F12-081 Business Structures: Unincorporated and Incorporated Report

VerifiedAdded on 2021/04/14

|21

|7917

|110

Report

AI Summary

This report provides a comprehensive overview of different business structures, comparing unincorporated and incorporated businesses. It begins by defining and analyzing sole trader and partnership models, detailing their characteristics, formation, management, and sources of funds. The report then transitions to incorporated businesses, differentiating between private and public companies, and examining their advantages and regulations. Key aspects such as liability, perpetual succession, and transferability of shares are discussed. The report also covers the legal structures, duties of directors, and a comparative evaluation of the formation of sole trader, partnership, and company structures, culminating in a critical evaluation and a business problem analysis, supported by relevant references.

Name: Bui Khanh Linh

Class: F12D

Student ID: F12-081

Table of Contents

I. Unincorporated business.......................................................................................................2

1. Sole trader:..........................................................................................................................2

2. Partnership:.........................................................................................................................3

II. Incorporated business........................................................................................................6

III. Legal structure..................................................................................................................12

IV. Duties of director..............................................................................................................12

V. Evaluation formation of sole trader. partnership, private and public company...........12

VI. Critical evaluate................................................................................................................14

VII. Business problem..............................................................................................................14

Reference:.....................................................................................................................................21

1

Class: F12D

Student ID: F12-081

Table of Contents

I. Unincorporated business.......................................................................................................2

1. Sole trader:..........................................................................................................................2

2. Partnership:.........................................................................................................................3

II. Incorporated business........................................................................................................6

III. Legal structure..................................................................................................................12

IV. Duties of director..............................................................................................................12

V. Evaluation formation of sole trader. partnership, private and public company...........12

VI. Critical evaluate................................................................................................................14

VII. Business problem..............................................................................................................14

Reference:.....................................................................................................................................21

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

I. Unincorporated business

Unincorporated business related to organizations that not separate of legal identity from the

owners. The owners are bear all of the liability of the business. There are two types of

unincorporated business which are sole trader (sole proprietorship) and partnership (Australian

Government, 2010). The owner of unincorporated busines is personally liable with the liabilities

of the business. As long as the owner live, the unincorporated business still exist.

1. Sole trader:

Definition: Sole trader is a type business that is own and manage by an individual. The owner of

sole trader responsible for all the profit and loss of his or her own business.

Characteristic:

- Single ownership: the business is owned by one person. He or she personally contribute

a whole capital for his or her own business

- Personally control: The owner wholly control of the business. He or she may ask

someone for advice but the decision-making right belongs to the owner.

- No legal entity: There is no separation between the legal entity and the owner of the

business. In case the owner is passed away or incapable of insolvency, the business is

considered to be dissolved.

- Unlimited liability: The owner must responsible for all the debt incurred during business

operation. If the asset is not enough to pay for the debt, the owner has to use personal

property to pay for it.

- Personally own profit and losses: The sole trader personally bear all the profit as well

as losses of the business

- Small scope: As the sole trader has limited source of fund then the operational scope is

limited

- Legal formation is unnecessary: Legal formalities in terms of establishing, management

and dissolve is not require

Formation

- General requirement: It is required to inform the HMRC in order to pay tax through

self-assessment. Therefore, sole trader have to filling the tax return annually.

- Responsibility: 'Sole trader have to register for the National Insurance number if the

business is operated in the UK

+ Sole trader must keep all the business records in terms of sales and expenditure

+ Filling the tax return through Self-assessment yearly

+ Paying the personal income tax based on the profit as well as national insurance in

terms of class 2 and 4

+ It is required that in case the revenue of sole trader exceed £85,000. Sole trader can also

register for VAT voluntarily if it is appropriate with his or her business

+ In case the business related to construction industry, sole trader have to register with

the HMRC for CIS (Construction Industry Scheme)

2

Unincorporated business related to organizations that not separate of legal identity from the

owners. The owners are bear all of the liability of the business. There are two types of

unincorporated business which are sole trader (sole proprietorship) and partnership (Australian

Government, 2010). The owner of unincorporated busines is personally liable with the liabilities

of the business. As long as the owner live, the unincorporated business still exist.

1. Sole trader:

Definition: Sole trader is a type business that is own and manage by an individual. The owner of

sole trader responsible for all the profit and loss of his or her own business.

Characteristic:

- Single ownership: the business is owned by one person. He or she personally contribute

a whole capital for his or her own business

- Personally control: The owner wholly control of the business. He or she may ask

someone for advice but the decision-making right belongs to the owner.

- No legal entity: There is no separation between the legal entity and the owner of the

business. In case the owner is passed away or incapable of insolvency, the business is

considered to be dissolved.

- Unlimited liability: The owner must responsible for all the debt incurred during business

operation. If the asset is not enough to pay for the debt, the owner has to use personal

property to pay for it.

