Management Accounting Report: Sollatek's Financial Analysis and Tools

VerifiedAdded on 2020/07/22

|16

|4455

|60

Report

AI Summary

This report provides a comprehensive analysis of management accounting, focusing on the tools and techniques essential for financial analysis and business improvement. The report begins with an executive summary highlighting the importance of management accounting in managing financial resources and achieving market success. It then delves into the different types of accounting, including non-profit, managerial, lean, and transfer pricing, and their applications. The core of the report examines methods for managing accounting reports, such as calculating marginal and absorption costs, and the use of cost reports, budget reports, performance reports, and index reporting. The report further explores the advantages and disadvantages of budgetary control tools, emphasizing their role in improving profitability and coordination. Finally, it compares various ways organizations adopt accounting systems. The report includes tables illustrating cost calculations and provides a detailed overview of management accounting principles and practices to enhance financial decision-making. This assignment is contributed by a student to be published on the website Desklib.

MANAGEMENT ACCOUNTING

ID:

College Name:

Lecturer Name:

Unit Handler Name:

Date of Submission:

ID:

College Name:

Lecturer Name:

Unit Handler Name:

Date of Submission:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The management accounting is an important part and concept of an organisation. An

organisation needs to manage their financial resources in order to achieve success in the market.

It has been found that there are some organisations that are unable to understand the significance

of using accounting tools. Such organisations have encountered loss in their businesses.

Management accounting helps an organisation to analyse the profit reports and financial reports

for gaining sustainability in their business. In order to analyse business performance,

management accountant is required to analyse the data that are obtained from financial reports

for making effective decision. This study is going to focus on the tools and techniques that can

be adopted by a firm to analyse accounts and finances for improving business.

2

The management accounting is an important part and concept of an organisation. An

organisation needs to manage their financial resources in order to achieve success in the market.

It has been found that there are some organisations that are unable to understand the significance

of using accounting tools. Such organisations have encountered loss in their businesses.

Management accounting helps an organisation to analyse the profit reports and financial reports

for gaining sustainability in their business. In order to analyse business performance,

management accountant is required to analyse the data that are obtained from financial reports

for making effective decision. This study is going to focus on the tools and techniques that can

be adopted by a firm to analyse accounts and finances for improving business.

2

Table of contents

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

P1 Explaining different types of accounting.................................................................................4

P2 Methods for managing accounting reports...............................................................................6

Task 2...............................................................................................................................................7

Task 3...............................................................................................................................................8

P4 Advantages and disadvantages of budgetary control tools.......................................................8

Task 4...........................................................................................................................................10

P5 Comparing ways in which organisation are adopting accounting systems............................10

Conclusion.....................................................................................................................................12

Reference List................................................................................................................................13

3

Introduction......................................................................................................................................4

Task 1...............................................................................................................................................4

P1 Explaining different types of accounting.................................................................................4

P2 Methods for managing accounting reports...............................................................................6

Task 2...............................................................................................................................................7

Task 3...............................................................................................................................................8

P4 Advantages and disadvantages of budgetary control tools.......................................................8

Task 4...........................................................................................................................................10

P5 Comparing ways in which organisation are adopting accounting systems............................10

Conclusion.....................................................................................................................................12

Reference List................................................................................................................................13

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Management accounting can be defined as the methods by which an organisation tries to

maintain their financial as well as accounting reports in the form of statistics. An organisation is

able to understand the total capital that is required by them in a financial year. It assists a

manager to make decision regarding a company's finances. Management accounting generally

publishes financial report on a weekly basis and this report is only meant for internal

stakeholders. This study sheds light on the various types of accounting systems that are used by

an organisation like Sollatek for managing their finances. A number of accounting tools are

available like cost analysis, absorption costing and profit analysis. There is an attempt to evaluate

tool related to budgetary controls and the control measure ensures success of a business. This

study is going to discuss about the methods or ways with the help of which an organisation is

able to adopt adequate technique for managing accounts.

