SPORTS LTD Financial Report: Sources of Funding and Analysis

VerifiedAdded on 2020/10/22

|13

|2985

|369

Report

AI Summary

This report presents a detailed financial analysis of SPORTS LTD, a UK-based company providing financial services. It begins with an introduction and literature review, discussing accounting models and investment appraisal techniques like Net Present Value (NPV). The report then explores the company's sources of funding, including bank loans and potential equity shares, as well as the implications of implementing new accounting software. It includes an analysis of investment appraisal using NPV, break-even analysis, and cash budgeting. The break-even analysis calculates the point where the company's costs equal revenue, while the cash budget forecasts cash inflows and outflows. The report concludes with an evaluation of the financial strategies and recommendations for future financial planning. The report aims to give a comprehensive overview of the company’s financial position and future plans.

Financial Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..............................................................................................................1

LITRATURE REVIEW......................................................................................................1

SOURCES OF FUNDING................................................................................................2

ANALYSIS OF INVESTMENT APRAISAL BY USING NPV.............................................3

Investment appraisal....................................................................................................3

COMPUTATION OF BREAK EVEN ANALYSIS AND CASH BUDGET...........................5

Break even analysis.....................................................................................................5

Cash Budget................................................................................................................ 6

EVALUATION...................................................................................................................8

CONCLUSION................................................................................................................. 8

REFERENCES.................................................................................................................9

INTRODUCTION..............................................................................................................1

LITRATURE REVIEW......................................................................................................1

SOURCES OF FUNDING................................................................................................2

ANALYSIS OF INVESTMENT APRAISAL BY USING NPV.............................................3

Investment appraisal....................................................................................................3

COMPUTATION OF BREAK EVEN ANALYSIS AND CASH BUDGET...........................5

Break even analysis.....................................................................................................5

Cash Budget................................................................................................................ 6

EVALUATION...................................................................................................................8

CONCLUSION................................................................................................................. 8

REFERENCES.................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial report is a part of financial statements which helps managers to see

actual position of its organisation (Perera and Chand, 2015). It means the full disclosure

of company,s financial statements, to all different users of it. It helps mangers to make

an analysis of its company's statements and find out any problems and develop

strategies to tackle those problems. The following report contains a detailed analysis of

SPORTS LTD working in UK, headquartered in South Africa providing financial services

to property developers, SME's and investment property funds in both Africa and UK.

This report also consists of sources of funding for SPORTS LTD and implication of new

accounting software.

LITRATURE REVIEW

As per Trujillo-Ponce, Samaniego-Medina and Cardone-Riportella (2014)

accounting models are models which are used by an organisation to manage its

resources and prepare its final statements. These models helps an organisation to work

effectively and efficiently and to follow general accounting concepts. Following are some

models of accounting:

As per Gotze, Northcott and Schuster (2016) investment appraisal is a method to

find out investment attractiveness so that it can get maximum return out of that

investment. It is used by mangers to identify viability of any project, this help

organisation to get an estimate amount of return from their investment to check whether

that particular invest will be profitable or not.

As per Comans, and et.all (2013) Break even analysis is a calculation of margin

of safety. It is a point where company's cost of production including both variable and

fixed cost is equal to revenue generated by sale of these goods. This is an analysis of

different level of prices, it is used by businesses to identify the level of sales which are

necessary in order top cover company's fixed cost.

As per Warren (2015) cash budgeting also known as cash budget is used by

mangers to identify budget to see the requirement of cash in an accounting year. It

helps mangers to identify that company has a sufficient to mange its operations or not.

1

Financial report is a part of financial statements which helps managers to see

actual position of its organisation (Perera and Chand, 2015). It means the full disclosure

of company,s financial statements, to all different users of it. It helps mangers to make

an analysis of its company's statements and find out any problems and develop

strategies to tackle those problems. The following report contains a detailed analysis of

SPORTS LTD working in UK, headquartered in South Africa providing financial services

to property developers, SME's and investment property funds in both Africa and UK.

This report also consists of sources of funding for SPORTS LTD and implication of new

accounting software.

LITRATURE REVIEW

As per Trujillo-Ponce, Samaniego-Medina and Cardone-Riportella (2014)

accounting models are models which are used by an organisation to manage its

resources and prepare its final statements. These models helps an organisation to work

effectively and efficiently and to follow general accounting concepts. Following are some

models of accounting:

As per Gotze, Northcott and Schuster (2016) investment appraisal is a method to

find out investment attractiveness so that it can get maximum return out of that

investment. It is used by mangers to identify viability of any project, this help

organisation to get an estimate amount of return from their investment to check whether

that particular invest will be profitable or not.

As per Comans, and et.all (2013) Break even analysis is a calculation of margin

of safety. It is a point where company's cost of production including both variable and

fixed cost is equal to revenue generated by sale of these goods. This is an analysis of

different level of prices, it is used by businesses to identify the level of sales which are

necessary in order top cover company's fixed cost.

As per Warren (2015) cash budgeting also known as cash budget is used by

mangers to identify budget to see the requirement of cash in an accounting year. It

helps mangers to identify that company has a sufficient to mange its operations or not.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

While preparing cash budget for a company previous sales and production data are

analysed to see an estimate use of cash in a company.

SOURCES OF FUNDING

Funding is one of the most important part of an organisation without funds it is

impossible for any organisation to survive (Dunne and et.all, 2013). It is one of a basic

necessities of an organisation which helps it to keep on going. These funds can be

raised from various sources as mentioned above in case study, SPORTS limited uses

only two methods for raising its capital. Earlier company was funded by its parent

organisation situated in South Africa, company has to always relies on its parent

company to support it financially. In this process it consumes time and approval for

every single transaction, but now company has decided to implement new software to

improve its efficiency which will help the company to raise its capital from other sources.

