Accounting Assignment

VerifiedAdded on 2019/11/20

|7

|1204

|213

Homework Assignment

AI Summary

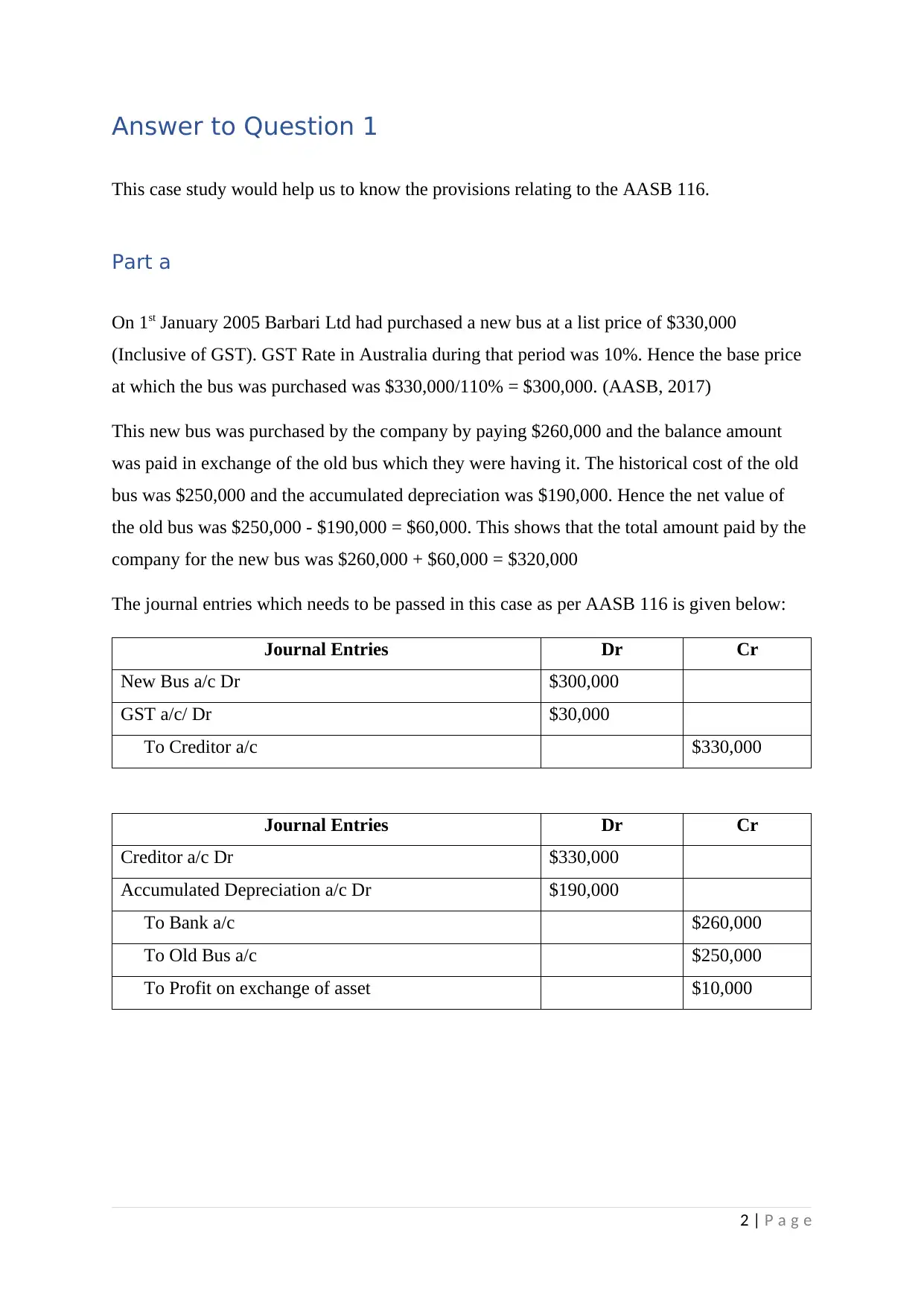

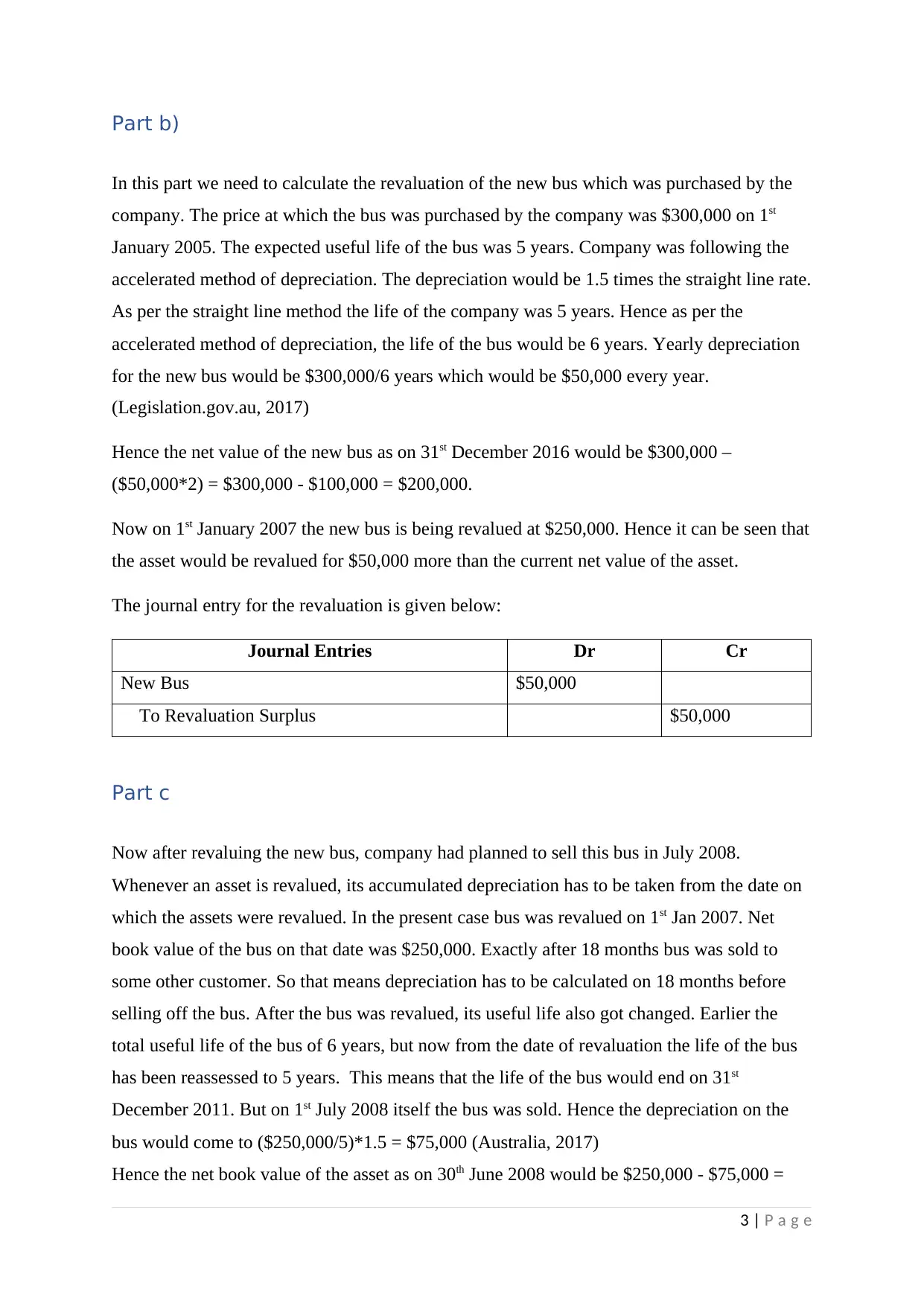

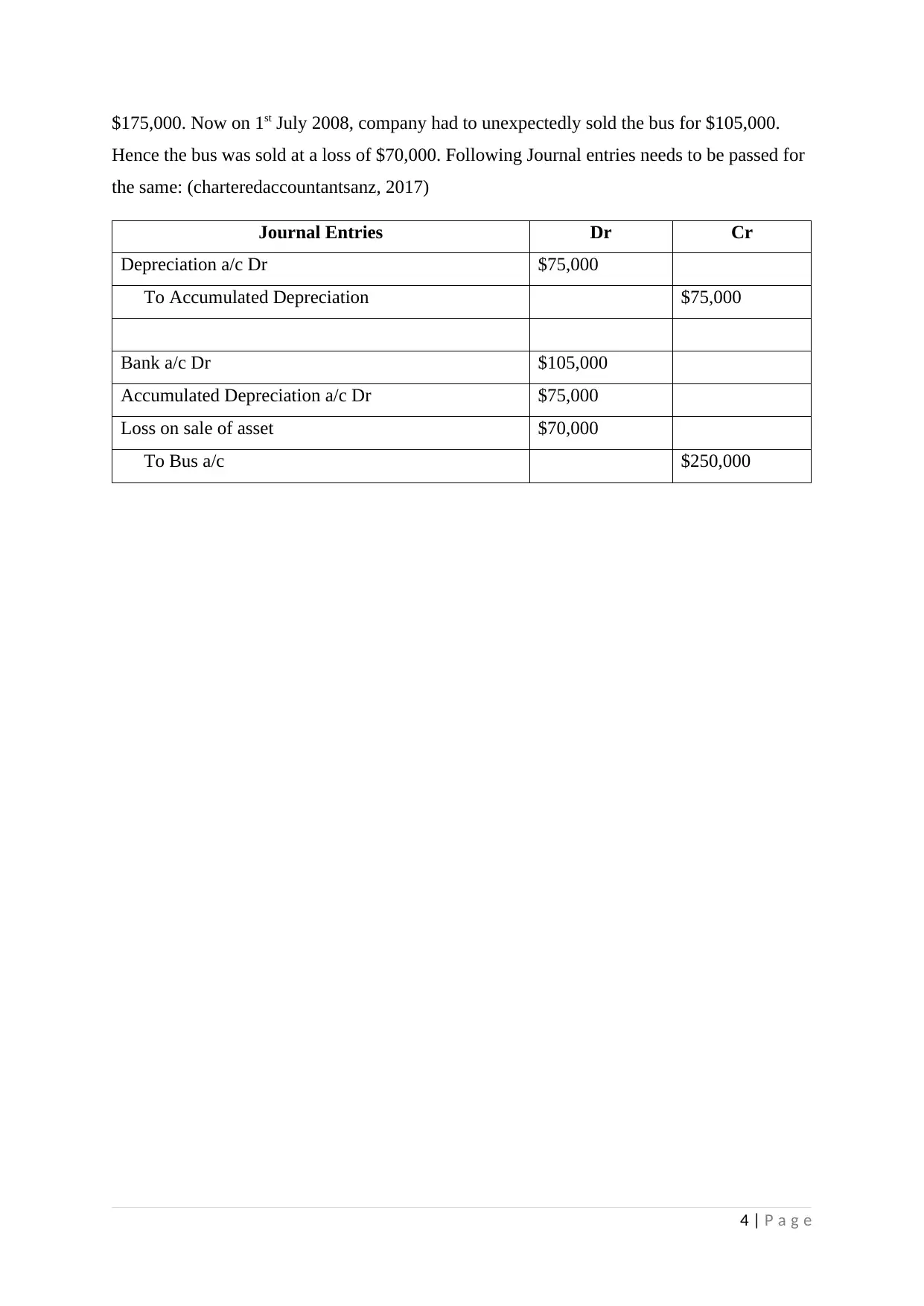

