Management Accounting Report for SRC Pvt Ltd: Analysis of Financials

VerifiedAdded on 2020/06/05

|19

|4688

|88

Report

AI Summary

This report provides a comprehensive analysis of the management accounting practices of SRC Pvt Ltd, a food processing company. It begins with an overview of management accounting, detailing its essential requirements and various systems such as cost accounting, batch costing, inventory management, and price optimization. The report then describes the different methods employed by the firm for management accounting reporting, including account receivables, production, sales, and income reports. Furthermore, it outlines the benefits of a management accounting system, highlighting advantages like improved efficiency, better pricing, and effective cash flow management. The report also integrates the management accounting system with the organizational process and calculates costs to prepare income statements using both marginal and absorption costing methods. Finally, it explores the planning tools and management accounting approaches used by SRC Pvt Ltd to address financial issues, providing a detailed examination of the company's financial performance and decision-making processes.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The system of accounting under which various elements like planning, implementing,

monitoring, review, analysis of financials are included is called as management accounting. The

particular approach is used by the companies for taking several kinds of internal business

decisions and make it profitable within the industry. The present report is on the basis of SRC

Private Limited company which is operating under the sector of food processing. The study

focuses on various concepts of management accounting which are adopted by the selected firm.

Apart from this, reporting systems which are required for the entity in terms of management

accounting for prepare the final accounts are explained at this report. Income statements with the

help of marginal and absorption method are to be made at the current study for the SRC Pvt Ltd.

Moreover, planning tools as well as management accounting approaches to combat issues arisen

within workplace regarding to the financials are described in this study.

1

The system of accounting under which various elements like planning, implementing,

monitoring, review, analysis of financials are included is called as management accounting. The

particular approach is used by the companies for taking several kinds of internal business

decisions and make it profitable within the industry. The present report is on the basis of SRC

Private Limited company which is operating under the sector of food processing. The study

focuses on various concepts of management accounting which are adopted by the selected firm.

Apart from this, reporting systems which are required for the entity in terms of management

accounting for prepare the final accounts are explained at this report. Income statements with the

help of marginal and absorption method are to be made at the current study for the SRC Pvt Ltd.

Moreover, planning tools as well as management accounting approaches to combat issues arisen

within workplace regarding to the financials are described in this study.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Client Comments Addressed by

writer

Page Number

You have not evaluated and explained management accounting

and essential requirements of its various systems

Yes 1,2,3

You have not evaluated benefits of MA system Yes 4

You have not evaluated integration of MA system and reporting

with organizational process

Yes 5

You have not calculated costs in order to prepare income

statements with the help of marginal and absorption

costing method

Yes 5,6

Not analysed undertaking MA techniques for producing

financial reporting documents

Yes 7

Not Explained various planning tools which are used for

budgetary control along with its merits and demerits

Yes 7, 8, 9 ,10

Not used different planning tools in the preparation of and

forecasting budget

Yes 11

You have not compared how SRC Pvt Ltd. Uses management

accounting systems in order to combat financial issues

Yes 12,13

You have not stated the planning tools that helps in responding

financial problems

Yes 13

You have not analysed how management accounting could lead

to resolve financial problems

Yes 13

2

writer

Page Number

You have not evaluated and explained management accounting

and essential requirements of its various systems

Yes 1,2,3

You have not evaluated benefits of MA system Yes 4

You have not evaluated integration of MA system and reporting

with organizational process

Yes 5

You have not calculated costs in order to prepare income

statements with the help of marginal and absorption

costing method

Yes 5,6

Not analysed undertaking MA techniques for producing

financial reporting documents

Yes 7

Not Explained various planning tools which are used for

budgetary control along with its merits and demerits

Yes 7, 8, 9 ,10

Not used different planning tools in the preparation of and

forecasting budget

Yes 11

You have not compared how SRC Pvt Ltd. Uses management

accounting systems in order to combat financial issues

Yes 12,13

You have not stated the planning tools that helps in responding

financial problems

Yes 13

You have not analysed how management accounting could lead

to resolve financial problems

Yes 13

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P1 Explanation of management accounting and essential requirements of its various systems for

the SRC Pvt. Ltd.

MA serves financial information or data and thereby gives indication to the team of

higher management about the areas that demand for improvement. Hence, MA is highly

significant which in turn provides assistance in decision making, planning, performance

management as well as control to the great extent. Management accounting is the concept where

different kind of techniques, approaches, systems and budgets are involved which help to

manage financial resources and enhance performance of the firm. Very basic objective of the

specific system is to assess internal business conditions and users of this are internal stakeholders

like managers, workforce etc. There are some financial reports and sheets are prepared but not

necessary to frame by considering legal systems and accounting standards (Ahmed and et.al.,

2013).

