Contemporary Issues in Accounting: SpeedCast Financial Report Analysis

VerifiedAdded on 2023/01/19

|14

|2250

|20

Report

AI Summary

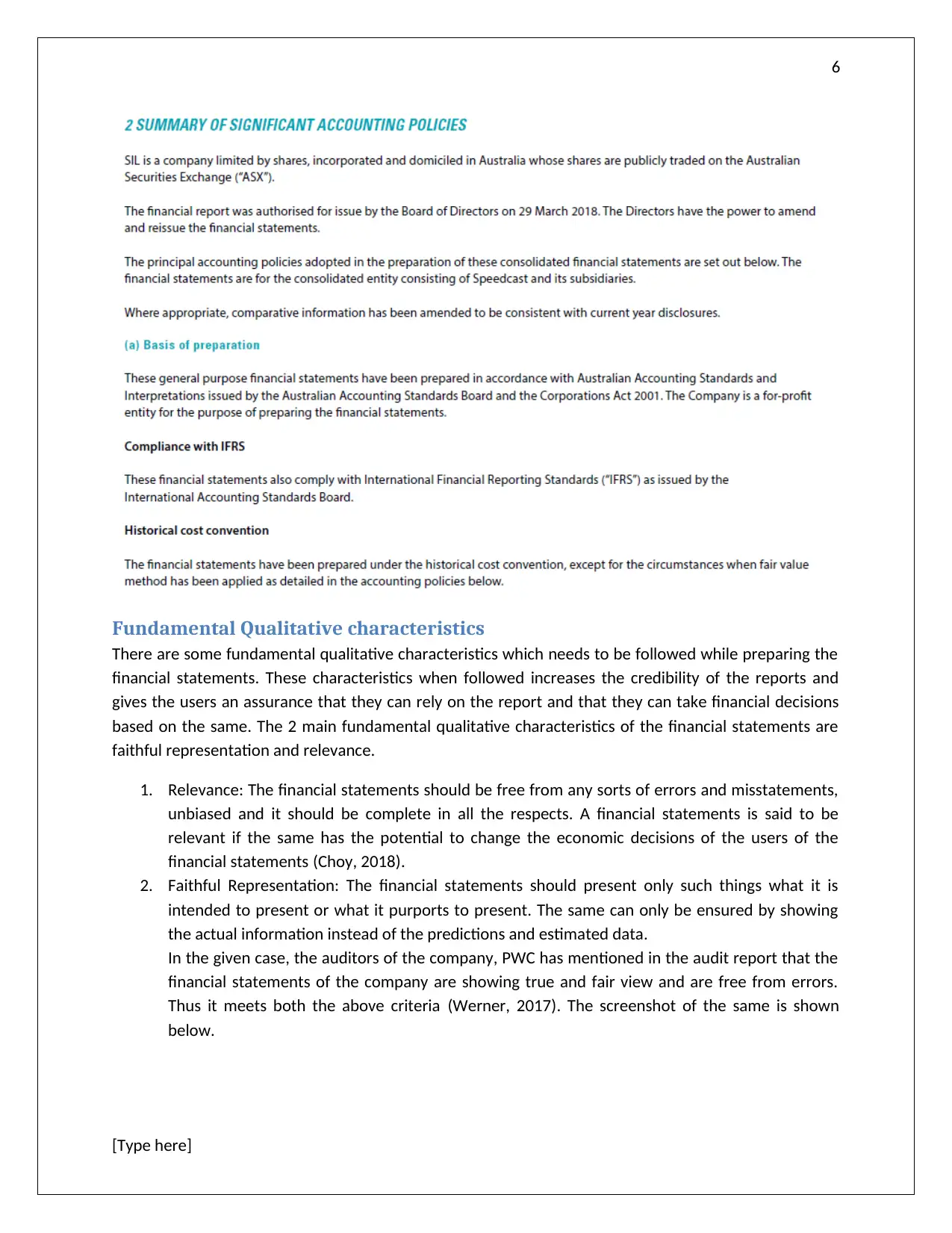

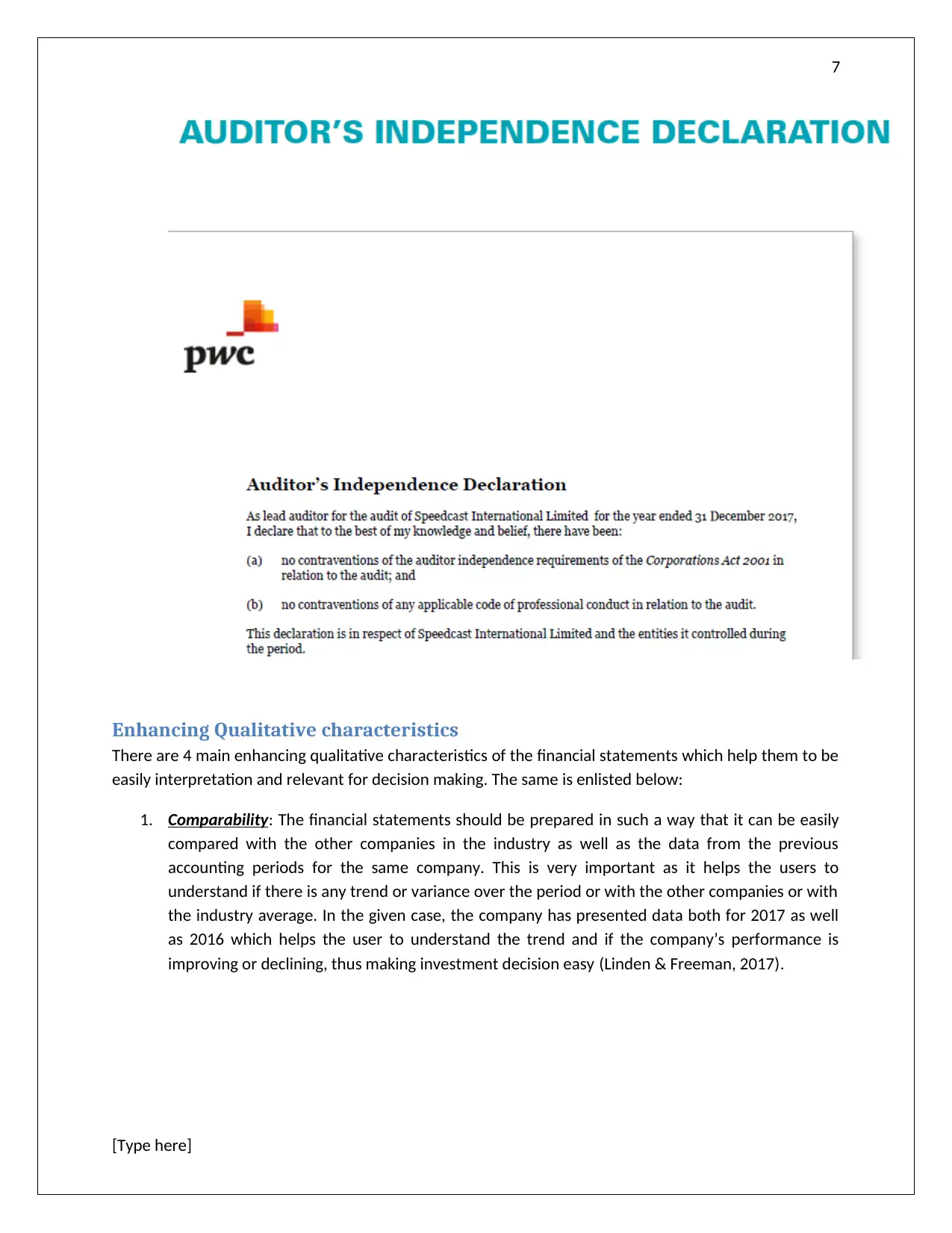

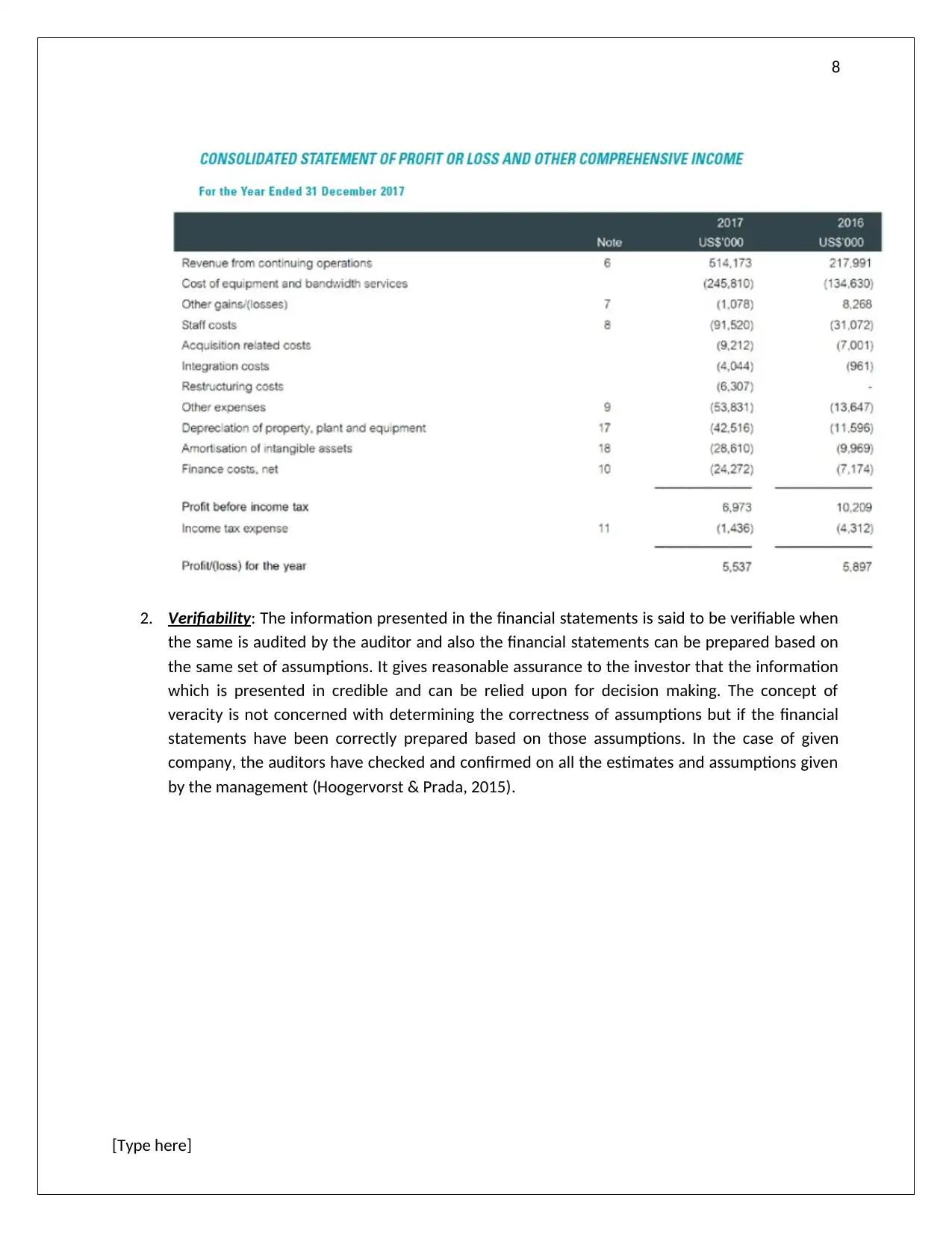

