ST Marine Case Study: An Analysis of Corporate Ethical Failures

VerifiedAdded on 2021/04/21

|14

|2839

|81

Case Study

AI Summary

This case study analyzes the ethical failures within Singapore Technologies (ST) Marine, focusing on the falsification of accounts, employee bribery, and abuse of power. The case details how senior executives, including the vice president of finance, engaged in fraudulent activities to facilitate bribes to customers' employees, resulting in a minimum of S$24.9 million in bribes over twelve years. The analysis identifies accounting fraud as a primary issue, highlighting how falsified expense claims were used to siphon money and award contracts unfairly. It also examines the bribery of employees to secure contracts and the abuse of power by senior management. The study recommends the implementation of ethical culture, multiple reporting mechanisms, transparent procurement processes, and employee awareness programs to prevent future occurrences. The document provides a comprehensive overview of the case, referencing relevant literature to support its findings and recommendations. The ST Marine case highlights the importance of ethical conduct, corporate governance, and internal controls in preventing financial misconduct.

Running head: ST Marine Case Analysis 1

ST Marine Case Analysis

by

Course:

Tutor:

University:

Department:

Date:

ST Marine Case Analysis

by

Course:

Tutor:

University:

Department:

Date:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ST Marine Case Analysis 2

Table of Contents

1.0 Introduction..........................................................................................................................3

2.0 Case Analysis.......................................................................................................................3

3.0 Recommendations................................................................................................................7

4.0 Conclusions..........................................................................................................................9

References................................................................................................................................10

Appendix: PBL Worksheet......................................................................................................13

Table of Contents

1.0 Introduction..........................................................................................................................3

2.0 Case Analysis.......................................................................................................................3

3.0 Recommendations................................................................................................................7

4.0 Conclusions..........................................................................................................................9

References................................................................................................................................10

Appendix: PBL Worksheet......................................................................................................13

ST Marine Case Analysis 3

1.0 Introduction

The case is about account falsification of S$48,887 by the former senior vice-president

(finance) and group financial controller of Singapore Technologies (ST) Marine group. Ong

Teck Liam (vice president) and other four top executives pleaded guilty to several charges.

The court learned that this practice was carried out to facilitate the payment of bribes to the

employees of ST Maritime customers. This report examines the case and lists of the issues

while justifying them. An in-depth explanation of each problem is provided and research

journals used to justify the actions as illegal, question the activities and offers conceivable

alternative resolutions. Section one deals with case analysis and three issues in the case are

identified and justified namely accounting fraud, employee bribery and abuse of power.

Recommendations are then made for each of the problems identified.

2.0 Case Analysis

The issues in the case can be summarised into three, namely, accounting fraud/falsification of

accounts, bribing of employees for favors in business and abuse of power or authority.

2.1 Accounting Fraud

Accounting fraud is the process by which accounting experts employ their knowledge to

manipulate the figures in the account books (Jones, 2011). According to Bebbington et al.

(2014), the process of accounting in its nature demands the execution of varied motives and

ideas. It is from this diversity that manipulation arises, falsehood and fabrication at some less

trustworthy accounting staff. According to Section 477A of the penal code of the Singapore

constitution, falsification of accounts is deemed as accounting fraud. An account can be any

book, writing, or any security of value. Accounting fraud takes place when there is a breach

in the financial system of an organization such that the fraud is not easily detected (Sharma,

& Panigrahi, 2013). Also, the scam usually involves more than one person because any

1.0 Introduction

The case is about account falsification of S$48,887 by the former senior vice-president

(finance) and group financial controller of Singapore Technologies (ST) Marine group. Ong

Teck Liam (vice president) and other four top executives pleaded guilty to several charges.

The court learned that this practice was carried out to facilitate the payment of bribes to the

employees of ST Maritime customers. This report examines the case and lists of the issues

while justifying them. An in-depth explanation of each problem is provided and research

journals used to justify the actions as illegal, question the activities and offers conceivable

alternative resolutions. Section one deals with case analysis and three issues in the case are

identified and justified namely accounting fraud, employee bribery and abuse of power.

Recommendations are then made for each of the problems identified.

