Analysis of Accounting Theory and Issues: Sonic Healthcare Report

VerifiedAdded on 2020/05/28

|19

|3133

|124

Report

AI Summary

This report provides a comprehensive analysis of Sonic Healthcare's compliance with the Australian Accounting Standards Board (AASB) conceptual framework and General Purpose Financial Reporting (GPFR). It examines the company's financial performance from 2013 to 2017, highlighting a decline in key financial parameters like EBITDA and net profit after tax in 2017, while revenue increased. The report assesses Sonic Healthcare's adherence to AASB standards regarding Property, Plant, and Equipment (PPE), contingent liabilities, inventories, revenue recognition, and dividend reporting. It also discusses the company's remuneration report and recent news, including insider trading activity. The analysis indicates Sonic Healthcare's full compliance with AASB standards and provides a critical evaluation of its financial position, concluding with a recommendation for investors. The report also includes extracts from the company's annual reports to support its analysis.

Running head: ACCOUNTING THEORY AND ISSUES

Accounting Theory and Issues

Name of the Student

Name of the University

Author’s Note

Accounting Theory and Issues

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ACCOUNTING THEORY AND ISSUES

Executive Summary

This report takes an attempt to analyze the compliance of Sonic Healthcare with the principles

and standards of the conceptual framework of AASB. The analysis indicates towards the decline

in financial performance of Sonic Healthcare in 2017. It can be seen that Sonic Healthcare has

full adherence to the standards and principles of AASB conceptual framework and GPFR. The

report also discusses about a recent tax fraud case of Sonic Healthcare. Lastly, the report

provides suggestion to the investor whether to invest in the company or not.

Executive Summary

This report takes an attempt to analyze the compliance of Sonic Healthcare with the principles

and standards of the conceptual framework of AASB. The analysis indicates towards the decline

in financial performance of Sonic Healthcare in 2017. It can be seen that Sonic Healthcare has

full adherence to the standards and principles of AASB conceptual framework and GPFR. The

report also discusses about a recent tax fraud case of Sonic Healthcare. Lastly, the report

provides suggestion to the investor whether to invest in the company or not.

2ACCOUNTING THEORY AND ISSUES

Table of Contents

Introduction......................................................................................................................................3

Company Profile..............................................................................................................................3

Conceptual Framework....................................................................................................................5

General Purpose Financial Reporting (GPFR)................................................................................6

Remuneration Report.......................................................................................................................7

Critical Analysis..............................................................................................................................8

Property, Plant and Equipment (PPE).........................................................................................8

Contingent Liability.....................................................................................................................9

Inventories.................................................................................................................................10

Revenue.....................................................................................................................................10

Dividends...................................................................................................................................11

Recent News..................................................................................................................................12

Comparison....................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................16

Table of Contents

Introduction......................................................................................................................................3

Company Profile..............................................................................................................................3

Conceptual Framework....................................................................................................................5

General Purpose Financial Reporting (GPFR)................................................................................6

Remuneration Report.......................................................................................................................7

Critical Analysis..............................................................................................................................8

Property, Plant and Equipment (PPE).........................................................................................8

Contingent Liability.....................................................................................................................9

Inventories.................................................................................................................................10

Revenue.....................................................................................................................................10

Dividends...................................................................................................................................11

Recent News..................................................................................................................................12

Comparison....................................................................................................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ACCOUNTING THEORY AND ISSUES

Introduction

The main objective of this report lies in the analysis and evaluation of the compliance of

different standards of accounting conceptual framework and general purpose financial reporting

by one Australian company. For the progress of this report, Sonic Healthcare Limited (Sonic

Healthcare) is taken into consideration for the purpose of analysis and evaluation. On a broader

note, the report aims at the analysis of the importance of conceptual framework for the

preparation and presentation of the financial statements of the selected organization (Nobes,

2014). It can be seen that Australia has a well developed conceptual framework provided by the

Australian Accounting Standard Board (AASB) for the Australian organizations to get assistance

in the process of financial reporting. Moreover, AASB has put the obligation on the Australian

companies to adhere to the regulations and standards of AASB conceptual framework in the

process of their financial reporting (Hope, Thomas & Vyas, 2013). This report consists of some

specific parts that analyze various dimensions of the conceptual framework and general purpose

financial reporting for Sonic Healthcare. Based on the outcome of the overall analysis, the

appropriate suggestion for the investors is provided in the conclusion part.

Company Profile

Sonic Healthcare is considered as one of the leading companies in Australia involved in

providing laboratory services, pathology services and radiology services. The company was

established in the year of 1987 and it is headquartered at Macquarie Park, Sydney, New South

Wales, Australia. The worldwide reputation of Sonic Healthcare can be seen in laboratory,

medicine, radiology and other diagnostic services. Apart from Australia, Sonic Healthcare has its

Introduction

The main objective of this report lies in the analysis and evaluation of the compliance of

different standards of accounting conceptual framework and general purpose financial reporting

by one Australian company. For the progress of this report, Sonic Healthcare Limited (Sonic

Healthcare) is taken into consideration for the purpose of analysis and evaluation. On a broader

note, the report aims at the analysis of the importance of conceptual framework for the

preparation and presentation of the financial statements of the selected organization (Nobes,

2014). It can be seen that Australia has a well developed conceptual framework provided by the

Australian Accounting Standard Board (AASB) for the Australian organizations to get assistance

in the process of financial reporting. Moreover, AASB has put the obligation on the Australian

companies to adhere to the regulations and standards of AASB conceptual framework in the

process of their financial reporting (Hope, Thomas & Vyas, 2013). This report consists of some

specific parts that analyze various dimensions of the conceptual framework and general purpose

financial reporting for Sonic Healthcare. Based on the outcome of the overall analysis, the

appropriate suggestion for the investors is provided in the conclusion part.

