Financial Report: Evaluating Sources of Finance for Business Growth

VerifiedAdded on 2020/01/28

|14

|4040

|59

Report

AI Summary

This report comprehensively analyzes the sources of finance available to both incorporated and unincorporated entities, detailing the advantages and disadvantages of each. It examines owner's funds, loans, equity capital, preference shares, debentures, and other financial instruments. The report further explores the implications of utilizing internal and external sources of finance, considering risk, control, and cost factors. A significant portion of the report is dedicated to Clariton Antiques Ltd., including financial planning, decision-making regarding financing options (partners, venture capitalists, and finance brokers), and the creation of a cash budget to improve their financial position. Additionally, it addresses costing methods, pricing models, capital budgeting techniques, and the essential components of financial statements, along with comparisons between different business structures (sole trader, partnership, and incorporated entities). The report concludes with an interpretation of financial statements using key ratios and a comparison with the previous year's performance. The report also includes analysis of the cost of finance (dividends, interest, and tax).

SOURCES OF FINANCE

STUDENT NAME:

STUDENT ID:

PROFESSOR’S NAME:

1

STUDENT NAME:

STUDENT ID:

PROFESSOR’S NAME:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Task 1............................................................................................................................................3

1.1 Identify and evaluate the available sources of finance to the incorporated entities and the

incorporporated entities respectively.............................................................................................3

1.2 What are the implications of utilising the internal and the external sources of finance?.........4

1.3 Identify the most beneficial sources of finance........................................................................5

Task 2............................................................................................................................................6

2.1 Analyse the cost of the available sources of finance taking into consideration the cost of

Dividends, Interest and Tax...........................................................................................................6

2.2 Discuss the essential of proper financial planning with reference to the organisation Clariton

Antiques Ltd...................................................................................................................................6

2.3 By utilising the given data assess the decision making in regards to the financing of the

takeover by the Partners, the Venture Capitalists and the Finance Broker...................................7

2.4 Discuss how the financial statements will be affected if the financing is made by the Finance

Broker and the Venture Capitalists respectively............................................................................7

Task 3............................................................................................................................................8

3.1 Present a Cash Budget for the entity Clariton Antiques Ltd. based on the given data and

thereby analyse the decision making in order to improve their financial position..........................8

3.2 Please mention the appropriate method of costing for the entity Clariton Antiques Ltd. and

thereby decide the pricing model...................................................................................................8

3.3 Please select the appropriate project to be undertaken in respect to the data given for

Clariton Antiques Ltd. by using the techniques of capital budgeting.............................................9

Task 4..........................................................................................................................................10

4.1 Please explain the essential components of the financial statements..................................10

4.2 Please compare the financial statements as presented by the Clariton Antiques Ltd., a sole

trader and a partnership firm.......................................................................................................11

4.3 Please make an interpretation of the financial statements by utilising the essential ratios and

also compare them with that of the preceding year.....................................................................12

Reference List:.............................................................................................................................13

2

Task 1............................................................................................................................................3

1.1 Identify and evaluate the available sources of finance to the incorporated entities and the

incorporporated entities respectively.............................................................................................3

1.2 What are the implications of utilising the internal and the external sources of finance?.........4

1.3 Identify the most beneficial sources of finance........................................................................5

Task 2............................................................................................................................................6

2.1 Analyse the cost of the available sources of finance taking into consideration the cost of

Dividends, Interest and Tax...........................................................................................................6

2.2 Discuss the essential of proper financial planning with reference to the organisation Clariton

Antiques Ltd...................................................................................................................................6

2.3 By utilising the given data assess the decision making in regards to the financing of the

takeover by the Partners, the Venture Capitalists and the Finance Broker...................................7

2.4 Discuss how the financial statements will be affected if the financing is made by the Finance

Broker and the Venture Capitalists respectively............................................................................7

Task 3............................................................................................................................................8

3.1 Present a Cash Budget for the entity Clariton Antiques Ltd. based on the given data and

thereby analyse the decision making in order to improve their financial position..........................8

3.2 Please mention the appropriate method of costing for the entity Clariton Antiques Ltd. and

thereby decide the pricing model...................................................................................................8

3.3 Please select the appropriate project to be undertaken in respect to the data given for

Clariton Antiques Ltd. by using the techniques of capital budgeting.............................................9

Task 4..........................................................................................................................................10

4.1 Please explain the essential components of the financial statements..................................10

4.2 Please compare the financial statements as presented by the Clariton Antiques Ltd., a sole

trader and a partnership firm.......................................................................................................11

4.3 Please make an interpretation of the financial statements by utilising the essential ratios and

also compare them with that of the preceding year.....................................................................12

Reference List:.............................................................................................................................13

2

Task 1

1.1 Identify and evaluate the available sources of finance to the incorporated

entities and the incorporporated entities respectively.

There are different sources of finance that are available to different kinds of business entities.

The availability of the sources of finance can be discussed for the two category of entities. They

can be:

● Unincorporated entities.

● Incorporated entities.