To raise it fund company decided to take a bank loan at 3% interest and loan

amount to be paid back in one year dividing it into 12 equal instalments, loan amount

take by company is of 18000 to open a new store in London to sell two software as

Small business tool (SBT) and Corporate business tool (CBT). Initially company will only

sell two products to test market and check that its break even analysis is achieved

during same period. SPORTS limited is also considering to implement new software for

its accounting purpose for this company has selected two software one is capital suit

and the other one is capital platform by which it can manges its resources and reduce

borrowing money from its parent organisation. At present company raised it funds

through loan to set up a new shop in London. There are other ways also to raise its fund

through issuing equity share, long term debts which include debentures and long term

bank borrowing.

Equity Shares: Equity shares are shares which are issued by company to raise

its capital, this type of shares gives the shareholders a controlling as per decided by

company (Valentinetti and Rea, 2012). Equity share holders are considered as owner of

business. Following are the advantage and disadvantages of equity share:

Advantages: It is considered as a permanent source of capital, company can issue

equity share whenever they require funds and company does not have to pay it back

2

analysed to see an estimate use of cash in a company.

SOURCES OF FUNDING

Funding is one of the most important part of an organisation without funds it is

impossible for any organisation to survive (Dunne and et.all, 2013). It is one of a basic

necessities of an organisation which helps it to keep on going. These funds can be

raised from various sources as mentioned above in case study, SPORTS limited uses

only two methods for raising its capital. Earlier company was funded by its parent

organisation situated in South Africa, company has to always relies on its parent

company to support it financially. In this process it consumes time and approval for

every single transaction, but now company has decided to implement new software to

improve its efficiency which will help the company to raise its capital from other sources.

To raise it fund company decided to take a bank loan at 3% interest and loan

amount to be paid back in one year dividing it into 12 equal instalments, loan amount

take by company is of 18000 to open a new store in London to sell two software as

Small business tool (SBT) and Corporate business tool (CBT). Initially company will only

sell two products to test market and check that its break even analysis is achieved

during same period. SPORTS limited is also considering to implement new software for

its accounting purpose for this company has selected two software one is capital suit

and the other one is capital platform by which it can manges its resources and reduce

borrowing money from its parent organisation. At present company raised it funds

through loan to set up a new shop in London. There are other ways also to raise its fund

through issuing equity share, long term debts which include debentures and long term

bank borrowing.

Equity Shares: Equity shares are shares which are issued by company to raise

its capital, this type of shares gives the shareholders a controlling as per decided by

company (Valentinetti and Rea, 2012). Equity share holders are considered as owner of

business. Following are the advantage and disadvantages of equity share:

Advantages: It is considered as a permanent source of capital, company can issue

equity share whenever they require funds and company does not have to pay it back

2

unless a company is going into liquidation. These shares does not have any fixed rate

to pay dividends every year.

Disadvantages: Equity shares are not redeemable which may lead to over capitalization

for a company. Equity shareholders some time create obstacles for a company by

organising and manipulation. Some times a dividend is paid at a higher returns during a

prosperous periods.

Long term loans: Long term loans are a type of loan which are given to a

company whose repayment time is after a long term, long term in case of accounting is

considered if a period is of more than one year (Chandar, Chang and Zheng, 2012).

Following are some advantages and disadvantages of it:

Advantages: These long term loans provide flexibility to an organisation as they don't

have to worry about there loans they only have to make their instalments on time and

can fully focus on their operations. It also helps to manage their working capital as it

provides funds for its daily operations.

Disadvantages: Most important disadvantage of these long term are their strict

documentation process. In bank loan documents which are required by these

institutions are strictly required and should be in proper form. It also create an additional

burden on its cost or production of the goods. To take a long term loan company has to

maintain its credit score and security needs should be provided.

ANALYSIS OF INVESTMENT APRAISAL BY USING NPV

Investment appraisal

Investment appraisal is finding out the rate of return which a company can earn

after taking that investment (Barth, 2013). It is calculated by using various different

methods such as internal rate of return (IRR), average rate of return, payback period

and net present value (NPV).

Capital suite

Draft figure

Year 0 1 2 3 4 5

New software cost 8800 9700 11940 16900 22170 28270

Working capital 900 600 800 300 700

3

to pay dividends every year.

Disadvantages: Equity shares are not redeemable which may lead to over capitalization

for a company. Equity shareholders some time create obstacles for a company by

organising and manipulation. Some times a dividend is paid at a higher returns during a

prosperous periods.

Long term loans: Long term loans are a type of loan which are given to a

company whose repayment time is after a long term, long term in case of accounting is

considered if a period is of more than one year (Chandar, Chang and Zheng, 2012).

Following are some advantages and disadvantages of it:

Advantages: These long term loans provide flexibility to an organisation as they don't

have to worry about there loans they only have to make their instalments on time and

can fully focus on their operations. It also helps to manage their working capital as it

provides funds for its daily operations.

Disadvantages: Most important disadvantage of these long term are their strict

documentation process. In bank loan documents which are required by these

institutions are strictly required and should be in proper form. It also create an additional

burden on its cost or production of the goods. To take a long term loan company has to

maintain its credit score and security needs should be provided.

ANALYSIS OF INVESTMENT APRAISAL BY USING NPV

Investment appraisal

Investment appraisal is finding out the rate of return which a company can earn

after taking that investment (Barth, 2013). It is calculated by using various different

methods such as internal rate of return (IRR), average rate of return, payback period

and net present value (NPV).

