Management Accounting Report: Cost Analysis for Sparky Ltd

VerifiedAdded on 2020/01/28

|13

|3620

|76

Report

AI Summary

This management accounting report analyzes the financial performance of Sparky Ltd, an electricity service provider. It begins by classifying costs (direct and indirect) and exploring costing methods like job, batch, process, contract, and service costing, with examples of FIFO, LIFO, and average costing. The report then presents a cost report, highlighting variances in material and overhead costs, and suggests performance indicators such as turnover, cost control, profitability, and customer base to assess areas for improvement. Recommendations are provided to reduce costs, enhance value, and improve quality through strategies like cost curtailment, value enhancement, and Total Quality Management. The report also details the budgeting process, exploring different methods like static, incremental, and zero-based budgeting, and includes a production budget and material purchase budget. Finally, the report addresses variance analysis, the preparation of an operating statement, and reporting findings to management to enhance business performance and achieve targets. This report provides a comprehensive overview of management accounting principles and their application in a real-world business context.

Management

accounting

1

accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Cost classification......................................................................................................................3

1.2 Costing method..........................................................................................................................4

1.3 Cost calculation..........................................................................................................................4

1.4 Analyse cost by using appropriate technique.............................................................................5

TASK 2.................................................................................................................................................5

2.1 Cost reports................................................................................................................................5

2.2 Performance indicators to determine potential improvements..................................................6

2.3 Suggestions to reduce cost, enhance value and quality.............................................................6

TASK 3.................................................................................................................................................7

3.1 Stating the nature and process of budgeting process ................................................................7

3.2 Selecting appropriate budgeting method by stating its need ....................................................7

3.3 Preparing budgets by taking account the chosen method .........................................................8

3.4 Preparing a cash budget ............................................................................................................9

TASK 4.................................................................................................................................................9

4.1 Calculating possible variances and giving recommendation for the improvement by assessing

the causes ........................................................................................................................................9

4.2 Preparing operating statement reconciling budget ..................................................................10

4.3 Reporting findings to the management according to the responsibility centre .......................10

CONCLUSION...................................................................................................................................11

References..........................................................................................................................................12

2

INTRODUCTION................................................................................................................................3

TASK 1.................................................................................................................................................3

1.1 Cost classification......................................................................................................................3

1.2 Costing method..........................................................................................................................4

1.3 Cost calculation..........................................................................................................................4

1.4 Analyse cost by using appropriate technique.............................................................................5

TASK 2.................................................................................................................................................5

2.1 Cost reports................................................................................................................................5

2.2 Performance indicators to determine potential improvements..................................................6

2.3 Suggestions to reduce cost, enhance value and quality.............................................................6

TASK 3.................................................................................................................................................7

3.1 Stating the nature and process of budgeting process ................................................................7

3.2 Selecting appropriate budgeting method by stating its need ....................................................7

3.3 Preparing budgets by taking account the chosen method .........................................................8

3.4 Preparing a cash budget ............................................................................................................9

TASK 4.................................................................................................................................................9

4.1 Calculating possible variances and giving recommendation for the improvement by assessing

the causes ........................................................................................................................................9

4.2 Preparing operating statement reconciling budget ..................................................................10

4.3 Reporting findings to the management according to the responsibility centre .......................10

CONCLUSION...................................................................................................................................11

References..........................................................................................................................................12

2

INTRODUCTION

Managers plays a crucial role in the organization as they construct policies, rules and take

decisions to enhance business performance. The process of analysing organization's financial

performance, cost report etc. in order to take decisions to control cost and increase profitability is

called management accounting. Sparky Ltd, is an organization who provide electricity services

through its electricians. Present report will demonstrate cost classification, techniques as well as

methods to determine the cost of a product or services. Moreover, budgeting technique and

variances analysis will be done to eliminate negative variances by employing remedial actions so

that Sparky Ltd, can achieve its business targets.

TASK 1

1.1 Cost classification

Sum of expenditures incurred for the production of goods and service is called cost. There

are two types of cost, direct or indirect cost, described below: Direct cost: Expenses which directly can be connected to a specific cost object, is called

direct cost. For instance, material which is used for the production of goods is called direct

material. While, worker's wages which is directly involved in the manufacturing process is

called direct labour (Wilson and et.al., 2016). While, other expenses which can be allocated

directly towards production is called direct overhead.

Indirect cost: Expenses which are not directly related to the production process, is known as

indirect cost. For instance, indirect material, indirect labour, administrative expenses,

supervision, insurance, depreciation etc.

On the basis of above discussion, Sparky Ltd, cost has been determined here as under:

1. Wages of electrician: It is a direct cost because electricians are directly involved in the

process of rendering electricity services to their clients. Therefore, it is a direct labour cost.

2. Tools depreciation: It is an indirect cost which can not be directly traced to a specific cost

element.

3. Accountant salary: It is an indirect cost because it is related to the office expenses instead of

manufacturing process (Tosun and Bağdadioğlu, 2016).

4. Cost of cable and material: This is a direct cost because material and cable are using on the

job.

5. Premises rent: It is an indirect cost because it is an expense to store business inventory not

the production process.

3

Managers plays a crucial role in the organization as they construct policies, rules and take

decisions to enhance business performance. The process of analysing organization's financial

performance, cost report etc. in order to take decisions to control cost and increase profitability is

called management accounting. Sparky Ltd, is an organization who provide electricity services

through its electricians. Present report will demonstrate cost classification, techniques as well as

methods to determine the cost of a product or services. Moreover, budgeting technique and

variances analysis will be done to eliminate negative variances by employing remedial actions so

that Sparky Ltd, can achieve its business targets.

TASK 1

1.1 Cost classification

Sum of expenditures incurred for the production of goods and service is called cost. There

are two types of cost, direct or indirect cost, described below: Direct cost: Expenses which directly can be connected to a specific cost object, is called

direct cost. For instance, material which is used for the production of goods is called direct

material. While, worker's wages which is directly involved in the manufacturing process is

called direct labour (Wilson and et.al., 2016). While, other expenses which can be allocated

directly towards production is called direct overhead.

Indirect cost: Expenses which are not directly related to the production process, is known as

indirect cost. For instance, indirect material, indirect labour, administrative expenses,

supervision, insurance, depreciation etc.

On the basis of above discussion, Sparky Ltd, cost has been determined here as under:

1. Wages of electrician: It is a direct cost because electricians are directly involved in the

process of rendering electricity services to their clients. Therefore, it is a direct labour cost.

2. Tools depreciation: It is an indirect cost which can not be directly traced to a specific cost

element.

3. Accountant salary: It is an indirect cost because it is related to the office expenses instead of

manufacturing process (Tosun and Bağdadioğlu, 2016).

4. Cost of cable and material: This is a direct cost because material and cable are using on the

job.

