Business Development: Operation Management at Snowham Airport

VerifiedAdded on 2023/01/12

|20

|3576

|36

Report

AI Summary

This report presents a comprehensive analysis of operation management challenges and solutions, using the Snowham International Airport as a detailed case study. The report examines several key areas, including coffee procurement strategies for Harvey Talbot, the layout and operational aspects of a new Juicemasters outlet, staff planning for the Turista call center, an analysis of Sycamore Security Systems, baggage handling problems, and the acquisition of a new fire engine for the airport. Each section includes detailed calculations, alternative solutions, and recommendations for improving efficiency and reducing costs. The report utilizes various business development concepts such as Economic Order Quantity (EOQ) to optimize operations and enhance profitability across different departments within the airport's ecosystem. It provides valuable insights for business development, project management, and operational efficiency.

OPERATION

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................3

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

Harvey Talbot – coffee procurement:.....................................................................................4

The new Juicemasters outlet:..................................................................................................6

Staff planning for the Turista call centre:...............................................................................8

Sycamore Security Systems:................................................................................................10

Baggage handling problems at Snowham Airport:..............................................................12

A new fire engine for the airport:.........................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

EXECUTIVE SUMMARY.............................................................................................................3

INTRODUCTION...........................................................................................................................4

MAIN BODY...................................................................................................................................4

Harvey Talbot – coffee procurement:.....................................................................................4

The new Juicemasters outlet:..................................................................................................6

Staff planning for the Turista call centre:...............................................................................8

Sycamore Security Systems:................................................................................................10

Baggage handling problems at Snowham Airport:..............................................................12

A new fire engine for the airport:.........................................................................................14

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

EXECUTIVE SUMMARY

Operation Management is essential element which help to define the core objectives of a

project and effective execution of all task related to project. This study summaries all the major

aspects of project management with help of multiple topics connected with case study of

Snowham International Airport. Each topic consist of specific issue which is to be solved for

improving overall operations. In study each issue is thoroughly analysed to provide effective

recommendations and identify issues in existing processes adopted.

Operation Management is essential element which help to define the core objectives of a

project and effective execution of all task related to project. This study summaries all the major

aspects of project management with help of multiple topics connected with case study of

Snowham International Airport. Each topic consist of specific issue which is to be solved for

improving overall operations. In study each issue is thoroughly analysed to provide effective

recommendations and identify issues in existing processes adopted.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

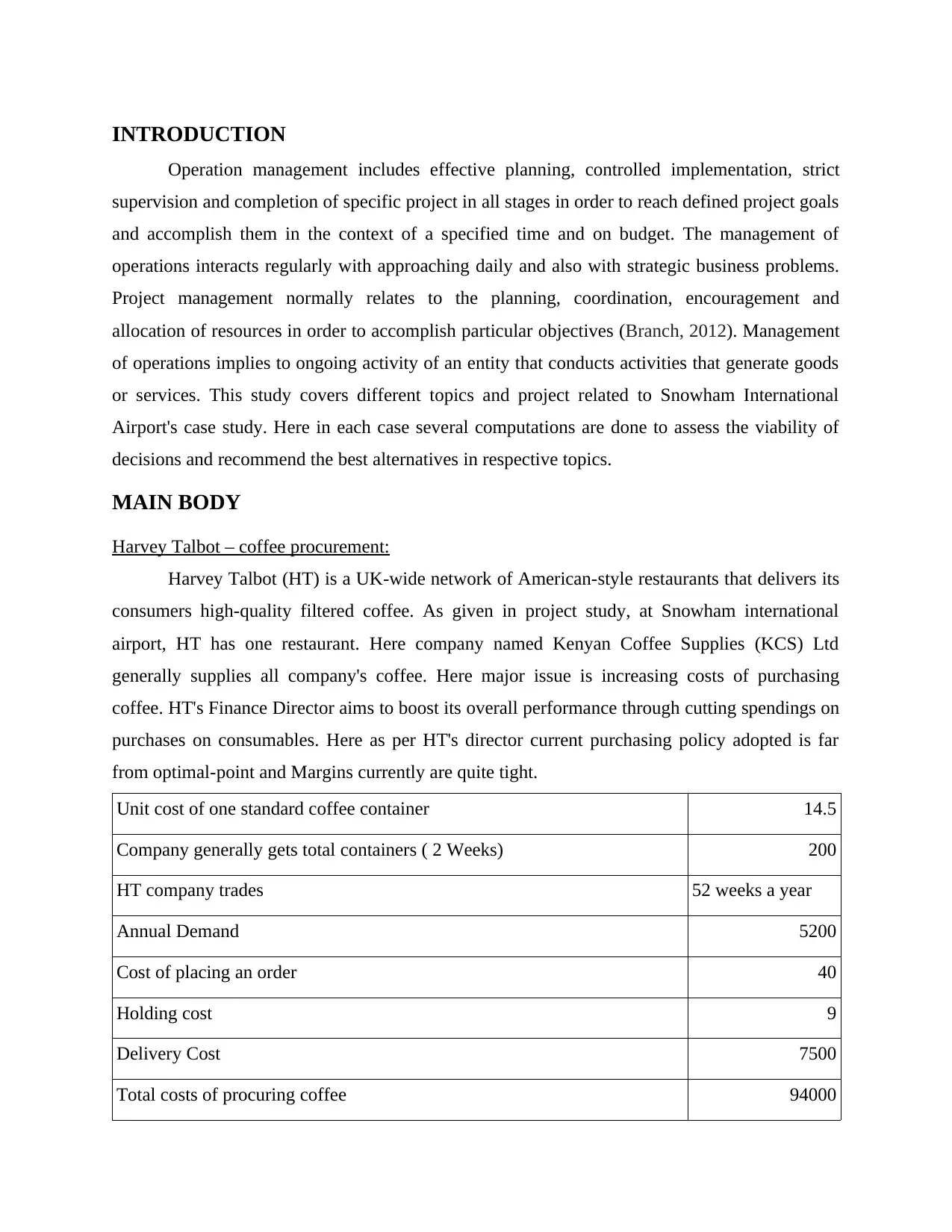

INTRODUCTION

Operation management includes effective planning, controlled implementation, strict

supervision and completion of specific project in all stages in order to reach defined project goals

and accomplish them in the context of a specified time and on budget. The management of

operations interacts regularly with approaching daily and also with strategic business problems.

