Comprehensive Financial Analysis Report: Spotless Holding Limited

VerifiedAdded on 2021/04/21

|17

|3334

|68

Report

AI Summary

This report conducts a comprehensive financial analysis of Spotless Holding Limited, evaluating its performance over three years. It begins with an introduction to financial analysis parameters, followed by a detailed examination of profitability using a Modified DuPont Analysis, assessing Return on Equity (ROE) and its components. Investment management is analyzed through working capital ratios, and financial management is evaluated using debt and long-term solvency ratios. The report also assesses the company's sustainable growth rate and provides a cash flow analysis, highlighting key trends and insights. The analysis covers various financial ratios, including gross profit margin, net profit margin, and debt-to-equity ratios, to determine the company's strengths and weaknesses. The conclusion summarizes the overall financial health of Spotless Holding Limited, providing recommendations for improvement.

1

Financial Analysis of the Spotless Holding Limited

Financial Analysis of the Spotless Holding Limited

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Introduction......................................................................................................................................3

Analysis of Financial Performance of ASX 200 Spotlight Group Holdings Limited using the

company results for the last three years...........................................................................................3

Profitability using a Modified DuPont Analysis..........................................................................3

Investment management using Working Capital ratios...............................................................4

Financial management using Debt and Long-term solvency ratios.............................................5

Sustainable growth rate of company............................................................................................5

Cash Flow Analysis.....................................................................................................................6

Conclusion.......................................................................................................................................6

References........................................................................................................................................7

Contents

Introduction......................................................................................................................................3

Analysis of Financial Performance of ASX 200 Spotlight Group Holdings Limited using the

company results for the last three years...........................................................................................3

Profitability using a Modified DuPont Analysis..........................................................................3

Investment management using Working Capital ratios...............................................................4

Financial management using Debt and Long-term solvency ratios.............................................5

Sustainable growth rate of company............................................................................................5

Cash Flow Analysis.....................................................................................................................6

Conclusion.......................................................................................................................................6

References........................................................................................................................................7

3

Introduction

The financial performance analysis of any company is based on multiple parameters such

as profitability analysis, investment analysis, financial management analysis, growth rate and

cash flow analysis. All these parameters decide the actual financial performance of the company

in the particular period. It is important to compare the financial ratios and other financial data

from one period to another in order to make proper financial analysis.

In the present report the financial performance of Spotless Holding Limited has been

evaluated for last three years using the ratio analysis as the main financial tool. Modified DuPont

has been calculated and explained in detailed in order to have greater insight of the breakdown of

return on equity and how it impacts the profitability position of the Spotless Holding Limited. In

addition to this financial analysis report the investment analysis through using the working

capital ratios, financial management using the solvency ratios, growth rate and cash flow

analysis.

Analysis of Financial Performance of ASX 200 Spotlight Group Holdings Limited using the

company results for the last three years

Profitability using a Modified DuPont Analysis

The net income realized by the company in the year 2016 is 14.92% whereas that in the

year 2017 is (55.67%) as depicted from its financial results. The Du Point Analysis helps in

breaking down the ROE (Return on Equity) into three distinct elements that are, profitability,

efficiency and financial leverage. The method is used by the investors for carrying out a

comparison and analysis of the ROE of a company with the historical trends of other companies

Introduction

The financial performance analysis of any company is based on multiple parameters such

as profitability analysis, investment analysis, financial management analysis, growth rate and

cash flow analysis. All these parameters decide the actual financial performance of the company

in the particular period. It is important to compare the financial ratios and other financial data

from one period to another in order to make proper financial analysis.

In the present report the financial performance of Spotless Holding Limited has been

evaluated for last three years using the ratio analysis as the main financial tool. Modified DuPont

has been calculated and explained in detailed in order to have greater insight of the breakdown of

return on equity and how it impacts the profitability position of the Spotless Holding Limited. In

addition to this financial analysis report the investment analysis through using the working

capital ratios, financial management using the solvency ratios, growth rate and cash flow

analysis.