Capital suite

Draft figure

Year 0 1 2 3 4 5

New software cost 8800 9700 11940 16900 22170 28270

Working capital 900 600 800 300 700

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

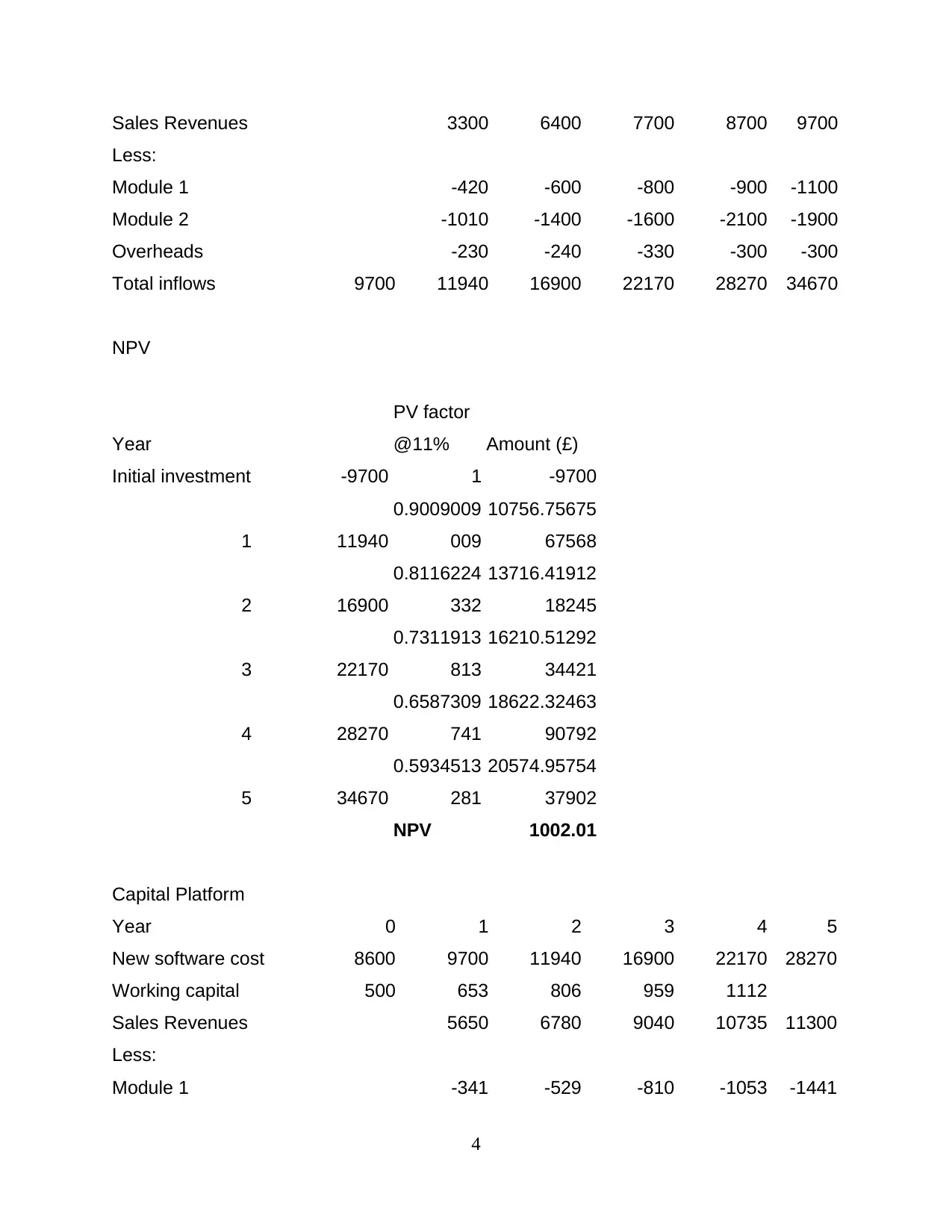

Sales Revenues 3300 6400 7700 8700 9700

Less:

Module 1 -420 -600 -800 -900 -1100

Module 2 -1010 -1400 -1600 -2100 -1900

Overheads -230 -240 -330 -300 -300

Total inflows 9700 11940 16900 22170 28270 34670

NPV

Year

PV factor

@11% Amount (£)

Initial investment -9700 1 -9700

1 11940

0.9009009

009

10756.75675

67568

2 16900

0.8116224

332

13716.41912

18245

3 22170

0.7311913

813

16210.51292

34421

4 28270

0.6587309

741

18622.32463

90792

5 34670

0.5934513

281

20574.95754

37902

NPV 1002.01

Capital Platform

Year 0 1 2 3 4 5

New software cost 8600 9700 11940 16900 22170 28270

Working capital 500 653 806 959 1112

Sales Revenues 5650 6780 9040 10735 11300

Less:

Module 1 -341 -529 -810 -1053 -1441

4

Less:

Module 1 -420 -600 -800 -900 -1100

Module 2 -1010 -1400 -1600 -2100 -1900

Overheads -230 -240 -330 -300 -300

Total inflows 9700 11940 16900 22170 28270 34670

NPV

Year

PV factor

@11% Amount (£)

Initial investment -9700 1 -9700

1 11940

0.9009009

009

10756.75675

67568

2 16900

0.8116224

332

13716.41912

18245

3 22170

0.7311913

813

16210.51292

34421

4 28270

0.6587309

741

18622.32463

90792

5 34670

0.5934513

281

20574.95754

37902

NPV 1002.01

Capital Platform

Year 0 1 2 3 4 5

New software cost 8600 9700 11940 16900 22170 28270

Working capital 500 653 806 959 1112

Sales Revenues 5650 6780 9040 10735 11300

Less:

Module 1 -341 -529 -810 -1053 -1441

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

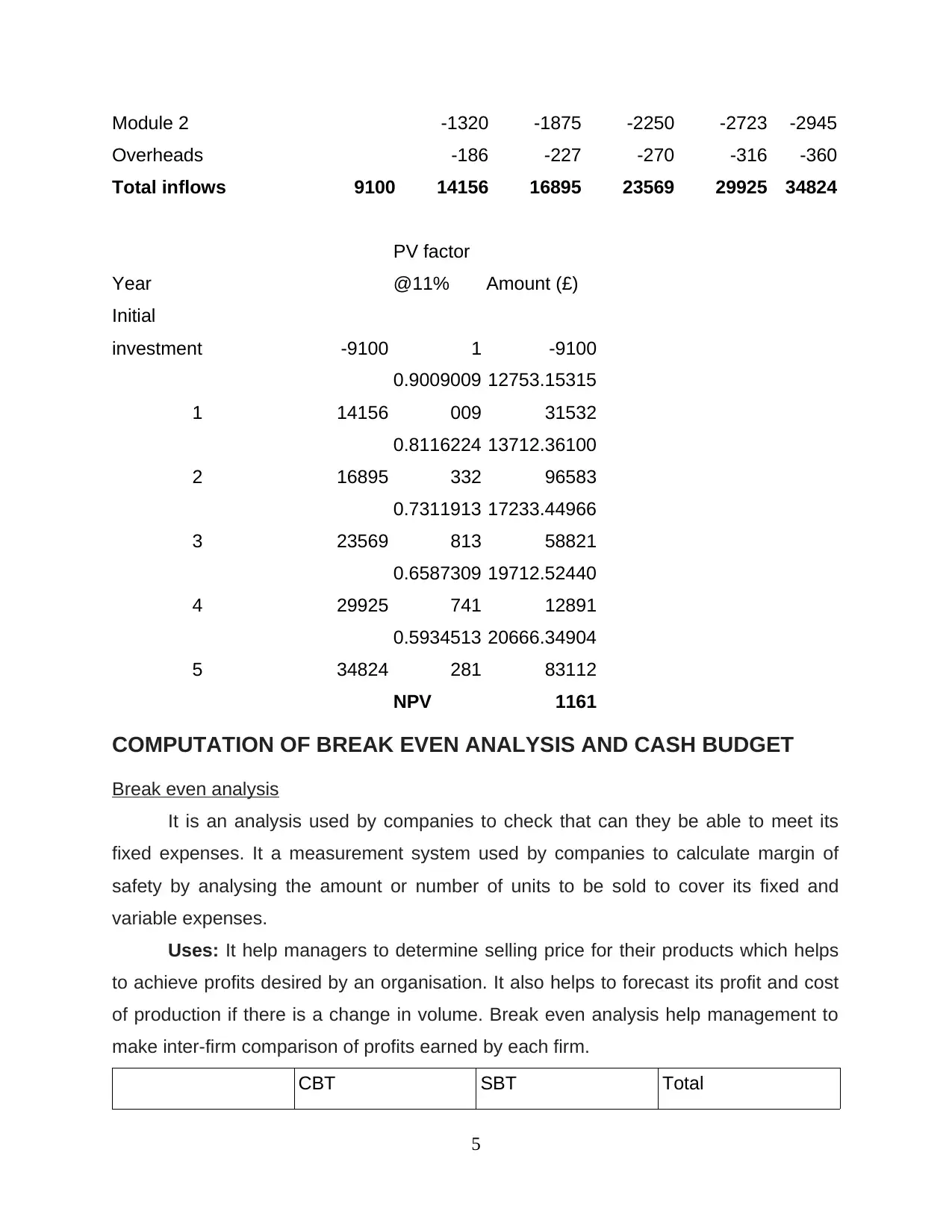

Module 2 -1320 -1875 -2250 -2723 -2945

Overheads -186 -227 -270 -316 -360

Total inflows 9100 14156 16895 23569 29925 34824

Year

PV factor

@11% Amount (£)

Initial

investment -9100 1 -9100

1 14156

0.9009009

009

12753.15315

31532

2 16895

0.8116224

332

13712.36100

96583

3 23569

0.7311913

813

17233.44966

58821

4 29925

0.6587309

741

19712.52440

12891

5 34824

0.5934513

281

20666.34904

83112

NPV 1161

COMPUTATION OF BREAK EVEN ANALYSIS AND CASH BUDGET

Break even analysis

It is an analysis used by companies to check that can they be able to meet its

fixed expenses. It a measurement system used by companies to calculate margin of

safety by analysing the amount or number of units to be sold to cover its fixed and

variable expenses.

Uses: It help managers to determine selling price for their products which helps

to achieve profits desired by an organisation. It also helps to forecast its profit and cost

of production if there is a change in volume. Break even analysis help management to

make inter-firm comparison of profits earned by each firm.