Project management normally relates to the planning, coordination, encouragement and

allocation of resources in order to accomplish particular objectives (Branch, 2012). Management

of operations implies to ongoing activity of an entity that conducts activities that generate goods

or services. This study covers different topics and project related to Snowham International

Airport's case study. Here in each case several computations are done to assess the viability of

decisions and recommend the best alternatives in respective topics.

MAIN BODY

Harvey Talbot – coffee procurement:

Harvey Talbot (HT) is a UK-wide network of American-style restaurants that delivers its

consumers high-quality filtered coffee. As given in project study, at Snowham international

airport, HT has one restaurant. Here company named Kenyan Coffee Supplies (KCS) Ltd

generally supplies all company's coffee. Here major issue is increasing costs of purchasing

coffee. HT's Finance Director aims to boost its overall performance through cutting spendings on

purchases on consumables. Here as per HT's director current purchasing policy adopted is far

from optimal-point and Margins currently are quite tight.

Unit cost of one standard coffee container 14.5

Company generally gets total containers ( 2 Weeks) 200

HT company trades 52 weeks a year

Annual Demand 5200

Cost of placing an order 40

Holding cost 9

Delivery Cost 7500

Total costs of procuring coffee 94000

Operation management includes effective planning, controlled implementation, strict

supervision and completion of specific project in all stages in order to reach defined project goals

and accomplish them in the context of a specified time and on budget. The management of

operations interacts regularly with approaching daily and also with strategic business problems.

Project management normally relates to the planning, coordination, encouragement and

allocation of resources in order to accomplish particular objectives (Branch, 2012). Management

of operations implies to ongoing activity of an entity that conducts activities that generate goods

or services. This study covers different topics and project related to Snowham International

Airport's case study. Here in each case several computations are done to assess the viability of

decisions and recommend the best alternatives in respective topics.

MAIN BODY

Harvey Talbot – coffee procurement:

Harvey Talbot (HT) is a UK-wide network of American-style restaurants that delivers its

consumers high-quality filtered coffee. As given in project study, at Snowham international

airport, HT has one restaurant. Here company named Kenyan Coffee Supplies (KCS) Ltd

generally supplies all company's coffee. Here major issue is increasing costs of purchasing

coffee. HT's Finance Director aims to boost its overall performance through cutting spendings on

purchases on consumables. Here as per HT's director current purchasing policy adopted is far

from optimal-point and Margins currently are quite tight.

Unit cost of one standard coffee container 14.5

Company generally gets total containers ( 2 Weeks) 200

HT company trades 52 weeks a year

Annual Demand 5200

Cost of placing an order 40

Holding cost 9

Delivery Cost 7500

Total costs of procuring coffee 94000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Calculation of annual aggregate cost:

Cost of one container ( 14.5 * 100 * 52 weeks) 75400

Cost of placing order (40 * 100 * 52 weeks) 208000

Holding cost (9 * 100 *52 weeks) 46800

Delivery Cost 7500

Cost of Procuring Coffee 94000

Total Annual Cost 431700

First Alternative:

Under first alternative, it is suggested by director that ordering will be more cost efficient

in case EOQ method is applied. The purpose of EOQ method is to determine the optimum figure

of units to be order. A company could reduce its unit acquisition, distribution, and storage costs.

This is effective approach which can minimise the overall cost by identifying optimal-point for

order (Battini, Persona and Sgarbossa, 2014). Following are merits and demerits of such

alternative, as follows:

Merit: Placing order as per EOQ is more systematic method also it will help company to

minimise overall inventory cost.

Demerit: EOQ is technical method which require calculations but in practical life it is not easy to

assess accurate EOQ due to other contingent factors. Also fluctuation in annual demand affects

EOQ.

Economic Order Quantity:

EOQ = √(2 * D * S)/ H

= √ ( 2 * 5200 * 40 ) / 9

= √ 416000÷9

= √ 46222.22

= 214.99 or 215 containers

Total cost based on EOQ alternative:

Cost of one container ( 14.5 * 100 * 52 weeks) 75400

Cost of placing order (40 * 100 * 52 weeks) 208000

Holding cost (9 * 100 *52 weeks) 46800

Delivery Cost 7500

Cost of Procuring Coffee 94000

Total Annual Cost 431700

First Alternative:

Under first alternative, it is suggested by director that ordering will be more cost efficient

in case EOQ method is applied. The purpose of EOQ method is to determine the optimum figure

of units to be order. A company could reduce its unit acquisition, distribution, and storage costs.

This is effective approach which can minimise the overall cost by identifying optimal-point for

order (Battini, Persona and Sgarbossa, 2014). Following are merits and demerits of such

alternative, as follows:

Merit: Placing order as per EOQ is more systematic method also it will help company to

minimise overall inventory cost.

Demerit: EOQ is technical method which require calculations but in practical life it is not easy to

assess accurate EOQ due to other contingent factors. Also fluctuation in annual demand affects

EOQ.

