 1,45,44,000 0.40

Smith Group Plc.

Sl.

No Particulars

Long Term

Liabilities

Capital

Employed

Rati

o

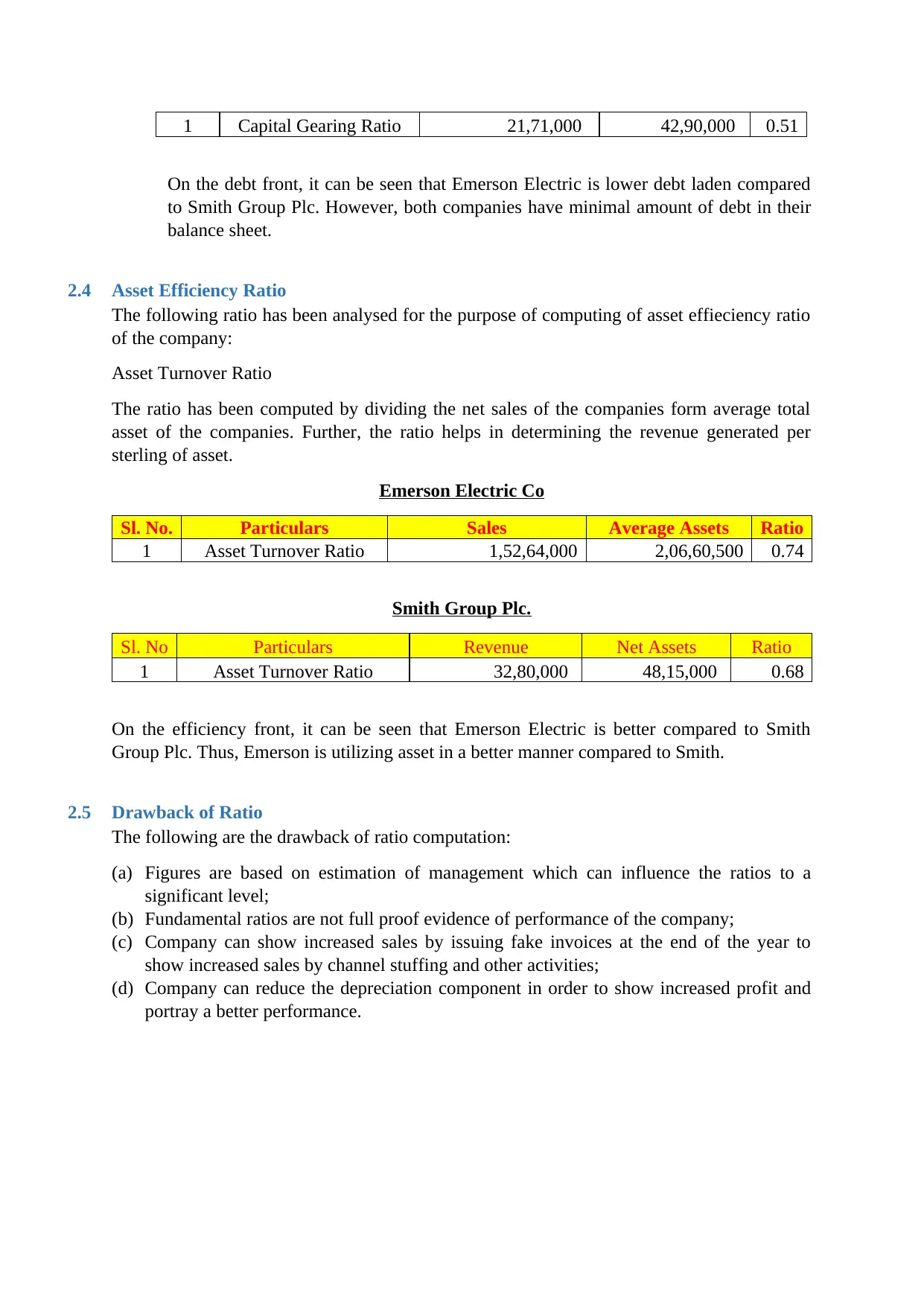

1 Capital Gearing Ratio 21,71,000 42,90,000 0.51

On the debt front, it can be seen that Emerson Electric is lower debt laden compared

to Smith Group Plc. However, both companies have minimal amount of debt in their

balance sheet.