Company Profile

Sonic Healthcare is considered as one of the leading companies in Australia involved in

providing laboratory services, pathology services and radiology services. The company was

established in the year of 1987 and it is headquartered at Macquarie Park, Sydney, New South

Wales, Australia. The worldwide reputation of Sonic Healthcare can be seen in laboratory,

medicine, radiology and other diagnostic services. Apart from Australia, Sonic Healthcare has its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ACCOUNTING THEORY AND ISSUES

presence in the countries like USA, Switzerland, Germany, Belgium, United Kingdom, New

Zealand and New Zealand (sonichealthcare.com, 2018).

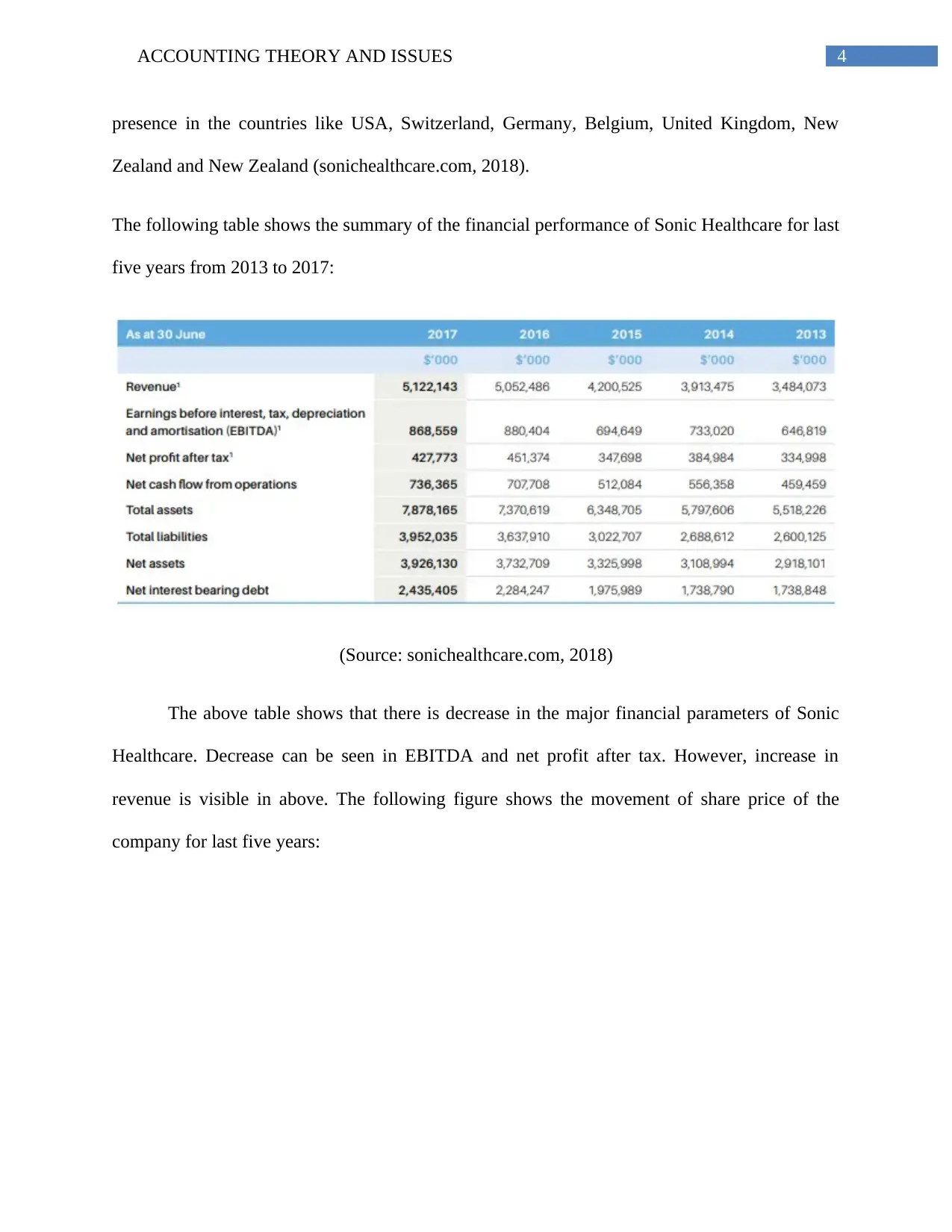

The following table shows the summary of the financial performance of Sonic Healthcare for last

five years from 2013 to 2017:

(Source: sonichealthcare.com, 2018)

The above table shows that there is decrease in the major financial parameters of Sonic

Healthcare. Decrease can be seen in EBITDA and net profit after tax. However, increase in

revenue is visible in above. The following figure shows the movement of share price of the

company for last five years:

presence in the countries like USA, Switzerland, Germany, Belgium, United Kingdom, New

Zealand and New Zealand (sonichealthcare.com, 2018).

