SPSS Regression and Time Series Analysis

VerifiedAdded on 2020/02/03

|17

|2272

|298

Report

AI Summary

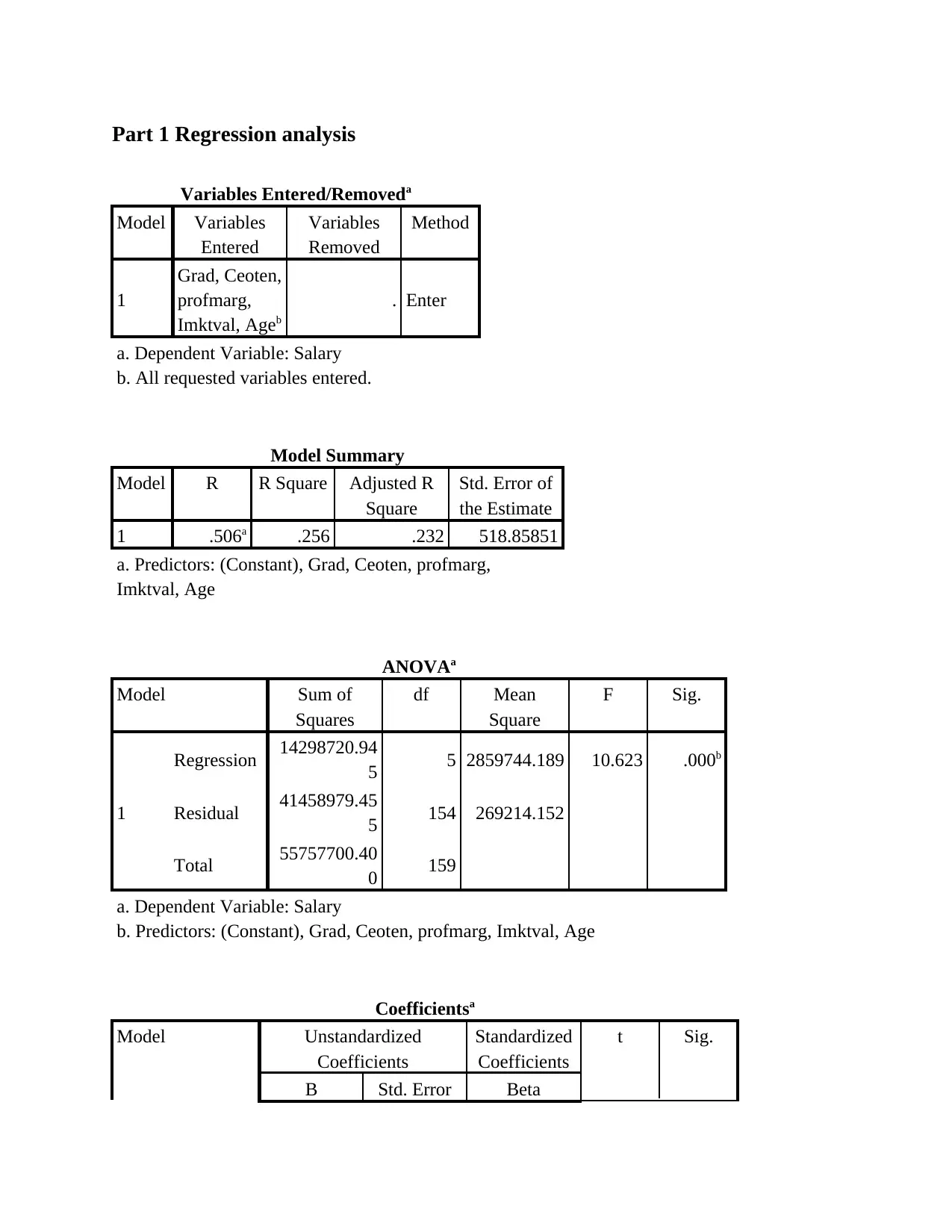

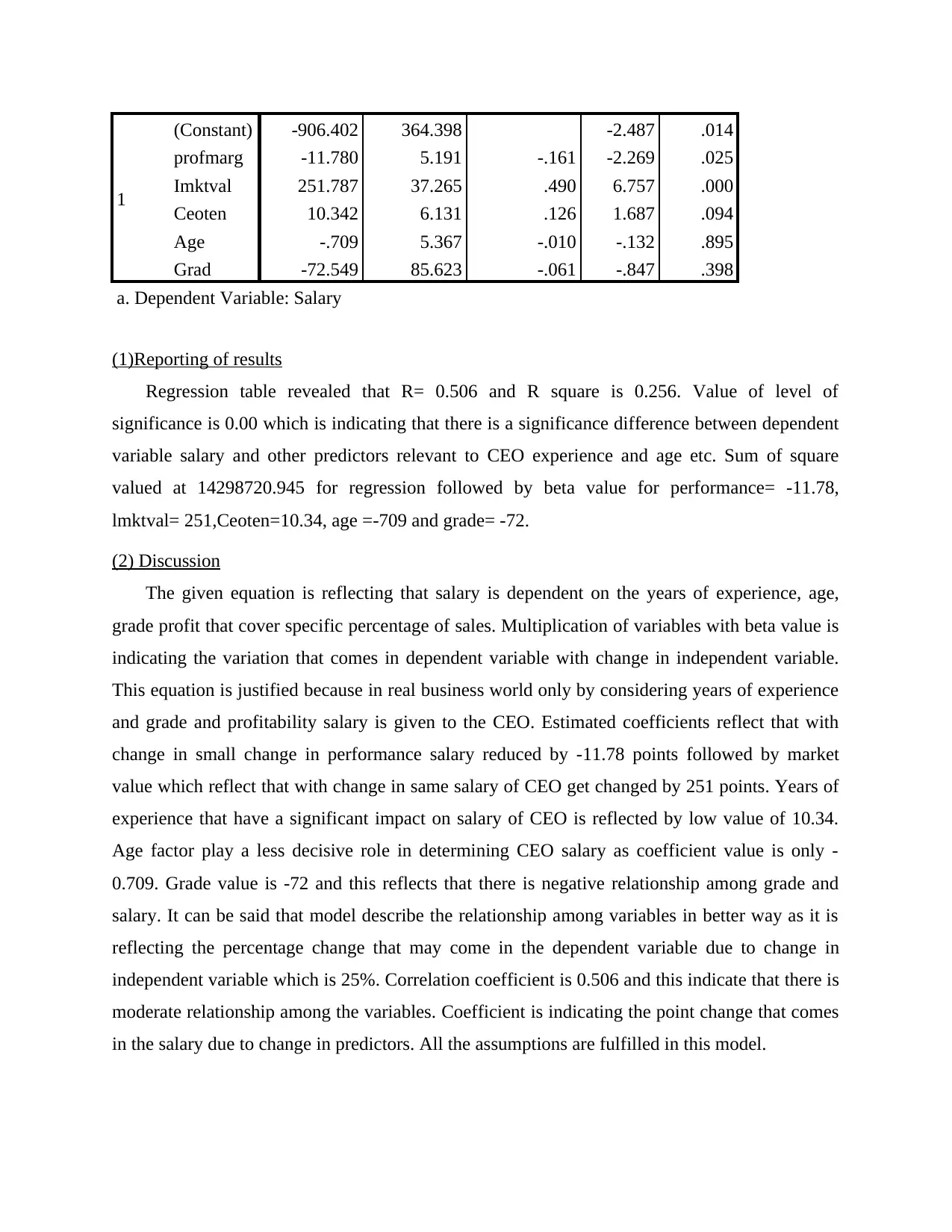

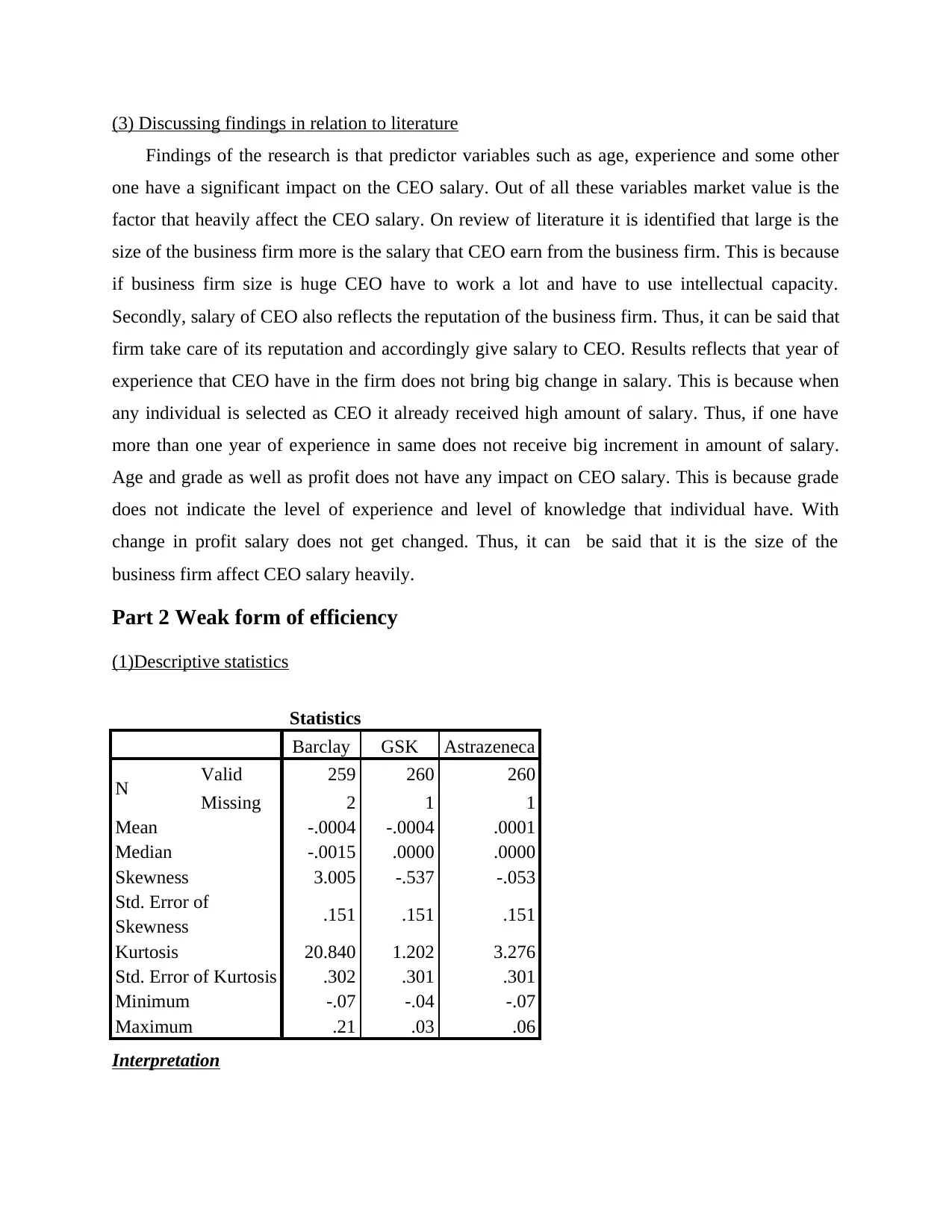