Analysis of Financial Performance of ASX 200 Spotlight Group Holdings Limited using the

company results for the last three years

Profitability using a Modified DuPont Analysis

The net income realized by the company in the year 2016 is 14.92% whereas that in the

year 2017 is (55.67%) as depicted from its financial results. The Du Point Analysis helps in

breaking down the ROE (Return on Equity) into three distinct elements that are, profitability,

efficiency and financial leverage. The method is used by the investors for carrying out a

comparison and analysis of the ROE of a company with the historical trends of other companies

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

(Damodaran, 2011). As evaluated form the financial results of the company, the use of modified

DuPont decomposition of ROE is calculated through the following formula:

ROE=ROA*Adjusted Financial leverage

ROE=ROA*CEL*CSL

o Where ROA is Return on Assets

o CEL is Common earnings leverage

o CSL is Capital structure leverage

The ROE calculated through the application of the above formula is same as that

calculated through the use of regular accounting rules and formula. However, the use of

alternative approach of decomposing profitability is different from that assessed through

modified DuPont. The ROE for the financial year 2016 is 14.77% whereas for that of the year

2017 is (82.56%) calculated through the use of the formula:

ROE=Operating ROA+ Financial Leverage+ Unexpected ROE

The method of DuPont analysis has provided a wider view of the return on equity of the

company. It has highlighted the strengths and areas of improvement of the company. The

analysis method has highlighted that lower ROE of the company in the year 2017 was due to

lower ROA and high financial leverage. The company profitability position in the year 2017 has

decreased significantly in comparison to the year 2016. The analysis method has helped in

identification of the key areas of improvement through the use of DuPont analysis method. The

use of alternative method of DuPont analyses has further helped in gaining detailed information

about the various factors impacting the ROE of the company such as net financial leverage and

unexpected ROE (Brigham, 2011).

(Damodaran, 2011). As evaluated form the financial results of the company, the use of modified

DuPont decomposition of ROE is calculated through the following formula:

ROE=ROA*Adjusted Financial leverage

ROE=ROA*CEL*CSL

o Where ROA is Return on Assets

o CEL is Common earnings leverage

o CSL is Capital structure leverage

The ROE calculated through the application of the above formula is same as that

calculated through the use of regular accounting rules and formula. However, the use of

alternative approach of decomposing profitability is different from that assessed through

modified DuPont. The ROE for the financial year 2016 is 14.77% whereas for that of the year

2017 is (82.56%) calculated through the use of the formula:

ROE=Operating ROA+ Financial Leverage+ Unexpected ROE

The method of DuPont analysis has provided a wider view of the return on equity of the

company. It has highlighted the strengths and areas of improvement of the company. The

analysis method has highlighted that lower ROE of the company in the year 2017 was due to

lower ROA and high financial leverage. The company profitability position in the year 2017 has

decreased significantly in comparison to the year 2016. The analysis method has helped in

identification of the key areas of improvement through the use of DuPont analysis method. The

use of alternative method of DuPont analyses has further helped in gaining detailed information

about the various factors impacting the ROE of the company such as net financial leverage and

unexpected ROE (Brigham, 2011).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

The profitability of the company also impacted by many other financial ratios such as

gross profit ratios, net profit ratio, return on capital employed, and operating profit ratio. So it is

important to discuss them in details for evaluating the profitability position of Spotless Holding

Limited. The gross profit margin of the Spotless Holding Company was 83.88% in year 2016

and it got increased to 84.01% in year 2017. The gross profit margin has not increased as it was

expected to grow in year 2017. The main reason behind the lower increase gross profit margin

was only due to decrease in sales revenue in year 2017 as compared to year 2016. EBIT margin

or operating margin ratio of Spotless Holding Limited was 6.54% in year 2016 and it got

decreased to -9.88% in year 2017. The possible reason behind such change was decrease in sales

and increase in other expenses in year 2017 as compared to year 2016. So it can be said that

profitability position of Spotless Holding Limited was poor in year 2017 as compared to

profitability performance in year 2016. The net profit margin has been worst impacted due to

poor profitability performance of the company in year 2017. The net profit margin was positive

3.8% in year 2016 but it got reduced to negative 11.6% in year 2017 (Davies and Crawford,

2011). It means company has suffered a major loss in year 2017 and the possible reason for

decrease in net profit ratio was due to improper handling of expenses, no proper planning of

sales forecast and poor sales in year 2017. So, at conclusion it can be said that the profitability

position of the company was not up to the mark as it was expected by the company in year 2017.

