Financial Analysis of St Brides Group: Cash and Zero-Based Budget

VerifiedAdded on 2023/01/09

|11

|2611

|23

Report

AI Summary

This report presents a financial analysis of the St Brides Group, a resort with 46 rooms and 26 sea views. The report is divided into two main tasks. The first task involves preparing a cash budget based on provided financial information, including cash sales and payments. The cash budget outlines the anticipated cash inflows and outflows over a specific period. The second task focuses on a detailed examination of zero-based budgeting (ZBB). The report explains the ZBB process, including identifying decision units, creating decision packages, ranking packages, allocating resources, and controlling and monitoring. It also highlights the advantages of ZBB over traditional budgeting, such as increased accuracy, improved coordination and communication, enhanced efficiency, and the reduction of redundant activities. Finally, the report discusses how an organization, like the St Brides Group, can introduce and implement ZBB in practical terms, emphasizing its application across various departments to align with corporate priorities and assess historical results and targets.

St Brides Group

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1........................................................................................................................................3

TASK 2........................................................................................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

TASK 1........................................................................................................................................3

TASK 2........................................................................................................................................4

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

The project report is based on St Brides group that owns and manages a huge resort. It

consists 46 rooms and 26 sea views. The report is divided in two tasks which consists different

types of information. In the first part of report a cash budget is prepared that is based on given

financial information about transactions. While in the second task of report a detailed analysis of

zero based budgeting has been done in an effective manner.

MAIN BODY

TASK 1

Preparation of cash budget.

Cash budget- A cash budget reflects a schedule or strategy for planned cash revenues and

payments throughout the year (Colquitt, 2019). Such cash flows include taxes earned,

investments charged and refunds and dividends from loans. It assumes that a forecast of cash is

an estimation of the potential financial condition of the business. Management generally

establishes the cash budget after expenditures have already produced for revenue, acquisitions

and capital expenditure. Such estimates ought to be rendered before the cash allocation, so that

the cash affects correctly over the time. For examples, until you can say how much money the

management wants to know a revenue number. Cash budget is utilized by executives to control a

company's cash flows. This ensures that the board will guarantee that the organization has

enough cash for paying of the bills. For starters, every two weeks the payroll must be charged

and every month the services must be charged. The financial expenditure helps managers to

foresee shortfalls in the cash flow of the business and fix the issues in anticipation of payments.

In other words, Cash budget is an estimation of the potential financial condition of a organization

in writing. In a hypothetical time, the fiscal schedule forecasts cash collections from various

outlets, monetary transfers in specific uses and the corresponding financial condition on a

monthly basis. This is also a systematic analysis of the planned periodic cash flow across the

business. The typical cash budget projection duration is one year, separated by monthly or

weekly intervals. This encourages regular variability in cash flow to be integrated. For situations

The project report is based on St Brides group that owns and manages a huge resort. It

consists 46 rooms and 26 sea views. The report is divided in two tasks which consists different

types of information. In the first part of report a cash budget is prepared that is based on given

financial information about transactions. While in the second task of report a detailed analysis of

zero based budgeting has been done in an effective manner.

MAIN BODY

TASK 1

Preparation of cash budget.

Cash budget- A cash budget reflects a schedule or strategy for planned cash revenues and

payments throughout the year (Colquitt, 2019). Such cash flows include taxes earned,

investments charged and refunds and dividends from loans. It assumes that a forecast of cash is

an estimation of the potential financial condition of the business. Management generally

establishes the cash budget after expenditures have already produced for revenue, acquisitions

and capital expenditure. Such estimates ought to be rendered before the cash allocation, so that

the cash affects correctly over the time. For examples, until you can say how much money the

management wants to know a revenue number. Cash budget is utilized by executives to control a

company's cash flows. This ensures that the board will guarantee that the organization has

enough cash for paying of the bills. For starters, every two weeks the payroll must be charged

and every month the services must be charged. The financial expenditure helps managers to

foresee shortfalls in the cash flow of the business and fix the issues in anticipation of payments.

In other words, Cash budget is an estimation of the potential financial condition of a organization

in writing. In a hypothetical time, the fiscal schedule forecasts cash collections from various

outlets, monetary transfers in specific uses and the corresponding financial condition on a

monthly basis. This is also a systematic analysis of the planned periodic cash flow across the

business. The typical cash budget projection duration is one year, separated by monthly or

weekly intervals. This encourages regular variability in cash flow to be integrated. For situations