2.0 Case Analysis

The issues in the case can be summarised into three, namely, accounting fraud/falsification of

accounts, bribing of employees for favors in business and abuse of power or authority.

2.1 Accounting Fraud

Accounting fraud is the process by which accounting experts employ their knowledge to

manipulate the figures in the account books (Jones, 2011). According to Bebbington et al.

(2014), the process of accounting in its nature demands the execution of varied motives and

ideas. It is from this diversity that manipulation arises, falsehood and fabrication at some less

trustworthy accounting staff. According to Section 477A of the penal code of the Singapore

constitution, falsification of accounts is deemed as accounting fraud. An account can be any

book, writing, or any security of value. Accounting fraud takes place when there is a breach

in the financial system of an organization such that the fraud is not easily detected (Sharma,

& Panigrahi, 2013). Also, the scam usually involves more than one person because any

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ST Marine Case Analysis 4

financial transaction or approval must undergo a process which involves various financial

managers vested with different authorities.

In the case under study, the account falsification was carried out by the vice-president of

finance by signing a set of bogus cheques falsified as refunds to the employees for the

entertainment expenses which were never incurred in reality. The reason for the falsification

of the accounts was to siphon money from the company and to bribe the employees’ of ST

Marine’s customers. This act amounts to accounting fraud and the vice president (finance),

Ong, is guilty of the offense. To make matters worse, she had detected this irregularity when

she was first employed at ST Marine, Ong was asked to sign cash cheques which had no

supporting receipts, and when she questioned her staff in the finance department, she was

notified of the illegality and that it had become a tradition. She agreed to join the status quo

and proceeded with false processing claims after hearing that former senior executives had

practiced the irregularity for over 12 years. She was even given a document on how to

secretly forge the claims without notice. Other officials that negotiated and paid the cash

bribes did so under the permission of the executive management of ST Marine such as the

former chief operating officer Han Kwang; ST Marine president See Teck among others.

The management should have fraud detection methods in place, and they should be visible to

all the staff. According to Omar et al. (2016), the visibility of the control methods to the

employees helps to prevent fraudulent behaviors. The organization should adopt multiple

reporting mechanisms as a way of detecting and preventing fraud (Stubbs, & Higgins, 2014).

Thus, the HR department needs to restructure the organizations reporting structure to

accommodate multiple report mechanisms.

2.2 Bribing of employees.

financial transaction or approval must undergo a process which involves various financial

managers vested with different authorities.

In the case under study, the account falsification was carried out by the vice-president of

finance by signing a set of bogus cheques falsified as refunds to the employees for the

entertainment expenses which were never incurred in reality. The reason for the falsification

of the accounts was to siphon money from the company and to bribe the employees’ of ST

Marine’s customers. This act amounts to accounting fraud and the vice president (finance),

Ong, is guilty of the offense. To make matters worse, she had detected this irregularity when

she was first employed at ST Marine, Ong was asked to sign cash cheques which had no

supporting receipts, and when she questioned her staff in the finance department, she was

notified of the illegality and that it had become a tradition. She agreed to join the status quo

and proceeded with false processing claims after hearing that former senior executives had

practiced the irregularity for over 12 years. She was even given a document on how to

secretly forge the claims without notice. Other officials that negotiated and paid the cash

bribes did so under the permission of the executive management of ST Marine such as the

former chief operating officer Han Kwang; ST Marine president See Teck among others.

The management should have fraud detection methods in place, and they should be visible to

all the staff. According to Omar et al. (2016), the visibility of the control methods to the

employees helps to prevent fraudulent behaviors. The organization should adopt multiple

reporting mechanisms as a way of detecting and preventing fraud (Stubbs, & Higgins, 2014).

Thus, the HR department needs to restructure the organizations reporting structure to

accommodate multiple report mechanisms.