Management accounting systems that can be undertaken by SRC are enumerated below

along with their applications:

Cost accounting: The system in which costing aspects are included which incurred in the

business process is identified as cost accounting. Through this, management of the SRC Pvt Ltd

able to assess level and amount of the total expenses which is supportive to make pricing

decisions. Further, it is the method of recording all those financial transactions which rely under

cost or expenses aspect. By considering this, the company able to determine that how many

expenditures are incurred there. On the basis of this, decision is taken for making further

expenses within workplace to produce food items like chocolate, cake and others. Basic need of

the cited system is to analyse total cost and take pricing decision to sale items in its respective

market. By using the system of cost accounting firm can get information about fixed and variable

expenses. Thus, by summing up both the expenses and dividing the same with food processing

units firm can determine per unit cost. Thus, by assessing such cost firm would become able to

set appropriate price of product that helps in getting suitable margin.

Batch costing system: Other approach in which also expenditures are determined by the

business of SRC Pvt Ltd but according to the batch system. When the firm having production

range in different kind of goods, then the batch costing is applied and adopted within working

environment (Hennes and et.al., 2013). At the present study, chosen enterprise has presence in

3

the SRC Pvt. Ltd.

MA serves financial information or data and thereby gives indication to the team of

higher management about the areas that demand for improvement. Hence, MA is highly

significant which in turn provides assistance in decision making, planning, performance

management as well as control to the great extent. Management accounting is the concept where

different kind of techniques, approaches, systems and budgets are involved which help to

manage financial resources and enhance performance of the firm. Very basic objective of the

specific system is to assess internal business conditions and users of this are internal stakeholders

like managers, workforce etc. There are some financial reports and sheets are prepared but not

necessary to frame by considering legal systems and accounting standards (Ahmed and et.al.,

2013).

Management accounting systems that can be undertaken by SRC are enumerated below

along with their applications:

Cost accounting: The system in which costing aspects are included which incurred in the

business process is identified as cost accounting. Through this, management of the SRC Pvt Ltd

able to assess level and amount of the total expenses which is supportive to make pricing

decisions. Further, it is the method of recording all those financial transactions which rely under

cost or expenses aspect. By considering this, the company able to determine that how many

expenditures are incurred there. On the basis of this, decision is taken for making further

expenses within workplace to produce food items like chocolate, cake and others. Basic need of

the cited system is to analyse total cost and take pricing decision to sale items in its respective

market. By using the system of cost accounting firm can get information about fixed and variable

expenses. Thus, by summing up both the expenses and dividing the same with food processing

units firm can determine per unit cost. Thus, by assessing such cost firm would become able to

set appropriate price of product that helps in getting suitable margin.

Batch costing system: Other approach in which also expenditures are determined by the

business of SRC Pvt Ltd but according to the batch system. When the firm having production

range in different kind of goods, then the batch costing is applied and adopted within working

environment (Hennes and et.al., 2013). At the present study, chosen enterprise has presence in

3

different products like cake, chocolate, boxes etc. Further, the batch costing is required for the

SRC company in order to compute and determine expense of every product range. It is easy and

supportive to analyse price of different type of the goods and services.

Inventory management: In the company stock or inventory having major place because

it sometimes reduces the capability of the management in terms of generating revenue. When

stock remains in the firm in higher quantity, then it leads to decline performance in the industry

because it is symbol of revenue decreasing. Due to this, essential need of stock management

system is to reduce and manage the overall inventory available within SRC private limited firm.

Moreover, to make valuation of inventory there are generally three types of procedures and

methods are available which are such as:

11 LIFO (Last in first out)

11 FIFO (First in first out)

11 WAM (Weighted average method)

Along with this, by applying the inventory management tools such as EOQ firm can

determine the units which need to be maintained for the smooth functioning of operations. This

in turn helps firm in saving ordering as well as holding cost to the significant level and thereby

would become able to make profit margin.

Price optimisation: Aspect of management accounting in which pricing element is

considered as the majority level and determine one price is known as price optimisation.

Normally business organisations change price of one product within specific period of time due

to several reasons like modifications, taxes, quality etc. At the different level of selling charges,

number of customers also differ in the market (Ahmed and Duellman, 2013). Hence, requirement

of the particular system is to opt one price at which more number of people purchase the goods

and items of food from SRC business.

P2 Describing several methods which are adopted by the firm in order to management

accounting reporting

In the management accounting some reports are prepared by which the firm able to

analyse level of its internal financial. In this kind of documents different financials are recorded

and transacted which are such as cost, revenue, expenses, production, stock, income etc. Further,

4

SRC company in order to compute and determine expense of every product range. It is easy and

supportive to analyse price of different type of the goods and services.