The following table shows the summary of the financial performance of Sonic Healthcare for last

five years from 2013 to 2017:

(Source: sonichealthcare.com, 2018)

The above table shows that there is decrease in the major financial parameters of Sonic

Healthcare. Decrease can be seen in EBITDA and net profit after tax. However, increase in

revenue is visible in above. The following figure shows the movement of share price of the

company for last five years:

5ACCOUNTING THEORY AND ISSUES

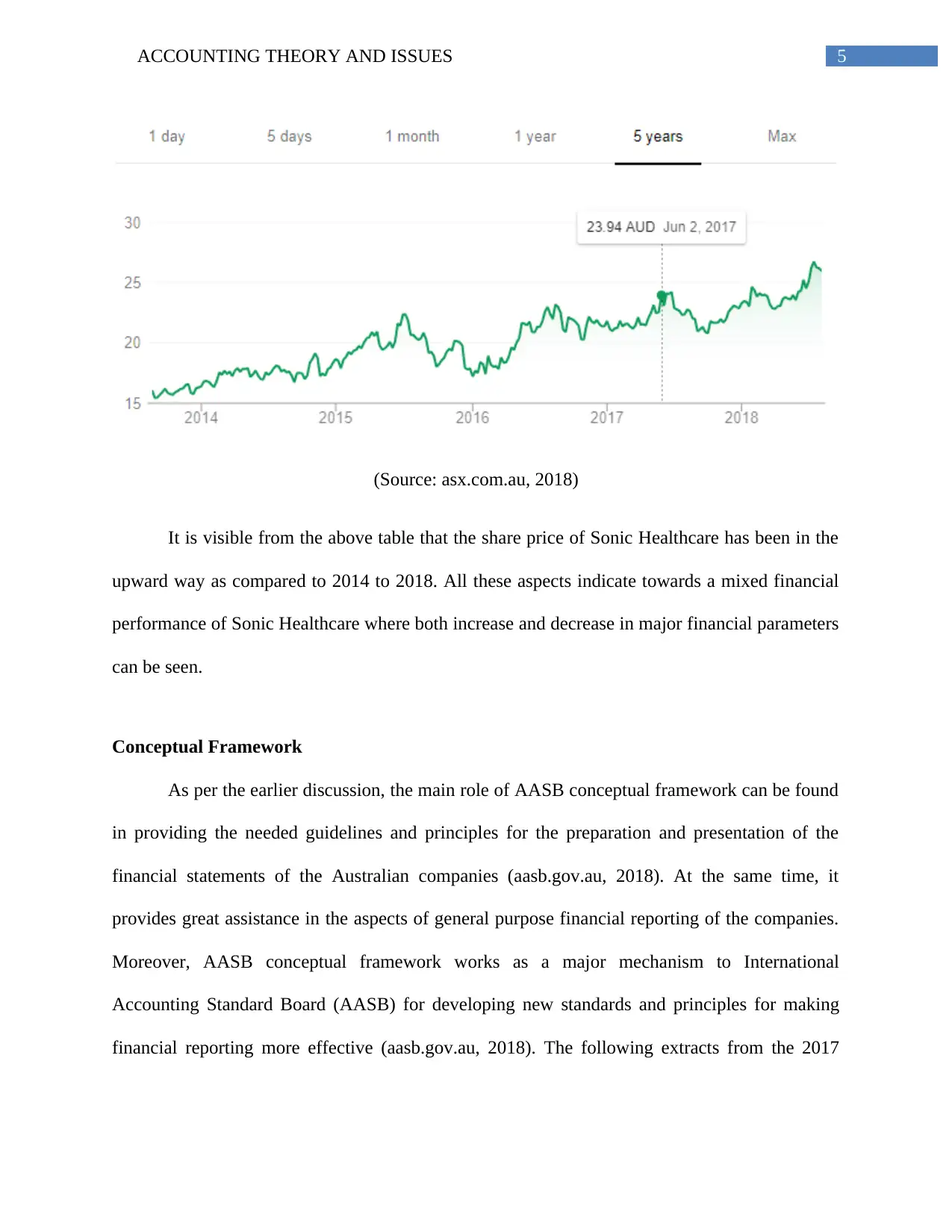

(Source: asx.com.au, 2018)

It is visible from the above table that the share price of Sonic Healthcare has been in the

upward way as compared to 2014 to 2018. All these aspects indicate towards a mixed financial

performance of Sonic Healthcare where both increase and decrease in major financial parameters

can be seen.

Conceptual Framework

As per the earlier discussion, the main role of AASB conceptual framework can be found

in providing the needed guidelines and principles for the preparation and presentation of the

financial statements of the Australian companies (aasb.gov.au, 2018). At the same time, it

provides great assistance in the aspects of general purpose financial reporting of the companies.

Moreover, AASB conceptual framework works as a major mechanism to International

Accounting Standard Board (AASB) for developing new standards and principles for making

financial reporting more effective (aasb.gov.au, 2018). The following extracts from the 2017

(Source: asx.com.au, 2018)

It is visible from the above table that the share price of Sonic Healthcare has been in the

upward way as compared to 2014 to 2018. All these aspects indicate towards a mixed financial

performance of Sonic Healthcare where both increase and decrease in major financial parameters

can be seen.

