Strategic Performance Management System Report: Analysis

VerifiedAdded on 2021/06/14

|16

|3656

|48

Report

AI Summary

This report delves into the Strategic Performance Management System (SPMS), focusing on the implementation of the Balanced Scorecard (BSC) within multinational organizations. It explores the BSC's ability to translate strategy into action through strategic alignment and the cause-and-effect relationships within an organization, emphasizing both financial and non-financial perspectives. The report examines the BSC system's four key perspectives: financial, operational, consumer, and people, and how they contribute to organizational objectives. It further analyzes the implementation process, including the top-down and incremental approaches, and the importance of a clear strategic vision. Challenges faced during implementation, such as vague strategies, lack of common vocabulary, and difficulties in initial implementation and cascading to the individual level, are discussed along with corresponding recommendations. The report highlights the significance of financial and non-financial measures, consumer perspectives, internal business processes, and learning and growth perspectives in measuring employee performance. The overall objective is to provide insights into the effective use of SPMS and BSC for enhancing performance management, strategic alignment, and compensation strategies in multinational companies.

Running head: STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

Implementation of Strategic Performance Measurement Systems (SPMS)

Name of the University:

Name of the Student:

Authors Note:

Implementation of Strategic Performance Measurement Systems (SPMS)

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

Table of Contents

1. Introduction......................................................................................................................2

2. Balanced Scorecard System.............................................................................................3

3. Balanced Scorecard Implementation in Multinational Organizations.............................5

3.1. Strategy Destination..................................................................................................7

3.2. Perspectives and Measures.......................................................................................7

4. Challenges Faced and Likely Recommendations to Overcome Them............................9

5. Limitations of BSC........................................................................................................11

6. Conclusion.....................................................................................................................12

References..........................................................................................................................13

Table of Contents

1. Introduction......................................................................................................................2

2. Balanced Scorecard System.............................................................................................3

3. Balanced Scorecard Implementation in Multinational Organizations.............................5

3.1. Strategy Destination..................................................................................................7

3.2. Perspectives and Measures.......................................................................................7

4. Challenges Faced and Likely Recommendations to Overcome Them............................9

5. Limitations of BSC........................................................................................................11

6. Conclusion.....................................................................................................................12

References..........................................................................................................................13

2STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

1. Introduction

Certain major factors of Strategic Performance Measurement Systems (SPMS) and the

Balanced Scorecard (BSC) are capable to translate strategy within action such as strategic

alignment (Adams, Muir and Hoque 2014). This can determine the cause and effect association

present within organization conducts and through extension of several company’s sub-units.

Most importantly, certain distinct perspectives and activities with important KPIs are maintained

all through the financial and the non-financial aspects. Considering the same, it is also revealed

that balanced scorecard is an only aspect that affects organizational performance in case it is

associated with the intrinsic and extrinsic incentives of managers (Akbar, Pilcher and Perrin

2015). In order to attain a sustainable and competitive environment it is vital for the companies

to measure the ways in which multi-national companies. This offers these companies with a

proper view of companies’ ability within the recent business markets. Along with the same, for

attaining success within the dynamic surrounding it is vital for these organizations to get linked

with Strategic Performance Measurement Systems (SPMS) within organizational strategy.

The objective of the paper is to analyze the issues associated with the implementation of

Strategic Performance Measurement Systems (SPMS) that is balance scorecard in consideration

to performance management analysis along with compensation within multi-national companies.

Preparing a report in this subject will facilitate in evaluating different implications associated

with strategic alignment, management performance analysis along with compensation within the

multi-national companies.

1. Introduction

Certain major factors of Strategic Performance Measurement Systems (SPMS) and the

Balanced Scorecard (BSC) are capable to translate strategy within action such as strategic

alignment (Adams, Muir and Hoque 2014). This can determine the cause and effect association

present within organization conducts and through extension of several company’s sub-units.

Most importantly, certain distinct perspectives and activities with important KPIs are maintained

all through the financial and the non-financial aspects. Considering the same, it is also revealed

that balanced scorecard is an only aspect that affects organizational performance in case it is

associated with the intrinsic and extrinsic incentives of managers (Akbar, Pilcher and Perrin

2015). In order to attain a sustainable and competitive environment it is vital for the companies

to measure the ways in which multi-national companies. This offers these companies with a

proper view of companies’ ability within the recent business markets. Along with the same, for

attaining success within the dynamic surrounding it is vital for these organizations to get linked

with Strategic Performance Measurement Systems (SPMS) within organizational strategy.