Economic Order Quantity:

EOQ = √(2 * D * S)/ H

= √ ( 2 * 5200 * 40 ) / 9

= √ 416000÷9

= √ 46222.22

= 214.99 or 215 containers

Total cost based on EOQ alternative:

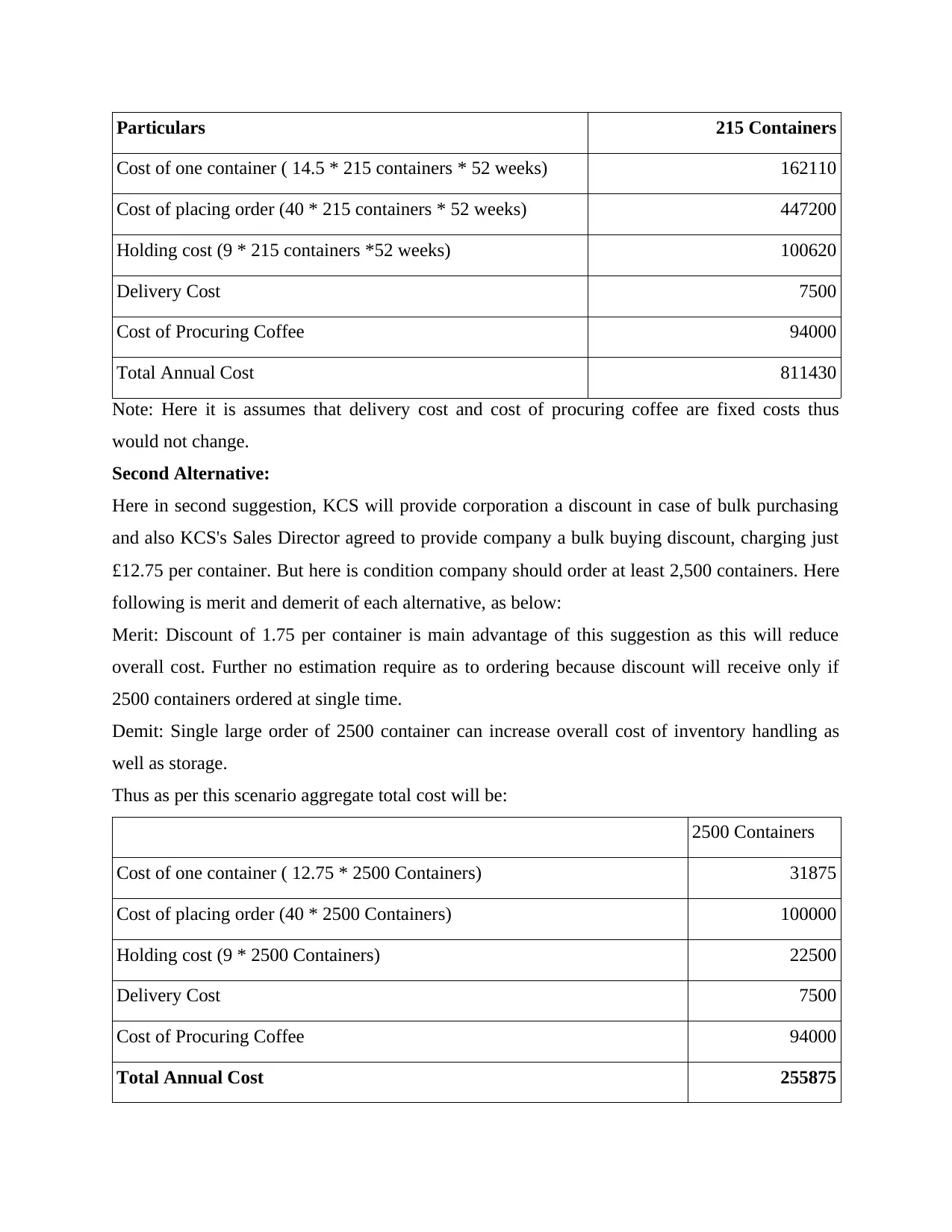

Particulars 215 Containers

Cost of one container ( 14.5 * 215 containers * 52 weeks) 162110

Cost of placing order (40 * 215 containers * 52 weeks) 447200

Holding cost (9 * 215 containers *52 weeks) 100620

Delivery Cost 7500

Cost of Procuring Coffee 94000

Total Annual Cost 811430

Note: Here it is assumes that delivery cost and cost of procuring coffee are fixed costs thus

would not change.

Second Alternative:

Here in second suggestion, KCS will provide corporation a discount in case of bulk purchasing

and also KCS's Sales Director agreed to provide company a bulk buying discount, charging just

£12.75 per container. But here is condition company should order at least 2,500 containers. Here

following is merit and demerit of each alternative, as below:

Merit: Discount of 1.75 per container is main advantage of this suggestion as this will reduce

overall cost. Further no estimation require as to ordering because discount will receive only if

2500 containers ordered at single time.

Demit: Single large order of 2500 container can increase overall cost of inventory handling as

well as storage.

Thus as per this scenario aggregate total cost will be:

2500 Containers

Cost of one container ( 12.75 * 2500 Containers) 31875

Cost of placing order (40 * 2500 Containers) 100000

Holding cost (9 * 2500 Containers) 22500

Delivery Cost 7500

Cost of Procuring Coffee 94000

Total Annual Cost 255875

Cost of one container ( 14.5 * 215 containers * 52 weeks) 162110

Cost of placing order (40 * 215 containers * 52 weeks) 447200

Holding cost (9 * 215 containers *52 weeks) 100620

Delivery Cost 7500

Cost of Procuring Coffee 94000

Total Annual Cost 811430

Note: Here it is assumes that delivery cost and cost of procuring coffee are fixed costs thus

would not change.

Second Alternative:

Here in second suggestion, KCS will provide corporation a discount in case of bulk purchasing

and also KCS's Sales Director agreed to provide company a bulk buying discount, charging just

£12.75 per container. But here is condition company should order at least 2,500 containers. Here

following is merit and demerit of each alternative, as below:

Merit: Discount of 1.75 per container is main advantage of this suggestion as this will reduce

overall cost. Further no estimation require as to ordering because discount will receive only if

2500 containers ordered at single time.