5. Premises rent: It is an indirect cost because it is an expense to store business inventory not

the production process.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.2 Costing method

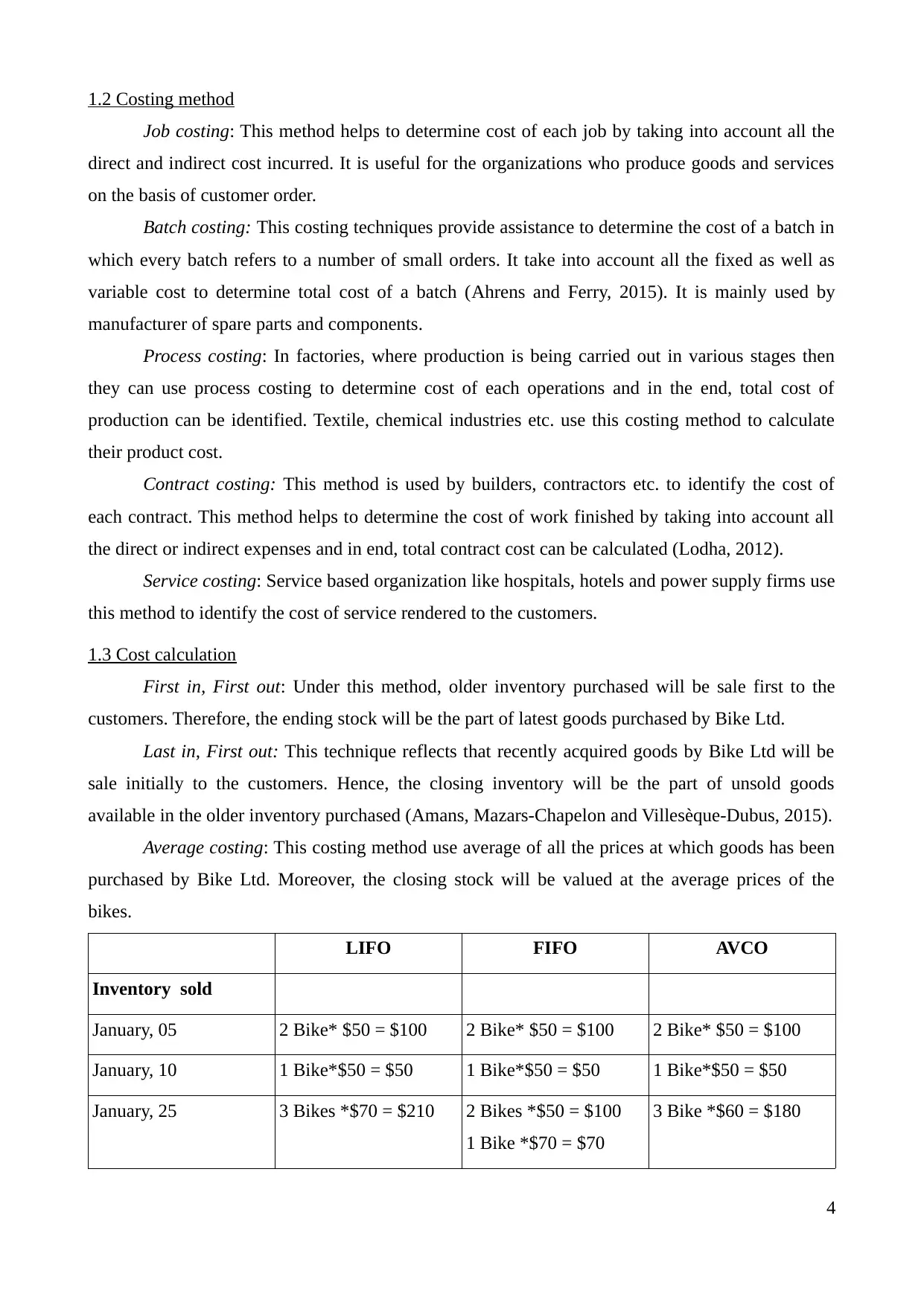

Job costing: This method helps to determine cost of each job by taking into account all the

direct and indirect cost incurred. It is useful for the organizations who produce goods and services

on the basis of customer order.

Batch costing: This costing techniques provide assistance to determine the cost of a batch in

which every batch refers to a number of small orders. It take into account all the fixed as well as

variable cost to determine total cost of a batch (Ahrens and Ferry, 2015). It is mainly used by

manufacturer of spare parts and components.

Process costing: In factories, where production is being carried out in various stages then

they can use process costing to determine cost of each operations and in the end, total cost of

production can be identified. Textile, chemical industries etc. use this costing method to calculate

their product cost.

Contract costing: This method is used by builders, contractors etc. to identify the cost of

each contract. This method helps to determine the cost of work finished by taking into account all

the direct or indirect expenses and in end, total contract cost can be calculated (Lodha, 2012).

Service costing: Service based organization like hospitals, hotels and power supply firms use

this method to identify the cost of service rendered to the customers.

1.3 Cost calculation

First in, First out: Under this method, older inventory purchased will be sale first to the

customers. Therefore, the ending stock will be the part of latest goods purchased by Bike Ltd.

Last in, First out: This technique reflects that recently acquired goods by Bike Ltd will be

sale initially to the customers. Hence, the closing inventory will be the part of unsold goods

available in the older inventory purchased (Amans, Mazars-Chapelon and Villesèque-Dubus, 2015).

Average costing: This costing method use average of all the prices at which goods has been

purchased by Bike Ltd. Moreover, the closing stock will be valued at the average prices of the

bikes.

LIFO FIFO AVCO

Inventory sold

January, 05 2 Bike* $50 = $100 2 Bike* $50 = $100 2 Bike* $50 = $100

January, 10 1 Bike*$50 = $50 1 Bike*$50 = $50 1 Bike*$50 = $50

January, 25 3 Bikes *$70 = $210 2 Bikes *$50 = $100

1 Bike *$70 = $70

3 Bike *$60 = $180

4

Job costing: This method helps to determine cost of each job by taking into account all the

direct and indirect cost incurred. It is useful for the organizations who produce goods and services

on the basis of customer order.

Batch costing: This costing techniques provide assistance to determine the cost of a batch in

which every batch refers to a number of small orders. It take into account all the fixed as well as

variable cost to determine total cost of a batch (Ahrens and Ferry, 2015). It is mainly used by

manufacturer of spare parts and components.

Process costing: In factories, where production is being carried out in various stages then

they can use process costing to determine cost of each operations and in the end, total cost of

production can be identified. Textile, chemical industries etc. use this costing method to calculate

their product cost.

Contract costing: This method is used by builders, contractors etc. to identify the cost of

each contract. This method helps to determine the cost of work finished by taking into account all

the direct or indirect expenses and in end, total contract cost can be calculated (Lodha, 2012).

Service costing: Service based organization like hospitals, hotels and power supply firms use

this method to identify the cost of service rendered to the customers.

1.3 Cost calculation

First in, First out: Under this method, older inventory purchased will be sale first to the

customers. Therefore, the ending stock will be the part of latest goods purchased by Bike Ltd.

Last in, First out: This technique reflects that recently acquired goods by Bike Ltd will be

sale initially to the customers. Hence, the closing inventory will be the part of unsold goods

available in the older inventory purchased (Amans, Mazars-Chapelon and Villesèque-Dubus, 2015).

Average costing: This costing method use average of all the prices at which goods has been

purchased by Bike Ltd. Moreover, the closing stock will be valued at the average prices of the

bikes.