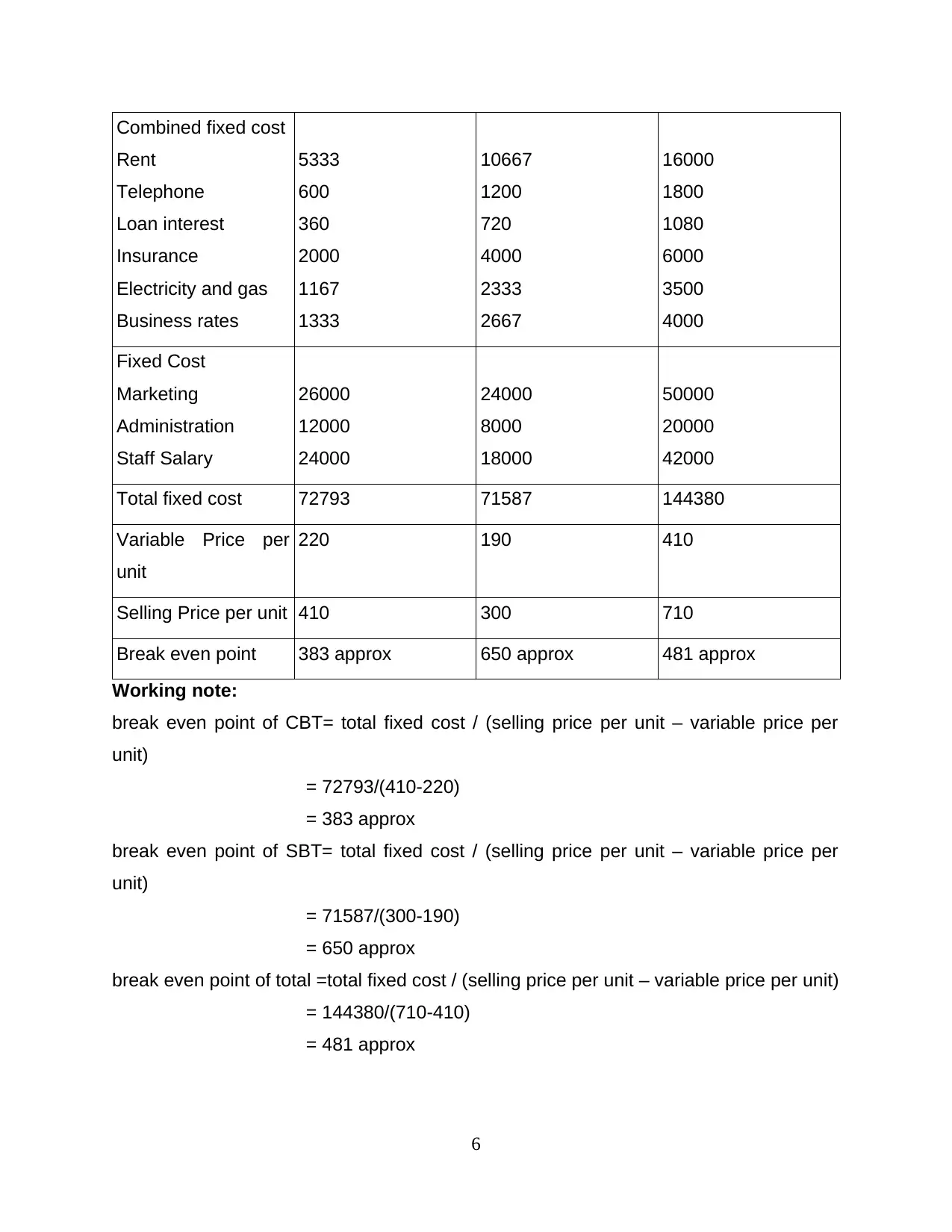

CBT SBT Total

5

Overheads -186 -227 -270 -316 -360

Total inflows 9100 14156 16895 23569 29925 34824

Year

PV factor

@11% Amount (£)

Initial

investment -9100 1 -9100

1 14156

0.9009009

009

12753.15315

31532

2 16895

0.8116224

332

13712.36100

96583

3 23569

0.7311913

813

17233.44966

58821

4 29925

0.6587309

741

19712.52440

12891

5 34824

0.5934513

281

20666.34904

83112

NPV 1161

COMPUTATION OF BREAK EVEN ANALYSIS AND CASH BUDGET

Break even analysis

It is an analysis used by companies to check that can they be able to meet its

fixed expenses. It a measurement system used by companies to calculate margin of

safety by analysing the amount or number of units to be sold to cover its fixed and

variable expenses.

Uses: It help managers to determine selling price for their products which helps

to achieve profits desired by an organisation. It also helps to forecast its profit and cost

of production if there is a change in volume. Break even analysis help management to

make inter-firm comparison of profits earned by each firm.

CBT SBT Total

5

Combined fixed cost

Rent

Telephone

Loan interest

Insurance

Electricity and gas

Business rates

5333

600

360

2000

1167

1333

10667

1200

720

4000

2333

2667

16000

1800

1080

6000

3500

4000

Fixed Cost

Marketing

Administration

Staff Salary

26000

12000

24000

24000

8000

18000

50000

20000

42000

Total fixed cost 72793 71587 144380

Variable Price per

unit

220 190 410

Selling Price per unit 410 300 710

Break even point 383 approx 650 approx 481 approx

Working note:

break even point of CBT= total fixed cost / (selling price per unit – variable price per

unit)

= 72793/(410-220)

= 383 approx

break even point of SBT= total fixed cost / (selling price per unit – variable price per

unit)

= 71587/(300-190)

= 650 approx

break even point of total =total fixed cost / (selling price per unit – variable price per unit)

= 144380/(710-410)

= 481 approx

6

Rent

Telephone

Loan interest

Insurance

Electricity and gas

Business rates

5333

600

360

2000

1167

1333

10667

1200

720

4000

2333

2667

16000

1800

1080

6000

3500

4000

Fixed Cost

Marketing

Administration

Staff Salary

26000

12000

24000

24000

8000

18000

50000

20000

42000

Total fixed cost 72793 71587 144380

Variable Price per

unit

220 190 410

Selling Price per unit 410 300 710

Break even point 383 approx 650 approx 481 approx

Working note:

break even point of CBT= total fixed cost / (selling price per unit – variable price per

unit)

= 72793/(410-220)

= 383 approx

break even point of SBT= total fixed cost / (selling price per unit – variable price per

unit)

= 71587/(300-190)

= 650 approx

break even point of total =total fixed cost / (selling price per unit – variable price per unit)

= 144380/(710-410)

