Comparative Financial Analysis: Sports Direct & JD Sports (2015-2016)

VerifiedAdded on 2020/09/08

|20

|4323

|67

Report

AI Summary

This report presents a detailed financial analysis comparing Sports Direct International PLC and JD Sports Fashion PLC for the years 2015 and 2016. The analysis focuses on key financial ratios, including current ratio, quick ratio, gross profit margin, operating profit margin, net profit margin, gearing ratio, earnings per share, return on capital employed, average inventory turnover period, and dividend payout ratio. The report evaluates the performance, investment potential, and financial position of both firms, offering insights into their profitability, financial health, and efficiency. Graphical representations are used to illustrate the trends and variations in the financial ratios. Recommendations are provided for improving financial performance, and the limitations of using financial ratios for interpretation are also discussed. The report also briefly touches upon investment appraisal techniques and their limitations in long-term decision-making.

Managerial Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A Analysing the financial ratios for 2015 and 2016...............................................................1

B Determining the performance, investment potential and financial position of both firms. 3

C Recommending ways to improve the financial performance of business........................12

D Evaluating the limitations of financial ratios to interpret firm performance....................12

QUESTION 2.................................................................................................................................13

A Application of investment appraisal techniques to advise senior manager......................13

B Evaluating the limitations over investment appraisal techniques for long term decision

making..................................................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A Analysing the financial ratios for 2015 and 2016...............................................................1

B Determining the performance, investment potential and financial position of both firms. 3

C Recommending ways to improve the financial performance of business........................12

D Evaluating the limitations of financial ratios to interpret firm performance....................12

QUESTION 2.................................................................................................................................13

A Application of investment appraisal techniques to advise senior manager......................13

B Evaluating the limitations over investment appraisal techniques for long term decision

making..................................................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

To develop the operational efficiency of business, there is essential requirement of having

adequate amount of funds. In order to meet various business needs such as expansion, sales,

purchase or investment, it is necessary that the business must have financial strength which in

turn is helpful for making adequate growth of business. In the present assessments, there has

been analysis based on the two sports industries: Sport Direct International PLC and JD Sports

Fashion PLC. Therefore, the managers of these organisations will be suggested to make

necessary improvements in their operational activities as to enhance the financial strength. The

report will also evaluate various investment appraisals which in turn have some limitations and

necessity in the business operations.

QUESTION 1

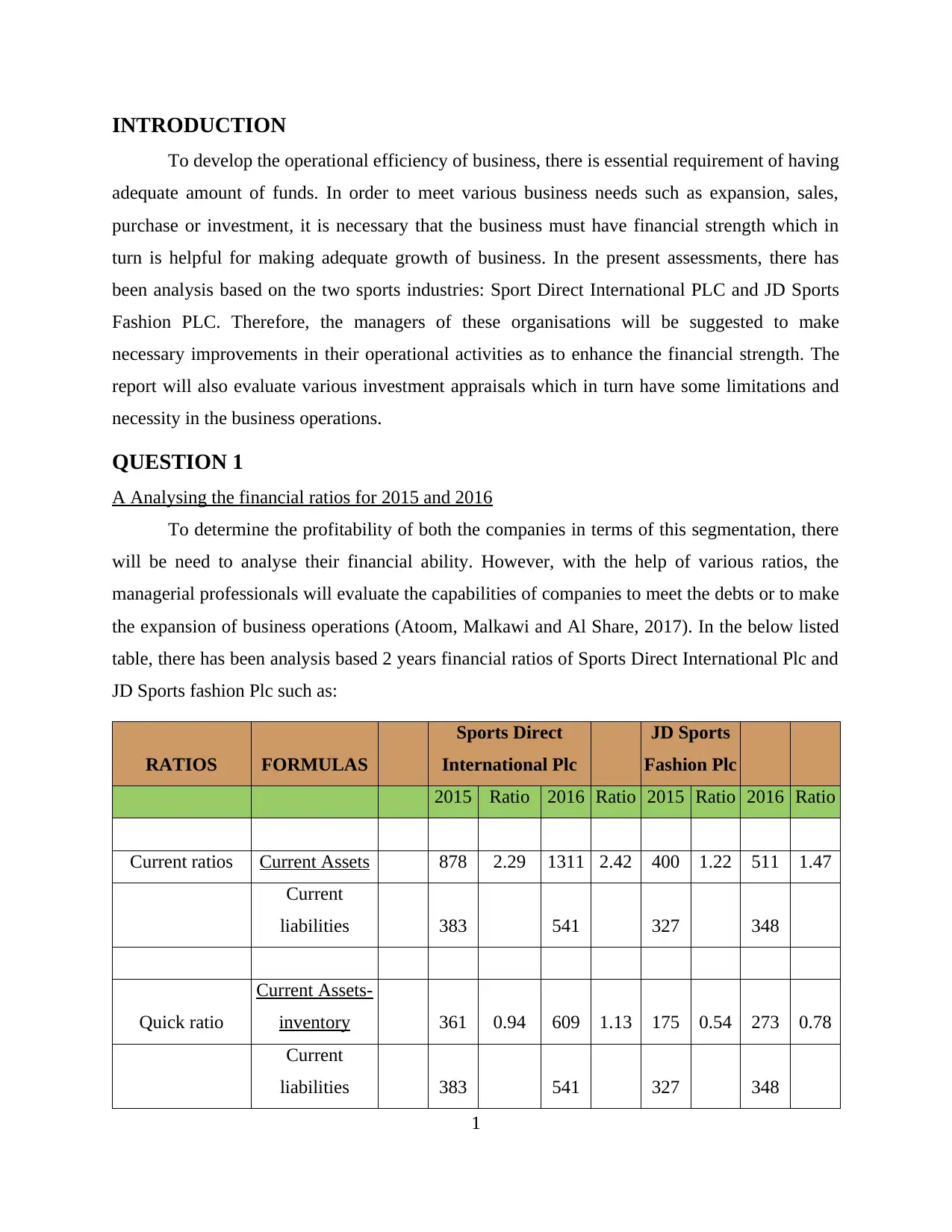

A Analysing the financial ratios for 2015 and 2016

To determine the profitability of both the companies in terms of this segmentation, there

will be need to analyse their financial ability. However, with the help of various ratios, the

managerial professionals will evaluate the capabilities of companies to meet the debts or to make

the expansion of business operations (Atoom, Malkawi and Al Share, 2017). In the below listed

table, there has been analysis based 2 years financial ratios of Sports Direct International Plc and

JD Sports fashion Plc such as:

RATIOS FORMULAS

Sports Direct

International Plc

JD Sports

Fashion Plc

2015 Ratio 2016 Ratio 2015 Ratio 2016 Ratio

Current ratios Current Assets 878 2.29 1311 2.42 400 1.22 511 1.47

Current

liabilities 383 541 327 348

Quick ratio

Current Assets-

inventory 361 0.94 609 1.13 175 0.54 273 0.78

Current

liabilities 383 541 327 348

1

To develop the operational efficiency of business, there is essential requirement of having

adequate amount of funds. In order to meet various business needs such as expansion, sales,

purchase or investment, it is necessary that the business must have financial strength which in

turn is helpful for making adequate growth of business. In the present assessments, there has

been analysis based on the two sports industries: Sport Direct International PLC and JD Sports

Fashion PLC. Therefore, the managers of these organisations will be suggested to make

necessary improvements in their operational activities as to enhance the financial strength. The

report will also evaluate various investment appraisals which in turn have some limitations and

necessity in the business operations.

