Corporate Finance: Sources of Finance and Reporting Entities

VerifiedAdded on 2022/10/04

|14

|2602

|18

Report

AI Summary

This report provides an analysis of corporate and financial accounting, focusing on the sources of finance used by companies, specifically Rio Tinto and BHP Billiton. The report examines the concepts of owners' equity, including shares, retained earnings, and unrealized gains/losses, and analyzes their movements over a three-year period. It also investigates total liabilities, including long-term debt, deferred income tax, and other liabilities, along with their movements. The report further explores the advantages and disadvantages of different sources of finance. Additionally, it delves into the reporting requirements for small and large proprietary companies, providing a comprehensive overview of corporate finance principles and practices.

RUNNING HEAD: CORPORATE AND FINANCIAL ACCOUNTING

0

Sources of Finance

[Type the document subtitle]

System 0032

[Pick the date]

0

Sources of Finance

[Type the document subtitle]

System 0032

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting

1

Abstract

The aim of this report is to understand different sources of finance that are used by the

companies. For that two companies are selected that are listed on ASX that are Rio Tinto and

BHP Billiton ltd. To understand these owners’ equity items are explained and total liabilities

items are explained. Further movement in last three years in these sections is elaborated with the

reason. Further part gives insight about the small and large proprietary company and the

reporting requirements of these companies.

1

Abstract

The aim of this report is to understand different sources of finance that are used by the

companies. For that two companies are selected that are listed on ASX that are Rio Tinto and

BHP Billiton ltd. To understand these owners’ equity items are explained and total liabilities

items are explained. Further movement in last three years in these sections is elaborated with the

reason. Further part gives insight about the small and large proprietary company and the

reporting requirements of these companies.

Corporate and Financial Accounting

2

Table of Contents

Abstract.......................................................................................................................................................1

Introduction.................................................................................................................................................3

Part A..........................................................................................................................................................3

i. Owners’ Equity................................................................................................................................3

ii. Movement........................................................................................................................................5

iii. Total Liabilities............................................................................................................................6

iv. Movements......................................................................................................................................8

v. Advantages and Disadvantages............................................................................................................9

Part B.........................................................................................................................................................10

Reporting Entities..................................................................................................................................10

Conclusion.................................................................................................................................................12

2

Table of Contents

Abstract.......................................................................................................................................................1

Introduction.................................................................................................................................................3

Part A..........................................................................................................................................................3

i. Owners’ Equity................................................................................................................................3

ii. Movement........................................................................................................................................5

iii. Total Liabilities............................................................................................................................6

iv. Movements......................................................................................................................................8

v. Advantages and Disadvantages............................................................................................................9

Part B.........................................................................................................................................................10

Reporting Entities..................................................................................................................................10

Conclusion.................................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting

3

Introduction

Sources of funds are the part of corporate financing as the companies use different ways to raise

the capital to run their business or to operate at the large scale. The two main areas that are

related to corporate financing are working capital and capital budgeting. The concept of capital

budgeting is related to sources of fund that companies used in order to finance investment. These

sources are either through owners fund or through borrowed fund. The main sources of finance

for the companies are debt, equity, retained earnings, working capital loans, venture funding and

term loans etc (Datta and Fuad, 2017). This report consists of understanding the sources of funds

that Rio Tinto and BHP Billiton use. These help to practically understand the concept of sources

of funds and the movement in the company’s liabilities and equity from last three years. Further,

the concept of small and large proprietary and their reporting entities is analyzed.

Part A

i. Owners’ Equity

In the balance sheet of the company, owners’ equity is the section that represents the capital

invested by the owners in the business during the year and the owners fund at the end of the year

excluding drawings. It is the amount that company raise through issuing shares to the public; the

owners are called shareholders of the company. The owner’s sources of finance are classified in

the sub heads as retained earnings, unrealized gains and common stocks or shares.