2.4 Asset Efficiency Ratio

The following ratio has been analysed for the purpose of computing of asset effieciency ratio

of the company:

Asset Turnover Ratio

The ratio has been computed by dividing the net sales of the companies form average total

asset of the companies. Further, the ratio helps in determining the revenue generated per

sterling of asset.

Emerson Electric Co

Sl. No. Particulars Sales Average Assets Ratio

1 Asset Turnover Ratio 1,52,64,000 2,06,60,500 0.74

Smith Group Plc.

Sl. No Particulars Revenue Net Assets Ratio

1 Asset Turnover Ratio 32,80,000 48,15,000 0.68

On the efficiency front, it can be seen that Emerson Electric is better compared to Smith

Group Plc. Thus, Emerson is utilizing asset in a better manner compared to Smith.

2.5 Drawback of Ratio

The following are the drawback of ratio computation:

(a) Figures are based on estimation of management which can influence the ratios to a

significant level;

(b) Fundamental ratios are not full proof evidence of performance of the company;

(c) Company can show increased sales by issuing fake invoices at the end of the year to

show increased sales by channel stuffing and other activities;

(d) Company can reduce the depreciation component in order to show increased profit and

portray a better performance.

On the debt front, it can be seen that Emerson Electric is lower debt laden compared

to Smith Group Plc. However, both companies have minimal amount of debt in their

balance sheet.

2.4 Asset Efficiency Ratio

The following ratio has been analysed for the purpose of computing of asset effieciency ratio

of the company:

Asset Turnover Ratio

The ratio has been computed by dividing the net sales of the companies form average total

asset of the companies. Further, the ratio helps in determining the revenue generated per

sterling of asset.

Emerson Electric Co

Sl. No. Particulars Sales Average Assets Ratio

1 Asset Turnover Ratio 1,52,64,000 2,06,60,500 0.74

Smith Group Plc.

Sl. No Particulars Revenue Net Assets Ratio

1 Asset Turnover Ratio 32,80,000 48,15,000 0.68

On the efficiency front, it can be seen that Emerson Electric is better compared to Smith

Group Plc. Thus, Emerson is utilizing asset in a better manner compared to Smith.

2.5 Drawback of Ratio

The following are the drawback of ratio computation:

(a) Figures are based on estimation of management which can influence the ratios to a

significant level;

(b) Fundamental ratios are not full proof evidence of performance of the company;

(c) Company can show increased sales by issuing fake invoices at the end of the year to

show increased sales by channel stuffing and other activities;

(d) Company can reduce the depreciation component in order to show increased profit and