Inventory management: In the company stock or inventory having major place because

it sometimes reduces the capability of the management in terms of generating revenue. When

stock remains in the firm in higher quantity, then it leads to decline performance in the industry

because it is symbol of revenue decreasing. Due to this, essential need of stock management

system is to reduce and manage the overall inventory available within SRC private limited firm.

Moreover, to make valuation of inventory there are generally three types of procedures and

methods are available which are such as:

11 LIFO (Last in first out)

11 FIFO (First in first out)

11 WAM (Weighted average method)

Along with this, by applying the inventory management tools such as EOQ firm can

determine the units which need to be maintained for the smooth functioning of operations. This

in turn helps firm in saving ordering as well as holding cost to the significant level and thereby

would become able to make profit margin.

Price optimisation: Aspect of management accounting in which pricing element is

considered as the majority level and determine one price is known as price optimisation.

Normally business organisations change price of one product within specific period of time due

to several reasons like modifications, taxes, quality etc. At the different level of selling charges,

number of customers also differ in the market (Ahmed and Duellman, 2013). Hence, requirement

of the particular system is to opt one price at which more number of people purchase the goods

and items of food from SRC business.

P2 Describing several methods which are adopted by the firm in order to management

accounting reporting

In the management accounting some reports are prepared by which the firm able to

analyse level of its internal financial. In this kind of documents different financials are recorded

and transacted which are such as cost, revenue, expenses, production, stock, income etc. Further,

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

various type of reports which considered under the management accounting reporting are

described below:

Account receivables report: The document in which those amounts are recorded which

comes from the credit sales are known as account receivables. When the company provide or sell

its products and services in the market at credit then the amount recorded in this report. Lower

the account receivables are better and profitable for the entity because it decreases the revenue

and profit generation power. Total amount of the respective report is treated under the balance

sheet of SRC Pvt Limited in the current assets side as debtors (Ball, 2013). On the basis of this, it

can be said that company needs to sell food items at the cash rather than on credit.

Production report: In the management accounting reporting, other kind of report

associated is like production where units which are manufactured by the firm included along

with the amount. On the basis of this, the management of SRC organisation can determine the

total number of food items and services which are produced by it. Further, decision of next

production is easily derived by which entity able to become financially sound. Moreover, amount

of the total production goes in the profit and loss account which helps to make pricing decision

and analyse profitability as well.

Sales report: In this kind of particular report, there are revenue earned by the firm is to be

recorded which playing role as a base of profit and loss statement. Every company has concern

towards the turnover or sales aspect while operating in the industry because higher the revenue is

sign of effective business performance (Warren and et.al., 2013). In this report, those

transactions are included which earned by selling the items of food and bakery on cash. If the

payment is not given in cash and turn into credit sales then money goes in the account

receivables report or balance sheet. Moreover, the summation of sales or revenue report is treated

under the profit and loss account with the same name. From this value, all the expenses which

are incurred in the firm are deducted and then condition of profitability is assessed by the

management.

Income report: In addition to above all reports, other is regarding to the income in which

whatever earn by the company in terms of profit is recorded. In the market sector, every entity

having presence and operation for maximise the income value. Under this report also revenue

data used for calculating the income generated by SRC firm (Adibah and et.al., 2013). Further,

5

described below:

Account receivables report: The document in which those amounts are recorded which

comes from the credit sales are known as account receivables. When the company provide or sell

its products and services in the market at credit then the amount recorded in this report. Lower

the account receivables are better and profitable for the entity because it decreases the revenue

and profit generation power. Total amount of the respective report is treated under the balance

sheet of SRC Pvt Limited in the current assets side as debtors (Ball, 2013). On the basis of this, it

can be said that company needs to sell food items at the cash rather than on credit.

Production report: In the management accounting reporting, other kind of report

associated is like production where units which are manufactured by the firm included along

with the amount. On the basis of this, the management of SRC organisation can determine the

total number of food items and services which are produced by it. Further, decision of next

production is easily derived by which entity able to become financially sound. Moreover, amount

of the total production goes in the profit and loss account which helps to make pricing decision

and analyse profitability as well.

Sales report: In this kind of particular report, there are revenue earned by the firm is to be

recorded which playing role as a base of profit and loss statement. Every company has concern

towards the turnover or sales aspect while operating in the industry because higher the revenue is

sign of effective business performance (Warren and et.al., 2013). In this report, those

transactions are included which earned by selling the items of food and bakery on cash. If the

payment is not given in cash and turn into credit sales then money goes in the account

receivables report or balance sheet. Moreover, the summation of sales or revenue report is treated

under the profit and loss account with the same name. From this value, all the expenses which

are incurred in the firm are deducted and then condition of profitability is assessed by the

management.