QUESTION 1

A Analysing the financial ratios for 2015 and 2016

To determine the profitability of both the companies in terms of this segmentation, there

will be need to analyse their financial ability. However, with the help of various ratios, the

managerial professionals will evaluate the capabilities of companies to meet the debts or to make

the expansion of business operations (Atoom, Malkawi and Al Share, 2017). In the below listed

table, there has been analysis based 2 years financial ratios of Sports Direct International Plc and

JD Sports fashion Plc such as:

RATIOS FORMULAS

Sports Direct

International Plc

JD Sports

Fashion Plc

2015 Ratio 2016 Ratio 2015 Ratio 2016 Ratio

Current ratios Current Assets 878 2.29 1311 2.42 400 1.22 511 1.47

Current

liabilities 383 541 327 348

Quick ratio

Current Assets-

inventory 361 0.94 609 1.13 175 0.54 273 0.78

Current

liabilities 383 541 327 348

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

GP Margin Gross profit *100 1241 43.81% 1285

44.25

% 740

48.62

% 884

48.52

%

net sales

revenue 2833 2904 1522 1822

Operating profit

ratio operating profit *100 287 10.13% 212

7.30

% 92

6.04

% 132

7.24

%

net sales

revenue 2833 2904 1522 1822

Net Profit ratio Net profit *100 240 8.47% 277

9.54

% 53

3.48

% 98

4.36

%

net sales

revenue 2833 2904 1522 1822

Gearing ratio

Long term-

liabilities *100 137 9.85% 333

18.31

% 43

12.11

% 42

9.48

%

Capital

employed 1391 1819 355 443

Earnings per

share

net income-

preferred

dividends 0.39 0.46 0.05 0.1

Weighted

average shares

o/s

Return on capital

employed EBIT 396 0.28 466 0.26 138 0.39 182 0.41

2

44.25

% 740

48.62

% 884

48.52

%

net sales

revenue 2833 2904 1522 1822

Operating profit

ratio operating profit *100 287 10.13% 212

7.30

% 92

6.04

% 132

7.24

%

net sales

revenue 2833 2904 1522 1822

Net Profit ratio Net profit *100 240 8.47% 277

9.54

% 53

3.48

% 98

4.36

%

net sales

revenue 2833 2904 1522 1822

Gearing ratio

Long term-

liabilities *100 137 9.85% 333

18.31

% 43

12.11

% 42

9.48

%

Capital

employed 1391 1819 355 443

Earnings per

share

net income-

preferred

dividends 0.39 0.46 0.05 0.1

Weighted

average shares

o/s

Return on capital

employed EBIT 396 0.28 466 0.26 138 0.39 182 0.41

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Capital

employed 1391 1819 355 443

Average

inventory

turnover period

Cost of goods

sold 1592 1.93 1620 1.87 783 2.62 937 2.72

Average

inventories 823.5 868 298.5 344

Dividend pay-out

ratio total dividends 0 0 0 0 10 0.19 10 0.10

net income 240 277 53 98

B Determining the performance, investment potential and financial position of both firms

By considering the financial analysis of both the corporations, there will be discussion

based on the profitability, financial ability and the efficiency of these organisations. Therefore, it

will be helpful for stakeholders to analyse the profitability of these companies in the long run and

the ability to meet the debts (Liang and et.al., 2016). There will be debate on various ratios with

the help of graphical presentation that will be beneficial in analysing profitability of the given

companies. The difference in the financials can be analysed as:

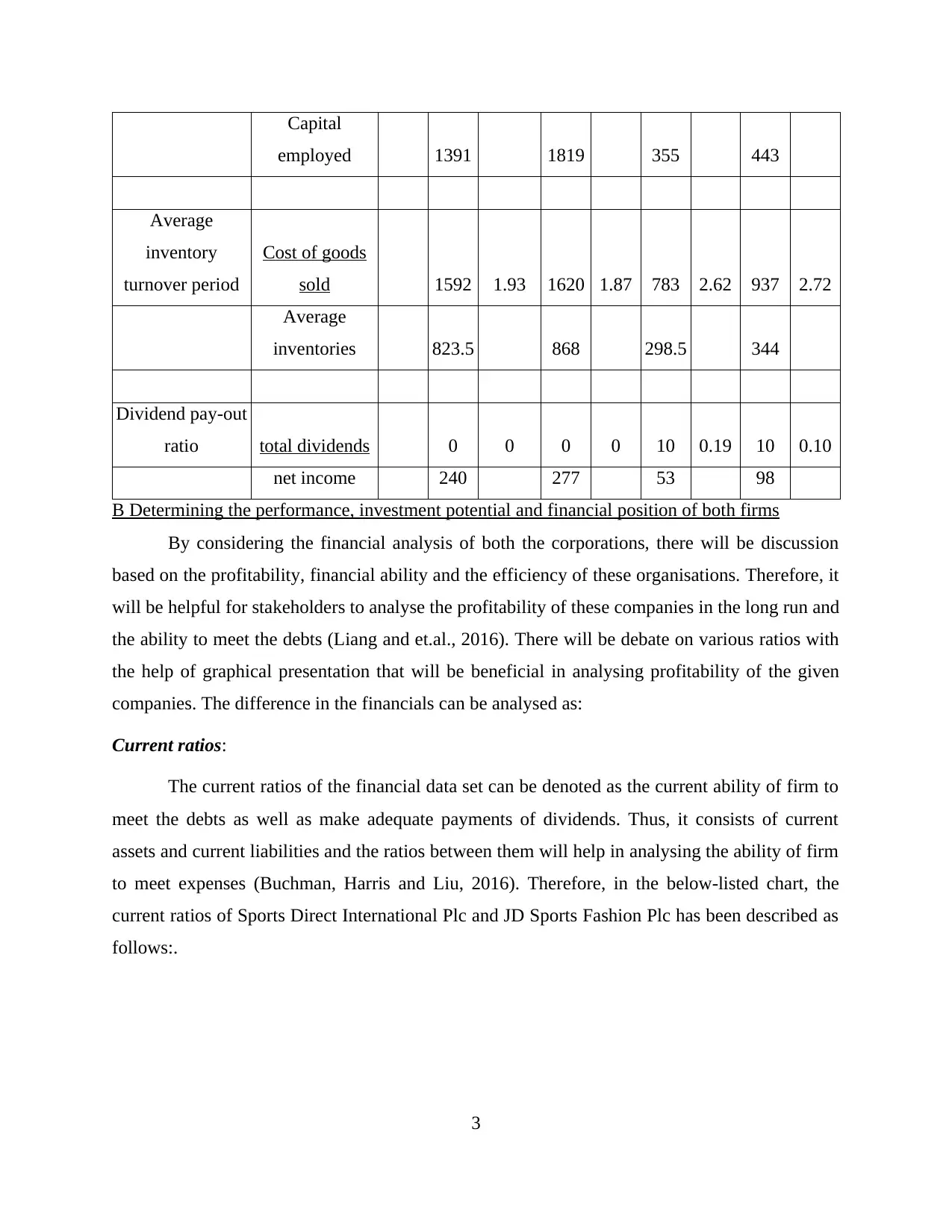

Current ratios:

The current ratios of the financial data set can be denoted as the current ability of firm to

meet the debts as well as make adequate payments of dividends. Thus, it consists of current

assets and current liabilities and the ratios between them will help in analysing the ability of firm

to meet expenses (Buchman, Harris and Liu, 2016). Therefore, in the below-listed chart, the

current ratios of Sports Direct International Plc and JD Sports Fashion Plc has been described as

follows:.

3

employed 1391 1819 355 443

Average

inventory

turnover period

Cost of goods

sold 1592 1.93 1620 1.87 783 2.62 937 2.72

Average

inventories 823.5 868 298.5 344

Dividend pay-out

ratio total dividends 0 0 0 0 10 0.19 10 0.10

net income 240 277 53 98

B Determining the performance, investment potential and financial position of both firms

By considering the financial analysis of both the corporations, there will be discussion

based on the profitability, financial ability and the efficiency of these organisations. Therefore, it

will be helpful for stakeholders to analyse the profitability of these companies in the long run and

the ability to meet the debts (Liang and et.al., 2016). There will be debate on various ratios with

the help of graphical presentation that will be beneficial in analysing profitability of the given

companies. The difference in the financials can be analysed as:

Current ratios:

The current ratios of the financial data set can be denoted as the current ability of firm to

meet the debts as well as make adequate payments of dividends. Thus, it consists of current

assets and current liabilities and the ratios between them will help in analysing the ability of firm

to meet expenses (Buchman, Harris and Liu, 2016). Therefore, in the below-listed chart, the

current ratios of Sports Direct International Plc and JD Sports Fashion Plc has been described as

follows:.

3

Sports Direct Internationals Plc JD Sports Fashion Plc

0.00

0.50

1.00

1.50

2.00

2.50

Current ratios

By considering the chart, it can be said that Sports Direct International plc is having

adequate current ratio which means that this organisation is quite capable of meeting its debts

more efficiently than compared to JD Sports Fashion Plc. The current ratios of Sports direct in

the year 2015 and 2016 as 2.29 and 2.42 respectively while on the other side, JD sports has the

ratios in 2015 and 2016 as 1.22 and 1.47 respectively. Therefore, it can be said that JD sports

need to make improvements in the operational activity as well as there is requirement to have

adequate amount of cash, bank and reserve balance which will be helpful in enhancing the

current ratios of firm. Thus, the operational ability of sports direct is quite appreciable under this

segmentation.

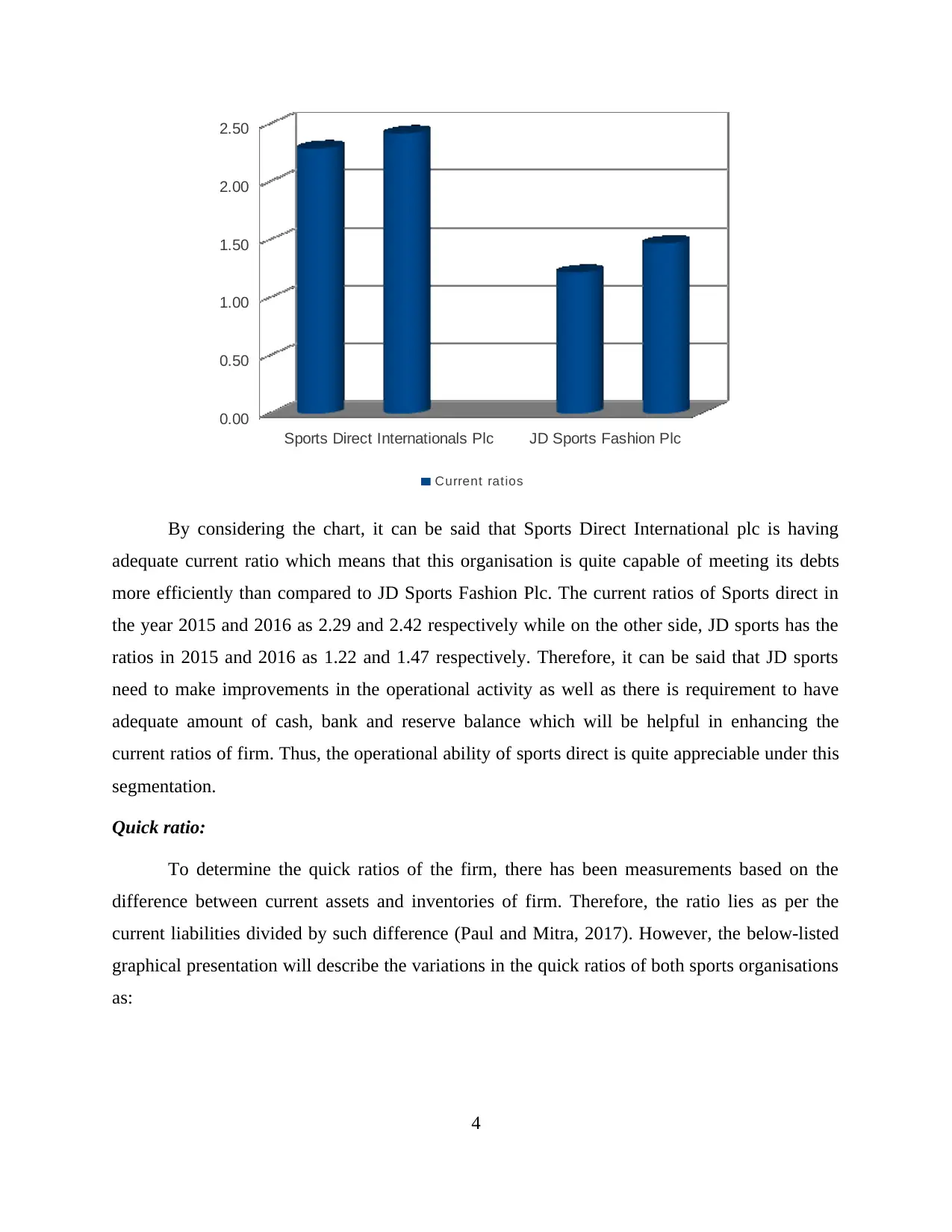

Quick ratio:

To determine the quick ratios of the firm, there has been measurements based on the

difference between current assets and inventories of firm. Therefore, the ratio lies as per the

current liabilities divided by such difference (Paul and Mitra, 2017). However, the below-listed

graphical presentation will describe the variations in the quick ratios of both sports organisations

as:

4

0.00

0.50

1.00

1.50

2.00

2.50

Current ratios

By considering the chart, it can be said that Sports Direct International plc is having

adequate current ratio which means that this organisation is quite capable of meeting its debts

more efficiently than compared to JD Sports Fashion Plc. The current ratios of Sports direct in

the year 2015 and 2016 as 2.29 and 2.42 respectively while on the other side, JD sports has the

ratios in 2015 and 2016 as 1.22 and 1.47 respectively. Therefore, it can be said that JD sports

need to make improvements in the operational activity as well as there is requirement to have

adequate amount of cash, bank and reserve balance which will be helpful in enhancing the

current ratios of firm. Thus, the operational ability of sports direct is quite appreciable under this

segmentation.

Quick ratio:

To determine the quick ratios of the firm, there has been measurements based on the

difference between current assets and inventories of firm. Therefore, the ratio lies as per the

current liabilities divided by such difference (Paul and Mitra, 2017). However, the below-listed

graphical presentation will describe the variations in the quick ratios of both sports organisations

as:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sports Direct Internationals Plc

JD Sports Fashion Plc

0

0.2

0.4

0.6

0.8

1

1.2

Q uic k ratio

By considering the quick ratios of both the plc: JD Sports Fashion Plc and Sports Direct

International Plc, it can be said that both the firms have appropriate ratios. While in accordance

with Sports Direct, the figure in 2015 and 2016 is as 0.94 and 1.13 respectively which describes

that in the current year, the firm has better sales and less closing stock which results in the

increment of such percentages. On the other side, JD sport has ratios for the same years as 0.54

and 0.78 respectively. It describes that the firm is having favourable growth as compared to the

last year but as per ratios of Sports Direct, the firm is having poor operational performances in

both the years. Therefore, there will be less sales or less amount of current assets available for

firm.

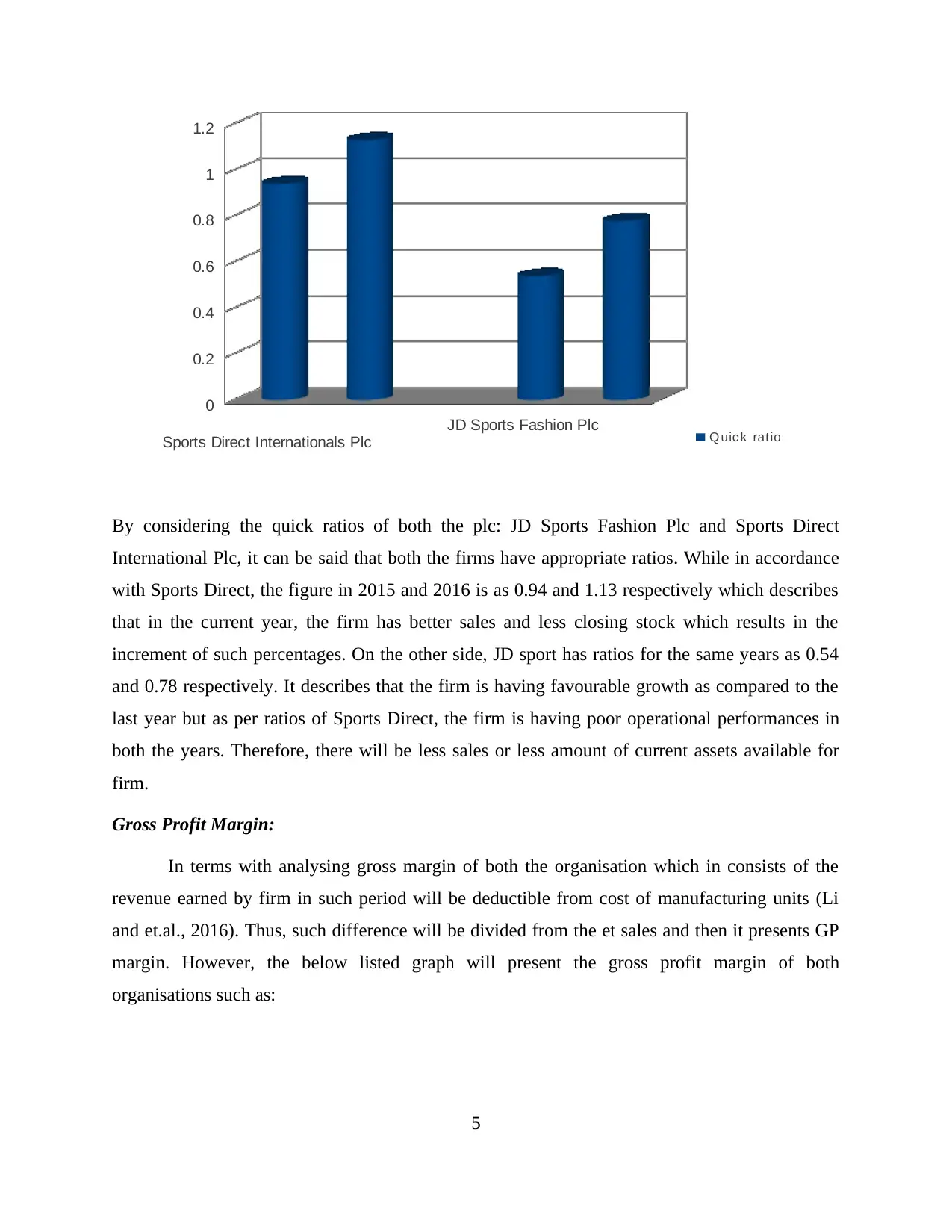

Gross Profit Margin:

In terms with analysing gross margin of both the organisation which in consists of the

revenue earned by firm in such period will be deductible from cost of manufacturing units (Li

and et.al., 2016). Thus, such difference will be divided from the et sales and then it presents GP

margin. However, the below listed graph will present the gross profit margin of both

organisations such as:

5

JD Sports Fashion Plc

0

0.2

0.4

0.6

0.8

1

1.2

Q uic k ratio

By considering the quick ratios of both the plc: JD Sports Fashion Plc and Sports Direct

International Plc, it can be said that both the firms have appropriate ratios. While in accordance

with Sports Direct, the figure in 2015 and 2016 is as 0.94 and 1.13 respectively which describes

that in the current year, the firm has better sales and less closing stock which results in the

increment of such percentages. On the other side, JD sport has ratios for the same years as 0.54

and 0.78 respectively. It describes that the firm is having favourable growth as compared to the

last year but as per ratios of Sports Direct, the firm is having poor operational performances in

both the years. Therefore, there will be less sales or less amount of current assets available for

firm.

