Taxation Law Case Study: Spriggs v Federal Commissioner of Taxation

VerifiedAdded on 2023/05/31

|12

|1027

|463

Case Study

AI Summary

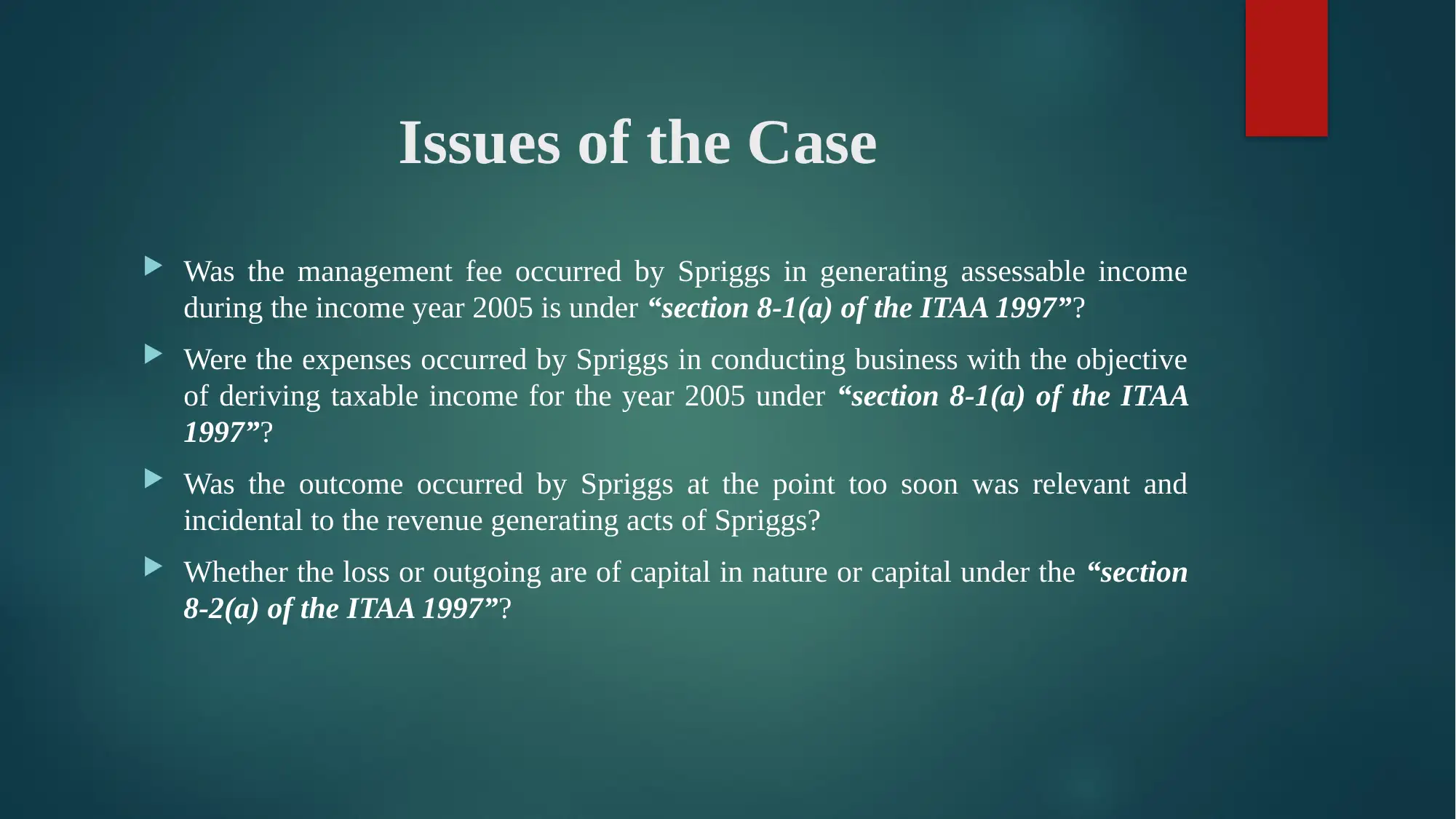

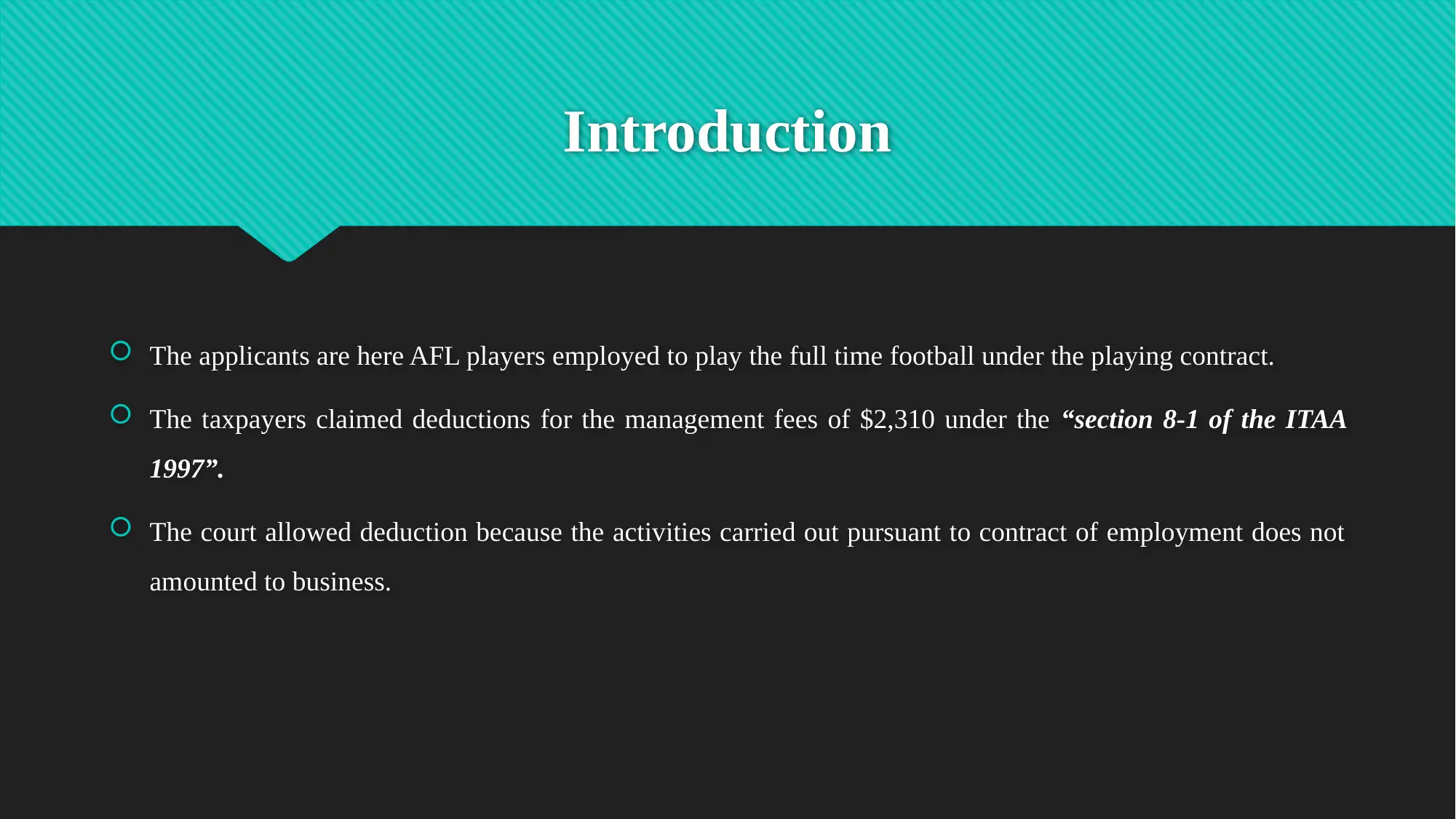