LIFO FIFO AVCO

Inventory sold

January, 05 2 Bike* $50 = $100 2 Bike* $50 = $100 2 Bike* $50 = $100

January, 10 1 Bike*$50 = $50 1 Bike*$50 = $50 1 Bike*$50 = $50

January, 25 3 Bikes *$70 = $210 2 Bikes *$50 = $100

1 Bike *$70 = $70

3 Bike *$60 = $180

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

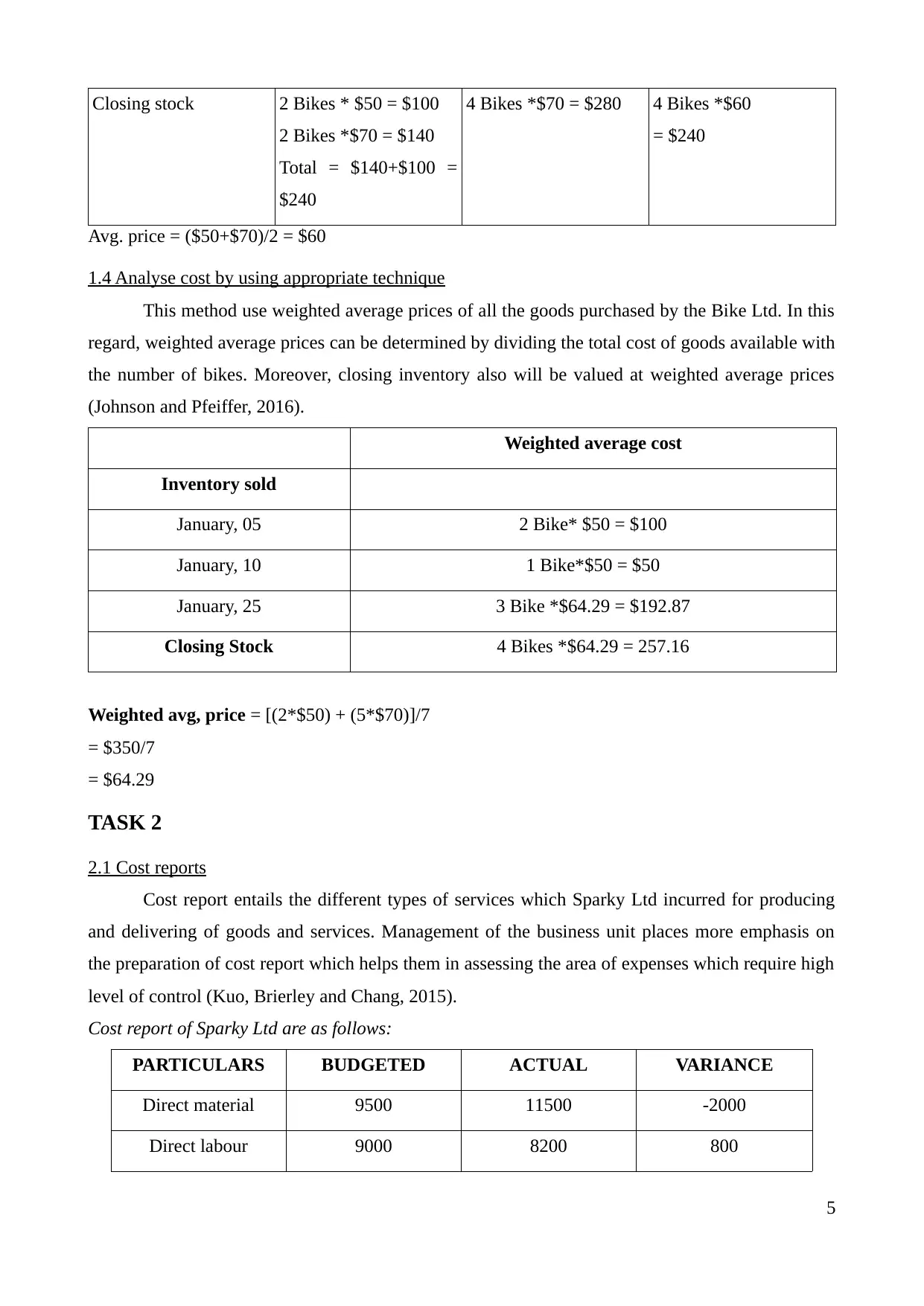

Closing stock 2 Bikes * $50 = $100

2 Bikes *$70 = $140

Total = $140+$100 =

$240

4 Bikes *$70 = $280 4 Bikes *$60

= $240

Avg. price = ($50+$70)/2 = $60

1.4 Analyse cost by using appropriate technique

This method use weighted average prices of all the goods purchased by the Bike Ltd. In this

regard, weighted average prices can be determined by dividing the total cost of goods available with

the number of bikes. Moreover, closing inventory also will be valued at weighted average prices

(Johnson and Pfeiffer, 2016).

Weighted average cost

Inventory sold

January, 05 2 Bike* $50 = $100

January, 10 1 Bike*$50 = $50

January, 25 3 Bike *$64.29 = $192.87

Closing Stock 4 Bikes *$64.29 = 257.16

Weighted avg, price = [(2*$50) + (5*$70)]/7

= $350/7

= $64.29

TASK 2

2.1 Cost reports

Cost report entails the different types of services which Sparky Ltd incurred for producing

and delivering of goods and services. Management of the business unit places more emphasis on

the preparation of cost report which helps them in assessing the area of expenses which require high

level of control (Kuo, Brierley and Chang, 2015).

Cost report of Sparky Ltd are as follows:

PARTICULARS BUDGETED ACTUAL VARIANCE

Direct material 9500 11500 -2000

Direct labour 9000 8200 800

5

2 Bikes *$70 = $140

Total = $140+$100 =

$240

4 Bikes *$70 = $280 4 Bikes *$60

= $240

Avg. price = ($50+$70)/2 = $60

1.4 Analyse cost by using appropriate technique

This method use weighted average prices of all the goods purchased by the Bike Ltd. In this

regard, weighted average prices can be determined by dividing the total cost of goods available with

the number of bikes. Moreover, closing inventory also will be valued at weighted average prices

(Johnson and Pfeiffer, 2016).

Weighted average cost

Inventory sold

January, 05 2 Bike* $50 = $100

January, 10 1 Bike*$50 = $50

January, 25 3 Bike *$64.29 = $192.87

Closing Stock 4 Bikes *$64.29 = 257.16

Weighted avg, price = [(2*$50) + (5*$70)]/7

= $350/7

= $64.29

TASK 2

2.1 Cost reports

Cost report entails the different types of services which Sparky Ltd incurred for producing

and delivering of goods and services. Management of the business unit places more emphasis on

the preparation of cost report which helps them in assessing the area of expenses which require high

level of control (Kuo, Brierley and Chang, 2015).

Cost report of Sparky Ltd are as follows:

PARTICULARS BUDGETED ACTUAL VARIANCE

Direct material 9500 11500 -2000

Direct labour 9000 8200 800

5

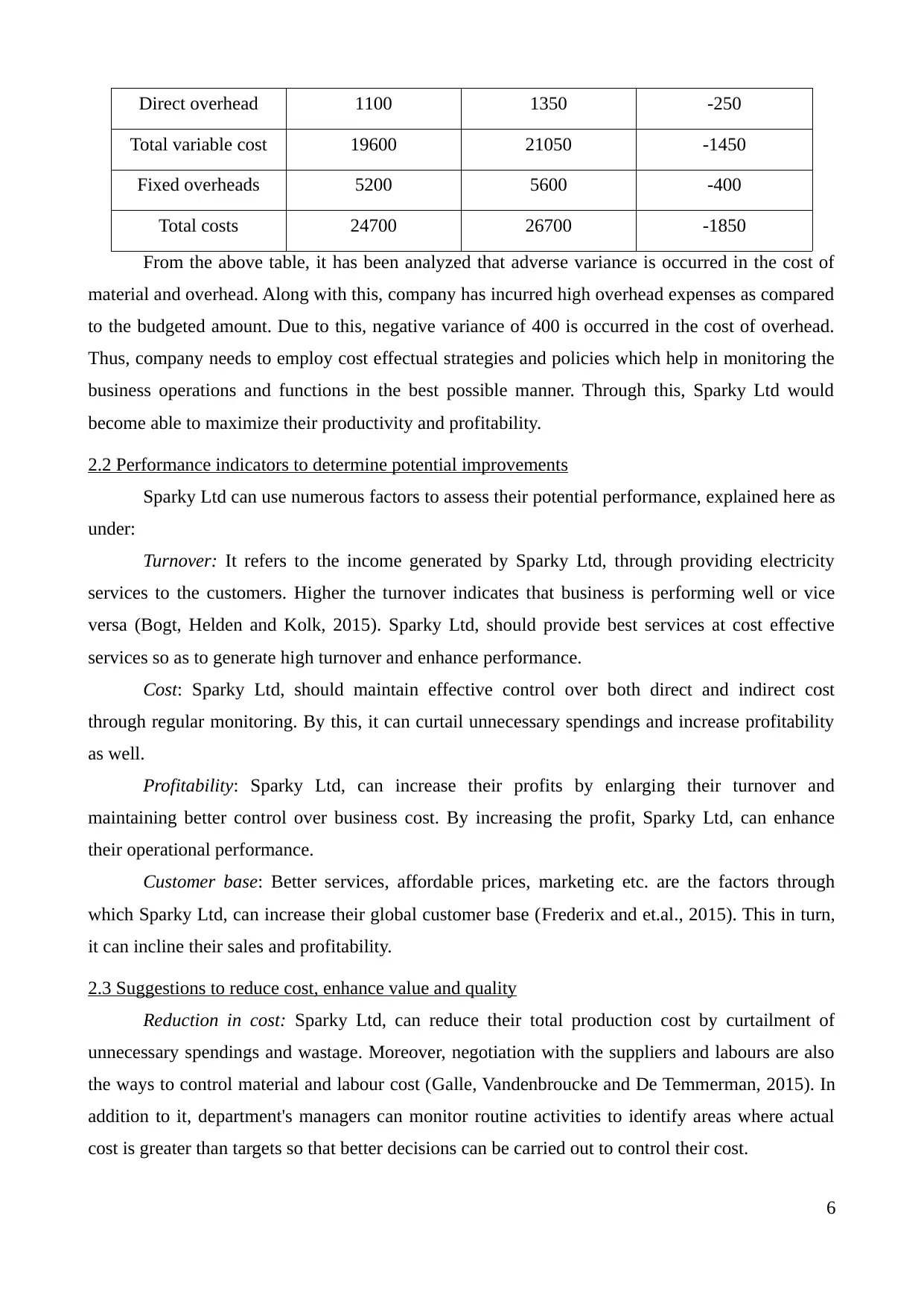

Direct overhead 1100 1350 -250

Total variable cost 19600 21050 -1450

Fixed overheads 5200 5600 -400

Total costs 24700 26700 -1850

From the above table, it has been analyzed that adverse variance is occurred in the cost of

material and overhead. Along with this, company has incurred high overhead expenses as compared

to the budgeted amount. Due to this, negative variance of 400 is occurred in the cost of overhead.

Thus, company needs to employ cost effectual strategies and policies which help in monitoring the

business operations and functions in the best possible manner. Through this, Sparky Ltd would

become able to maximize their productivity and profitability.

2.2 Performance indicators to determine potential improvements

Sparky Ltd can use numerous factors to assess their potential performance, explained here as

under:

Turnover: It refers to the income generated by Sparky Ltd, through providing electricity

services to the customers. Higher the turnover indicates that business is performing well or vice

versa (Bogt, Helden and Kolk, 2015). Sparky Ltd, should provide best services at cost effective

services so as to generate high turnover and enhance performance.

Cost: Sparky Ltd, should maintain effective control over both direct and indirect cost

through regular monitoring. By this, it can curtail unnecessary spendings and increase profitability

as well.

Profitability: Sparky Ltd, can increase their profits by enlarging their turnover and

maintaining better control over business cost. By increasing the profit, Sparky Ltd, can enhance

their operational performance.

Customer base: Better services, affordable prices, marketing etc. are the factors through

which Sparky Ltd, can increase their global customer base (Frederix and et.al., 2015). This in turn,

it can incline their sales and profitability.

2.3 Suggestions to reduce cost, enhance value and quality

Reduction in cost: Sparky Ltd, can reduce their total production cost by curtailment of

unnecessary spendings and wastage. Moreover, negotiation with the suppliers and labours are also

the ways to control material and labour cost (Galle, Vandenbroucke and De Temmerman, 2015). In

addition to it, department's managers can monitor routine activities to identify areas where actual

cost is greater than targets so that better decisions can be carried out to control their cost.

6

Total variable cost 19600 21050 -1450

Fixed overheads 5200 5600 -400

Total costs 24700 26700 -1850

From the above table, it has been analyzed that adverse variance is occurred in the cost of

material and overhead. Along with this, company has incurred high overhead expenses as compared

to the budgeted amount. Due to this, negative variance of 400 is occurred in the cost of overhead.

Thus, company needs to employ cost effectual strategies and policies which help in monitoring the

business operations and functions in the best possible manner. Through this, Sparky Ltd would

become able to maximize their productivity and profitability.

2.2 Performance indicators to determine potential improvements

Sparky Ltd can use numerous factors to assess their potential performance, explained here as

under:

Turnover: It refers to the income generated by Sparky Ltd, through providing electricity

services to the customers. Higher the turnover indicates that business is performing well or vice

versa (Bogt, Helden and Kolk, 2015). Sparky Ltd, should provide best services at cost effective

services so as to generate high turnover and enhance performance.

Cost: Sparky Ltd, should maintain effective control over both direct and indirect cost

through regular monitoring. By this, it can curtail unnecessary spendings and increase profitability

as well.

Profitability: Sparky Ltd, can increase their profits by enlarging their turnover and

maintaining better control over business cost. By increasing the profit, Sparky Ltd, can enhance

their operational performance.

Customer base: Better services, affordable prices, marketing etc. are the factors through

which Sparky Ltd, can increase their global customer base (Frederix and et.al., 2015). This in turn,

it can incline their sales and profitability.

2.3 Suggestions to reduce cost, enhance value and quality

Reduction in cost: Sparky Ltd, can reduce their total production cost by curtailment of

unnecessary spendings and wastage. Moreover, negotiation with the suppliers and labours are also

the ways to control material and labour cost (Galle, Vandenbroucke and De Temmerman, 2015). In

addition to it, department's managers can monitor routine activities to identify areas where actual

cost is greater than targets so that better decisions can be carried out to control their cost.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Enhance value: Sparky Ltd, can enhance their value by rendering qualitative services to the

customers. Through this, they can increase their turnover as well as profitability. Further, it can

provide better return to the shareholders which helps to increase investor's worth. In addition,

business expansion, technological development, introduction of new product or service etc. are the

ways available to increase Sparky Ltd's value.

Enhance quality: Total Quality Management (TQM) is the best technique to enhance quality

of electricity services (Akhavan, Ward and Bozic, 2016). In this approach, all the staff member of

Sparky Ltd, will put their efforts to enhance the quality of production process, products and

services. Along with this, use of advanced and upgraded technology also provide huge assistance to

increase their product quality.

TASK 3

3.1 Stating the nature and process of budgeting process

Budgeting meaning- Budgeting is a process of expressing qualified resource requirements. It is a

tool of planning and control, it involves the steps of setting short term objective, specifying

programs, and expressing them in the budget.

Objectives;

Budgeting helps to know how much money we have coming in, and going out of the sparky

Ltd.

A budgeting is especially useful for giving a company guidance regarding the direction in

which it is supposed to be going. By framing budget business unit is able to avoid unnecessary expenses by comparing the

actual performance with the standard one (Messner, 2016). Hence, by assessing the

deviation company is become able to undertake effectual measures within the suitable time

frame.

Nature of budgeting process

Estimating the future goal and gather data.

Identifying the resources and alternatives.

Creating the budget plan.

Monitor outcome analysis variances.

Adjust budget expectation and goal.

3.2 Selecting appropriate budgeting method by stating its need

There are different types of budgeting methods available to Sparky Ltd, to construct their budget to

prepare future plan. Here, some methods which company can use, are described below:

7

customers. Through this, they can increase their turnover as well as profitability. Further, it can

provide better return to the shareholders which helps to increase investor's worth. In addition,

business expansion, technological development, introduction of new product or service etc. are the

ways available to increase Sparky Ltd's value.

