Cost Overruns and Stakeholder Roles in Construction Projects: A Review

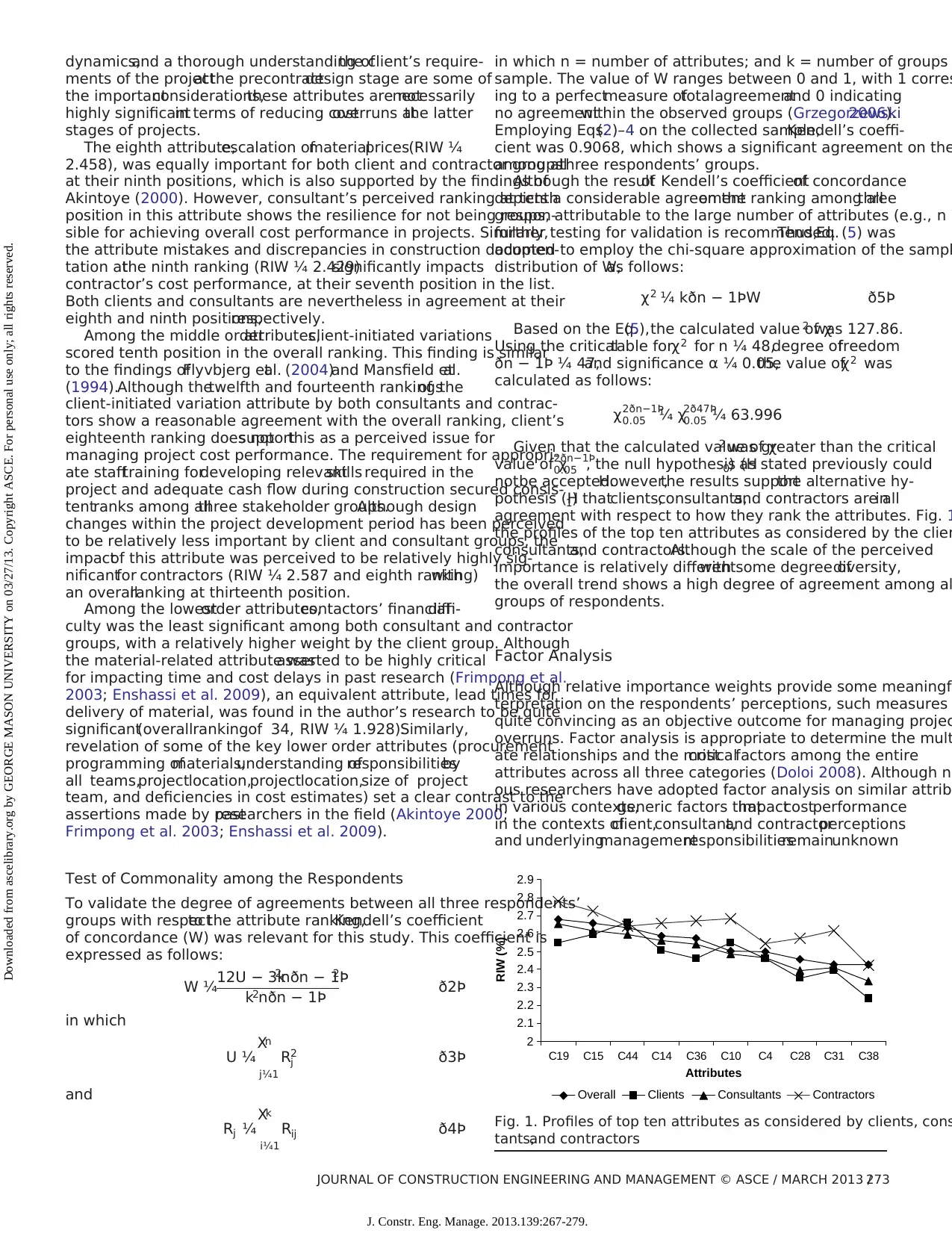

VerifiedAdded on 2022/10/11

|13

|14788

|76

Report

AI Summary

This report examines the issue of cost overruns in construction projects, a chronic problem in the industry. It delves into the roles and responsibilities of key stakeholders, including clients, consultants, and contractors, in managing these overruns. The research, based on a literature review and industry inputs, identifies 73 attributes related to cost performance. Planning and scheduling deficiencies are found to have the highest impact, with robust control procedures, adequate programming, efficient design, and effective site management being critical factors. The client's role in facilitating effective management of these factors is also crucial. Multivariate regression analysis highlights the influence of five significant factors on managing cost overruns. The findings aim to bridge a knowledge gap by shifting priorities in cost estimation and management practices across all industry sectors. The report also includes a literature review of factors affecting cost performance, such as poor site management, decision-making speed, and client-initiated variations, emphasizing the need for a comprehensive understanding of stakeholder responsibilities to improve cost performance.

Cost Overruns and Failure in Project

Management: Understanding the Roles

of Key Stakeholders in Construction Projects

Hemanta Doloi1

Abstract: The subjectof poorcostperformance has been widely published in the mainstream projectand construction management

literature. Nevertheless, the underlying responsibilities of the key stakeholders (clients, consultants, and contractors) in

problem in the Australian construction industry remain unclear. By performing an in-depth analysis of the roles and resp

key stakeholders, this research is intended to unfold the industrywide perception of cost performance being heavily relia

performance alone.Based on a thorough literature review and relevantindustry inputs,73 attributes associated with costperformance

were identified for investigation.Based on the relative importance weighing technique on 48 selected attributes,planning and scheduling

deficiencies have the highest impact on cost performance from clients, consultants, and contractors’ perspectives. Confi