- Personally own profit and losses: The sole trader personally bear all the profit as well

as losses of the business

- Small scope: As the sole trader has limited source of fund then the operational scope is

limited

- Legal formation is unnecessary: Legal formalities in terms of establishing, management

and dissolve is not require

Formation

- General requirement: It is required to inform the HMRC in order to pay tax through

self-assessment. Therefore, sole trader have to filling the tax return annually.

- Responsibility: 'Sole trader have to register for the National Insurance number if the

business is operated in the UK

+ Sole trader must keep all the business records in terms of sales and expenditure

+ Filling the tax return through Self-assessment yearly

+ Paying the personal income tax based on the profit as well as national insurance in

terms of class 2 and 4

+ It is required that in case the revenue of sole trader exceed £85,000. Sole trader can also

register for VAT voluntarily if it is appropriate with his or her business

+ In case the business related to construction industry, sole trader have to register with

the HMRC for CIS (Construction Industry Scheme)

2

- Business name: Sole trader can use his or her own name to name the business and it do

not have to be registered. The name the owner as well as the business must be consisted

in paperwork related to the business

+ The name of sole trader must not contain the terms ‘limited’, ‘Ltd’, ‘limited liability

partnership’, ‘LLP’, ‘public limited company’ or ‘plc’. Also, the name must not be

insulting and as same as the already existed business name. Moreover, the name should

not include sensitive terms or any related to government or local authorities unless there

is permission

Management:

- It is unnecessary for sole trader to answer any questions from board of directors or

business partner

- As sole trader personally own the business, there is no need to form any regulations or

agreement between partners with the purpose of management and operation

- The owner can decide how to run on his or her own business without any involvement

Source of funds

Equity capital Debt capital

- Owner’s money: the owner can contribute to the

business’s equity by his or her own money

- Retained earnings from reinvestment: Profits are

created in the previous trading year and its able to

cover all the daily expense of the sole trader

- Sales of inventory and assets: This source of

fund not only can attract customers but also

release the inventory

- Money borrowed from relatives and friends:

these are common source of fund for sole

trader’s business

- Sponsor from credit card: Credit cards funds

through cash in advance or covering expense

- Bank loans: The owner is required to have

collateral or personal property so as to ensure the

debt

- Grants: It is unnecessary for sole trader to pay

back this source

- Trade credit financing: the sole trader can

receive this fund whenever he or she need but it

requires deadline of repayment.

2. Partnership:

Definition and characteristic

Partnership refers to organizations run by two or more people and share the income with each

other. Partners can represent for each other during the business operation and each individual

personally responsible for the company’s liability.

Characteristic:

Membership: the range of member is from 2 to 100 including individuals must have full

legal compacity to become partner, except people with mental disorder or mental problem,

people under 18 and people do not have the ability to pay for the debt.

3

not have to be registered. The name the owner as well as the business must be consisted

in paperwork related to the business

+ The name of sole trader must not contain the terms ‘limited’, ‘Ltd’, ‘limited liability

partnership’, ‘LLP’, ‘public limited company’ or ‘plc’. Also, the name must not be

insulting and as same as the already existed business name. Moreover, the name should

not include sensitive terms or any related to government or local authorities unless there

is permission

Management:

- It is unnecessary for sole trader to answer any questions from board of directors or

business partner

- As sole trader personally own the business, there is no need to form any regulations or

agreement between partners with the purpose of management and operation

- The owner can decide how to run on his or her own business without any involvement

Source of funds

Equity capital Debt capital

- Owner’s money: the owner can contribute to the

business’s equity by his or her own money

- Retained earnings from reinvestment: Profits are

created in the previous trading year and its able to

cover all the daily expense of the sole trader

- Sales of inventory and assets: This source of

fund not only can attract customers but also

release the inventory

- Money borrowed from relatives and friends:

these are common source of fund for sole

trader’s business

- Sponsor from credit card: Credit cards funds

through cash in advance or covering expense

- Bank loans: The owner is required to have

collateral or personal property so as to ensure the

debt

- Grants: It is unnecessary for sole trader to pay

back this source

- Trade credit financing: the sole trader can

receive this fund whenever he or she need but it

requires deadline of repayment.

2. Partnership:

Definition and characteristic

Partnership refers to organizations run by two or more people and share the income with each

other. Partners can represent for each other during the business operation and each individual

personally responsible for the company’s liability.

Characteristic:

Membership: the range of member is from 2 to 100 including individuals must have full

legal compacity to become partner, except people with mental disorder or mental problem,

people under 18 and people do not have the ability to pay for the debt.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Unlimited liability: All the members are collectively and individually for all the debts of the

business. They have to use their personal property and asset to pay for the liability in case the

asset of the company is not enough to pay for the debt.

Sharing of profit and loss Profits and losses are divided proportionally based on agreement

between members. In case any terms in the contract is broken, the profit as well as losses is

divided equally

Mutual agency All the partners are represent for the company. Each of their action is binding

the company as well as each other.

Voluntary registration The registration to become a member of the partnership is not

mandatory but is recommended. One of the benefits is that it is possible to sue to the court in

case there is a dispute incur internal or external of the company

Continually Partnerships may dissolve upon partners death, bankruptcy or retirement. Or

else, the remain partners could continue the operations by making new agreement.