2.2 Bribing of employees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ST Marine Case Analysis 5

Bribery is an act where corrupt dealings are carried out with employees of potential

contractors or customers with the aim of securing a commercial advantage over competitors

(Ameyaw et al., 2012). Cases of bribery have become common in the current competitive

and financial crisis market where each organization is ready to go for any miles including

engaging in illegalities to ensure that they remain competitive in the market and perform the

best. Bribery is another form of corruption, an act that is illegalized by all nations in the

world because it weakens the markets and welfare, and makes the leadership, institutions, and

businesses to appear distrustful (Brammer, & Walker, 2011). Cheung, Rau, & Stouraitis,

(2012) assert that bribe allegations can take different forms depending on the nature of the

business and are deemed by firms as the sure shortcut to company development and success.

In the case of account falsification in Singapore, employees of ST Marine customers’ were

bribed so that they could award contracts for ship repair, building, or conversion services.

This also compromises the procedure that is required in the awarding of contracts, where all

the bidders are evaluated, and the winner is awarded by qualification only. The ship repair

contracts were awarded because the employees of the customer company had been

compromised through a bribe. Thus ST Marine gained an unfair advantage over their

competitors hence amounting to a crime punishable in any court of law. Just like Cheung,

Rau, & Stouraitis, (2012) note that firms engage in bribes for the award of contracts for more

significant benefits, ST Marine is an example to that effect. The court found out that ST

Marine had spent a minimum of S$24.9 million in bribes for over twelve years. This is

evidence that the company was gaining from its practice of bribing even though it was illegal.

The verdict of the court of law on Ong guilty for accounting fraud and facilitating bribe

alongside four other senior executives is proof of the illegality of their actions.

To stop the culture of employee bribery at ST Marine which has been fostered for long, the

organization needs to create a transparent and open process of contract acquisition. The HR

Bribery is an act where corrupt dealings are carried out with employees of potential

contractors or customers with the aim of securing a commercial advantage over competitors

(Ameyaw et al., 2012). Cases of bribery have become common in the current competitive

and financial crisis market where each organization is ready to go for any miles including

engaging in illegalities to ensure that they remain competitive in the market and perform the

best. Bribery is another form of corruption, an act that is illegalized by all nations in the

world because it weakens the markets and welfare, and makes the leadership, institutions, and

businesses to appear distrustful (Brammer, & Walker, 2011). Cheung, Rau, & Stouraitis,

(2012) assert that bribe allegations can take different forms depending on the nature of the

business and are deemed by firms as the sure shortcut to company development and success.

In the case of account falsification in Singapore, employees of ST Marine customers’ were

bribed so that they could award contracts for ship repair, building, or conversion services.

This also compromises the procedure that is required in the awarding of contracts, where all

the bidders are evaluated, and the winner is awarded by qualification only. The ship repair

contracts were awarded because the employees of the customer company had been

compromised through a bribe. Thus ST Marine gained an unfair advantage over their

competitors hence amounting to a crime punishable in any court of law. Just like Cheung,

Rau, & Stouraitis, (2012) note that firms engage in bribes for the award of contracts for more

significant benefits, ST Marine is an example to that effect. The court found out that ST

Marine had spent a minimum of S$24.9 million in bribes for over twelve years. This is

evidence that the company was gaining from its practice of bribing even though it was illegal.

The verdict of the court of law on Ong guilty for accounting fraud and facilitating bribe

alongside four other senior executives is proof of the illegality of their actions.

To stop the culture of employee bribery at ST Marine which has been fostered for long, the

organization needs to create a transparent and open process of contract acquisition. The HR

ST Marine Case Analysis 6

team should modify the policies on the procurement process after serious scrutiny to detect

any loopholes. Armstrong & Taylor (2014) reasons that organizational policies on

procurement serve to prevent any gaps where only a few people are involved in the process.

The human resource department should also encourage awareness of the code of ethics at the

workplace (Bishop, 2013). The HR management should organize seminars and workshops to

sensitize the employees of these ethics.