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

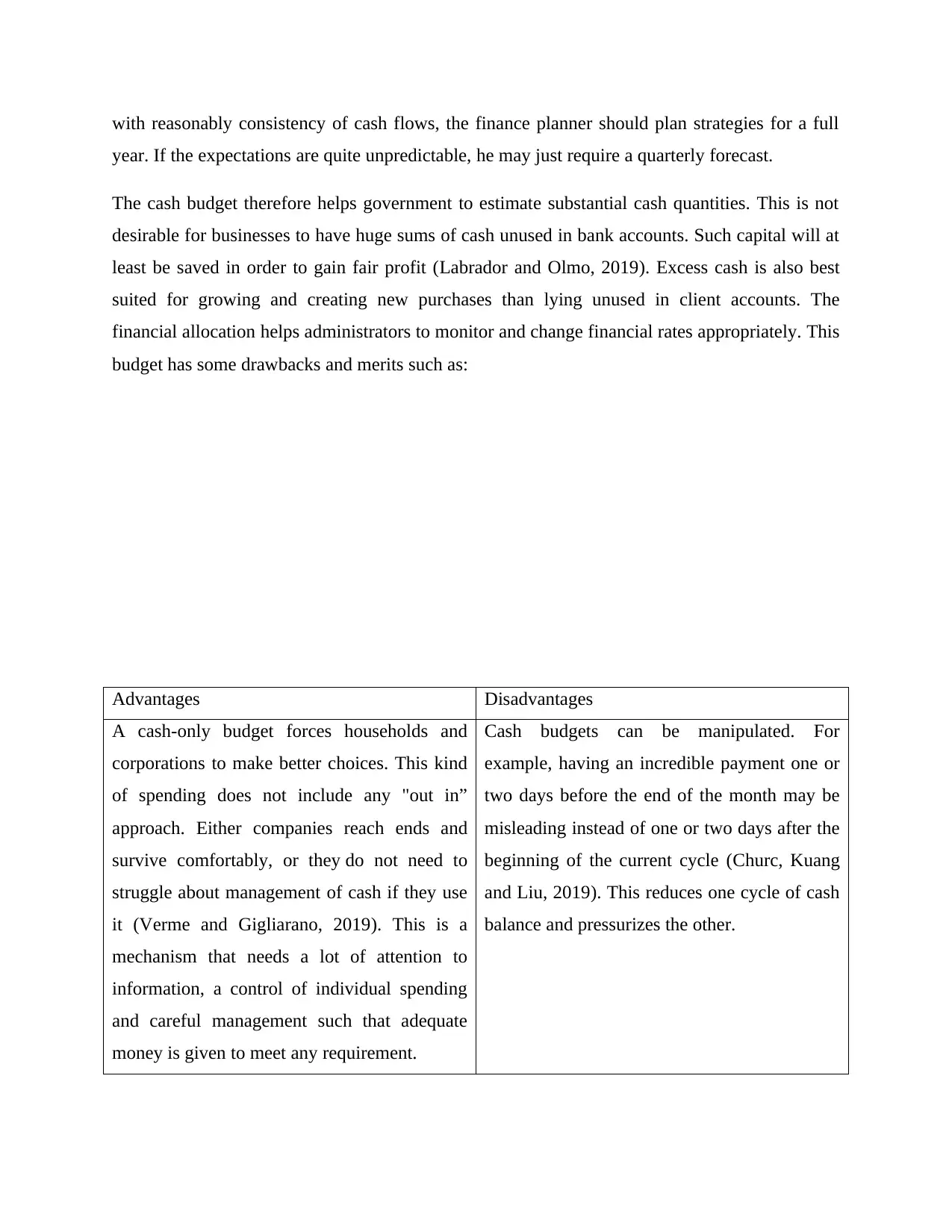

with reasonably consistency of cash flows, the finance planner should plan strategies for a full

year. If the expectations are quite unpredictable, he may just require a quarterly forecast.

The cash budget therefore helps government to estimate substantial cash quantities. This is not

desirable for businesses to have huge sums of cash unused in bank accounts. Such capital will at

least be saved in order to gain fair profit (Labrador and Olmo, 2019). Excess cash is also best

suited for growing and creating new purchases than lying unused in client accounts. The

financial allocation helps administrators to monitor and change financial rates appropriately. This

budget has some drawbacks and merits such as:

Advantages Disadvantages

A cash-only budget forces households and

corporations to make better choices. This kind

of spending does not include any "out in”

approach. Either companies reach ends and

survive comfortably, or they do not need to

struggle about management of cash if they use

it (Verme and Gigliarano, 2019). This is a

mechanism that needs a lot of attention to

information, a control of individual spending

and careful management such that adequate

money is given to meet any requirement.

Cash budgets can be manipulated. For

example, having an incredible payment one or

two days before the end of the month may be

misleading instead of one or two days after the

beginning of the current cycle (Churc, Kuang

and Liu, 2019). This reduces one cycle of cash

balance and pressurizes the other.

year. If the expectations are quite unpredictable, he may just require a quarterly forecast.

The cash budget therefore helps government to estimate substantial cash quantities. This is not

desirable for businesses to have huge sums of cash unused in bank accounts. Such capital will at

least be saved in order to gain fair profit (Labrador and Olmo, 2019). Excess cash is also best

suited for growing and creating new purchases than lying unused in client accounts. The

financial allocation helps administrators to monitor and change financial rates appropriately. This

budget has some drawbacks and merits such as:

Advantages Disadvantages

A cash-only budget forces households and

corporations to make better choices. This kind

of spending does not include any "out in”

approach. Either companies reach ends and

survive comfortably, or they do not need to

struggle about management of cash if they use

it (Verme and Gigliarano, 2019). This is a

mechanism that needs a lot of attention to

information, a control of individual spending

and careful management such that adequate

money is given to meet any requirement.