Demit: Single large order of 2500 container can increase overall cost of inventory handling as

well as storage.

Thus as per this scenario aggregate total cost will be:

2500 Containers

Cost of one container ( 12.75 * 2500 Containers) 31875

Cost of placing order (40 * 2500 Containers) 100000

Holding cost (9 * 2500 Containers) 22500

Delivery Cost 7500

Cost of Procuring Coffee 94000

Total Annual Cost 255875

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Note: Here it is assumes that delivery cost and cost of procuring coffee are fixed costs thus

would not change. Also it is assumed that single order will be placed in a year.

As per the above calculations based on suggestions it has been analysed that current

annual cost is £ 431700, if organisation consider the first alternative then annual cost will be £

811430, while as per second suggestion such amount will be £ 255875. Thus suggestion second

will be more appropriate. As cost in this alternative will be lower as compare to other one.

The new Juicemasters outlet:

Here in this section main issue is that one outlet has become vacant which is leased to

independent company named Juice-masters. The corporation is specialize in broader variety of

healthy juices and smoothies alternatives along with several cold-vegetarian snacks like

baguettes. Speciality beverages like teas/coffees are also available for consumers. Corporation

has already opened outlets in 3 other major airports. Company's Chief Executive officer is

enthusiastic regarding new outlet in Snowham. In this context following is overview of interior

of area provided as follows:

Area: 17 m x 15 m corner

2 side Storage Space

Staff Toilet Facility

2 doors and 4 windows

One Main Window

Based on above details, here is following is layout for recommended floor layout, as follows:

Queueing: For managing customers crowed, there should be two queues for making payment in

two separate single windows as well as two queue for collecting food items at main window.

Ordering: Self ordering system should be adopted here, as this system provides increase in order

accuracy and require less staff.

Delivery: In peak hours, customer will collect order from main window and during period other

than peak hours delivery will be made by staff in waiting area.

Payment Processes: Company should provide all payment alternatives like credit and debit card,

cash currency, mobile banking etc. From payment windows, customer will get token or receipt

after making payment. At the time of delivery customer will provide such token/receipt. At the

end of the day tokens and payment should be matched which can increase accuracy in entire

process.

would not change. Also it is assumed that single order will be placed in a year.

As per the above calculations based on suggestions it has been analysed that current

annual cost is £ 431700, if organisation consider the first alternative then annual cost will be £

811430, while as per second suggestion such amount will be £ 255875. Thus suggestion second

will be more appropriate. As cost in this alternative will be lower as compare to other one.

The new Juicemasters outlet:

Here in this section main issue is that one outlet has become vacant which is leased to

independent company named Juice-masters. The corporation is specialize in broader variety of

healthy juices and smoothies alternatives along with several cold-vegetarian snacks like

baguettes. Speciality beverages like teas/coffees are also available for consumers. Corporation

has already opened outlets in 3 other major airports. Company's Chief Executive officer is

enthusiastic regarding new outlet in Snowham. In this context following is overview of interior

of area provided as follows:

Area: 17 m x 15 m corner

2 side Storage Space

Staff Toilet Facility

2 doors and 4 windows

One Main Window

Based on above details, here is following is layout for recommended floor layout, as follows:

Queueing: For managing customers crowed, there should be two queues for making payment in

two separate single windows as well as two queue for collecting food items at main window.

Ordering: Self ordering system should be adopted here, as this system provides increase in order

accuracy and require less staff.

Delivery: In peak hours, customer will collect order from main window and during period other

than peak hours delivery will be made by staff in waiting area.

Payment Processes: Company should provide all payment alternatives like credit and debit card,

cash currency, mobile banking etc. From payment windows, customer will get token or receipt

after making payment. At the time of delivery customer will provide such token/receipt. At the

end of the day tokens and payment should be matched which can increase accuracy in entire

process.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Furniture and equipment: Here following is list of all the major items of furniture and

equipments, as follows:

Refrigerator Knives

Ice machine (small/ medium size) Cutting board

Juicer Portion scale

Blender POS system

Dishwasher Napkins

Measuring cups Counter Tables

Large trash can Chairs

Plastic wraps Fruit Peeling Machine

Job Roles:

Juicer:

Customer Service:

All buyers are treated with dignity and gratitude.

Describe everyday items on the Glowing menu as well as its advantages. This involves

drinks, juices and other items.

Helping customers in making order process by offering suggestions and describing each

item's nutrient value.

Food and Drink Prep & Production:

Appropriately decreasing food wasting following recipes.

Juice & drinks are made as per consumer and restaurant requirements.

Washing, cutting and preparing all the fruits and ingredients for juices and smoothies.

Know the components of juices and make recommendations based on consumer tastes.

Cashier:

The payments are handled quickly and accurately.

Re-stocking refrigerated bottled beverages and utensils where required.

Update inventories of shop on regular basis.

Periodically tally all receipts and payments.

equipments, as follows:

Refrigerator Knives

Ice machine (small/ medium size) Cutting board

Juicer Portion scale

Blender POS system

Dishwasher Napkins

Measuring cups Counter Tables

Large trash can Chairs

Plastic wraps Fruit Peeling Machine

Job Roles:

Juicer:

Customer Service:

All buyers are treated with dignity and gratitude.

Describe everyday items on the Glowing menu as well as its advantages. This involves

drinks, juices and other items.

Helping customers in making order process by offering suggestions and describing each

item's nutrient value.

Food and Drink Prep & Production:

Appropriately decreasing food wasting following recipes.

Juice & drinks are made as per consumer and restaurant requirements.

Washing, cutting and preparing all the fruits and ingredients for juices and smoothies.

Know the components of juices and make recommendations based on consumer tastes.

Cashier:

The payments are handled quickly and accurately.

Re-stocking refrigerated bottled beverages and utensils where required.

Update inventories of shop on regular basis.

Periodically tally all receipts and payments.