Rio Tinto Balance sheet (Owners’ Equity)

Total equity 2016 2017 2018

Redeemable

Preferred Stock

- - -

Non-

Redeemable

- - -

Common stock 3.35B 3.22B 2.9B

Retained

Earnings

17.51B 17.56B 21.22B

3

Introduction

Sources of funds are the part of corporate financing as the companies use different ways to raise

the capital to run their business or to operate at the large scale. The two main areas that are

related to corporate financing are working capital and capital budgeting. The concept of capital

budgeting is related to sources of fund that companies used in order to finance investment. These

sources are either through owners fund or through borrowed fund. The main sources of finance

for the companies are debt, equity, retained earnings, working capital loans, venture funding and

term loans etc (Datta and Fuad, 2017). This report consists of understanding the sources of funds

that Rio Tinto and BHP Billiton use. These help to practically understand the concept of sources

of funds and the movement in the company’s liabilities and equity from last three years. Further,

the concept of small and large proprietary and their reporting entities is analyzed.

Part A

i. Owners’ Equity

In the balance sheet of the company, owners’ equity is the section that represents the capital

invested by the owners in the business during the year and the owners fund at the end of the year

excluding drawings. It is the amount that company raise through issuing shares to the public; the

owners are called shareholders of the company. The owner’s sources of finance are classified in

the sub heads as retained earnings, unrealized gains and common stocks or shares.

Rio Tinto Balance sheet (Owners’ Equity)

Total equity 2016 2017 2018

Redeemable

Preferred Stock

- - -

Non-

Redeemable

- - -

Common stock 3.35B 3.22B 2.9B

Retained

Earnings

17.51B 17.56B 21.22B

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting

4

Treasury Stock - - -

Cumulative

Transaction

-2.09B 354.83M -2.52B

Unrealized

gain/loss

-101.97M 14.78M -

Total Equity 31.8B 33.05B 34.5B

(Marketwatch, 2018)

BHP Billiton Ltd. Balance sheet (Owners’ equity)

Total equity 2016 2017 2018

Redeemable

Preferred Stock

- - -

Non-

Redeemable

- - -

Common stock 3.01B 2.92B 3.04B

Retained

Earnings

66.54B 66.6B 69.11B

Treasury Stock -44.32M -3.91M -6.77M

Cumulative

Transaction

55.06M 52.15M 56.85M

Unrealized

gain/loss

14.77M 13.04M 21.66M

Total Equity 72.91B 74.65B 75.24B

(Marketwatch, 2018)

Description of items that are listed in the balance sheet and in section owners’ equity:

Shares: Shares are the part of capital that companies issue in order to raise funds from the public.

These are issued at the face value by the public listed companies. Public purchased share of the

company and become shareholders. These shares are considered as the owners funds because the

company can pay them after releasing and clearing all its debts. Most of the shares or stocks are

divided into preference share and non-preference shares. Further that is divided into redeemable

4

Treasury Stock - - -

Cumulative

Transaction

-2.09B 354.83M -2.52B

Unrealized

gain/loss

-101.97M 14.78M -

Total Equity 31.8B 33.05B 34.5B

(Marketwatch, 2018)

BHP Billiton Ltd. Balance sheet (Owners’ equity)

Total equity 2016 2017 2018

Redeemable

Preferred Stock

- - -

Non-

Redeemable

- - -

Common stock 3.01B 2.92B 3.04B

Retained

Earnings

66.54B 66.6B 69.11B

Treasury Stock -44.32M -3.91M -6.77M

Cumulative

Transaction

55.06M 52.15M 56.85M

Unrealized

gain/loss

14.77M 13.04M 21.66M

Total Equity 72.91B 74.65B 75.24B

(Marketwatch, 2018)

Description of items that are listed in the balance sheet and in section owners’ equity:

Shares: Shares are the part of capital that companies issue in order to raise funds from the public.