Gross Profit Margin:

In terms with analysing gross margin of both the organisation which in consists of the

revenue earned by firm in such period will be deductible from cost of manufacturing units (Li

and et.al., 2016). Thus, such difference will be divided from the et sales and then it presents GP

margin. However, the below listed graph will present the gross profit margin of both

organisations such as:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sports Direct Internationals Plc JD Sports Fashion Plc

41.00%

42.00%

43.00%

44.00%

45.00%

46.00%

47.00%

48.00%

49.00%

43.81%

44.25%

48.62% 48.52%

GP M argin

The above listed chart determines gross profit margin of Sports Direct International plc

and JD Sports Fashion Plc which presents the huge variations in such analysis. However, in

accordance with the Sports direct the GP margin was in 2015 and 2016 is as 43.81% and

44.25%. On the other side JD sports has the ratios for the same years as 48.62% and 48.52%.

Therefore, it can be analysed that JD sports has the adequate amount of sales during the period as

well as there will be law cost of goods sold which in turn reflect the high profitability.

Operating profit margin:

In terms with the operating profit margin there has been reduction of all the operating

expenses and addition of all the operating income which in turn presents the operating profits.

However, to analyse the ratio there is need to divide OP to the net sales or revenue of the

business than the respected outcome will be known as the operating ratio (Chen, Chou and

Huang, 2016). However, it will be helpful in analysing that how capable the company is to meet

the operational cost of the business transactions. Thus, the following graph will reflect Operating

profit of both the sports industries Sports direct International Plc and JD Sports Fashion plc such

as:

6

41.00%

42.00%

43.00%

44.00%

45.00%

46.00%

47.00%

48.00%

49.00%

43.81%

44.25%

48.62% 48.52%

GP M argin

The above listed chart determines gross profit margin of Sports Direct International plc

and JD Sports Fashion Plc which presents the huge variations in such analysis. However, in

accordance with the Sports direct the GP margin was in 2015 and 2016 is as 43.81% and

44.25%. On the other side JD sports has the ratios for the same years as 48.62% and 48.52%.

Therefore, it can be analysed that JD sports has the adequate amount of sales during the period as

well as there will be law cost of goods sold which in turn reflect the high profitability.

Operating profit margin:

In terms with the operating profit margin there has been reduction of all the operating

expenses and addition of all the operating income which in turn presents the operating profits.

However, to analyse the ratio there is need to divide OP to the net sales or revenue of the

business than the respected outcome will be known as the operating ratio (Chen, Chou and

Huang, 2016). However, it will be helpful in analysing that how capable the company is to meet

the operational cost of the business transactions. Thus, the following graph will reflect Operating

profit of both the sports industries Sports direct International Plc and JD Sports Fashion plc such

as:

6

Sports Direct Internationals Plc

JD Sports Fashion Plc

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

10.13%

7.30%

6.04%

7.24%

O perating profit ratio

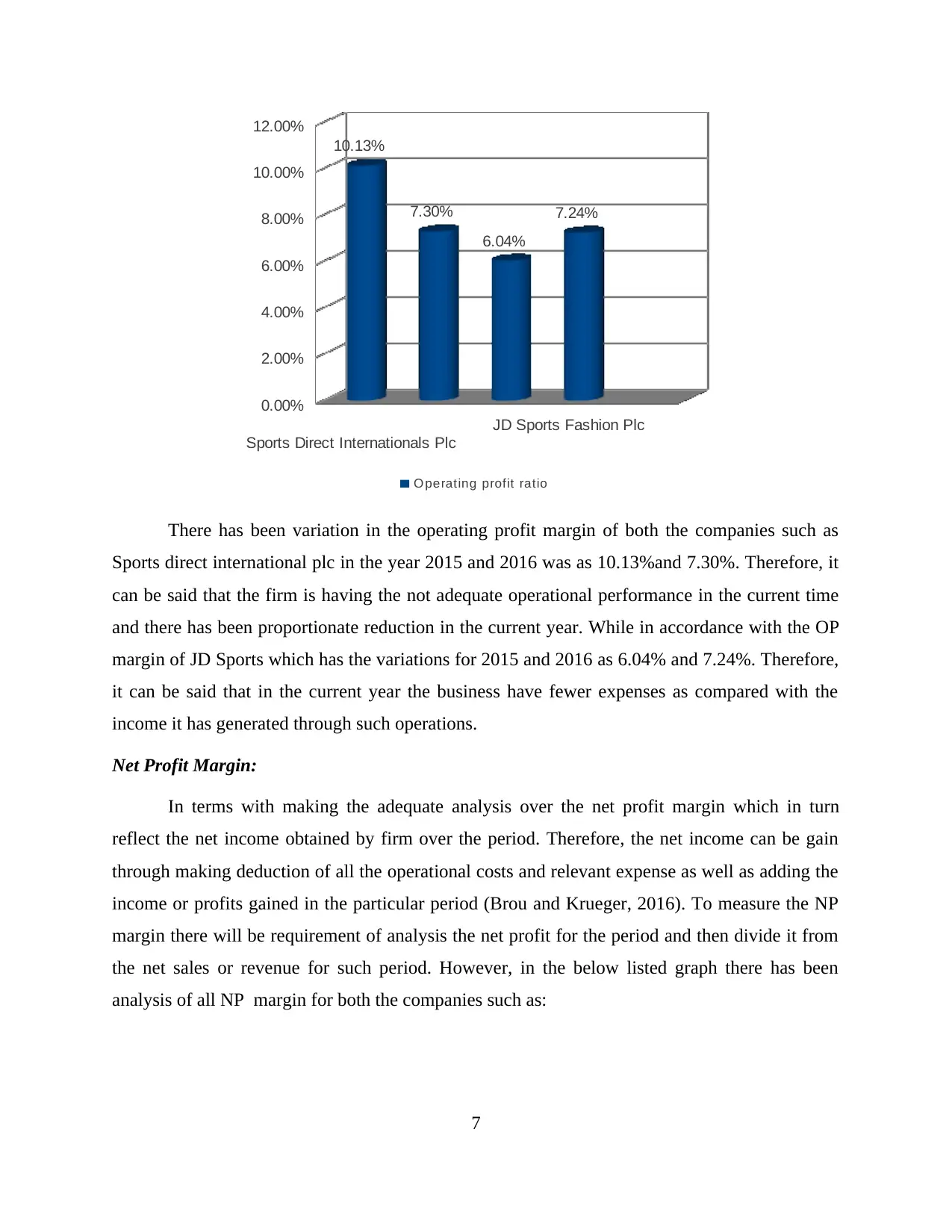

There has been variation in the operating profit margin of both the companies such as

Sports direct international plc in the year 2015 and 2016 was as 10.13%and 7.30%. Therefore, it

can be said that the firm is having the not adequate operational performance in the current time

and there has been proportionate reduction in the current year. While in accordance with the OP

margin of JD Sports which has the variations for 2015 and 2016 as 6.04% and 7.24%. Therefore,

it can be said that in the current year the business have fewer expenses as compared with the

income it has generated through such operations.

