FIN200 Assignment: Analyzing SML, CML, Minimum Variance, and CAPM

VerifiedAdded on 2023/06/07

|13

|2810

|369

Report

AI Summary

This report provides a comprehensive analysis of key concepts in corporate financial accounting, including the Security Market Line (SML), Capital Market Line (CML), minimum variance portfolios, and the Capital Asset Pricing Model (CAPM). It elucidates the differences between SML and CML, highlighting their graphical representations and risk measurement methodologies. The report also explores the importance of minimum variance portfolios in mitigating risk through diversification and hedging strategies. Furthermore, it justifies the relevance of the CAPM equation in calculating the required rate of return by considering both the time value of money and risk premium, offering insights into investment decision-making processes.

CORPORATE FINANCIAL ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

In the world of technology and advancements, the share market is one of the most dynamic fields

affected by the forces of demand and supply (Adelaja, 2015).

For the fruitful investment decisions to be made in the market, it is important that one should

have a clear idea about the forces of market. There is a much known concept called portfolio

analysis. Analysis of stocks on an individual basis and analysis of the entire portfolio is

important for the investor's decision making as investors expect returns and returns are possible

only when the market is rising or the economy is growing and a complete idea is available to the

investors. However, the analysis of the market is a broad concept that makes use of various other

concepts such as CAPM, CML, CAL and SML discussed in details below.

In the world of technology and advancements, the share market is one of the most dynamic fields

affected by the forces of demand and supply (Adelaja, 2015).

For the fruitful investment decisions to be made in the market, it is important that one should

have a clear idea about the forces of market. There is a much known concept called portfolio

analysis. Analysis of stocks on an individual basis and analysis of the entire portfolio is

important for the investor's decision making as investors expect returns and returns are possible

only when the market is rising or the economy is growing and a complete idea is available to the

investors. However, the analysis of the market is a broad concept that makes use of various other

concepts such as CAPM, CML, CAL and SML discussed in details below.