portray a better performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

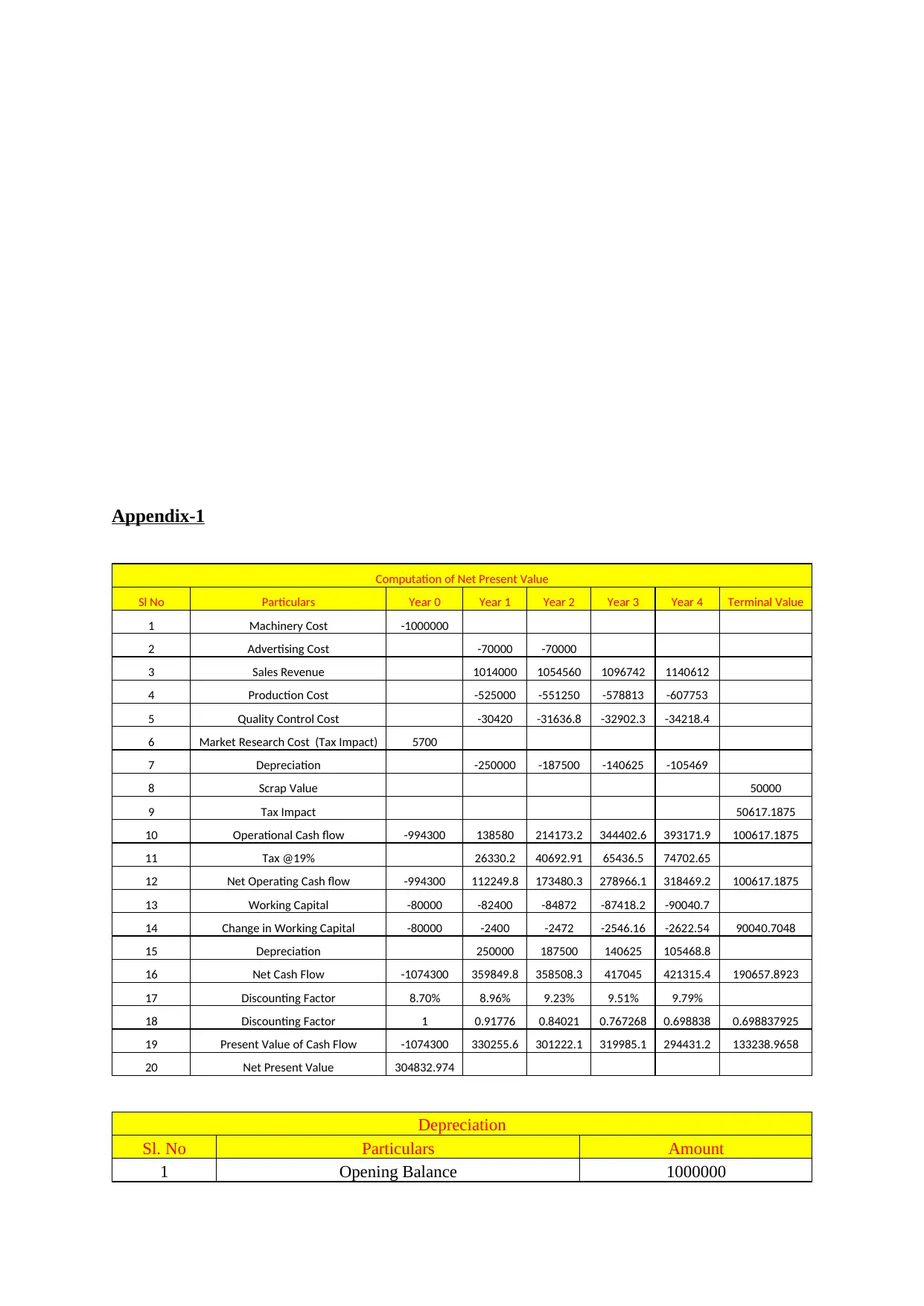

3. Project Appraisal

3.1 Part A

Under the present situation, the board is considering investment in new catheter

manufacturing equipment which shall entail an outflow of 1 Mio Sterling to the company and

an initial working capital investment of 80000 Sterling and shall increase by 3% year on year.

The computation of Net Present Value has been based on following assumptions:

(a) Expenditure on Market Research Cost is a sunk Cost;

(b) Tax benefit of Market Research Cost shall be available;

(c) Advertisement cost remains fixed at 70000 Sterling for two years and there is no such

expenditure thereafter.

(d) The real weighted average cost of capital has been increased by inflation of 3%;

(e) Working capital is realised at the end of the project;

(f) The prices stated in the facts are at year zero;

(g) The capital loss on sale of machinery shall be absorbed in the current business or other

units of Company.

On the basis of above, assumptions Net Present Value of the project of investment in new

catheter manufacturing equipment has been computed at Sterling 304,832.97 which is

positive for the company and adds to the wealth of shareholders. Hence, the project shall be

undertaken based on quantitative factors. However, the project may be rejected if qualitative

factors are taken into consideration.

Further, the method of computation of Net Present Value (a tool of capital budgeting) is

enriched with all other assumptions which are as implied to computation.

For detailed computation, refer Appendix-1.

3.2 Part B

Market Research cost has been treated as sunk cost since the same has been expended before

initiation of the project and does not bear any impact as company has to bear that expenditure

even though the project is not accepted or undertaken. Further, the tax benefit associated with

the cost has been considered while computing the Net Present Value of the project as the

same is on account of the current project. Thus, on the basis of same tax impact of 19% on

the expenditure of 19000 i.e 5700 has been considered for the purpose of analysis while the

remaining portion of the balance i.e. $ 13,300 has been considered as sunk cost and not

relevant for the purpose of analysis. In addition, no further details regarding the relevance of

the said expenditure has been considered,

Depreciation may be defined as outwear, obsolescence, wear and tear of asset. The same is an

allowable expenditure under the Income Tax Act. Further, depreciation is a notional cash

outflow which is entitled to tax reduction or capital allowance. Thus, while computing the

Operating cash flow after cash or net operational flow, depreciation is reduced initially for

computing the tax liability and then added back to compute the net cash flow. Since, the said

expenditure is notional and thus not result in actual outflow of resources of the company.