Source: (Bishop, 2013)

2.3 Abuse of power

Abuse of power is an act that is practiced by those of higher authorities at the workplace and

is regarded as a crime (Rosenblatt, 2012). Abuse of authority can take place in different

forms depending on the situation (Bartling, Fehr, & Schmidt, 2013). Abuse of power can be

defined as taking advantage of the vested powers and misusing them for vested interest. In

the case, the allegations of account falsification are perpetrated by senior executive officers of

ST Marine who include the senior vice-president of finance, the former chief operating

officer, Aerospace president among others. Ong who was the vice-president (finance) is the

one vested with the authority of approving any financial expenses and without her signature,

Integrity

Accountability

Transparency

Professionalism

HRM Code of Ethics

team should modify the policies on the procurement process after serious scrutiny to detect

any loopholes. Armstrong & Taylor (2014) reasons that organizational policies on

procurement serve to prevent any gaps where only a few people are involved in the process.

The human resource department should also encourage awareness of the code of ethics at the

workplace (Bishop, 2013). The HR management should organize seminars and workshops to

sensitize the employees of these ethics.

Source: (Bishop, 2013)

2.3 Abuse of power

Abuse of power is an act that is practiced by those of higher authorities at the workplace and

is regarded as a crime (Rosenblatt, 2012). Abuse of authority can take place in different

forms depending on the situation (Bartling, Fehr, & Schmidt, 2013). Abuse of power can be

defined as taking advantage of the vested powers and misusing them for vested interest. In

the case, the allegations of account falsification are perpetrated by senior executive officers of

ST Marine who include the senior vice-president of finance, the former chief operating

officer, Aerospace president among others. Ong who was the vice-president (finance) is the

one vested with the authority of approving any financial expenses and without her signature,

Integrity

Accountability

Transparency

Professionalism

HRM Code of Ethics

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ST Marine Case Analysis 7

no money can be released. This is the same case with other senior management officials

implicated in the case. The document on how to manipulate figures in the finance department

was presented to Ong after she suspected some illegality in the cash cheques she was to

approve. She as informed that the former chief operating officer used to authorize the

disbursement of such fictitious claims. This, therefore, implies that the culture of accounting

fraud was initiated and propelled by those in power whose responsibility was to prevent such

issues from taking place. According to Wells (2013), it is the senior management that is

usually in the forefront in the cases of briberies for the award of contracts because they would

want the organizations they are heading to perform and this way serves to be a quicker

method.

The issue of misuse of power in the case is a result of the lack of efficient and effective audit

by the board of directors. To curb any possibility of this issue arising again, ST Marine

should set a reporting system where all the staff in the organization are made aware of the

fraud risk policy and the associated consequences (Joseph et al., 2015). The human resource

management should organize for a routine awareness campaign in addition to sticking

organizational values at common meeting places to continually remind the employees of what

is expected of them. The organization should also implement internal controls that will ensure

the safety of accounting records. This can be done by segregating duties in the finance

department so that not a single individual can ratify a financial transaction (Adetoso et al.,

2013).

3.0 Recommendations

The issue surrounding the case of ST Marine for over 12 years now is an ethical issue that

requires the establishment and development of an ethical culture. Goetsch, & Davis (2014)

observes that ethics management process is the central role of the HR department in

no money can be released. This is the same case with other senior management officials

implicated in the case. The document on how to manipulate figures in the finance department

was presented to Ong after she suspected some illegality in the cash cheques she was to

approve. She as informed that the former chief operating officer used to authorize the

disbursement of such fictitious claims. This, therefore, implies that the culture of accounting

fraud was initiated and propelled by those in power whose responsibility was to prevent such

issues from taking place. According to Wells (2013), it is the senior management that is

usually in the forefront in the cases of briberies for the award of contracts because they would

want the organizations they are heading to perform and this way serves to be a quicker

method.

The issue of misuse of power in the case is a result of the lack of efficient and effective audit

by the board of directors. To curb any possibility of this issue arising again, ST Marine

should set a reporting system where all the staff in the organization are made aware of the

fraud risk policy and the associated consequences (Joseph et al., 2015). The human resource

management should organize for a routine awareness campaign in addition to sticking

organizational values at common meeting places to continually remind the employees of what

is expected of them. The organization should also implement internal controls that will ensure

the safety of accounting records. This can be done by segregating duties in the finance

department so that not a single individual can ratify a financial transaction (Adetoso et al.,

2013).

