Business Finance Report: SSHA Project Evaluation and Sensitivity

VerifiedAdded on 2021/06/14

|8

|1525

|41

Report

AI Summary

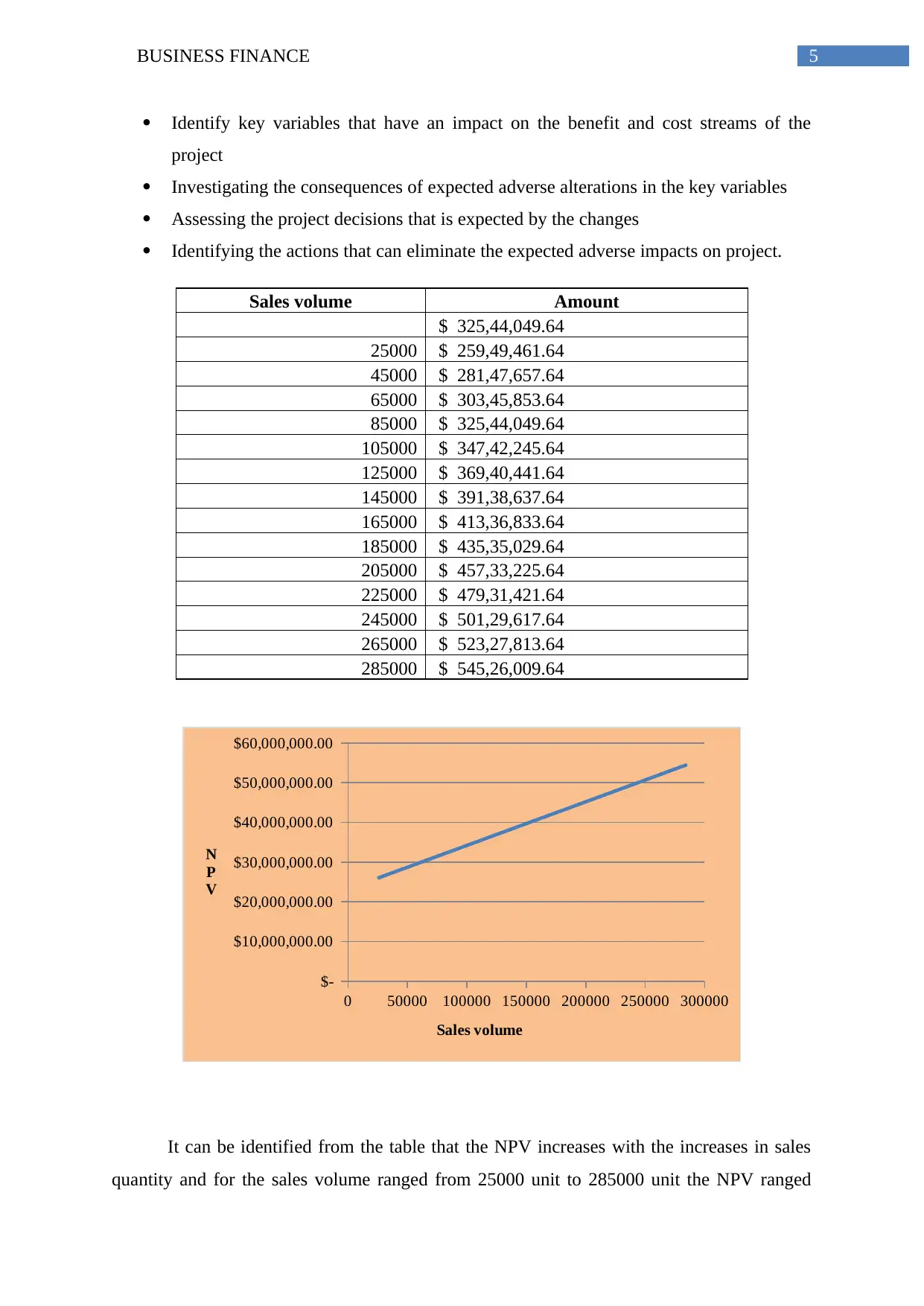

This report provides a comprehensive business finance analysis of a new SSHA project, evaluating its financial viability using various capital budgeting techniques. The analysis includes calculations of the non-discounted payback period, profitability index, IRR, and NPV. The report emphasizes the importance of NPV in project acceptance decisions. Furthermore, it delves into sensitivity analysis, exploring how changes in selling price and sales quantity impact the project's NPV. The analysis reveals the positive correlation between selling price and NPV, as well as sales quantity and NPV. The report concludes that based on the positive NPV, the project should be accepted, while also considering the potential impact of cannibalization on other models' sales. The report utilizes various sources to support the analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.