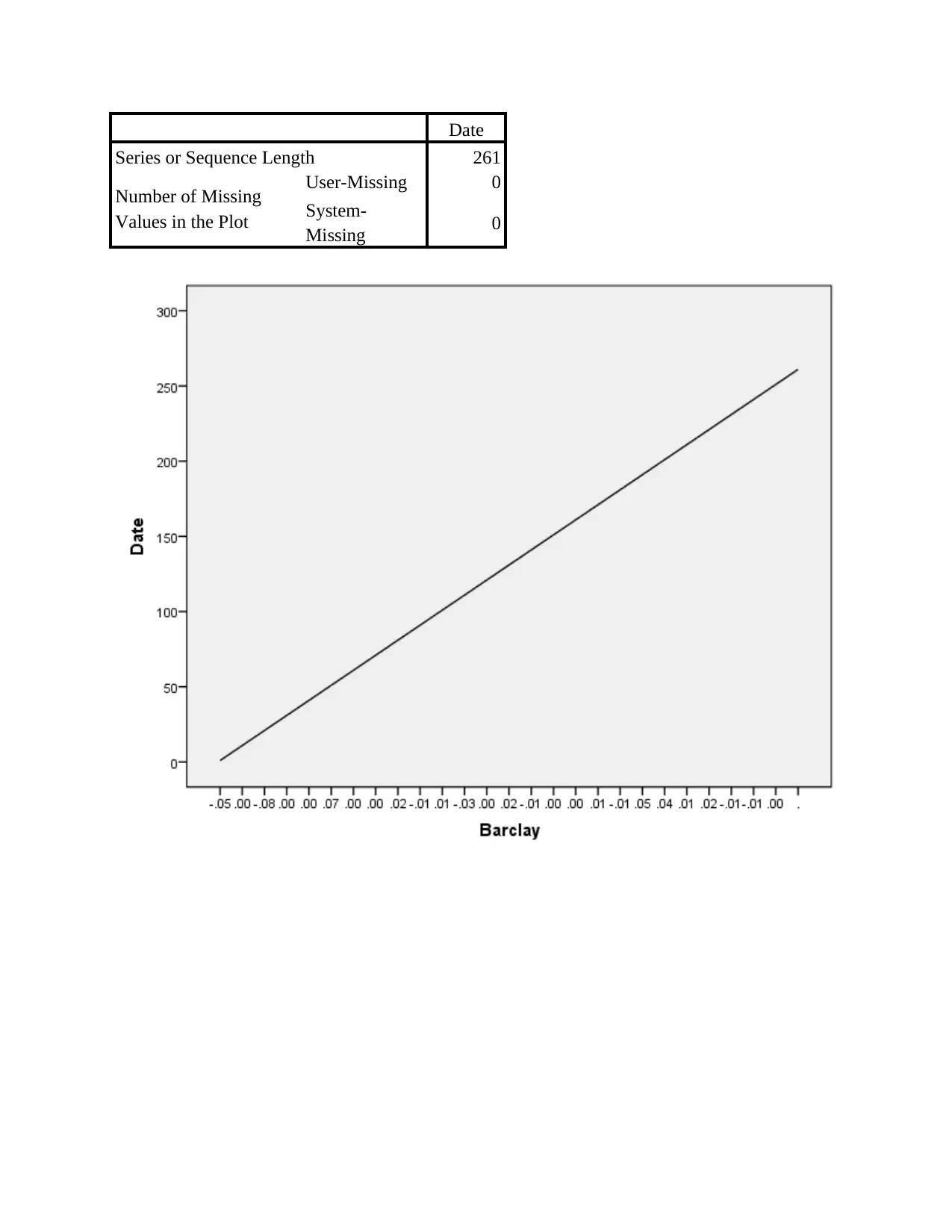

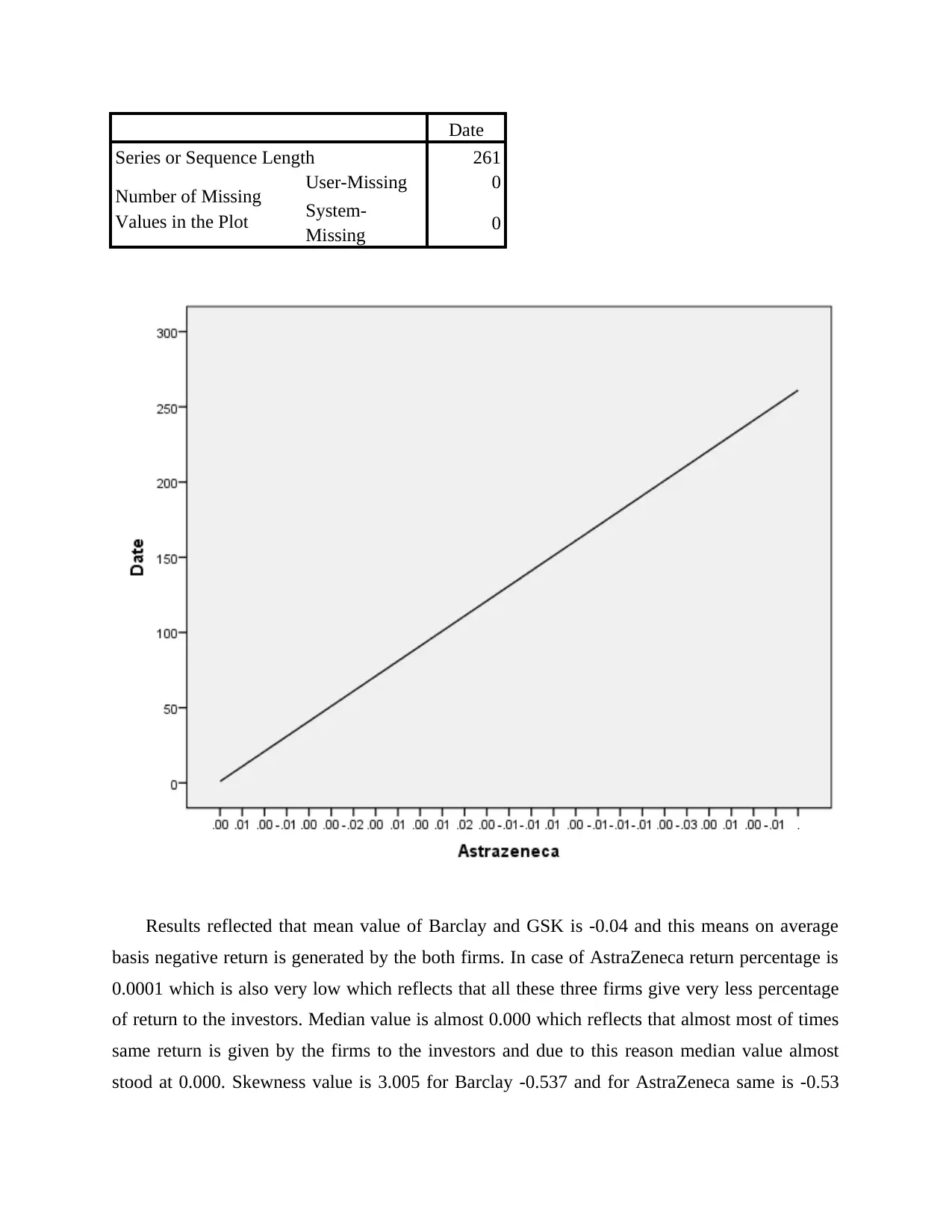

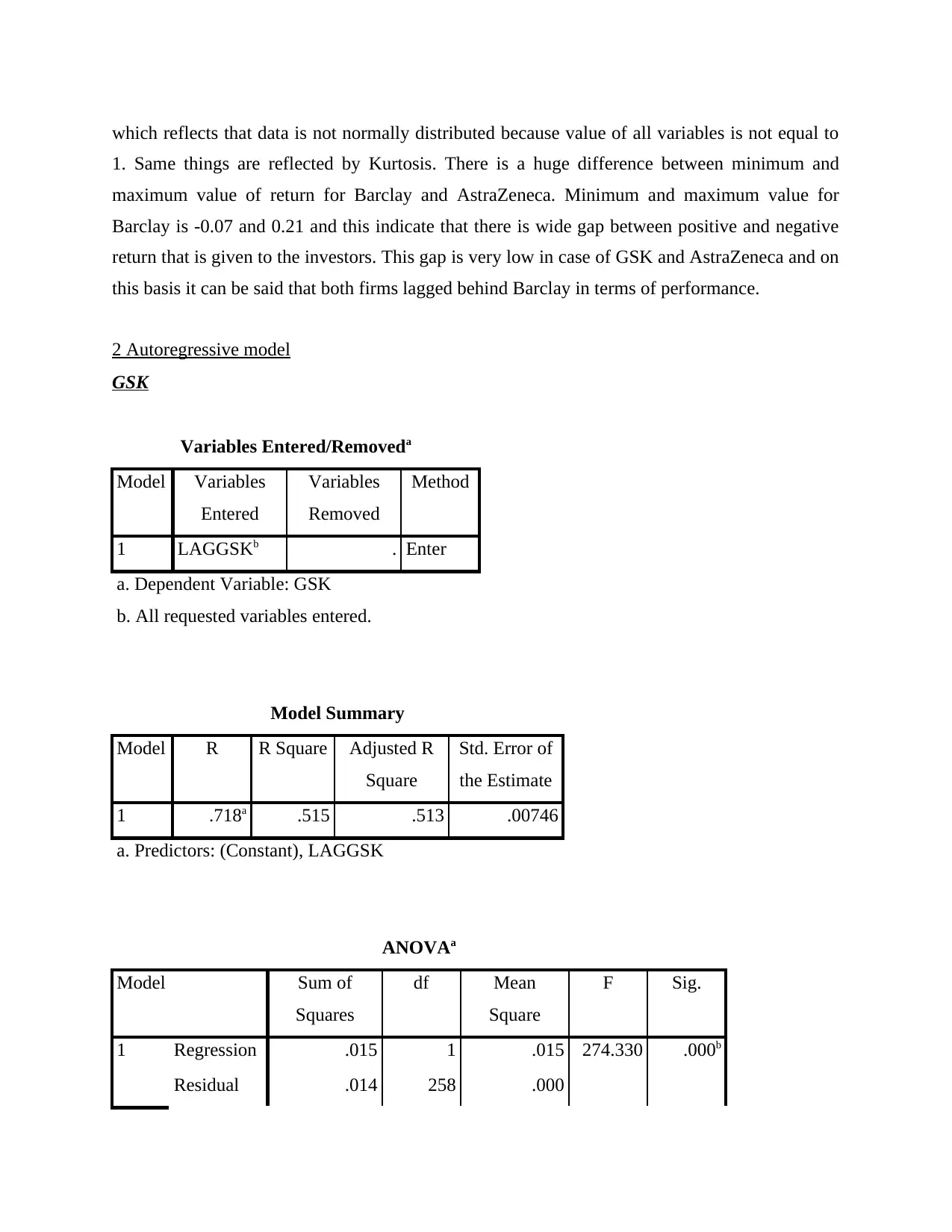

This report presents a comprehensive analysis of financial data using SPSS statistical software. The report is divided into two main parts. Part 1 focuses on regression analysis to determine the factors influencing CEO salaries. It details the regression model, reports the results (R, R-squared, ANOVA, coefficients), discusses the findings in relation to existing literature, and interprets the significance of variables like experience, age, and market value. Part 2 investigates the weak form of market efficiency by analyzing the daily returns of three companies (Barclay, GSK, and AstraZeneca). Descriptive statistics are presented, followed by an autoregressive model analysis for each company to assess the impact of lagged returns on current returns. The report also examines the day-of-the-week effect on returns. Overall, the report demonstrates the application of statistical methods to analyze financial data and draw meaningful conclusions about CEO compensation and market efficiency.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.