While, profitability performance of Spotless Holding Limited was far better as compared with

other year financial performance.

Investment management using Working Capital ratios

The analysis of the working capital ratios of a company helps in determining its

investment position and thus supports the decision-making process of the investors. The working

The profitability of the company also impacted by many other financial ratios such as

gross profit ratios, net profit ratio, return on capital employed, and operating profit ratio. So it is

important to discuss them in details for evaluating the profitability position of Spotless Holding

Limited. The gross profit margin of the Spotless Holding Company was 83.88% in year 2016

and it got increased to 84.01% in year 2017. The gross profit margin has not increased as it was

expected to grow in year 2017. The main reason behind the lower increase gross profit margin

was only due to decrease in sales revenue in year 2017 as compared to year 2016. EBIT margin

or operating margin ratio of Spotless Holding Limited was 6.54% in year 2016 and it got

decreased to -9.88% in year 2017. The possible reason behind such change was decrease in sales

and increase in other expenses in year 2017 as compared to year 2016. So it can be said that

profitability position of Spotless Holding Limited was poor in year 2017 as compared to

profitability performance in year 2016. The net profit margin has been worst impacted due to

poor profitability performance of the company in year 2017. The net profit margin was positive

3.8% in year 2016 but it got reduced to negative 11.6% in year 2017 (Davies and Crawford,

2011). It means company has suffered a major loss in year 2017 and the possible reason for

decrease in net profit ratio was due to improper handling of expenses, no proper planning of

sales forecast and poor sales in year 2017. So, at conclusion it can be said that the profitability

position of the company was not up to the mark as it was expected by the company in year 2017.

While, profitability performance of Spotless Holding Limited was far better as compared with

other year financial performance.

Investment management using Working Capital ratios

The analysis of the working capital ratios of a company helps in determining its

investment position and thus supports the decision-making process of the investors. The working

6

capital ratios provided an evaluation of the cash position, inventory, accounts receivable and

payable and its ability in meeting the short as well as long-term obligations. As analyzed from

the working capital ratios of the company for the last three years it can be said that its proportion

of cash utilization for generating sale sis increasing and this indicates weakness of the company

in cash management. The receivable turnover is decreasing which indicates its efficiency to

collects its accounts receivable has decreased which is not a good sign for the company. The

company efficiency to use fixed assets for generating sales is also showing sign of negative

growth over the last three years. Therefore, it can be said on the basis of analysis of working

capital ratios of the company that its investment management is not proper and it should adopt

adequate measures for managing its current assets and liabilities (Brealey et al., 2012).

It is depicted from the comparison of asset turnover ratios for the year 2017 in

comparison to the year 2016 that the company efficiency to realize sales from the use of assets is

decreasing. This is mainly due to decrease in the sales revenue generated by the company as such

the total assets turnover as well as fixed asset turnover ratios have shown a significant decrease

in the year 2017 as compared to the year 2016. The company inventory turnover ratio has also

decreased considerably in the year 2017 depicting that its ability to manage inventory is not good

and there is significant reduction in its efficiency to generate revenue from selling the inventory.

The increase in the current liabilities of the company is largely responsible for reducing its

working capital turnover ratio in the year 2017 as compared to the year 2016. Its efficiency to

pay its suppliers has also been decreased in the year 2017 as indicated from its accounts payable

turnover ratio. This further is a sign of worsening financial condition of the company can cause

loss of trust from the suppliers in long-term. As such, it can be regarded in general that working

capital management in the company is not sound because there is increase in its current

capital ratios provided an evaluation of the cash position, inventory, accounts receivable and

payable and its ability in meeting the short as well as long-term obligations. As analyzed from

the working capital ratios of the company for the last three years it can be said that its proportion

of cash utilization for generating sale sis increasing and this indicates weakness of the company

in cash management. The receivable turnover is decreasing which indicates its efficiency to

collects its accounts receivable has decreased which is not a good sign for the company. The

company efficiency to use fixed assets for generating sales is also showing sign of negative

growth over the last three years. Therefore, it can be said on the basis of analysis of working

capital ratios of the company that its investment management is not proper and it should adopt

adequate measures for managing its current assets and liabilities (Brealey et al., 2012).