Contractual relationship It is possible to establish and maintain the relationship between

members by contract

Trader of interest Partners must be given unanimous is there is any transfer of interest

between each other.

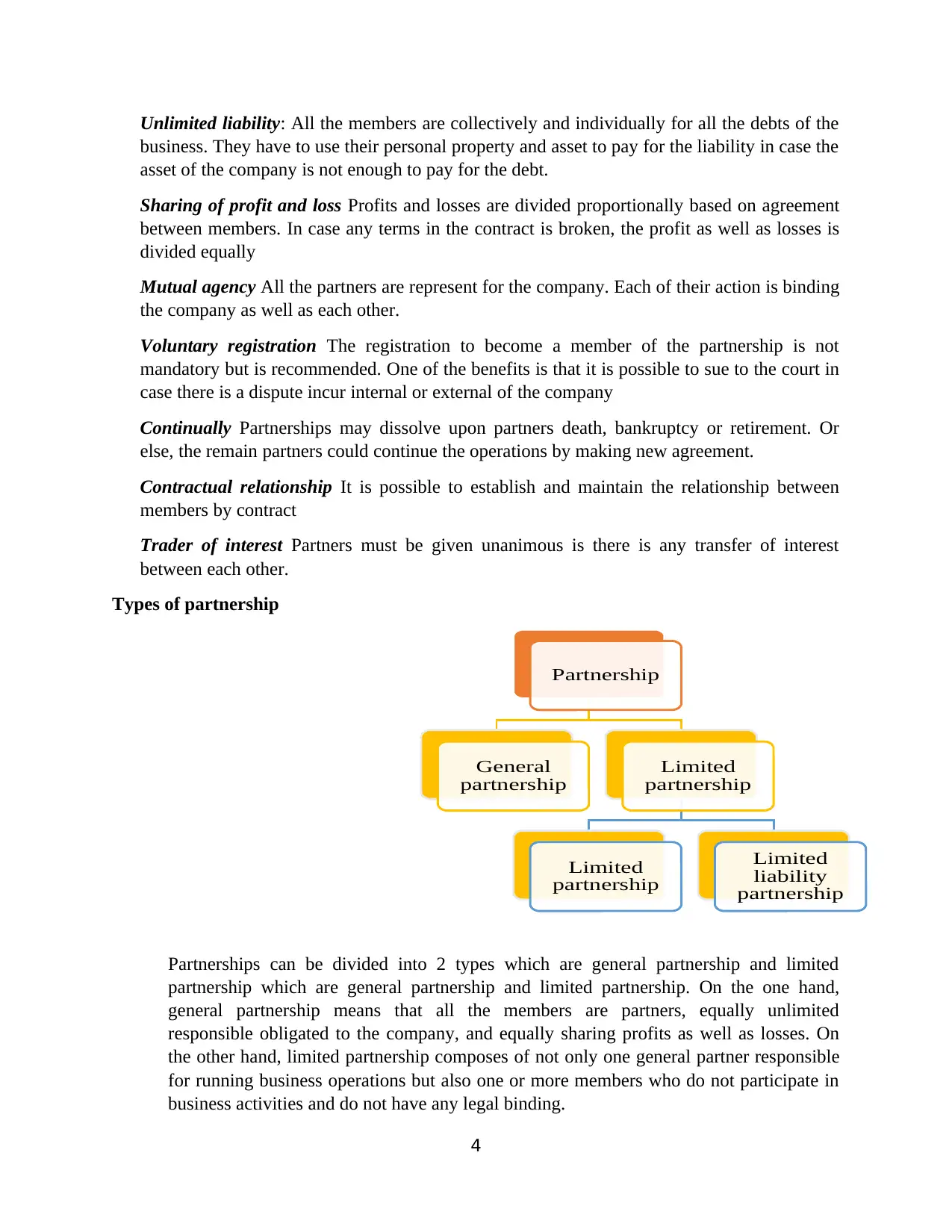

Types of partnership

Partnerships can be divided into 2 types which are general partnership and limited

partnership which are general partnership and limited partnership. On the one hand,

general partnership means that all the members are partners, equally unlimited

responsible obligated to the company, and equally sharing profits as well as losses. On

the other hand, limited partnership composes of not only one general partner responsible

for running business operations but also one or more members who do not participate in

business activities and do not have any legal binding.

4

Partnership

General

partnership

Limited

partnership

Limited

partnership

Limited

liability

partnership

business. They have to use their personal property and asset to pay for the liability in case the

asset of the company is not enough to pay for the debt.

Sharing of profit and loss Profits and losses are divided proportionally based on agreement

between members. In case any terms in the contract is broken, the profit as well as losses is

divided equally

Mutual agency All the partners are represent for the company. Each of their action is binding

the company as well as each other.

Voluntary registration The registration to become a member of the partnership is not

mandatory but is recommended. One of the benefits is that it is possible to sue to the court in

case there is a dispute incur internal or external of the company

Continually Partnerships may dissolve upon partners death, bankruptcy or retirement. Or

else, the remain partners could continue the operations by making new agreement.