Conceptual Framework

As per the earlier discussion, the main role of AASB conceptual framework can be found

in providing the needed guidelines and principles for the preparation and presentation of the

financial statements of the Australian companies (aasb.gov.au, 2018). At the same time, it

provides great assistance in the aspects of general purpose financial reporting of the companies.

Moreover, AASB conceptual framework works as a major mechanism to International

Accounting Standard Board (AASB) for developing new standards and principles for making

financial reporting more effective (aasb.gov.au, 2018). The following extracts from the 2017

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ACCOUNTING THEORY AND ISSUES

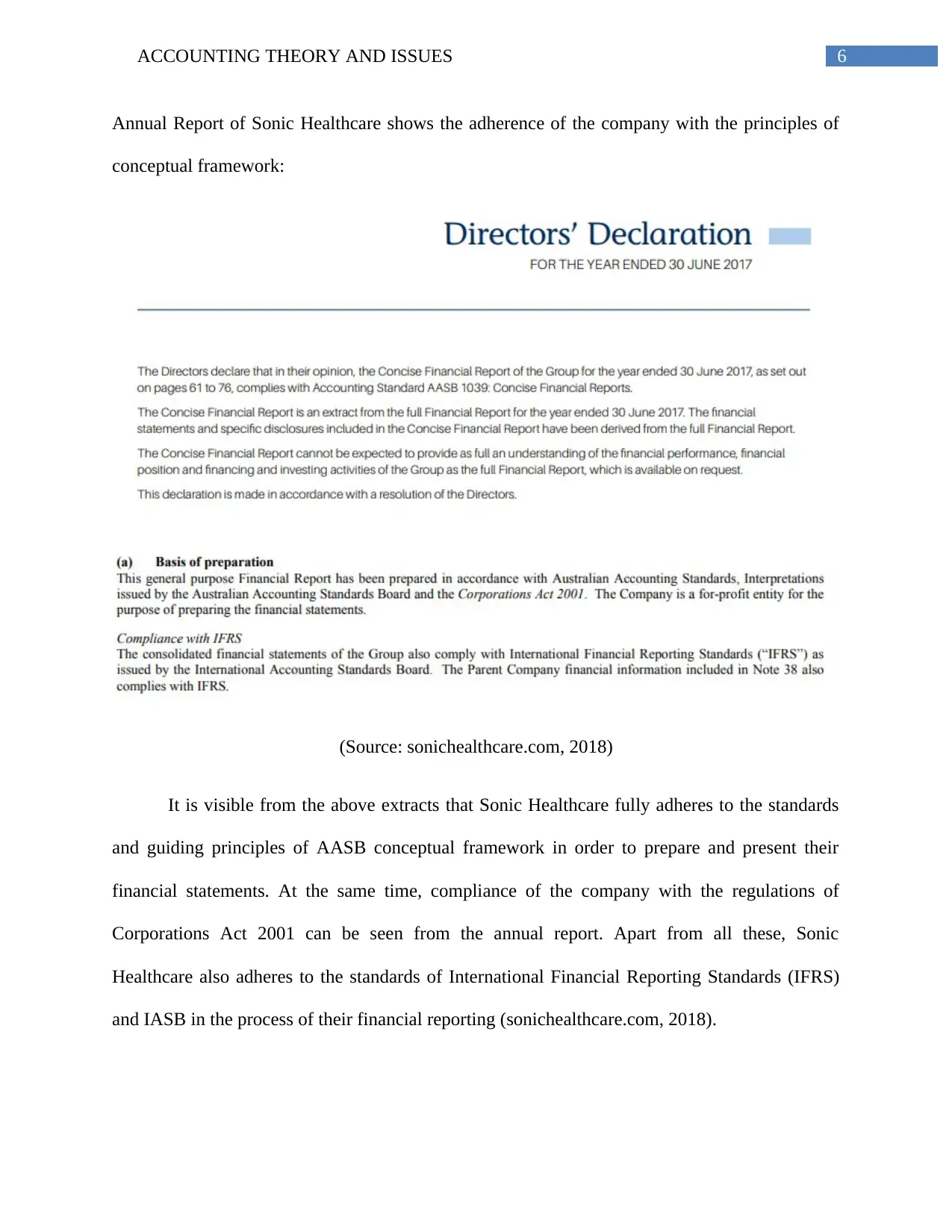

Annual Report of Sonic Healthcare shows the adherence of the company with the principles of

conceptual framework:

(Source: sonichealthcare.com, 2018)

It is visible from the above extracts that Sonic Healthcare fully adheres to the standards

and guiding principles of AASB conceptual framework in order to prepare and present their

financial statements. At the same time, compliance of the company with the regulations of

Corporations Act 2001 can be seen from the annual report. Apart from all these, Sonic

Healthcare also adheres to the standards of International Financial Reporting Standards (IFRS)

and IASB in the process of their financial reporting (sonichealthcare.com, 2018).