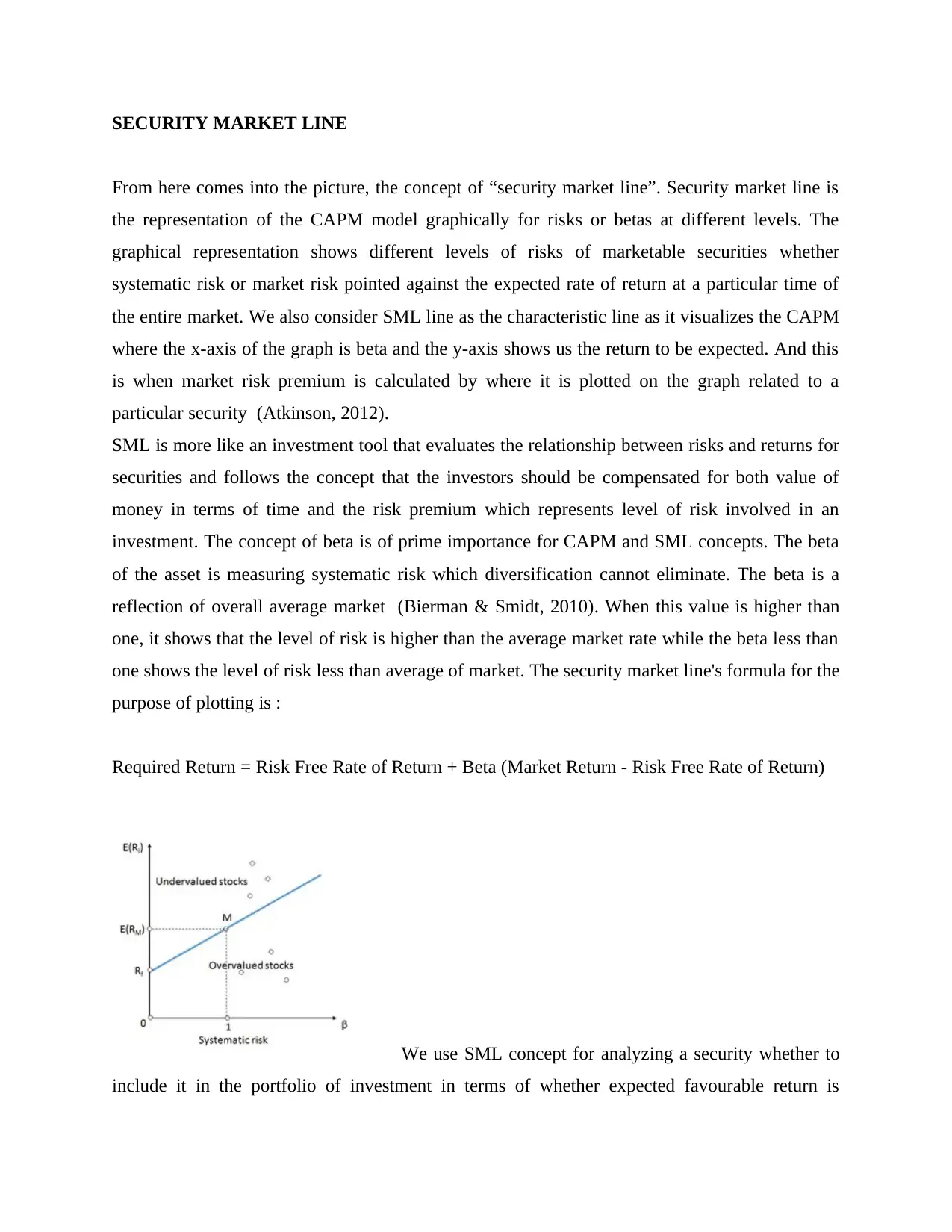

SECURITY MARKET LINE

From here comes into the picture, the concept of “security market line”. Security market line is

the representation of the CAPM model graphically for risks or betas at different levels. The

graphical representation shows different levels of risks of marketable securities whether

systematic risk or market risk pointed against the expected rate of return at a particular time of

the entire market. We also consider SML line as the characteristic line as it visualizes the CAPM

where the x-axis of the graph is beta and the y-axis shows us the return to be expected. And this

is when market risk premium is calculated by where it is plotted on the graph related to a

particular security (Atkinson, 2012).

SML is more like an investment tool that evaluates the relationship between risks and returns for

securities and follows the concept that the investors should be compensated for both value of

money in terms of time and the risk premium which represents level of risk involved in an

investment. The concept of beta is of prime importance for CAPM and SML concepts. The beta

of the asset is measuring systematic risk which diversification cannot eliminate. The beta is a

reflection of overall average market (Bierman & Smidt, 2010). When this value is higher than

one, it shows that the level of risk is higher than the average market rate while the beta less than

one shows the level of risk less than average of market. The security market line's formula for the

purpose of plotting is :

Required Return = Risk Free Rate of Return + Beta (Market Return - Risk Free Rate of Return)

We use SML concept for analyzing a security whether to

include it in the portfolio of investment in terms of whether expected favourable return is

From here comes into the picture, the concept of “security market line”. Security market line is

the representation of the CAPM model graphically for risks or betas at different levels. The

graphical representation shows different levels of risks of marketable securities whether

systematic risk or market risk pointed against the expected rate of return at a particular time of

the entire market. We also consider SML line as the characteristic line as it visualizes the CAPM

where the x-axis of the graph is beta and the y-axis shows us the return to be expected. And this

is when market risk premium is calculated by where it is plotted on the graph related to a

particular security (Atkinson, 2012).

SML is more like an investment tool that evaluates the relationship between risks and returns for

securities and follows the concept that the investors should be compensated for both value of

money in terms of time and the risk premium which represents level of risk involved in an

investment. The concept of beta is of prime importance for CAPM and SML concepts. The beta

of the asset is measuring systematic risk which diversification cannot eliminate. The beta is a

reflection of overall average market (Bierman & Smidt, 2010). When this value is higher than

one, it shows that the level of risk is higher than the average market rate while the beta less than

one shows the level of risk less than average of market. The security market line's formula for the

purpose of plotting is :

Required Return = Risk Free Rate of Return + Beta (Market Return - Risk Free Rate of Return)

We use SML concept for analyzing a security whether to

include it in the portfolio of investment in terms of whether expected favourable return is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

received or not against its risk level. When the security is plotted above the SML, the security is

considered to be undervalued because that means that the security offers a return which is way

greater than its risk (Dayananda, Irons, Harrison, Herbohn, & Rowland, 2008). On the other

hand, in case of vice - versa, the stock is considered as overvalued in terms of price because in

that case, the expected return doesn't exceed the risks involved. The frequent use of SML is in

comparing the two securities of similar nature that offers almost same return in order ro estimate

that which security involves the minimum level of risk involved in relation to expected return. In

a similar way, two stocks are compared with equal risk that which security offers highest

expected return.