Net Profit Margin:

In terms with making the adequate analysis over the net profit margin which in turn

reflect the net income obtained by firm over the period. Therefore, the net income can be gain

through making deduction of all the operational costs and relevant expense as well as adding the

income or profits gained in the particular period (Brou and Krueger, 2016). To measure the NP

margin there will be requirement of analysis the net profit for the period and then divide it from

the net sales or revenue for such period. However, in the below listed graph there has been

analysis of all NP margin for both the companies such as:

7

JD Sports Fashion Plc

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

10.13%

7.30%

6.04%

7.24%

O perating profit ratio

There has been variation in the operating profit margin of both the companies such as

Sports direct international plc in the year 2015 and 2016 was as 10.13%and 7.30%. Therefore, it

can be said that the firm is having the not adequate operational performance in the current time

and there has been proportionate reduction in the current year. While in accordance with the OP

margin of JD Sports which has the variations for 2015 and 2016 as 6.04% and 7.24%. Therefore,

it can be said that in the current year the business have fewer expenses as compared with the

income it has generated through such operations.

Net Profit Margin:

In terms with making the adequate analysis over the net profit margin which in turn

reflect the net income obtained by firm over the period. Therefore, the net income can be gain

through making deduction of all the operational costs and relevant expense as well as adding the

income or profits gained in the particular period (Brou and Krueger, 2016). To measure the NP

margin there will be requirement of analysis the net profit for the period and then divide it from

the net sales or revenue for such period. However, in the below listed graph there has been

analysis of all NP margin for both the companies such as:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sports Direct Internationals Plc

JD Sports Fashion Plc

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

8.47%

9.54%

3.48%

4.36%

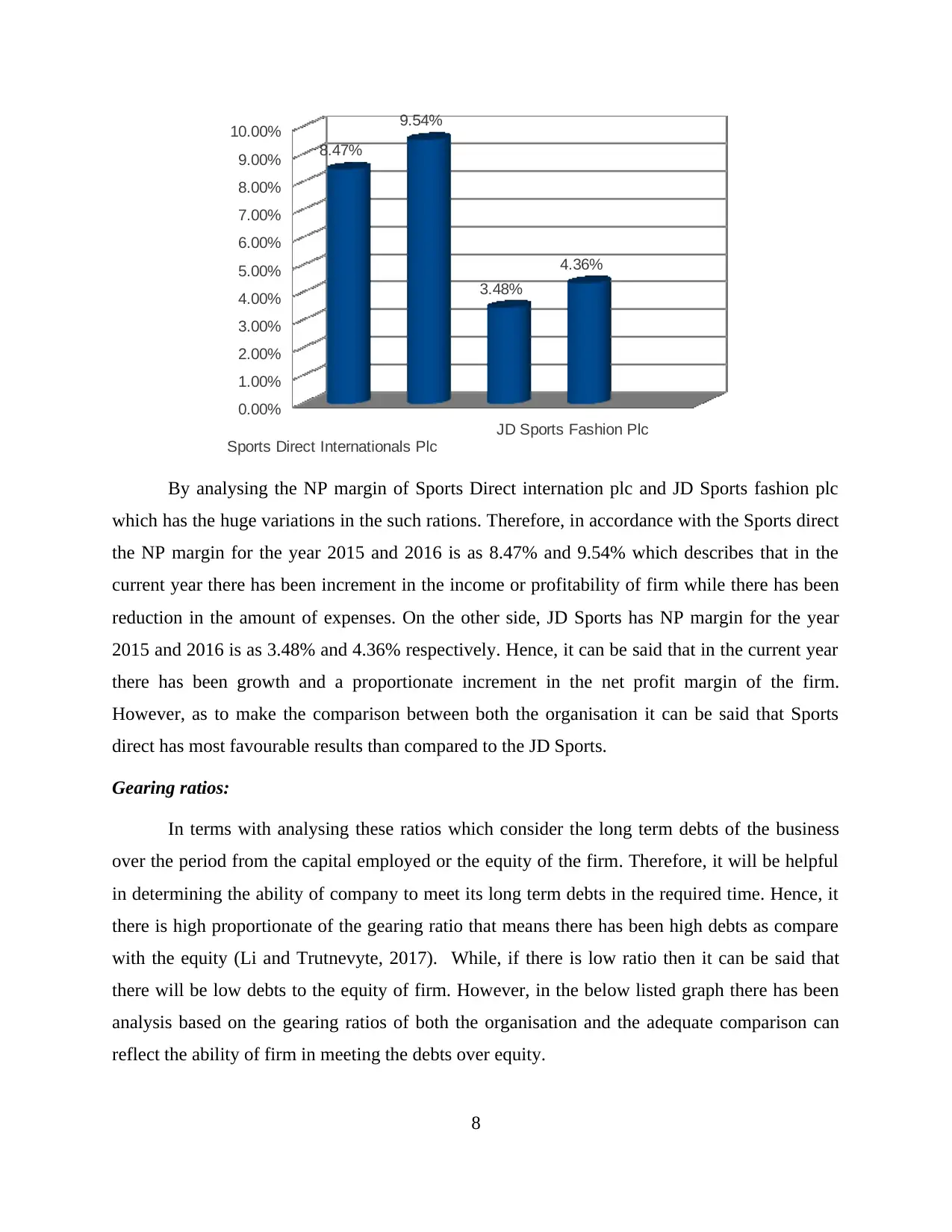

By analysing the NP margin of Sports Direct internation plc and JD Sports fashion plc

which has the huge variations in the such rations. Therefore, in accordance with the Sports direct

the NP margin for the year 2015 and 2016 is as 8.47% and 9.54% which describes that in the

current year there has been increment in the income or profitability of firm while there has been

reduction in the amount of expenses. On the other side, JD Sports has NP margin for the year

2015 and 2016 is as 3.48% and 4.36% respectively. Hence, it can be said that in the current year

there has been growth and a proportionate increment in the net profit margin of the firm.

However, as to make the comparison between both the organisation it can be said that Sports

direct has most favourable results than compared to the JD Sports.