Unincorporated entities: The unincorporated entities refers to those entities which are not

incorporated under any act of corporation in any of the territories. The unincorporated entities

mainly refers to the sole traders, partnership firms, co- operative societies and the self employed

persons respectively. But nowadays many of the co- operative societies are incorporated under

respective Corporate Law of any of the territories around the globe. Many of the partnership

Firms are also getting registered as Limited Liability Partnership Firms under the relevant

corporate laws (Lowenstein, 2014)

Now we are to judge the available sources of finance to the unincorporated entities. The

available sources of the finance to an unincorporated concern can be listed as follows:

1. Owner’s Fund: The unincorporated entities can easily avail the capital from the owners.

Owner’s capital is the least risky source of fund for an unincorporated entity as most of

these unincorporated entities are not recognised as a separate legal entity.

2. Loan from relative: The unincorporated concern can also easily get the required loan

from the relatives of the owners. These are also less risky source of capital.

3. Loan from the Banks and Financial Institutions: The sole traders and the partnership

firms and also the other unincorporated entities can avail Loan from Bank but this is

restricted to the amount of the fixed assets available to the entity. This is a risky capital

for the unincorporated entities since most of them are not recognised as Separate Legal

Entity. The banks also keeps the fixed assets of these business as mortgage prior to

sanctioning of Loan. This is also a costly source of capital since interest is also charged

on these source.

4. Cash Credit Loan: Cash Credit Loan is type of Loan which is offered by the Banks in

order to meet the working capital requirement of the business. Cash Credit Loan is easily

available to all the category of entities depending on the position of the working capital

and the operational efficiency of the enterprise.

3

1.1 Identify and evaluate the available sources of finance to the incorporated

entities and the incorporporated entities respectively.

There are different sources of finance that are available to different kinds of business entities.

The availability of the sources of finance can be discussed for the two category of entities. They

can be:

● Unincorporated entities.

● Incorporated entities.

Unincorporated entities: The unincorporated entities refers to those entities which are not

incorporated under any act of corporation in any of the territories. The unincorporated entities

mainly refers to the sole traders, partnership firms, co- operative societies and the self employed

persons respectively. But nowadays many of the co- operative societies are incorporated under

respective Corporate Law of any of the territories around the globe. Many of the partnership

Firms are also getting registered as Limited Liability Partnership Firms under the relevant

corporate laws (Lowenstein, 2014)

Now we are to judge the available sources of finance to the unincorporated entities. The

available sources of the finance to an unincorporated concern can be listed as follows:

1. Owner’s Fund: The unincorporated entities can easily avail the capital from the owners.

Owner’s capital is the least risky source of fund for an unincorporated entity as most of

these unincorporated entities are not recognised as a separate legal entity.

2. Loan from relative: The unincorporated concern can also easily get the required loan

from the relatives of the owners. These are also less risky source of capital.

3. Loan from the Banks and Financial Institutions: The sole traders and the partnership

firms and also the other unincorporated entities can avail Loan from Bank but this is

restricted to the amount of the fixed assets available to the entity. This is a risky capital

for the unincorporated entities since most of them are not recognised as Separate Legal

Entity. The banks also keeps the fixed assets of these business as mortgage prior to

sanctioning of Loan. This is also a costly source of capital since interest is also charged

on these source.

4. Cash Credit Loan: Cash Credit Loan is type of Loan which is offered by the Banks in

order to meet the working capital requirement of the business. Cash Credit Loan is easily

available to all the category of entities depending on the position of the working capital

and the operational efficiency of the enterprise.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incorporated Entities: The Incorporated entities refers to those entities which are registered under

the corporate law of any of the territories of the globe. Mainly the companies are the

incorporated entities but in the current days many of the co- operative societies and the

partnership firms (LLP) are getting registered under the act of corporation in many of the

territories around the globe (Henning, 2015).

The sources of finance that are available to the incorporated entities can be the following as

hereby mentioned:

1. Equity Capital: The Incorporated Entities can issue equity capital to the members as well

as in the market. Equity Capital is the least risky capital for the entity as there is no

obligation of dividend as well as no obligation of repayment except in the case of

liquidation.

2. Preference Capital: The company can easily raise funds through issuing of the preference

shares in the market since there is a fixed rate of dividend on these shares.

3. Debentures: Debentures are also an efficient sources of finance to the company if the

company is desirous of raising debt capital. The cost of debenture is also low compared

to the cost of equity and preference since there is a tax benefit on the interest on the

debentures.

4. Loan from Financial Institutions: Those companies which are unable to issue debentures

in the market can avail the facility of the loan from the financial institutions in order to

raise debt capital. But this is a very risky capital for the company since these capital

involves the floatation costs and also the assets of the company are secured against the

loan.

5. Trade Finance: The companies can also avail the facility of the trade finance though the

issuing of the Letter of Credit to the banks and thereby can avail export loan.

6. Government Aid: The Incorporated entities gets aid from the Government from time to

time with respect to subsidies, tax relief, etc.

It is to be noted that in addition to the above mentioned sources of finance the incorporated

entities also can avail all the facilities that are available to the unincorporated entities except for

Loan from Relative but the company can also avail Loan from the Director’s Relative after

proving for Explanatory Statement (Egger et al. 2014).