CAPITAL MARKET LINE

We shall now have an understanding about the capital market line (CML) under the CAPM

concept that is used to identify the tradeoffs between return and risk for efficient portfolios. The

concept is a representation of portfolios that combines the risk free return rate in an optimal

manner and the market portfolio of assets with allot of risks. All the investors under the CAPM

concept choose a point in equilibrium on the CML, by the tools of lending and borrowing at the

freely risky rate, as this would be maximizing the return given the risk level. The CML is the line

that connects the rate of return free of risk with the tangent point on the efficient frontier of

portfolios at optimum level that for a particular risk level offers the maximum expected return or

for a given expected return offers the lowest risk level. The portfolios with most favorable trade

off between the risks or variances and expected return lies on the line. The tangent point is

known as the market portfolio which is considered as optimal one for risky securities. Following

the assumption of mean variance analysis, the potential investors look for maximizing their

return expected for a given level of risk and that there is a freely risky return - meaning all

investors will choose the portfolios that lies on the CML (Donohue, 2015).

Taking references from Tobin's separation theory, identification of market portfolio is one thing

while combining the risk free assets and that market portfolio is another thing. An investor would

consider investing in either risk free assets or some sort of combination of it with the portfolio of

the market depending on the risk fear (Girard, 2014).

considered to be undervalued because that means that the security offers a return which is way

greater than its risk (Dayananda, Irons, Harrison, Herbohn, & Rowland, 2008). On the other

hand, in case of vice - versa, the stock is considered as overvalued in terms of price because in

that case, the expected return doesn't exceed the risks involved. The frequent use of SML is in

comparing the two securities of similar nature that offers almost same return in order ro estimate

that which security involves the minimum level of risk involved in relation to expected return. In

a similar way, two stocks are compared with equal risk that which security offers highest

expected return.

CAPITAL MARKET LINE

We shall now have an understanding about the capital market line (CML) under the CAPM

concept that is used to identify the tradeoffs between return and risk for efficient portfolios. The

concept is a representation of portfolios that combines the risk free return rate in an optimal

manner and the market portfolio of assets with allot of risks. All the investors under the CAPM

concept choose a point in equilibrium on the CML, by the tools of lending and borrowing at the

freely risky rate, as this would be maximizing the return given the risk level. The CML is the line

that connects the rate of return free of risk with the tangent point on the efficient frontier of

portfolios at optimum level that for a particular risk level offers the maximum expected return or

for a given expected return offers the lowest risk level. The portfolios with most favorable trade

off between the risks or variances and expected return lies on the line. The tangent point is

known as the market portfolio which is considered as optimal one for risky securities. Following

the assumption of mean variance analysis, the potential investors look for maximizing their

return expected for a given level of risk and that there is a freely risky return - meaning all

investors will choose the portfolios that lies on the CML (Donohue, 2015).

Taking references from Tobin's separation theory, identification of market portfolio is one thing

while combining the risk free assets and that market portfolio is another thing. An investor would

consider investing in either risk free assets or some sort of combination of it with the portfolio of

the market depending on the risk fear (Girard, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

