Financial Management Case Study: Smith Inc. Analysis and Solutions

VerifiedAdded on 2021/12/22

|11

|1825

|28

Case Study

AI Summary

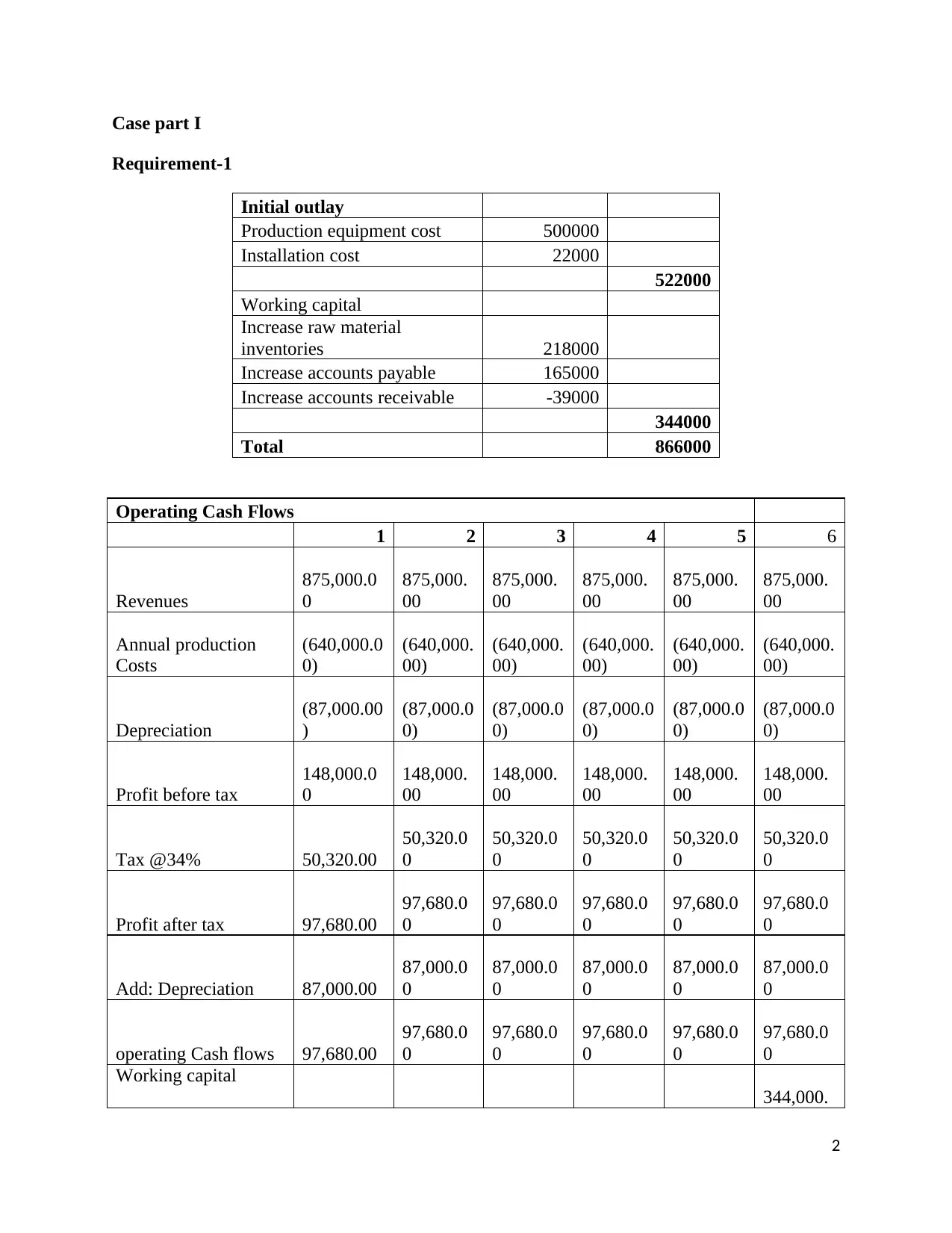