= 481 approx

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

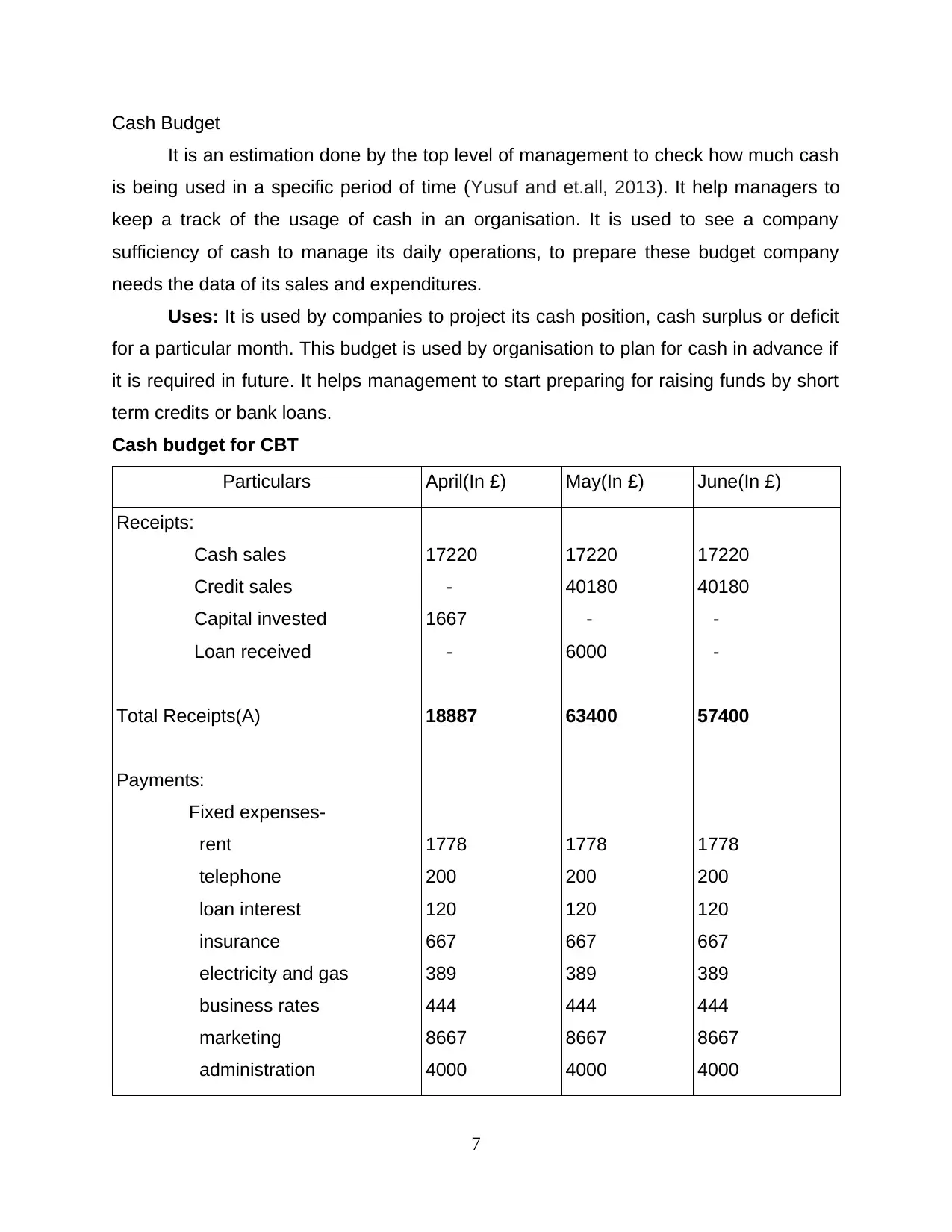

Cash Budget

It is an estimation done by the top level of management to check how much cash

is being used in a specific period of time (Yusuf and et.all, 2013). It help managers to

keep a track of the usage of cash in an organisation. It is used to see a company

sufficiency of cash to manage its daily operations, to prepare these budget company

needs the data of its sales and expenditures.

Uses: It is used by companies to project its cash position, cash surplus or deficit

for a particular month. This budget is used by organisation to plan for cash in advance if

it is required in future. It helps management to start preparing for raising funds by short

term credits or bank loans.

Cash budget for CBT

Particulars April(In £) May(In £) June(In £)

Receipts:

Cash sales

Credit sales

Capital invested

Loan received

Total Receipts(A)

Payments:

Fixed expenses-

rent

telephone

loan interest

insurance

electricity and gas

business rates

marketing

administration

17220

-

1667

-

18887

1778

200

120

667

389

444

8667

4000

17220

40180

-

6000

63400

1778

200

120

667

389

444

8667

4000

17220

40180

-

-

57400

1778

200

120

667

389

444

8667

4000

7

It is an estimation done by the top level of management to check how much cash

is being used in a specific period of time (Yusuf and et.all, 2013). It help managers to

keep a track of the usage of cash in an organisation. It is used to see a company

sufficiency of cash to manage its daily operations, to prepare these budget company

needs the data of its sales and expenditures.

Uses: It is used by companies to project its cash position, cash surplus or deficit

for a particular month. This budget is used by organisation to plan for cash in advance if

it is required in future. It helps management to start preparing for raising funds by short

term credits or bank loans.