1.2 What are the implications of utilising the internal and the external sources

of finance?

There are ample of financial resources that are available to the entities. But it is essential for the

management of the company to decide an appropriate source of finance prior to opting them in

order to decide their impact in the financial statements of the entity as well as to ensure the

optimum utilisation of the resources.

The implications of utilising internal and the external sources of finance can be discussed in the

following contexts. They are herein mentioned:

4

the corporate law of any of the territories of the globe. Mainly the companies are the

incorporated entities but in the current days many of the co- operative societies and the

partnership firms (LLP) are getting registered under the act of corporation in many of the

territories around the globe (Henning, 2015).

The sources of finance that are available to the incorporated entities can be the following as

hereby mentioned:

1. Equity Capital: The Incorporated Entities can issue equity capital to the members as well

as in the market. Equity Capital is the least risky capital for the entity as there is no

obligation of dividend as well as no obligation of repayment except in the case of

liquidation.

2. Preference Capital: The company can easily raise funds through issuing of the preference

shares in the market since there is a fixed rate of dividend on these shares.

3. Debentures: Debentures are also an efficient sources of finance to the company if the

company is desirous of raising debt capital. The cost of debenture is also low compared

to the cost of equity and preference since there is a tax benefit on the interest on the

debentures.

4. Loan from Financial Institutions: Those companies which are unable to issue debentures

in the market can avail the facility of the loan from the financial institutions in order to

raise debt capital. But this is a very risky capital for the company since these capital

involves the floatation costs and also the assets of the company are secured against the

loan.

5. Trade Finance: The companies can also avail the facility of the trade finance though the

issuing of the Letter of Credit to the banks and thereby can avail export loan.

6. Government Aid: The Incorporated entities gets aid from the Government from time to

time with respect to subsidies, tax relief, etc.

It is to be noted that in addition to the above mentioned sources of finance the incorporated

entities also can avail all the facilities that are available to the unincorporated entities except for

Loan from Relative but the company can also avail Loan from the Director’s Relative after

proving for Explanatory Statement (Egger et al. 2014).

1.2 What are the implications of utilising the internal and the external sources

of finance?

There are ample of financial resources that are available to the entities. But it is essential for the

management of the company to decide an appropriate source of finance prior to opting them in

order to decide their impact in the financial statements of the entity as well as to ensure the

optimum utilisation of the resources.

The implications of utilising internal and the external sources of finance can be discussed in the

following contexts. They are herein mentioned:

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Risk: If we consider from the viewpoint of risk, it can be said that the internal sources of

finance are the least risky in nature since the company is not liable to pay dividends or

interest on these sources each year. The company is also not liable to repay these internal

source of capital except in the event of liquidation. Whereas the external sources of

finance are quite risky in nature since the company has a burden of repayment as well as

burden of interests and dividends (on Preference Shares) even in any of the accounting

year the company is unable to make profits.

2. Control: If we are considering from the viewpoint of control then it is better for the

companies to opt for Debt Capital and undergo external financing. At the time of

incorporating the debt capital the control structure of the company is not diluted.

Therefore the existing shareholders can enjoy their control and also the promoter’s share

of the company is protected.

3. Cost: From the viewpoint of Cost it is better for the company to incorporate debt capital

in its capital structure. By utilising of the debt capital the company can enjoy tax benefit

since the interest payable on loans are deductible from the income of the company

whereas no deduction is available for the dividends paid to the Equity and the Preference

Shareholders. Also the cost of Debt is lower than the Cost of Equity (ke), Cost of

Preference Capital (kP) and the cost of Retained Earnings (kr). Therefore it can be said

that the Debt Financing is Less costly for the organisation. The company can also able to

enjoy Trading on Equity and can operate on favourable financial leverage if the returns

are higher than the Cost of Debt.

1.3 Identify the most beneficial sources of finance.

We can see that the company has a favourable debt equity ratio which is less than 2:1, we can

say that Clariton Antiques Limited can opt for Debt Financing (Obreja, 2013).By using the Debt

Financing the company can enjoy trading on Equity as well as operate on Financial Leverage. It

also has a good Proprietary ratio so it is better for the company to select Debt Capital (Amess,

Stiebale and Wright, 2016).

5

finance are the least risky in nature since the company is not liable to pay dividends or

interest on these sources each year. The company is also not liable to repay these internal

source of capital except in the event of liquidation. Whereas the external sources of

finance are quite risky in nature since the company has a burden of repayment as well as

burden of interests and dividends (on Preference Shares) even in any of the accounting

year the company is unable to make profits.

2. Control: If we are considering from the viewpoint of control then it is better for the

companies to opt for Debt Capital and undergo external financing. At the time of

incorporating the debt capital the control structure of the company is not diluted.

Therefore the existing shareholders can enjoy their control and also the promoter’s share

of the company is protected.

3. Cost: From the viewpoint of Cost it is better for the company to incorporate debt capital

in its capital structure. By utilising of the debt capital the company can enjoy tax benefit

since the interest payable on loans are deductible from the income of the company

whereas no deduction is available for the dividends paid to the Equity and the Preference

Shareholders. Also the cost of Debt is lower than the Cost of Equity (ke), Cost of

Preference Capital (kP) and the cost of Retained Earnings (kr). Therefore it can be said

that the Debt Financing is Less costly for the organisation. The company can also able to

enjoy Trading on Equity and can operate on favourable financial leverage if the returns

are higher than the Cost of Debt.