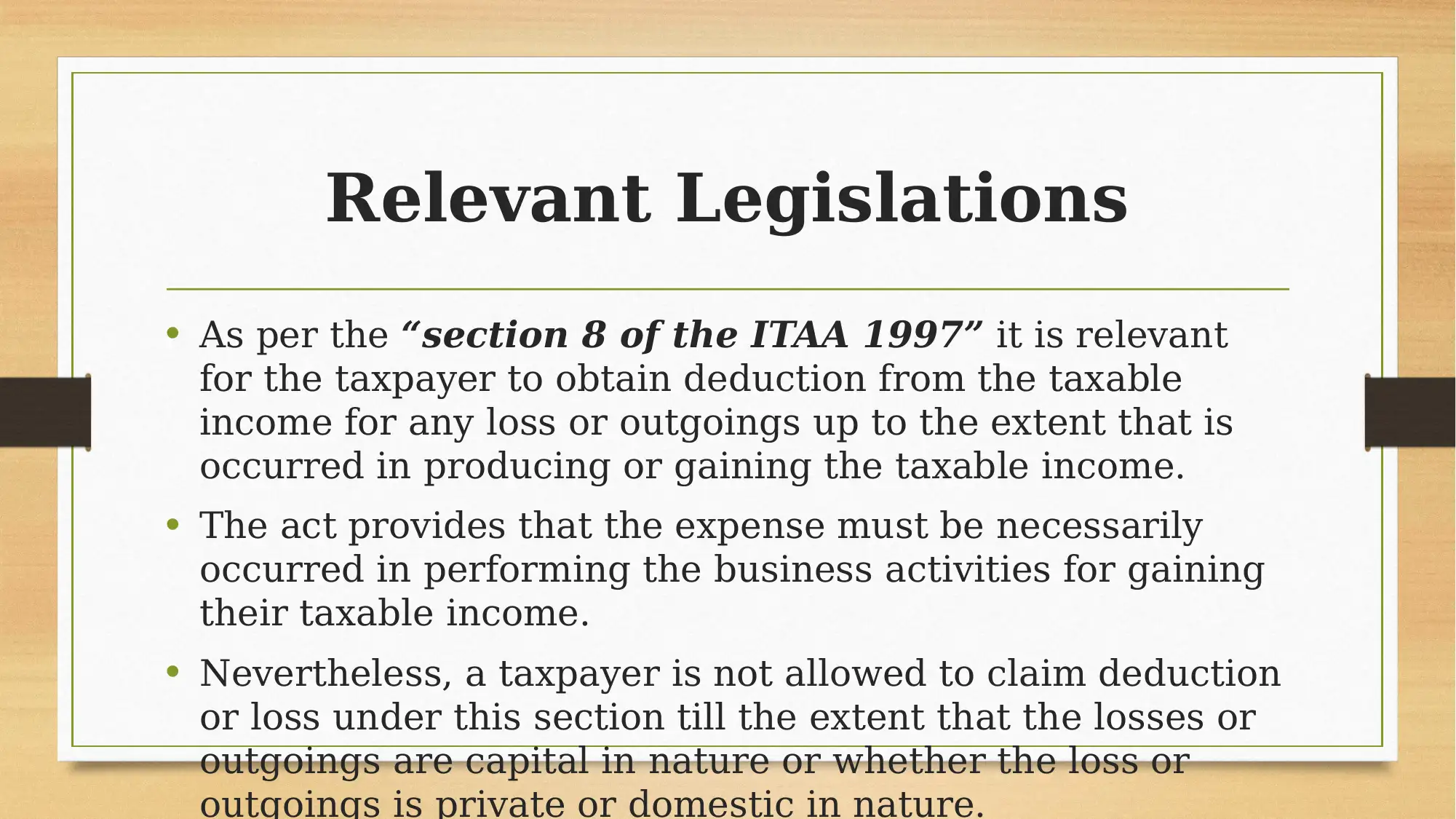

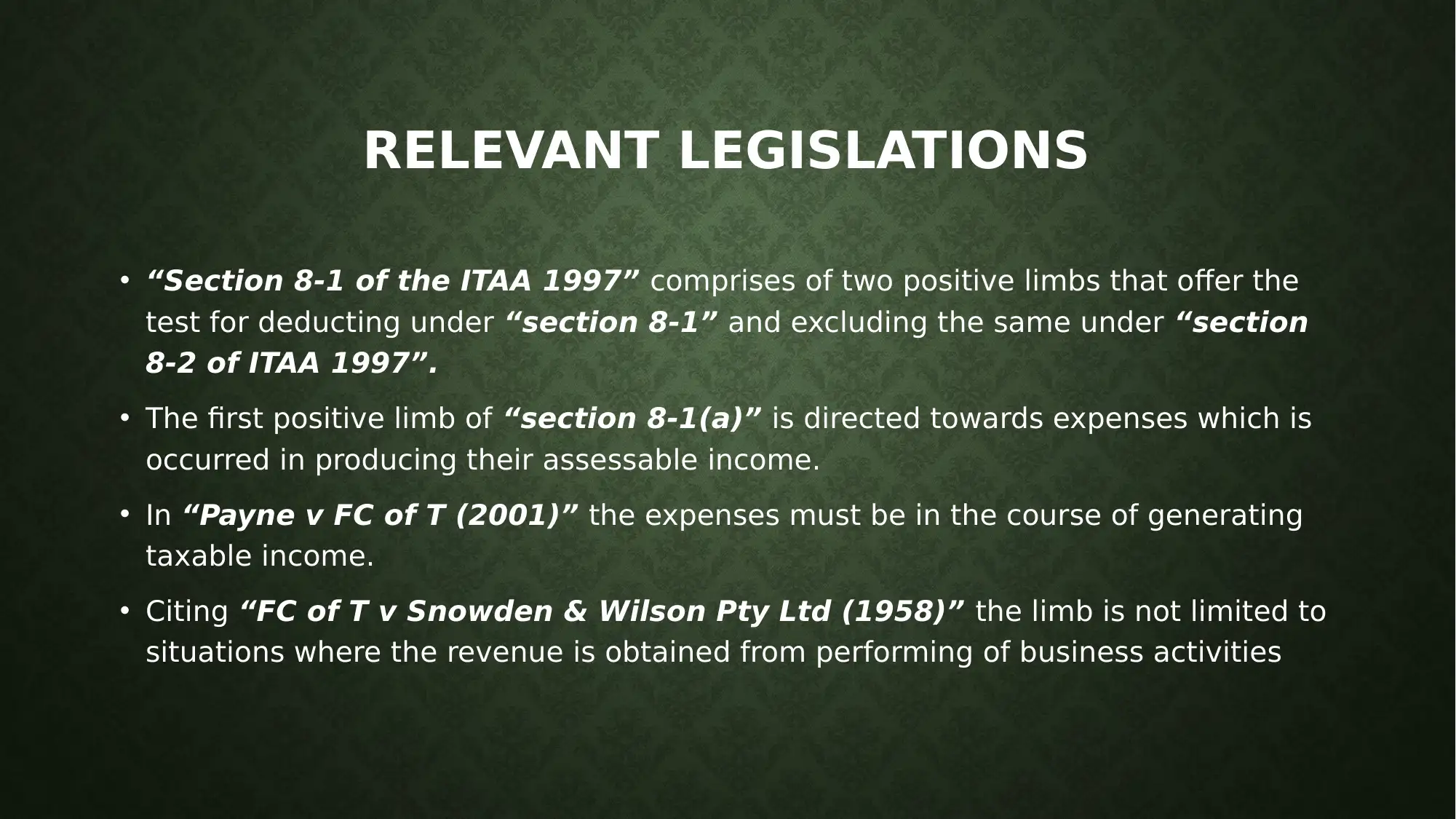

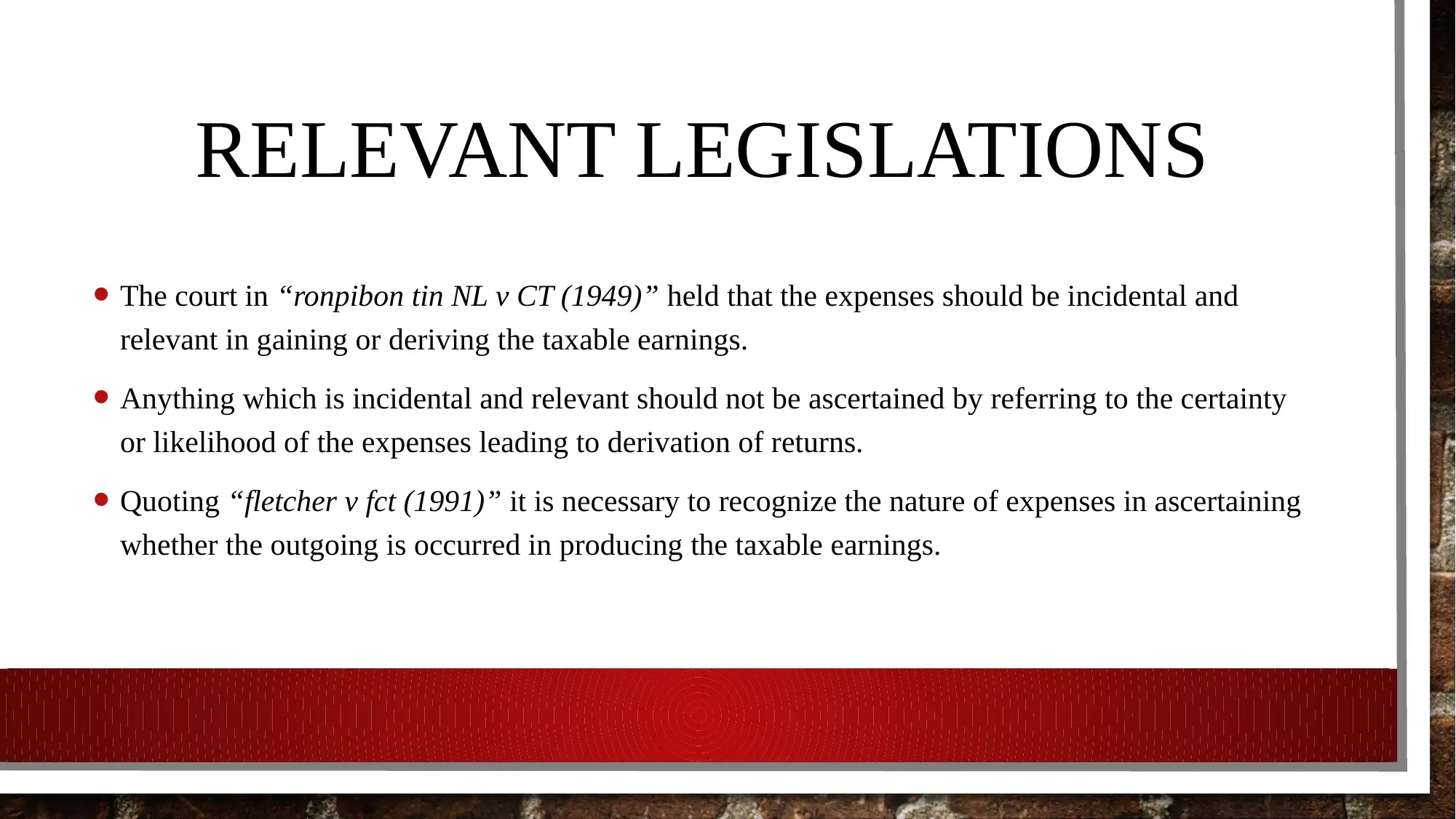

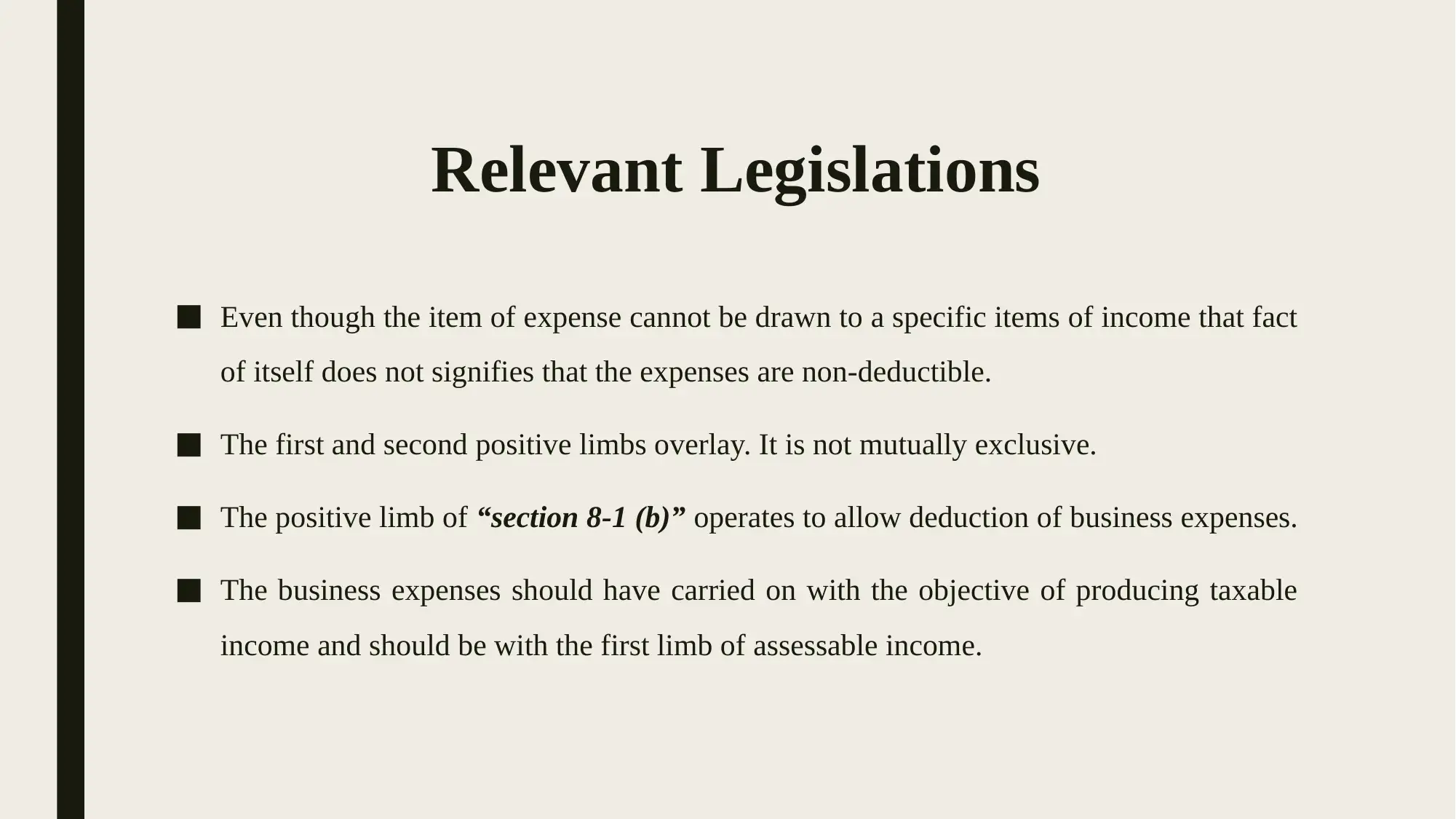

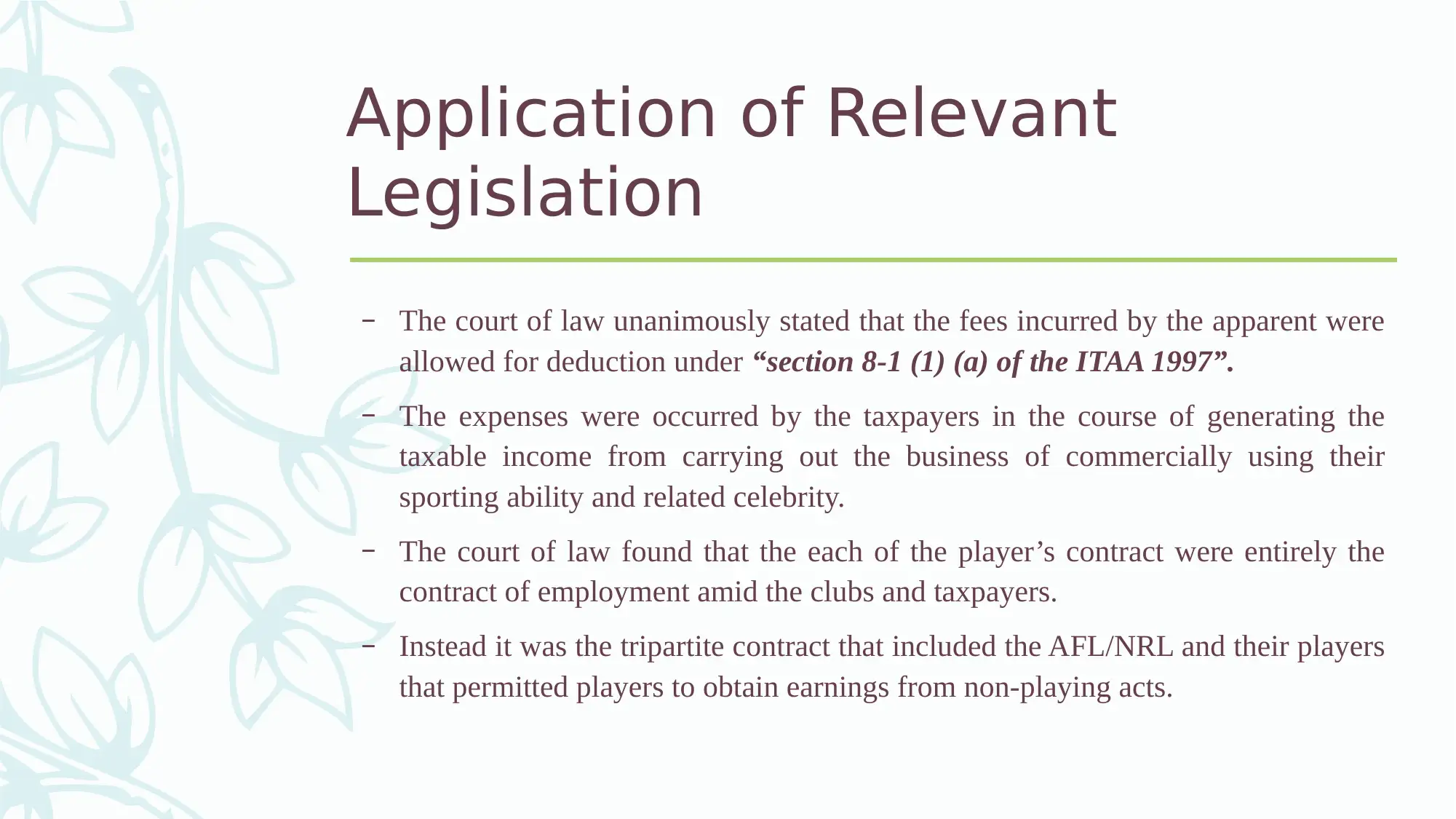