Income report: In addition to above all reports, other is regarding to the income in which

whatever earn by the company in terms of profit is recorded. In the market sector, every entity

having presence and operation for maximise the income value. Under this report also revenue

data used for calculating the income generated by SRC firm (Adibah and et.al., 2013). Further,

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

generally three types of incomes are considered in this report which is like gross, operating and

net or final yield.

M1: Benefits of MA system

Advantages of cost accounting

Helps in measuring expenses and thereby improves efficiency level Provides input and assist in fixing the price

Advantages of inventory control

Helps in managing cash flow and maximizing the profit level;

Reduces labour cost and facilitates business intelligence

D1: Integration of MA system and reporting with organizational process

From assessment, it has been identified that MA systems and reporting are highly

associated with the organizational process. Moreover, MA system helps in preparing reports

pertaining to the activities and functions of an organization.

P3 & D2 Calculating costs in order to prepare income statements with the help of marginal and

absorption costing methods

The statement or report which shows that company is up to which level efficient in terms

of generating income and profit is known as income statement. Generally two kinds of processes

are undertaken by the cited company to assess profitability which is like absorption and

marginal. Moreover, accounts of profit and loss using these methods are stated below:

Cost of each unit of cake

Particulars Amount (in GBP)

Direct material 50000

Direct labour 30000

Variable manufacturing overhead 20000

Variable selling and administrative expenses 30000

Fixed manufacturing overhead 40000

Fixed selling and administrative expenses 30000

6

net or final yield.

M1: Benefits of MA system

Advantages of cost accounting

Helps in measuring expenses and thereby improves efficiency level Provides input and assist in fixing the price

Advantages of inventory control

Helps in managing cash flow and maximizing the profit level;

Reduces labour cost and facilitates business intelligence

D1: Integration of MA system and reporting with organizational process

From assessment, it has been identified that MA systems and reporting are highly

associated with the organizational process. Moreover, MA system helps in preparing reports

pertaining to the activities and functions of an organization.

P3 & D2 Calculating costs in order to prepare income statements with the help of marginal and

absorption costing methods

The statement or report which shows that company is up to which level efficient in terms

of generating income and profit is known as income statement. Generally two kinds of processes

are undertaken by the cited company to assess profitability which is like absorption and

marginal. Moreover, accounts of profit and loss using these methods are stated below:

Cost of each unit of cake

Particulars Amount (in GBP)