3.1 Part A

Under the present situation, the board is considering investment in new catheter

manufacturing equipment which shall entail an outflow of 1 Mio Sterling to the company and

an initial working capital investment of 80000 Sterling and shall increase by 3% year on year.

The computation of Net Present Value has been based on following assumptions:

(a) Expenditure on Market Research Cost is a sunk Cost;

(b) Tax benefit of Market Research Cost shall be available;

(c) Advertisement cost remains fixed at 70000 Sterling for two years and there is no such

expenditure thereafter.

(d) The real weighted average cost of capital has been increased by inflation of 3%;

(e) Working capital is realised at the end of the project;

(f) The prices stated in the facts are at year zero;

(g) The capital loss on sale of machinery shall be absorbed in the current business or other

units of Company.

On the basis of above, assumptions Net Present Value of the project of investment in new

catheter manufacturing equipment has been computed at Sterling 304,832.97 which is

positive for the company and adds to the wealth of shareholders. Hence, the project shall be

undertaken based on quantitative factors. However, the project may be rejected if qualitative

factors are taken into consideration.

Further, the method of computation of Net Present Value (a tool of capital budgeting) is

enriched with all other assumptions which are as implied to computation.

For detailed computation, refer Appendix-1.

3.2 Part B

Market Research cost has been treated as sunk cost since the same has been expended before

initiation of the project and does not bear any impact as company has to bear that expenditure

even though the project is not accepted or undertaken. Further, the tax benefit associated with

the cost has been considered while computing the Net Present Value of the project as the

same is on account of the current project. Thus, on the basis of same tax impact of 19% on

the expenditure of 19000 i.e 5700 has been considered for the purpose of analysis while the

remaining portion of the balance i.e. $ 13,300 has been considered as sunk cost and not

relevant for the purpose of analysis. In addition, no further details regarding the relevance of

the said expenditure has been considered,

Depreciation may be defined as outwear, obsolescence, wear and tear of asset. The same is an

allowable expenditure under the Income Tax Act. Further, depreciation is a notional cash

outflow which is entitled to tax reduction or capital allowance. Thus, while computing the

Operating cash flow after cash or net operational flow, depreciation is reduced initially for

computing the tax liability and then added back to compute the net cash flow. Since, the said

expenditure is notional and thus not result in actual outflow of resources of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Therefore, this does not bear much impact on the project except on account of tax benefit

provided under the Act. Thus, in the present case depreciation has been computed at 25%

under diminishing balance method and the value has been reduced from each year cash flow

for the purpose of computation of Net Present Value.

Further, the method of computation of Net Present Value (a tool of capital budgeting) is

enriched with all other assumptions which are as implied to computation.