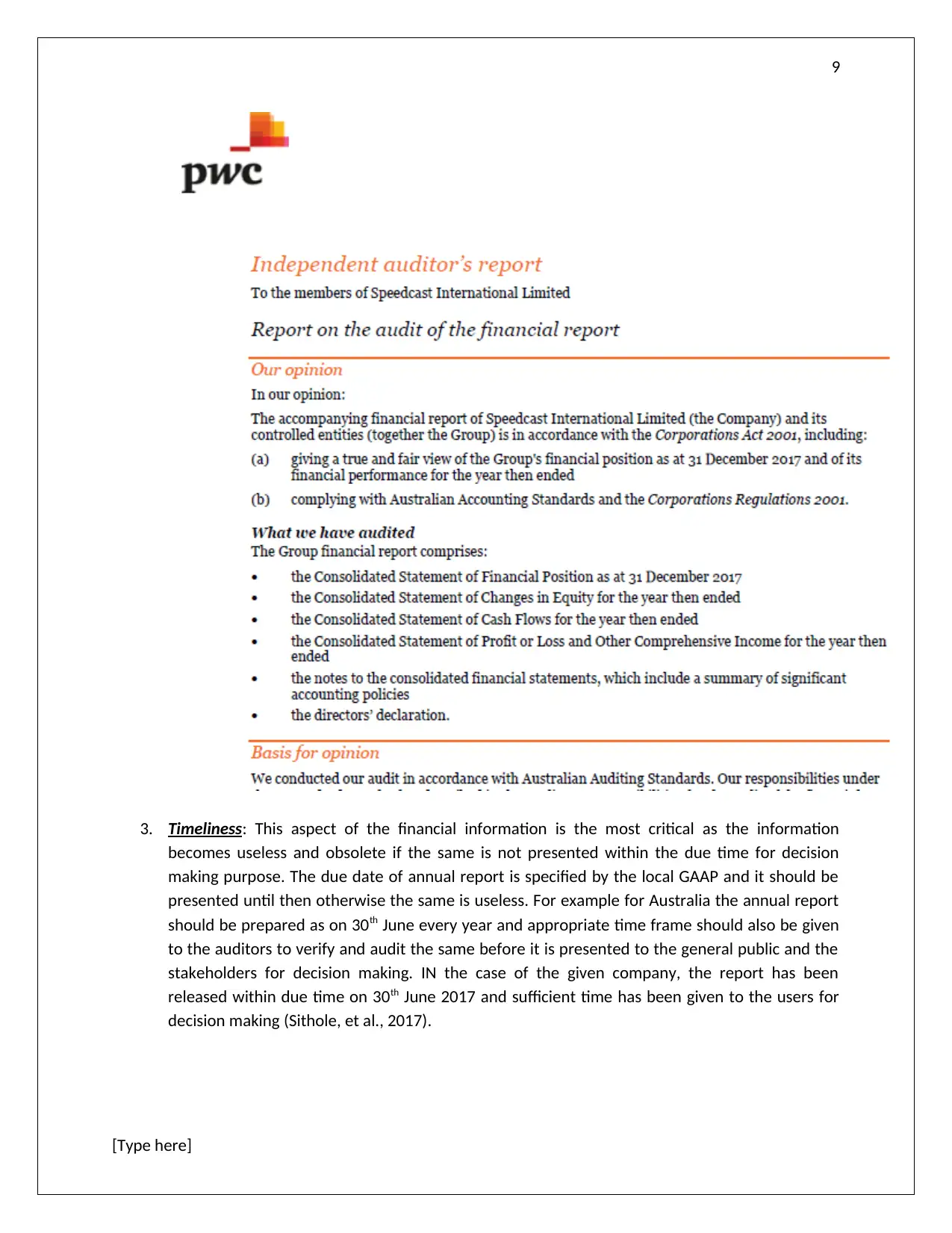

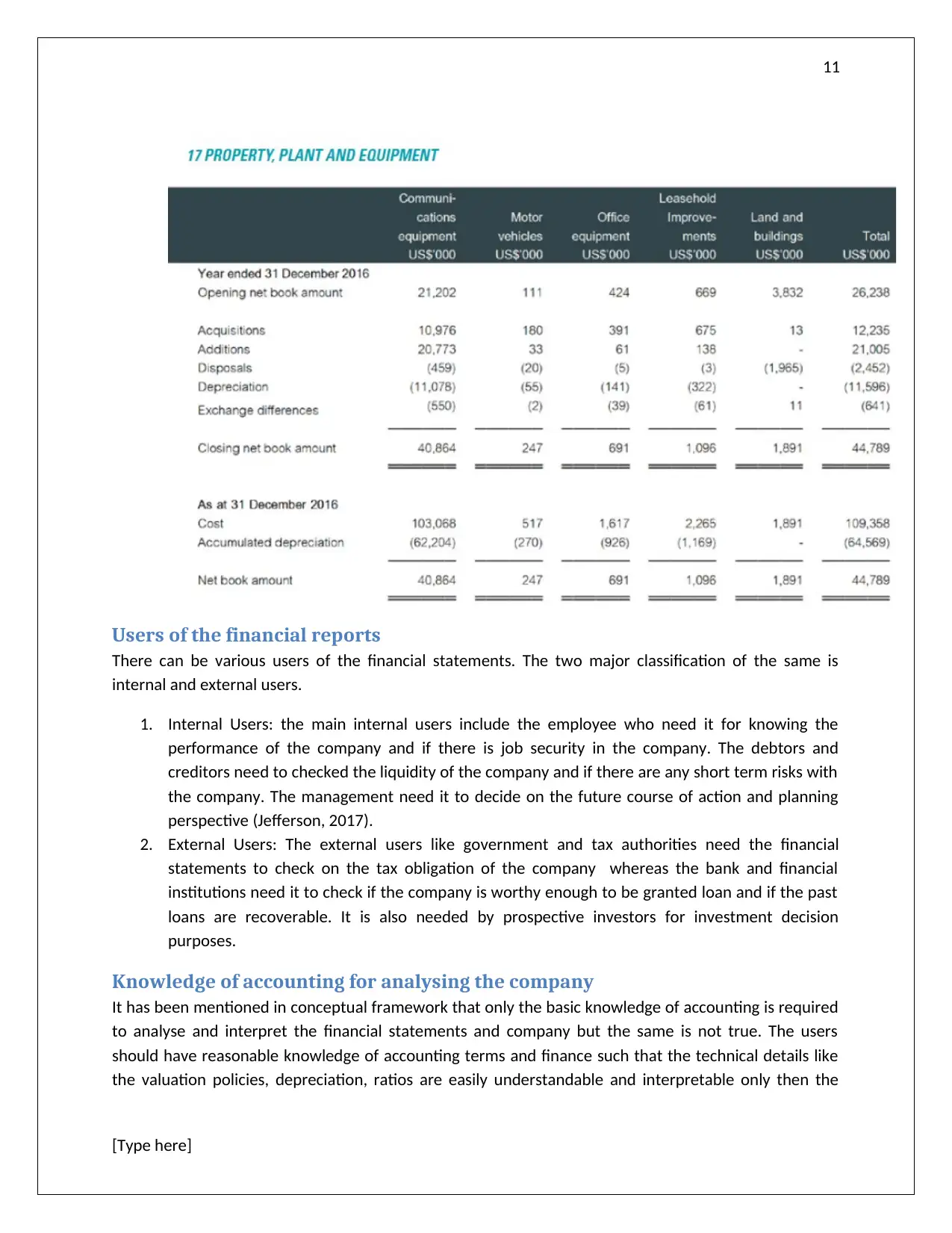

This report presents a financial analysis of SpeedCast, a communication satellite technology company. It examines the company's compliance with the measurement requirements of the conceptual framework, focusing on the application of accounting standards like AASB 9, AASB 15, AASB 17, and AASB 2. The analysis evaluates the company's adherence to fundamental and enhancing qualitative characteristics, including relevance, faithful representation, comparability, verifiability, timeliness, and understandability. The report assesses the usability of the financial statements for various users, such as investors and creditors, and discusses the required level of accounting knowledge for effective analysis. Finally, it concludes on whether SpeedCast meets the requirements of General Purpose Financial Reporting, supported by screenshots from the annual report and academic research, using Harvard referencing.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.