The objective of the paper is to analyze the issues associated with the implementation of

Strategic Performance Measurement Systems (SPMS) that is balance scorecard in consideration

to performance management analysis along with compensation within multi-national companies.

Preparing a report in this subject will facilitate in evaluating different implications associated

with strategic alignment, management performance analysis along with compensation within the

multi-national companies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

2. Balanced Scorecard System

The balanced scorecard system is a strategic planning and reporting technique that

considers the company’s objectives and it is segmented among four equally vital perspectives

such as financial, operational, consumer and people (Garengo and Sharma 2014). Objectives of

the multi-national organizations are segmented into such perspectives that offer these companies

with options to maintain clear implementation path. The balanced scorecard system also has

strategy map in which the financial perspective stays at top and has certain objectives which

contributes to the bottom line. Another consumer perspective supports such objectives that

results in addressing consumer requirements that results in increased sales (Guenther, Endrikat

and Guenther 2016). If the balanced scorecard is in place with managing performance,

employees observe the ways in which job makes a difference to the multi-national organizations.

The balanced scorecard portion includes of lagging and leading metrics that the organization or

the departments they can be analyzed on to determine whether they are on the track. The balance

scorecard performance measurement metrics lays a foundation for clear performance

expectations along with the ambiguity elimination of ambiguity focused on employee priorities.

With a complete scorecard in place, the employees realize where to place their position

and can easily determine the areas within which the balance scorecard can result in the success of

the organizational strategy (Gutierrez et al. 2015). Employee performance evaluations along with

status reports are highly centered on the findings of the balanced scorecard that offers employees

structures and supervisors to focusing on coaching and evaluation. This also facilitates in

developing employees structure for coaching and analysis that keeps all the employees informed.

Relied on the analysis of the balance scorecard and strategy map, on Strategy facilitates these

multinational companies regardless of the budget and size in developing their comprehensive

2. Balanced Scorecard System

The balanced scorecard system is a strategic planning and reporting technique that

considers the company’s objectives and it is segmented among four equally vital perspectives

such as financial, operational, consumer and people (Garengo and Sharma 2014). Objectives of

the multi-national organizations are segmented into such perspectives that offer these companies

with options to maintain clear implementation path. The balanced scorecard system also has

strategy map in which the financial perspective stays at top and has certain objectives which

contributes to the bottom line. Another consumer perspective supports such objectives that

results in addressing consumer requirements that results in increased sales (Guenther, Endrikat

and Guenther 2016). If the balanced scorecard is in place with managing performance,

employees observe the ways in which job makes a difference to the multi-national organizations.

The balanced scorecard portion includes of lagging and leading metrics that the organization or

the departments they can be analyzed on to determine whether they are on the track. The balance

scorecard performance measurement metrics lays a foundation for clear performance

expectations along with the ambiguity elimination of ambiguity focused on employee priorities.

With a complete scorecard in place, the employees realize where to place their position

and can easily determine the areas within which the balance scorecard can result in the success of

the organizational strategy (Gutierrez et al. 2015). Employee performance evaluations along with

status reports are highly centered on the findings of the balanced scorecard that offers employees

structures and supervisors to focusing on coaching and evaluation. This also facilitates in

developing employees structure for coaching and analysis that keeps all the employees informed.

Relied on the analysis of the balance scorecard and strategy map, on Strategy facilitates these

multinational companies regardless of the budget and size in developing their comprehensive

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

plan within few weeks along with monitoring implementation all year long (Hartnell et al. 2016).