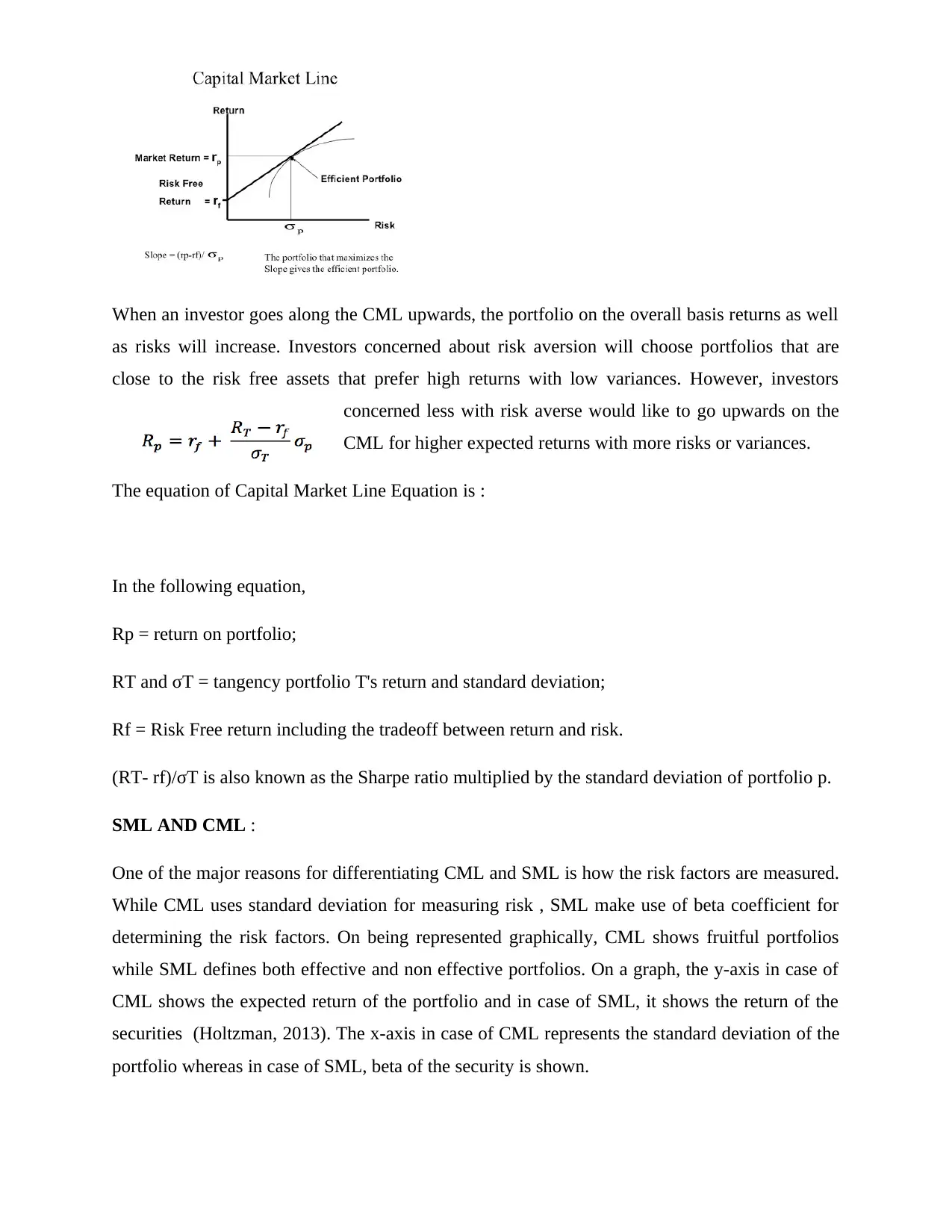

When an investor goes along the CML upwards, the portfolio on the overall basis returns as well

as risks will increase. Investors concerned about risk aversion will choose portfolios that are

close to the risk free assets that prefer high returns with low variances. However, investors

concerned less with risk averse would like to go upwards on the

CML for higher expected returns with more risks or variances.

The equation of Capital Market Line Equation is :

In the following equation,

Rp = return on portfolio;

RT and σT = tangency portfolio T's return and standard deviation;

Rf = Risk Free return including the tradeoff between return and risk.

(RT- rf)/σT is also known as the Sharpe ratio multiplied by the standard deviation of portfolio p.

SML AND CML :

One of the major reasons for differentiating CML and SML is how the risk factors are measured.

While CML uses standard deviation for measuring risk , SML make use of beta coefficient for

determining the risk factors. On being represented graphically, CML shows fruitful portfolios

while SML defines both effective and non effective portfolios. On a graph, the y-axis in case of

CML shows the expected return of the portfolio and in case of SML, it shows the return of the

securities (Holtzman, 2013). The x-axis in case of CML represents the standard deviation of the

portfolio whereas in case of SML, beta of the security is shown.

as risks will increase. Investors concerned about risk aversion will choose portfolios that are

close to the risk free assets that prefer high returns with low variances. However, investors

concerned less with risk averse would like to go upwards on the

CML for higher expected returns with more risks or variances.

The equation of Capital Market Line Equation is :

In the following equation,

Rp = return on portfolio;

RT and σT = tangency portfolio T's return and standard deviation;

Rf = Risk Free return including the tradeoff between return and risk.

(RT- rf)/σT is also known as the Sharpe ratio multiplied by the standard deviation of portfolio p.

SML AND CML :

One of the major reasons for differentiating CML and SML is how the risk factors are measured.