Enhance quality: Total Quality Management (TQM) is the best technique to enhance quality

of electricity services (Akhavan, Ward and Bozic, 2016). In this approach, all the staff member of

Sparky Ltd, will put their efforts to enhance the quality of production process, products and

services. Along with this, use of advanced and upgraded technology also provide huge assistance to

increase their product quality.

TASK 3

3.1 Stating the nature and process of budgeting process

Budgeting meaning- Budgeting is a process of expressing qualified resource requirements. It is a

tool of planning and control, it involves the steps of setting short term objective, specifying

programs, and expressing them in the budget.

Objectives;

Budgeting helps to know how much money we have coming in, and going out of the sparky

Ltd.

A budgeting is especially useful for giving a company guidance regarding the direction in

which it is supposed to be going. By framing budget business unit is able to avoid unnecessary expenses by comparing the

actual performance with the standard one (Messner, 2016). Hence, by assessing the

deviation company is become able to undertake effectual measures within the suitable time

frame.

Nature of budgeting process

Estimating the future goal and gather data.

Identifying the resources and alternatives.

Creating the budget plan.

Monitor outcome analysis variances.

Adjust budget expectation and goal.

3.2 Selecting appropriate budgeting method by stating its need

There are different types of budgeting methods available to Sparky Ltd, to construct their budget to

prepare future plan. Here, some methods which company can use, are described below:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Static budgeting: It is prepared only for a specified production level, so it is also known as

the fixed budgeting method. It is not possible to produce target number of units in real

market. Incremental budgeting: In this type of budgeting, management does not intend to spend a

great deal of time formulating of budget or where it does not perceive any need to conduct

the re- evaluation of business (Wilson and et.al., 2016).

Zero-based budgeting; In this budgeting company have to justified all expenses for each

new period. It helps to ensure optimum utilization of resource. It manages the cost and

enlarge profitability.

3.3 Preparing budgets by taking account the chosen method

Production budget

Particulars July August September

Forecasted sales 42000 48000 60000

Add: Closing stock 7500 9100 10900

Total 49500 57100 70900

Less: Opening stock 5200 6800 8800

Production Required 44300 50300 62100

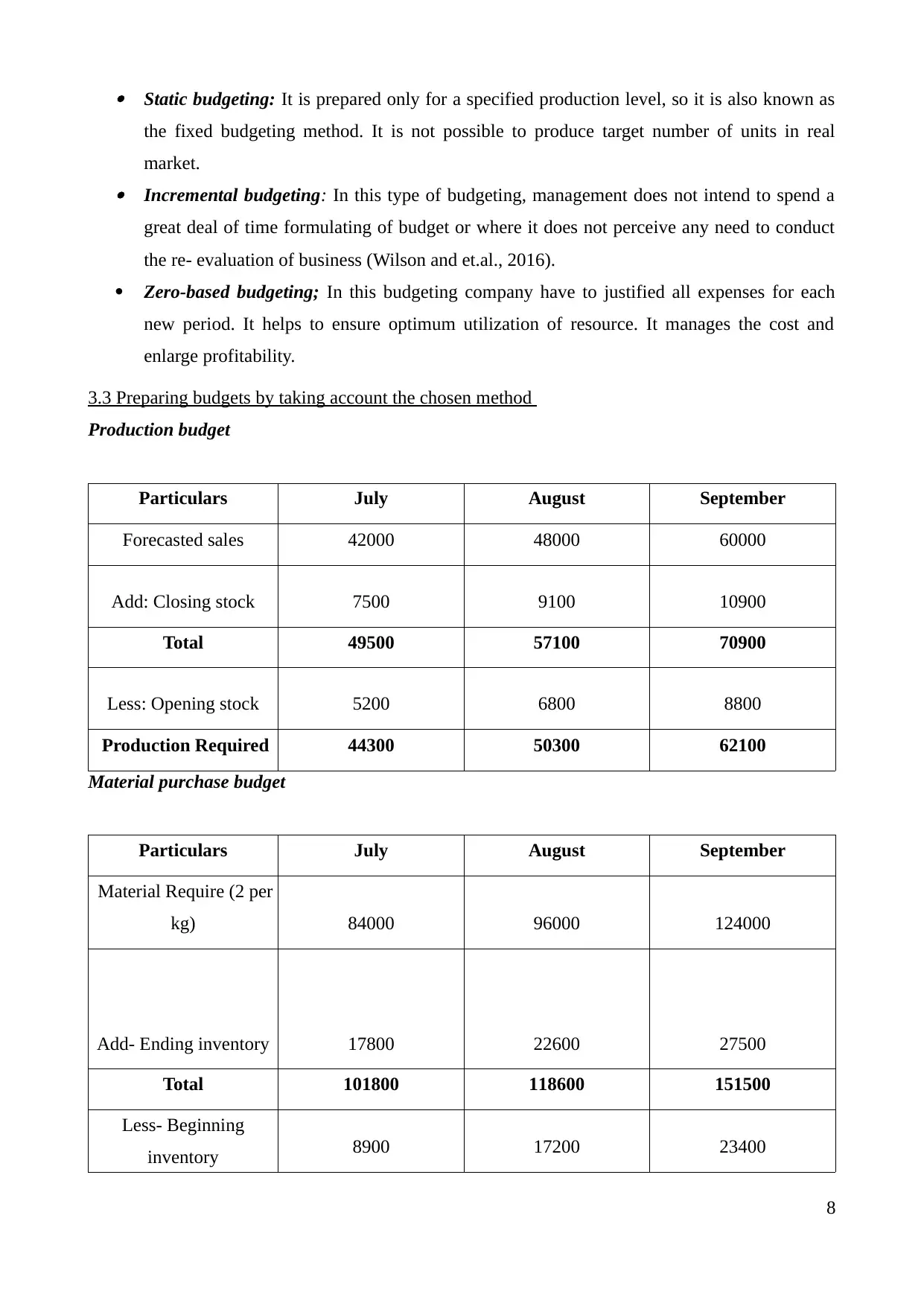

Material purchase budget

Particulars July August September

Material Require (2 per

kg) 84000 96000 124000

Add- Ending inventory 17800 22600 27500

Total 101800 118600 151500

Less- Beginning

inventory 8900 17200 23400

8

the fixed budgeting method. It is not possible to produce target number of units in real

market. Incremental budgeting: In this type of budgeting, management does not intend to spend a

great deal of time formulating of budget or where it does not perceive any need to conduct

the re- evaluation of business (Wilson and et.al., 2016).

Zero-based budgeting; In this budgeting company have to justified all expenses for each

new period. It helps to ensure optimum utilization of resource. It manages the cost and

enlarge profitability.