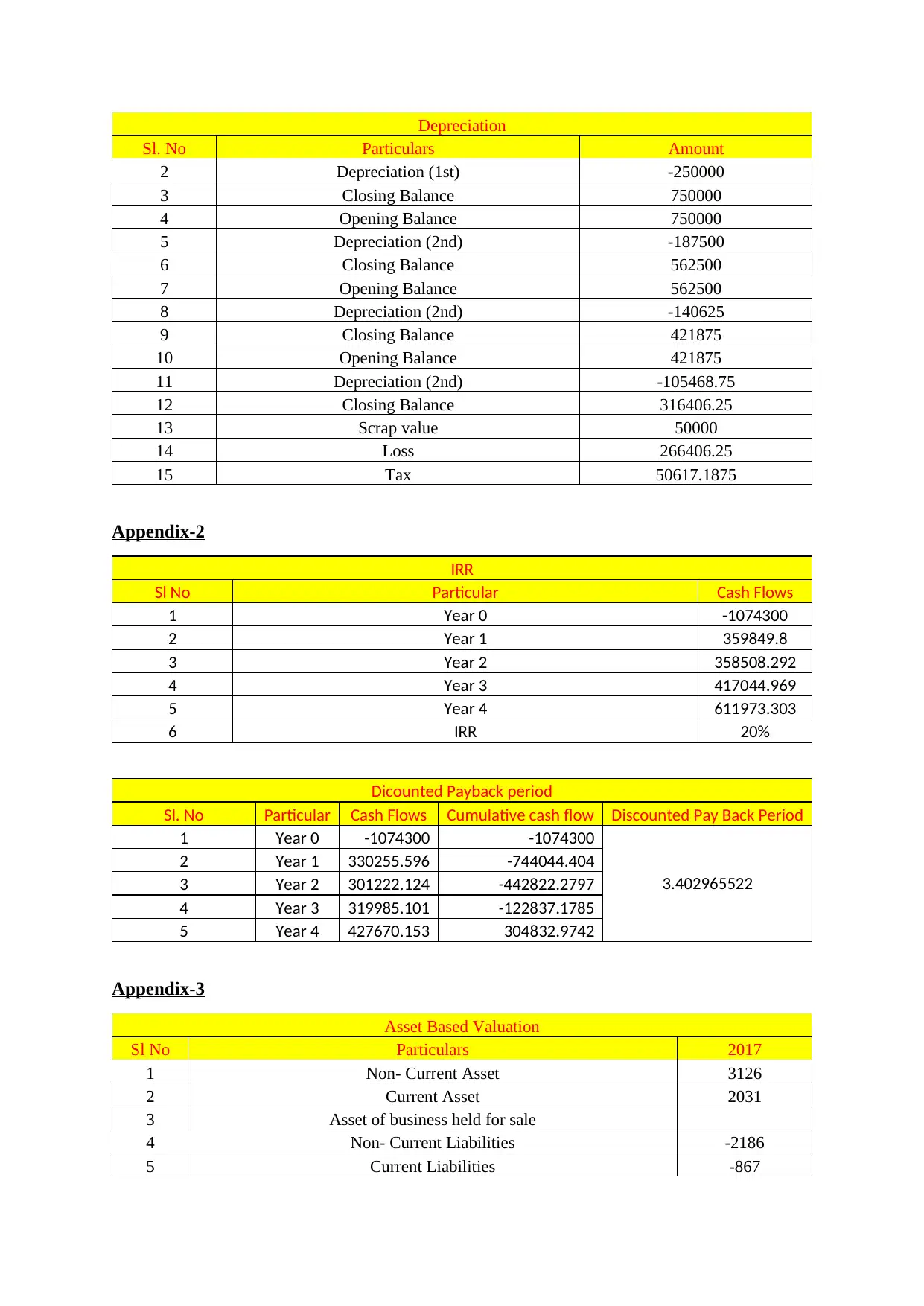

3.3 Part C

Internal Rate of Return is the rate at which return has been provided by the project. In layman

terms it implies the rate of interest at which the net present value of the project is zero or

present value of inflows is equal to the present value of outflows. (Investing Answers Inc,

2018)

Further, the method of computation of Discounted Payback period (a tool of capital

budgeting) is enriched with all other assumptions which are as implied to computation.

Discounted Payback Period is a financial analysis tool under which the time period is

considered within the outflow of resources for a project shall be realised. In layman terms it

means the time period in which the net present value of the out flows of the project is equal to

the net present value of the inflows of the project. Further, this method of financial analysis

does not consider cash flows post the payback period.

The Discounted payback period of the project is computed at 3.40 years. For detailed

computation refer Appendix-2.

Further, the method of computation of Internal Rate of Return (a tool of capital budgeting) is

enriched with all other assumptions which are as implied to computation.

On comparison of both method, it shall be seen that the internal rate of Return is a better

measure compared to discounted payback period wherein the cash flows post post payback

period is not considered. Further, the inflation factor is not accounted in IRR. However, the

rate of IRR is much above the hurdle rate.

4. Company Valuation

4.1 Part A

(a) Asset Based Valuation: Under this method of computation of valuation of equity share,

net asset is computed by reducing total liabilities from total assets. Post this, the value of

net asset is divided by the number of equity shares outstanding. The computation has

been annexed herewith and market as Appendix 3. Further, asset based valuation has

been done on the basis of value presented in Financial Statement of the company and the

values are measured at Fair Market Value in terms of International Financial Reporting

Standard (IFRS). Further, the method measures the company valuation based on

following assumptions:

provided under the Act. Thus, in the present case depreciation has been computed at 25%

under diminishing balance method and the value has been reduced from each year cash flow

for the purpose of computation of Net Present Value.