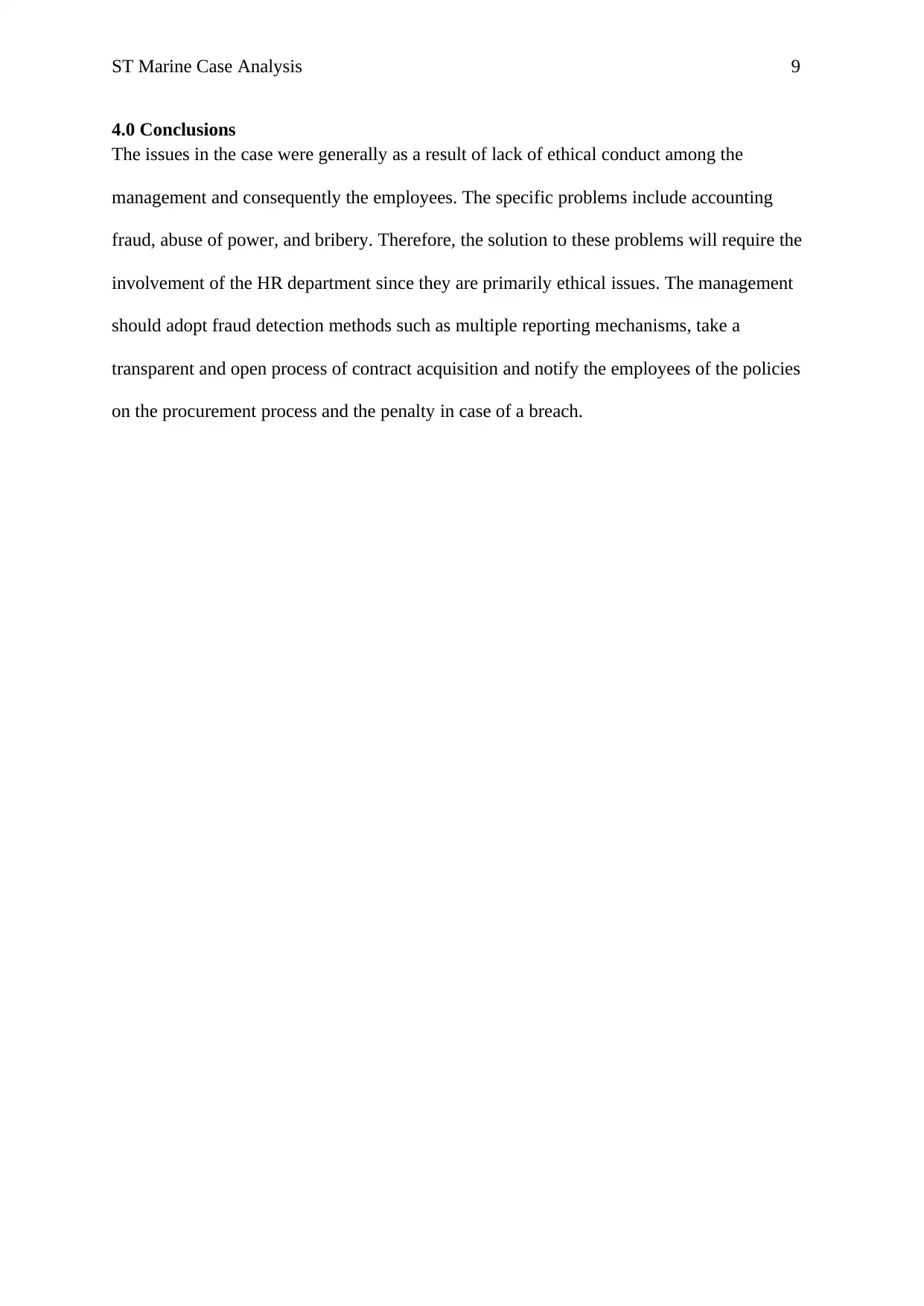

3.0 Recommendations

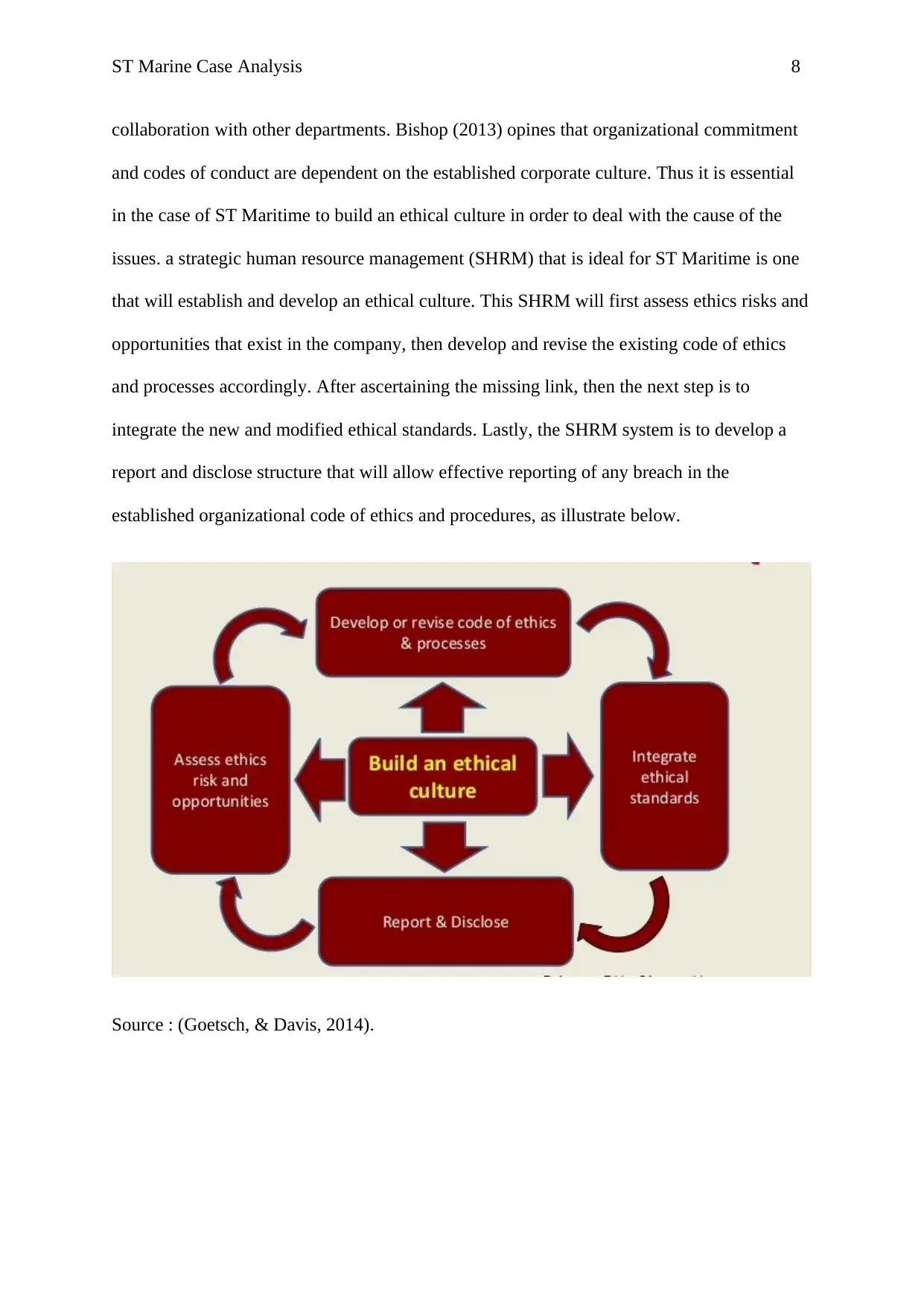

The issue surrounding the case of ST Marine for over 12 years now is an ethical issue that

requires the establishment and development of an ethical culture. Goetsch, & Davis (2014)

observes that ethics management process is the central role of the HR department in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ST Marine Case Analysis 8

collaboration with other departments. Bishop (2013) opines that organizational commitment

and codes of conduct are dependent on the established corporate culture. Thus it is essential

in the case of ST Maritime to build an ethical culture in order to deal with the cause of the

issues. a strategic human resource management (SHRM) that is ideal for ST Maritime is one

that will establish and develop an ethical culture. This SHRM will first assess ethics risks and

opportunities that exist in the company, then develop and revise the existing code of ethics

and processes accordingly. After ascertaining the missing link, then the next step is to

integrate the new and modified ethical standards. Lastly, the SHRM system is to develop a

report and disclose structure that will allow effective reporting of any breach in the

established organizational code of ethics and procedures, as illustrate below.