Cash budgets can be manipulated. For

example, having an incredible payment one or

two days before the end of the month may be

misleading instead of one or two days after the

beginning of the current cycle (Churc, Kuang

and Liu, 2019). This reduces one cycle of cash

balance and pressurizes the other.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

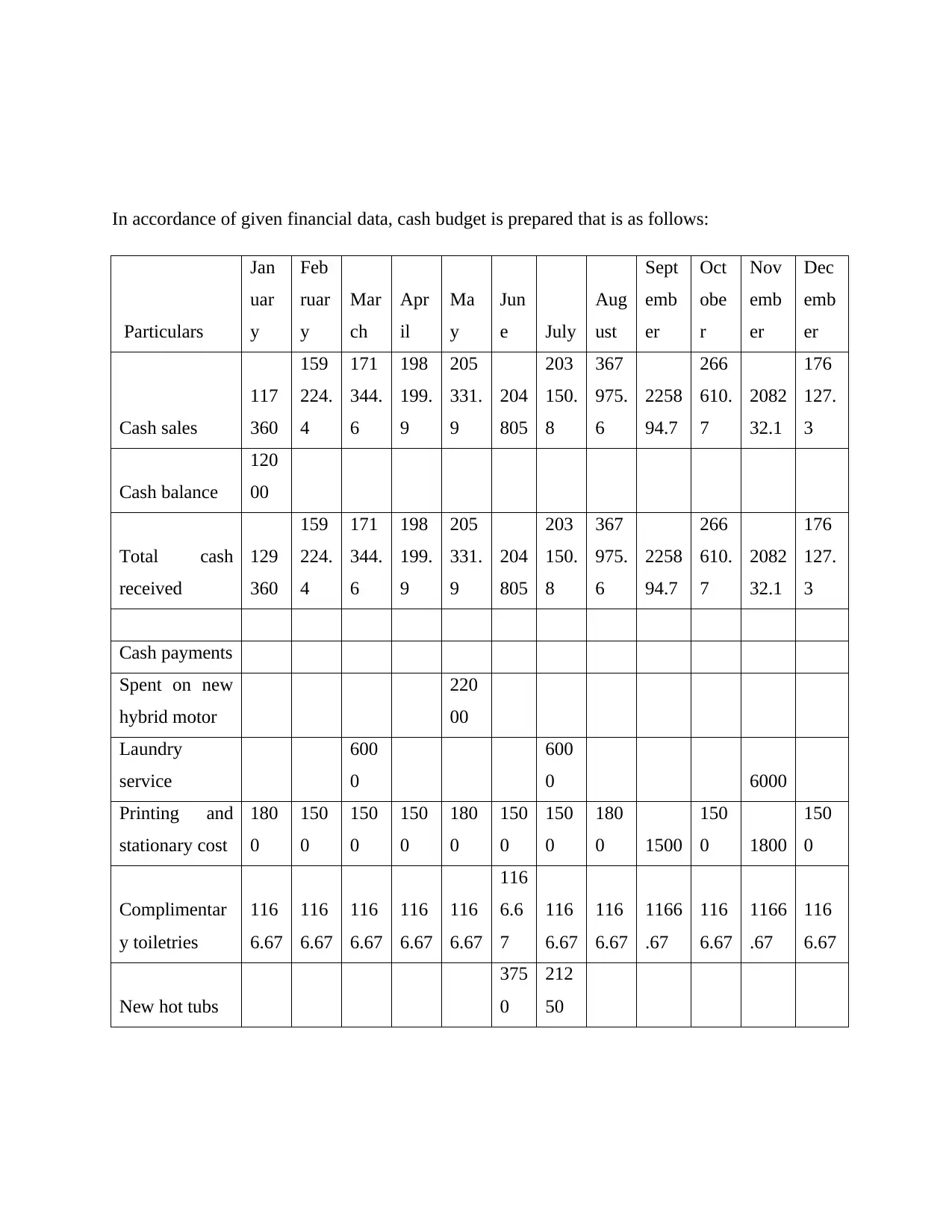

In accordance of given financial data, cash budget is prepared that is as follows:

Particulars

Jan

uar

y

Feb

ruar

y

Mar

ch

Apr

il

Ma

y

Jun

e July

Aug

ust

Sept

emb

er

Oct

obe

r

Nov

emb

er

Dec

emb

er

Cash sales

117

360

159

224.

4

171

344.

6

198

199.

9

205

331.

9

204

805

203

150.

8

367

975.

6

2258

94.7

266

610.

7

2082

32.1

176

127.

3

Cash balance

120

00

Total cash

received

129

360

159

224.

4

171

344.

6

198

199.

9

205

331.

9

204

805

203

150.

8

367

975.

6

2258

94.7

266

610.

7

2082

32.1

176

127.