L.O.1

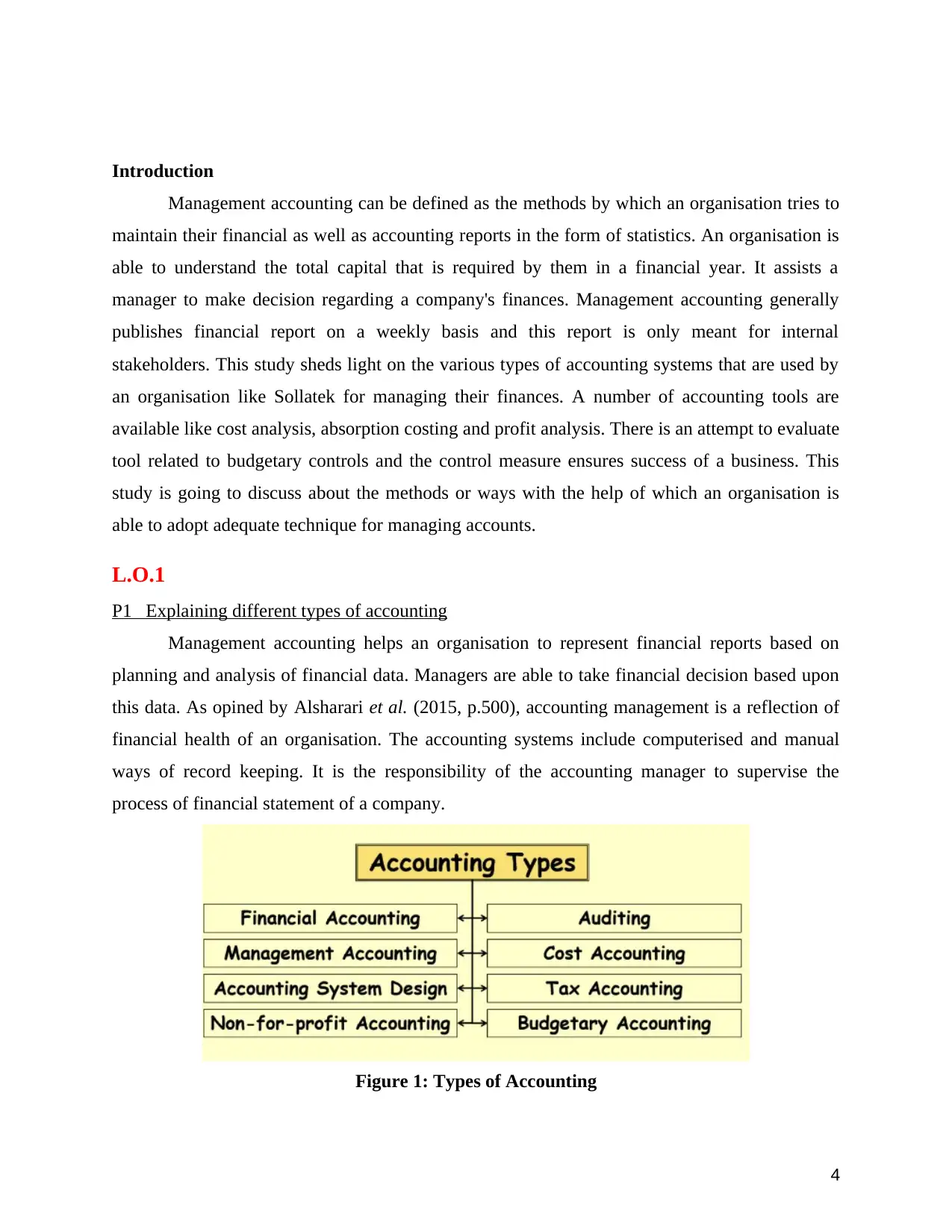

P1 Explaining different types of accounting

Management accounting helps an organisation to represent financial reports based on

planning and analysis of financial data. Managers are able to take financial decision based upon

this data. As opined by Alsharari et al. (2015, p.500), accounting management is a reflection of

financial health of an organisation. The accounting systems include computerised and manual

ways of record keeping. It is the responsibility of the accounting manager to supervise the

process of financial statement of a company.

Figure 1: Types of Accounting

4

Management accounting can be defined as the methods by which an organisation tries to

maintain their financial as well as accounting reports in the form of statistics. An organisation is

able to understand the total capital that is required by them in a financial year. It assists a

manager to make decision regarding a company's finances. Management accounting generally

publishes financial report on a weekly basis and this report is only meant for internal

stakeholders. This study sheds light on the various types of accounting systems that are used by

an organisation like Sollatek for managing their finances. A number of accounting tools are

available like cost analysis, absorption costing and profit analysis. There is an attempt to evaluate

tool related to budgetary controls and the control measure ensures success of a business. This

study is going to discuss about the methods or ways with the help of which an organisation is

able to adopt adequate technique for managing accounts.

L.O.1

P1 Explaining different types of accounting

Management accounting helps an organisation to represent financial reports based on

planning and analysis of financial data. Managers are able to take financial decision based upon

this data. As opined by Alsharari et al. (2015, p.500), accounting management is a reflection of

financial health of an organisation. The accounting systems include computerised and manual

ways of record keeping. It is the responsibility of the accounting manager to supervise the

process of financial statement of a company.