It is depicted from the comparison of asset turnover ratios for the year 2017 in

comparison to the year 2016 that the company efficiency to realize sales from the use of assets is

decreasing. This is mainly due to decrease in the sales revenue generated by the company as such

the total assets turnover as well as fixed asset turnover ratios have shown a significant decrease

in the year 2017 as compared to the year 2016. The company inventory turnover ratio has also

decreased considerably in the year 2017 depicting that its ability to manage inventory is not good

and there is significant reduction in its efficiency to generate revenue from selling the inventory.

The increase in the current liabilities of the company is largely responsible for reducing its

working capital turnover ratio in the year 2017 as compared to the year 2016. Its efficiency to

pay its suppliers has also been decreased in the year 2017 as indicated from its accounts payable

turnover ratio. This further is a sign of worsening financial condition of the company can cause

loss of trust from the suppliers in long-term. As such, it can be regarded in general that working

capital management in the company is not sound because there is increase in its current

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

obligations and decrease in the current assets. This is a point of major concern for the company

as it can negatively impact its sustainable growth and development. As depicted from the results

of the various working capital ratios, the company is not able to manage its inventories, accounts

receivable and payable and cash (Lumby and Jones, 2007). The inefficiency of the company to

repay its increasing debts can cause the service providers to stop providing services to the

company. It can also lead to the occurrence of situation of bankruptcy for the company if it is not

able to meet its obligations in the long-term.

Financial management using Debt and Long-term solvency ratios

The analysis of the debt and solvency ratios will help in assessing the financial

strengths and weakness of the company and thus identifying its financial position. As analyzed

from its liquidity ratios, the ability of the company to meet its current obligations with the

current assets has decreased over the selected financial period of time. The current, quick, cash

and operating cash flow ratios all have significantly decreased in the year 2017 as compared to

the year 2016. The debt position of the company have also increased in the year 2017 as can be

analyzed from its debt-to-equity,, debt to capital, net debt to equity and interest coverage ratios.

Debt to equity ratios was 1.020 times in year 2016 and it got increase 2.016 times in year 2017

that indicates there has been considerable increase in debt capital. The increase in debt capital

shows the poor capital structure of the company (Ross, Jaffe and Kakani, 2008).

As such, it can be said that the financial management of the company is not adequate

because its solvency position is declining with increase in its debt level. The company is

increasing its debt level while its position to meet its debt obligations is decreasing. As such, it

needs to place large emphasis on its capital structuring through maintaining an appropriate

obligations and decrease in the current assets. This is a point of major concern for the company

as it can negatively impact its sustainable growth and development. As depicted from the results

of the various working capital ratios, the company is not able to manage its inventories, accounts

receivable and payable and cash (Lumby and Jones, 2007). The inefficiency of the company to

repay its increasing debts can cause the service providers to stop providing services to the

company. It can also lead to the occurrence of situation of bankruptcy for the company if it is not

able to meet its obligations in the long-term.

Financial management using Debt and Long-term solvency ratios

The analysis of the debt and solvency ratios will help in assessing the financial

strengths and weakness of the company and thus identifying its financial position. As analyzed

from its liquidity ratios, the ability of the company to meet its current obligations with the

current assets has decreased over the selected financial period of time. The current, quick, cash

and operating cash flow ratios all have significantly decreased in the year 2017 as compared to

the year 2016. The debt position of the company have also increased in the year 2017 as can be

analyzed from its debt-to-equity,, debt to capital, net debt to equity and interest coverage ratios.

Debt to equity ratios was 1.020 times in year 2016 and it got increase 2.016 times in year 2017

that indicates there has been considerable increase in debt capital. The increase in debt capital

shows the poor capital structure of the company (Ross, Jaffe and Kakani, 2008).

As such, it can be said that the financial management of the company is not adequate

because its solvency position is declining with increase in its debt level. The company is

increasing its debt level while its position to meet its debt obligations is decreasing. As such, it

needs to place large emphasis on its capital structuring through maintaining an appropriate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

balance between debt and equity and improving its liquidity position (Vernimmen and Quiry,

2009).