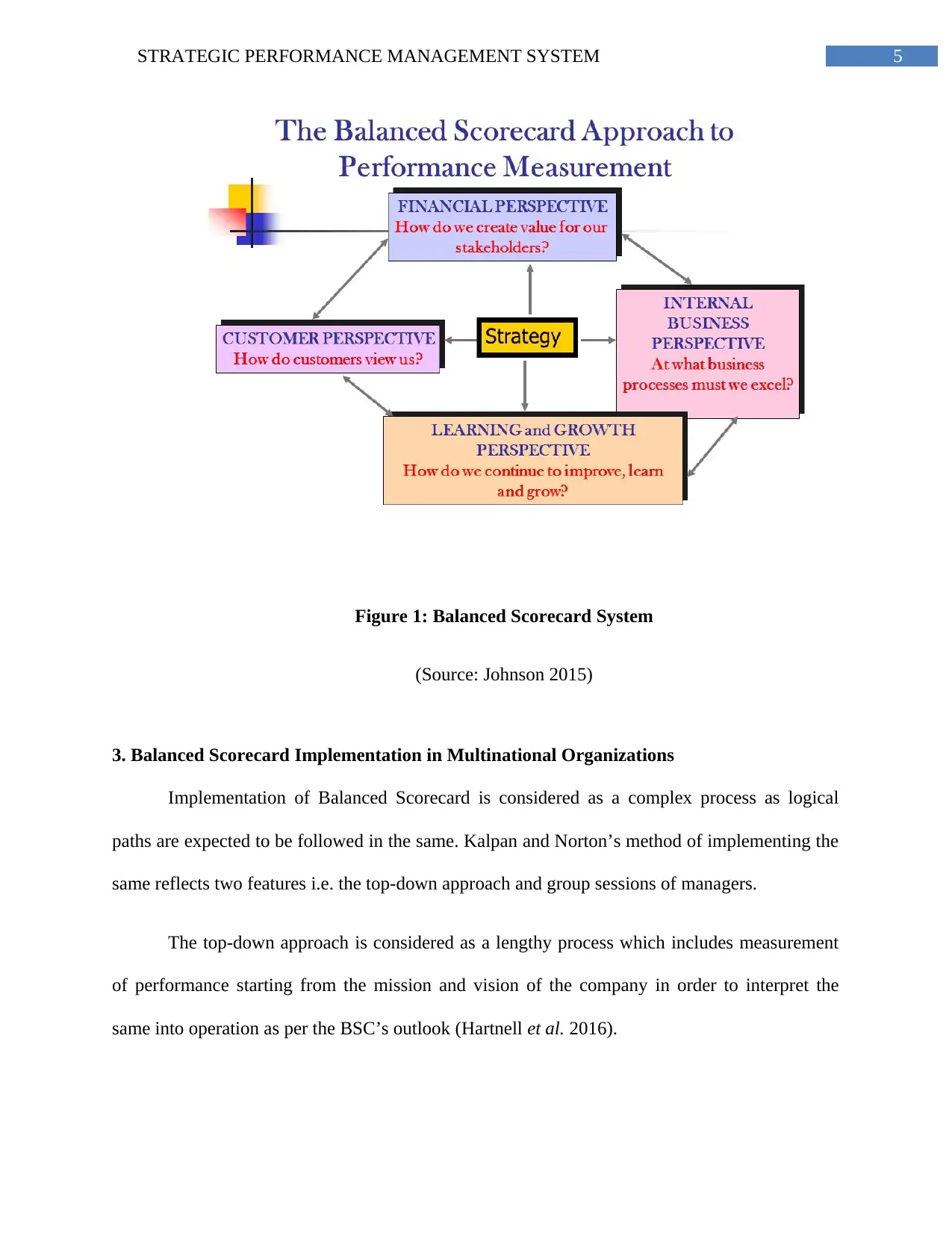

In measuring the performance of the employees within the multinational organizations four

perspectives of the balance scorecard is considered:

The internal business perspective: Manages must require to know whether the

multinational companies deals with consumer needs

The consumers perspective: Managers require focusing on the important internal

operations that facilitate them to deal with the needs of the consumers

The financial perspective: Companies ability to innovate, learn and innovate is directly

linked to its value as a company (Johnson 2015).

The learning and innovation perspective: Considering this aspect, within the

multinational organizations employees are trained in a way that such measures re

basically centered on the market share and profit. For public sector, balance scorecard is

employed in an organizational level.

plan within few weeks along with monitoring implementation all year long (Hartnell et al. 2016).