Cash budget for CBT

Particulars April(In £) May(In £) June(In £)

Receipts:

Cash sales

Credit sales

Capital invested

Loan received

Total Receipts(A)

Payments:

Fixed expenses-

rent

telephone

loan interest

insurance

electricity and gas

business rates

marketing

administration

17220

-

1667

-

18887

1778

200

120

667

389

444

8667

4000

17220

40180

-

6000

63400

1778

200

120

667

389

444

8667

4000

17220

40180

-

-

57400

1778

200

120

667

389

444

8667

4000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

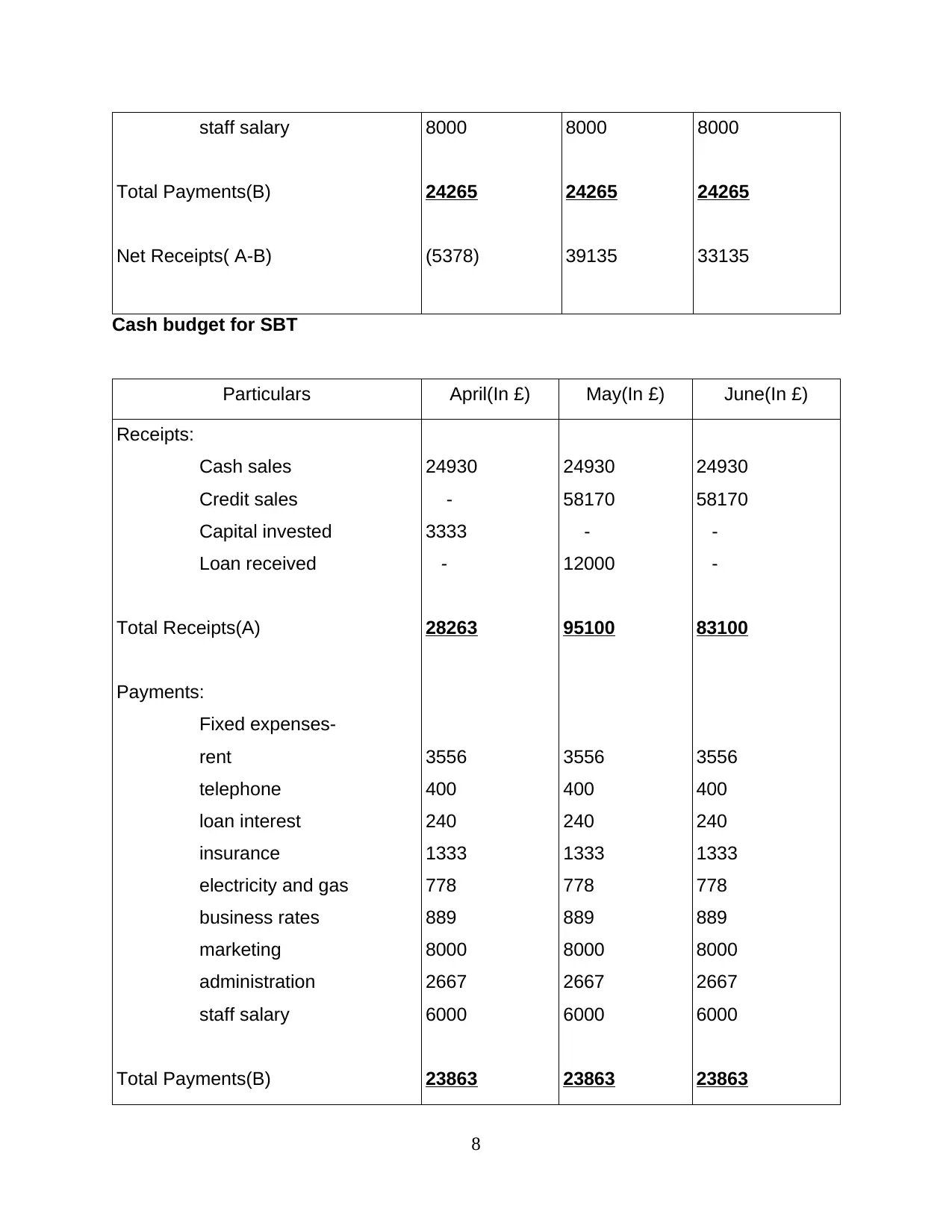

staff salary

Total Payments(B)

Net Receipts( A-B)

8000

24265

(5378)

8000

24265

39135

8000

24265

33135

Cash budget for SBT

Particulars April(In £) May(In £) June(In £)

Receipts:

Cash sales

Credit sales

Capital invested

Loan received

Total Receipts(A)

Payments:

Fixed expenses-

rent

telephone

loan interest

insurance

electricity and gas

business rates

marketing

administration

staff salary

Total Payments(B)

24930

-

3333

-

28263

3556

400

240

1333

778

889

8000

2667

6000

23863

24930

58170

-

12000

95100

3556

400

240

1333

778

889

8000

2667

6000

23863

24930

58170

-

-

83100

3556

400

240

1333

778

889

8000

2667

6000

23863

8

Total Payments(B)

Net Receipts( A-B)

8000

24265

(5378)

8000

24265

39135

8000

24265

33135

Cash budget for SBT

Particulars April(In £) May(In £) June(In £)

Receipts:

Cash sales

Credit sales

Capital invested

Loan received

Total Receipts(A)

Payments:

Fixed expenses-

rent

telephone

loan interest

insurance

electricity and gas

business rates

marketing

administration

staff salary

Total Payments(B)