Figure 1: Types of Accounting

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Source: Youssef, 2014, p.10)

Sollatek is required to adopt an appropriate technique for accounting management. There are

a number of accounting management system that can be used by Sollatek for managing their

finances in an effective manner. The different types of accounting systems have been discussed

below:

Non-profit accounting: In this type of accounting system finds of an organisation are

required to track so as to ensure that donations that are specified for a purpose are spent

in a proper manner. This type of accounting is not able to provide personal benefits to the

owner of a firm.

Managerial accounting: Managerial accounting is able to assist a manager to give

adequate information regarding capital flow. Cost accounting system falls in this category

(Arora and Soral, 2017, p.46). Cost accounting refers to actual costs that are levied upon

product delivery.

Lean accounting: Lean accounting aims at examining a number of accounting processes

for determining costs by eliminating wastage of resources. One of the advantages of

using lean accounting for an organisation like Sollatek is that the company will be able to

conserve time and also reduce resource wastage by their methods. These techniques

might also help Sollatek to identify financial impact over their organisation. Despite

advantages, it also has certain loopholes such as this accounting system is unable to

address specific costs. It more emphasizes over values stream. This might prove

unfruitful for Sollatek.

Transfer pricing: It refers to the notional value at which services and goods are

transferred among division (Bouten and Hoozee, 2013, p.334). This type of accounting

system is able to help Sollatek for measuring divisional performance. One of weaknesses

of transfer pricing is that it for the execution of transfer pricings.

P2 Methods for managing accounting reports

Calculating marginal cost

Marginal costing

Year 1

5

Sollatek is required to adopt an appropriate technique for accounting management. There are

a number of accounting management system that can be used by Sollatek for managing their

finances in an effective manner. The different types of accounting systems have been discussed

below:

Non-profit accounting: In this type of accounting system finds of an organisation are

required to track so as to ensure that donations that are specified for a purpose are spent

in a proper manner. This type of accounting is not able to provide personal benefits to the

owner of a firm.

Managerial accounting: Managerial accounting is able to assist a manager to give

adequate information regarding capital flow. Cost accounting system falls in this category

(Arora and Soral, 2017, p.46). Cost accounting refers to actual costs that are levied upon

product delivery.

Lean accounting: Lean accounting aims at examining a number of accounting processes

for determining costs by eliminating wastage of resources. One of the advantages of

using lean accounting for an organisation like Sollatek is that the company will be able to

conserve time and also reduce resource wastage by their methods. These techniques

might also help Sollatek to identify financial impact over their organisation. Despite

advantages, it also has certain loopholes such as this accounting system is unable to

address specific costs. It more emphasizes over values stream. This might prove

unfruitful for Sollatek.

Transfer pricing: It refers to the notional value at which services and goods are

transferred among division (Bouten and Hoozee, 2013, p.334). This type of accounting

system is able to help Sollatek for measuring divisional performance. One of weaknesses

of transfer pricing is that it for the execution of transfer pricings.