While CML uses standard deviation for measuring risk , SML make use of beta coefficient for

determining the risk factors. On being represented graphically, CML shows fruitful portfolios

while SML defines both effective and non effective portfolios. On a graph, the y-axis in case of

CML shows the expected return of the portfolio and in case of SML, it shows the return of the

securities (Holtzman, 2013). The x-axis in case of CML represents the standard deviation of the

portfolio whereas in case of SML, beta of the security is shown.

CML shows the risk free assets and market portfolio while SML determines the other factors of

security. SML shows the expected returns on an individual basis in case of all securities unlike

CML. While CML determines the return or risks for efficient portfolios, SML determines the

return or risks associated with individual stocks. However, SML can be a tool valued enough for

valuation of equity and comparison purposes; it shouldn't be use for isolation purposes as the

expected return rate over risk free return rate is not considered as the only reason for decision

making related to investment. That is why, capital market line is considered better when it comes

to measurement of risk factors (McLaney & Adril, 2016).

security. SML shows the expected returns on an individual basis in case of all securities unlike

CML. While CML determines the return or risks for efficient portfolios, SML determines the

return or risks associated with individual stocks. However, SML can be a tool valued enough for

valuation of equity and comparison purposes; it shouldn't be use for isolation purposes as the

expected return rate over risk free return rate is not considered as the only reason for decision

making related to investment. That is why, capital market line is considered better when it comes

to measurement of risk factors (McLaney & Adril, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MINIMUM VARIANCE PORTFOLIO

As the name suggests, minimum variance portfolio is a portfolio with diversified securities that

consists of risky assets on an individual basis, which are hedged in case they are traded together

which in return results in the lowest possible risk for the expected rate of return. This refers to

the leveraging of the risk in each asset with an offsetting investment which, thus, hedges the total

risk of the portfolio for the level of accepted risk in relation to the expected rate of return of the

portfolio. Putting the money in a minimum variance portfolio would be risky if it is traded

individually (Menifield, 2014). However, when traded through a portfolio, the risk is hedged.

The name has been originated from the Markowitz Portfolio Theory which shows us that the risk

can be replaced or eliminated by the volatility and therefore, less risk in investment correlates

with less volatility variance.

To construct a minimum variance portfolio, an investor should consider a pairing of low volatile

money investments or a combination of money investments that are volatile and have a low link

between each other. The second case of portfolio is preferred more while building minimum

variance portfolios (Peterson & Fabozzi, 2012).

Talking about minimum variance portfolio model, we can consider categories of mutual funds

that have a low link with each other. This can be explained through an example: 40 percent S&P

500 index fund, 20 percent emerging markets stock fund, 10 percent small cap stock fund and 30

percent bond index fund. While the first three are volatile in nature, all the four are correlated

with each other on a lower level. Except for bond index fund, all the four when combined

together gives lower volatility than what it gives on an individual basis.

Investments having a Lower correlation are headed under those investments that perform

differently given the market conditions and the political environment is constant. This is one of

the examples of diversification. When an investor wants to expand his portfolio through

diversification, their prime motive is to deduct volatility and this forms the basis of the minimum

variance portfolio (Rivenbark, Vogt, & Marlowe, 2009). One of the most common examples of

minimum variance portfolio is a combination of a bond mutual fund and a stock mutual fund. In

that case, when prices of stock rises, bond prices may show a slight negativity whereas when

stock prices fell, bond prices usually rise. This is because usually stocks and bonds moves in the

As the name suggests, minimum variance portfolio is a portfolio with diversified securities that

consists of risky assets on an individual basis, which are hedged in case they are traded together

which in return results in the lowest possible risk for the expected rate of return. This refers to

the leveraging of the risk in each asset with an offsetting investment which, thus, hedges the total

risk of the portfolio for the level of accepted risk in relation to the expected rate of return of the

portfolio. Putting the money in a minimum variance portfolio would be risky if it is traded

individually (Menifield, 2014). However, when traded through a portfolio, the risk is hedged.

The name has been originated from the Markowitz Portfolio Theory which shows us that the risk

can be replaced or eliminated by the volatility and therefore, less risk in investment correlates

with less volatility variance.

To construct a minimum variance portfolio, an investor should consider a pairing of low volatile

money investments or a combination of money investments that are volatile and have a low link

between each other. The second case of portfolio is preferred more while building minimum

variance portfolios (Peterson & Fabozzi, 2012).