24930

-

3333

-

28263

3556

400

240

1333

778

889

8000

2667

6000

23863

24930

58170

-

12000

95100

3556

400

240

1333

778

889

8000

2667

6000

23863

24930

58170

-

-

83100

3556

400

240

1333

778

889

8000

2667

6000

23863

8

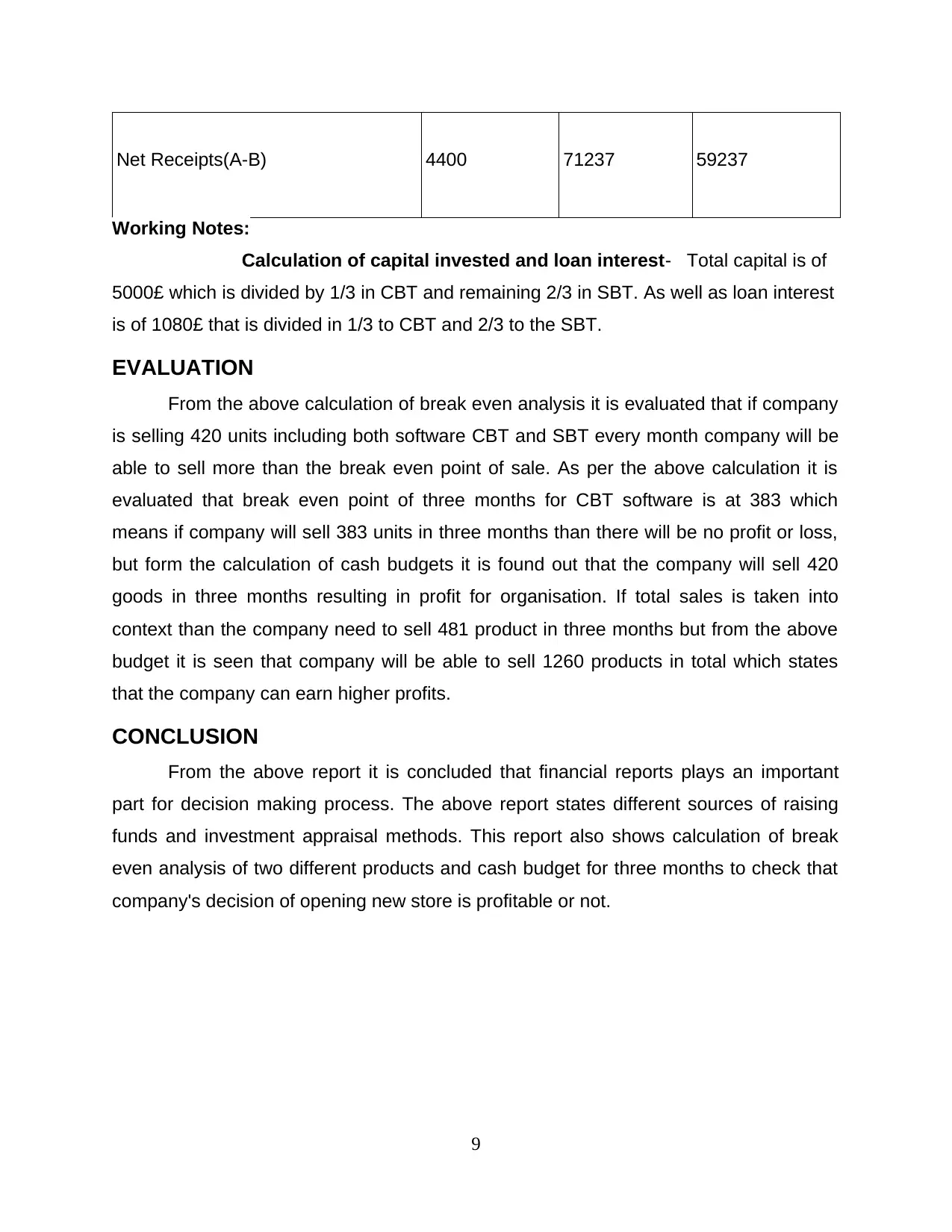

Net Receipts(A-B) 4400 71237 59237

Working Notes:

Calculation of capital invested and loan interest- Total capital is of

5000£ which is divided by 1/3 in CBT and remaining 2/3 in SBT. As well as loan interest

is of 1080£ that is divided in 1/3 to CBT and 2/3 to the SBT.

EVALUATION

From the above calculation of break even analysis it is evaluated that if company

is selling 420 units including both software CBT and SBT every month company will be

able to sell more than the break even point of sale. As per the above calculation it is

evaluated that break even point of three months for CBT software is at 383 which

means if company will sell 383 units in three months than there will be no profit or loss,

but form the calculation of cash budgets it is found out that the company will sell 420

goods in three months resulting in profit for organisation. If total sales is taken into

context than the company need to sell 481 product in three months but from the above

budget it is seen that company will be able to sell 1260 products in total which states

that the company can earn higher profits.

CONCLUSION

From the above report it is concluded that financial reports plays an important

part for decision making process. The above report states different sources of raising

funds and investment appraisal methods. This report also shows calculation of break

even analysis of two different products and cash budget for three months to check that

company's decision of opening new store is profitable or not.

9

Working Notes:

Calculation of capital invested and loan interest- Total capital is of

5000£ which is divided by 1/3 in CBT and remaining 2/3 in SBT. As well as loan interest

is of 1080£ that is divided in 1/3 to CBT and 2/3 to the SBT.

EVALUATION

From the above calculation of break even analysis it is evaluated that if company

is selling 420 units including both software CBT and SBT every month company will be

able to sell more than the break even point of sale. As per the above calculation it is

evaluated that break even point of three months for CBT software is at 383 which

means if company will sell 383 units in three months than there will be no profit or loss,

but form the calculation of cash budgets it is found out that the company will sell 420

goods in three months resulting in profit for organisation. If total sales is taken into

context than the company need to sell 481 product in three months but from the above

budget it is seen that company will be able to sell 1260 products in total which states

that the company can earn higher profits.

CONCLUSION

From the above report it is concluded that financial reports plays an important

part for decision making process. The above report states different sources of raising

funds and investment appraisal methods. This report also shows calculation of break

even analysis of two different products and cash budget for three months to check that

company's decision of opening new store is profitable or not.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.