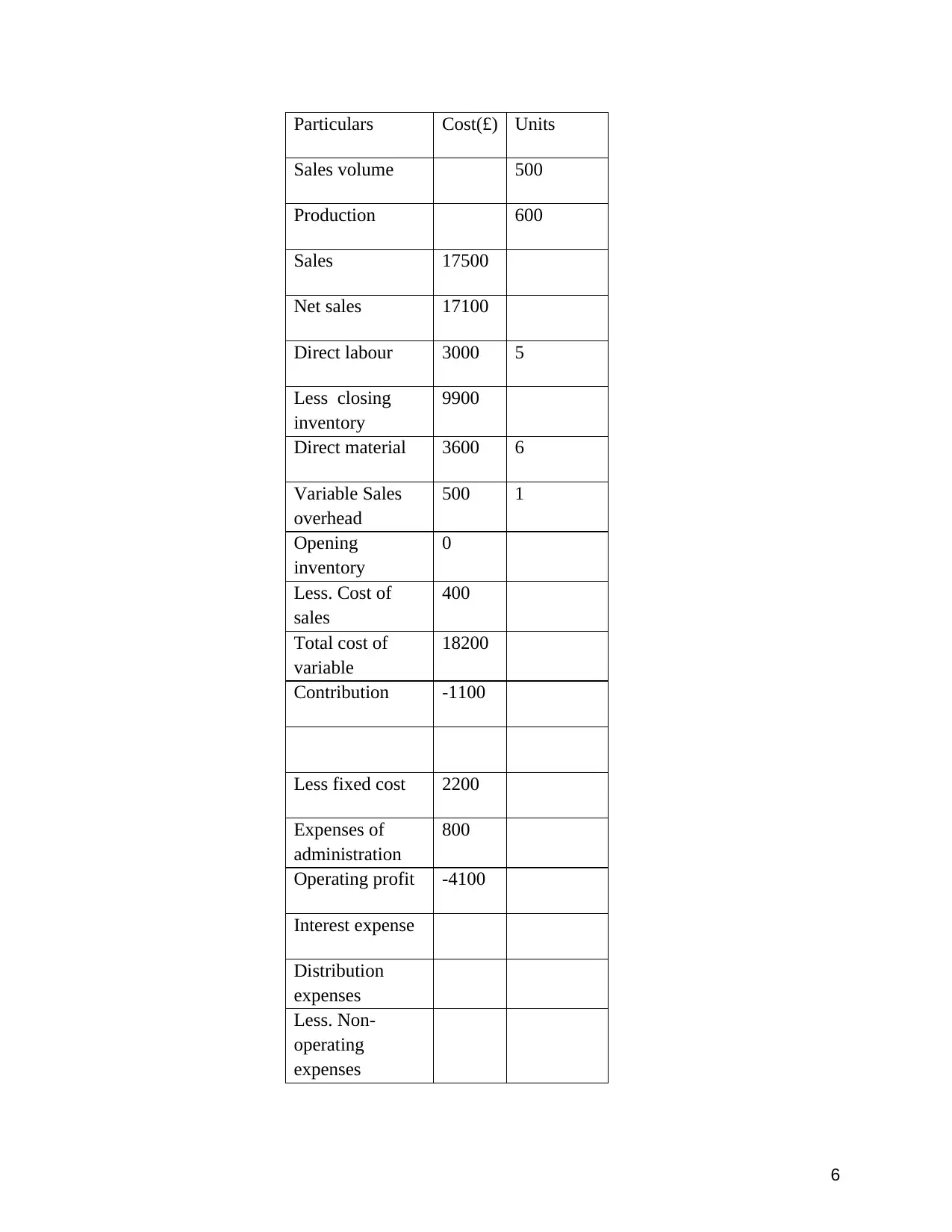

P2 Methods for managing accounting reports

Calculating marginal cost

Marginal costing

Year 1

5

Particulars Cost(£) Units

Sales volume 500

Production 600

Sales 17500

Net sales 17100

Direct labour 3000 5

Less closing

inventory

9900

Direct material 3600 6

Variable Sales

overhead

500 1

Opening

inventory

0

Less. Cost of

sales

400

Total cost of

variable

18200

Contribution -1100

Less fixed cost 2200

Expenses of

administration

800

Operating profit -4100

Interest expense

Distribution

expenses

Less. Non-

operating

expenses

6

Sales volume 500

Production 600

Sales 17500

Net sales 17100

Direct labour 3000 5

Less closing

inventory

9900

Direct material 3600 6

Variable Sales

overhead

500 1

Opening

inventory

0

Less. Cost of

sales

400

Total cost of

variable

18200

Contribution -1100

Less fixed cost 2200

Expenses of

administration

800

Operating profit -4100

Interest expense

Distribution

expenses

Less. Non-

operating

expenses

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less tax -1230

Net profit after

tax

-2870

Net profit before

tax

-4100

Table 1: Marginal cost

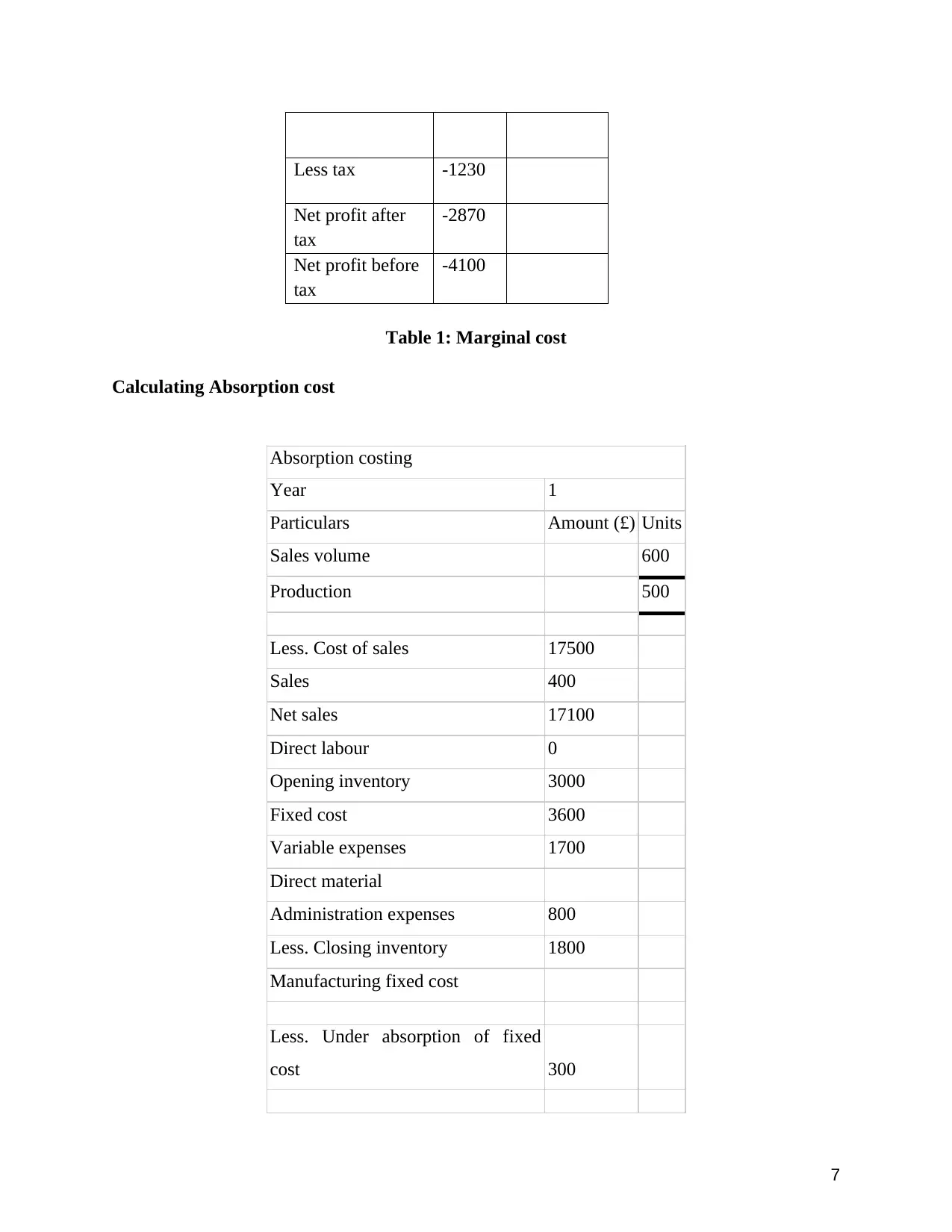

Calculating Absorption cost

Absorption costing

Year 1

Particulars Amount (£) Units

Sales volume 600

Production 500

Less. Cost of sales 17500

Sales 400

Net sales 17100

Direct labour 0

Opening inventory 3000

Fixed cost 3600

Variable expenses 1700

Direct material

Administration expenses 800

Less. Closing inventory 1800

Manufacturing fixed cost