Talking about minimum variance portfolio model, we can consider categories of mutual funds

that have a low link with each other. This can be explained through an example: 40 percent S&P

500 index fund, 20 percent emerging markets stock fund, 10 percent small cap stock fund and 30

percent bond index fund. While the first three are volatile in nature, all the four are correlated

with each other on a lower level. Except for bond index fund, all the four when combined

together gives lower volatility than what it gives on an individual basis.

Investments having a Lower correlation are headed under those investments that perform

differently given the market conditions and the political environment is constant. This is one of

the examples of diversification. When an investor wants to expand his portfolio through

diversification, their prime motive is to deduct volatility and this forms the basis of the minimum

variance portfolio (Rivenbark, Vogt, & Marlowe, 2009). One of the most common examples of

minimum variance portfolio is a combination of a bond mutual fund and a stock mutual fund. In

that case, when prices of stock rises, bond prices may show a slight negativity whereas when

stock prices fell, bond prices usually rise. This is because usually stocks and bonds moves in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

same direction but they have a low correlation when it comes to performance. With minimum

variance portfolio, an investor can efficiently combine the investments together that are risky and

can still manage to achieve high returns without bearing the high risk level (Robinson, 2014).

variance portfolio, an investor can efficiently combine the investments together that are risky and

can still manage to achieve high returns without bearing the high risk level (Robinson, 2014).