Contractual relationship It is possible to establish and maintain the relationship between

members by contract

Trader of interest Partners must be given unanimous is there is any transfer of interest

between each other.

Types of partnership

Partnerships can be divided into 2 types which are general partnership and limited

partnership which are general partnership and limited partnership. On the one hand,

general partnership means that all the members are partners, equally unlimited

responsible obligated to the company, and equally sharing profits as well as losses. On

the other hand, limited partnership composes of not only one general partner responsible

for running business operations but also one or more members who do not participate in

business activities and do not have any legal binding.

4

Partnership

General

partnership

Limited

partnership

Limited

partnership

Limited

liability

partnership

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management of partnership

General Partnership: There is an equality in the responsibility between partners in managing

the business as well as profit and losses and the legal decision. Moreover, partner can represent

for the company in making decision.

Limited Partnership and Limited Liability Partnership

In terms of limited partnership, partners had unlimited liability with all decision, managing as

well as profit and losses of the company

In terms of limited liability partnership, unlike the limited partnership, partners do not have to

not only take responsible for profit and losses of the firm but also enter in the decision-making of

the business.

Setting up a business partnership

General requirements

Establish an agreement between partners to divided equally responsibility in terms of assets

as well as profits and losses. Moreover, they have to responsible for tax paying for their

shares as well as sharing profit with each other base on agreements. In addition, it is possible

that not only an actual person but also organizations or companies can become partners.

Steps to setting up business:

The first step is deciding the company’s name. In detailed, it is illegal if the name is identical

with the name of the previous companies because of the intellectual property right. The

second step is choosing the representator of the company or a nominated partner with the

purpose of managing tax returns as well as recoding business reference. The last step is

registering the company’s name to the HMRC (Her Majesty Revenue and Customs) to pay

tax later.

Deed of partnership (Article of partnership)

Partnership is an association from 2 to 20 partners. There has to be an agreement about

responsibilities as well as rights of partners (normally known as Deed of Partnership or The

Article of Partnership). Moreover, they must take responsibilities for all the debt of the

partnership.

Source of finance:

Equity Loan

- Savings, stocks and bonds:

- Funds from your personal circle of

family, friends and acquaintances

- Retirement account funds

- Business grant

- Business loan

- Venture capital funding from

investors

- Crowdfunding

II. Incorporated business

5

General Partnership: There is an equality in the responsibility between partners in managing

the business as well as profit and losses and the legal decision. Moreover, partner can represent

for the company in making decision.

Limited Partnership and Limited Liability Partnership

In terms of limited partnership, partners had unlimited liability with all decision, managing as

well as profit and losses of the company

In terms of limited liability partnership, unlike the limited partnership, partners do not have to

not only take responsible for profit and losses of the firm but also enter in the decision-making of

the business.

Setting up a business partnership

General requirements

Establish an agreement between partners to divided equally responsibility in terms of assets

as well as profits and losses. Moreover, they have to responsible for tax paying for their

shares as well as sharing profit with each other base on agreements. In addition, it is possible

that not only an actual person but also organizations or companies can become partners.

Steps to setting up business:

The first step is deciding the company’s name. In detailed, it is illegal if the name is identical

with the name of the previous companies because of the intellectual property right. The

second step is choosing the representator of the company or a nominated partner with the

purpose of managing tax returns as well as recoding business reference. The last step is

registering the company’s name to the HMRC (Her Majesty Revenue and Customs) to pay

tax later.

Deed of partnership (Article of partnership)

Partnership is an association from 2 to 20 partners. There has to be an agreement about

responsibilities as well as rights of partners (normally known as Deed of Partnership or The

Article of Partnership). Moreover, they must take responsibilities for all the debt of the

partnership.

Source of finance:

Equity Loan

- Savings, stocks and bonds:

- Funds from your personal circle of

family, friends and acquaintances

- Retirement account funds

- Business grant

- Business loan

- Venture capital funding from

investors

- Crowdfunding

II. Incorporated business

5

A company refers to a registered organization that is established by an artificial legal person

or a group of artificial legal persons with the purpose of implementing business activities. In

case the business out of funds, the owners are not required to use personal property to pay for

it. The life cycle of incorporated businesses is not tie with the life of the owners. In other

words, the life of the business could be long-lasting. The incorporated business consists of

private limited company and public limited company.

1. Characteristic

Incorporated association: register limited liability of each shareholder

Separate legal entity: There is separation in terms of responsibility between shareholders and

the company. This means that the company does not have to liable with the actions of its

members.

Limited liability: The liability of the members is limited within the amount that they

contributed

Perpetual succession: As the life of the company is not stick with the life of the owner, the

change of shareholders or lack of solvency does not affect the life span of the incorporated

business.

Common seal: Every company should have a common seal which represent for a natural

person

Transferability of shares: The shares can be transferred by the shareholders in the stock

exchange market

Separate property: The personally property of owners of shareholders are separated from

company’s property

Capacity to sue and be sued: A company is able to sue and be sue by a third party

Artificial person: The owner of the company can be a person that is recognized by the law as

a legal artificial person.