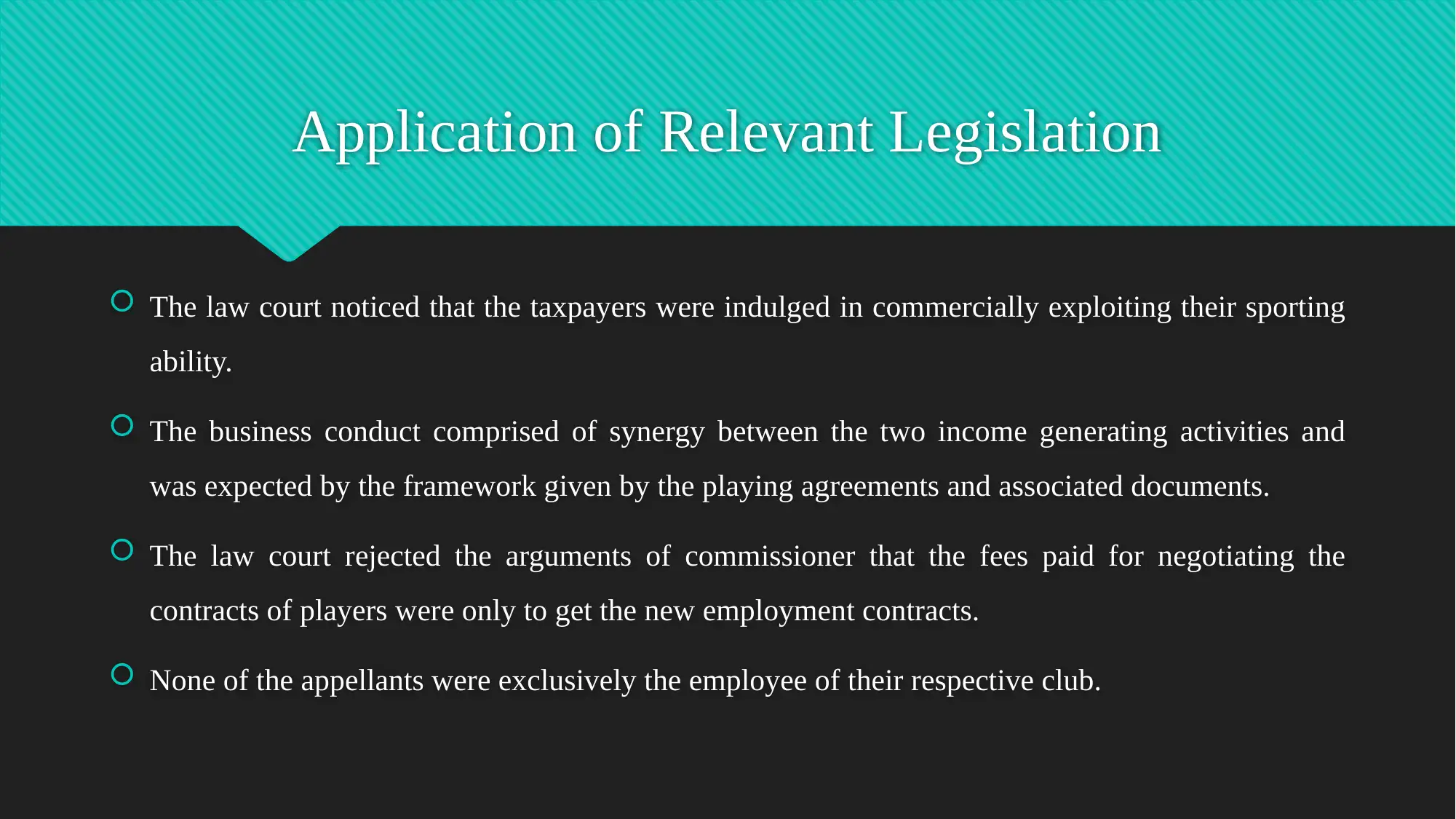

This case study analyzes the Spriggs v Federal Commissioner of Taxation [2007] case, focusing on the deductibility of management fees claimed by AFL players under section 8-1(a) of the ITAA 1997. The central issues revolve around whether the management fees and other expenses incurred in generating assessable income were deductible, whether the expenses were incidental to revenue generation, and if the expenses were capital in nature. The court determined that the management fees were deductible as they were incurred in the course of generating taxable income from the players' sporting activities and related commercial ventures. The court found that the players' contracts were employment contracts but also allowed for earnings from non-playing activities, and that the management fees were necessarily incurred in conducting their business activities. The analysis considers relevant legislation, including section 8-1 and 8-2 of the ITAA 1997, and highlights the court's rejection of the Commissioner's arguments regarding the nature of the expenses.

1 out of 12

Related Documents

![Taxation Law: Spriggs v Federal Commissioner of Taxation [2007]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fdocument%2Fpages%2Fspriggs-taxation-law-case-page-2.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.