Annual Report of Sonic Healthcare shows the adherence of the company with the principles of

conceptual framework:

(Source: sonichealthcare.com, 2018)

It is visible from the above extracts that Sonic Healthcare fully adheres to the standards

and guiding principles of AASB conceptual framework in order to prepare and present their

financial statements. At the same time, compliance of the company with the regulations of

Corporations Act 2001 can be seen from the annual report. Apart from all these, Sonic

Healthcare also adheres to the standards of International Financial Reporting Standards (IFRS)

and IASB in the process of their financial reporting (sonichealthcare.com, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING THEORY AND ISSUES

In this context, it needs to be mentioned that the AASB conceptual framework has some

specific contribution towards promoting as well as maintaining the introduced principles,

standards and regulations of financial reporting (Pannicke, Berlinger & Dopf, 2013). At the same

time, this conceptual framework also has a specific role to play towards the Generally Accepted

Accounting Principles (GAAP) in order to review the standards and principles of financial

reporting. Thus, the underlying objective of AASB conceptual framework is to provide the

investors and users of the financial statements with the required financial information for the

process of investment decision-making. It is also considered as a useful tool for the auditors to

review the financial statements of the companies (Henderson et al., 2015).

General Purpose Financial Reporting (GPFR)

The main aim of GPFR is to provide assistance to the investors and other users of the

financial statements in the process of investment decision-making by delivering the needed

financial information about the business organizations. There are four components of GPFR in

the companies; they are income statement or profit or loss statement; balance sheet or the

statement of financial position; statement of change in equity and the statement of cash flows

(Lawrence, 2013). It is the responsibility on the business entities to prepare and present all the

components of GPFR so that the investors and users can gain required information. It needs to be

mentioned that the different components of GPFR consider the interest of both the existing as

well as potential shareholders of the business entities. As per the conceptual framework,

financial information of GPFR must have both the fundamental and enhancing qualitative

characteristics in order to make them more purposeful and acceptable to the users. The

fundamental qualitative characteristics are Relevance and Faithful Representation. The

enhancing qualitative characteristics are Comparability, Verifiability, Timeliness and

In this context, it needs to be mentioned that the AASB conceptual framework has some

specific contribution towards promoting as well as maintaining the introduced principles,

standards and regulations of financial reporting (Pannicke, Berlinger & Dopf, 2013). At the same

time, this conceptual framework also has a specific role to play towards the Generally Accepted

Accounting Principles (GAAP) in order to review the standards and principles of financial

reporting. Thus, the underlying objective of AASB conceptual framework is to provide the

investors and users of the financial statements with the required financial information for the

process of investment decision-making. It is also considered as a useful tool for the auditors to

review the financial statements of the companies (Henderson et al., 2015).

General Purpose Financial Reporting (GPFR)

The main aim of GPFR is to provide assistance to the investors and other users of the

financial statements in the process of investment decision-making by delivering the needed

financial information about the business organizations. There are four components of GPFR in

the companies; they are income statement or profit or loss statement; balance sheet or the

statement of financial position; statement of change in equity and the statement of cash flows

(Lawrence, 2013). It is the responsibility on the business entities to prepare and present all the

components of GPFR so that the investors and users can gain required information. It needs to be

mentioned that the different components of GPFR consider the interest of both the existing as

well as potential shareholders of the business entities. As per the conceptual framework,

financial information of GPFR must have both the fundamental and enhancing qualitative

characteristics in order to make them more purposeful and acceptable to the users. The

fundamental qualitative characteristics are Relevance and Faithful Representation. The

enhancing qualitative characteristics are Comparability, Verifiability, Timeliness and

8ACCOUNTING THEORY AND ISSUES

Understandability. The analysis of the financial statements of Sonic Healthcare shows the

presence of all of these characteristics in the financial information of different financial

statements (Hail, 2013).

Remuneration Report

The analysis of the 2017 Annual Report of Sonic Healthcare states that the remuneration

committee of the company adheres to the guidelines of Corporations Act 2001 to calculate

different components of the executive remuneration. As per the remuneration policy of Sonic

Healthcare, the executive remuneration must reflect the roles and responsibilities of the

executive directors. There are three parts in the remuneration structure of Sonic Healthcare for

their executive directors. They are Fixed Remuneration, Short-Term Incentives (STI) and Long-

Term Incentives (LTI). Fixed remuneration is provided as per the base level of remuneration, but

the payment of STI and LTI is based on the performance of the executive directors

(sonichealthcare.com, 2018). The following extract shows the company’s performance as an

outcome of executive remuneration in 2017:

Understandability. The analysis of the financial statements of Sonic Healthcare shows the

presence of all of these characteristics in the financial information of different financial

statements (Hail, 2013).

Remuneration Report

The analysis of the 2017 Annual Report of Sonic Healthcare states that the remuneration

committee of the company adheres to the guidelines of Corporations Act 2001 to calculate

different components of the executive remuneration. As per the remuneration policy of Sonic

Healthcare, the executive remuneration must reflect the roles and responsibilities of the

executive directors. There are three parts in the remuneration structure of Sonic Healthcare for

their executive directors. They are Fixed Remuneration, Short-Term Incentives (STI) and Long-

Term Incentives (LTI). Fixed remuneration is provided as per the base level of remuneration, but

the payment of STI and LTI is based on the performance of the executive directors

(sonichealthcare.com, 2018). The following extract shows the company’s performance as an

outcome of executive remuneration in 2017:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ACCOUNTING THEORY AND ISSUES

(Source: sonichealthcare.com, 2018)