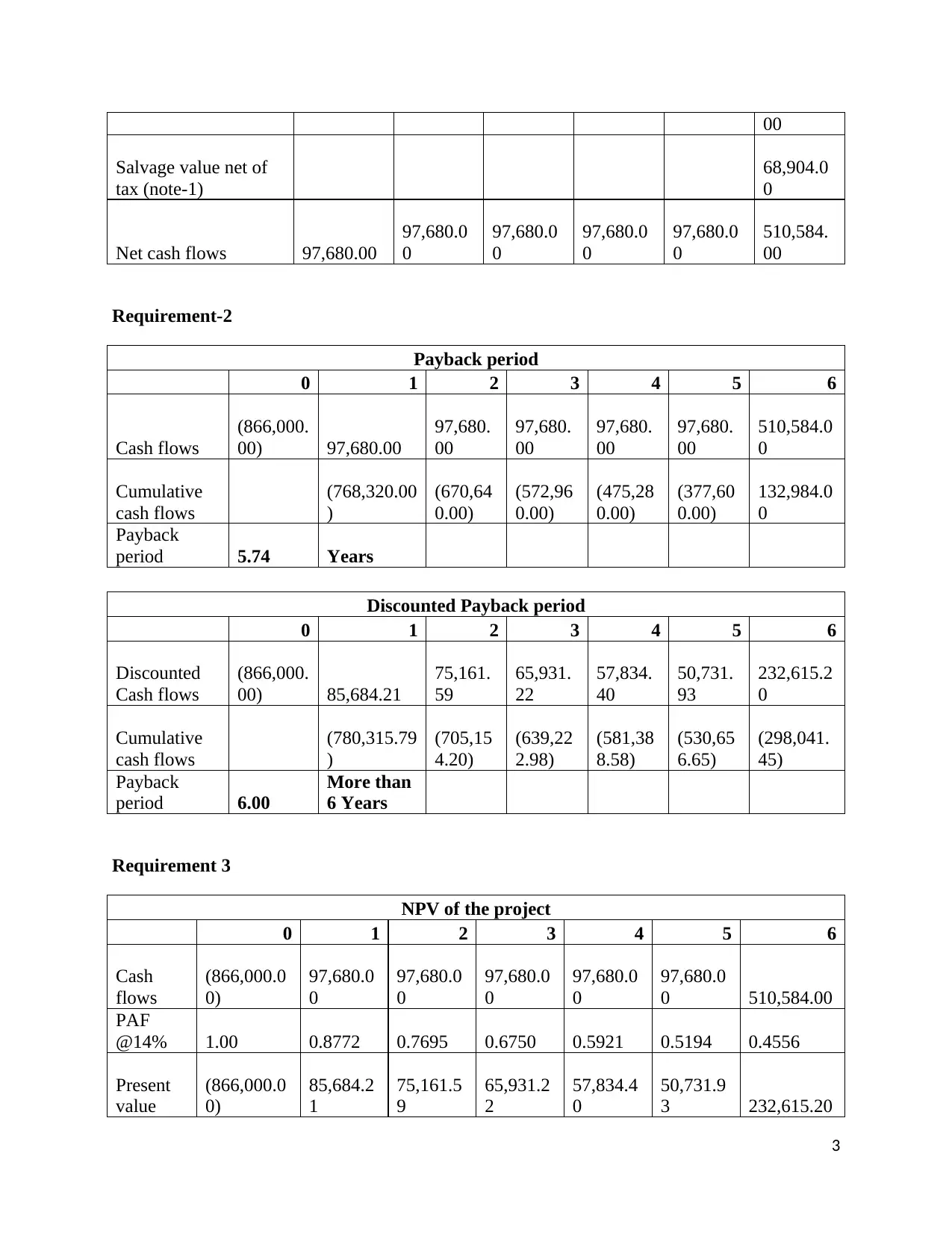

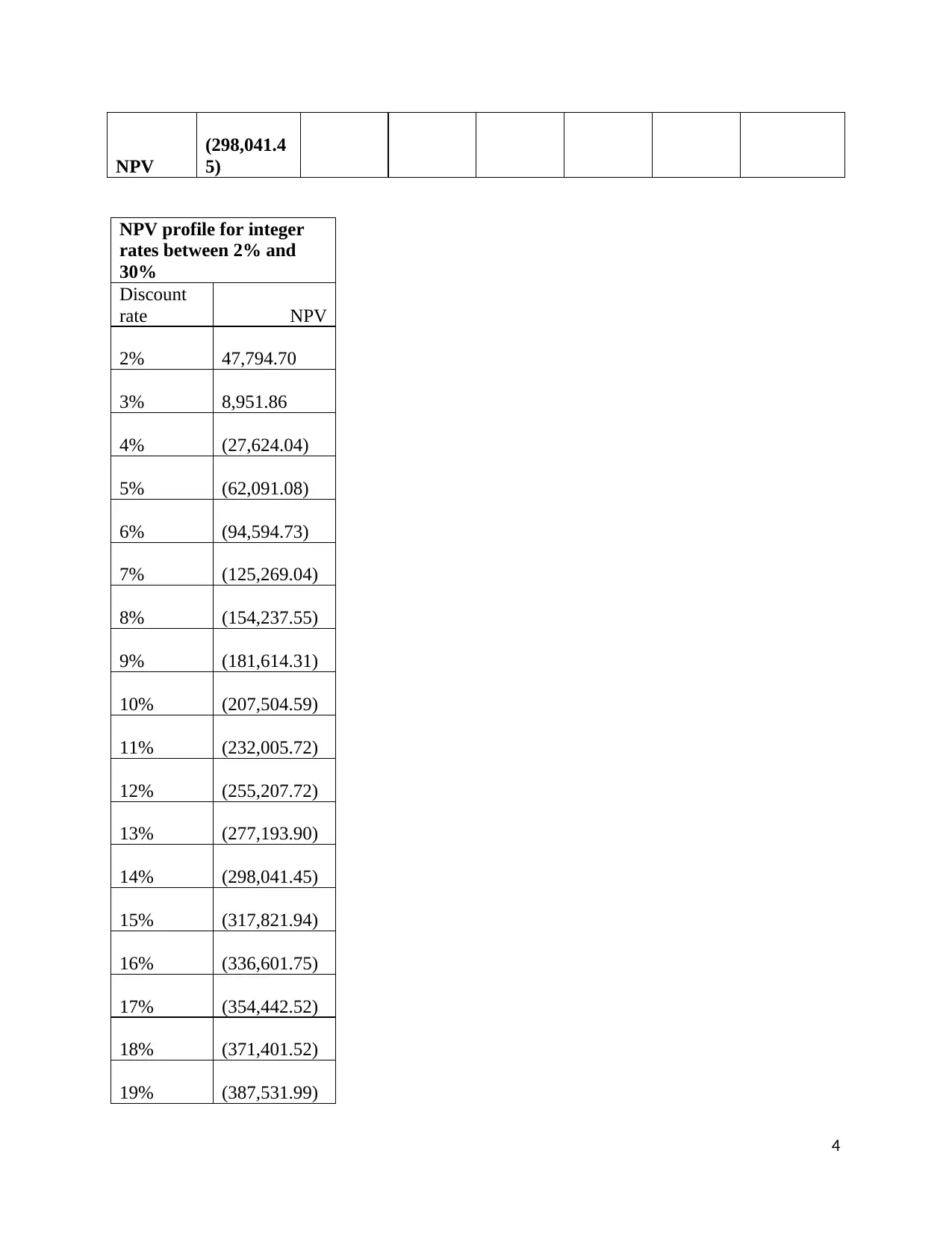

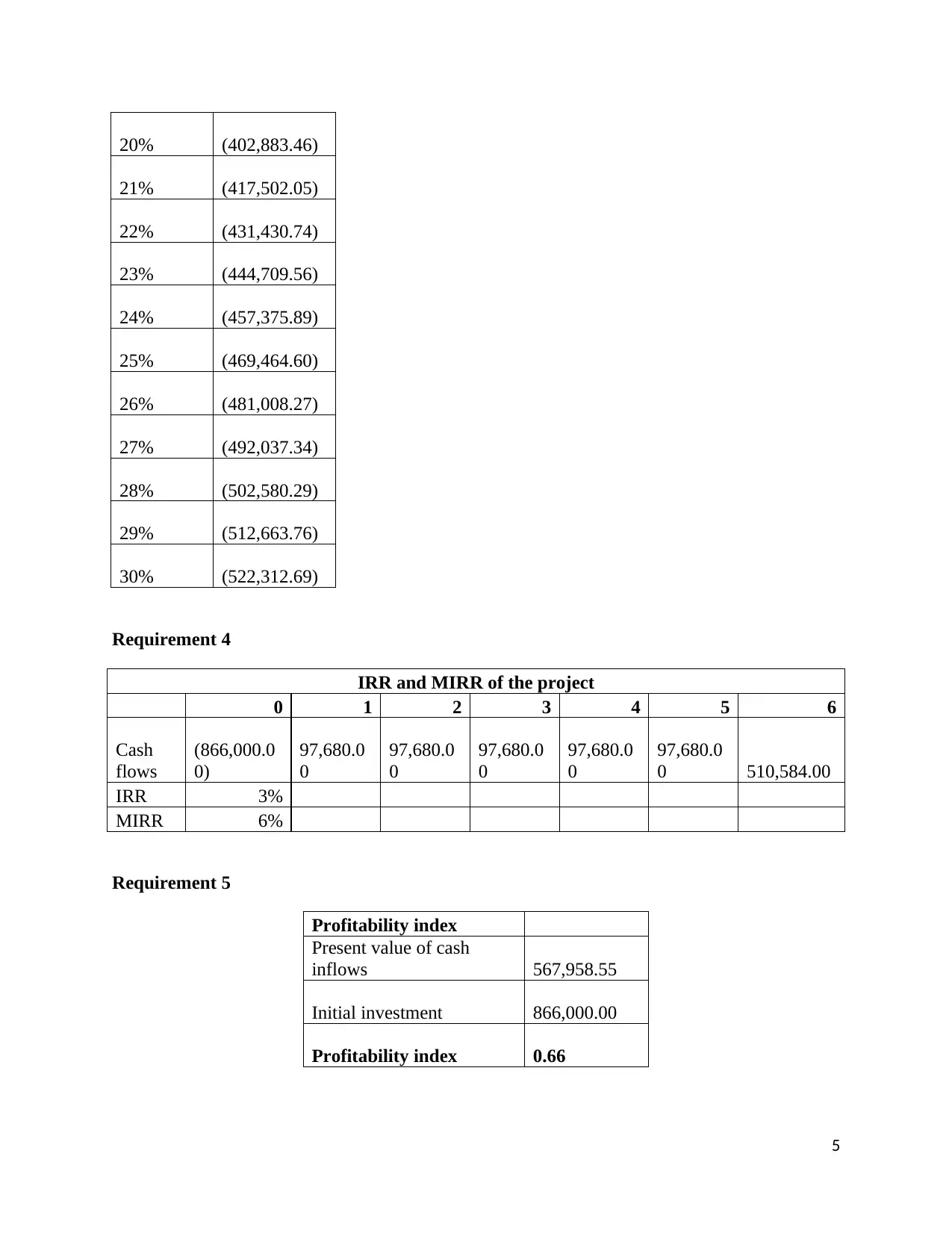

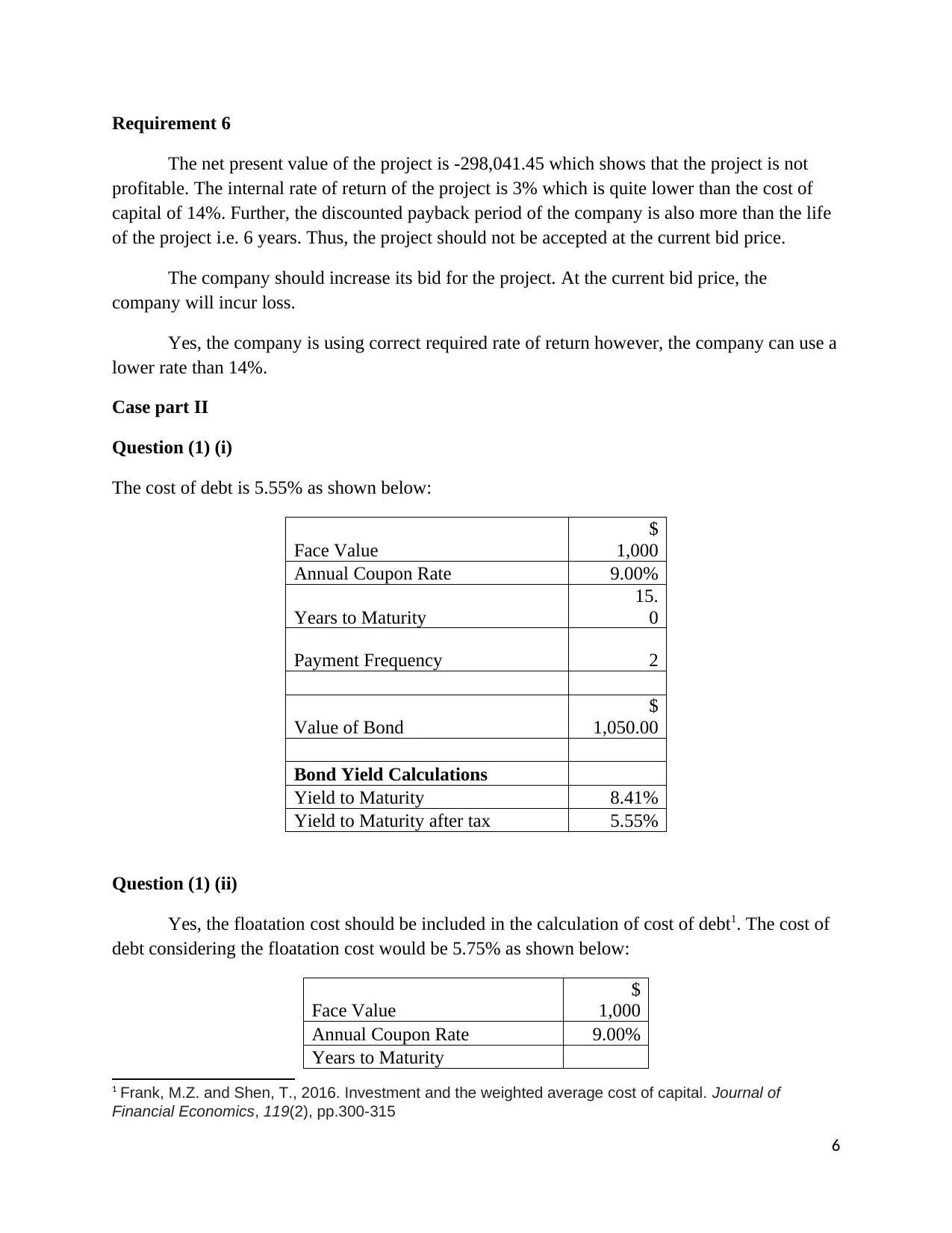

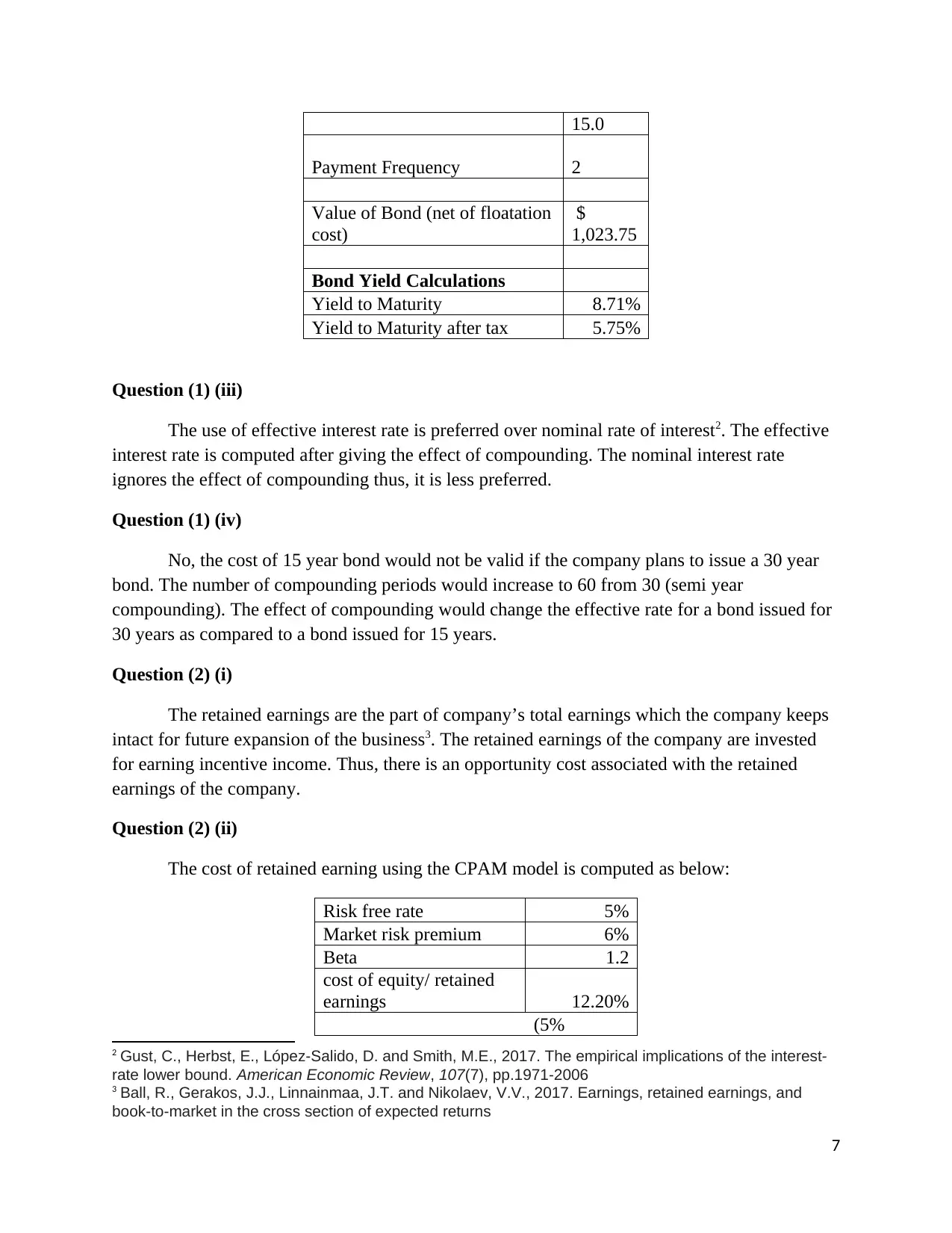