Separation of ownership from management: The Board of Director is selected by its

members. However, members cannot involve in the management of daily affairs

2. Differentiate public and private company

Public company Private company

Definition Listed in stock market, sale

share in stock exchange

market which attract more

investors

Only selling shares to

willing investors

Traded on Trade on stock exchange Traded by few investors

Regulations More heavily regulated by

the stock exchange

regulations the because

Unless the revenue of the

company does not exceed

100 million USD as well as

6

or a group of artificial legal persons with the purpose of implementing business activities. In

case the business out of funds, the owners are not required to use personal property to pay for

it. The life cycle of incorporated businesses is not tie with the life of the owners. In other

words, the life of the business could be long-lasting. The incorporated business consists of

private limited company and public limited company.

1. Characteristic

Incorporated association: register limited liability of each shareholder

Separate legal entity: There is separation in terms of responsibility between shareholders and

the company. This means that the company does not have to liable with the actions of its

members.

Limited liability: The liability of the members is limited within the amount that they

contributed

Perpetual succession: As the life of the company is not stick with the life of the owner, the

change of shareholders or lack of solvency does not affect the life span of the incorporated

business.

Common seal: Every company should have a common seal which represent for a natural

person

Transferability of shares: The shares can be transferred by the shareholders in the stock

exchange market

Separate property: The personally property of owners of shareholders are separated from

company’s property

Capacity to sue and be sued: A company is able to sue and be sue by a third party

Artificial person: The owner of the company can be a person that is recognized by the law as

a legal artificial person.

Separation of ownership from management: The Board of Director is selected by its

members. However, members cannot involve in the management of daily affairs

2. Differentiate public and private company

Public company Private company

Definition Listed in stock market, sale

share in stock exchange

market which attract more

investors

Only selling shares to

willing investors

Traded on Trade on stock exchange Traded by few investors

Regulations More heavily regulated by

the stock exchange

regulations the because

Unless the revenue of the

company does not exceed

100 million USD as well as

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

listed in stock market. 500 shareholders, it does not

have to follow the

regulations by SEC

Advantages Have responsibility of public

the financial report for

potential investors

Having the rights of

refusing to disclose any

information related to the

company’s financial report

Size Public companies are big

companies

Private companies can be

big companies

Source of funds Money from selling shares

and bonds

Private investors and

venture capital.

3. Setting up limited company

a. Checking if the type of business is appropriate to form a limited company

How the business pay tax and be funded based on what kind of business is it.

b. Choosing the name of the company

It is impossible that the chosen name is similar to the one of previous companies. Also, the

name must be ended by ‘Limited’ or ‘Ltd’

c. Choosing directors, a secretary as well as guarantors, shareholders and SPCs

The company must have at least one director but it is unnecessary to have a secretary. To be

specify, the director of a company can be a shareholder or a guarantor. Moreover, the

company need to determine the SPCs who

- Owning more than 25% of the shares

- Having more than 25% of the voting rights

- Having the right of appointing or dismissing the majority of members in the board of

directors

d. Preparing documents related to agreement about business operation

It is necessary for companies to prepare both memorandum as well as article of association:

Memorandum of association

In case of online company registration, the memorandum can be created automatically. In

contrast, companies have to apply the available memorandum template.

It is impossible to have any correction or updating once the company is registered.

Article of association

Companies may either

- Using standard form

- Creating their own and send them when company registration

e. Checking documents to be kept

7

have to follow the

regulations by SEC

Advantages Have responsibility of public

the financial report for

potential investors

Having the rights of

refusing to disclose any

information related to the

company’s financial report

Size Public companies are big

companies

Private companies can be

big companies

Source of funds Money from selling shares

and bonds

Private investors and

venture capital.

3. Setting up limited company

a. Checking if the type of business is appropriate to form a limited company

How the business pay tax and be funded based on what kind of business is it.

b. Choosing the name of the company

It is impossible that the chosen name is similar to the one of previous companies. Also, the

name must be ended by ‘Limited’ or ‘Ltd’

c. Choosing directors, a secretary as well as guarantors, shareholders and SPCs

The company must have at least one director but it is unnecessary to have a secretary. To be

specify, the director of a company can be a shareholder or a guarantor. Moreover, the

company need to determine the SPCs who

- Owning more than 25% of the shares

- Having more than 25% of the voting rights

- Having the right of appointing or dismissing the majority of members in the board of

directors

d. Preparing documents related to agreement about business operation

It is necessary for companies to prepare both memorandum as well as article of association:

Memorandum of association

In case of online company registration, the memorandum can be created automatically. In

contrast, companies have to apply the available memorandum template.

It is impossible to have any correction or updating once the company is registered.

Article of association

Companies may either

- Using standard form

- Creating their own and send them when company registration

e. Checking documents to be kept

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

According to the UK Government, companies must keep records about the company as well

as financial and accounting records.