3.3 Preparing budgets by taking account the chosen method

Production budget

Particulars July August September

Forecasted sales 42000 48000 60000

Add: Closing stock 7500 9100 10900

Total 49500 57100 70900

Less: Opening stock 5200 6800 8800

Production Required 44300 50300 62100

Material purchase budget

Particulars July August September

Material Require (2 per

kg) 84000 96000 124000

Add- Ending inventory 17800 22600 27500

Total 101800 118600 151500

Less- Beginning

inventory 8900 17200 23400

8

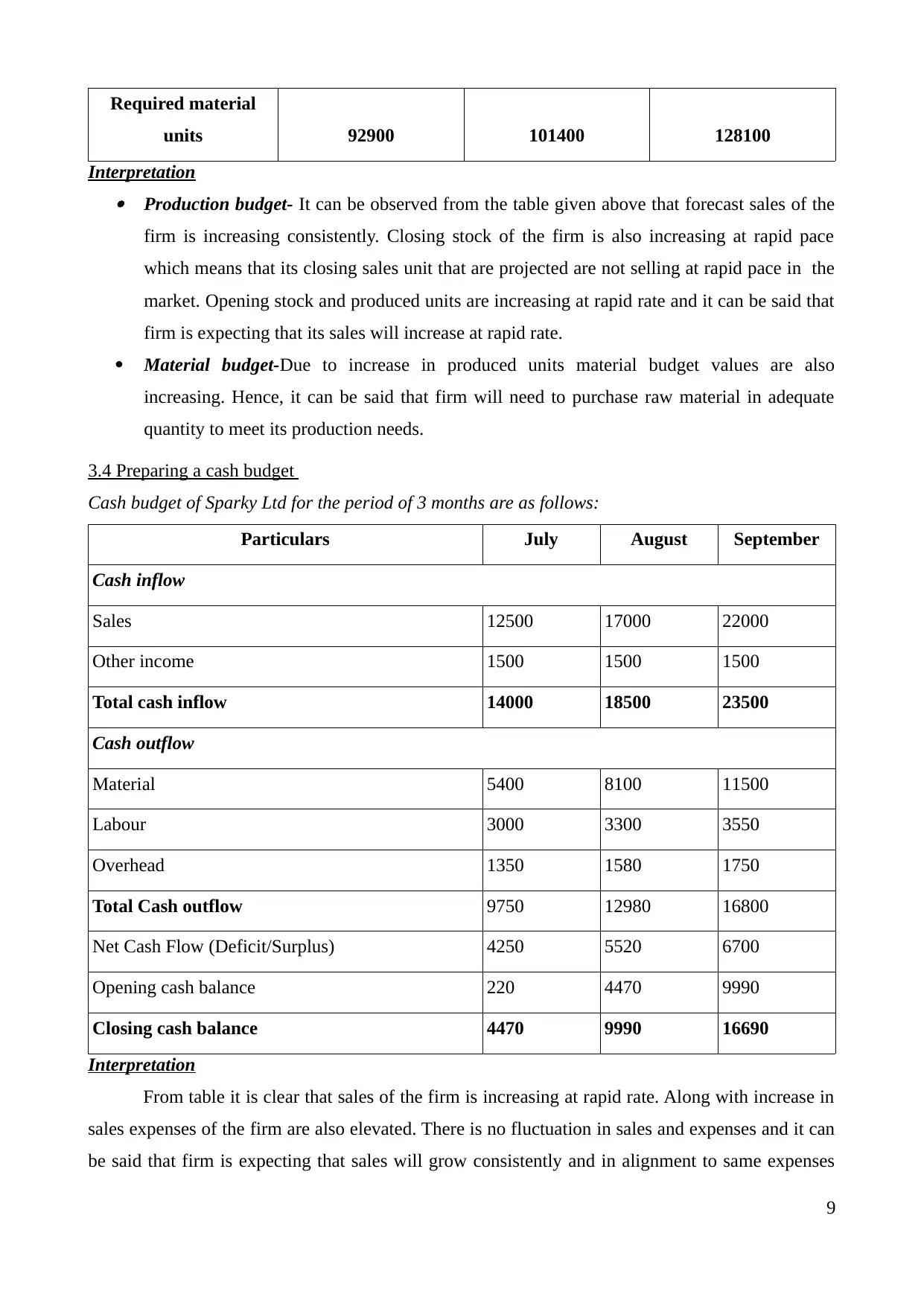

Required material

units 92900 101400 128100

Interpretation Production budget- It can be observed from the table given above that forecast sales of the

firm is increasing consistently. Closing stock of the firm is also increasing at rapid pace

which means that its closing sales unit that are projected are not selling at rapid pace in the

market. Opening stock and produced units are increasing at rapid rate and it can be said that

firm is expecting that its sales will increase at rapid rate.

Material budget-Due to increase in produced units material budget values are also

increasing. Hence, it can be said that firm will need to purchase raw material in adequate

quantity to meet its production needs.

3.4 Preparing a cash budget

Cash budget of Sparky Ltd for the period of 3 months are as follows:

Particulars July August September

Cash inflow

Sales 12500 17000 22000

Other income 1500 1500 1500

Total cash inflow 14000 18500 23500

Cash outflow

Material 5400 8100 11500

Labour 3000 3300 3550

Overhead 1350 1580 1750

Total Cash outflow 9750 12980 16800

Net Cash Flow (Deficit/Surplus) 4250 5520 6700

Opening cash balance 220 4470 9990

Closing cash balance 4470 9990 16690

Interpretation

From table it is clear that sales of the firm is increasing at rapid rate. Along with increase in

sales expenses of the firm are also elevated. There is no fluctuation in sales and expenses and it can

be said that firm is expecting that sales will grow consistently and in alignment to same expenses

9

units 92900 101400 128100

Interpretation Production budget- It can be observed from the table given above that forecast sales of the

firm is increasing consistently. Closing stock of the firm is also increasing at rapid pace

which means that its closing sales unit that are projected are not selling at rapid pace in the

market. Opening stock and produced units are increasing at rapid rate and it can be said that

firm is expecting that its sales will increase at rapid rate.

Material budget-Due to increase in produced units material budget values are also

increasing. Hence, it can be said that firm will need to purchase raw material in adequate

quantity to meet its production needs.

3.4 Preparing a cash budget

Cash budget of Sparky Ltd for the period of 3 months are as follows:

Particulars July August September

Cash inflow

Sales 12500 17000 22000

Other income 1500 1500 1500

Total cash inflow 14000 18500 23500

Cash outflow

Material 5400 8100 11500

Labour 3000 3300 3550

Overhead 1350 1580 1750

Total Cash outflow 9750 12980 16800

Net Cash Flow (Deficit/Surplus) 4250 5520 6700

Opening cash balance 220 4470 9990

Closing cash balance 4470 9990 16690

Interpretation

From table it is clear that sales of the firm is increasing at rapid rate. Along with increase in

sales expenses of the firm are also elevated. There is no fluctuation in sales and expenses and it can

be said that firm is expecting that sales will grow consistently and in alignment to same expenses

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

will also increase.