Further, the method of computation of Net Present Value (a tool of capital budgeting) is

enriched with all other assumptions which are as implied to computation.

3.3 Part C

Internal Rate of Return is the rate at which return has been provided by the project. In layman

terms it implies the rate of interest at which the net present value of the project is zero or

present value of inflows is equal to the present value of outflows. (Investing Answers Inc,

2018)

Further, the method of computation of Discounted Payback period (a tool of capital

budgeting) is enriched with all other assumptions which are as implied to computation.

Discounted Payback Period is a financial analysis tool under which the time period is

considered within the outflow of resources for a project shall be realised. In layman terms it

means the time period in which the net present value of the out flows of the project is equal to

the net present value of the inflows of the project. Further, this method of financial analysis

does not consider cash flows post the payback period.

The Discounted payback period of the project is computed at 3.40 years. For detailed

computation refer Appendix-2.

Further, the method of computation of Internal Rate of Return (a tool of capital budgeting) is

enriched with all other assumptions which are as implied to computation.

On comparison of both method, it shall be seen that the internal rate of Return is a better

measure compared to discounted payback period wherein the cash flows post post payback

period is not considered. Further, the inflation factor is not accounted in IRR. However, the

rate of IRR is much above the hurdle rate.

4. Company Valuation

4.1 Part A

(a) Asset Based Valuation: Under this method of computation of valuation of equity share,

net asset is computed by reducing total liabilities from total assets. Post this, the value of

net asset is divided by the number of equity shares outstanding. The computation has

been annexed herewith and market as Appendix 3. Further, asset based valuation has

been done on the basis of value presented in Financial Statement of the company and the

values are measured at Fair Market Value in terms of International Financial Reporting

Standard (IFRS). Further, the method measures the company valuation based on

following assumptions:

Asset Values reported in Financial Statement are true representative of the actual

values of the company;

Other Assumptions as inherent in the method.

On the basis of above, the value that has been determined per share stands at 5.32

Sterling.

(b) Dividend Based Valuation: Under dividend based valuation model, dividend paid is used

for the computation of share price of the company. Further, the growth rate is computed

by using the retention ratio and Return on Equity. Further, the following assumptions are

used in the above model:

The growth rate shall not be greater than cost of capital;

Cost of Capital has been computed on the basis of CAPM;

Other assumption as inherent to the model.

The valuation of the said model cannot be determined as the growth rate exceeds the cost

of capital of company.

For detailed computation, refer Appendix-4.

(c) Price Earnings Ratio Model: It value the company that value the current share price of

the company in comparison to earning per share of the company. Through price earnings

ratio generally we provide a relative value to the stock. One major drawback is that when

we compare PE ratio of different companies’ valuation and the rate of growth may vary

widely due to different ways company earn money and the varying time factor the

company earn money. Under the said model, the P/E ratio is computed based on

competitor’s average and sect oral average. The computed P/E is multiplied by Earnings

per Share of the company to determine the Price of shares of the company.

On the basis of above, the value that has been determined per share stands at 1534.67

Sterling.

For detailed computation refer Appendix-5.

4.2 PART B

On perusal of the above valuation models, it can be inferred that none of the model is perfect

as every model has its own assumptions and technique of computation of price of equity.

Further, the actual prices of share are not dependent on a particular factor rather the same is

influenced by a group of factors like investor sentiments, company specific factors, market

perception, global news etc. In this scenario, the most appropriate valuation shall be the

valuation done by P/E method, which is nearly close to the value of market.

5. Conclusion

values of the company;

Other Assumptions as inherent in the method.

On the basis of above, the value that has been determined per share stands at 5.32

Sterling.

(b) Dividend Based Valuation: Under dividend based valuation model, dividend paid is used

for the computation of share price of the company. Further, the growth rate is computed

by using the retention ratio and Return on Equity. Further, the following assumptions are

used in the above model:

The growth rate shall not be greater than cost of capital;

Cost of Capital has been computed on the basis of CAPM;

Other assumption as inherent to the model.

The valuation of the said model cannot be determined as the growth rate exceeds the cost

of capital of company.

For detailed computation, refer Appendix-4.