Direct material 50000

Direct labour 30000

Variable manufacturing overhead 20000

Variable selling and administrative expenses 30000

Fixed manufacturing overhead 40000

Fixed selling and administrative expenses 30000

6

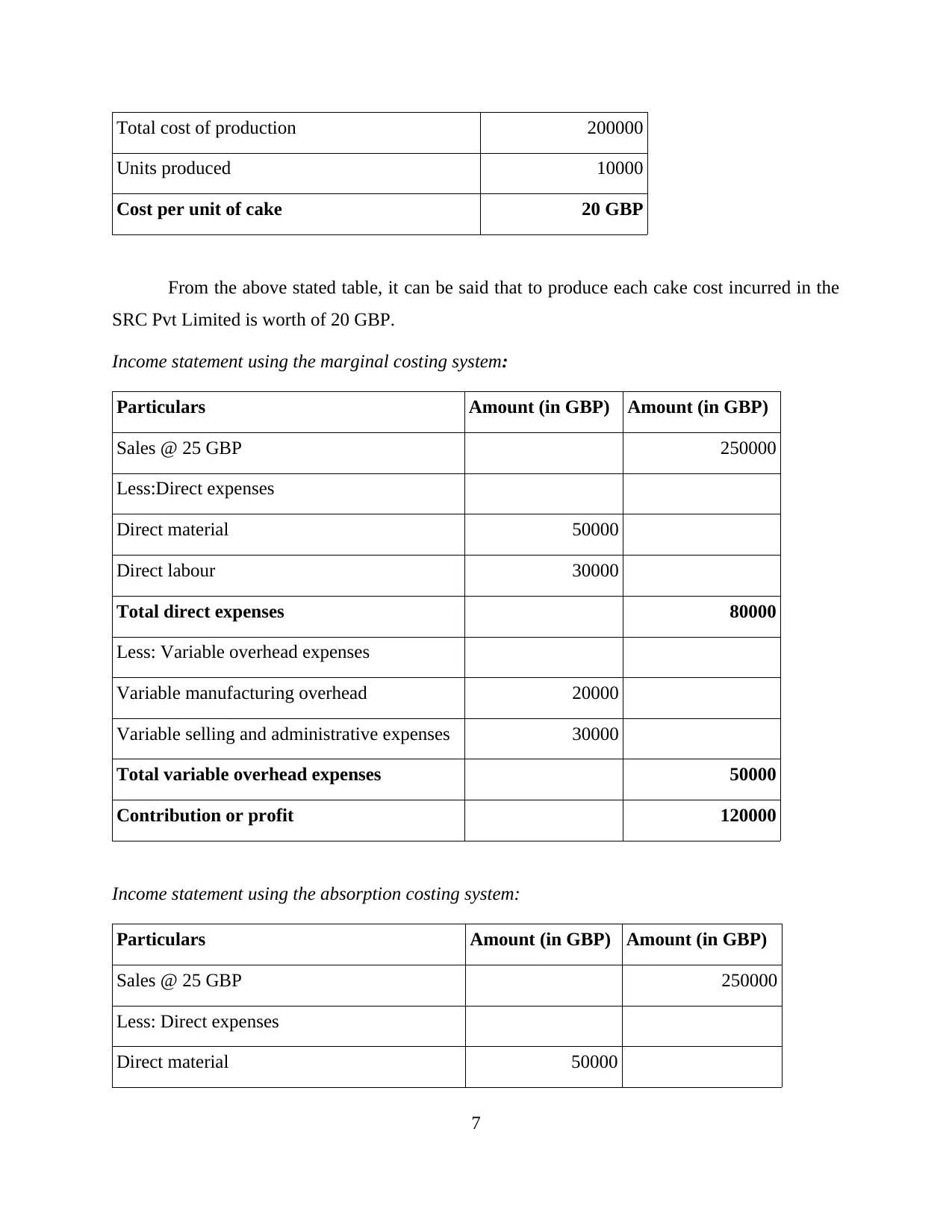

Total cost of production 200000

Units produced 10000

Cost per unit of cake 20 GBP

From the above stated table, it can be said that to produce each cake cost incurred in the

SRC Pvt Limited is worth of 20 GBP.

Income statement using the marginal costing system:

Particulars Amount (in GBP) Amount (in GBP)

Sales @ 25 GBP 250000

Less:Direct expenses

Direct material 50000

Direct labour 30000

Total direct expenses 80000

Less: Variable overhead expenses

Variable manufacturing overhead 20000

Variable selling and administrative expenses 30000

Total variable overhead expenses 50000

Contribution or profit 120000

Income statement using the absorption costing system:

Particulars Amount (in GBP) Amount (in GBP)

Sales @ 25 GBP 250000

Less: Direct expenses

Direct material 50000

7

Units produced 10000

Cost per unit of cake 20 GBP

From the above stated table, it can be said that to produce each cake cost incurred in the

SRC Pvt Limited is worth of 20 GBP.

Income statement using the marginal costing system:

Particulars Amount (in GBP) Amount (in GBP)

Sales @ 25 GBP 250000

Less:Direct expenses

Direct material 50000

Direct labour 30000

Total direct expenses 80000

Less: Variable overhead expenses

Variable manufacturing overhead 20000

Variable selling and administrative expenses 30000

Total variable overhead expenses 50000

Contribution or profit 120000

Income statement using the absorption costing system:

Particulars Amount (in GBP) Amount (in GBP)