Sustainable growth rate of company

The sustainable growth rate of a company refers to the maximum growth rate a business

can achieve without increasing its financial leverage or debt sources of funds. It can be regarded

to the maximum growth achieved by a company on the basis of its asset utilization, debt position

and dividend payout. The sustainable growth rate as calculated for the Spotlight Group Holdings

Limited on the basis of its profitability position and dividend payout ratio is negative for the year

2017. Therefore, it can be said that the company ability to continue its sustainable growth is

diminishing due to increase in its debt level, profitability level and dividend generated for the

shareholders. The company if not able to maintain the interests of the shareholders through

providing them higher returns on the equity invested then its ability to sustain in the long-term is

doubtful. The company needs to restructure its financial operations and take critical decisions for

achieving sustainable growth and development (Brealey et al., 2012).

Cash Flow Analysis

The cash flow analysis helps in determining the cash inflow and outflow incurred by a

company over a specified period of time. There is increase in cash flow from operations in year

2017 as compared to year 2016 by $48900. There is decrease in dividend payment in year 2017

as compared to year 2016. It can be said that cash flow position of the company is much better

than in year 2017 as compared to year 2016. There has been considerable rise in the cash balance

that is maintained for the equity capital. The cash balance maintained for the equity buyback has

balance between debt and equity and improving its liquidity position (Vernimmen and Quiry,

2009).

Sustainable growth rate of company

The sustainable growth rate of a company refers to the maximum growth rate a business

can achieve without increasing its financial leverage or debt sources of funds. It can be regarded

to the maximum growth achieved by a company on the basis of its asset utilization, debt position

and dividend payout. The sustainable growth rate as calculated for the Spotlight Group Holdings

Limited on the basis of its profitability position and dividend payout ratio is negative for the year

2017. Therefore, it can be said that the company ability to continue its sustainable growth is

diminishing due to increase in its debt level, profitability level and dividend generated for the

shareholders. The company if not able to maintain the interests of the shareholders through

providing them higher returns on the equity invested then its ability to sustain in the long-term is

doubtful. The company needs to restructure its financial operations and take critical decisions for

achieving sustainable growth and development (Brealey et al., 2012).

Cash Flow Analysis

The cash flow analysis helps in determining the cash inflow and outflow incurred by a

company over a specified period of time. There is increase in cash flow from operations in year

2017 as compared to year 2016 by $48900. There is decrease in dividend payment in year 2017

as compared to year 2016. It can be said that cash flow position of the company is much better

than in year 2017 as compared to year 2016. There has been considerable rise in the cash balance

that is maintained for the equity capital. The cash balance maintained for the equity buyback has

9

been increased from 48300 thousand dollars in year 2016 to 81000 thousand dollars in year

2017. It means company can buyback more equity shares in the current year. The same increase

can be seen for the cash flow available for the debt payback. It means company has made the

changes in cash collection policy and also in cash expenditure policies. Due to such changes the

cash flow position was much better in year 2017 as compared to cash flow position in year 2016

(Moles and Kidwekk, 2011).

Conclusion

On the basis of overall financial analysis of Spotless Holding Limited for last three years

it can be said that company has shown very poor financial performance as compared with the

performance in year 2016. Spotless has suffered major loss in year 2017 due to poor

management strategies and performance. The budgets are not properly followed that give rise to

increase in unnecessary expenses and ultimately it ends with loss in year 2017. The cash flow

position was remarkably good in year 2017 as compared to year 2016 due to some changes in

cash policies made by the company in last year.

been increased from 48300 thousand dollars in year 2016 to 81000 thousand dollars in year

2017. It means company can buyback more equity shares in the current year. The same increase

can be seen for the cash flow available for the debt payback. It means company has made the

changes in cash collection policy and also in cash expenditure policies. Due to such changes the

cash flow position was much better in year 2017 as compared to cash flow position in year 2016

(Moles and Kidwekk, 2011).

Conclusion

On the basis of overall financial analysis of Spotless Holding Limited for last three years

it can be said that company has shown very poor financial performance as compared with the

performance in year 2016. Spotless has suffered major loss in year 2017 due to poor

management strategies and performance. The budgets are not properly followed that give rise to

increase in unnecessary expenses and ultimately it ends with loss in year 2017. The cash flow

position was remarkably good in year 2017 as compared to year 2016 due to some changes in

cash policies made by the company in last year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

References

Brealey, R. et al. 2012. Principles of Corporate Finance. Tata McGraw-Hill Education.

