Accounting Solved Assignments

VerifiedAdded on 2019/11/26

|15

|2372

|14

Homework Assignment

AI Summary

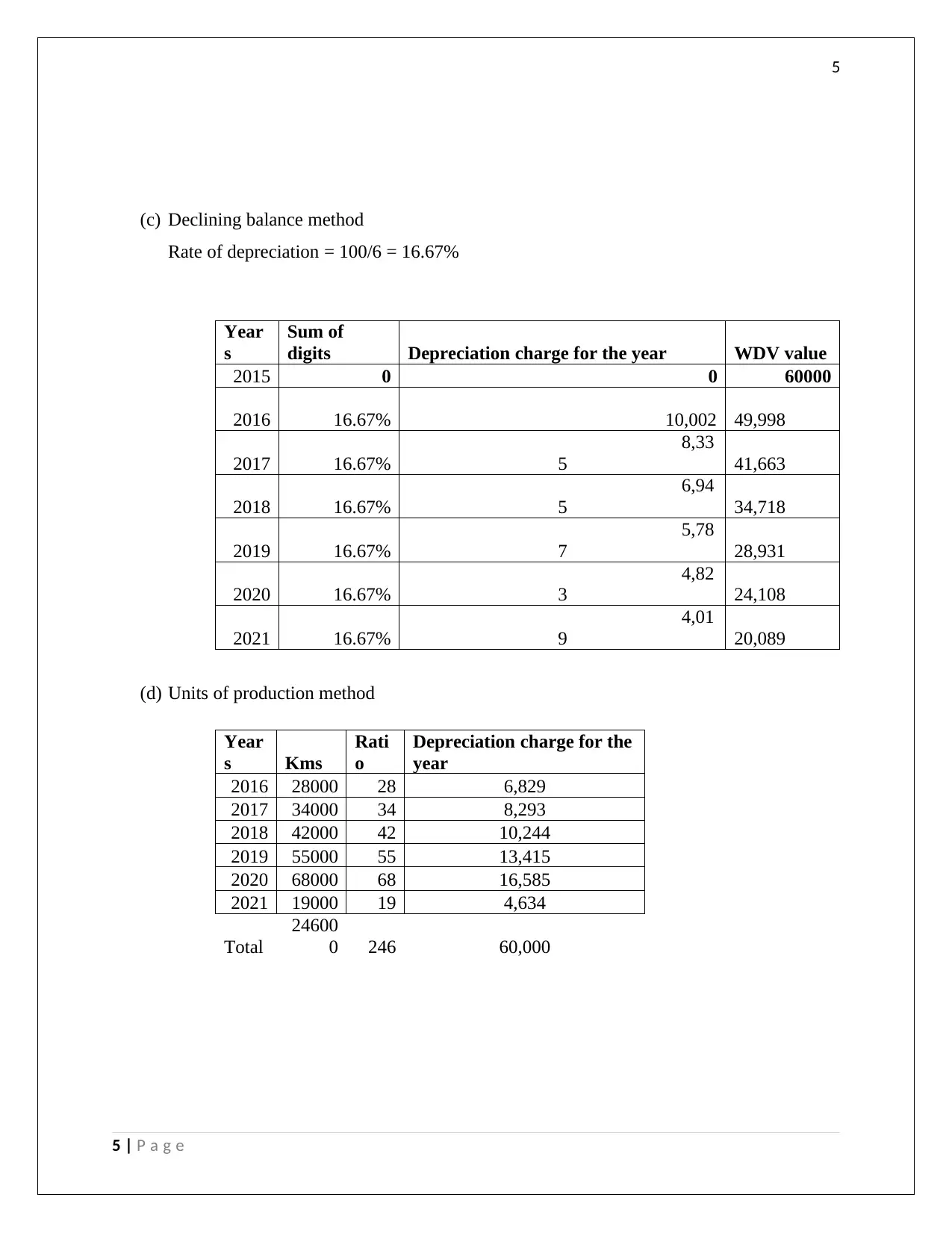

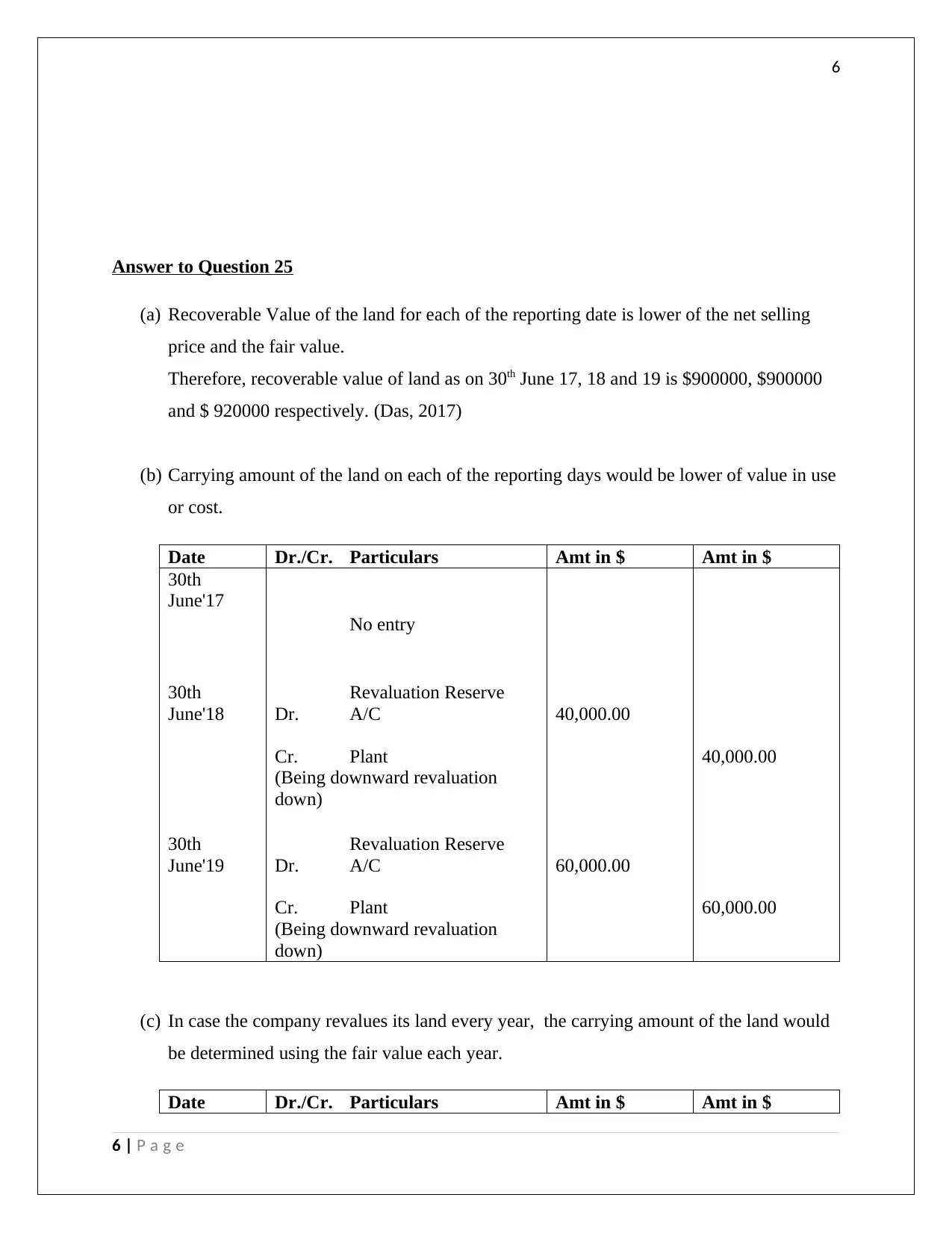

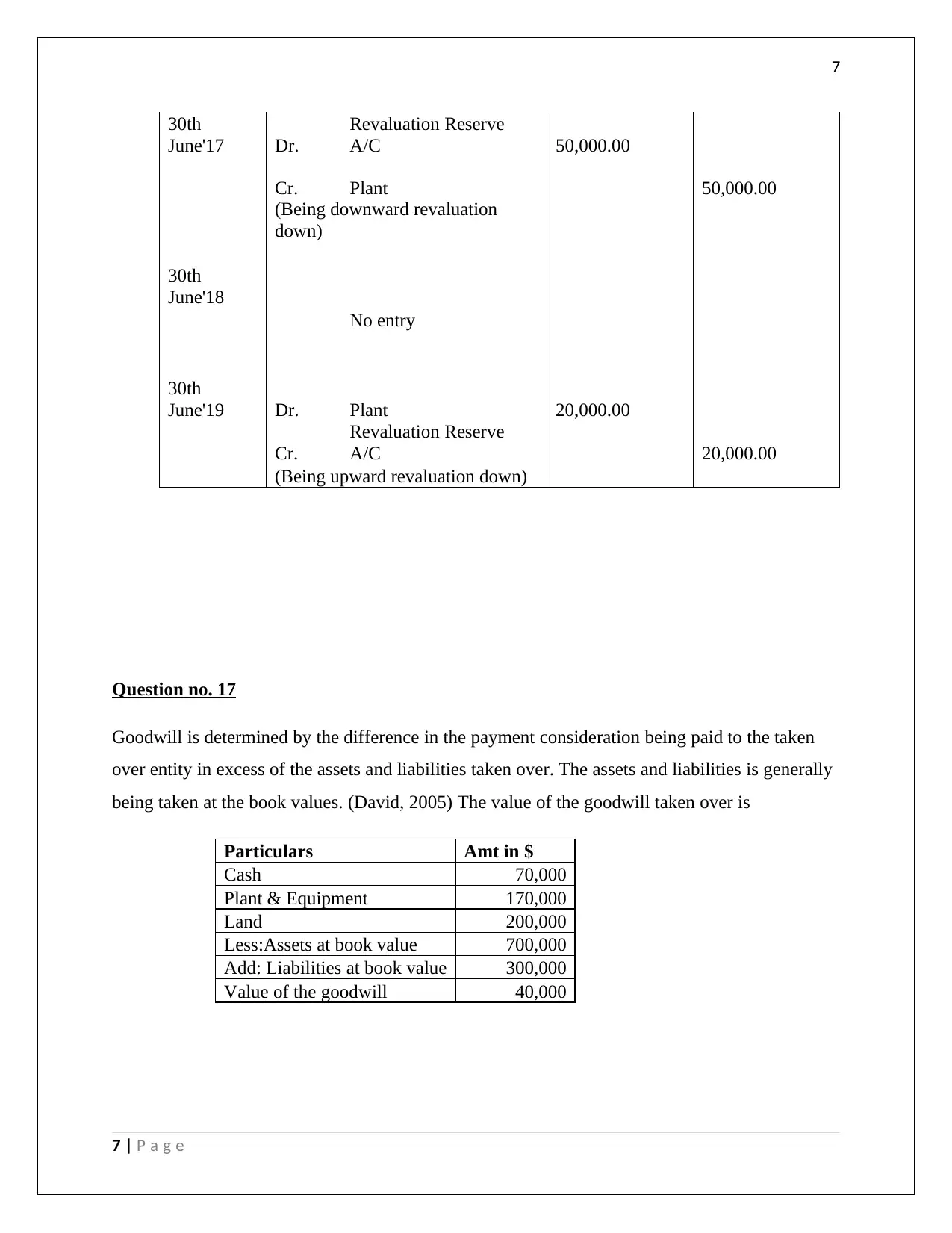

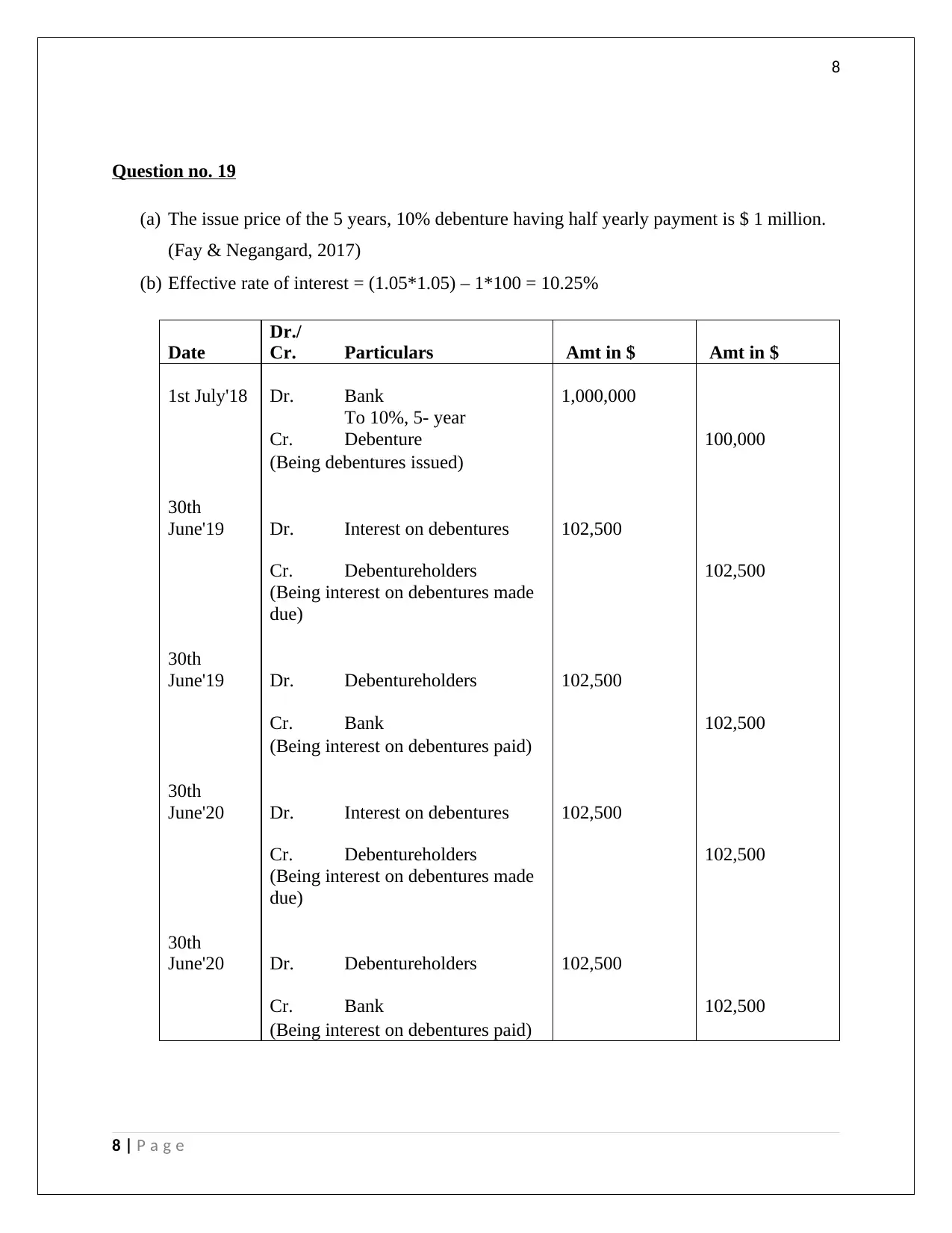

This document contains solved assignments for an accounting course. It includes solutions to various questions covering topics such as plant capitalization, depreciation methods (straight-line, sum-of-the-digits, declining balance, units of production), land valuation, goodwill calculation, debenture accounting, lease accounting, foreign currency translation, and bonus share issuance. Each question is answered with detailed calculations and journal entries where applicable. The solutions also cite relevant accounting standards and refer to several academic papers for further reading. The document is presented in a format suitable for students seeking assistance with their accounting homework.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.