Management Accounting Report: Sonic Healthcare Remuneration Review

VerifiedAdded on 2020/02/18

|5

|1061

|44

Report

AI Summary

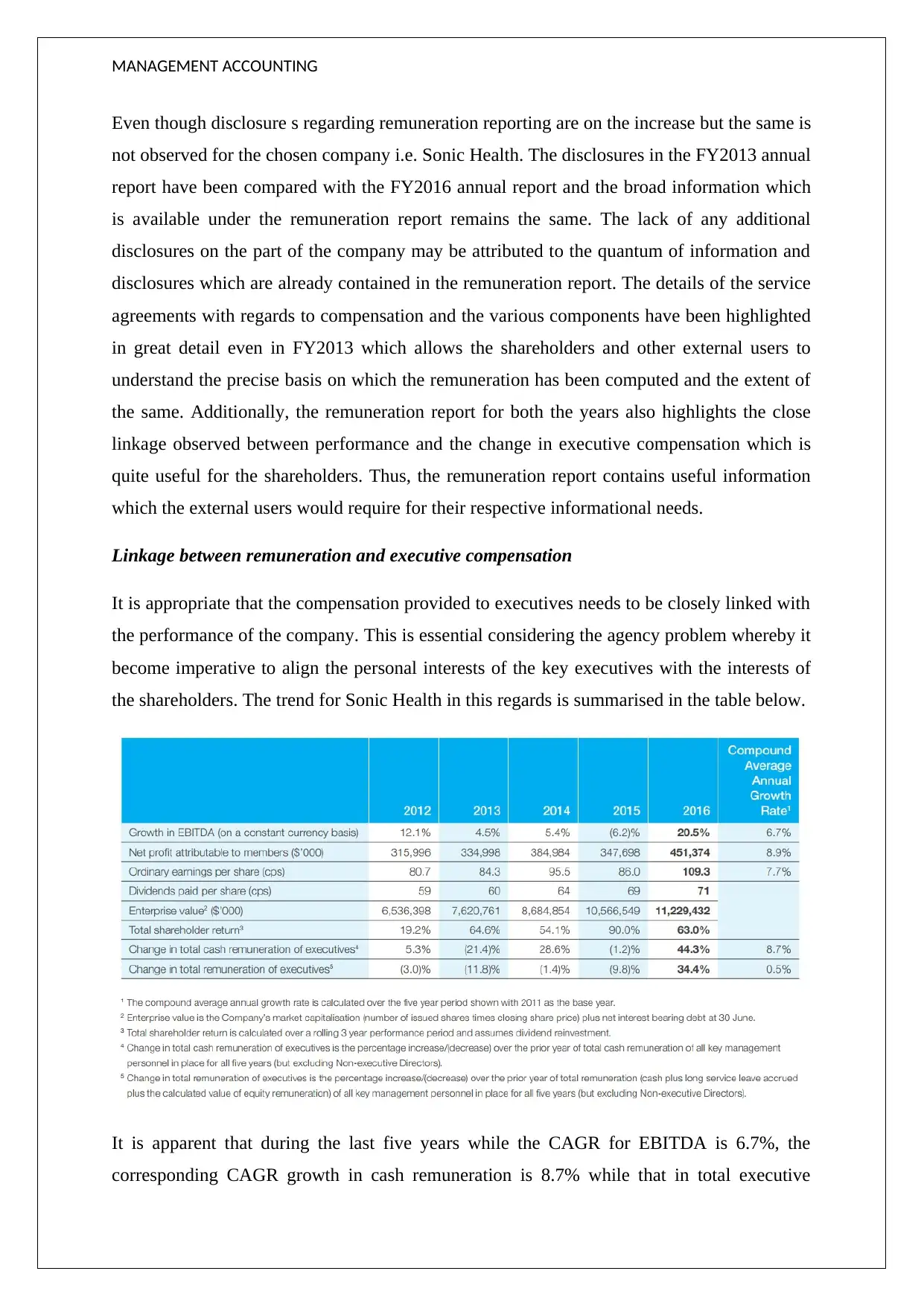

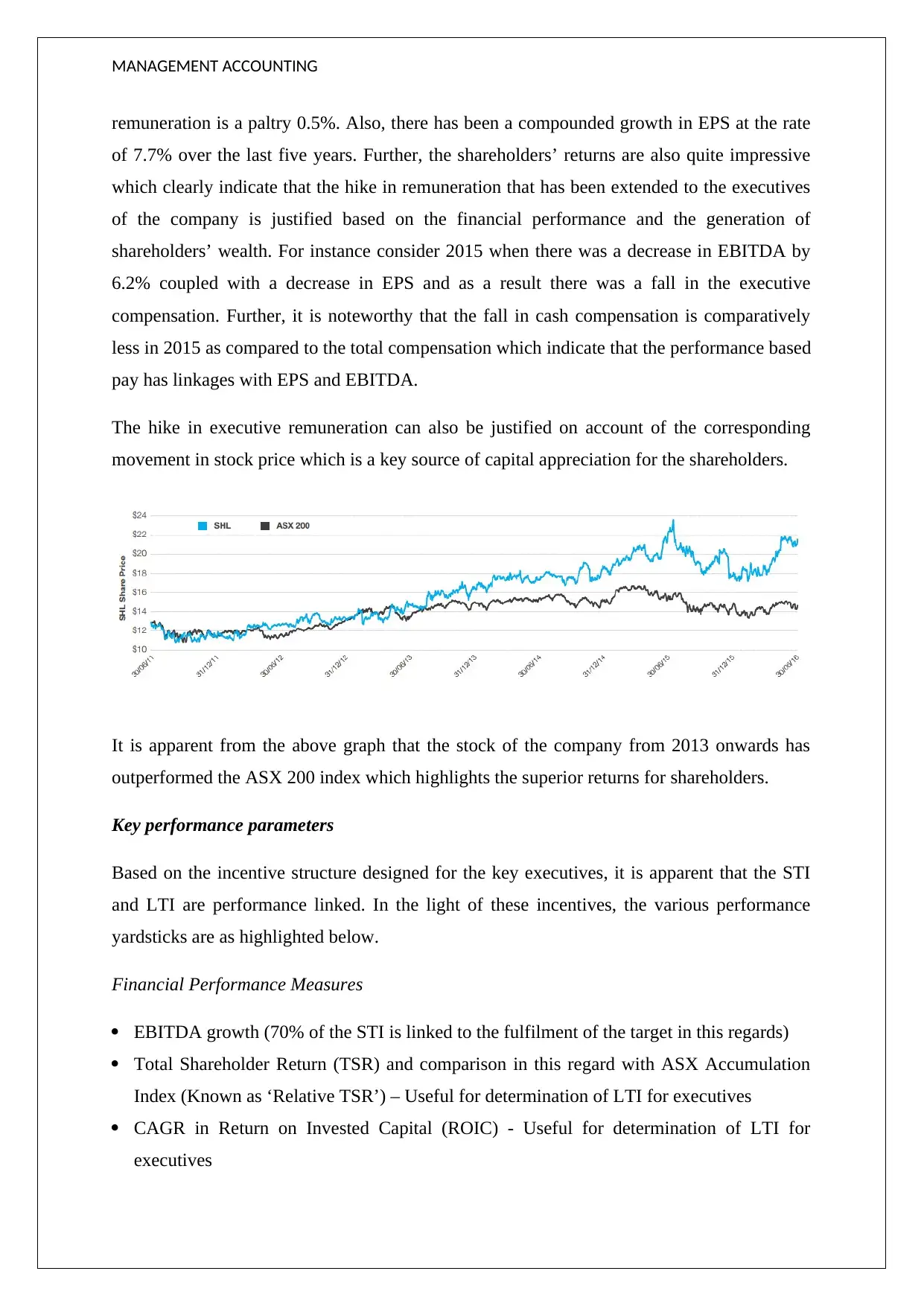

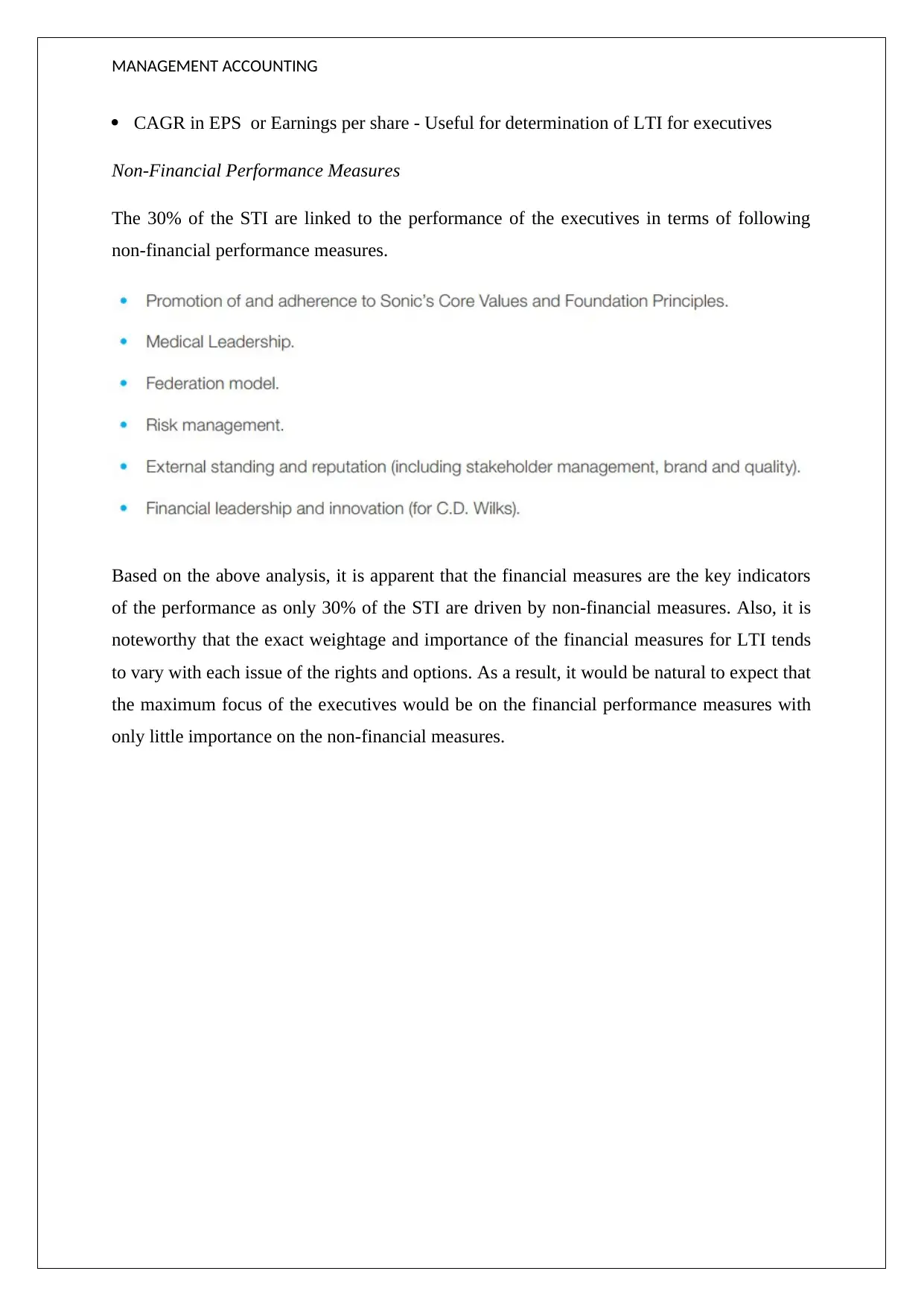

This report provides an analysis of Sonic Healthcare's remuneration report, focusing on the company's executive compensation structure and its link to financial performance. The report examines the use of incentives, including fixed remuneration, short-term incentives (STI) based on EBITDA growth, and long-term incentives (LTI) linked to multi-year performance metrics like TSR and ROIC. It highlights the modifications in executive remuneration reporting over time and assesses the linkage between remuneration and executive compensation, demonstrating how executive pay aligns with company performance and shareholder returns. Key performance parameters, both financial (EBITDA, EPS, ROIC) and non-financial, are discussed, revealing the weightage of financial measures in determining executive compensation. The report concludes that the company's remuneration practices are closely tied to financial performance, justifying executive compensation based on financial results and shareholder wealth generation.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.