Sales @ 25 GBP 250000

Less: Direct expenses

Direct material 50000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

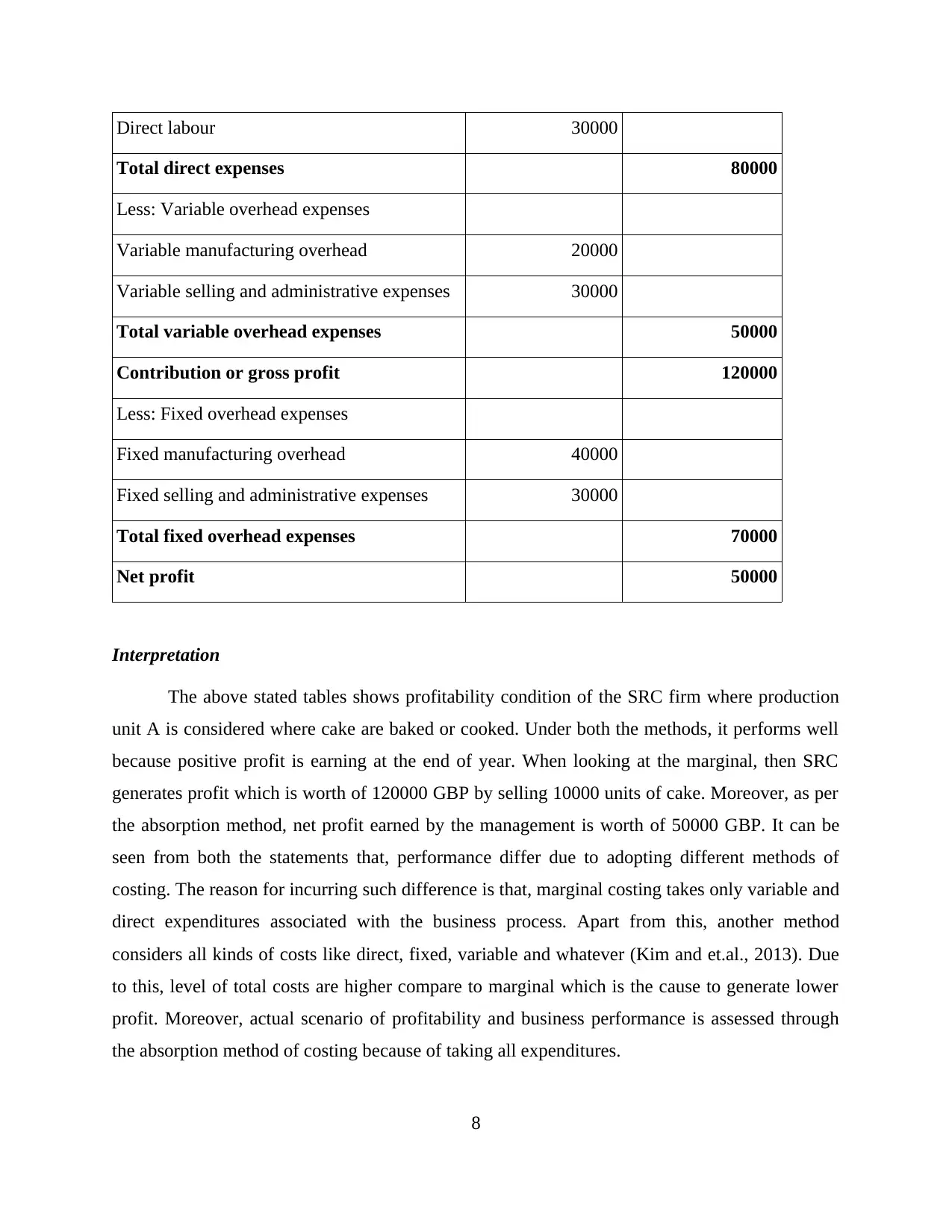

Direct labour 30000

Total direct expenses 80000

Less: Variable overhead expenses

Variable manufacturing overhead 20000

Variable selling and administrative expenses 30000

Total variable overhead expenses 50000

Contribution or gross profit 120000

Less: Fixed overhead expenses

Fixed manufacturing overhead 40000

Fixed selling and administrative expenses 30000

Total fixed overhead expenses 70000

Net profit 50000

Interpretation

The above stated tables shows profitability condition of the SRC firm where production

unit A is considered where cake are baked or cooked. Under both the methods, it performs well

because positive profit is earning at the end of year. When looking at the marginal, then SRC

generates profit which is worth of 120000 GBP by selling 10000 units of cake. Moreover, as per

the absorption method, net profit earned by the management is worth of 50000 GBP. It can be

seen from both the statements that, performance differ due to adopting different methods of

costing. The reason for incurring such difference is that, marginal costing takes only variable and

direct expenditures associated with the business process. Apart from this, another method

considers all kinds of costs like direct, fixed, variable and whatever (Kim and et.al., 2013). Due

to this, level of total costs are higher compare to marginal which is the cause to generate lower

profit. Moreover, actual scenario of profitability and business performance is assessed through

the absorption method of costing because of taking all expenditures.

8

Total direct expenses 80000

Less: Variable overhead expenses

Variable manufacturing overhead 20000

Variable selling and administrative expenses 30000

Total variable overhead expenses 50000

Contribution or gross profit 120000

Less: Fixed overhead expenses

Fixed manufacturing overhead 40000

Fixed selling and administrative expenses 30000

Total fixed overhead expenses 70000

Net profit 50000

Interpretation

The above stated tables shows profitability condition of the SRC firm where production

unit A is considered where cake are baked or cooked. Under both the methods, it performs well

because positive profit is earning at the end of year. When looking at the marginal, then SRC

generates profit which is worth of 120000 GBP by selling 10000 units of cake. Moreover, as per

the absorption method, net profit earned by the management is worth of 50000 GBP. It can be

seen from both the statements that, performance differ due to adopting different methods of

costing. The reason for incurring such difference is that, marginal costing takes only variable and

direct expenditures associated with the business process. Apart from this, another method

considers all kinds of costs like direct, fixed, variable and whatever (Kim and et.al., 2013). Due

to this, level of total costs are higher compare to marginal which is the cause to generate lower

profit. Moreover, actual scenario of profitability and business performance is assessed through

the absorption method of costing because of taking all expenditures.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2: Undertaking MA techniques for producing financial reporting documents