3

Cash payments

Spent on new

hybrid motor

220

00

Laundry

service

600

0

600

0 6000

Printing and

stationary cost

180

0

150

0

150

0

150

0

180

0

150

0

150

0

180

0 1500

150

0 1800

150

0

Complimentar

y toiletries

116

6.67

116

6.67

116

6.67

116

6.67

116

6.67

116

6.6

7

116

6.67

116

6.67

1166

.67

116

6.67

1166

.67

116

6.67

New hot tubs

375

0

212

50

Particulars

Jan

uar

y

Feb

ruar

y

Mar

ch

Apr

il

Ma

y

Jun

e July

Aug

ust

Sept

emb

er

Oct

obe

r

Nov

emb

er

Dec

emb

er

Cash sales

117

360

159

224.

4

171

344.

6

198

199.

9

205

331.

9

204

805

203

150.

8

367

975.

6

2258

94.7

266

610.

7

2082

32.1

176

127.

3

Cash balance

120

00

Total cash

received

129

360

159

224.

4

171

344.

6

198

199.

9

205

331.

9

204

805

203

150.

8

367

975.

6

2258

94.7

266

610.

7

2082

32.1

176

127.

3

Cash payments

Spent on new

hybrid motor

220

00

Laundry

service

600

0

600

0 6000

Printing and

stationary cost

180

0

150

0

150

0

150

0

180

0

150

0

150

0

180

0 1500

150

0 1800

150

0

Complimentar

y toiletries

116

6.67

116

6.67

116

6.67

116

6.67

116

6.67

116

6.6

7

116

6.67

116

6.67

1166

.67

116

6.67

1166

.67

116

6.67

New hot tubs

375

0

212

50

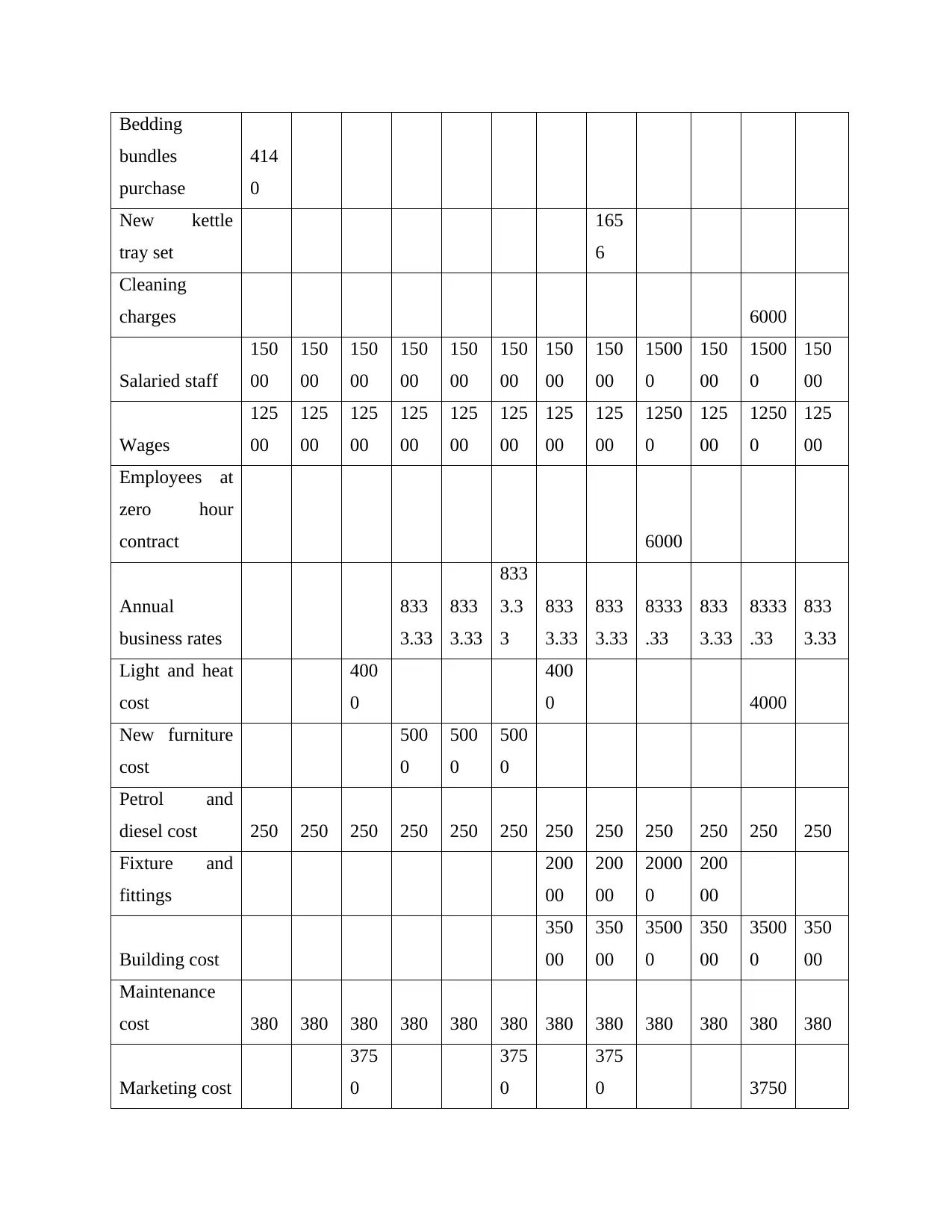

Bedding

bundles

purchase

414

0

New kettle

tray set

165

6

Cleaning

charges 6000

Salaried staff

150

00

150

00

150

00

150

00

150

00

150

00

150

00

150

00

1500

0

150

00

1500

0

150

00

Wages

125

00

125

00

125

00

125

00

125

00

125

00

125

00

125

00

1250

0

125

00

1250

0

125

00

Employees at

zero hour

contract 6000

Annual

business rates

833

3.33

833

3.33

833

3.3

3

833

3.33

833

3.33

8333

.33

833

3.33

8333

.33

833

3.33

Light and heat

cost

400

0

400

0 4000

New furniture

cost

500

0

500

0

500

0

Petrol and

diesel cost 250 250 250 250 250 250 250 250 250 250 250 250

Fixture and

fittings

200

00

200

00

2000

0

200

00

Building cost

350

00

350

00

3500

0

350

00

3500

0

350

00

Maintenance

cost 380 380 380 380 380 380 380 380 380 380 380 380

Marketing cost

375

0

375

0

375

0 3750

bundles

purchase

414

0

New kettle

tray set

165

6

Cleaning

charges 6000

Salaried staff

150

00

150

00

150

00

150

00

150

00

150

00

150

00

150

00

1500

0

150

00

1500

0

150

00

Wages

125

00

125

00

125

00

125

00

125

00

125

00

125

00

125

00

1250

0

125

00

1250

0

125

00

Employees at

zero hour

contract 6000

Annual

business rates

833

3.33

833

3.33

833

3.3

3