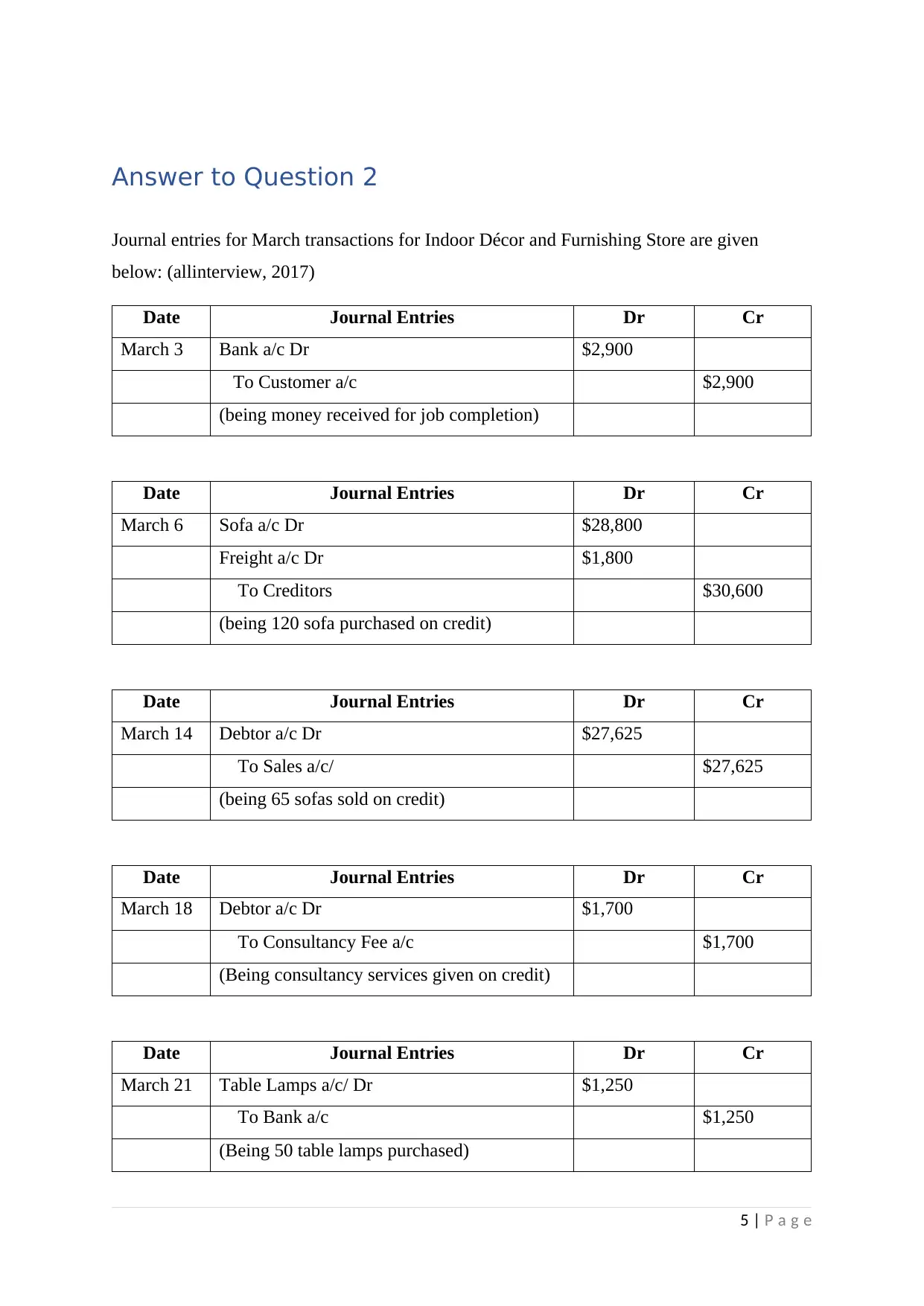

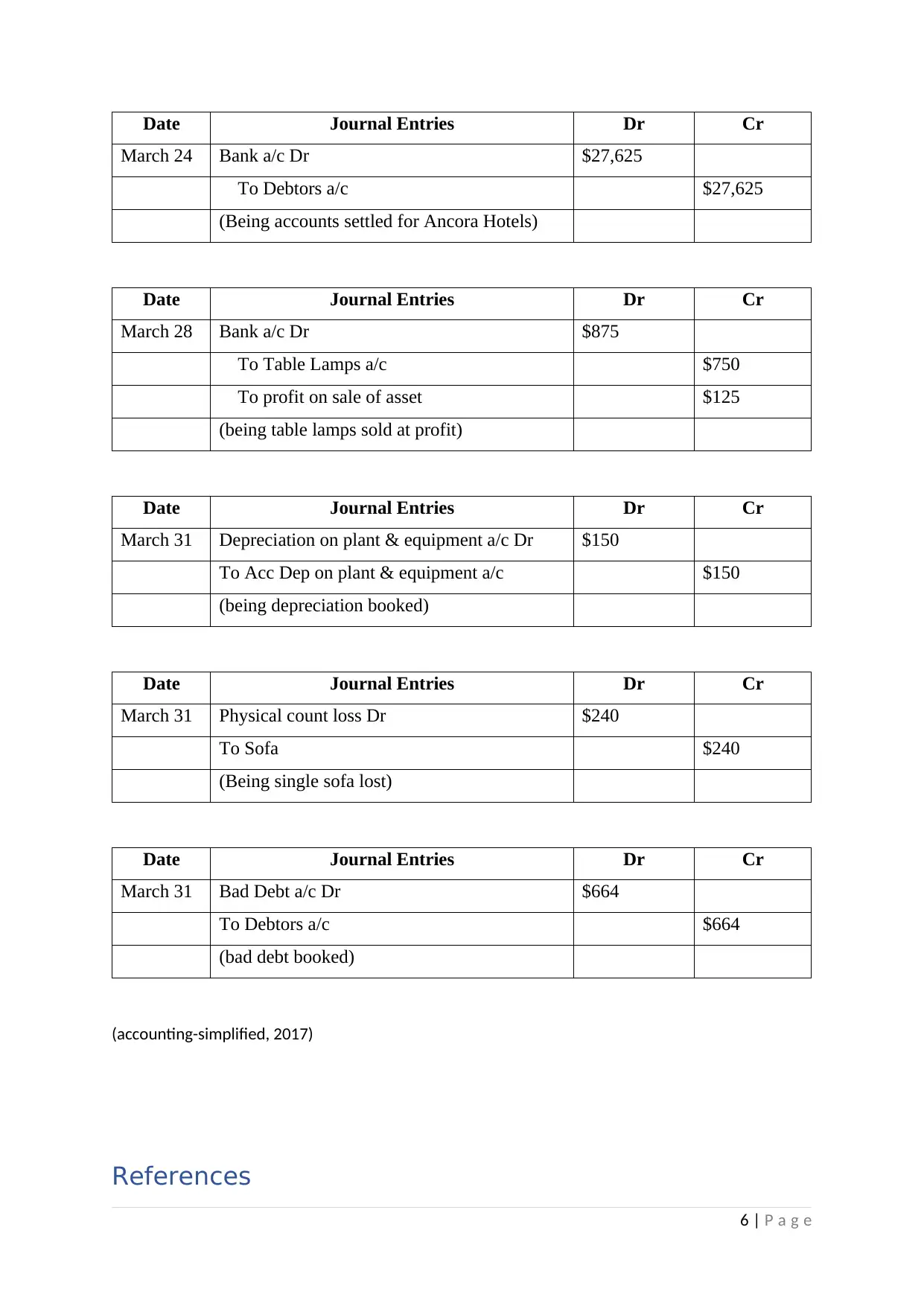

This document presents solutions to an accounting assignment. The first question is a case study involving Barbari Ltd., focusing on AASB 116 (Property, Plant and Equipment). It covers the accounting treatment of a bus purchase involving a trade-in, depreciation calculations using the accelerated method, asset revaluation, and the accounting implications of the subsequent sale of the bus. Detailed journal entries are provided for each transaction. The second question involves preparing journal entries for various transactions of Indoor Décor and Furnishing Store during the month of March, including sales, purchases, consultancy fees, and bad debts. The solutions demonstrate a thorough understanding of accounting principles and procedures, with references to relevant standards and websites.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.