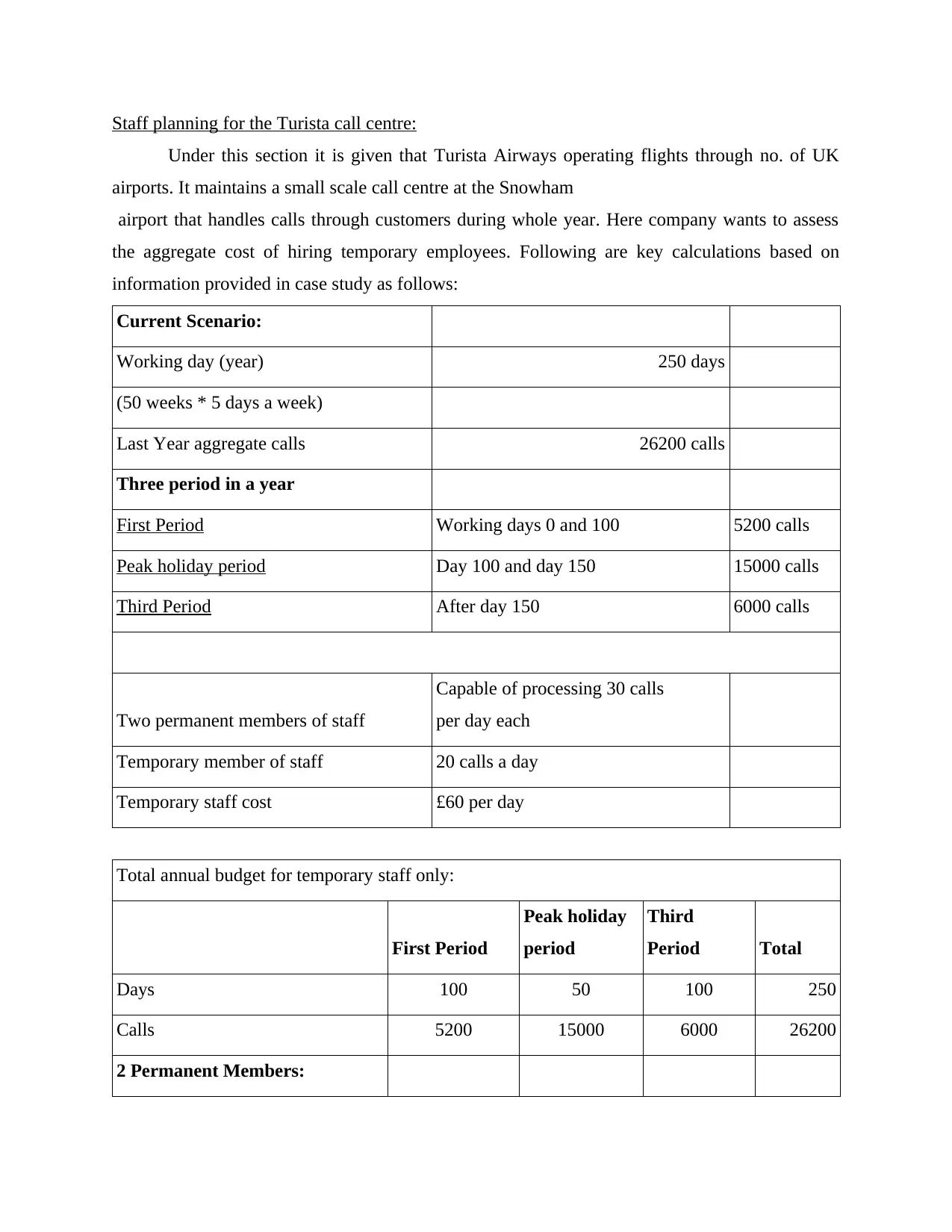

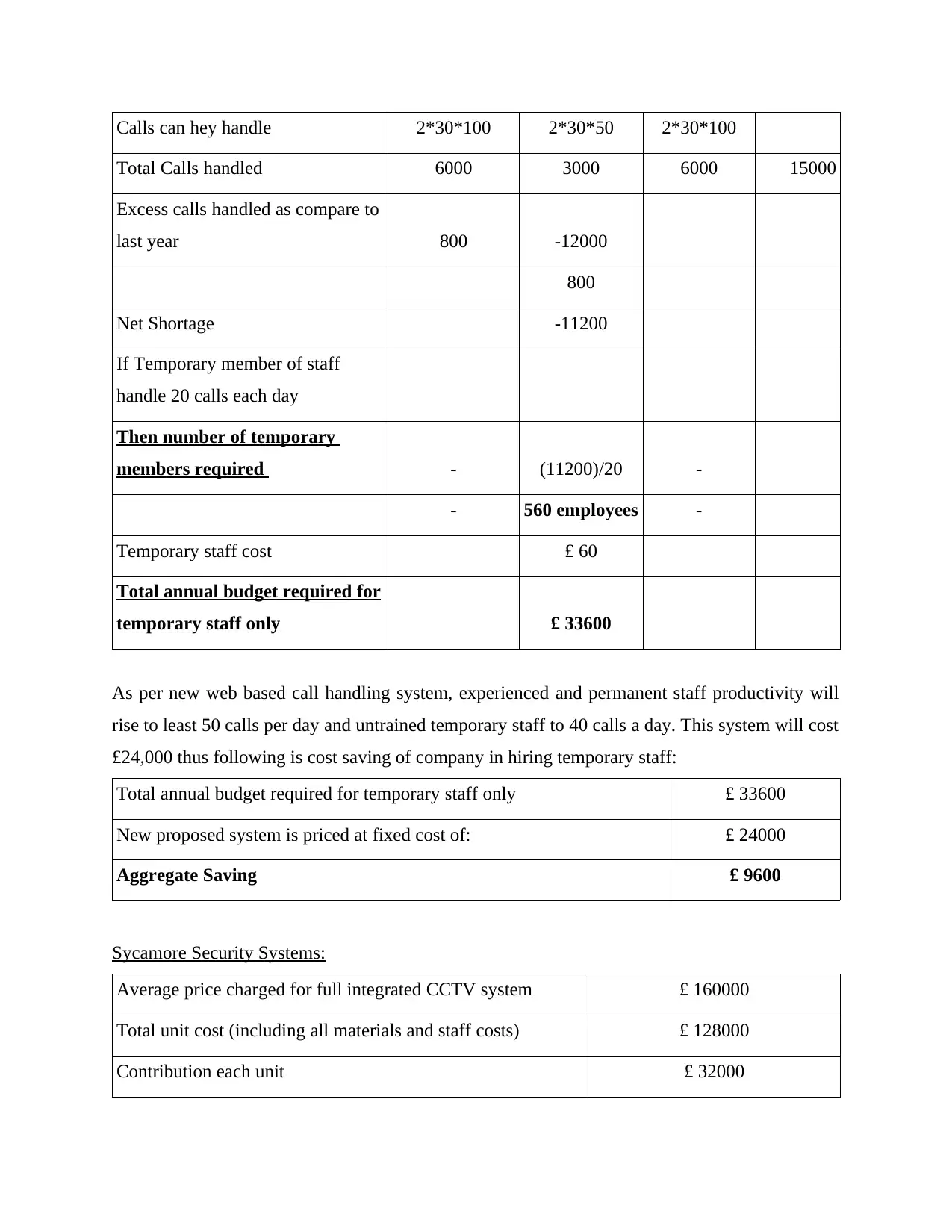

Staff planning for the Turista call centre:

Under this section it is given that Turista Airways operating flights through no. of UK

airports. It maintains a small scale call centre at the Snowham

airport that handles calls through customers during whole year. Here company wants to assess

the aggregate cost of hiring temporary employees. Following are key calculations based on

information provided in case study as follows:

Current Scenario:

Working day (year) 250 days

(50 weeks * 5 days a week)

Last Year aggregate calls 26200 calls

Three period in a year

First Period Working days 0 and 100 5200 calls

Peak holiday period Day 100 and day 150 15000 calls

Third Period After day 150 6000 calls

Two permanent members of staff

Capable of processing 30 calls

per day each

Temporary member of staff 20 calls a day

Temporary staff cost £60 per day

Total annual budget for temporary staff only:

First Period

Peak holiday

period

Third

Period Total

Days 100 50 100 250

Calls 5200 15000 6000 26200

2 Permanent Members:

Under this section it is given that Turista Airways operating flights through no. of UK

airports. It maintains a small scale call centre at the Snowham

airport that handles calls through customers during whole year. Here company wants to assess

the aggregate cost of hiring temporary employees. Following are key calculations based on

information provided in case study as follows:

Current Scenario:

Working day (year) 250 days

(50 weeks * 5 days a week)

Last Year aggregate calls 26200 calls

Three period in a year

First Period Working days 0 and 100 5200 calls

Peak holiday period Day 100 and day 150 15000 calls

Third Period After day 150 6000 calls

Two permanent members of staff

Capable of processing 30 calls

per day each

Temporary member of staff 20 calls a day

Temporary staff cost £60 per day

Total annual budget for temporary staff only:

First Period

Peak holiday

period

Third

Period Total

Days 100 50 100 250

Calls 5200 15000 6000 26200

2 Permanent Members:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calls can hey handle 2*30*100 2*30*50 2*30*100

Total Calls handled 6000 3000 6000 15000

Excess calls handled as compare to

last year 800 -12000

800

Net Shortage -11200

If Temporary member of staff

handle 20 calls each day

Then number of temporary

members required - (11200)/20 -

- 560 employees -

Temporary staff cost £ 60

Total annual budget required for

temporary staff only £ 33600

As per new web based call handling system, experienced and permanent staff productivity will

rise to least 50 calls per day and untrained temporary staff to 40 calls a day. This system will cost

£24,000 thus following is cost saving of company in hiring temporary staff:

Total annual budget required for temporary staff only £ 33600

New proposed system is priced at fixed cost of: £ 24000

Aggregate Saving £ 9600

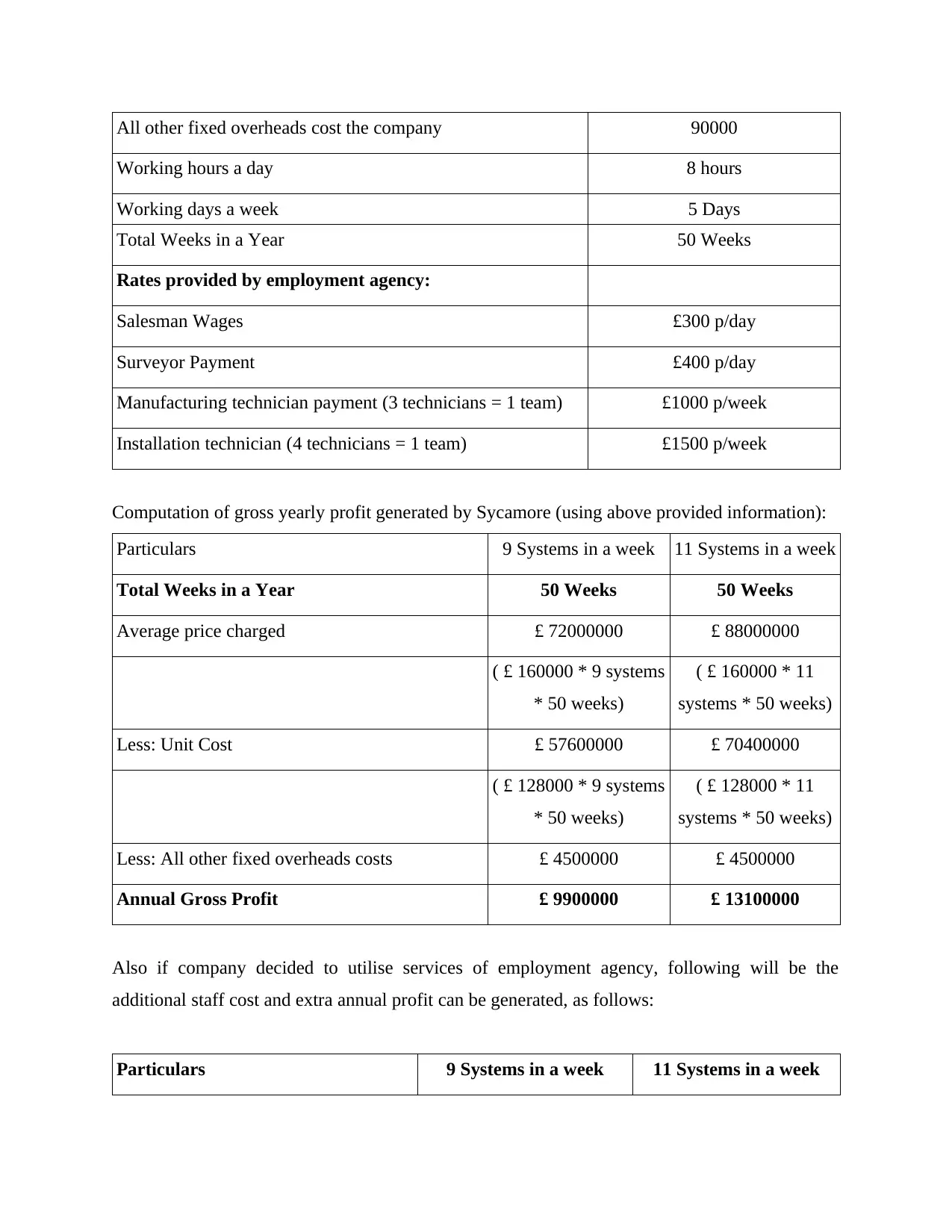

Sycamore Security Systems:

Average price charged for full integrated CCTV system £ 160000

Total unit cost (including all materials and staff costs) £ 128000

Contribution each unit £ 32000

Total Calls handled 6000 3000 6000 15000

Excess calls handled as compare to

last year 800 -12000

800

Net Shortage -11200

If Temporary member of staff

handle 20 calls each day

Then number of temporary

members required - (11200)/20 -

- 560 employees -

Temporary staff cost £ 60

Total annual budget required for

temporary staff only £ 33600

As per new web based call handling system, experienced and permanent staff productivity will

rise to least 50 calls per day and untrained temporary staff to 40 calls a day. This system will cost

£24,000 thus following is cost saving of company in hiring temporary staff:

Total annual budget required for temporary staff only £ 33600

New proposed system is priced at fixed cost of: £ 24000

Aggregate Saving £ 9600

Sycamore Security Systems:

Average price charged for full integrated CCTV system £ 160000

Total unit cost (including all materials and staff costs) £ 128000

Contribution each unit £ 32000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All other fixed overheads cost the company 90000

Working hours a day 8 hours

Working days a week 5 Days

Total Weeks in a Year 50 Weeks

Rates provided by employment agency:

Salesman Wages £300 p/day

Surveyor Payment £400 p/day

Manufacturing technician payment (3 technicians = 1 team) £1000 p/week

Installation technician (4 technicians = 1 team) £1500 p/week

Computation of gross yearly profit generated by Sycamore (using above provided information):

Particulars 9 Systems in a week 11 Systems in a week

Total Weeks in a Year 50 Weeks 50 Weeks

Average price charged £ 72000000 £ 88000000

( £ 160000 * 9 systems

* 50 weeks)

( £ 160000 * 11

systems * 50 weeks)

Less: Unit Cost £ 57600000 £ 70400000

( £ 128000 * 9 systems

* 50 weeks)

( £ 128000 * 11

systems * 50 weeks)