Brigham, E. 2011. Financial Management Theory and Practice. Atlantic Publishers & Distri.

Damodaran, A, 2011. Applied corporate finance. John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Lumby,S and Jones,C. 2007. Corporate finance theory & practice. Thomson.

Moles, P. and Kidwekk, D. 2011. Corporate finance. John Wiley &sons.

Ross, A., Jaffe, J. and Kakani, R.K. 2008. Corporate Finance. Pearson.

Vernimmen, P. and Quiry, P. 2009. Corporate Finance: Theory and Practice. John Wiley &

Sons.

References

Brealey, R. et al. 2012. Principles of Corporate Finance. Tata McGraw-Hill Education.

Brigham, E. 2011. Financial Management Theory and Practice. Atlantic Publishers & Distri.

Damodaran, A, 2011. Applied corporate finance. John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Lumby,S and Jones,C. 2007. Corporate finance theory & practice. Thomson.

Moles, P. and Kidwekk, D. 2011. Corporate finance. John Wiley &sons.

Ross, A., Jaffe, J. and Kakani, R.K. 2008. Corporate Finance. Pearson.

Vernimmen, P. and Quiry, P. 2009. Corporate Finance: Theory and Practice. John Wiley &

Sons.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Appendix

Measuring overall profitability

Data items and ratio

Spotless

2017 Spotless 2016

Net income ($'000) -347,400 122,200

Average shareholders' equity ($'000) 624050 818850

Return on equity -55.67% 14.92%

Modified DuPont decomposition of

ROE

Values:

Sales 3,006,300

3,176,10

0

Interest expense -44,000 -40,400

Interest income 500 500

Net interest expense (income) -43,500 -39,900

Minority interest ($'000) 0 0

Average total assets ($'000) 2,076,450

2,147,80

0

Preferred dividends 0 0

Calculation:

Profit margin (PM) -10.54% 4.73%

Asset turnover (AT) 1.45 1.48

Appendix

Measuring overall profitability

Data items and ratio

Spotless

2017 Spotless 2016

Net income ($'000) -347,400 122,200

Average shareholders' equity ($'000) 624050 818850

Return on equity -55.67% 14.92%

Modified DuPont decomposition of

ROE

Values:

Sales 3,006,300

3,176,10

0

Interest expense -44,000 -40,400

Interest income 500 500

Net interest expense (income) -43,500 -39,900

Minority interest ($'000) 0 0

Average total assets ($'000) 2,076,450

2,147,80

0

Preferred dividends 0 0

Calculation:

Profit margin (PM) -10.54% 4.73%

Asset turnover (AT) 1.45 1.48

12

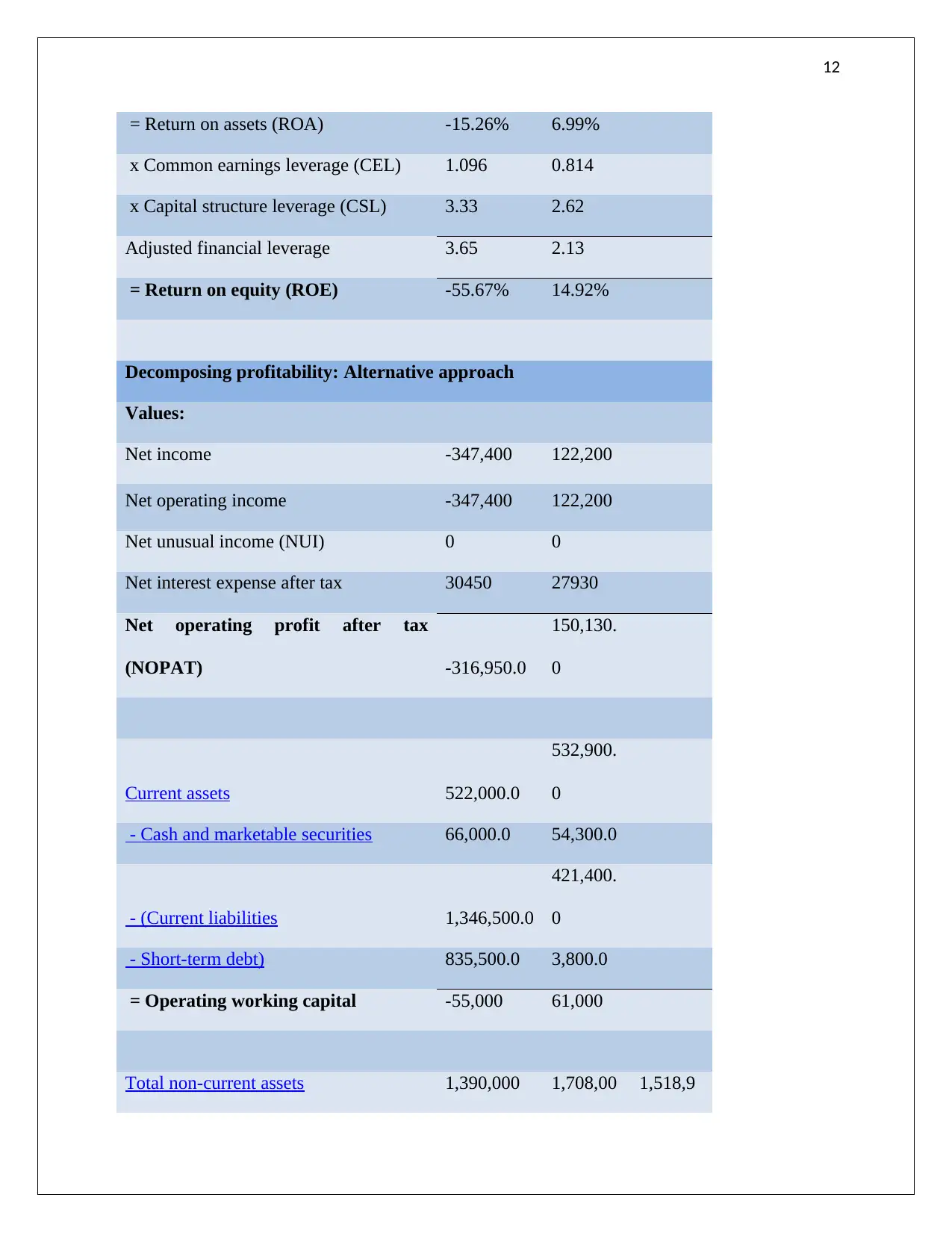

= Return on assets (ROA) -15.26% 6.99%

x Common earnings leverage (CEL) 1.096 0.814

x Capital structure leverage (CSL) 3.33 2.62

Adjusted financial leverage 3.65 2.13

= Return on equity (ROE) -55.67% 14.92%

Decomposing profitability: Alternative approach

Values:

Net income -347,400 122,200

Net operating income -347,400 122,200

Net unusual income (NUI) 0 0

Net interest expense after tax 30450 27930

Net operating profit after tax

(NOPAT) -316,950.0

150,130.

0

Current assets 522,000.0

532,900.

0

- Cash and marketable securities 66,000.0 54,300.0

- (Current liabilities 1,346,500.0

421,400.

0

- Short-term debt) 835,500.0 3,800.0

= Operating working capital -55,000 61,000

Total non-current assets 1,390,000 1,708,00 1,518,9

= Return on assets (ROA) -15.26% 6.99%

x Common earnings leverage (CEL) 1.096 0.814

x Capital structure leverage (CSL) 3.33 2.62

Adjusted financial leverage 3.65 2.13

= Return on equity (ROE) -55.67% 14.92%

Decomposing profitability: Alternative approach

Values:

Net income -347,400 122,200

Net operating income -347,400 122,200

Net unusual income (NUI) 0 0

Net interest expense after tax 30450 27930

Net operating profit after tax

(NOPAT) -316,950.0

150,130.

0

Current assets 522,000.0

532,900.

0

- Cash and marketable securities 66,000.0 54,300.0

- (Current liabilities 1,346,500.0

421,400.

0

- Short-term debt) 835,500.0 3,800.0

= Operating working capital -55,000 61,000

Total non-current assets 1,390,000 1,708,00 1,518,9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.