FIN200 Trimester 2 2018: SML, CML, Minimum Variance & CAPM Analysis

VerifiedAdded on 2023/06/08

|12

|958

|375

Report

AI Summary

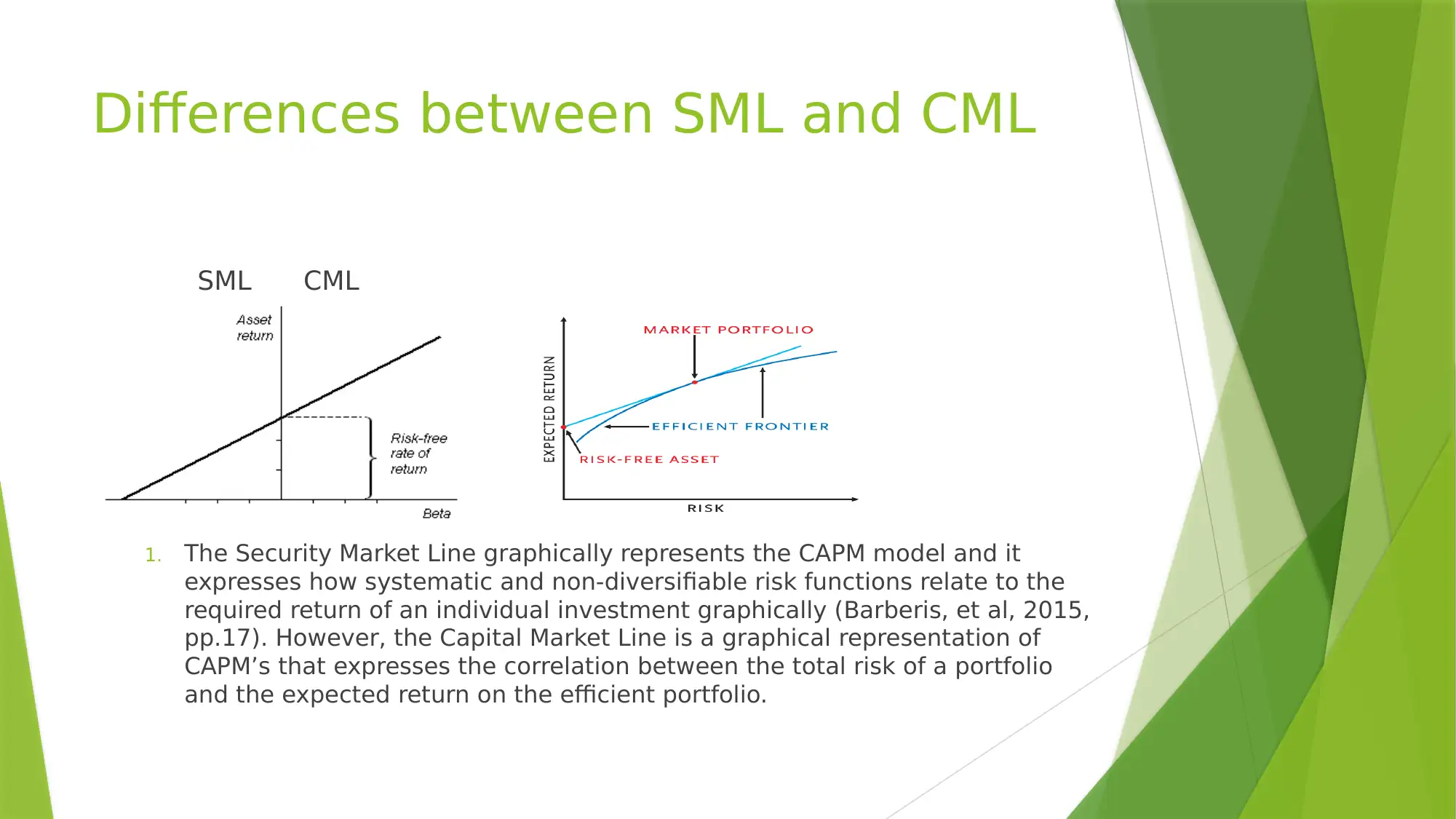

This report provides a comprehensive analysis of corporate financial management concepts, focusing on the Security Market Line (SML), Capital Market Line (CML), and the Capital Asset Pricing Model (CAPM). It elucidates the key differences between SML and CML, highlighting that SML graphically represents the CAPM model using beta to measure risk, while CML represents the correlation between total portfolio risk and expected return using standard deviation. The report also emphasizes the importance of minimum variance portfolios in minimizing price volatility and hedging against losses, especially given the difficulty in predicting future returns. Furthermore, it underscores the relevance of the CAPM equation in measuring the required rate of return on investment, citing its graphical representation, theoretical derivation, and explicit consideration of systematic risk compared to other models like the dividend growth model and WACC. The report concludes that CAPM offers a more relevant approach for assessing investment returns and managing risks in corporate finance.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.