Detailed Analysis of Sources of Funds for ANZ and Commonwealth Bank

VerifiedAdded on 2022/10/17

|21

|3548

|244

Report

AI Summary

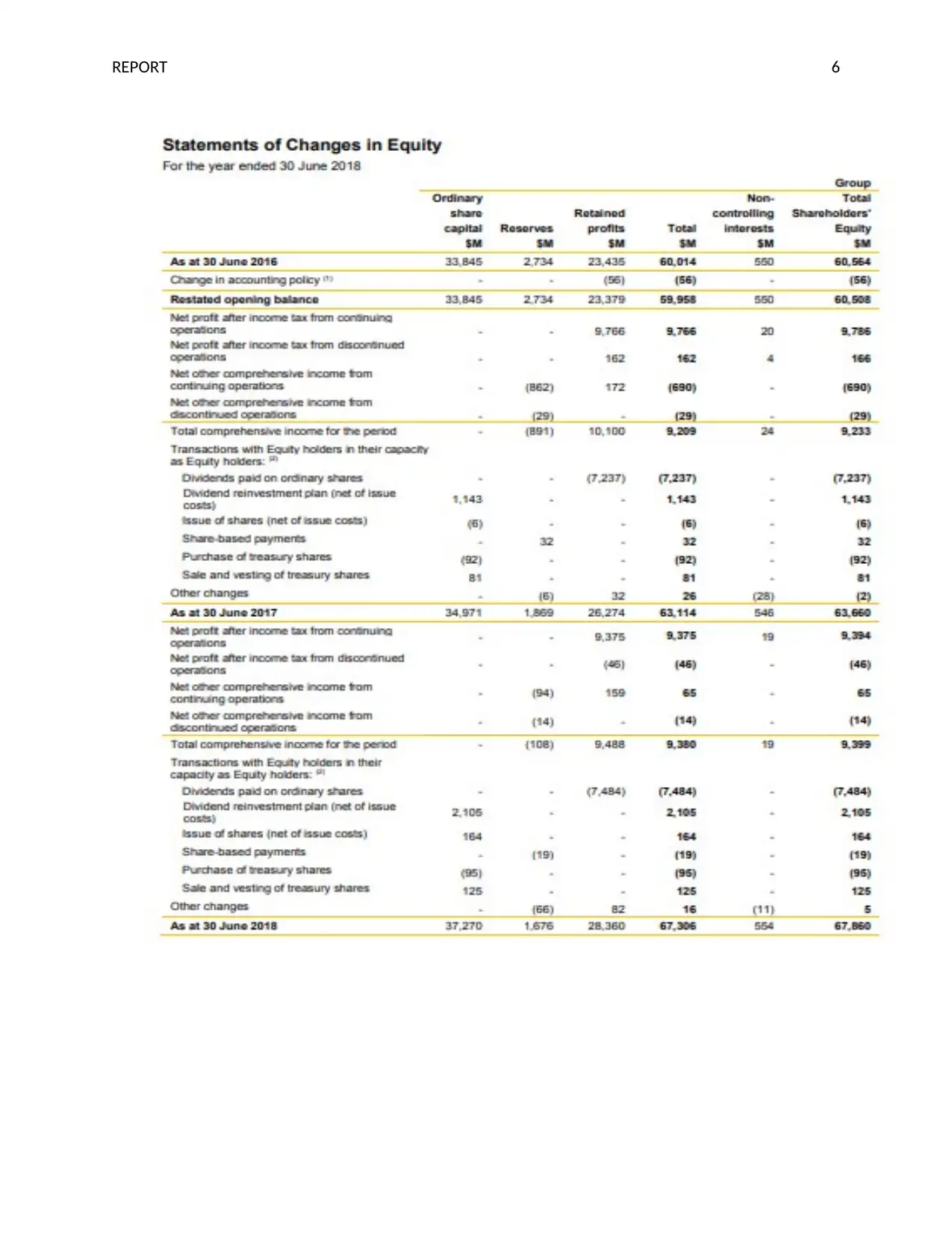

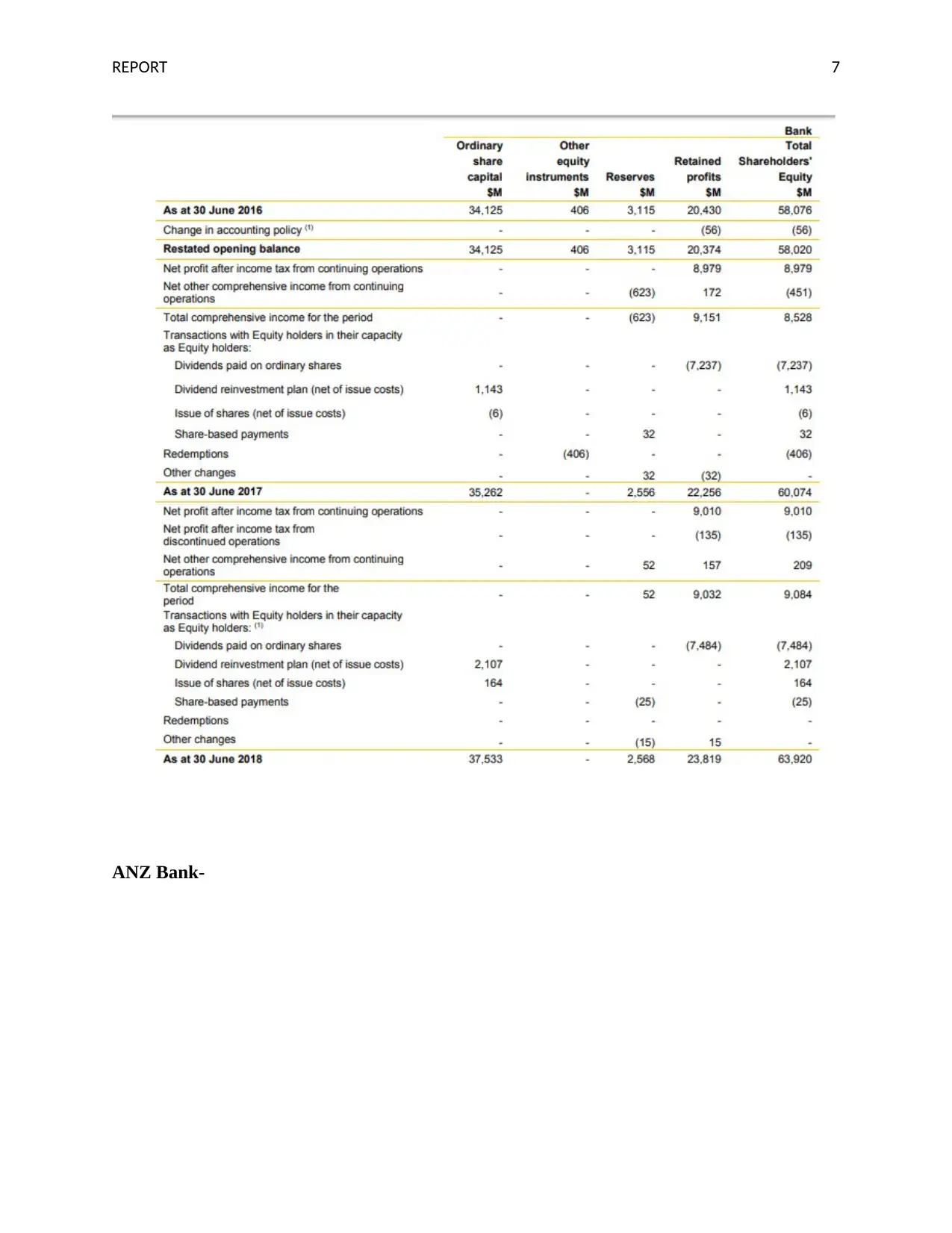

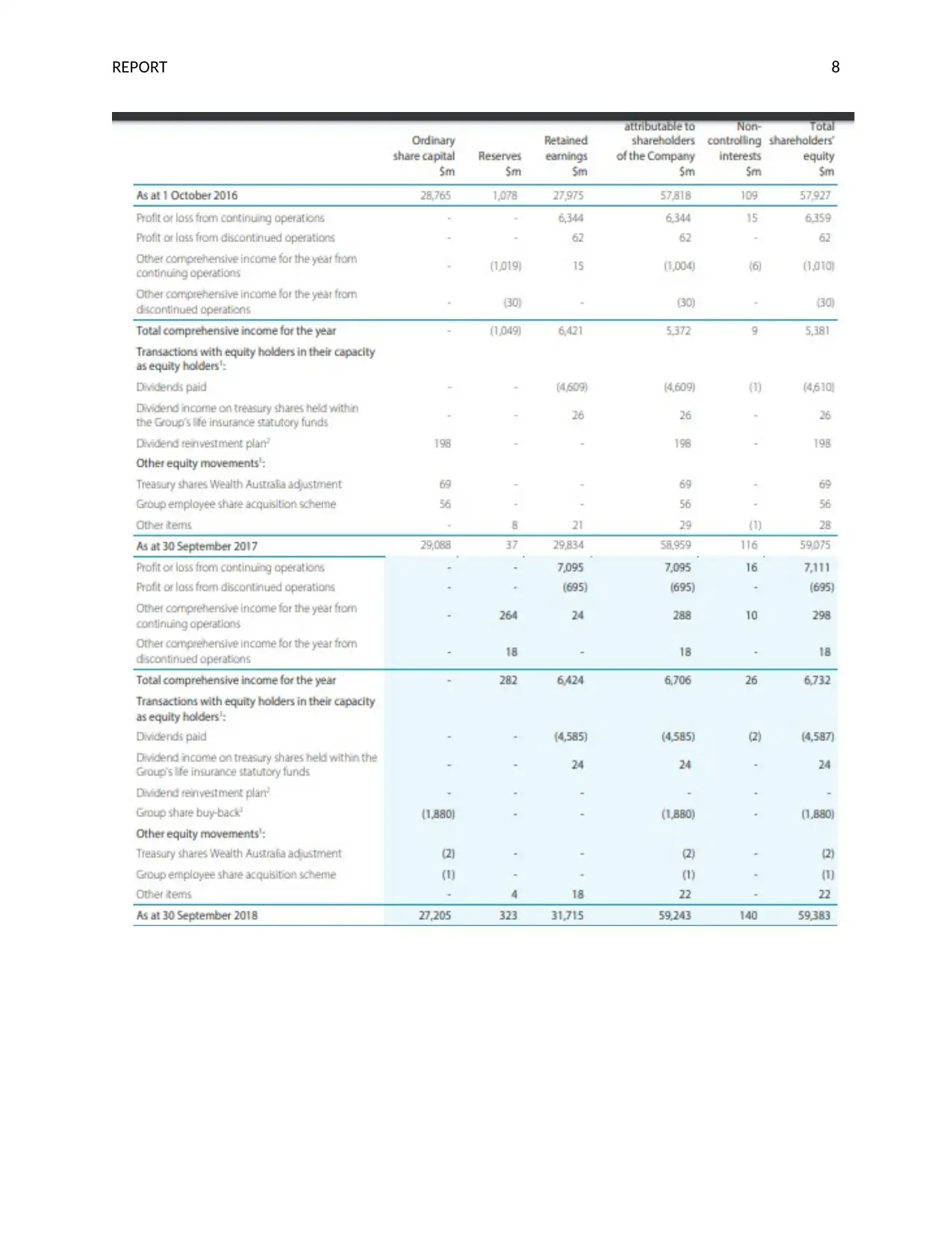

This report provides a comprehensive analysis of the sources of funds utilized by ANZ Bank and Commonwealth Bank. It begins with an abstract outlining the importance of external funding for corporate expansion, research, and competitive advantage. The report then delves into the specifics of owner's equity, including items like ordinary share capital, reserves, and retained earnings, and tracks movements in these items over a three-year period for both banks. The analysis extends to liabilities, categorizing them as short-term or long-term and examining their components, such as deposits, borrowings, and various provisions. The report further discusses the advantages and disadvantages of different funding sources, differentiating between internal, ownership, and non-ownership capital. Finally, the report clarifies the concepts of small and large proprietary companies and the implications of these classifications on compliance and reporting requirements. The report concludes by summarizing the key findings and providing references for further study.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.