Detailed Cost Management Plan for St Dimas Assisted Living Project

VerifiedAdded on 2021/06/17

|4

|990

|26

Project

AI Summary

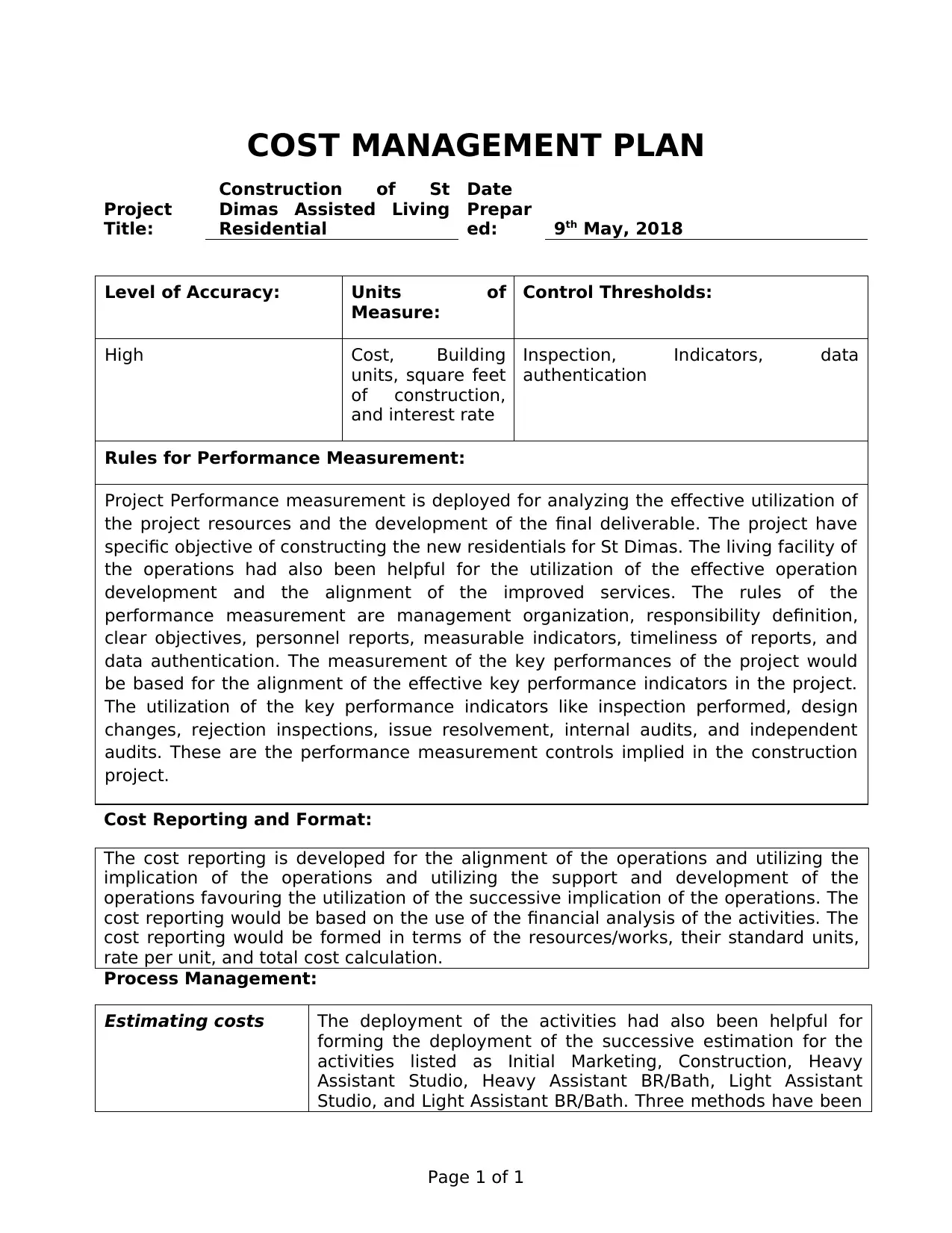

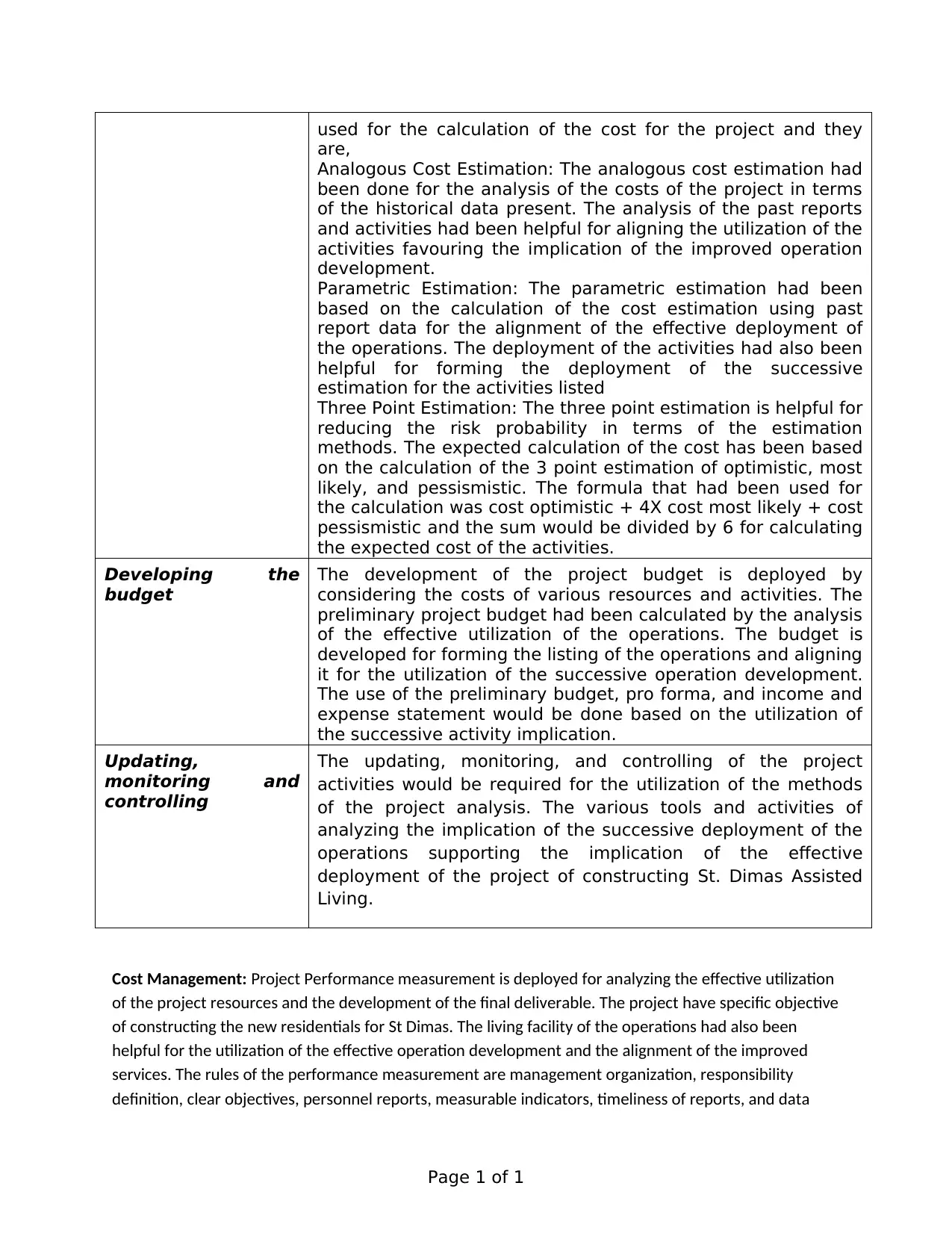

This project presents a detailed cost management plan for the construction of St. Dimas Assisted Living residential facility. It outlines the project's objectives, performance measurement rules, and cost reporting formats. The plan covers various aspects of cost management, including estimating costs using analogous, parametric, and three-point estimation methods. It also addresses budget development, updating, monitoring, and controlling project activities. The project emphasizes the importance of project performance measurement for effective resource utilization and achieving project deliverables. Key performance indicators like inspections, design changes, and audits are used to monitor project progress and ensure cost control. The document also includes a bibliography of relevant academic sources.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.