833

3.33

833

3.33

8333

.33

833

3.33

8333

.33

833

3.33

Light and heat

cost

400

0

400

0 4000

New furniture

cost

500

0

500

0

500

0

Petrol and

diesel cost 250 250 250 250 250 250 250 250 250 250 250 250

Fixture and

fittings

200

00

200

00

2000

0

200

00

Building cost

350

00

350

00

3500

0

350

00

3500

0

350

00

Maintenance

cost 380 380 380 380 380 380 380 380 380 380 380 380

Marketing cost

375

0

375

0

375

0 3750

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

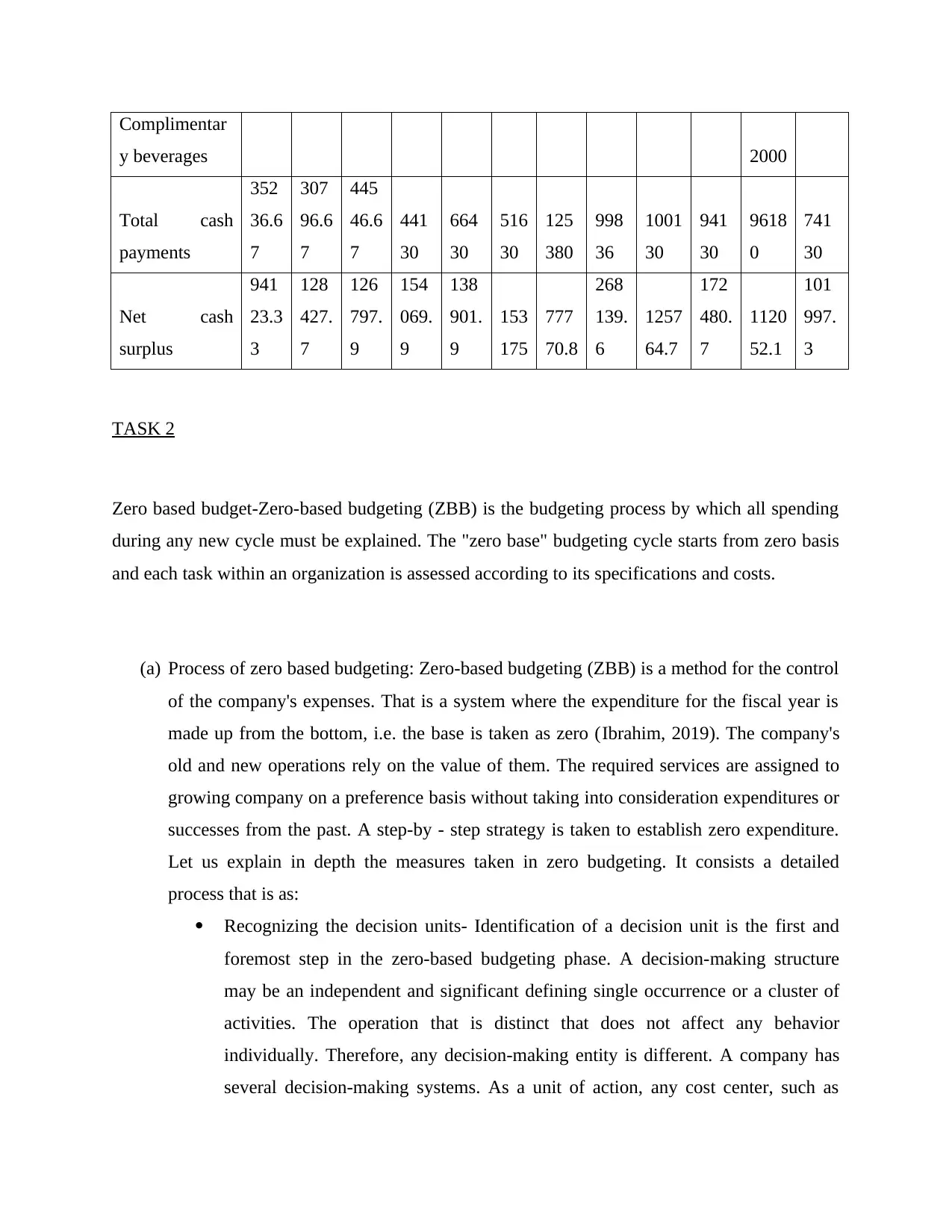

Complimentar

y beverages 2000

Total cash

payments

352

36.6

7

307

96.6

7

445

46.6

7

441

30

664

30

516

30

125

380

998

36

1001

30

941

30

9618

0

741

30

Net cash

surplus

941

23.3

3

128

427.

7

126

797.

9

154

069.

9

138

901.

9

153

175

777

70.8

268

139.

6

1257

64.7

172

480.

7

1120

52.1

101

997.

3

TASK 2

Zero based budget-Zero-based budgeting (ZBB) is the budgeting process by which all spending

during any new cycle must be explained. The "zero base" budgeting cycle starts from zero basis

and each task within an organization is assessed according to its specifications and costs.

(a) Process of zero based budgeting: Zero-based budgeting (ZBB) is a method for the control

of the company's expenses. That is a system where the expenditure for the fiscal year is

made up from the bottom, i.e. the base is taken as zero (Ibrahim, 2019). The company's

old and new operations rely on the value of them. The required services are assigned to

growing company on a preference basis without taking into consideration expenditures or

successes from the past. A step-by - step strategy is taken to establish zero expenditure.

Let us explain in depth the measures taken in zero budgeting. It consists a detailed

process that is as:

Recognizing the decision units- Identification of a decision unit is the first and

foremost step in the zero-based budgeting phase. A decision-making structure

may be an independent and significant defining single occurrence or a cluster of

activities. The operation that is distinct that does not affect any behavior

individually. Therefore, any decision-making entity is different. A company has

several decision-making systems. As a unit of action, any cost center, such as

y beverages 2000

Total cash

payments

352

36.6

7

307

96.6

7

445

46.6

7

441

30

664

30

516

30

125

380

998

36

1001

30

941

30

9618

0

741

30

Net cash

surplus

941

23.3

3

128

427.

7

126

797.

9

154

069.

9

138

901.

9

153

175

777

70.8

268

139.

6

1257

64.7

172

480.

7

1120

52.1

101

997.

3