TASK 4

4.1 Calculating possible variances and giving recommendation for the improvement by assessing

the causes

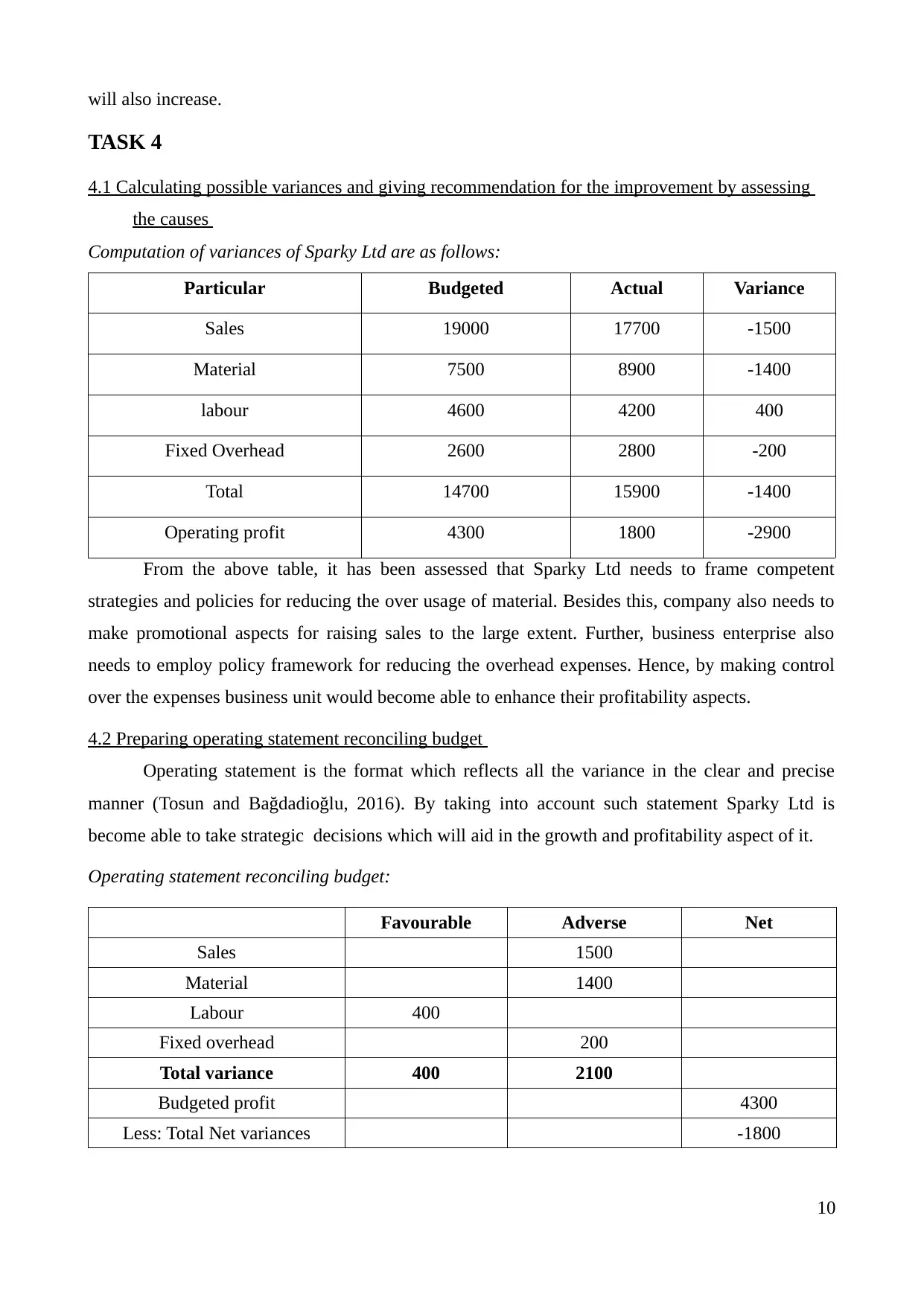

Computation of variances of Sparky Ltd are as follows:

Particular Budgeted Actual Variance

Sales 19000 17700 -1500

Material 7500 8900 -1400

labour 4600 4200 400

Fixed Overhead 2600 2800 -200

Total 14700 15900 -1400

Operating profit 4300 1800 -2900

From the above table, it has been assessed that Sparky Ltd needs to frame competent

strategies and policies for reducing the over usage of material. Besides this, company also needs to

make promotional aspects for raising sales to the large extent. Further, business enterprise also

needs to employ policy framework for reducing the overhead expenses. Hence, by making control

over the expenses business unit would become able to enhance their profitability aspects.

4.2 Preparing operating statement reconciling budget

Operating statement is the format which reflects all the variance in the clear and precise

manner (Tosun and Bağdadioğlu, 2016). By taking into account such statement Sparky Ltd is

become able to take strategic decisions which will aid in the growth and profitability aspect of it.

Operating statement reconciling budget:

Favourable Adverse Net

Sales 1500

Material 1400

Labour 400

Fixed overhead 200

Total variance 400 2100

Budgeted profit 4300

Less: Total Net variances -1800

10

TASK 4

4.1 Calculating possible variances and giving recommendation for the improvement by assessing

the causes

Computation of variances of Sparky Ltd are as follows:

Particular Budgeted Actual Variance

Sales 19000 17700 -1500

Material 7500 8900 -1400

labour 4600 4200 400

Fixed Overhead 2600 2800 -200

Total 14700 15900 -1400

Operating profit 4300 1800 -2900

From the above table, it has been assessed that Sparky Ltd needs to frame competent

strategies and policies for reducing the over usage of material. Besides this, company also needs to

make promotional aspects for raising sales to the large extent. Further, business enterprise also

needs to employ policy framework for reducing the overhead expenses. Hence, by making control

over the expenses business unit would become able to enhance their profitability aspects.

4.2 Preparing operating statement reconciling budget

Operating statement is the format which reflects all the variance in the clear and precise

manner (Tosun and Bağdadioğlu, 2016). By taking into account such statement Sparky Ltd is

become able to take strategic decisions which will aid in the growth and profitability aspect of it.

Operating statement reconciling budget:

Favourable Adverse Net

Sales 1500

Material 1400

Labour 400

Fixed overhead 200

Total variance 400 2100

Budgeted profit 4300

Less: Total Net variances -1800

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

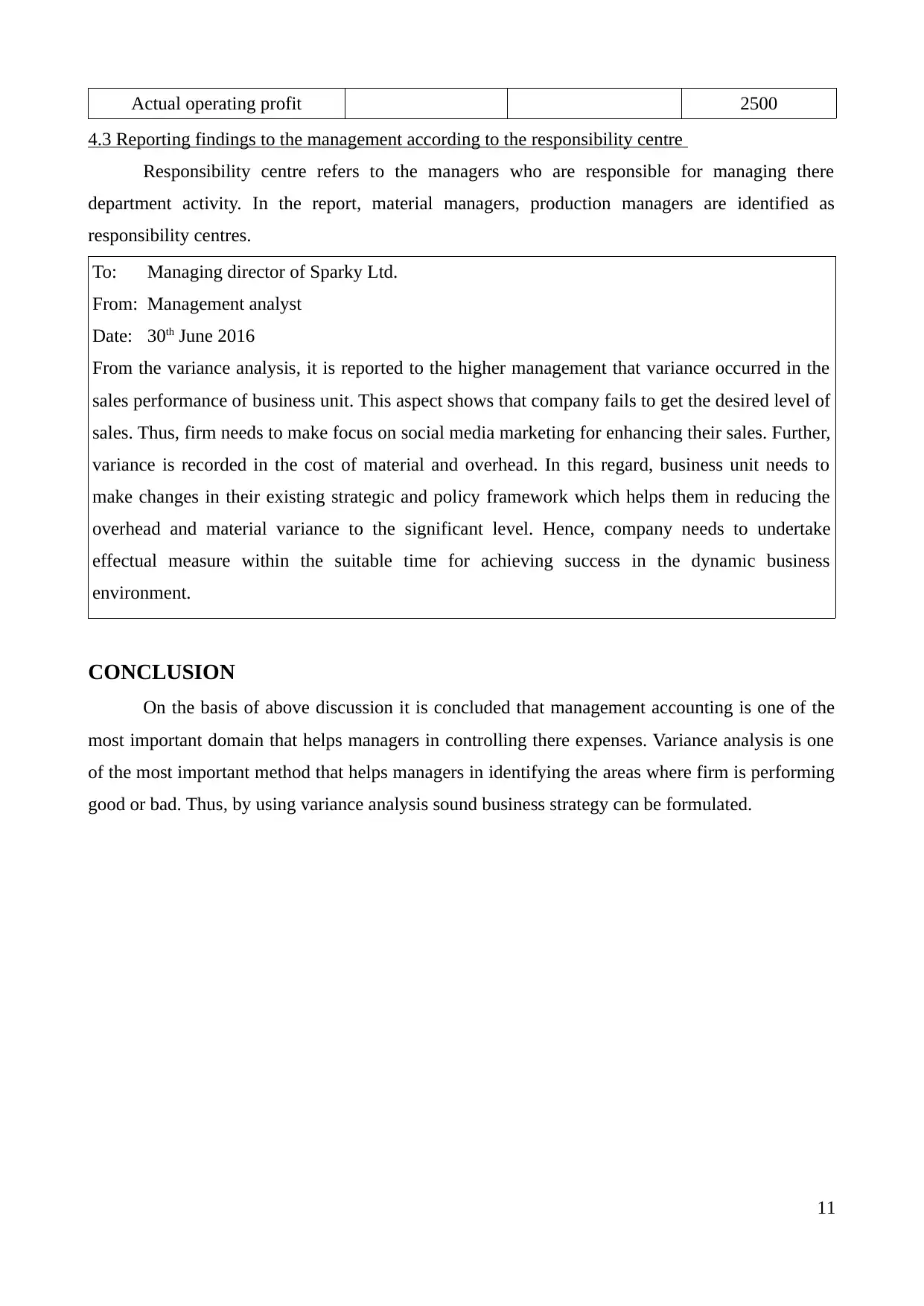

Actual operating profit 2500

4.3 Reporting findings to the management according to the responsibility centre

Responsibility centre refers to the managers who are responsible for managing there

