Ethical Considerations in Auditing Smith Limited's Financials

VerifiedAdded on 2023/06/05

|7

|538

|324

Case Study

AI Summary

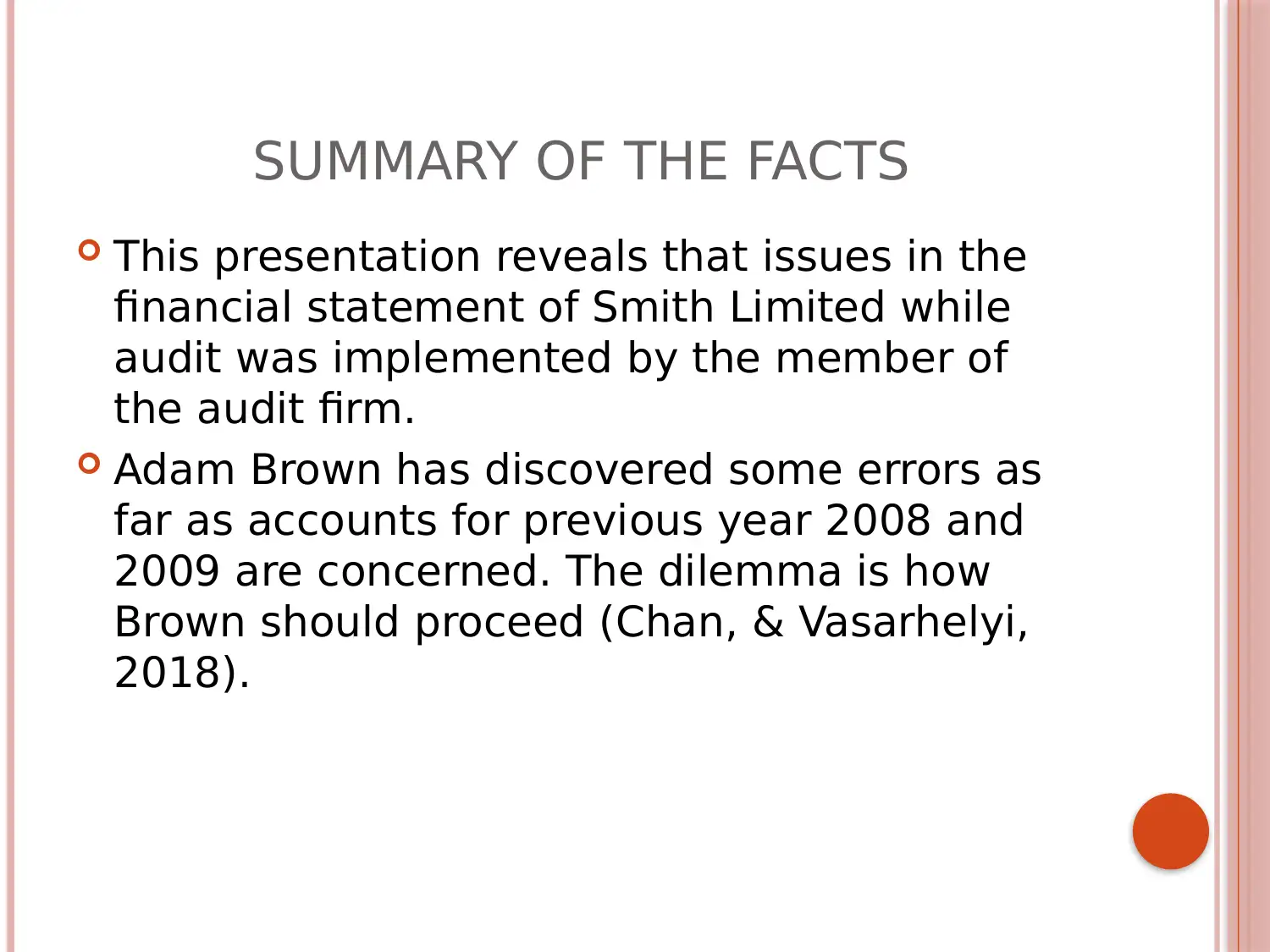

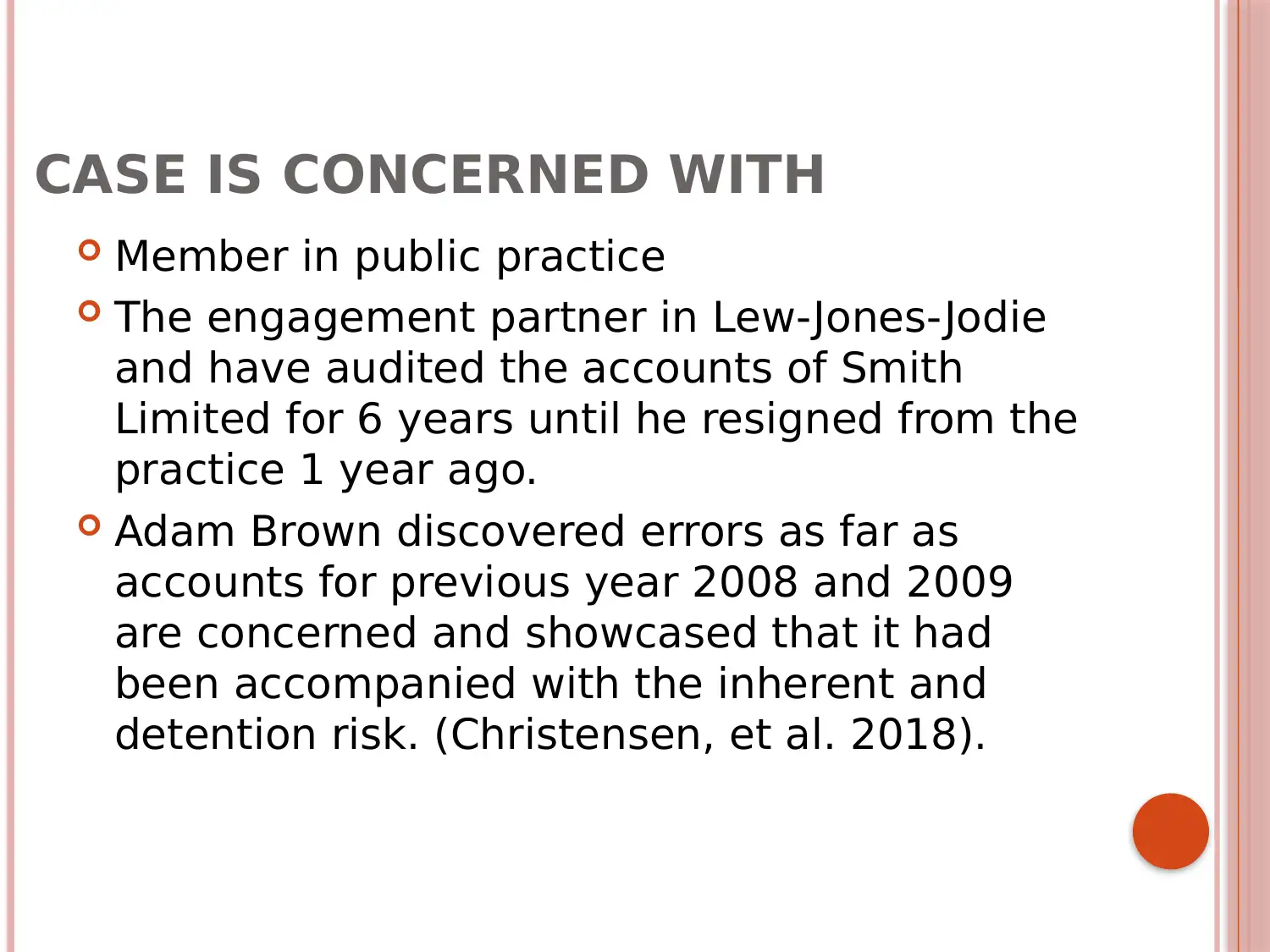

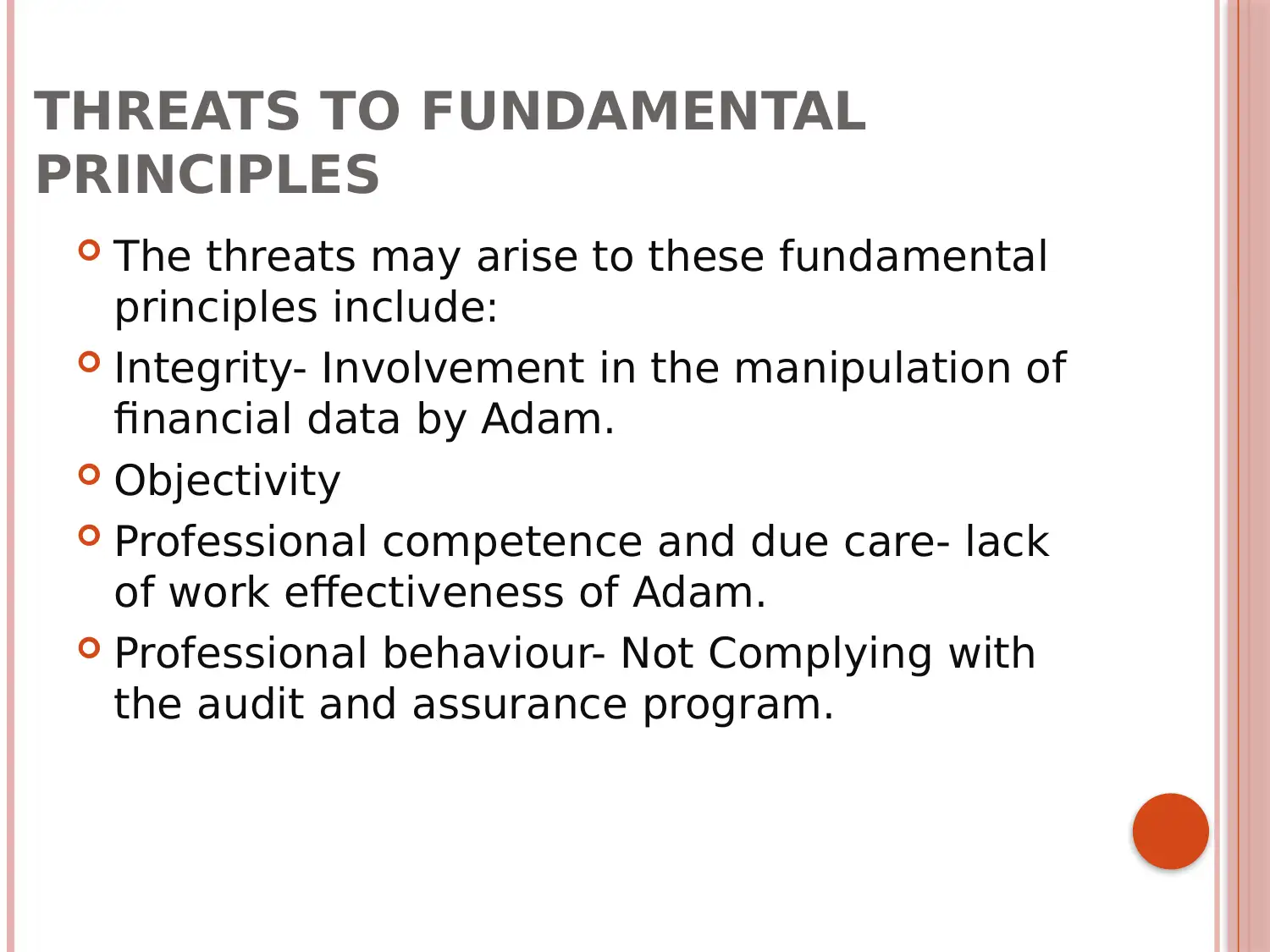

This case study analyzes the ethical dilemmas faced by an auditor, Adam Brown, who discovers errors in the previously audited financial statements of Smith Limited for the years 2008 and 2009. The core issues revolve around threats to fundamental principles such as integrity, objectivity, professional competence, and professional behavior. The case highlights the importance of adhering to auditing standards and ethical guidelines, particularly regarding communication with previous auditors and maintaining independence. Adam Brown is advised to involve the management of Smith Limited in addressing the discrepancies and facilitating communication with the previous auditor to ensure transparency and avoid any self-review or familiarity threats. The study emphasizes the need for auditors to exercise due diligence and professional skepticism in their work.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.