These are issued at the face value by the public listed companies. Public purchased share of the

company and become shareholders. These shares are considered as the owners funds because the

company can pay them after releasing and clearing all its debts. Most of the shares or stocks are

divided into preference share and non-preference shares. Further that is divided into redeemable

Corporate and Financial Accounting

5

and non-redeemable amount. The preference share get first prefer to be paid at the time of

winding up and others shareholders get preference after them. Raising capital through shares is

the less risky way to raise the finance for the company expansion and operations.

Retained earnings: Retained earnings are the part of profit that firms keep aside in order to meet

their uncertainties. Higher the retained earnings of the company better the position of the

company in the market. Most of the companies keep certain part of their profits aside. The main

benefits of retained earnings to the company are that if company has profits than retained

earnings are more. Increasing retained earnings indicate the growth of the company.

Unrealized gains/losses: The losses or gains that are realized by the company on its assets all that

are stated in the unrealized gains and losses and reduced the amount of shareholders in the

company. This helps the companies to gain from the tax perspective.

Treasury stocks: When the company purchase its own shares in order to make the value of shares

stable in the market it is stated in the balance sheet as treasury stock. Company uses this strategy

in order to come up from the position of undervalued shares (Schreder et,al, 2019).

ii. Movement

Movements in the owners’ equity section of Rio Tinto:

It can be analyzed from the balance sheet of the company that the amount in the equity section

has raised from 31.8B to 34.3B in there years. That is the good indicator as Rio Tinto raised

capital through owners’ equity in these three years. However it doesn’t indicate that the company

not raised fund through debt but the increases in owner’s funds is the indicator that company

raised funds by issuing shares in the public. Total equity at the end of year 2016 was 31.8billion

and at the end of 2017 it was recorded at 33.05billion. This showed that the company raised

capital of 1.25 billion in a year. At the end of 2018, the company showed increase of 1.45billion.

This state that the company raised approximately 2 billion in three year and out of that shares or

common stock value decrease that indicate that company total equity increases because of its

retained earnings. Shares value declined from 3.22 billion to 2.9billion in 2017 and 2018.

Whereas company retained earnings was increased by 3.26 billion. Overall the company total

equity increased because of retained earnings not because of the shares issued by the company

5

and non-redeemable amount. The preference share get first prefer to be paid at the time of

winding up and others shareholders get preference after them. Raising capital through shares is

the less risky way to raise the finance for the company expansion and operations.

Retained earnings: Retained earnings are the part of profit that firms keep aside in order to meet

their uncertainties. Higher the retained earnings of the company better the position of the

company in the market. Most of the companies keep certain part of their profits aside. The main

benefits of retained earnings to the company are that if company has profits than retained

earnings are more. Increasing retained earnings indicate the growth of the company.

Unrealized gains/losses: The losses or gains that are realized by the company on its assets all that

are stated in the unrealized gains and losses and reduced the amount of shareholders in the

company. This helps the companies to gain from the tax perspective.

Treasury stocks: When the company purchase its own shares in order to make the value of shares

stable in the market it is stated in the balance sheet as treasury stock. Company uses this strategy

in order to come up from the position of undervalued shares (Schreder et,al, 2019).

ii. Movement

Movements in the owners’ equity section of Rio Tinto:

It can be analyzed from the balance sheet of the company that the amount in the equity section

has raised from 31.8B to 34.3B in there years. That is the good indicator as Rio Tinto raised

capital through owners’ equity in these three years. However it doesn’t indicate that the company

not raised fund through debt but the increases in owner’s funds is the indicator that company

raised funds by issuing shares in the public. Total equity at the end of year 2016 was 31.8billion

and at the end of 2017 it was recorded at 33.05billion. This showed that the company raised

capital of 1.25 billion in a year. At the end of 2018, the company showed increase of 1.45billion.

This state that the company raised approximately 2 billion in three year and out of that shares or

common stock value decrease that indicate that company total equity increases because of its

retained earnings. Shares value declined from 3.22 billion to 2.9billion in 2017 and 2018.

