Cox Electric Profit Calculation: Spreadsheet Model & Data Analysis

VerifiedAdded on 2022/09/27

|7

|1000

|22

Homework Assignment

AI Summary

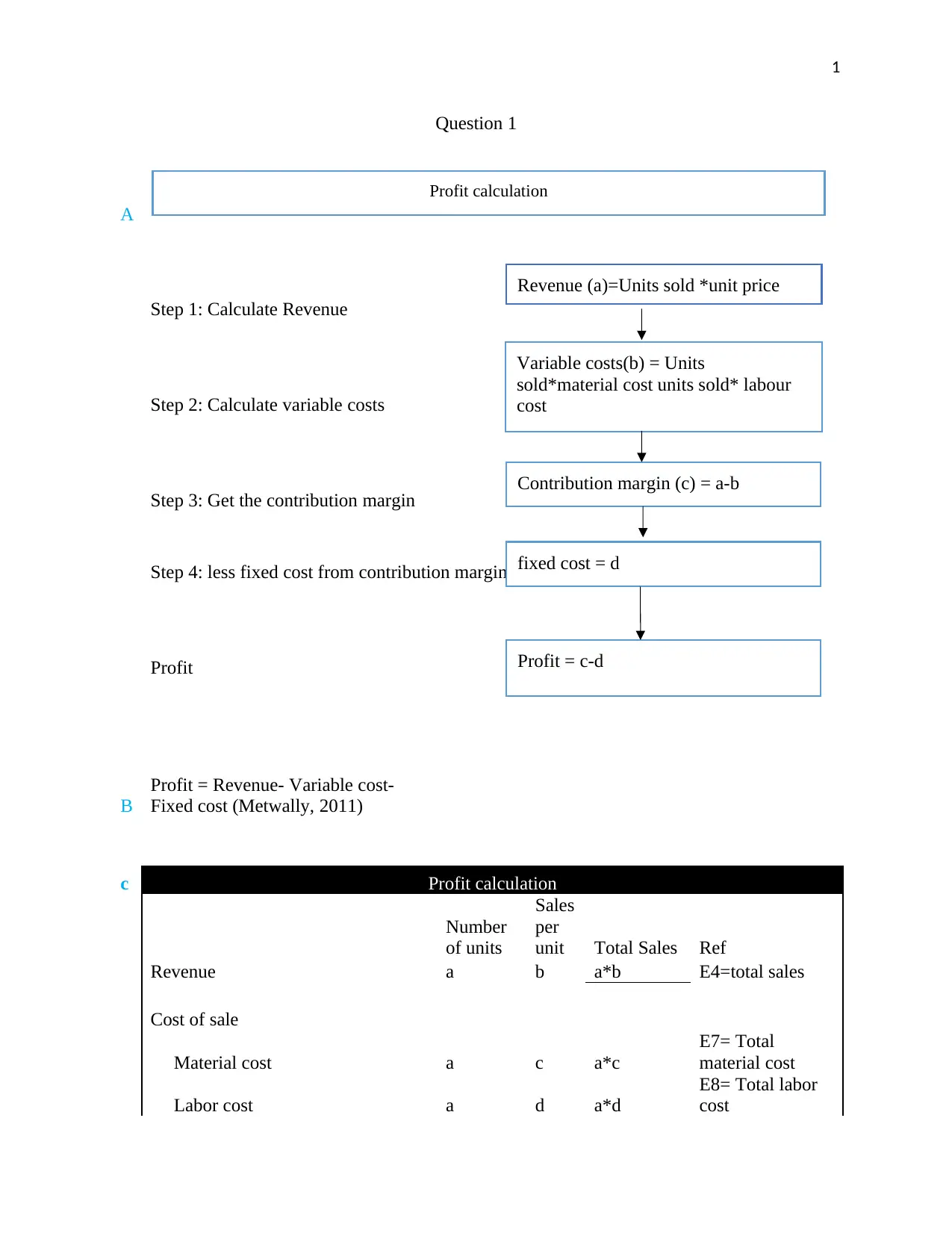

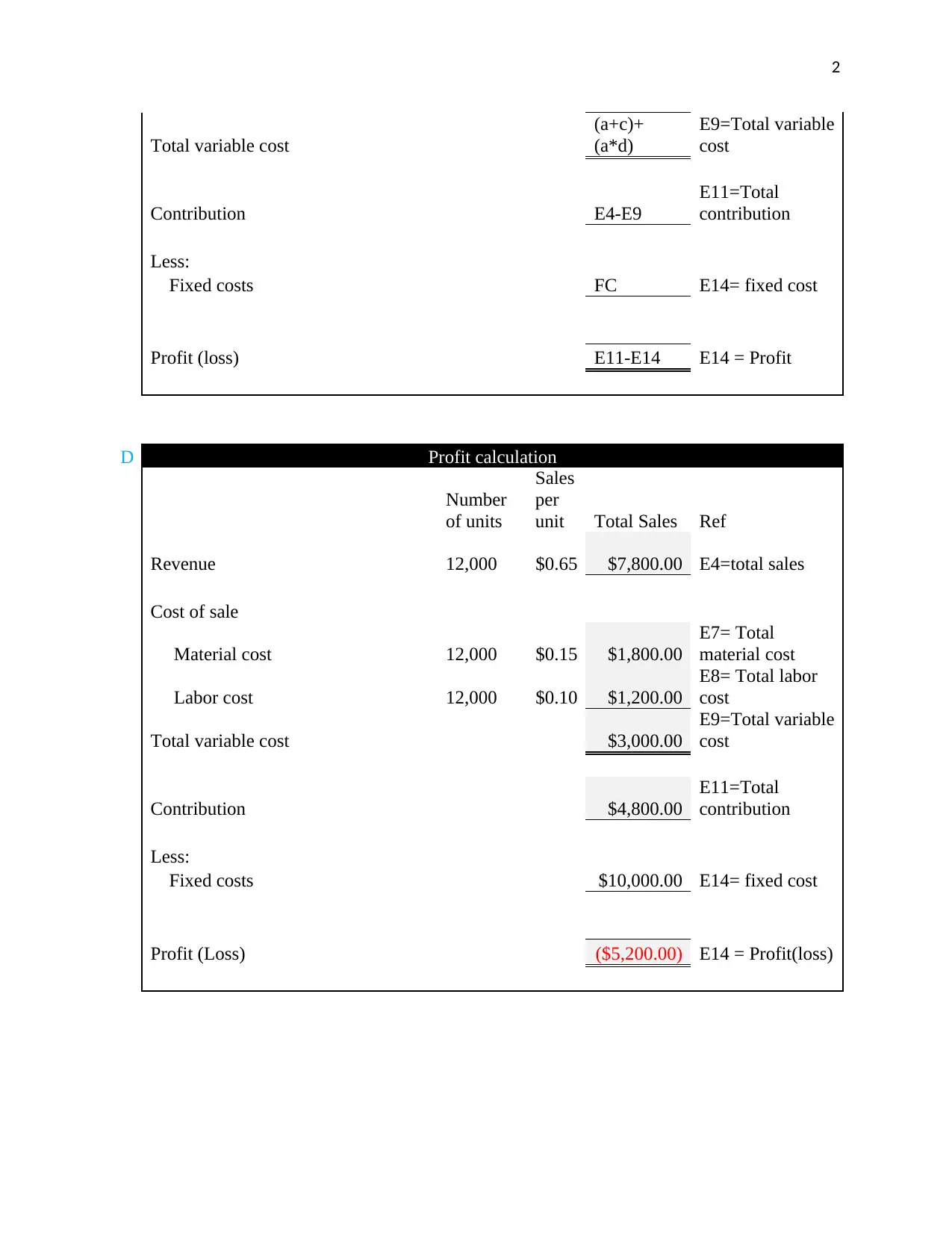