TASK 2

Zero based budget-Zero-based budgeting (ZBB) is the budgeting process by which all spending

during any new cycle must be explained. The "zero base" budgeting cycle starts from zero basis

and each task within an organization is assessed according to its specifications and costs.

(a) Process of zero based budgeting: Zero-based budgeting (ZBB) is a method for the control

of the company's expenses. That is a system where the expenditure for the fiscal year is

made up from the bottom, i.e. the base is taken as zero (Ibrahim, 2019). The company's

old and new operations rely on the value of them. The required services are assigned to

growing company on a preference basis without taking into consideration expenditures or

successes from the past. A step-by - step strategy is taken to establish zero expenditure.

Let us explain in depth the measures taken in zero budgeting. It consists a detailed

process that is as:

Recognizing the decision units- Identification of a decision unit is the first and

foremost step in the zero-based budgeting phase. A decision-making structure

may be an independent and significant defining single occurrence or a cluster of

activities. The operation that is distinct that does not affect any behavior

individually. Therefore, any decision-making entity is different. A company has

several decision-making systems. As a unit of action, any cost center, such as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

promotion, manufacturing, human resources, research and growth, etc. This step

is necessary to explain any element of budgetary expenditure. Decision unit’s

manager must explain spending and budget allocation for his decision unit.

Measures to Zero Based Budgeting (ZBB) The management's reasoning will not

be focused on the spending for the previous year or on the investment for the past

year of the decision entity. Because the budget from scratch is planned for zero-

based budgeting, it can also be freshly justified with the appropriate budget.

Making decision packages- The decision units defined in the initial stage are

separated into smaller decision bundles. In this process. Such sets of actions will

be aligned with the organization's goals. Growing package of decisions serves as

an individual plan that calls for funding allocation. Each policy package specifies

the roles, tasks and operations of the project, the requirement for proposals, its

economic and intangible advantages, the lack of incentives if the project does not

obtain support, etc. A formal decision package must contain the following

information:

The purpose for which the collection of decisions is taken.