Less. Under absorption of fixed

cost 300

7

Net profit after

tax

-2870

Net profit before

tax

-4100

Table 1: Marginal cost

Calculating Absorption cost

Absorption costing

Year 1

Particulars Amount (£) Units

Sales volume 600

Production 500

Less. Cost of sales 17500

Sales 400

Net sales 17100

Direct labour 0

Opening inventory 3000

Fixed cost 3600

Variable expenses 1700

Direct material

Administration expenses 800

Less. Closing inventory 1800

Manufacturing fixed cost

Less. Under absorption of fixed

cost 300

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit before interest and tax 6900

Less. Interest expenses

Profit before tax 6900

Less. Tax 2070

Profit after tax 4830

Table 2: Absorption cost

Management accounting reports are a method for designing accounting reports to a

company. It provides a framework to an organisation for analysing their capital flow and

investments. The main objective of accounting reports is to assist a firm for planning and

analysing their financial status. Management accounting is solely dependent upon a number of

reports such as cash flow, income and balance sheet reports. All these reposts are used for

examining information of a company.

A small business firm like Sollatek could manage their finances by maintaining an

accounting report (Cleary and Quinn, 2016, p.260). It might help this organisation to keep a track

over their financial assets or resources. Management accounting not only helps an organisation

for providing a guideline for finance but also for taking strategic decision by an organisation.