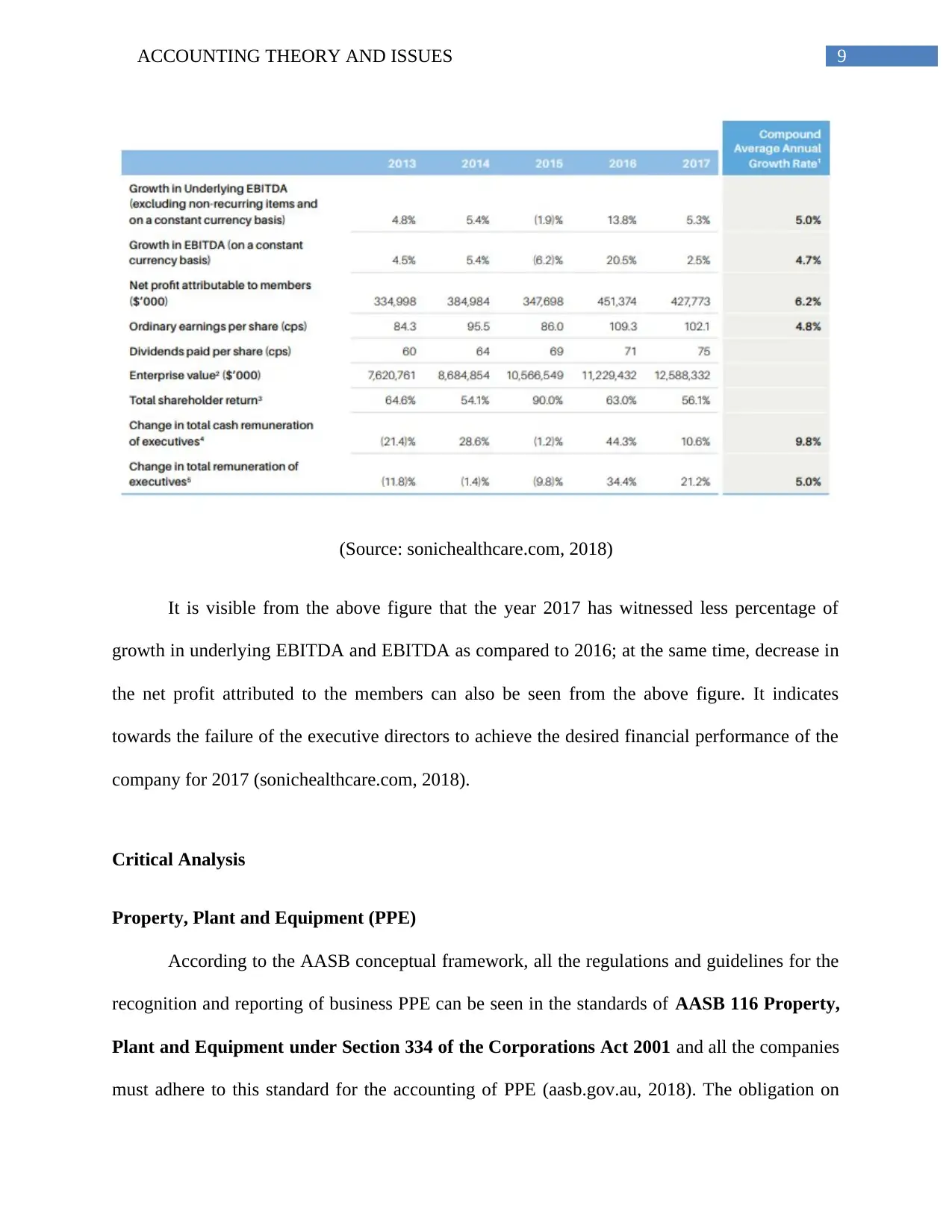

It is visible from the above figure that the year 2017 has witnessed less percentage of

growth in underlying EBITDA and EBITDA as compared to 2016; at the same time, decrease in

the net profit attributed to the members can also be seen from the above figure. It indicates

towards the failure of the executive directors to achieve the desired financial performance of the

company for 2017 (sonichealthcare.com, 2018).

Critical Analysis

Property, Plant and Equipment (PPE)

According to the AASB conceptual framework, all the regulations and guidelines for the

recognition and reporting of business PPE can be seen in the standards of AASB 116 Property,

Plant and Equipment under Section 334 of the Corporations Act 2001 and all the companies

must adhere to this standard for the accounting of PPE (aasb.gov.au, 2018). The obligation on

(Source: sonichealthcare.com, 2018)

It is visible from the above figure that the year 2017 has witnessed less percentage of

growth in underlying EBITDA and EBITDA as compared to 2016; at the same time, decrease in

the net profit attributed to the members can also be seen from the above figure. It indicates

towards the failure of the executive directors to achieve the desired financial performance of the

company for 2017 (sonichealthcare.com, 2018).

Critical Analysis

Property, Plant and Equipment (PPE)

According to the AASB conceptual framework, all the regulations and guidelines for the

recognition and reporting of business PPE can be seen in the standards of AASB 116 Property,

Plant and Equipment under Section 334 of the Corporations Act 2001 and all the companies

must adhere to this standard for the accounting of PPE (aasb.gov.au, 2018). The obligation on

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ACCOUNTING THEORY AND ISSUES