By doing assessment, it has found that management accounting technique such as

absorption and marginal costing helps in assessing profit margin. Thus, by considering such

technique manager of SRC Ltd can prepare suitable report and thereby would become able to

provide information to them that whether absorption costing will offer suitable results or

marginal.

P4 Explaining various planning tools which are used for budgetary control along with its merits

and demerits

In the budgetary section, there are several kinds of techniques and tools involved which

support to the firm in terms of making effectual financial plan. Along with this, it is able to set

standards which help to meet with the objectives in proper manner. Furthermore, those tools

which are highly used by the SRC Pvt Limited entity for budgetary control are explained with

the advantages and limitation as below:

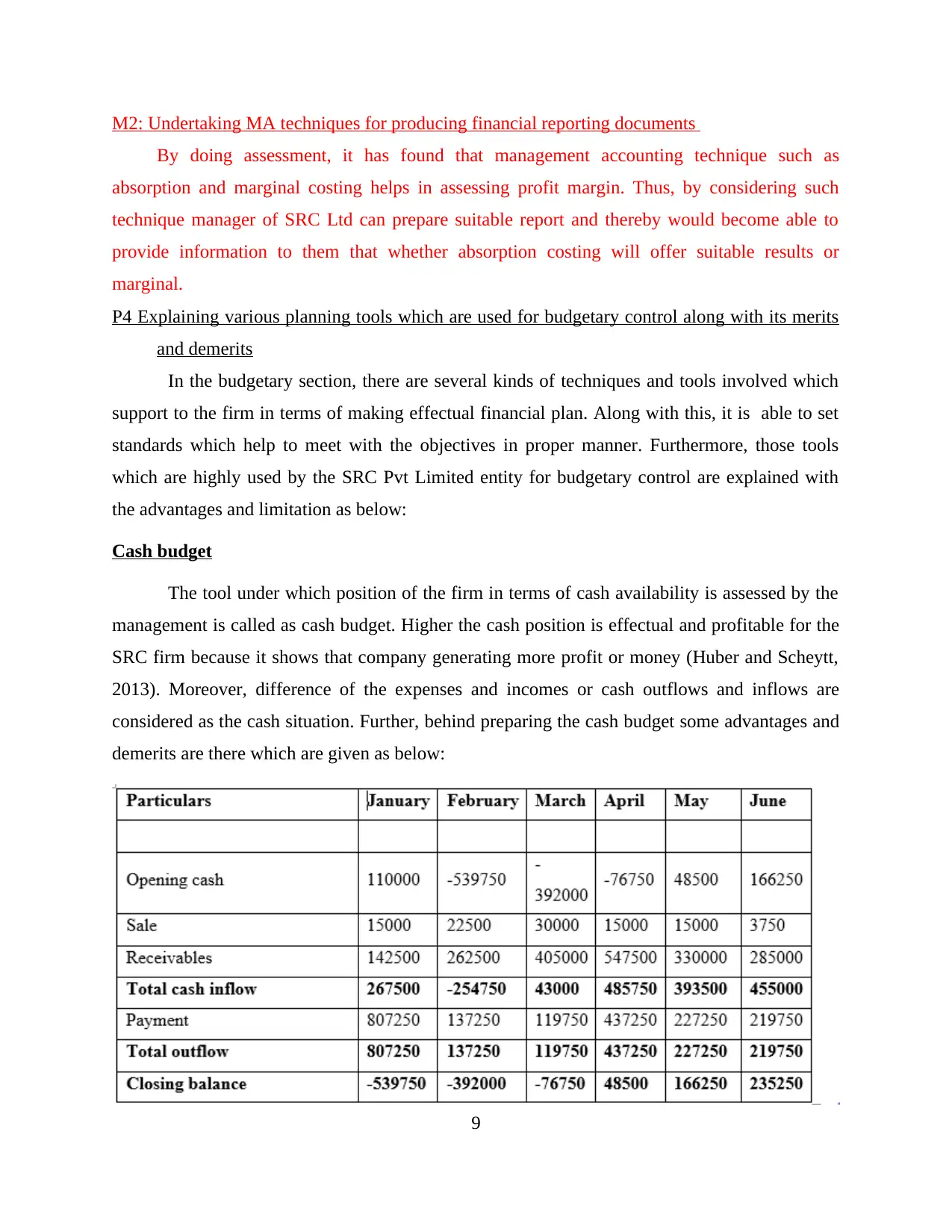

Cash budget

The tool under which position of the firm in terms of cash availability is assessed by the

management is called as cash budget. Higher the cash position is effectual and profitable for the