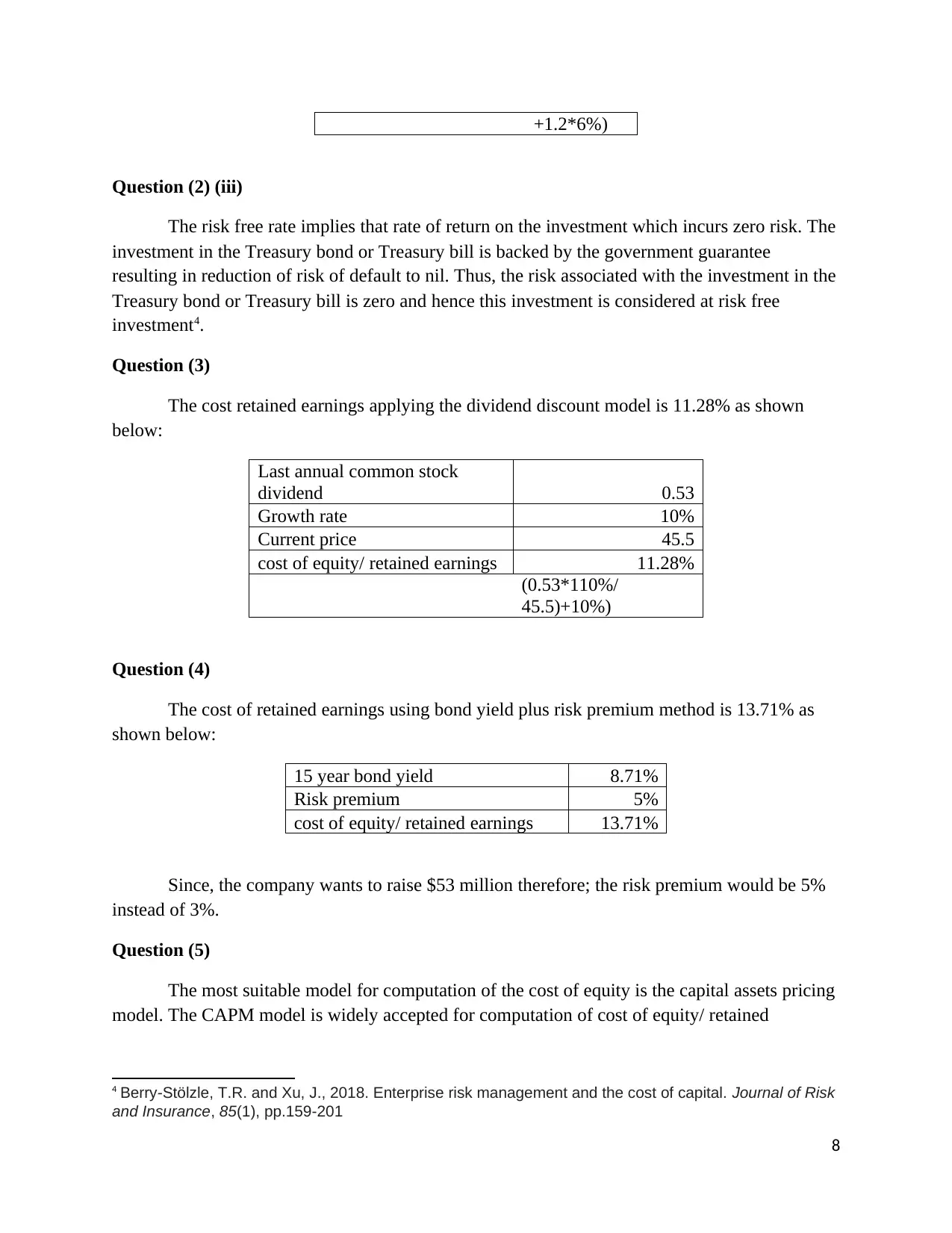

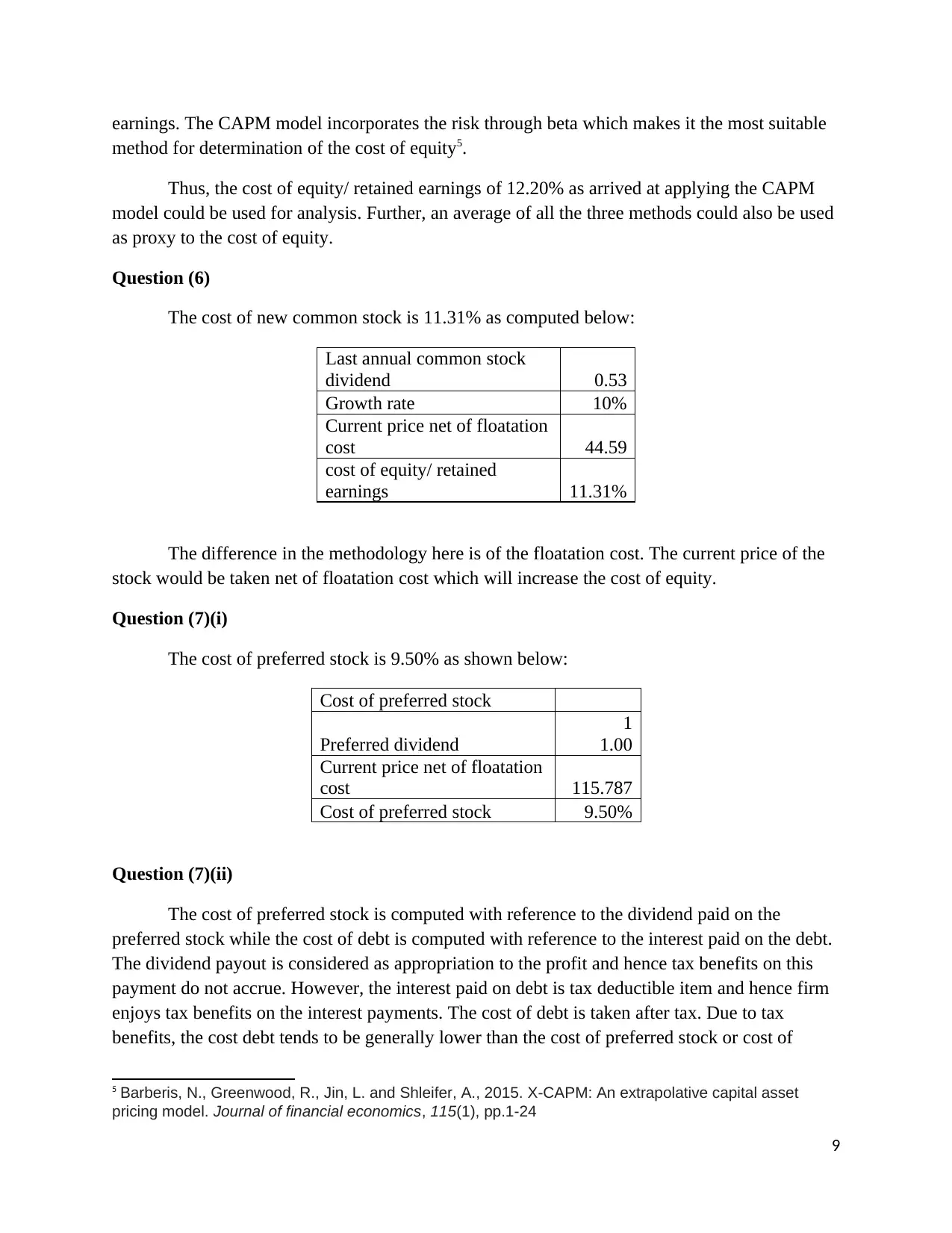

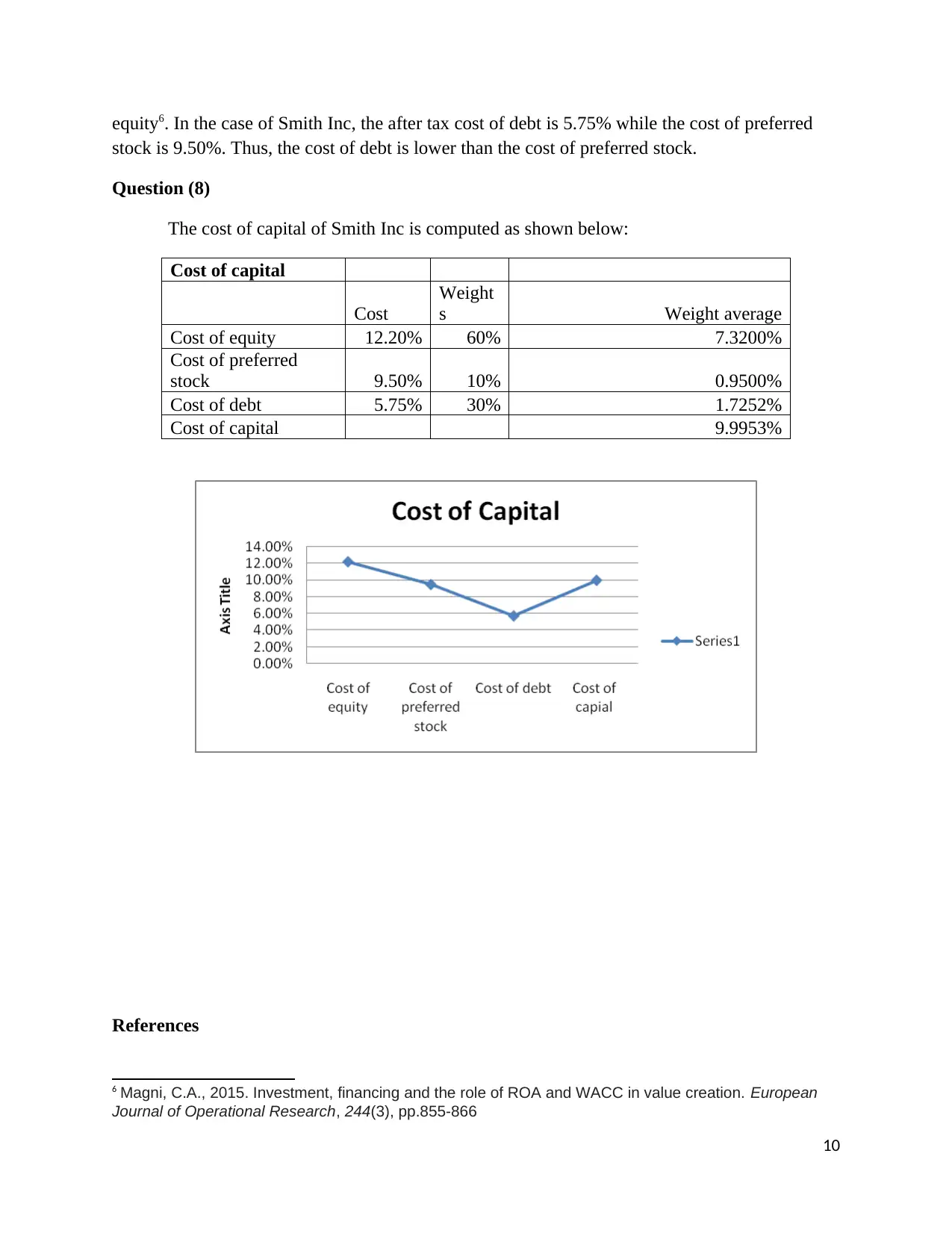

This case study presents a detailed financial analysis of Smith Inc., encompassing capital budgeting decisions and the calculation of the company's cost of capital. Part I of the case focuses on evaluating a potential project, calculating the initial outlay, operating cash flows, payback periods (both regular and discounted), Net Present Value (NPV), Internal Rate of Return (IRR), Modified Internal Rate of Return (MIRR), Profitability Index (PI), and providing recommendations based on these metrics. The analysis reveals that the project is not financially viable at the current bid price. Part II of the case delves into the cost of capital, examining the cost of debt, retained earnings (using CAPM, dividend discount model, and bond yield plus risk premium methods), and preferred stock. It also calculates the weighted average cost of capital (WACC) and the cost of new common stock, providing a comprehensive overview of Smith Inc.'s financial structure and decision-making processes, along with relevant references.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.