In measuring the performance of the employees within the multinational organizations four

perspectives of the balance scorecard is considered:

The internal business perspective: Manages must require to know whether the

multinational companies deals with consumer needs

The consumers perspective: Managers require focusing on the important internal

operations that facilitate them to deal with the needs of the consumers

The financial perspective: Companies ability to innovate, learn and innovate is directly

linked to its value as a company (Johnson 2015).

The learning and innovation perspective: Considering this aspect, within the

multinational organizations employees are trained in a way that such measures re

basically centered on the market share and profit. For public sector, balance scorecard is

employed in an organizational level.

5STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

Figure 1: Balanced Scorecard System

(Source: Johnson 2015)

3. Balanced Scorecard Implementation in Multinational Organizations

Implementation of Balanced Scorecard is considered as a complex process as logical

paths are expected to be followed in the same. Kalpan and Norton’s method of implementing the

same reflects two features i.e. the top-down approach and group sessions of managers.

The top-down approach is considered as a lengthy process which includes measurement

of performance starting from the mission and vision of the company in order to interpret the

same into operation as per the BSC’s outlook (Hartnell et al. 2016).

Figure 1: Balanced Scorecard System

(Source: Johnson 2015)

3. Balanced Scorecard Implementation in Multinational Organizations

Implementation of Balanced Scorecard is considered as a complex process as logical

paths are expected to be followed in the same. Kalpan and Norton’s method of implementing the

same reflects two features i.e. the top-down approach and group sessions of managers.

The top-down approach is considered as a lengthy process which includes measurement

of performance starting from the mission and vision of the company in order to interpret the

same into operation as per the BSC’s outlook (Hartnell et al. 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

Hence, this approach has been mainly associated with the large enterprises as the studies

made by Hudson stated the issue of implementing the same on SMEs could be difficult. He

mentioned that the identification of the critical success factor and the measuring the key

performance of various perspective happens parallelly. Henceforth, a new approach has been

proposed that was defined as “incremental”. The major strategic objective of the same was

“name, act, use, learn” cycle, but this also came to a halt as it required an actual validation of the

strategic vision.

It has been observed that in majority of the SMEs, the roles of various person overlap

which creates informal management system and the ideals of entrepreneurs are not formally

expressed. Therefore, the approach crashes with the cultural framework of the organization.

Hence, a circular approach has been implemented for such organization which includes

four main steps which measures the operation of every individual on a regular basis. In this

method, those under control are gauged. In the observation, it has been noted that lack of vision

is grater in SMEs against that of large companies.

The first step encompasses the performances that are being controlled, including

individual dashboard as well as implicit management dashboard. While observing the controlled

performances, the phenomena in which those are controlled is unveiled through implicit strategy

map. The third step includes the identifying the critical phenomena through desired strategy map.

Therefore, after designing the new performance measurement system as well as the management

system, the key performance measures are taken up.

Hence, this approach has been mainly associated with the large enterprises as the studies

made by Hudson stated the issue of implementing the same on SMEs could be difficult. He

mentioned that the identification of the critical success factor and the measuring the key

performance of various perspective happens parallelly. Henceforth, a new approach has been

proposed that was defined as “incremental”. The major strategic objective of the same was

“name, act, use, learn” cycle, but this also came to a halt as it required an actual validation of the

strategic vision.

It has been observed that in majority of the SMEs, the roles of various person overlap

which creates informal management system and the ideals of entrepreneurs are not formally

expressed. Therefore, the approach crashes with the cultural framework of the organization.

Hence, a circular approach has been implemented for such organization which includes

four main steps which measures the operation of every individual on a regular basis. In this

method, those under control are gauged. In the observation, it has been noted that lack of vision

is grater in SMEs against that of large companies.

The first step encompasses the performances that are being controlled, including

individual dashboard as well as implicit management dashboard. While observing the controlled

performances, the phenomena in which those are controlled is unveiled through implicit strategy

map. The third step includes the identifying the critical phenomena through desired strategy map.

Therefore, after designing the new performance measurement system as well as the management

system, the key performance measures are taken up.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

3.1. Strategy Destination

Strategic performance management systems are deemed to be focused in three

perspectives that make them applicable within the multinational organizations for attaining high

competitive advantages. These perspectives are explained under:

They encompass the financial measures that gather the short term consequences of

manager decisions concerned with the problems that include revenue growth, asset

utilization along with cash flows (Valmohammadi and Roshanzamir 2015).