Source : (Goetsch, & Davis, 2014).

collaboration with other departments. Bishop (2013) opines that organizational commitment

and codes of conduct are dependent on the established corporate culture. Thus it is essential

in the case of ST Maritime to build an ethical culture in order to deal with the cause of the

issues. a strategic human resource management (SHRM) that is ideal for ST Maritime is one

that will establish and develop an ethical culture. This SHRM will first assess ethics risks and

opportunities that exist in the company, then develop and revise the existing code of ethics

and processes accordingly. After ascertaining the missing link, then the next step is to

integrate the new and modified ethical standards. Lastly, the SHRM system is to develop a

report and disclose structure that will allow effective reporting of any breach in the

established organizational code of ethics and procedures, as illustrate below.

Source : (Goetsch, & Davis, 2014).

ST Marine Case Analysis 9

4.0 Conclusions

The issues in the case were generally as a result of lack of ethical conduct among the

management and consequently the employees. The specific problems include accounting

fraud, abuse of power, and bribery. Therefore, the solution to these problems will require the

involvement of the HR department since they are primarily ethical issues. The management

should adopt fraud detection methods such as multiple reporting mechanisms, take a

transparent and open process of contract acquisition and notify the employees of the policies

on the procurement process and the penalty in case of a breach.

4.0 Conclusions

The issues in the case were generally as a result of lack of ethical conduct among the

management and consequently the employees. The specific problems include accounting

fraud, abuse of power, and bribery. Therefore, the solution to these problems will require the

involvement of the HR department since they are primarily ethical issues. The management

should adopt fraud detection methods such as multiple reporting mechanisms, take a

transparent and open process of contract acquisition and notify the employees of the policies

on the procurement process and the penalty in case of a breach.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ST Marine Case Analysis 10

References

Adetoso, J., Oladejo, K., & Akesinro, A. S. (2013). Effectiveness of internal auditor in

controlling fraud and other financial irregularities in private universities in south-

west, Nigeria. Research Journal of Finance and Accounting, 4(13), 106-110.

Ameyaw, C., Mensah, S., & Osei-Tutu, E. (2012). Public procurement in Ghana: the

implementation challenges to the public procurement law 2003 (Act 663).

International Journal of Construction supply chain management, 2(2), 55-65.

Armstrong, M., & Taylor, S. (2014). Armstrong's handbook of human resource management

practice. Kogan Page Publishers.

Bartling, B., Fehr, E., & Schmidt, K. M. (2013). Jeea-Fbbva Lecture 2012: Use and Abuse of

Authority: A Behavioral Foundation of the Employment Relation. Journal of the

European Economic Association, 11(4), 711-742.

Bebbington, J., Unerman, J., & O'Dwyer, B. (Eds.). (2014). Sustainability accounting and

accountability. Routledge.

Bishop, W. H. (2013). The role of ethics in 21st century organizations. Journal of Business

Ethics, 118(3), 635-637.

Brammer, S., & Walker, H. (2011). Sustainable procurement in the public sector: an

international comparative study. International Journal of Operations & Production

Management, 31(4), 452-476.

Cheung, Y. L., Rau, P. R., & Stouraitis, A. (2012). How much do firms pay as bribes and

References

Adetoso, J., Oladejo, K., & Akesinro, A. S. (2013). Effectiveness of internal auditor in

controlling fraud and other financial irregularities in private universities in south-

west, Nigeria. Research Journal of Finance and Accounting, 4(13), 106-110.

Ameyaw, C., Mensah, S., & Osei-Tutu, E. (2012). Public procurement in Ghana: the

implementation challenges to the public procurement law 2003 (Act 663).