(c) Price Earnings Ratio Model: It value the company that value the current share price of

the company in comparison to earning per share of the company. Through price earnings

ratio generally we provide a relative value to the stock. One major drawback is that when

we compare PE ratio of different companies’ valuation and the rate of growth may vary

widely due to different ways company earn money and the varying time factor the

company earn money. Under the said model, the P/E ratio is computed based on

competitor’s average and sect oral average. The computed P/E is multiplied by Earnings

per Share of the company to determine the Price of shares of the company.

On the basis of above, the value that has been determined per share stands at 1534.67

Sterling.

For detailed computation refer Appendix-5.

4.2 PART B

On perusal of the above valuation models, it can be inferred that none of the model is perfect

as every model has its own assumptions and technique of computation of price of equity.

Further, the actual prices of share are not dependent on a particular factor rather the same is

influenced by a group of factors like investor sentiments, company specific factors, market

perception, global news etc. In this scenario, the most appropriate valuation shall be the

valuation done by P/E method, which is nearly close to the value of market.

5. Conclusion

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The financial position of the company is quite better and the project is viable to be accepted,

as it would give us better return to the business. As the project Net Present Value, Internal

Rate of Return and discounted payback period is quite good comparison to industry the

project is viable to be accepted.

References:

CFI Education Inc., 2018. Net Present Value (NPV). [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/valuation/net-present-value-

npv/

[Accessed 11 December 2018].

Investing Answers Inc, 2018. Internal Rate of Return (IRR). [Online]

Available at: https://investinganswers.com/financial-dictionary/investing/internal-rate-return-irr-2130

[Accessed 9 December 2018].

London Stock Exchange Plc, 2018. SMIN SMITHS GROUP PLC ORD 37.5P. [Online]

Available at: https://www.londonstockexchange.com/exchange/prices/stocks/summary/

fundamentals.html?fourWayKey=GB00B1WY2338GBGBXSET1

[Accessed 9 December 2018].

as it would give us better return to the business. As the project Net Present Value, Internal

Rate of Return and discounted payback period is quite good comparison to industry the

project is viable to be accepted.

References:

CFI Education Inc., 2018. Net Present Value (NPV). [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/valuation/net-present-value-

npv/

[Accessed 11 December 2018].

Investing Answers Inc, 2018. Internal Rate of Return (IRR). [Online]

Available at: https://investinganswers.com/financial-dictionary/investing/internal-rate-return-irr-2130

[Accessed 9 December 2018].

London Stock Exchange Plc, 2018. SMIN SMITHS GROUP PLC ORD 37.5P. [Online]

Available at: https://www.londonstockexchange.com/exchange/prices/stocks/summary/

fundamentals.html?fourWayKey=GB00B1WY2338GBGBXSET1

[Accessed 9 December 2018].