The balanced scorecard has supplement financial measures with non-financial measures

which signify operational achievements that are likely to drive the organizations financial

performance.

The balanced scorecard is designed to fulfill multiple purposes from simple cost

determination to difficult value creation with an emphasis on implementation of the

strategy (Valmohammadi and Roshanzamir 2015).

3.2. Perspectives and Measures

There are performance management systems that is attaining increased popularity in the

multinational organizations is focused on relevant perspectives and characteristics related with

suitable implementation of balanced scorecard approach within the organizations (Silvi,

Bartolini, Raffoni and Visani 2015). The perspectives of the managers in multinational

companies can be observed as attaining increased interest within the management accounting.

The balanced scorecard measures that are employed by the multinational organizations are

explained below:

3.1. Strategy Destination

Strategic performance management systems are deemed to be focused in three

perspectives that make them applicable within the multinational organizations for attaining high

competitive advantages. These perspectives are explained under:

They encompass the financial measures that gather the short term consequences of

manager decisions concerned with the problems that include revenue growth, asset

utilization along with cash flows (Valmohammadi and Roshanzamir 2015).

The balanced scorecard has supplement financial measures with non-financial measures

which signify operational achievements that are likely to drive the organizations financial

performance.

The balanced scorecard is designed to fulfill multiple purposes from simple cost

determination to difficult value creation with an emphasis on implementation of the

strategy (Valmohammadi and Roshanzamir 2015).

3.2. Perspectives and Measures

There are performance management systems that is attaining increased popularity in the

multinational organizations is focused on relevant perspectives and characteristics related with

suitable implementation of balanced scorecard approach within the organizations (Silvi,

Bartolini, Raffoni and Visani 2015). The perspectives of the managers in multinational

companies can be observed as attaining increased interest within the management accounting.

The balanced scorecard measures that are employed by the multinational organizations are

explained below:

8STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

Financial perspectives: The financial perspective or measure deals with the concerns

through which the multinational companies can generate economic growth in the

shareholder value along with measuring the profitability aspect of the strategy (Silvi,

Bartolini, Raffoni and Visani 2015).

Consumer Perspective: Typical measures related with consumer value include the

market share, consumer retention and acquisition along with profitability and satisfaction

of consumers. Considering the same consumer perspective explains the value proposal

that will have applied by the consumers in addressing their demands that can facilitate in

generating more sales to highly desired consumer groups (Upadhaya, Munir and Blount

2014).

Internal business process perspective: This perspective centres on all the related

activities along with the needed major processes of the organization in order to attain

success at offering the value anticipated by the consumers both productively and

effectively (Upadhaya, Munir and Blount 2014). This perspective includes measures

related to procedures of companies for developing and turns out to be popular.

Learning and growth perspective: The measures related with this perspective is

focused on introducing continuous improvement measures related with the product

production, processes along with the consumer training (Silvi, Bartolini, Raffoni and

Visani 2015). The major focus of such perspectives was laid on investing for the future

like the new equipments along with research and development related with employee

training. These measures also employ necessary employee skills along with

implementing incentive databases for improvement of employee performances as well as

organizational profit.

Financial perspectives: The financial perspective or measure deals with the concerns

through which the multinational companies can generate economic growth in the

shareholder value along with measuring the profitability aspect of the strategy (Silvi,

Bartolini, Raffoni and Visani 2015).

Consumer Perspective: Typical measures related with consumer value include the

market share, consumer retention and acquisition along with profitability and satisfaction

of consumers. Considering the same consumer perspective explains the value proposal

that will have applied by the consumers in addressing their demands that can facilitate in

generating more sales to highly desired consumer groups (Upadhaya, Munir and Blount

2014).

Internal business process perspective: This perspective centres on all the related

activities along with the needed major processes of the organization in order to attain

success at offering the value anticipated by the consumers both productively and

effectively (Upadhaya, Munir and Blount 2014). This perspective includes measures

related to procedures of companies for developing and turns out to be popular.