Sollatek can make use of these techniques in an effective manner for both taking strategic

decision as well as help to achieve financial sustainability. As a accounting manager, it is their

responsibility to use this information for developing appropriate solutions for their business.

8

Less. Interest expenses

Profit before tax 6900

Less. Tax 2070

Profit after tax 4830

Table 2: Absorption cost

Management accounting reports are a method for designing accounting reports to a

company. It provides a framework to an organisation for analysing their capital flow and

investments. The main objective of accounting reports is to assist a firm for planning and

analysing their financial status. Management accounting is solely dependent upon a number of

reports such as cash flow, income and balance sheet reports. All these reposts are used for

examining information of a company.

A small business firm like Sollatek could manage their finances by maintaining an

accounting report (Cleary and Quinn, 2016, p.260). It might help this organisation to keep a track

over their financial assets or resources. Management accounting not only helps an organisation

for providing a guideline for finance but also for taking strategic decision by an organisation.

Sollatek can make use of these techniques in an effective manner for both taking strategic

decision as well as help to achieve financial sustainability. As a accounting manager, it is their

responsibility to use this information for developing appropriate solutions for their business.

8

Figure 1: Accounting Reports

(Source: Self-created)

Cost report:

The accounting manager at Sollatek is able to manage their accounts by computing costs

of products and services. The data take into consideration labour cost, overheads and cost of

products. According to Cooper et al.(2013), cost report is a kind of accounting report that

summarises planning and purposes of profit margins. Budget report is also categorised under

accounting reports and it can be said that a small business like Sollatek could be benefited from

analysis of their budgeting. Performance of this organisation is to be measured by the use of

budget reports. It can be said that owners of Sollatek can use budget report for giving incentives

to their employees. The funds that are budgeted can also be used for providing bonuses to

employees of sollatek.

Performance reports:

Performance reports are another type of management accounting report and it is adopted

by a firm for analysing allocation of revenues and expenditures. One of the advantages of using

performance report is that it gives scope to the account manager for scrutinising using their

9

Accounting

reports

Index

reporting

Performance

reports

Cost report

(Source: Self-created)

Cost report:

The accounting manager at Sollatek is able to manage their accounts by computing costs

of products and services. The data take into consideration labour cost, overheads and cost of

products. According to Cooper et al.(2013), cost report is a kind of accounting report that

summarises planning and purposes of profit margins. Budget report is also categorised under

accounting reports and it can be said that a small business like Sollatek could be benefited from

analysis of their budgeting. Performance of this organisation is to be measured by the use of

budget reports. It can be said that owners of Sollatek can use budget report for giving incentives

to their employees. The funds that are budgeted can also be used for providing bonuses to

employees of sollatek.

Performance reports:

Performance reports are another type of management accounting report and it is adopted

by a firm for analysing allocation of revenues and expenditures. One of the advantages of using

performance report is that it gives scope to the account manager for scrutinising using their

9

Accounting

reports

Index

reporting

Performance

reports

Cost report

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

budgets and also to prepare new budgets. The performance reports are calculated on an annual

basis (Cullen et al. 2013, p.226). However, there are certain companies that need quarterly

reports. Administrators of Sollatek could adopt these perforce reports for forecasting

performance of this company. This system ensures reduction of cost on wastages and utilising

costs for the benefit of a firm.

Index reporting:

Index reporting provides actual status of assets and it enables an organisation to identify the

outcomes of a work. The data that are obtained from index reposts are mainly taken from

economic accounting. Small business need to plan their resources as per the budget requirements

and it is the responsibility of account department to maintain accounting reports for managing

resources in planned way. Budget planning is an important aspect of account management and it

need to be regulated and reviewed by account manager (Dixon and Gaffikin, 2014, p.702). A

number of tools are used for management accounting report and these are as follows:

❏ Simulations

❏ KPI

❏ Balance scorecards

❏ Financial modeling

❏ Management information system

In order to run a business in an effective way, these tools are sued by an organisation for

consulting account management reports. Account managers are able to take strategic decision

based upon these reports.

Apart from benefits, management accounting reposts also have certain demerits. Some of its

limitations are as follows:

Bias: As per the viewpoint of Ellington and Williams, (2013, p.502), management

accounting reports are often charged of personal bias. This is because interpretation or

analysis of these reports is totally based on ability of analyst.

Limited Knowledge: Lack of knowledge in the costing, economics and statistic might

pose a threat to a firm. Analysis of this report needed to be conducted in an ethical

manner otherwise it might give misinformation to stakeholders about capital investment

of an organisation.