1.3 Identify the most beneficial sources of finance.

We can see that the company has a favourable debt equity ratio which is less than 2:1, we can

say that Clariton Antiques Limited can opt for Debt Financing (Obreja, 2013).By using the Debt

Financing the company can enjoy trading on Equity as well as operate on Financial Leverage. It

also has a good Proprietary ratio so it is better for the company to select Debt Capital (Amess,

Stiebale and Wright, 2016).

5

Task 2

2.1 Analyse the cost of the available sources of finance taking into

consideration the cost of Dividends, Interest and Tax.

Please refer to the below screenshot for the above solution.

2.2 Discuss the essential of proper financial planning with reference to the

organisation Clariton Antiques Ltd.

The essential of the financial Planning can be discussed as follows:

a) Budgeting: Budgeting refers to the pre analysis of the activities of the business prior to

commencing of the financial year. Budgeting set the standard in which the business needs

to operate. Budgeting also helps to ensure the appropriate cash flows from a project prior

to its commencing (Baiocchi and Ganuza, 2014).

b) Implications of failure to Finance: The firm can at any time not be able to procure the

appropriate finance at the time of commencing of a project. At this time the company

needs to evaluate all the available sources of finance by which the expansion can be

made.

c) Overtrading: Overtrading refers to the concept of expansion of the business. It may be

merger and Acquisition, or commencing of a new project in the existing premises. The

effect of the overtrading should be analysed thoroughly prior to moving for overtrading

and expansion.

6

2.1 Analyse the cost of the available sources of finance taking into

consideration the cost of Dividends, Interest and Tax.

Please refer to the below screenshot for the above solution.

2.2 Discuss the essential of proper financial planning with reference to the

organisation Clariton Antiques Ltd.

The essential of the financial Planning can be discussed as follows:

a) Budgeting: Budgeting refers to the pre analysis of the activities of the business prior to

commencing of the financial year. Budgeting set the standard in which the business needs

to operate. Budgeting also helps to ensure the appropriate cash flows from a project prior

to its commencing (Baiocchi and Ganuza, 2014).

b) Implications of failure to Finance: The firm can at any time not be able to procure the

appropriate finance at the time of commencing of a project. At this time the company

needs to evaluate all the available sources of finance by which the expansion can be

made.

c) Overtrading: Overtrading refers to the concept of expansion of the business. It may be

merger and Acquisition, or commencing of a new project in the existing premises. The

effect of the overtrading should be analysed thoroughly prior to moving for overtrading