Whereas company retained earnings was increased by 3.26 billion. Overall the company total

equity increased because of retained earnings not because of the shares issued by the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting

6

rather the amount equity had declined that indicate that Rio Tinto didn’t issue shares in these

three years.

Movements in the owners’ equity section of BHP Billiton ltd:

The balance sheet of the company is analyzed in order to know the movement during three years.

The common stock of BHP Billiton increased from 2017 to 2018 by 12 million and decreases in

2017 from 2016. This indicates that last year company issues share worth $12 million in order to

expand its operation. The retained earning of the company in these three years was also increased

by $2.51billion. The reason behind this was the increasing profits of the company as retained

earnings is the part of profit and company keep aside the profit last year in order to meet

uncertain events. Further the unrealized gains of the companies also increased by 8.62 million.

This increases the amount of total equity but this is the amount that companies only show in the

balance sheet and are visuals that cannot be converted into cash. This indicates that in order to

strengthen the balance sheet the company did this and increased the value of unrealized gain. The

amount of total equity was increased by 59 million in these three years.

iii. Total Liabilities

The amount of total liabilities indicates the financial obligations of the company to the outsiders

for a specific time period. In the total liability section of balance sheet the long term and short

term liabilities are given. Long term liabilities include debts and long term loans, company issue

debentures in order to raise funds outside the company premises. This can be better explained

and understood with the help of two company’s balance sheet section.

6

rather the amount equity had declined that indicate that Rio Tinto didn’t issue shares in these

three years.

Movements in the owners’ equity section of BHP Billiton ltd:

The balance sheet of the company is analyzed in order to know the movement during three years.

The common stock of BHP Billiton increased from 2017 to 2018 by 12 million and decreases in

2017 from 2016. This indicates that last year company issues share worth $12 million in order to

expand its operation. The retained earning of the company in these three years was also increased

by $2.51billion. The reason behind this was the increasing profits of the company as retained

earnings is the part of profit and company keep aside the profit last year in order to meet

uncertain events. Further the unrealized gains of the companies also increased by 8.62 million.

This increases the amount of total equity but this is the amount that companies only show in the

balance sheet and are visuals that cannot be converted into cash. This indicates that in order to

strengthen the balance sheet the company did this and increased the value of unrealized gain. The

amount of total equity was increased by 59 million in these three years.

iii. Total Liabilities

The amount of total liabilities indicates the financial obligations of the company to the outsiders

for a specific time period. In the total liability section of balance sheet the long term and short

term liabilities are given. Long term liabilities include debts and long term loans, company issue

debentures in order to raise funds outside the company premises. This can be better explained

and understood with the help of two company’s balance sheet section.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting

7

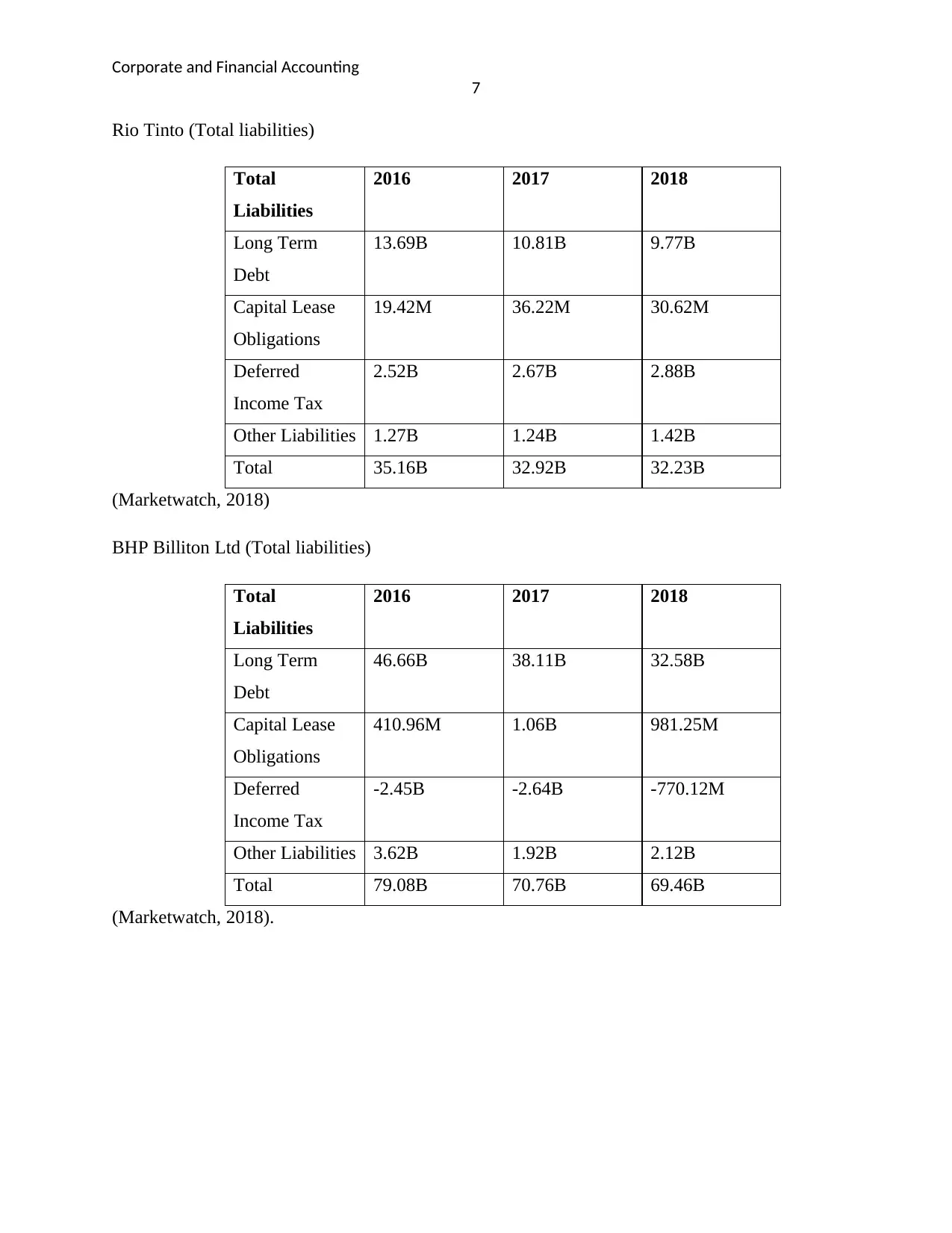

Rio Tinto (Total liabilities)

Total

Liabilities

2016 2017 2018

Long Term

Debt

13.69B 10.81B 9.77B

Capital Lease

Obligations

19.42M 36.22M 30.62M

Deferred

Income Tax

2.52B 2.67B 2.88B

Other Liabilities 1.27B 1.24B 1.42B

Total 35.16B 32.92B 32.23B

(Marketwatch, 2018)

BHP Billiton Ltd (Total liabilities)

Total

Liabilities

2016 2017 2018

Long Term

Debt

46.66B 38.11B 32.58B

Capital Lease

Obligations

410.96M 1.06B 981.25M

Deferred

Income Tax

-2.45B -2.64B -770.12M

Other Liabilities 3.62B 1.92B 2.12B

Total 79.08B 70.76B 69.46B

(Marketwatch, 2018).

7

Rio Tinto (Total liabilities)

Total

Liabilities

2016 2017 2018

Long Term

Debt

13.69B 10.81B 9.77B

Capital Lease

Obligations

19.42M 36.22M 30.62M

Deferred

Income Tax

2.52B 2.67B 2.88B

Other Liabilities 1.27B 1.24B 1.42B

Total 35.16B 32.92B 32.23B

(Marketwatch, 2018)

BHP Billiton Ltd (Total liabilities)

Total

Liabilities

2016 2017 2018

Long Term

Debt

46.66B 38.11B 32.58B

Capital Lease

Obligations

410.96M 1.06B 981.25M

Deferred

Income Tax

-2.45B -2.64B -770.12M

Other Liabilities 3.62B 1.92B 2.12B

Total 79.08B 70.76B 69.46B

(Marketwatch, 2018).