department activity. In the report, material managers, production managers are identified as

responsibility centres.

To: Managing director of Sparky Ltd.

From: Management analyst

Date: 30th June 2016

From the variance analysis, it is reported to the higher management that variance occurred in the

sales performance of business unit. This aspect shows that company fails to get the desired level of

sales. Thus, firm needs to make focus on social media marketing for enhancing their sales. Further,

variance is recorded in the cost of material and overhead. In this regard, business unit needs to

make changes in their existing strategic and policy framework which helps them in reducing the

overhead and material variance to the significant level. Hence, company needs to undertake

effectual measure within the suitable time for achieving success in the dynamic business

environment.

CONCLUSION

On the basis of above discussion it is concluded that management accounting is one of the

most important domain that helps managers in controlling there expenses. Variance analysis is one

of the most important method that helps managers in identifying the areas where firm is performing

good or bad. Thus, by using variance analysis sound business strategy can be formulated.

11

4.3 Reporting findings to the management according to the responsibility centre

Responsibility centre refers to the managers who are responsible for managing there

department activity. In the report, material managers, production managers are identified as

responsibility centres.

To: Managing director of Sparky Ltd.

From: Management analyst

Date: 30th June 2016

From the variance analysis, it is reported to the higher management that variance occurred in the

sales performance of business unit. This aspect shows that company fails to get the desired level of

sales. Thus, firm needs to make focus on social media marketing for enhancing their sales. Further,

variance is recorded in the cost of material and overhead. In this regard, business unit needs to

make changes in their existing strategic and policy framework which helps them in reducing the

overhead and material variance to the significant level. Hence, company needs to undertake

effectual measure within the suitable time for achieving success in the dynamic business

environment.

CONCLUSION

On the basis of above discussion it is concluded that management accounting is one of the

most important domain that helps managers in controlling there expenses. Variance analysis is one

of the most important method that helps managers in identifying the areas where firm is performing

good or bad. Thus, by using variance analysis sound business strategy can be formulated.

11

REFERENCES

Books and Journals

Ahrens, T. and Ferry, L., 2015. Newcastle City Council and the grassroots: accountability and

budgeting under austerity. Accounting, Auditing & Accountability Journal. 28(6). pp.909-

933.

Akhavan, S., Ward, L. and Bozic, K.J., 2016. Time-driven activity-based costing more accurately

reflects costs in arthroplasty surgery. Clinical Orthopaedics and Related Research®.

474(1). pp.8-15.

Amans, P., Mazars-Chapelon, A. and Villesèque-Dubus, F., 2015. Budgeting in institutional

complexity: The case of performing arts organizations. Management Accounting Research.

27. pp.47-66.

Bogt, H.J., Helden, G.J. and Kolk, B., 2015. Challenging the NPM Ideas About Performance

Management: Selectivity and Differentiation in Outcome‐Oriented Performance Budgeting.

Financial Accountability & Management. 31(3). pp.287-315.

Frederix, G.W.J. and et.al., 2015. Real world cost of human epidermal receptor 2‐positive

metastatic breast cancer patients: a longitudinal incidence‐based observational costing study

in the Netherlands and Belgium. European journal of cancer care. 24(3). pp.340-354.

Galle, W., Vandenbroucke, M. and De Temmerman, N., 2015. Life cycle costing as an early stage

feasibility analysis: The adaptable transformation of Willy Van Der Meeren's student

residences. Procedia Economics and Finance. 21. pp.14-22.

Johnson, N.B. and Pfeiffer, T., 2016. Capital Budgeting and Divisional Performance Measurement.

Foundations and Trends (R) in Accounting. 10(1). pp.1-100.

Kuo, C.W., Brierley, G. and Chang, Y.H., 2015. Monitoring channel responses to flood events of

low to moderate magnitudes in a bedrock-dominated river using morphological budgeting

by terrestrial laser scanning. Geomorphology. 235. pp.1-14.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Tosun, C. and Bağdadioğlu, N., 2016. Evaluating gender responsive budgeting in Turkey.

International Journal of Monetary Economics and Finance. 9(2). pp.187-197.

Wilson, A.L. and et.al., 2016. Improving shopping and budgeting behaviours in people with

depression. Journal of Nutrition & Intermediary Metabolism. 4. pp.47.

Online

12

Books and Journals

Ahrens, T. and Ferry, L., 2015. Newcastle City Council and the grassroots: accountability and

budgeting under austerity. Accounting, Auditing & Accountability Journal. 28(6). pp.909-

933.

Akhavan, S., Ward, L. and Bozic, K.J., 2016. Time-driven activity-based costing more accurately

reflects costs in arthroplasty surgery. Clinical Orthopaedics and Related Research®.

474(1). pp.8-15.

Amans, P., Mazars-Chapelon, A. and Villesèque-Dubus, F., 2015. Budgeting in institutional

complexity: The case of performing arts organizations. Management Accounting Research.

27. pp.47-66.

Bogt, H.J., Helden, G.J. and Kolk, B., 2015. Challenging the NPM Ideas About Performance

Management: Selectivity and Differentiation in Outcome‐Oriented Performance Budgeting.

Financial Accountability & Management. 31(3). pp.287-315.

Frederix, G.W.J. and et.al., 2015. Real world cost of human epidermal receptor 2‐positive

metastatic breast cancer patients: a longitudinal incidence‐based observational costing study

in the Netherlands and Belgium. European journal of cancer care. 24(3). pp.340-354.

Galle, W., Vandenbroucke, M. and De Temmerman, N., 2015. Life cycle costing as an early stage

feasibility analysis: The adaptable transformation of Willy Van Der Meeren's student

residences. Procedia Economics and Finance. 21. pp.14-22.

Johnson, N.B. and Pfeiffer, T., 2016. Capital Budgeting and Divisional Performance Measurement.

Foundations and Trends (R) in Accounting. 10(1). pp.1-100.

Kuo, C.W., Brierley, G. and Chang, Y.H., 2015. Monitoring channel responses to flood events of

low to moderate magnitudes in a bedrock-dominated river using morphological budgeting

by terrestrial laser scanning. Geomorphology. 235. pp.1-14.

Messner, M., 2016. Does industry matter? How industry context shapes management accounting

practice. Management Accounting Research. 31. pp.103-111.

Tosun, C. and Bağdadioğlu, N., 2016. Evaluating gender responsive budgeting in Turkey.

International Journal of Monetary Economics and Finance. 9(2). pp.187-197.

Wilson, A.L. and et.al., 2016. Improving shopping and budgeting behaviours in people with

depression. Journal of Nutrition & Intermediary Metabolism. 4. pp.47.

Online

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.