sis on the combined responses across all three groups suggests that robust control procedures and adequate programm

design and effective site management,are the mostcriticalfactors.These factors are primarily associated with the responsibilities o

contractors and consultants for managing cost overruns in projects. However, the client’s responsibility in facilitating eff

of these factors within the project environment is crucial. Multivariate regression analysis performed on eight factors’ sc

influence of five significant factors (p < 5%) on managing cost overruns. The findings are expected to abridge a significa

shifting the priorities in costestimation and managementpractices across allindustry sectors.DOI: 10.1061/(ASCE)CO.1943-7862

.0000621.© 2013 American Society ofCivil Engineers.

CE Database subject headings: Construction costs; Estimation;Projectmanagement.

Author keywords: Costoverrun;Costestimation;Costperformance; Projectmanagement.

Introduction

The factors thatinfluence costduring the conception and design

phases within the construction process have been widely investi-

gated, primarily based on the contractor’s cost-estimating practices

(Akintoye 2000; Cheung et al.2008).Hicks (1992) revealed that

regardless of management competence and the financial strength of

the contractor, accurate cost estimation at an early stage is the key

to avoid cost overrun in projects (Hicks 1992). Cost estimation is a

technicalprocess of predicting expenditure,and success depends

on accurate integration of project information, resources, and con-

trolover projectimplementation (Baloiand Price 2003).Factors

influencing cost performance based on initial estimates have been

widely published and primarily concern project complexity,tech-

nology requirements,vagueness in scope,and the projectteam

requirements (Mansfield etal. 1994;Akintoye 2000;Frimpong

et al. 2003; Love et al. 2005). Empirical evidence suggests that con-

tractors’ efficiency in the estimating process and appropriate tender

pricing depictsthe cost performancein construction projects

(Skitmore and Wilcock 1994). Therefore, contractors’ ability in us-

ing sophisticated methods and their rationalizations atthe tender

development stage are considered crucial in achieving cost success

in mostprojects (Green 1989).In many instances,all of these

factorsidentified atan early stage ofthe construction process

are described as uncontrollable risks (Akinciand Fischer 1998).