and expansion.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

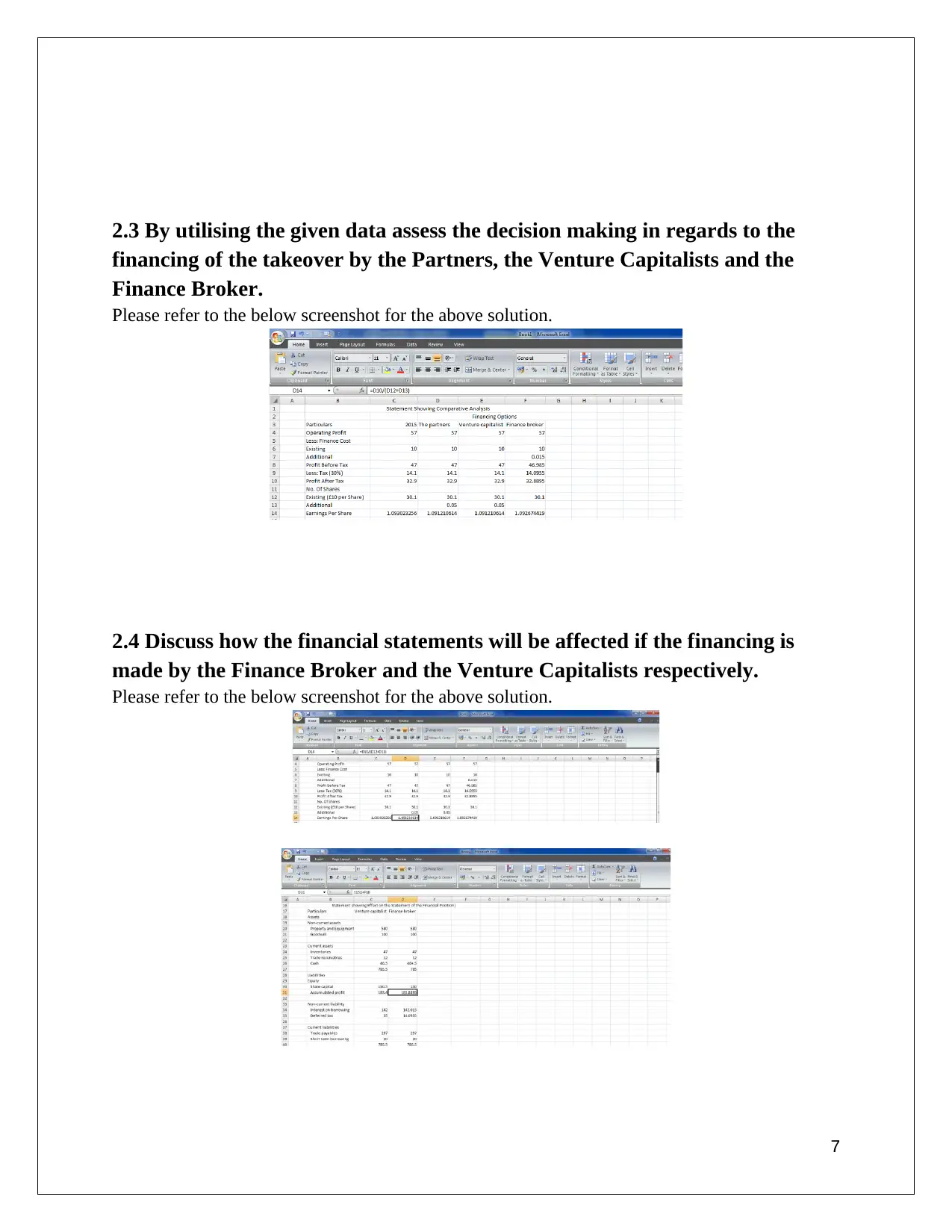

2.3 By utilising the given data assess the decision making in regards to the

financing of the takeover by the Partners, the Venture Capitalists and the

Finance Broker.

Please refer to the below screenshot for the above solution.

2.4 Discuss how the financial statements will be affected if the financing is

made by the Finance Broker and the Venture Capitalists respectively.

Please refer to the below screenshot for the above solution.

7

financing of the takeover by the Partners, the Venture Capitalists and the

Finance Broker.

Please refer to the below screenshot for the above solution.

2.4 Discuss how the financial statements will be affected if the financing is

made by the Finance Broker and the Venture Capitalists respectively.

Please refer to the below screenshot for the above solution.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Task 3

3.1 Present a Cash Budget for the entity Clariton Antiques Ltd. based on the

given data and thereby analyse the decision making in order to improve their

financial position.

Please refer to the below screenshot and the related excel File for the above solution

Here in this contexts we can say that the firm can opt for overdraft facilities from the banks in

order to facilitate the management of working capital.

3.2 Please mention the appropriate method of costing for the entity Clariton

Antiques Ltd. and thereby decide the pricing model.

Any organisation with no production activities can be mainly be either a service organisation or a

trading organisation.

If Clariton Antiques Limited is a Service Entity then it will be required to follow the technique of

operating costing in order to decide the price of its services. The operating Costing model is

model of cost sheet for the service entities, where all the related costs in providing of the services

like administration charges, charges for Depreciation, Electricity, transport expenses and all

other expenses specific to the service are included to decide the entire cost of the service.

Thereafter the percentage of profit is added to determine the total revenue and then the total

revenue is then divided by the No. of Clients or Passenger Km. in case of the transport

companies.

If Clariton Antiques Limited is a trading concern then it can follow the normal Cost Sheet but the

following items will be excluded as compared to the manufacturing entities:

8

3.1 Present a Cash Budget for the entity Clariton Antiques Ltd. based on the

given data and thereby analyse the decision making in order to improve their

financial position.

Please refer to the below screenshot and the related excel File for the above solution

Here in this contexts we can say that the firm can opt for overdraft facilities from the banks in

order to facilitate the management of working capital.

3.2 Please mention the appropriate method of costing for the entity Clariton

Antiques Ltd. and thereby decide the pricing model.

Any organisation with no production activities can be mainly be either a service organisation or a

trading organisation.

If Clariton Antiques Limited is a Service Entity then it will be required to follow the technique of

operating costing in order to decide the price of its services. The operating Costing model is

model of cost sheet for the service entities, where all the related costs in providing of the services

like administration charges, charges for Depreciation, Electricity, transport expenses and all

other expenses specific to the service are included to decide the entire cost of the service.

Thereafter the percentage of profit is added to determine the total revenue and then the total

revenue is then divided by the No. of Clients or Passenger Km. in case of the transport

companies.

If Clariton Antiques Limited is a trading concern then it can follow the normal Cost Sheet but the

following items will be excluded as compared to the manufacturing entities:

8

● Cost of Work in Progress.

● Prime Cost.

● Cost of Production. etc.