Records about the company:

- Directors, shareholders and secretaires

- Results of voting and resolutions of shareholders

- Guarantee of debentures repayment with a specific of time and who to pay

- Guarantee of indemnifying

- Transactions of buying shares

- Loans and mortgages secured by company’s assets

- Register of SPCs

Accounting records

- Earnings and expenditures

- Assets owned by the company

- Debts that the company owe or is owed

- Company’s stocks by the end of fiscal year

- Purchasing and selling goods (including suppliers and buyers)

- The stocktaking you used to work out the stock figure

Financial records

- Receipts, petty cash records, orders and many others representing for the spending of the

company

- Invoices, till roll or sales book for the money received by the company

- Other relevant documents such as bank statement or correspondence.

f. Registering the company

First of all, it is compulsory to provide the official address of the company that have been

registered. In detailed, the address must be a real one and in the same nation as registered.

Next, the company need to choose the SIC (Standard industrial classification) code

describing the natural of its business.

After that, registering to the Companies House. The company can also register with HRMC

after register the company for any related tax.

4. Business operation of limited company

a. The responsibilities of Directors

- Following the regulations of the company

- Reserving company profile as well as documents of changes

- Filing accounts and tax return of the company

- Do not keep secret with other shareholders if the director can earn benefit from any

transactions made by the company

- Pay CIT

8

as financial and accounting records.

Records about the company:

- Directors, shareholders and secretaires

- Results of voting and resolutions of shareholders

- Guarantee of debentures repayment with a specific of time and who to pay

- Guarantee of indemnifying

- Transactions of buying shares

- Loans and mortgages secured by company’s assets

- Register of SPCs

Accounting records

- Earnings and expenditures

- Assets owned by the company

- Debts that the company owe or is owed

- Company’s stocks by the end of fiscal year

- Purchasing and selling goods (including suppliers and buyers)

- The stocktaking you used to work out the stock figure

Financial records

- Receipts, petty cash records, orders and many others representing for the spending of the

company

- Invoices, till roll or sales book for the money received by the company

- Other relevant documents such as bank statement or correspondence.

f. Registering the company

First of all, it is compulsory to provide the official address of the company that have been

registered. In detailed, the address must be a real one and in the same nation as registered.

Next, the company need to choose the SIC (Standard industrial classification) code

describing the natural of its business.

After that, registering to the Companies House. The company can also register with HRMC

after register the company for any related tax.

4. Business operation of limited company

a. The responsibilities of Directors

- Following the regulations of the company

- Reserving company profile as well as documents of changes

- Filing accounts and tax return of the company

- Do not keep secret with other shareholders if the director can earn benefit from any

transactions made by the company

- Pay CIT

8

The director can hire a person in charge of the activities listed above. However, the legal

responsible still belongs to the directors. In the case of the directors do not meet the

responsibilities then he or she might be fined, prosecuted or even dismissed.

b. Taking money out of a limited company

Salary, expenses and benefits

Only registered as an employer, it is possible for the company to pay salary, expenditure or

benefit for employees.

The salary payments include both income tax as well as National Insurance so it should be

taken out and pay for the HMRC along with National Insurance contributed by employees.

If anyone in the company uses the company’s belongings for personal purposes then it has to

be reported as a benefit and he or she must pay any tax due

Dividends

Dividend payment is not included in business cost when paying filing CIT.

Dividend must be paid for all shareholders. In order to pay dividend, it is a must to hold a

meeting with the purpose of dividend declaration. After the meeting, all the records must be

kept by the directors.

Tax on dividend

The company do not have to pay for taxes on dividend and it would not be levied on

shareholders unless it exceeds £2.000.

c. Directors’ loan

Directors’ loan incurred when directors or close family members withdraw the amount of

money from the company is higher than the amount of money invested.

Any payments or borrowings that related to directors’ loan must be kept in the director’s loan

account. At the end of the fiscal year of the company, the money that the directors owe the

company or vice versa will be on the balance sheet in the annual count of directors.

d. Changes of the company the needed to be recorded

Changing the company’s registered address

The requirement of changes must be reached to Companies House. If it is approved then

Companies House will inform the HMRC. The new registered address must be in the same

part of the UK as registered before.

Other changes

These changes needed to be informed to the HMRC:

- The directors’ business’ contact detail changes

9

responsible still belongs to the directors. In the case of the directors do not meet the

responsibilities then he or she might be fined, prosecuted or even dismissed.

b. Taking money out of a limited company

Salary, expenses and benefits

Only registered as an employer, it is possible for the company to pay salary, expenditure or

benefit for employees.

The salary payments include both income tax as well as National Insurance so it should be

taken out and pay for the HMRC along with National Insurance contributed by employees.

If anyone in the company uses the company’s belongings for personal purposes then it has to

be reported as a benefit and he or she must pay any tax due

Dividends

Dividend payment is not included in business cost when paying filing CIT.

Dividend must be paid for all shareholders. In order to pay dividend, it is a must to hold a

meeting with the purpose of dividend declaration. After the meeting, all the records must be

kept by the directors.