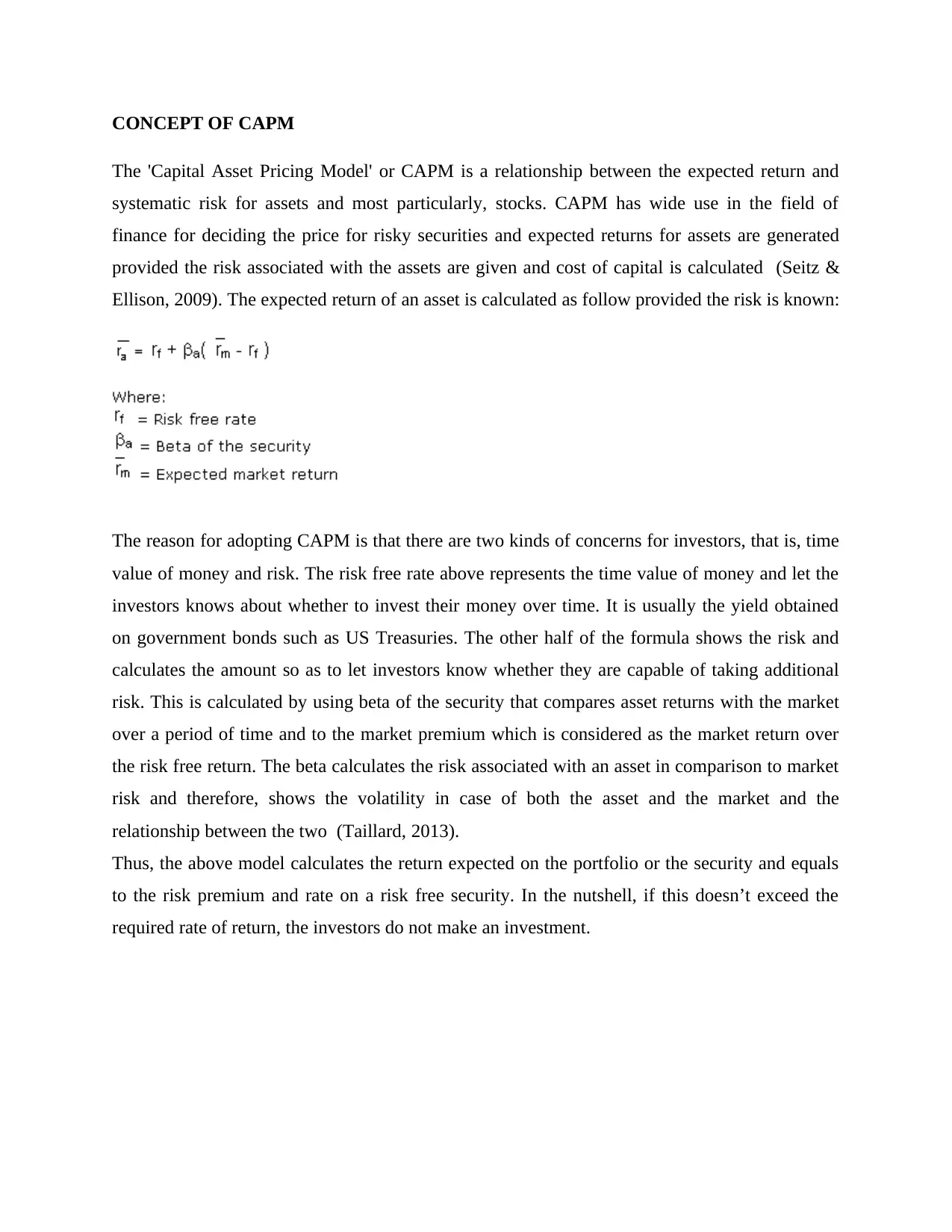

CONCEPT OF CAPM

The 'Capital Asset Pricing Model' or CAPM is a relationship between the expected return and

systematic risk for assets and most particularly, stocks. CAPM has wide use in the field of

finance for deciding the price for risky securities and expected returns for assets are generated

provided the risk associated with the assets are given and cost of capital is calculated (Seitz &

Ellison, 2009). The expected return of an asset is calculated as follow provided the risk is known:

The reason for adopting CAPM is that there are two kinds of concerns for investors, that is, time

value of money and risk. The risk free rate above represents the time value of money and let the

investors knows about whether to invest their money over time. It is usually the yield obtained

on government bonds such as US Treasuries. The other half of the formula shows the risk and

calculates the amount so as to let investors know whether they are capable of taking additional

risk. This is calculated by using beta of the security that compares asset returns with the market

over a period of time and to the market premium which is considered as the market return over

the risk free return. The beta calculates the risk associated with an asset in comparison to market

risk and therefore, shows the volatility in case of both the asset and the market and the

relationship between the two (Taillard, 2013).

Thus, the above model calculates the return expected on the portfolio or the security and equals

to the risk premium and rate on a risk free security. In the nutshell, if this doesn’t exceed the

required rate of return, the investors do not make an investment.

The 'Capital Asset Pricing Model' or CAPM is a relationship between the expected return and

systematic risk for assets and most particularly, stocks. CAPM has wide use in the field of

finance for deciding the price for risky securities and expected returns for assets are generated

provided the risk associated with the assets are given and cost of capital is calculated (Seitz &

Ellison, 2009). The expected return of an asset is calculated as follow provided the risk is known:

The reason for adopting CAPM is that there are two kinds of concerns for investors, that is, time

value of money and risk. The risk free rate above represents the time value of money and let the

investors knows about whether to invest their money over time. It is usually the yield obtained

on government bonds such as US Treasuries. The other half of the formula shows the risk and

calculates the amount so as to let investors know whether they are capable of taking additional

risk. This is calculated by using beta of the security that compares asset returns with the market

over a period of time and to the market premium which is considered as the market return over

the risk free return. The beta calculates the risk associated with an asset in comparison to market

risk and therefore, shows the volatility in case of both the asset and the market and the

relationship between the two (Taillard, 2013).

Thus, the above model calculates the return expected on the portfolio or the security and equals

to the risk premium and rate on a risk free security. In the nutshell, if this doesn’t exceed the

required rate of return, the investors do not make an investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

WHY CAPM?

"The CAPM is an important area of financial management. In fact, it has even been suggested

that finance only became ‘a fully-fledged, scientific discipline’ when William Sharpe published

his derivation of the CAPM in 1986” (Shapiro, 2007).

Being a popular concept for more than 40 years, the reasons of choosing CAPM formulas over

other formulas can be explained as below:

A single systematic risk is considered which reflects the reality of the diversified

portfolios in which investors have an interest and an unsystematic risk is significantly

eliminated (Siciliano, 2015).

It has derived from the relationship between systematic risk and required return through a

theoretical approach which is frequently researched about and tested on a regular basis.

Generally, for the calculation of cost of equity, the CAPM approach is better than the

dividend growth model (DGM) as it considers a company’s systematic risk level in

relation to the stock market wholly.

For the use of it in investment appraisal, it is justifiably better than WACC approach in

providing discount rates.

"The CAPM is an important area of financial management. In fact, it has even been suggested

that finance only became ‘a fully-fledged, scientific discipline’ when William Sharpe published

his derivation of the CAPM in 1986” (Shapiro, 2007).