Learning and growth perspective: The measures related with this perspective is

focused on introducing continuous improvement measures related with the product

production, processes along with the consumer training (Silvi, Bartolini, Raffoni and

Visani 2015). The major focus of such perspectives was laid on investing for the future

like the new equipments along with research and development related with employee

training. These measures also employ necessary employee skills along with

implementing incentive databases for improvement of employee performances as well as

organizational profit.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

4. Challenges Faced and Likely Recommendations to Overcome Them

Several challenges are faced by the multinational organizations and the likely

recommendations are offered to the companies in order to deal with such issues in

implementation of suitable performance management systems (Taylor and Taylor 2014). These

challenges along with related recommendations are explained under:

Vague Strategy: Certain strategies are observed to be of high level along with future

looking with aspirations and ideals (Silvi, Bartolini, Raffoni and Visani 2015). Or

maintaining an effective business structure there is an increased risk of diluting such

capability for transformation is into an efficient balanced scorecard. The best

recommendation in dealing with such condition, recommendations are provided to refine

and revisit the strategy with the owners along with attaining clarified directions based on

the business aspirations. For better performance management the employees must be

aware of the statements of the desired multinational organizations along with state of

their planning horizon (Upadhaya, Munir and Blount 2014).

Lack of Common Vocabulary: It is deemed extremely common to have distinct

definitions related with strategy aspects all through the multinational companies (Searcy

2016). The significance of the mission, vision, goals, and objectives along with other

aspects requires to be communicated to the employees. Such aspects are also to be

communicated to all the stakeholders all across the organization. Such recommendations

are to be followed by the multinational companies all across the world for the reason that

lack of common vocabulary might result in the risk of misalignment that can further get

increased all across the company (Ralston, Blackhurst, Cantor and Crum 2015). The best

recommendation to deal with such situation is to develop the destinations of such

4. Challenges Faced and Likely Recommendations to Overcome Them

Several challenges are faced by the multinational organizations and the likely

recommendations are offered to the companies in order to deal with such issues in

implementation of suitable performance management systems (Taylor and Taylor 2014). These

challenges along with related recommendations are explained under:

Vague Strategy: Certain strategies are observed to be of high level along with future

looking with aspirations and ideals (Silvi, Bartolini, Raffoni and Visani 2015). Or

maintaining an effective business structure there is an increased risk of diluting such

capability for transformation is into an efficient balanced scorecard. The best

recommendation in dealing with such condition, recommendations are provided to refine

and revisit the strategy with the owners along with attaining clarified directions based on

the business aspirations. For better performance management the employees must be

aware of the statements of the desired multinational organizations along with state of

their planning horizon (Upadhaya, Munir and Blount 2014).

Lack of Common Vocabulary: It is deemed extremely common to have distinct

definitions related with strategy aspects all through the multinational companies (Searcy

2016). The significance of the mission, vision, goals, and objectives along with other

aspects requires to be communicated to the employees. Such aspects are also to be

communicated to all the stakeholders all across the organization. Such recommendations

are to be followed by the multinational companies all across the world for the reason that

lack of common vocabulary might result in the risk of misalignment that can further get

increased all across the company (Ralston, Blackhurst, Cantor and Crum 2015). The best

recommendation to deal with such situation is to develop the destinations of such

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

common vocabulary, publish it along with remaining participants regarding the

definitions at the starting point of the planning meetings.

Difficulty in initial implementation: There is an increased tendency to get confused

with the technicalities and details related with the balanced scorecard (Rajnoha, Stefko,

Merková and Dobrovic 2016). The strategic maps, themes along with cascading to

individual level might result in loss of confusion regarding the initial approach. The best

recommendation in such scenario is to phase the approach through starting with

articulating balanced scorecard all through four perspectives in preparing the strategy

map (Singh, Darwish and Potočnik 2016). This can offer a sense of clarity for action plan

that must be interacted all through the organization.

Cascading to individual level acts as challenge: This challenge is faced regarding the

engagement level of the employees within the multinational companies. This entails

attaining their agreement along with commitment to set targets. In case that engagement

is not attained the BSC in individual level will be nothing other than documentations

exercise at the end of a reporting period (Pollanen, Abdel-Maksoud, Elbanna and

Mahama 2017). Annoyer challenge is that the behavior will never get changed. The

suitable recommendation for this to get involved in developing business scorecard

objectives and targets and have them gets participated within setting targets.