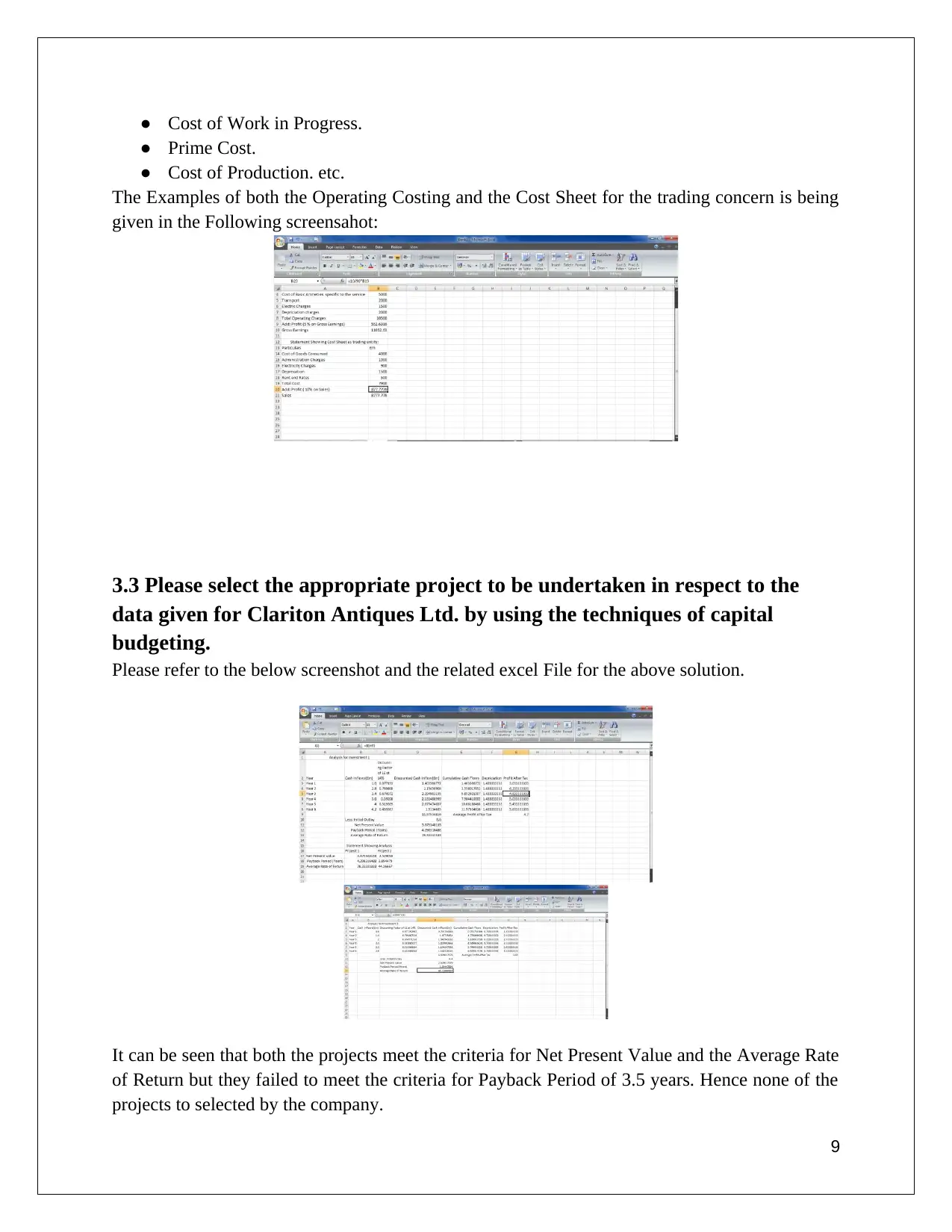

The Examples of both the Operating Costing and the Cost Sheet for the trading concern is being

given in the Following screensahot:

3.3 Please select the appropriate project to be undertaken in respect to the

data given for Clariton Antiques Ltd. by using the techniques of capital

budgeting.

Please refer to the below screenshot and the related excel File for the above solution.

It can be seen that both the projects meet the criteria for Net Present Value and the Average Rate

of Return but they failed to meet the criteria for Payback Period of 3.5 years. Hence none of the

projects to selected by the company.

9

● Prime Cost.

● Cost of Production. etc.

The Examples of both the Operating Costing and the Cost Sheet for the trading concern is being

given in the Following screensahot:

3.3 Please select the appropriate project to be undertaken in respect to the

data given for Clariton Antiques Ltd. by using the techniques of capital

budgeting.

Please refer to the below screenshot and the related excel File for the above solution.

It can be seen that both the projects meet the criteria for Net Present Value and the Average Rate

of Return but they failed to meet the criteria for Payback Period of 3.5 years. Hence none of the

projects to selected by the company.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 4

4.1 Please explain the essential components of the financial statements.

The key components of the financial statements can be discussed as under:

1. Income Statement: Income Statement refers to the statement of Profits and Losses of an

entity. This statement is a detailed statement of the revenue and the expenses of the

organisation. This statement depicts the areas from the revenue has been generated and

the areas from where there is revenue leakage in disguise. This statement provides a base

for evaluating the operating efficiency of the concern (Lee et al. 2017).

2. Statement of Cash Flows: The Cash Flow Statement depicts the activities of from where

the cash has been generated and the activities where the cash has been used. It mainly

contains three divisions. They are Cash Flows from Operating Activities, Cash Flows

from Investing Activities and Cash Flow from Financing Activities ( Miao, Teoh and

Zhu, 2016). The Cash Flow Statement depicts the picture of how the business has

efficiently utilised its cash as well as how the operations of the business have been

effective in generating appropriate cash flows to the organisation.