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix-1

Computation of Net Present Value

Sl No Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Terminal Value

1 Machinery Cost -1000000

2 Advertising Cost -70000 -70000

3 Sales Revenue 1014000 1054560 1096742 1140612

4 Production Cost -525000 -551250 -578813 -607753

5 Quality Control Cost -30420 -31636.8 -32902.3 -34218.4

6 Market Research Cost (Tax Impact) 5700

7 Depreciation -250000 -187500 -140625 -105469

8 Scrap Value 50000

9 Tax Impact 50617.1875

10 Operational Cash flow -994300 138580 214173.2 344402.6 393171.9 100617.1875

11 Tax @19% 26330.2 40692.91 65436.5 74702.65

12 Net Operating Cash flow -994300 112249.8 173480.3 278966.1 318469.2 100617.1875

13 Working Capital -80000 -82400 -84872 -87418.2 -90040.7

14 Change in Working Capital -80000 -2400 -2472 -2546.16 -2622.54 90040.7048

15 Depreciation 250000 187500 140625 105468.8

16 Net Cash Flow -1074300 359849.8 358508.3 417045 421315.4 190657.8923

17 Discounting Factor 8.70% 8.96% 9.23% 9.51% 9.79%

18 Discounting Factor 1 0.91776 0.84021 0.767268 0.698838 0.698837925

19 Present Value of Cash Flow -1074300 330255.6 301222.1 319985.1 294431.2 133238.9658

20 Net Present Value 304832.974

Depreciation

Sl. No Particulars Amount

1 Opening Balance 1000000

Computation of Net Present Value

Sl No Particulars Year 0 Year 1 Year 2 Year 3 Year 4 Terminal Value

1 Machinery Cost -1000000

2 Advertising Cost -70000 -70000

3 Sales Revenue 1014000 1054560 1096742 1140612

4 Production Cost -525000 -551250 -578813 -607753

5 Quality Control Cost -30420 -31636.8 -32902.3 -34218.4

6 Market Research Cost (Tax Impact) 5700

7 Depreciation -250000 -187500 -140625 -105469

8 Scrap Value 50000

9 Tax Impact 50617.1875

10 Operational Cash flow -994300 138580 214173.2 344402.6 393171.9 100617.1875

11 Tax @19% 26330.2 40692.91 65436.5 74702.65

12 Net Operating Cash flow -994300 112249.8 173480.3 278966.1 318469.2 100617.1875

13 Working Capital -80000 -82400 -84872 -87418.2 -90040.7

14 Change in Working Capital -80000 -2400 -2472 -2546.16 -2622.54 90040.7048

15 Depreciation 250000 187500 140625 105468.8

16 Net Cash Flow -1074300 359849.8 358508.3 417045 421315.4 190657.8923

17 Discounting Factor 8.70% 8.96% 9.23% 9.51% 9.79%

18 Discounting Factor 1 0.91776 0.84021 0.767268 0.698838 0.698837925

19 Present Value of Cash Flow -1074300 330255.6 301222.1 319985.1 294431.2 133238.9658

20 Net Present Value 304832.974

Depreciation

Sl. No Particulars Amount

1 Opening Balance 1000000

Depreciation

Sl. No Particulars Amount

2 Depreciation (1st) -250000

3 Closing Balance 750000

4 Opening Balance 750000

5 Depreciation (2nd) -187500

6 Closing Balance 562500

7 Opening Balance 562500

8 Depreciation (2nd) -140625

9 Closing Balance 421875

10 Opening Balance 421875

11 Depreciation (2nd) -105468.75

12 Closing Balance 316406.25

13 Scrap value 50000

14 Loss 266406.25

15 Tax 50617.1875

Appendix-2

IRR

Sl No Particular Cash Flows

1 Year 0 -1074300

2 Year 1 359849.8

3 Year 2 358508.292

4 Year 3 417044.969

5 Year 4 611973.303

6 IRR 20%

Dicounted Payback period

Sl. No Particular Cash Flows Cumulative cash flow Discounted Pay Back Period

1 Year 0 -1074300 -1074300

3.402965522

2 Year 1 330255.596 -744044.404

3 Year 2 301222.124 -442822.2797

4 Year 3 319985.101 -122837.1785

5 Year 4 427670.153 304832.9742

Appendix-3

Asset Based Valuation

Sl No Particulars 2017

1 Non- Current Asset 3126

2 Current Asset 2031

3 Asset of business held for sale

4 Non- Current Liabilities -2186

5 Current Liabilities -867

Sl. No Particulars Amount

2 Depreciation (1st) -250000

3 Closing Balance 750000

4 Opening Balance 750000

5 Depreciation (2nd) -187500

6 Closing Balance 562500

7 Opening Balance 562500

8 Depreciation (2nd) -140625

9 Closing Balance 421875

10 Opening Balance 421875

11 Depreciation (2nd) -105468.75

12 Closing Balance 316406.25

13 Scrap value 50000

14 Loss 266406.25

15 Tax 50617.1875

Appendix-2

IRR

Sl No Particular Cash Flows

1 Year 0 -1074300

2 Year 1 359849.8

3 Year 2 358508.292

4 Year 3 417044.969

5 Year 4 611973.303

6 IRR 20%

Dicounted Payback period

Sl. No Particular Cash Flows Cumulative cash flow Discounted Pay Back Period

1 Year 0 -1074300 -1074300

3.402965522

2 Year 1 330255.596 -744044.404

3 Year 2 301222.124 -442822.2797

4 Year 3 319985.101 -122837.1785

5 Year 4 427670.153 304832.9742

Appendix-3

Asset Based Valuation

Sl No Particulars 2017

1 Non- Current Asset 3126

2 Current Asset 2031

3 Asset of business held for sale

4 Non- Current Liabilities -2186

5 Current Liabilities -867

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.