The goals and priorities of the broader decision-making structure.

Decision Package Goals and Targets.

Analysis of task needs.

Assessment of the task's technological and organizational feasibility.

Analysis of the alternative path.

Ranking decision packages- This is the third stage of the budgeting cycle, which

is zero. Within this phase, all packages for decisions are categorized in the order

of significance and preference within the Decision Unit and between different

decision units (Rasugu, 2019). The rationale behind priority decision-making

systems is that finite capital can be distributed effectively. Decision packages are

graded based on an interpretation of cost-benefit. All solutions are analyzed

during this phase in order to choose the correct and most cost-effective choices.

Top leadership holds all the freedom to accept or deny the collection of decisions.

is necessary to explain any element of budgetary expenditure. Decision unit’s

manager must explain spending and budget allocation for his decision unit.

Measures to Zero Based Budgeting (ZBB) The management's reasoning will not

be focused on the spending for the previous year or on the investment for the past

year of the decision entity. Because the budget from scratch is planned for zero-

based budgeting, it can also be freshly justified with the appropriate budget.

Making decision packages- The decision units defined in the initial stage are

separated into smaller decision bundles. In this process. Such sets of actions will

be aligned with the organization's goals. Growing package of decisions serves as

an individual plan that calls for funding allocation. Each policy package specifies

the roles, tasks and operations of the project, the requirement for proposals, its

economic and intangible advantages, the lack of incentives if the project does not

obtain support, etc. A formal decision package must contain the following

information:

The purpose for which the collection of decisions is taken.

The goals and priorities of the broader decision-making structure.

Decision Package Goals and Targets.

Analysis of task needs.

Assessment of the task's technological and organizational feasibility.

Analysis of the alternative path.

Ranking decision packages- This is the third stage of the budgeting cycle, which

is zero. Within this phase, all packages for decisions are categorized in the order

of significance and preference within the Decision Unit and between different

decision units (Rasugu, 2019). The rationale behind priority decision-making

systems is that finite capital can be distributed effectively. Decision packages are

graded based on an interpretation of cost-benefit. All solutions are analyzed

during this phase in order to choose the correct and most cost-effective choices.

Top leadership holds all the freedom to accept or deny the collection of decisions.

Only those packages of decision are accepted that help the company achieve its

established target.

Allocating available resources- The zero-based budgeting phase may follow the

last phase. In this stage, the decision packages which are listed in the last phase

are provided funding. We may then assume that the decisions on finance are made

in this phase. The allocation of funds and other means is focused on the decision

package score. Thus, stronger support is given for the most successful decision

packages. This means that precious services are utilized optimally.

Controlling and monitoring- It is the final move of planning the ZBB. Decision

packages for their efficiency and result are tracked and assessed in this phase.

Measuring the efficiency of decision packages allows administrators to realize if

the resources are distributed appropriately or not.

(a) Advantages of ZBB over traditional budgeting.

The zero based budgeting plays a key role for different types of business. In the case of

above hotel, they can apply this budget which can contribute in future in such manner:

Accuracy- In comparison to traditional budgeting approaches involving unilateral

financial adjustments in the prior year, zero-based budgeting allows all

departments to take care of and measure of the cash flow activities. It aims in a

sense to reduce expenses as it offers a clear picture of expense towards the target

results.

Coordination and communication- It also increases departmental teamwork and

collaboration and motivates staff to engage in decisions (Hijal-Moghrabi, 2019).

Efficiency- It aims to maintain efficient resources allocation (departments-wise),

as it does not analyze the statistical statistics but discusses the current figures.

Reduction in redundant activities- This helps find the potential and cost-effective

approaches to achieve things by removing any non-productive or disruptive

activities.

established target.

Allocating available resources- The zero-based budgeting phase may follow the

last phase. In this stage, the decision packages which are listed in the last phase

are provided funding. We may then assume that the decisions on finance are made

in this phase. The allocation of funds and other means is focused on the decision

package score. Thus, stronger support is given for the most successful decision

packages. This means that precious services are utilized optimally.

Controlling and monitoring- It is the final move of planning the ZBB. Decision

packages for their efficiency and result are tracked and assessed in this phase.

Measuring the efficiency of decision packages allows administrators to realize if

the resources are distributed appropriately or not.

(a) Advantages of ZBB over traditional budgeting.

The zero based budgeting plays a key role for different types of business. In the case of

above hotel, they can apply this budget which can contribute in future in such manner:

Accuracy- In comparison to traditional budgeting approaches involving unilateral

financial adjustments in the prior year, zero-based budgeting allows all

departments to take care of and measure of the cash flow activities. It aims in a

sense to reduce expenses as it offers a clear picture of expense towards the target

results.

Coordination and communication- It also increases departmental teamwork and

collaboration and motivates staff to engage in decisions (Hijal-Moghrabi, 2019).

Efficiency- It aims to maintain efficient resources allocation (departments-wise),

as it does not analyze the statistical statistics but discusses the current figures.