10

basis (Cullen et al. 2013, p.226). However, there are certain companies that need quarterly

reports. Administrators of Sollatek could adopt these perforce reports for forecasting

performance of this company. This system ensures reduction of cost on wastages and utilising

costs for the benefit of a firm.

Index reporting:

Index reporting provides actual status of assets and it enables an organisation to identify the

outcomes of a work. The data that are obtained from index reposts are mainly taken from

economic accounting. Small business need to plan their resources as per the budget requirements

and it is the responsibility of account department to maintain accounting reports for managing

resources in planned way. Budget planning is an important aspect of account management and it

need to be regulated and reviewed by account manager (Dixon and Gaffikin, 2014, p.702). A

number of tools are used for management accounting report and these are as follows:

❏ Simulations

❏ KPI

❏ Balance scorecards

❏ Financial modeling

❏ Management information system

In order to run a business in an effective way, these tools are sued by an organisation for

consulting account management reports. Account managers are able to take strategic decision

based upon these reports.

Apart from benefits, management accounting reposts also have certain demerits. Some of its

limitations are as follows:

Bias: As per the viewpoint of Ellington and Williams, (2013, p.502), management

accounting reports are often charged of personal bias. This is because interpretation or

analysis of these reports is totally based on ability of analyst.

Limited Knowledge: Lack of knowledge in the costing, economics and statistic might

pose a threat to a firm. Analysis of this report needed to be conducted in an ethical

manner otherwise it might give misinformation to stakeholders about capital investment

of an organisation.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

L.O. 2

P3 Calculating costs by using useful techniques

The tables mentioned above indicate towards the differences that are encountered in both

the management techniques for accounting. It has been found that different costs are charged in

regards to overall cost heads. The table is indicating towards the fact that differences between

absorption and marginal costing are significant. The table that is representing marginal costs

shows that a business organisation is able to take into consideration the variable expenses. At the

time of calculating absorption costs, the organisation is able to utilise fixed cost. It is found that

an increase in the marginal cost show that the firm is gaining profit. A firm’s profit margin are

well represented through increase in the marginal costing (Francioli and Quagli, 2016, p.20). On

the other hand, it has been found that the company is incurring losses in terms of absorption

costs. The above table is showing that the profit earned by the firm is £ 4830. Contribution

margin is adopted for consideration profits of the firm. In absorption cost, profit seems to be

about £ -2870. It can be assessed that this firm is incurring lows in the absorption costing. This

firm is required to increase their absorption techniques for developing their firm and earning

more profits. Net profits are an important way to find out marginal cost.

L.O.3

P4 Advantages and disadvantages of budgetary control tools

Budgetary control is an important tool that is used by a small business organisation for

preparing an analysis for finances in the future periods. An analysis of budgetary control helps an

organisation to measure performances of a firm. Some of the objectives of budgetary controls are

as follows, it increases profitability of a firm. Budgetary control tools are a centralized form of

control system. It aims at determining objectives of a firm.

Advantages of budgetary control tools:

The budgetary control tools try to fix targets for a firm to encourage their employees to

work in an effective manner (Fullerton et al. 2014, p.415). If employees are given target then it is

quite easier for them to make efforts for reaching at a fixed goal or target. It can be said that this

control method is a way to keep a track over the activities of a small business organisation.

Coordination can be achieved with the use of budgetary control tools. The cost of production can

11

P3 Calculating costs by using useful techniques

The tables mentioned above indicate towards the differences that are encountered in both

the management techniques for accounting. It has been found that different costs are charged in

regards to overall cost heads. The table is indicating towards the fact that differences between

absorption and marginal costing are significant. The table that is representing marginal costs

shows that a business organisation is able to take into consideration the variable expenses. At the

time of calculating absorption costs, the organisation is able to utilise fixed cost. It is found that

an increase in the marginal cost show that the firm is gaining profit. A firm’s profit margin are

well represented through increase in the marginal costing (Francioli and Quagli, 2016, p.20). On

the other hand, it has been found that the company is incurring losses in terms of absorption

costs. The above table is showing that the profit earned by the firm is £ 4830. Contribution

margin is adopted for consideration profits of the firm. In absorption cost, profit seems to be

about £ -2870. It can be assessed that this firm is incurring lows in the absorption costing. This

firm is required to increase their absorption techniques for developing their firm and earning

more profits. Net profits are an important way to find out marginal cost.

L.O.3

P4 Advantages and disadvantages of budgetary control tools

Budgetary control is an important tool that is used by a small business organisation for

preparing an analysis for finances in the future periods. An analysis of budgetary control helps an

organisation to measure performances of a firm. Some of the objectives of budgetary controls are

as follows, it increases profitability of a firm. Budgetary control tools are a centralized form of

control system. It aims at determining objectives of a firm.