International Journal of Construction supply chain management, 2(2), 55-65.

Armstrong, M., & Taylor, S. (2014). Armstrong's handbook of human resource management

practice. Kogan Page Publishers.

Bartling, B., Fehr, E., & Schmidt, K. M. (2013). Jeea-Fbbva Lecture 2012: Use and Abuse of

Authority: A Behavioral Foundation of the Employment Relation. Journal of the

European Economic Association, 11(4), 711-742.

Bebbington, J., Unerman, J., & O'Dwyer, B. (Eds.). (2014). Sustainability accounting and

accountability. Routledge.

Bishop, W. H. (2013). The role of ethics in 21st century organizations. Journal of Business

Ethics, 118(3), 635-637.

Brammer, S., & Walker, H. (2011). Sustainable procurement in the public sector: an

international comparative study. International Journal of Operations & Production

Management, 31(4), 452-476.

Cheung, Y. L., Rau, P. R., & Stouraitis, A. (2012). How much do firms pay as bribes and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ST Marine Case Analysis 11

what benefits do they get? Evidence from corruption cases worldwide (No. w17981).

National Bureau of Economic Research.

Goetsch, D. L., & Davis, S. B. (2014). Quality management for organizational excellence.

Upper Saddle River, NJ: pearson.

Jones, M. (Ed.). (2011). Creative accounting, fraud and international accounting scandals.

John Wiley & Sons.

Joseph, O. N., Albert, O., & Byaruhanga, J. (2015). Effect of Internal Control on Fraud

Detection and Prevention in District Treasuries of Kakamega County. Int. J. Bus.

Manag. Invent, 4(1), 47-57.

Omar, M., Nawawi, A., & Puteh Salin, A. S. A. (2016). The causes, impact and prevention of

employee fraud: A case study of an automotive company. Journal of Financial Crime,

23(4), 1012-1027.

Rosenblatt, V. (2012). Hierarchies, power inequalities, and organizational corruption. Journal

of Business Ethics, 111(2), 237-251.

Sharma, A., & Panigrahi, P. K. (2013). A review of financial accounting fraud detection

based on data mining techniques. arXiv preprint arXiv:1309.3944.

Stubbs, W., & Higgins, C. (2014). Integrated reporting and internal mechanisms of

change. Accounting, Auditing & Accountability Journal, 27(7), 1068-1089.

Wells, J. (2013). Corruption and collusion in construction: A view from the

what benefits do they get? Evidence from corruption cases worldwide (No. w17981).

National Bureau of Economic Research.

Goetsch, D. L., & Davis, S. B. (2014). Quality management for organizational excellence.

Upper Saddle River, NJ: pearson.

Jones, M. (Ed.). (2011). Creative accounting, fraud and international accounting scandals.

John Wiley & Sons.

Joseph, O. N., Albert, O., & Byaruhanga, J. (2015). Effect of Internal Control on Fraud

Detection and Prevention in District Treasuries of Kakamega County. Int. J. Bus.

Manag. Invent, 4(1), 47-57.

Omar, M., Nawawi, A., & Puteh Salin, A. S. A. (2016). The causes, impact and prevention of

employee fraud: A case study of an automotive company. Journal of Financial Crime,

23(4), 1012-1027.

Rosenblatt, V. (2012). Hierarchies, power inequalities, and organizational corruption. Journal

of Business Ethics, 111(2), 237-251.

Sharma, A., & Panigrahi, P. K. (2013). A review of financial accounting fraud detection

based on data mining techniques. arXiv preprint arXiv:1309.3944.

Stubbs, W., & Higgins, C. (2014). Integrated reporting and internal mechanisms of

change. Accounting, Auditing & Accountability Journal, 27(7), 1068-1089.

Wells, J. (2013). Corruption and collusion in construction: A view from the

ST Marine Case Analysis 12

industry. Corruption, grabbing and development: real world challenges. ISBN:

7781782544401 D, 1, 23-24.

industry. Corruption, grabbing and development: real world challenges. ISBN:

7781782544401 D, 1, 23-24.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.