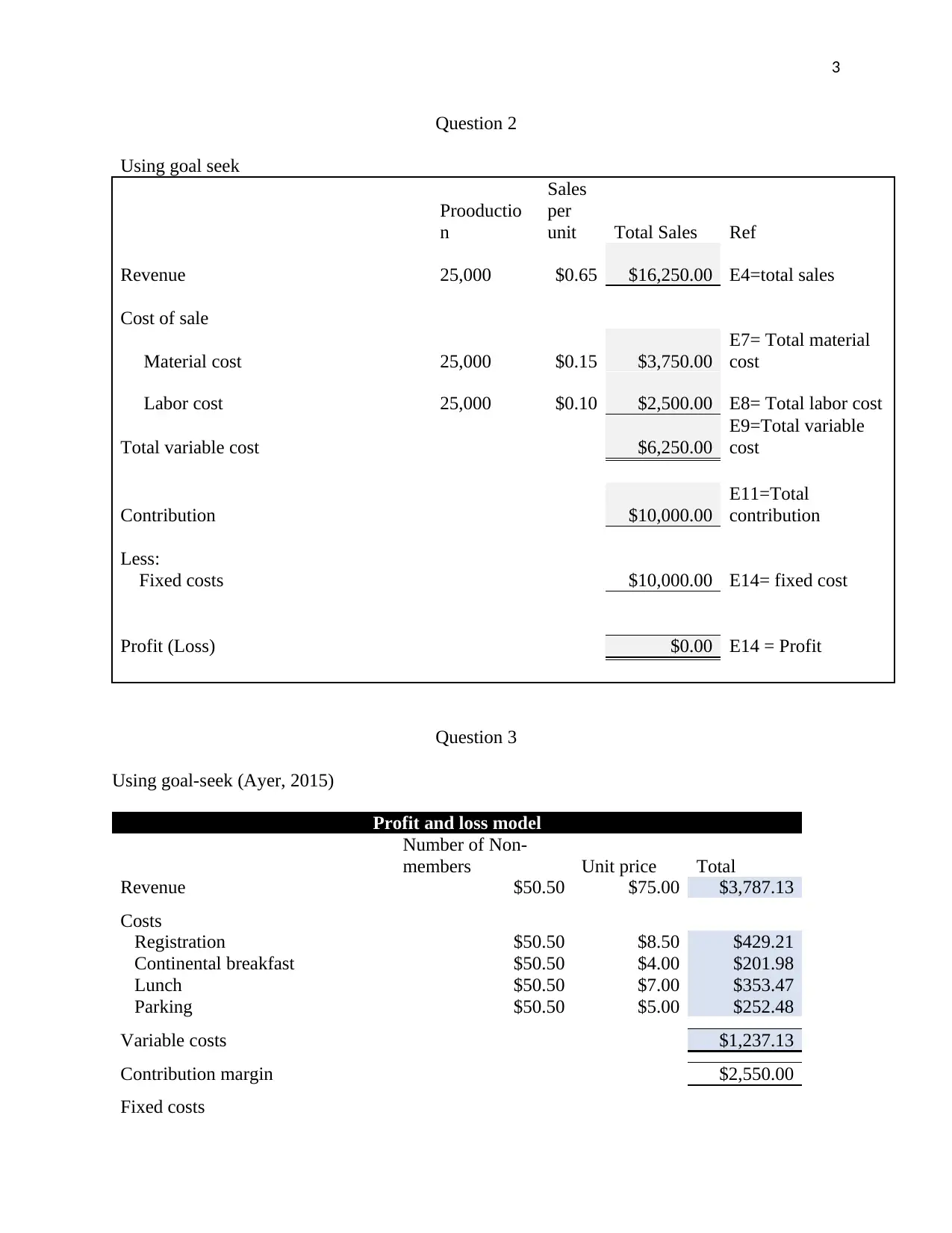

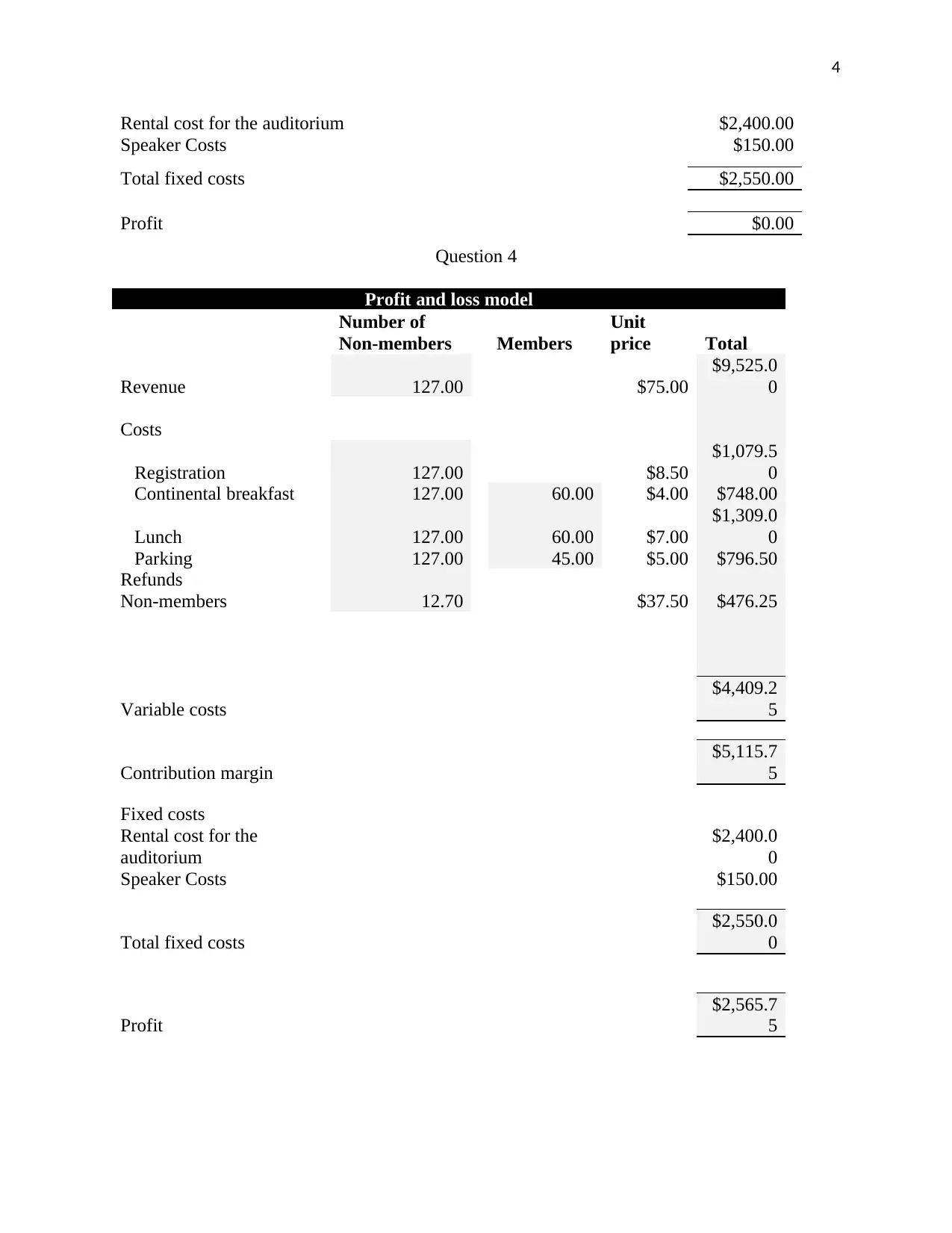

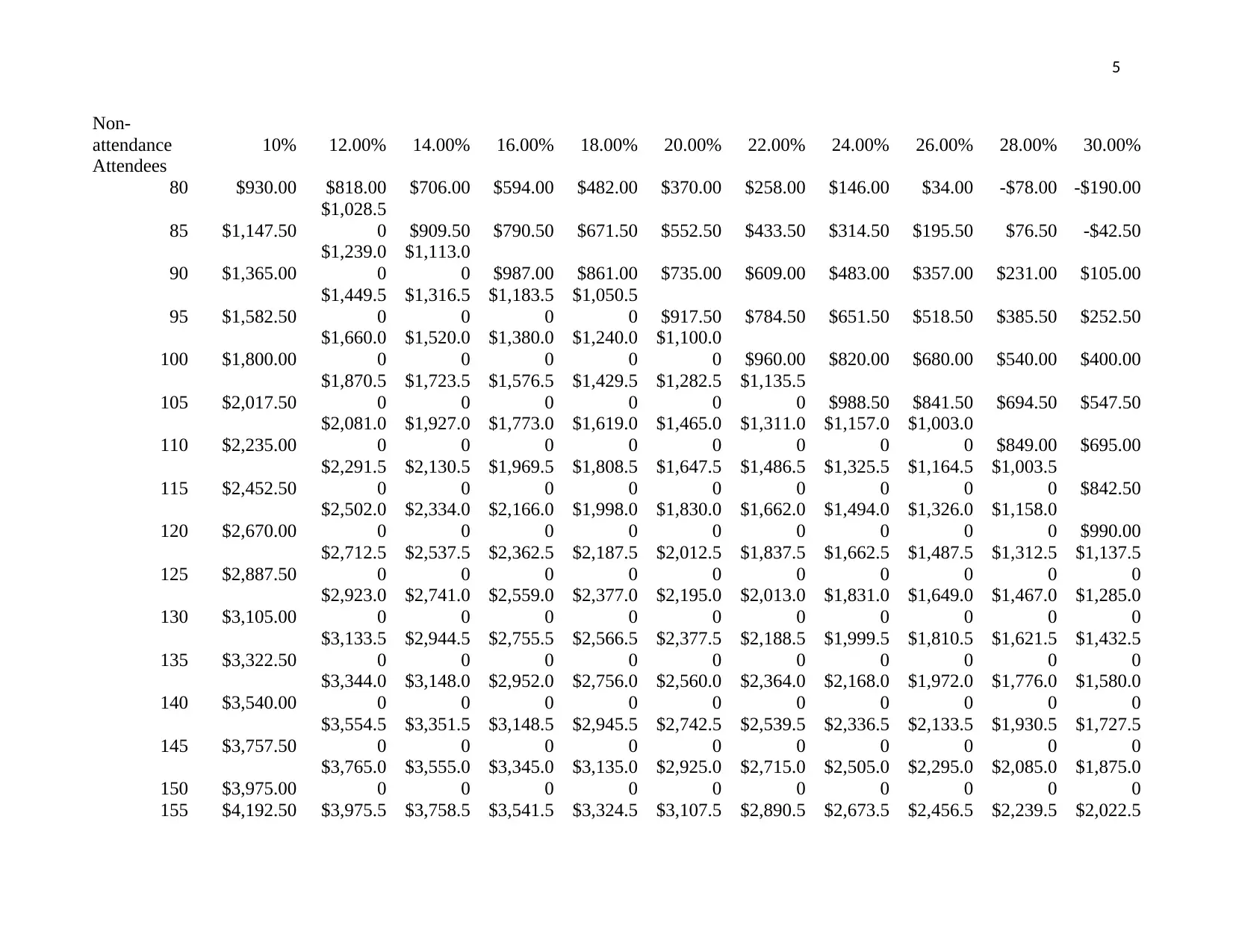

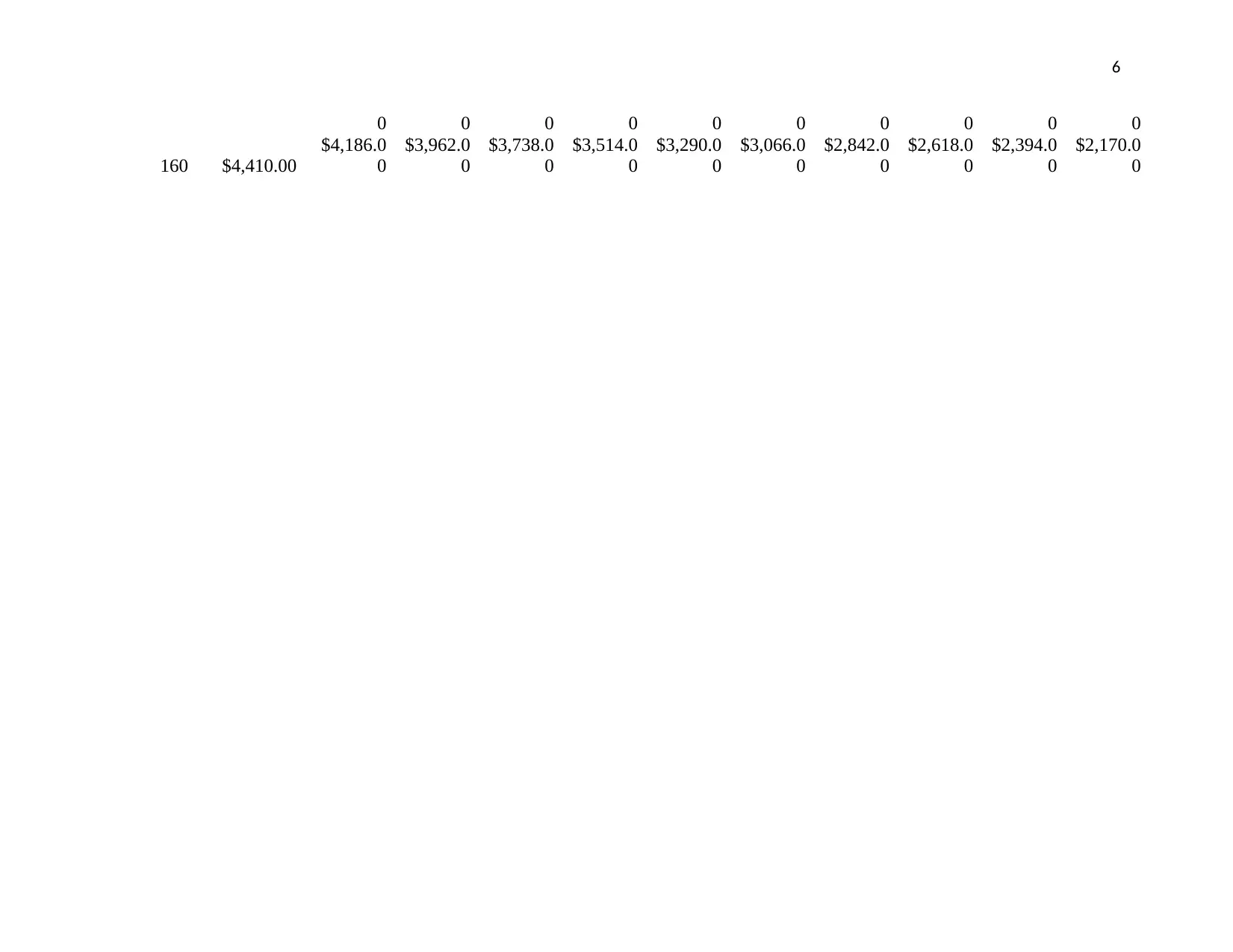

This assignment solution addresses profit calculation using spreadsheet modeling techniques, focusing on a case study involving Cox Electric. The solution begins with the fundamental formulas for calculating revenue, variable costs, contribution margin, and profit, including step-by-step instructions. The assignment then uses an Excel model to calculate profit for a given production volume of 12,000 units. Furthermore, the solution demonstrates the use of Goal Seek to determine production levels needed to achieve a break-even point and analyze the profit and loss model. The assignment also explores the impact of variable costs and fixed costs on profitability, along with the use of data tables to analyze profit across varying production volumes and attendance rates. The solution includes references to relevant academic sources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.