Advantages of budgetary control tools:

The budgetary control tools try to fix targets for a firm to encourage their employees to

work in an effective manner (Fullerton et al. 2014, p.415). If employees are given target then it is

quite easier for them to make efforts for reaching at a fixed goal or target. It can be said that this

control method is a way to keep a track over the activities of a small business organisation.

Coordination can be achieved with the use of budgetary control tools. The cost of production can

11

be minimised because this system aims at eliminating any sort of resource wastage and thereby

helping a firm to retain control over their profit.

Budgetary control brings profit to an organisation by helping manager to take effective

decision based on the budget analysis. Performance of employees could also be improved by

budgetary control (Hiebl et al. 2013, p.120). This is because the budgets can be used by

employers to give incentives to employee which in turn will increase their confidence.

Management gets a guideline regarding the decisions that they are required to take for keeping a

control over their capital investments. Sollatek could get guidelines regarding formulation of

policies and goals for defining finances of their enterprise. The above mentioned advantages

indicate towards the fact that an organisation is able to make use of this budgetary control system

for managing an accounting system.

Disadvantages of budgetary control tools:

In inflationary situation, it is quite difficult for a form, to plan a budget. Budgetary control

system is able to make budgets for future. It can be said that future is unpredictable and therefore

it become quite difficult for analysing a budget without understanding future economic

conditions (Makrygiannakis et al. 2016, p.1235). Top management are responsible for making

budgetary control and in case account manager is not capable enough to monitor the budgets in

an appropriate manner then it might pose a challenge to that organisation's financial statement. A

small organisation like Sollatek is unable to incur heavy expenditures that will be required for

budgetary controls.

It can be assessed that budgetary control tools are able to bring chances of success to any

organisation. According to Quinn and Jackson, (2014, p.208), forecasting techniques are a useful

tool for analysing probability and time series. It could be used for forecasting future costing. On

the contrary future is unpredictable and therefore these techniques are going to represent a false

analysis of costing for any organisation. It has been found that budgeting provides a target to any

firm and this could be taken as an advantage for fixing responsibility to employees. Sollatek is

able to manage department by setting target. Targets could encourage employees to get a

direction and they might move towards a target. Target setting proceed to be useful for a

business. However, it is to be analysed that in the absence of an effective manager, a target

cannot be fixed and therefore it will result in low performance of employees. As argued by

Richardson (2017, p.10), implementation of budgetary techniques might help Sollatek to excel

12

helping a firm to retain control over their profit.

Budgetary control brings profit to an organisation by helping manager to take effective

decision based on the budget analysis. Performance of employees could also be improved by

budgetary control (Hiebl et al. 2013, p.120). This is because the budgets can be used by

employers to give incentives to employee which in turn will increase their confidence.

Management gets a guideline regarding the decisions that they are required to take for keeping a

control over their capital investments. Sollatek could get guidelines regarding formulation of

policies and goals for defining finances of their enterprise. The above mentioned advantages

indicate towards the fact that an organisation is able to make use of this budgetary control system

for managing an accounting system.

Disadvantages of budgetary control tools:

In inflationary situation, it is quite difficult for a form, to plan a budget. Budgetary control

system is able to make budgets for future. It can be said that future is unpredictable and therefore

it become quite difficult for analysing a budget without understanding future economic

conditions (Makrygiannakis et al. 2016, p.1235). Top management are responsible for making

budgetary control and in case account manager is not capable enough to monitor the budgets in

an appropriate manner then it might pose a challenge to that organisation's financial statement. A

small organisation like Sollatek is unable to incur heavy expenditures that will be required for

budgetary controls.

It can be assessed that budgetary control tools are able to bring chances of success to any

organisation. According to Quinn and Jackson, (2014, p.208), forecasting techniques are a useful

tool for analysing probability and time series. It could be used for forecasting future costing. On

the contrary future is unpredictable and therefore these techniques are going to represent a false

analysis of costing for any organisation. It has been found that budgeting provides a target to any

firm and this could be taken as an advantage for fixing responsibility to employees. Sollatek is

able to manage department by setting target. Targets could encourage employees to get a

direction and they might move towards a target. Target setting proceed to be useful for a

business. However, it is to be analysed that in the absence of an effective manager, a target

cannot be fixed and therefore it will result in low performance of employees. As argued by

Richardson (2017, p.10), implementation of budgetary techniques might help Sollatek to excel

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.