Reduction in redundant activities- This helps find the potential and cost-effective

approaches to achieve things by removing any non-productive or disruptive

activities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(b) How organization can introduce this budget in practical terms.

ZBB facilitates the execution of top-level corporate priorities in the budgeting phase by

connecting them to different operational areas of the business, where expenses can then be

grouped and assessed toward historical results and existing targets (Vadapalli, 2019). This

can be applied in companies in practical life by assessing its needs and nature of operations is

performed inside company. Such as in the aspect of above hotel, it can be applied for each

section whether it is finance or human resource department. By applying this budget, it will

become easier for above company’s manager to bring accuracy in financial data and they will

be able to make effective use of financial resources.

CONCLUSION

On the basis of above project report this can be concluded, budgets are too crucial in the

sense of better financial management. It is so because budgets provide an overview about how to

use financial resources for better purpose. The report articulates about cash budget and its role

for companies. As well as a budget is also prepared in accordance of given financial data. From

the second part of report this can be concluded that zero based budget is an effective budget

which can bring accuracy in financial transactions as well as it can be implemented in any kinds

of organization.

ZBB facilitates the execution of top-level corporate priorities in the budgeting phase by

connecting them to different operational areas of the business, where expenses can then be

grouped and assessed toward historical results and existing targets (Vadapalli, 2019). This

can be applied in companies in practical life by assessing its needs and nature of operations is

performed inside company. Such as in the aspect of above hotel, it can be applied for each

section whether it is finance or human resource department. By applying this budget, it will

become easier for above company’s manager to bring accuracy in financial data and they will

be able to make effective use of financial resources.

CONCLUSION

On the basis of above project report this can be concluded, budgets are too crucial in the

sense of better financial management. It is so because budgets provide an overview about how to

use financial resources for better purpose. The report articulates about cash budget and its role

for companies. As well as a budget is also prepared in accordance of given financial data. From

the second part of report this can be concluded that zero based budget is an effective budget

which can bring accuracy in financial transactions as well as it can be implemented in any kinds

of organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journal:

Colquitt, E.A., 2019. Integrated automated bill and budget reconciliation, cash flow allocation

and payment software system. U.S. Patent 10,210,583.

Labrador, M. and Olmo, J., 2019. Management accounting innovations for rationalizing the cost

of services: The reassessment of cash and accrual accounting. Public Money &

Management, 39(6), pp.401-408.

Verme, P. and Gigliarano, C., 2019. Optimal targeting under budget constraints in a

humanitarian context. World Development, 119, pp.224-233.

Church, B.K., Kuang, X.J. and Liu, Y.S., 2019. The effects of measurement basis and slack

benefits on honesty in budget reporting. Accounting, Organizations and Society, 72,

pp.74-84.

Ibrahim, M.M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management, 17(2).

Rasugu, E.N., 2019. Factors Affecting Implementation of Zero-Based Budgeting In Chemical

Organizations: A Case of Diversey Eastern and Central Africa Limited (Doctoral

dissertation, United States International University-Africa).

Hijal-Moghrabi, I., 2019. Why Is it So Hard to Rationalize the Budgetary Process? A Behavioral

Analysis of Performance-Based Budgeting. Public Organization Review, 19(3), pp.387-

406.

Vadapalli, R., 2019. Relevance of Zero-Based Budgeting (ZBB) to Commercial Banks in Asia

under Present" Slow Economic Growth"-A Perspective on Cost Governance. The

Management Accountant Journal, 54(9), pp.36-39.

Books and journal:

Colquitt, E.A., 2019. Integrated automated bill and budget reconciliation, cash flow allocation

and payment software system. U.S. Patent 10,210,583.

Labrador, M. and Olmo, J., 2019. Management accounting innovations for rationalizing the cost

of services: The reassessment of cash and accrual accounting. Public Money &

Management, 39(6), pp.401-408.

Verme, P. and Gigliarano, C., 2019. Optimal targeting under budget constraints in a

humanitarian context. World Development, 119, pp.224-233.

Church, B.K., Kuang, X.J. and Liu, Y.S., 2019. The effects of measurement basis and slack

benefits on honesty in budget reporting. Accounting, Organizations and Society, 72,

pp.74-84.

Ibrahim, M.M., 2019. Designing zero-based budgeting for public organizations. Problems and

Perspectives in Management, 17(2).

Rasugu, E.N., 2019. Factors Affecting Implementation of Zero-Based Budgeting In Chemical

Organizations: A Case of Diversey Eastern and Central Africa Limited (Doctoral

dissertation, United States International University-Africa).

Hijal-Moghrabi, I., 2019. Why Is it So Hard to Rationalize the Budgetary Process? A Behavioral

Analysis of Performance-Based Budgeting. Public Organization Review, 19(3), pp.387-

406.

Vadapalli, R., 2019. Relevance of Zero-Based Budgeting (ZBB) to Commercial Banks in Asia

under Present" Slow Economic Growth"-A Perspective on Cost Governance. The

Management Accountant Journal, 54(9), pp.36-39.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.