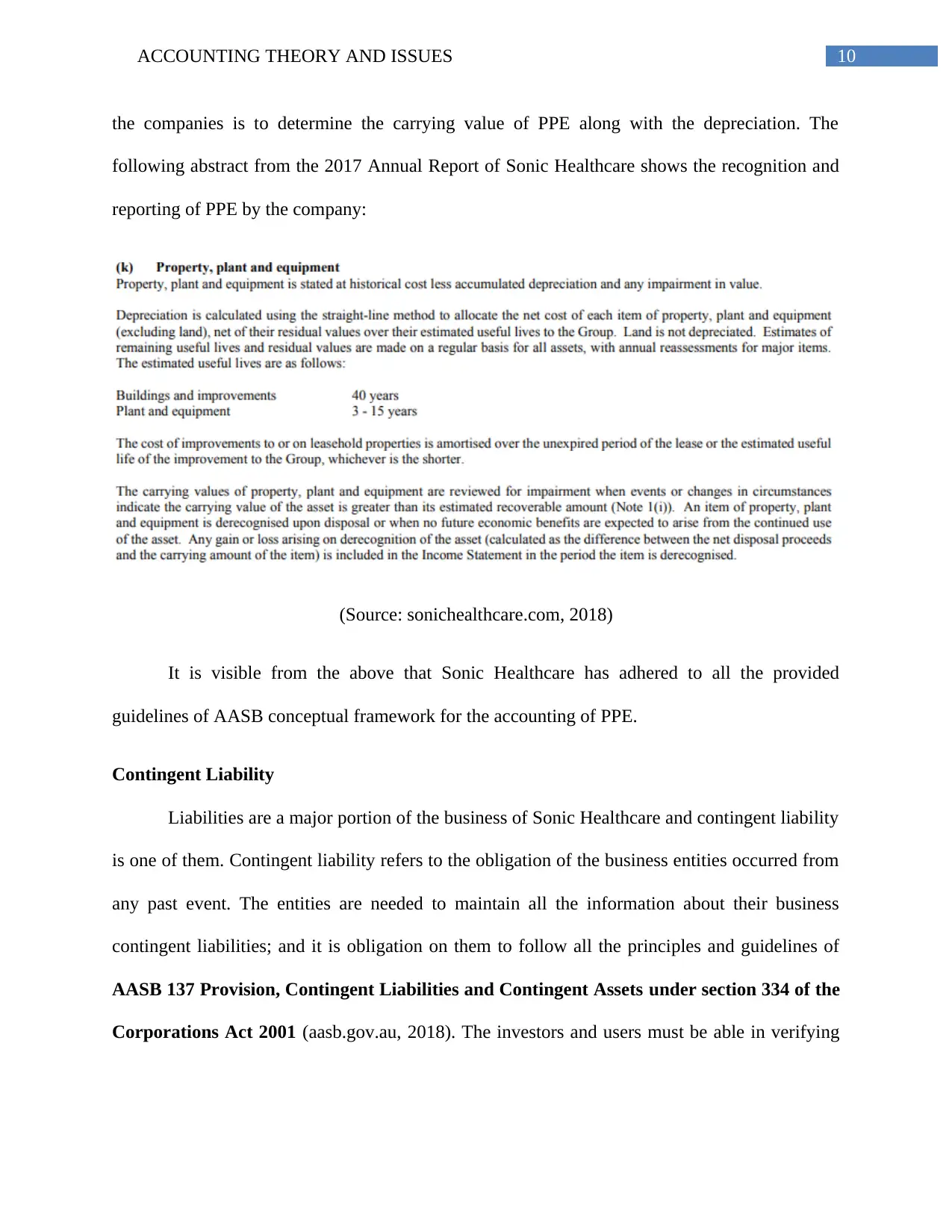

the companies is to determine the carrying value of PPE along with the depreciation. The

following abstract from the 2017 Annual Report of Sonic Healthcare shows the recognition and

reporting of PPE by the company:

(Source: sonichealthcare.com, 2018)

It is visible from the above that Sonic Healthcare has adhered to all the provided

guidelines of AASB conceptual framework for the accounting of PPE.

Contingent Liability

Liabilities are a major portion of the business of Sonic Healthcare and contingent liability

is one of them. Contingent liability refers to the obligation of the business entities occurred from

any past event. The entities are needed to maintain all the information about their business

contingent liabilities; and it is obligation on them to follow all the principles and guidelines of

AASB 137 Provision, Contingent Liabilities and Contingent Assets under section 334 of the

Corporations Act 2001 (aasb.gov.au, 2018). The investors and users must be able in verifying

the companies is to determine the carrying value of PPE along with the depreciation. The

following abstract from the 2017 Annual Report of Sonic Healthcare shows the recognition and

reporting of PPE by the company:

(Source: sonichealthcare.com, 2018)

It is visible from the above that Sonic Healthcare has adhered to all the provided

guidelines of AASB conceptual framework for the accounting of PPE.

Contingent Liability

Liabilities are a major portion of the business of Sonic Healthcare and contingent liability

is one of them. Contingent liability refers to the obligation of the business entities occurred from

any past event. The entities are needed to maintain all the information about their business

contingent liabilities; and it is obligation on them to follow all the principles and guidelines of

AASB 137 Provision, Contingent Liabilities and Contingent Assets under section 334 of the

Corporations Act 2001 (aasb.gov.au, 2018). The investors and users must be able in verifying