3. Statement of Changes in Equity and Gains: Ball, Li and Shivakumar (2015) Stated that

Statement of changes in Equity refers to the changes affected in the equity structure of

the company at the end of the accounting year as compared to the preceding accounting

year. It may be affected due to increase in the Paid - up Capital or for increase or

decrease in the reserves and surplus. It can also happen as a result of buy back.

Statement of changes in the Gains refer to the statement which shows all the changes in

the Profit and Loss balance and General Reserves.

4. Statement of Financial Position: Statement of Financial Position refers to the statement of

Assets and Liabilities. It can be also be termed as the Balance Sheet of the entity. It

shows the entire financial position of the enterprise. The banks and the financial

institutions grant loans based on the picture of the Balance Sheet (Gupta, Mills and

Towery, 2014).

5. Notes to the Financial Statements: Notes to the Financial Statement is also termed as

Notes to Accounts. These notes provides the details about all the items of the financial

statement of the entity. Based on these notes a detailed and a wider picture of the Balance

Sheet can be determined (Brochet, Jagolinzer and Riedl, 2013).

10

4.1 Please explain the essential components of the financial statements.

The key components of the financial statements can be discussed as under:

1. Income Statement: Income Statement refers to the statement of Profits and Losses of an

entity. This statement is a detailed statement of the revenue and the expenses of the

organisation. This statement depicts the areas from the revenue has been generated and

the areas from where there is revenue leakage in disguise. This statement provides a base

for evaluating the operating efficiency of the concern (Lee et al. 2017).

2. Statement of Cash Flows: The Cash Flow Statement depicts the activities of from where

the cash has been generated and the activities where the cash has been used. It mainly

contains three divisions. They are Cash Flows from Operating Activities, Cash Flows

from Investing Activities and Cash Flow from Financing Activities ( Miao, Teoh and

Zhu, 2016). The Cash Flow Statement depicts the picture of how the business has

efficiently utilised its cash as well as how the operations of the business have been

effective in generating appropriate cash flows to the organisation.

3. Statement of Changes in Equity and Gains: Ball, Li and Shivakumar (2015) Stated that

Statement of changes in Equity refers to the changes affected in the equity structure of

the company at the end of the accounting year as compared to the preceding accounting

year. It may be affected due to increase in the Paid - up Capital or for increase or

decrease in the reserves and surplus. It can also happen as a result of buy back.

Statement of changes in the Gains refer to the statement which shows all the changes in

the Profit and Loss balance and General Reserves.

4. Statement of Financial Position: Statement of Financial Position refers to the statement of

Assets and Liabilities. It can be also be termed as the Balance Sheet of the entity. It

shows the entire financial position of the enterprise. The banks and the financial

institutions grant loans based on the picture of the Balance Sheet (Gupta, Mills and

Towery, 2014).

5. Notes to the Financial Statements: Notes to the Financial Statement is also termed as

Notes to Accounts. These notes provides the details about all the items of the financial

statement of the entity. Based on these notes a detailed and a wider picture of the Balance

Sheet can be determined (Brochet, Jagolinzer and Riedl, 2013).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.2 Please compare the financial statements as presented by the Clariton

Antiques Ltd., a sole trader and a partnership firm.

We are well aware of the fact that in the modern world in the era of cross border flow of capital

different types financial statements has to maintained by different organisations based on their

structure, type, legal status, etc. Law requires the companies and some of the other categories of

entities are required to maintain a separate form of financial statements in order to comply with

the legislations as well as in the context of Audit Compliance. The Auditor is required to verify

the reliability of the financial statements and report on the transparency and the fairness of the

financial statements.

So the comparison between the financial statements of the entity Clariton Antiques Ltd. and that

of a sole trader and a partnership firm can be framed as we proceed. We are aware that Clariton

Antiques Ltd. is a registered company and therefore has to follow the Statement Format in the

preparation of its Balance Sheet. First comes the analysis of the format of the Statement of Profit

and Loss. Here, the Statement of Profit and Loss can also be termed as the Income Statement.

Here, the company terms the sales as the Revenue from Operations. The operating expenses viz

the cost of goods sold, Cost of Sales as determined from the Cost Sheet, the administrative

expenses, the cost of production and all the other operating expenses are deducted to arrive at the

Operating Profit. Now from the operating profit all the other or the non- operating income and

expenses are adjusted in order to derive the Income before the Interest and Taxes. Now the

Interest Expenses is deducted to arrive at Profit before Tax. From Profit before Tax the Tax

Expenses are deducted to finally arrive at the Figure of Profit After Tax. Now the Preference

Dividend if any is paid out of these Profit after Tax and then we could get the figure of Profit

available to the Equity Shareholders (PAFESH). Now this PAFESH will determine the Basic and

the Diluted EPS and this PAFESH is also available to be distributed as dividends to the Equity

Shareholders.