Being a popular concept for more than 40 years, the reasons of choosing CAPM formulas over

other formulas can be explained as below:

A single systematic risk is considered which reflects the reality of the diversified

portfolios in which investors have an interest and an unsystematic risk is significantly

eliminated (Siciliano, 2015).

It has derived from the relationship between systematic risk and required return through a

theoretical approach which is frequently researched about and tested on a regular basis.

Generally, for the calculation of cost of equity, the CAPM approach is better than the

dividend growth model (DGM) as it considers a company’s systematic risk level in

relation to the stock market wholly.

For the use of it in investment appraisal, it is justifiably better than WACC approach in

providing discount rates.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONCLUSION

The researchers have always found that CAPM has been able to stand up well against the

criticisms although such critics a have been increasing since last few years. Until and unless a

better concept is coming into existence, the CAPM remains one of the most useful formulas in

the field of financial management.

The researchers have always found that CAPM has been able to stand up well against the

criticisms although such critics a have been increasing since last few years. Until and unless a

better concept is coming into existence, the CAPM remains one of the most useful formulas in

the field of financial management.

Bibliography

Adelaja, T. (2015). Capital Budgeting: Investment Appraisal Techniques Under Certainty.

Chicago: CreateSpace Independent Publishing Platform .

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Bierman, H., & Smidt, S. (2010). The Capital Budgeting Decision. Boston: Routledge.

Dayananda, D., Irons, R., Harrison, S., Herbohn, J., & Rowland, P. (2008). Capital Budgeting:

Financial Appraisal of Investment Projects. Cambridge: Cambridge University Press.

Donohue, R. (2015). An introduction to-- cashflow analysis. Mission Viejo, CA: Regent School

Press.

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

Holtzman, M. (2013). Managerial Accounting For Dummies. Hoboken, NJ: Wiley.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Menifield, C. E. (2014). The Basics of Public Budgeting and Financial Management: A

Handbook for Academics and Practitioners. Lanham, Md.: University Press of America.

Peterson, P. P., & Fabozzi, F. J. (2012). Capital Budgeting. New York, NY: Wiley.

Rivenbark, W. C., Vogt, J., & Marlowe, J. (2009). Capital Budgeting and Finance: A Guide for

Local Governments. Washington, D.C.: ICMA Press.

Robinson, T. (2014). Business accounting. New York, NY: Prentice Hall.

Seitz, N., & Ellison, M. (2009). Capital Budgeting and Long-Term Financing Decisions. New

York: Thomson Learning.

Shapiro, A. C. (2007). Capital Budgeting and Investment Analysis. New Jersey: Wiley.

Adelaja, T. (2015). Capital Budgeting: Investment Appraisal Techniques Under Certainty.

Chicago: CreateSpace Independent Publishing Platform .

Atkinson, A. A. (2012). Management accounting. Upper Saddle River, N.J.: Paerson.

Bierman, H., & Smidt, S. (2010). The Capital Budgeting Decision. Boston: Routledge.

Dayananda, D., Irons, R., Harrison, S., Herbohn, J., & Rowland, P. (2008). Capital Budgeting:

Financial Appraisal of Investment Projects. Cambridge: Cambridge University Press.

Donohue, R. (2015). An introduction to-- cashflow analysis. Mission Viejo, CA: Regent School

Press.

Girard, S. L. (2014). Business finance basics. Pompton Plains, NJ: Career Press.

Holtzman, M. (2013). Managerial Accounting For Dummies. Hoboken, NJ: Wiley.

McLaney, E., & Adril, D. P. (2016). Accounting and Finance: An Introduction. United

Kingdom: Pearson.

Menifield, C. E. (2014). The Basics of Public Budgeting and Financial Management: A

Handbook for Academics and Practitioners. Lanham, Md.: University Press of America.

Peterson, P. P., & Fabozzi, F. J. (2012). Capital Budgeting. New York, NY: Wiley.

Rivenbark, W. C., Vogt, J., & Marlowe, J. (2009). Capital Budgeting and Finance: A Guide for

Local Governments. Washington, D.C.: ICMA Press.

Robinson, T. (2014). Business accounting. New York, NY: Prentice Hall.

Seitz, N., & Ellison, M. (2009). Capital Budgeting and Long-Term Financing Decisions. New

York: Thomson Learning.

Shapiro, A. C. (2007). Capital Budgeting and Investment Analysis. New Jersey: Wiley.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.