SRC firm because it shows that company generating more profit or money (Huber and Scheytt,

2013). Moreover, difference of the expenses and incomes or cash outflows and inflows are

considered as the cash situation. Further, behind preparing the cash budget some advantages and

demerits are there which are given as below:

9

By doing assessment, it has found that management accounting technique such as

absorption and marginal costing helps in assessing profit margin. Thus, by considering such

technique manager of SRC Ltd can prepare suitable report and thereby would become able to

provide information to them that whether absorption costing will offer suitable results or

marginal.

P4 Explaining various planning tools which are used for budgetary control along with its merits

and demerits

In the budgetary section, there are several kinds of techniques and tools involved which

support to the firm in terms of making effectual financial plan. Along with this, it is able to set

standards which help to meet with the objectives in proper manner. Furthermore, those tools

which are highly used by the SRC Pvt Limited entity for budgetary control are explained with

the advantages and limitation as below:

Cash budget

The tool under which position of the firm in terms of cash availability is assessed by the

management is called as cash budget. Higher the cash position is effectual and profitable for the

SRC firm because it shows that company generating more profit or money (Huber and Scheytt,

2013). Moreover, difference of the expenses and incomes or cash outflows and inflows are

considered as the cash situation. Further, behind preparing the cash budget some advantages and

demerits are there which are given as below:

9

Benefits:

The cash budget is supportive for the SRC company in order to predetermine cash

position that it will generate how many incomes and incur expenses in the further fiscal

period. When cash outflows are lower in comparison to inflows then it can be said that it

performs well in the industry.

It helps to make the financial plan according to fluctuations in sales and expenses as per

the season. On the basis of that expenses are to be planned by the entity for next year

which is symbol of becoming more financially strong in the food industry.

Along with this, through cash budget the SRC firm able to establish effective and strong

relation between different activities and functions of the organisation (Methot and

Wetzel, 2013). Due to this, goals and objectives which are agreed and determined by it

can be achieve on the deadline.

By considering and using the cash budget in the firm allocations or allotments of the

financial resources can be done in adequate manner. In addition to this, requirement of the cash amount or capital is also determined along

with the appropriate financing sources.

Disadvantages:

The cash budget is prepared by the management on the basis of estimations and

assumptions. Further, due to improper and ineffective estimations the firm cannot make

better decisions at the workplace (McIntosh, 2017).

Further, due to lack of flexibility in cash budget the company cannot make fruitful

decisions. By this, proper and smooth planning cannot be done which is sign of

hampering the business profit.

At the time of preparing cash budget any kind of non financial factors and elements are

not discussed which impact on the firm. Because of this particular reason cash position

cannot be forecasted properly which lead to hamper objective achievement within

deadlines.

Production budget

10

The cash budget is supportive for the SRC company in order to predetermine cash

position that it will generate how many incomes and incur expenses in the further fiscal

period. When cash outflows are lower in comparison to inflows then it can be said that it

performs well in the industry.

It helps to make the financial plan according to fluctuations in sales and expenses as per

the season. On the basis of that expenses are to be planned by the entity for next year

which is symbol of becoming more financially strong in the food industry.

Along with this, through cash budget the SRC firm able to establish effective and strong

relation between different activities and functions of the organisation (Methot and

Wetzel, 2013). Due to this, goals and objectives which are agreed and determined by it

can be achieve on the deadline.

By considering and using the cash budget in the firm allocations or allotments of the

financial resources can be done in adequate manner. In addition to this, requirement of the cash amount or capital is also determined along

with the appropriate financing sources.

Disadvantages:

The cash budget is prepared by the management on the basis of estimations and

assumptions. Further, due to improper and ineffective estimations the firm cannot make

better decisions at the workplace (McIntosh, 2017).

Further, due to lack of flexibility in cash budget the company cannot make fruitful

decisions. By this, proper and smooth planning cannot be done which is sign of

hampering the business profit.

At the time of preparing cash budget any kind of non financial factors and elements are

not discussed which impact on the firm. Because of this particular reason cash position

cannot be forecasted properly which lead to hamper objective achievement within

deadlines.

Production budget

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.