Now If we at the picture of the partnership firms and the sole trader they prepare two respective

accounts relating to the Profit and Loss. Firstly they prepare the Trading A/c where the direct

expenses viz Purchase of Raw Materials, Inventories, Wages and Opening stock are debited and

is credited with Sales to arrive at the Gross Profit. Now from this Gross Profit we are required to

pay all the indirect expenses in the Profit and Loss Account. All the Indirect Incomes are also

credited in the Profit and Loss to arrive at the figure of Net Profit. This Net Profit is directly

transferred to the owner’s fund and the general reserves. In Partnership Firms one more extra A/c

is created i.e The Profit and Loss Appropriation A/c where all the expenses of the partners are

debited and credited with the charge on the partners to derive at the Distributable Profits which is

either transferred to the Reserves or is shared among the capital accounts of the partners.

So it can be said that the Profit and Loss Statement of the company is much more significant to

the performance of the company compared to that of the Partnership Firm or the Sole Traders.

Now coming to the Statement of Financial Position or the Balance Sheet we can see that both the

sides of the Balance Sheet viz the Assets and the Liabilities are divided into two groups i.e Non-

11

Antiques Ltd., a sole trader and a partnership firm.

We are well aware of the fact that in the modern world in the era of cross border flow of capital

different types financial statements has to maintained by different organisations based on their

structure, type, legal status, etc. Law requires the companies and some of the other categories of

entities are required to maintain a separate form of financial statements in order to comply with

the legislations as well as in the context of Audit Compliance. The Auditor is required to verify

the reliability of the financial statements and report on the transparency and the fairness of the

financial statements.

So the comparison between the financial statements of the entity Clariton Antiques Ltd. and that

of a sole trader and a partnership firm can be framed as we proceed. We are aware that Clariton

Antiques Ltd. is a registered company and therefore has to follow the Statement Format in the

preparation of its Balance Sheet. First comes the analysis of the format of the Statement of Profit

and Loss. Here, the Statement of Profit and Loss can also be termed as the Income Statement.

Here, the company terms the sales as the Revenue from Operations. The operating expenses viz

the cost of goods sold, Cost of Sales as determined from the Cost Sheet, the administrative

expenses, the cost of production and all the other operating expenses are deducted to arrive at the

Operating Profit. Now from the operating profit all the other or the non- operating income and

expenses are adjusted in order to derive the Income before the Interest and Taxes. Now the

Interest Expenses is deducted to arrive at Profit before Tax. From Profit before Tax the Tax

Expenses are deducted to finally arrive at the Figure of Profit After Tax. Now the Preference

Dividend if any is paid out of these Profit after Tax and then we could get the figure of Profit

available to the Equity Shareholders (PAFESH). Now this PAFESH will determine the Basic and

the Diluted EPS and this PAFESH is also available to be distributed as dividends to the Equity

Shareholders.

Now If we at the picture of the partnership firms and the sole trader they prepare two respective

accounts relating to the Profit and Loss. Firstly they prepare the Trading A/c where the direct

expenses viz Purchase of Raw Materials, Inventories, Wages and Opening stock are debited and

is credited with Sales to arrive at the Gross Profit. Now from this Gross Profit we are required to

pay all the indirect expenses in the Profit and Loss Account. All the Indirect Incomes are also

credited in the Profit and Loss to arrive at the figure of Net Profit. This Net Profit is directly

transferred to the owner’s fund and the general reserves. In Partnership Firms one more extra A/c

is created i.e The Profit and Loss Appropriation A/c where all the expenses of the partners are

debited and credited with the charge on the partners to derive at the Distributable Profits which is

either transferred to the Reserves or is shared among the capital accounts of the partners.

So it can be said that the Profit and Loss Statement of the company is much more significant to

the performance of the company compared to that of the Partnership Firm or the Sole Traders.

Now coming to the Statement of Financial Position or the Balance Sheet we can see that both the

sides of the Balance Sheet viz the Assets and the Liabilities are divided into two groups i.e Non-

11

Current and Current Assets and Liabilities. In the Equity and Liabilities Section there is one

more group i.e Shareholder’s Fund where all the credits of the shareholders i.e Paid Up Capital,

Reserves and Surplus are recorded. Whereas in the Balance Sheet of the Sole Trader and the

Partnership Firms , there are generally two halves of the Balance Sheet i.e the Assets and

Liabilities. Only appropriate marshalling of the Assets and the Liabilities are done. It can also be

said that the picture of the Balance Sheet is more clear and relevant in case of a company.

4.3 Please make an interpretation of the financial statements by utilising the

essential ratios and also compare them with that of the preceding year.

The Effective financial ratios in order to evaluate the performance and the financial performance

of the entity are hereby given in the below screenshot and the related Excel File.

12

more group i.e Shareholder’s Fund where all the credits of the shareholders i.e Paid Up Capital,

Reserves and Surplus are recorded. Whereas in the Balance Sheet of the Sole Trader and the

Partnership Firms , there are generally two halves of the Balance Sheet i.e the Assets and

Liabilities. Only appropriate marshalling of the Assets and the Liabilities are done. It can also be

said that the picture of the Balance Sheet is more clear and relevant in case of a company.

4.3 Please make an interpretation of the financial statements by utilising the

essential ratios and also compare them with that of the preceding year.

The Effective financial ratios in order to evaluate the performance and the financial performance

of the entity are hereby given in the below screenshot and the related Excel File.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.