Tax on dividend

The company do not have to pay for taxes on dividend and it would not be levied on

shareholders unless it exceeds £2.000.

c. Directors’ loan

Directors’ loan incurred when directors or close family members withdraw the amount of

money from the company is higher than the amount of money invested.

Any payments or borrowings that related to directors’ loan must be kept in the director’s loan

account. At the end of the fiscal year of the company, the money that the directors owe the

company or vice versa will be on the balance sheet in the annual count of directors.

d. Changes of the company the needed to be recorded

Changing the company’s registered address

The requirement of changes must be reached to Companies House. If it is approved then

Companies House will inform the HMRC. The new registered address must be in the same

part of the UK as registered before.

Other changes

These changes needed to be informed to the HMRC:

- The directors’ business’ contact detail changes

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

- Appointing a secretary or tax advisor

The following changes must be informed to the Companies House within 14 days:

- Where the records is and which records are kept

- Directors and their personal information

- SPCs or their personal information

- Company’s secretary

In case the company want to issue more share, it must be informed to the Companies House

within a month.

Changes approved by shareholders

It is necessary to have votes form shareholders if:

- Changing company’s name

- Dismissing a director

- Change the company’s article of association

Most of the resolution need the majority of shareholder to be passed. In some cases, special

resolution need 75% of agreement to be passed. The changes as well as resolution must be

reported to the Companies House.

Shareholder voting

The amount of share that a shareholder contributed decided whether he or she has the voting

right or not rather than the number of shareholders. The number of shareholders that attend to

the meeting is limited based on the amount of share that they contributed.

e. Company and Accounting records

The company must have responsibility of reserving the documents and records related to the

company itself as well as financial and accounting records (point e in the Steps to setting up a

company). Otherwise, the company can hire an accountant to help the company with taxes.

Moreover, the records must be kept carefully for the HMRC to check whether the company

pay the right amount of tax or not.

The records must be kept in 6 years from the end of the fiscal year of the company. In

contrast, it is possible to reserve the records more than 6 years unless:

- The transactions consists of two or more accounting periods of the company

- Purchasing an asset that it’s life span last more than 6 years

- Late tax return filing

- HMRC start to check the tax return compliance

In case of the records are lost or stolen, the company must inform to the Corporation Tax

office immediately and mention about this situation in the Company tax return.

f. Confirmation statement

10

The following changes must be informed to the Companies House within 14 days:

- Where the records is and which records are kept

- Directors and their personal information

- SPCs or their personal information

- Company’s secretary

In case the company want to issue more share, it must be informed to the Companies House

within a month.

Changes approved by shareholders

It is necessary to have votes form shareholders if:

- Changing company’s name

- Dismissing a director

- Change the company’s article of association

Most of the resolution need the majority of shareholder to be passed. In some cases, special

resolution need 75% of agreement to be passed. The changes as well as resolution must be

reported to the Companies House.

Shareholder voting

The amount of share that a shareholder contributed decided whether he or she has the voting

right or not rather than the number of shareholders. The number of shareholders that attend to

the meeting is limited based on the amount of share that they contributed.

e. Company and Accounting records

The company must have responsibility of reserving the documents and records related to the

company itself as well as financial and accounting records (point e in the Steps to setting up a

company). Otherwise, the company can hire an accountant to help the company with taxes.

Moreover, the records must be kept carefully for the HMRC to check whether the company

pay the right amount of tax or not.

The records must be kept in 6 years from the end of the fiscal year of the company. In

contrast, it is possible to reserve the records more than 6 years unless:

- The transactions consists of two or more accounting periods of the company

- Purchasing an asset that it’s life span last more than 6 years

- Late tax return filing

- HMRC start to check the tax return compliance

In case of the records are lost or stolen, the company must inform to the Corporation Tax

office immediately and mention about this situation in the Company tax return.

f. Confirmation statement

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Companies need to check the information of the company registered to Companies House

annually to ensure its correct

Checking company’s information

- Information about register office, directors, secretary as well as the place where the

record is

- Information about the company’s capital statement and shareholders

- SIC code

- SPCs list

Reporting changes

It is possible to report changes in terms of information about capital statement and

shareholders as well as SIC. On the contrary, companies could not report changes using

confirmation statement as it should be filed separately with Companies House including

company’s officer, registered address, where the record is kept and SPCs.

Due dates

The deadline for confirmation statement will be sent through emails or letters to the office.

The due date often a year after the establishment of the company or the filling latest annual

return date. The statement confirmation can be filled exceeding 14 days after the deadline.

There would be penalties up to £5,000 and the company would be removed if there is no

confirmation.

g. Signs, stationery and promotional material

It is required to show the sign that is easy to read and recognize of the company at the office

or anywhere there is business operation of the company.