Gearing ratios:

In terms with analysing these ratios which consider the long term debts of the business

over the period from the capital employed or the equity of the firm. Therefore, it will be helpful

in determining the ability of company to meet its long term debts in the required time. Hence, it

there is high proportionate of the gearing ratio that means there has been high debts as compare

with the equity (Li and Trutnevyte, 2017). While, if there is low ratio then it can be said that

there will be low debts to the equity of firm. However, in the below listed graph there has been

analysis based on the gearing ratios of both the organisation and the adequate comparison can

reflect the ability of firm in meeting the debts over equity.

8

JD Sports Fashion Plc

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

8.47%

9.54%

3.48%

4.36%

By analysing the NP margin of Sports Direct internation plc and JD Sports fashion plc

which has the huge variations in the such rations. Therefore, in accordance with the Sports direct

the NP margin for the year 2015 and 2016 is as 8.47% and 9.54% which describes that in the

current year there has been increment in the income or profitability of firm while there has been

reduction in the amount of expenses. On the other side, JD Sports has NP margin for the year

2015 and 2016 is as 3.48% and 4.36% respectively. Hence, it can be said that in the current year

there has been growth and a proportionate increment in the net profit margin of the firm.

However, as to make the comparison between both the organisation it can be said that Sports

direct has most favourable results than compared to the JD Sports.

Gearing ratios:

In terms with analysing these ratios which consider the long term debts of the business

over the period from the capital employed or the equity of the firm. Therefore, it will be helpful

in determining the ability of company to meet its long term debts in the required time. Hence, it

there is high proportionate of the gearing ratio that means there has been high debts as compare

with the equity (Li and Trutnevyte, 2017). While, if there is low ratio then it can be said that

there will be low debts to the equity of firm. However, in the below listed graph there has been

analysis based on the gearing ratios of both the organisation and the adequate comparison can

reflect the ability of firm in meeting the debts over equity.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sports Direct Internationals Plc

JD Sports Fashion Plc

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

9.85%

18.31%

12.11%

9.48%

G earing ratio

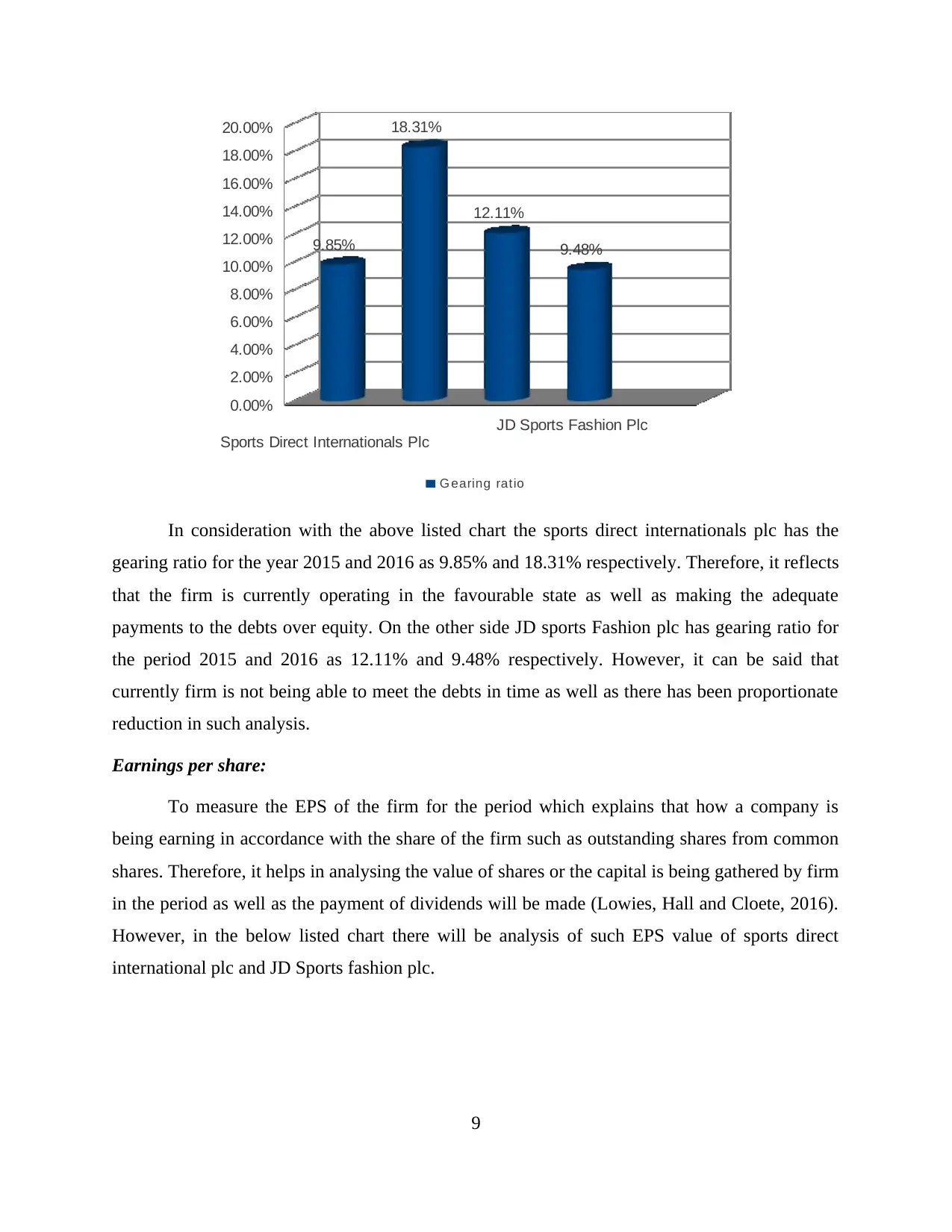

In consideration with the above listed chart the sports direct internationals plc has the

gearing ratio for the year 2015 and 2016 as 9.85% and 18.31% respectively. Therefore, it reflects

that the firm is currently operating in the favourable state as well as making the adequate

payments to the debts over equity. On the other side JD sports Fashion plc has gearing ratio for

the period 2015 and 2016 as 12.11% and 9.48% respectively. However, it can be said that

currently firm is not being able to meet the debts in time as well as there has been proportionate

reduction in such analysis.

Earnings per share:

To measure the EPS of the firm for the period which explains that how a company is

being earning in accordance with the share of the firm such as outstanding shares from common

shares. Therefore, it helps in analysing the value of shares or the capital is being gathered by firm

in the period as well as the payment of dividends will be made (Lowies, Hall and Cloete, 2016).

However, in the below listed chart there will be analysis of such EPS value of sports direct

international plc and JD Sports fashion plc.