Getting lost in tracking mechanics: The lack of automation in order to record and

rolling up leads to implementation that might consider derail the team within the

mechanics of recording the targets and actual. This will be computed at the time the team

attempts to developed formulas to roll up win an overall result by the department or

objectives all through the four perspectives of balanced scorecard (Piotrowicz and

common vocabulary, publish it along with remaining participants regarding the

definitions at the starting point of the planning meetings.

Difficulty in initial implementation: There is an increased tendency to get confused

with the technicalities and details related with the balanced scorecard (Rajnoha, Stefko,

Merková and Dobrovic 2016). The strategic maps, themes along with cascading to

individual level might result in loss of confusion regarding the initial approach. The best

recommendation in such scenario is to phase the approach through starting with

articulating balanced scorecard all through four perspectives in preparing the strategy

map (Singh, Darwish and Potočnik 2016). This can offer a sense of clarity for action plan

that must be interacted all through the organization.

Cascading to individual level acts as challenge: This challenge is faced regarding the

engagement level of the employees within the multinational companies. This entails

attaining their agreement along with commitment to set targets. In case that engagement

is not attained the BSC in individual level will be nothing other than documentations

exercise at the end of a reporting period (Pollanen, Abdel-Maksoud, Elbanna and

Mahama 2017). Annoyer challenge is that the behavior will never get changed. The

suitable recommendation for this to get involved in developing business scorecard

objectives and targets and have them gets participated within setting targets.

Getting lost in tracking mechanics: The lack of automation in order to record and

rolling up leads to implementation that might consider derail the team within the

mechanics of recording the targets and actual. This will be computed at the time the team

attempts to developed formulas to roll up win an overall result by the department or

objectives all through the four perspectives of balanced scorecard (Piotrowicz and

11STRATEGIC PERFORMANCE MANAGEMENT SYSTEM

Cuthbertson 2015). The best recommendation to deal with such challenges is to interact

with the employees belonging to multinational organizations regarding the objectives of

balanced scorecard implementation. In such scenario, the objective of these organizations

will be to employ the balanced scorecard as a navigation compass for steering the

organization that can result in high performing organizations.

5. Limitations of BSC

Despite of having several useful implications in the performance management within

multinational organizations, there are certain limitations of this performance measurement

systems approach. This must be taken into consideration by these organizations so that they are

able to conduct performance evaluation in consideration to compensation (Keong Choong 2014).

The limitations of balance scorecard system are explained under:

It might be an overwhelming structure it cannot be precisely copied from instances. It

needs strong leadership in order to be highly successful. Balance scorecard cannot be

implemented efficiently as new leadership is not convinced that this reformate

measurement system is a viable option

Time as well as financial cost investment: Balanced scorecard systems needs a huge

investment and the multinational organizations are required to manage its systems in

active manner and constantly that comes with financial costs and time (Klovienė and

Speziale 2014). Moreover, all the employees need to understand the ways in which such

system works which might result in increased training costs.

Lack of external focus-Balanced scorecard might provide multinational organizations

with wide internal focus and does not offer a clear view of overall picture. For such

Cuthbertson 2015). The best recommendation to deal with such challenges is to interact

with the employees belonging to multinational organizations regarding the objectives of

balanced scorecard implementation. In such scenario, the objective of these organizations

will be to employ the balanced scorecard as a navigation compass for steering the

organization that can result in high performing organizations.

5. Limitations of BSC

Despite of having several useful implications in the performance management within

multinational organizations, there are certain limitations of this performance measurement

systems approach. This must be taken into consideration by these organizations so that they are

able to conduct performance evaluation in consideration to compensation (Keong Choong 2014).

The limitations of balance scorecard system are explained under:

It might be an overwhelming structure it cannot be precisely copied from instances. It

needs strong leadership in order to be highly successful. Balance scorecard cannot be

implemented efficiently as new leadership is not convinced that this reformate

measurement system is a viable option

Time as well as financial cost investment: Balanced scorecard systems needs a huge

investment and the multinational organizations are required to manage its systems in

active manner and constantly that comes with financial costs and time (Klovienė and

Speziale 2014). Moreover, all the employees need to understand the ways in which such

system works which might result in increased training costs.

Lack of external focus-Balanced scorecard might provide multinational organizations

with wide internal focus and does not offer a clear view of overall picture. For such

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.