Besides that, the name of the company must be included in all the business records related to

the company. On the business letters, order forms as well as official website, it is the must to

perform:

- The registered number of the company

- Officially registered address

- The place that the company register in

- Limited company

- Directors’ list

- Shares (must include the amount of money that is paid up which is owned by

shareholders)

5. Source of finance

Debt Capital Equity Capital

- Bank loans

- Personal loans

- Bonds

- Selling shares of stock

11

annually to ensure its correct

Checking company’s information

- Information about register office, directors, secretary as well as the place where the

record is

- Information about the company’s capital statement and shareholders

- SIC code

- SPCs list

Reporting changes

It is possible to report changes in terms of information about capital statement and

shareholders as well as SIC. On the contrary, companies could not report changes using

confirmation statement as it should be filed separately with Companies House including

company’s officer, registered address, where the record is kept and SPCs.

Due dates

The deadline for confirmation statement will be sent through emails or letters to the office.

The due date often a year after the establishment of the company or the filling latest annual

return date. The statement confirmation can be filled exceeding 14 days after the deadline.

There would be penalties up to £5,000 and the company would be removed if there is no

confirmation.

g. Signs, stationery and promotional material

It is required to show the sign that is easy to read and recognize of the company at the office

or anywhere there is business operation of the company.

Besides that, the name of the company must be included in all the business records related to

the company. On the business letters, order forms as well as official website, it is the must to

perform:

- The registered number of the company

- Officially registered address

- The place that the company register in

- Limited company

- Directors’ list

- Shares (must include the amount of money that is paid up which is owned by

shareholders)

5. Source of finance

Debt Capital Equity Capital

- Bank loans

- Personal loans

- Bonds

- Selling shares of stock

11

- Credit card debt

III. Legal structure

Sole trader Partnership Public companies Private companies

Liability Unlimited Unlimited Limited Limited

Life span Existence rely on

the existence of the

owner

Existence rely on the

existence of the

owner

Permanent Permanent

Registration HMRC HMRC Companies House Companies House

Tax liability PIT PIT CIT CIT

Legal entity There is no legal

person

There is no legal

person

Legal person Legal person

IV. Duties of director

Organizing: The director needs to divide the works equally and coherently among employees so

as to gain the goal of the company

Planning: The director has the responsibility of setting up the plan in order to evaluate the

internal as well as external environment, as a result, will be able to determine and develop

objectives, scope and field.

Controlling: The director needs to not only ensure that the business operation of the business is

stick to the plan but also set up principals, standards and policies for the business.

Commanding: As a leader of the company, the director responsible for managing, leading,

communicating and promoting the workforce in the most effective way so as to succeed in the

path to achieve the set goal.

Coordinating: The director can not only manage the business by his or her own but also hire an

expert or qualified manager with the purpose of controlling, supporting in business operation as

well as boosting up the willpower of the employees for the most working efficiency.

It is required that directors of 4 types of business which are sole trader, partnership, private

companies as well as public companies have to complete all of their duties. Clearly, they have to

fulfill the OPCCC (Organizing, Planning, Controlling, Commanding and Coordinating). The

obligation is separated equally between directors. Nevertheless, there is only one director in sole

trader while the others have more than one.

In addition, on the one hand, in terms of partnership, the responsibility of the director would be

decided based on the Deed of Partnership. On the other hand, like sole trader, directors of limited

companies have responsible to fulfill the OPCCC, however, they do not have to combine

personal property with business’s equity.

V. Evaluation formation of sole trader. partnership, private and public company

12

III. Legal structure

Sole trader Partnership Public companies Private companies

Liability Unlimited Unlimited Limited Limited

Life span Existence rely on

the existence of the

owner

Existence rely on the

existence of the

owner

Permanent Permanent

Registration HMRC HMRC Companies House Companies House

Tax liability PIT PIT CIT CIT

Legal entity There is no legal

person

There is no legal

person

Legal person Legal person

IV. Duties of director

Organizing: The director needs to divide the works equally and coherently among employees so

as to gain the goal of the company

Planning: The director has the responsibility of setting up the plan in order to evaluate the

internal as well as external environment, as a result, will be able to determine and develop

objectives, scope and field.

Controlling: The director needs to not only ensure that the business operation of the business is

stick to the plan but also set up principals, standards and policies for the business.

Commanding: As a leader of the company, the director responsible for managing, leading,

communicating and promoting the workforce in the most effective way so as to succeed in the

path to achieve the set goal.

Coordinating: The director can not only manage the business by his or her own but also hire an

expert or qualified manager with the purpose of controlling, supporting in business operation as

well as boosting up the willpower of the employees for the most working efficiency.

It is required that directors of 4 types of business which are sole trader, partnership, private

companies as well as public companies have to complete all of their duties. Clearly, they have to

fulfill the OPCCC (Organizing, Planning, Controlling, Commanding and Coordinating). The

obligation is separated equally between directors. Nevertheless, there is only one director in sole

trader while the others have more than one.

In addition, on the one hand, in terms of partnership, the responsibility of the director would be

decided based on the Deed of Partnership. On the other hand, like sole trader, directors of limited

companies have responsible to fulfill the OPCCC, however, they do not have to combine

personal property with business’s equity.

V. Evaluation formation of sole trader. partnership, private and public company

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.