9

JD Sports Fashion Plc

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

20.00%

9.85%

18.31%

12.11%

9.48%

G earing ratio

In consideration with the above listed chart the sports direct internationals plc has the

gearing ratio for the year 2015 and 2016 as 9.85% and 18.31% respectively. Therefore, it reflects

that the firm is currently operating in the favourable state as well as making the adequate

payments to the debts over equity. On the other side JD sports Fashion plc has gearing ratio for

the period 2015 and 2016 as 12.11% and 9.48% respectively. However, it can be said that

currently firm is not being able to meet the debts in time as well as there has been proportionate

reduction in such analysis.

Earnings per share:

To measure the EPS of the firm for the period which explains that how a company is

being earning in accordance with the share of the firm such as outstanding shares from common

shares. Therefore, it helps in analysing the value of shares or the capital is being gathered by firm

in the period as well as the payment of dividends will be made (Lowies, Hall and Cloete, 2016).

However, in the below listed chart there will be analysis of such EPS value of sports direct

international plc and JD Sports fashion plc.

9

Sports Direct Internationals Plc

JD Sports Fashion Plc

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0.39

0.46

0.05

0.1

E arning per s hare

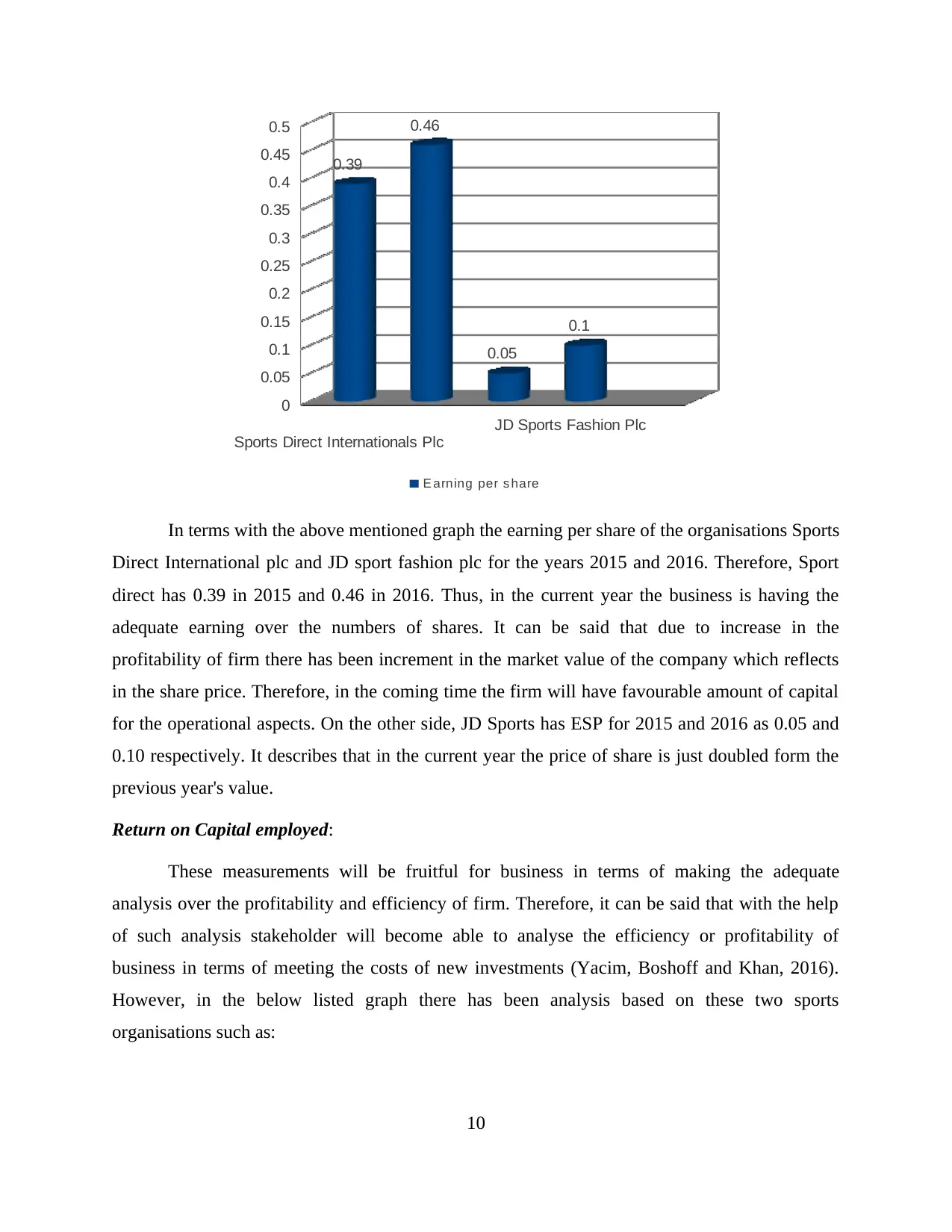

In terms with the above mentioned graph the earning per share of the organisations Sports

Direct International plc and JD sport fashion plc for the years 2015 and 2016. Therefore, Sport

direct has 0.39 in 2015 and 0.46 in 2016. Thus, in the current year the business is having the

adequate earning over the numbers of shares. It can be said that due to increase in the

profitability of firm there has been increment in the market value of the company which reflects

in the share price. Therefore, in the coming time the firm will have favourable amount of capital

for the operational aspects. On the other side, JD Sports has ESP for 2015 and 2016 as 0.05 and

0.10 respectively. It describes that in the current year the price of share is just doubled form the

previous year's value.

Return on Capital employed:

These measurements will be fruitful for business in terms of making the adequate

analysis over the profitability and efficiency of firm. Therefore, it can be said that with the help

of such analysis stakeholder will become able to analyse the efficiency or profitability of

business in terms of meeting the costs of new investments (Yacim, Boshoff and Khan, 2016).

However, in the below listed graph there has been analysis based on these two sports

organisations such as:

10

JD Sports Fashion Plc

0

0.05

0.1

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

0.39

0.46

0.05

0.1

E arning per s hare

In terms with the above mentioned graph the earning per share of the organisations Sports

Direct International plc and JD sport fashion plc for the years 2015 and 2016. Therefore, Sport

direct has 0.39 in 2015 and 0.46 in 2016. Thus, in the current year the business is having the

adequate earning over the numbers of shares. It can be said that due to increase in the

profitability of firm there has been increment in the market value of the company which reflects

in the share price. Therefore, in the coming time the firm will have favourable amount of capital

for the operational aspects. On the other side, JD Sports has ESP for 2015 and 2016 as 0.05 and

0.10 respectively. It describes that in the current year the price of share is just doubled form the

previous year's value.

Return on Capital employed:

These measurements will be fruitful for business in terms of making the adequate

analysis over the profitability and efficiency of firm. Therefore, it can be said that with the help

of such analysis stakeholder will become able to analyse the efficiency or profitability of

business in terms of meeting the costs of new investments (Yacim, Boshoff and Khan, 2016).

However, in the below listed graph there has been analysis based on these two sports

organisations such as:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.