11ACCOUNTING THEORY AND ISSUES

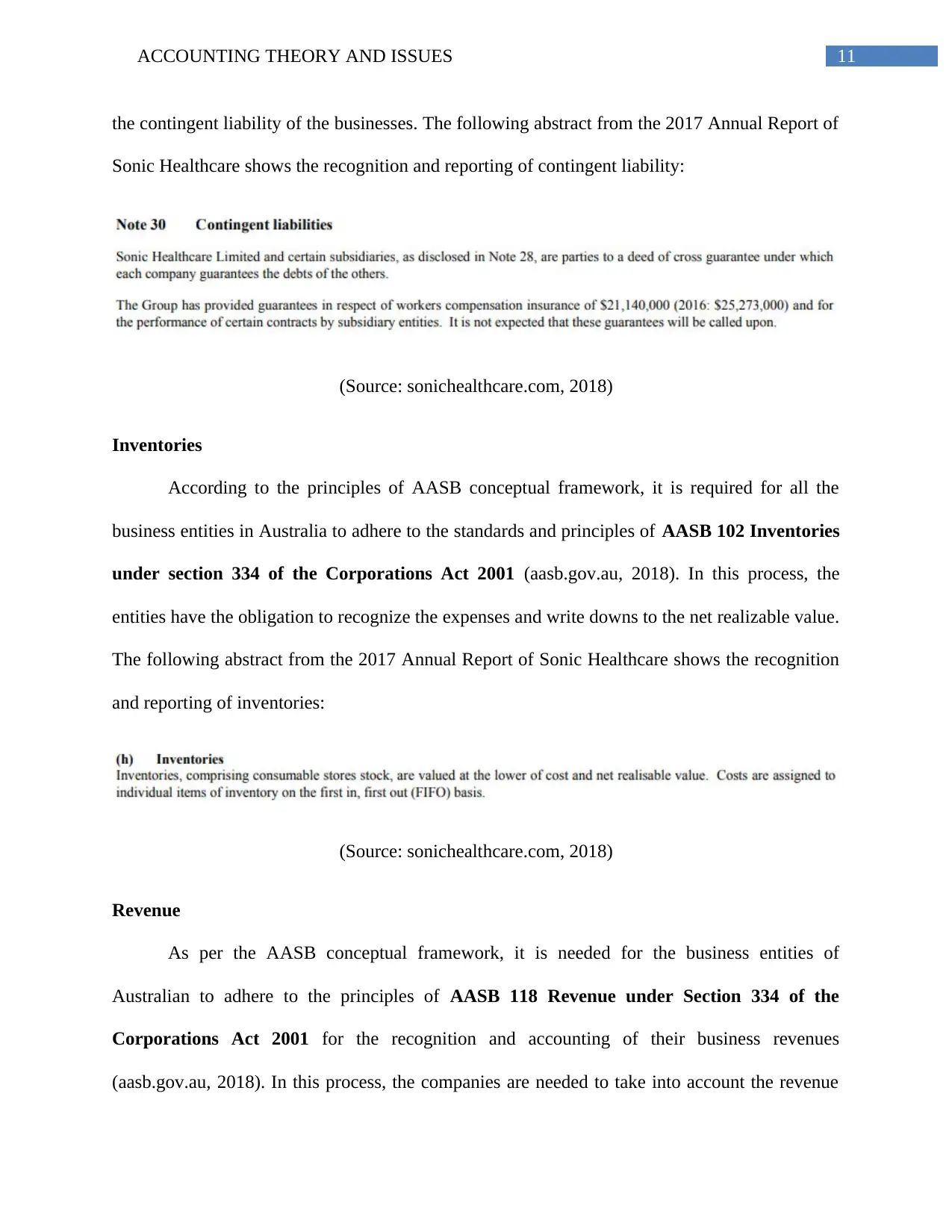

the contingent liability of the businesses. The following abstract from the 2017 Annual Report of

Sonic Healthcare shows the recognition and reporting of contingent liability:

(Source: sonichealthcare.com, 2018)

Inventories

According to the principles of AASB conceptual framework, it is required for all the

business entities in Australia to adhere to the standards and principles of AASB 102 Inventories

under section 334 of the Corporations Act 2001 (aasb.gov.au, 2018). In this process, the

entities have the obligation to recognize the expenses and write downs to the net realizable value.

The following abstract from the 2017 Annual Report of Sonic Healthcare shows the recognition

and reporting of inventories:

(Source: sonichealthcare.com, 2018)

Revenue

As per the AASB conceptual framework, it is needed for the business entities of

Australian to adhere to the principles of AASB 118 Revenue under Section 334 of the

Corporations Act 2001 for the recognition and accounting of their business revenues

(aasb.gov.au, 2018). In this process, the companies are needed to take into account the revenue

the contingent liability of the businesses. The following abstract from the 2017 Annual Report of

Sonic Healthcare shows the recognition and reporting of contingent liability:

(Source: sonichealthcare.com, 2018)

Inventories

According to the principles of AASB conceptual framework, it is required for all the

business entities in Australia to adhere to the standards and principles of AASB 102 Inventories

under section 334 of the Corporations Act 2001 (aasb.gov.au, 2018). In this process, the

entities have the obligation to recognize the expenses and write downs to the net realizable value.

The following abstract from the 2017 Annual Report of Sonic Healthcare shows the recognition

and reporting of inventories:

(Source: sonichealthcare.com, 2018)

Revenue

As per the AASB conceptual framework, it is needed for the business entities of

Australian to adhere to the principles of AASB 118 Revenue under Section 334 of the

Corporations Act 2001 for the recognition and accounting of their business revenues

(aasb.gov.au, 2018). In this process, the companies are needed to take into account the revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.