Corporate and Financial Accounting

8

Long term debts: The debts for the company is the liability, as company raise funds from the

market by issuing debentures or bonds and through this instrument organization borrow

money(Shi, 2015).

Debentures are the most common way to raise fund through this source. This amount has to be

paid to debenture holders on a specific time and the company has to pay interest on this amount.

Deferred Income tax: This is the amount that comes from the difference of tax paid by the

company and tax calculated by the tax department. If the company has to pay the tax it is liability

for the company.

Others liabilities: The amount that cannot be shown in the balance sheet with different head is

shown in this heading. This is the accumulated liability of the company including all its

miscellaneous activity.

Capital Lease Obligations: This is the amount that are due on the lease agreement of the

company to take the assets on lease. This is the sum of rent that company will pay on the lease

assets (Reid, 2018).

iv. Movements

Rio Tinto movements in the liability section:

The company total liability has decreased from three years it is a good indicator as company paid

some of its liabilities. The company paid $2.93 billion, in these three years. The long term debt

of the company in 2016 was $13.69 billion and in 2018 amount was $9.77billion. This indicates

that the company paid $3.92billion in a year. This means company paid to its debenture holder

in this year with principal amount and interest. Further, company wanted to reduce its portion of

debt from the balance sheet in order to make sure that the portion of equity and debts can be

stabilized. The ideal ratio is 2:1 and company paid its liability in order to maintain this ratio.

Through that the company can reduce its interest expenses. Other liabilities are also increased

that is the reason that the company total liabilities increases.

8

Long term debts: The debts for the company is the liability, as company raise funds from the

market by issuing debentures or bonds and through this instrument organization borrow

money(Shi, 2015).

Debentures are the most common way to raise fund through this source. This amount has to be

paid to debenture holders on a specific time and the company has to pay interest on this amount.

Deferred Income tax: This is the amount that comes from the difference of tax paid by the

company and tax calculated by the tax department. If the company has to pay the tax it is liability

for the company.

Others liabilities: The amount that cannot be shown in the balance sheet with different head is

shown in this heading. This is the accumulated liability of the company including all its

miscellaneous activity.

Capital Lease Obligations: This is the amount that are due on the lease agreement of the

company to take the assets on lease. This is the sum of rent that company will pay on the lease

assets (Reid, 2018).

iv. Movements

Rio Tinto movements in the liability section:

The company total liability has decreased from three years it is a good indicator as company paid

some of its liabilities. The company paid $2.93 billion, in these three years. The long term debt

of the company in 2016 was $13.69 billion and in 2018 amount was $9.77billion. This indicates

that the company paid $3.92billion in a year. This means company paid to its debenture holder

in this year with principal amount and interest. Further, company wanted to reduce its portion of

debt from the balance sheet in order to make sure that the portion of equity and debts can be

stabilized. The ideal ratio is 2:1 and company paid its liability in order to maintain this ratio.

Through that the company can reduce its interest expenses. Other liabilities are also increased

that is the reason that the company total liabilities increases.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate and Financial Accounting

9

BHP Billiton Ltd.

The long term debt of the company is decreased by $14.08billion from 2017 to 2018. Further, the

company total liabilities also decreases that is because the company paid to its debenture holders.

The huge amount was paid by the company in the last financial year. The reason behind this can

be that the company earned more profits and opted for other source to raise fund. The equity

portion of the company increases that showed that company raise funds from shares and paid

back to its debtors.

v. Advantages and Disadvantages

Sources of finance are borrowed fund and owners funds, mainly companies use these sources bot

have their advantages and drawbacks. The equity is considered as the less risky source as the

company is not liable to pay to them if the company is not earning profits. But to the debenture

holders the company has to pay on time with the interest. Further, equity is the expensive way of

raising funds but debt is less expensive than the owner’s fund. . In a nutshell, which source of

fund is best suitable depend on the company situation and position but an ideal proportion of

equity and debt (Kieschnick and Moussawi, 2018).