Less: All other fixed overheads costs £ 4500000 £ 4500000

Annual Gross Profit £ 9900000 £ 13100000

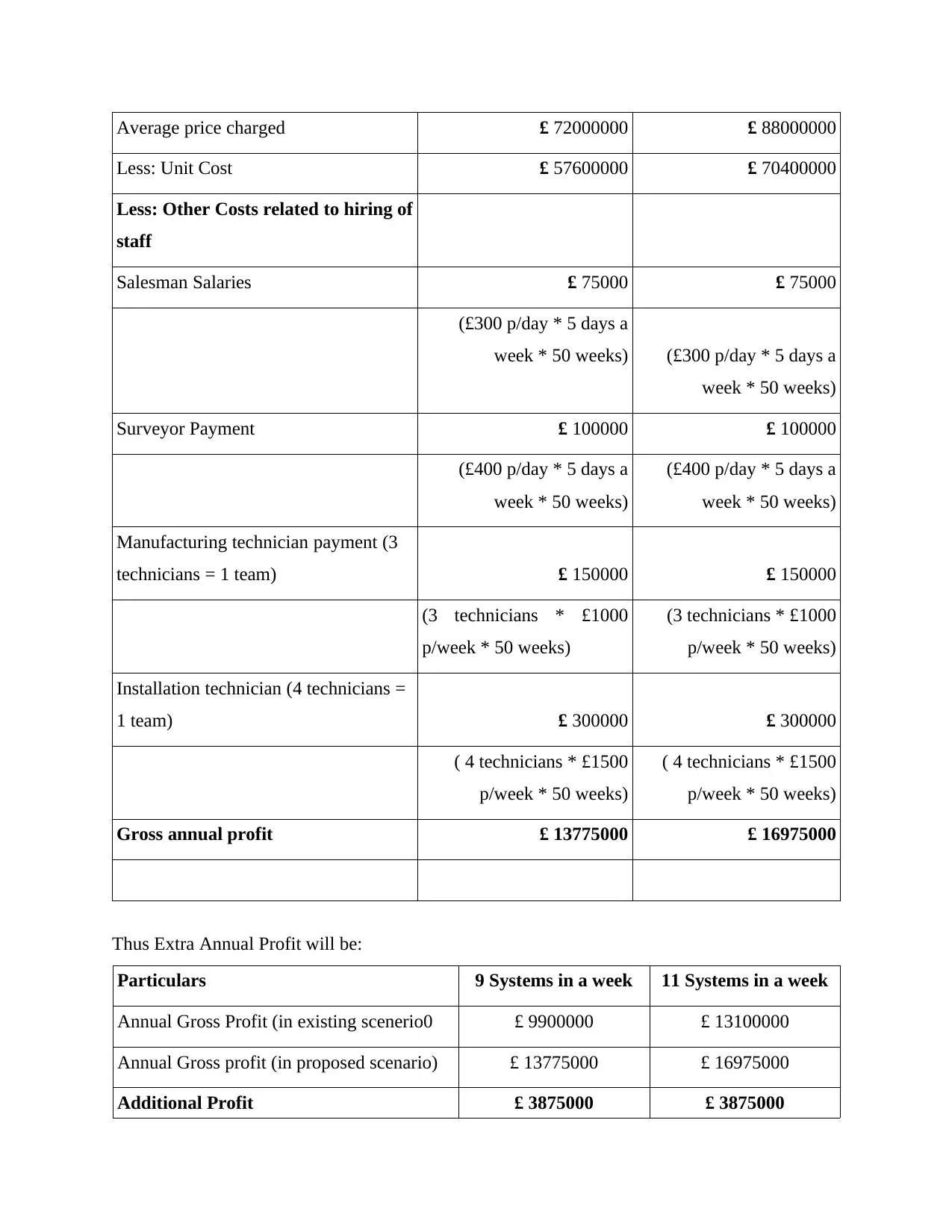

Also if company decided to utilise services of employment agency, following will be the

additional staff cost and extra annual profit can be generated, as follows:

Particulars 9 Systems in a week 11 Systems in a week

Working hours a day 8 hours

Working days a week 5 Days

Total Weeks in a Year 50 Weeks

Rates provided by employment agency:

Salesman Wages £300 p/day

Surveyor Payment £400 p/day

Manufacturing technician payment (3 technicians = 1 team) £1000 p/week

Installation technician (4 technicians = 1 team) £1500 p/week

Computation of gross yearly profit generated by Sycamore (using above provided information):

Particulars 9 Systems in a week 11 Systems in a week

Total Weeks in a Year 50 Weeks 50 Weeks

Average price charged £ 72000000 £ 88000000

( £ 160000 * 9 systems

* 50 weeks)

( £ 160000 * 11

systems * 50 weeks)

Less: Unit Cost £ 57600000 £ 70400000

( £ 128000 * 9 systems

* 50 weeks)

( £ 128000 * 11

systems * 50 weeks)

Less: All other fixed overheads costs £ 4500000 £ 4500000

Annual Gross Profit £ 9900000 £ 13100000

Also if company decided to utilise services of employment agency, following will be the

additional staff cost and extra annual profit can be generated, as follows:

Particulars 9 Systems in a week 11 Systems in a week

Average price charged £ 72000000 £ 88000000

Less: Unit Cost £ 57600000 £ 70400000

Less: Other Costs related to hiring of

staff

Salesman Salaries £ 75000 £ 75000

(£300 p/day * 5 days a

week * 50 weeks) (£300 p/day * 5 days a

week * 50 weeks)

Surveyor Payment £ 100000 £ 100000

(£400 p/day * 5 days a

week * 50 weeks)

(£400 p/day * 5 days a

week * 50 weeks)

Manufacturing technician payment (3

technicians = 1 team) £ 150000 £ 150000

(3 technicians * £1000

p/week * 50 weeks)

(3 technicians * £1000

p/week * 50 weeks)

Installation technician (4 technicians =

1 team) £ 300000 £ 300000

( 4 technicians * £1500

p/week * 50 weeks)

( 4 technicians * £1500

p/week * 50 weeks)

Gross annual profit £ 13775000 £ 16975000

Thus Extra Annual Profit will be:

Particulars 9 Systems in a week 11 Systems in a week

Annual Gross Profit (in existing scenerio0 £ 9900000 £ 13100000

Annual Gross profit (in proposed scenario) £ 13775000 £ 16975000

Additional Profit £ 3875000 £ 3875000

Less: Unit Cost £ 57600000 £ 70400000

Less: Other Costs related to hiring of

staff

Salesman Salaries £ 75000 £ 75000

(£300 p/day * 5 days a

week * 50 weeks) (£300 p/day * 5 days a

week * 50 weeks)

Surveyor Payment £ 100000 £ 100000

(£400 p/day * 5 days a

week * 50 weeks)

(£400 p/day * 5 days a

week * 50 weeks)

Manufacturing technician payment (3

technicians = 1 team) £ 150000 £ 150000

(3 technicians * £1000

p/week * 50 weeks)

(3 technicians * £1000

p/week * 50 weeks)

Installation technician (4 technicians =

1 team) £ 300000 £ 300000

( 4 technicians * £1500

p/week * 50 weeks)

( 4 technicians * £1500

p/week * 50 weeks)

Gross annual profit £ 13775000 £ 16975000

Thus Extra Annual Profit will be:

Particulars 9 Systems in a week 11 Systems in a week

Annual Gross Profit (in existing scenerio0 £ 9900000 £ 13100000

Annual Gross profit (in proposed scenario) £ 13775000 £ 16975000

Additional Profit £ 3875000 £ 3875000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.