9

BHP Billiton Ltd.

The long term debt of the company is decreased by $14.08billion from 2017 to 2018. Further, the

company total liabilities also decreases that is because the company paid to its debenture holders.

The huge amount was paid by the company in the last financial year. The reason behind this can

be that the company earned more profits and opted for other source to raise fund. The equity

portion of the company increases that showed that company raise funds from shares and paid

back to its debtors.

v. Advantages and Disadvantages

Sources of finance are borrowed fund and owners funds, mainly companies use these sources bot

have their advantages and drawbacks. The equity is considered as the less risky source as the

company is not liable to pay to them if the company is not earning profits. But to the debenture

holders the company has to pay on time with the interest. Further, equity is the expensive way of

raising funds but debt is less expensive than the owner’s fund. . In a nutshell, which source of

fund is best suitable depend on the company situation and position but an ideal proportion of

equity and debt (Kieschnick and Moussawi, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate and Financial Accounting

10

Part B

Reporting Entities

The concept of proprietary company can be understood with the classification and proprietary

company reporting requirement. The proprietary company can be classified into two broad

categories; that are small proprietary company and large proprietary company (Buck, 2019).

The reporting requirements of small proprietary company are:

The revenue earned by the company during the year including all its entities should be

less than $50 million.

The assets of the company should be less than the $25 billion for the year considering all

its entities.

The employed in the company should be less than 100 at the end of the year.

The companies that comes under this category don’t have to prepare the “audited financial

statements with ASIC”. The audited report need to be presented only when the company is

controlled by the foreigner or shareholders of the company requested the report at the end of the

year.

Large proprietary company should meet the following requirements:

The revenue generated by the company at the end of year should be more than $50 billion

The assets of the company at the end of the year including all its entities should be more

than $25billion.

The company and entities it controls should have more than 100 workers working at the

end of the year.

Reporting entity: GPFR (General purposed financial report

Non Reporting entity: SPFR (Special purpose financial report

10

Part B

Reporting Entities

The concept of proprietary company can be understood with the classification and proprietary

company reporting requirement. The proprietary company can be classified into two broad

categories; that are small proprietary company and large proprietary company (Buck, 2019).

The reporting requirements of small proprietary company are:

The revenue earned by the company during the year including all its entities should be

less than $50 million.

The assets of the company should be less than the $25 billion for the year considering all

its entities.

The employed in the company should be less than 100 at the end of the year.

The companies that comes under this category don’t have to prepare the “audited financial

statements with ASIC”. The audited report need to be presented only when the company is

controlled by the foreigner or shareholders of the company requested the report at the end of the

year.

Large proprietary company should meet the following requirements:

The revenue generated by the company at the end of year should be more than $50 billion

The assets of the company at the end of the year including all its entities should be more

than $25billion.

The company and entities it controls should have more than 100 workers working at the

end of the year.

Reporting entity: GPFR (General purposed financial report

Non Reporting entity: SPFR (Special purpose financial report

Corporate and Financial Accounting

11

Conclusion

It is concluded from the above analysis that the sources of finance available for the companies

are owners fund and borrower funds. This is further divided into long term and short term funds

and this depend on the requirement of the companies. From the companies that are chosen in the

above section it is analyzed that both of them use equity or owners funds in the major proportion

and borrower funds in the less proportion.

11

Conclusion

It is concluded from the above analysis that the sources of finance available for the companies

are owners fund and borrower funds. This is further divided into long term and short term funds

and this depend on the requirement of the companies. From the companies that are chosen in the

above section it is analyzed that both of them use equity or owners funds in the major proportion

and borrower funds in the less proportion.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.