Appropriate consideration ofthese uncontrollable risksduring

the initialstage ofthe estimating phase significantly increases

the chance ofminimizing any mistakes overthe course ofthe

construction phase. However, some of the key questions regar

responsibility,deliberation,and managementof such risks in the

construction supply chain remain unclear in the discipline dom

Identification ofthe cost-related risks,underlying drivers,and

impediments foreffective managementmustbe assessed in the

contextsof threekey stakeholders:clients,contractors,and

consultants.

This research is intended to investigate the perceived unde

standing and importance of the key attributes among these th

key stakeholders’ groups with respect to achieving the target

performance in projects.Estimation of projectcosts atthe early

stages of the design process and the ability to manage these c

throughout the construction phase is paramount to a project’s

all success. Past research illustrates that construction cost ove

and the subsequent poor cost performance are the attributes

lack of understanding among allparticipating teams across the

construction industry (Akintoye 2000;Frimpong etal. 2003).

However,an accurate understanding ofthe key attributes in the

context of the responsibility and management ability among c

and consultantcontractors has notbeen explored.By identifying

the factors affecting costoverruns,this research highlights the

criticality fortheireffective managementwithin the rolesand

responsibilitiesamong clients,consultants,and contractorsin

construction projects.

1Senior Lecturer, Faculty of Architecture, Building and Planning, Univ.

of Melbourne,Victoria 3010,Australia.E-mail:hdoloi@unimelb.edu.au

Note. This manuscript was submitted on November 13, 2009; approved

on June 6, 2012; published online on July 25, 2012. Discussion period open

until August 1, 2013; separate discussions must be submitted for individual

papers. This paper is part of the Journal of Construction Engineering and

Management, Vol. 139, No. 3, March 1, 2013. © ASCE, ISSN 0733-9364/

2013/3-267-279/$25.00.

JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013 /267

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

Management: Understanding the Roles

of Key Stakeholders in Construction Projects

Hemanta Doloi1

Abstract: The subjectof poorcostperformance has been widely published in the mainstream projectand construction management

literature. Nevertheless, the underlying responsibilities of the key stakeholders (clients, consultants, and contractors) in

problem in the Australian construction industry remain unclear. By performing an in-depth analysis of the roles and resp

key stakeholders, this research is intended to unfold the industrywide perception of cost performance being heavily relia

performance alone.Based on a thorough literature review and relevantindustry inputs,73 attributes associated with costperformance

were identified for investigation.Based on the relative importance weighing technique on 48 selected attributes,planning and scheduling

deficiencies have the highest impact on cost performance from clients, consultants, and contractors’ perspectives. Confi

sis on the combined responses across all three groups suggests that robust control procedures and adequate programm

design and effective site management,are the mostcriticalfactors.These factors are primarily associated with the responsibilities o

contractors and consultants for managing cost overruns in projects. However, the client’s responsibility in facilitating eff

of these factors within the project environment is crucial. Multivariate regression analysis performed on eight factors’ sc

influence of five significant factors (p < 5%) on managing cost overruns. The findings are expected to abridge a significa

shifting the priorities in costestimation and managementpractices across allindustry sectors.DOI: 10.1061/(ASCE)CO.1943-7862

.0000621.© 2013 American Society ofCivil Engineers.

CE Database subject headings: Construction costs; Estimation;Projectmanagement.

Author keywords: Costoverrun;Costestimation;Costperformance; Projectmanagement.

Introduction

The factors thatinfluence costduring the conception and design

phases within the construction process have been widely investi-

gated, primarily based on the contractor’s cost-estimating practices

(Akintoye 2000; Cheung et al.2008).Hicks (1992) revealed that

regardless of management competence and the financial strength of

the contractor, accurate cost estimation at an early stage is the key

to avoid cost overrun in projects (Hicks 1992). Cost estimation is a

technicalprocess of predicting expenditure,and success depends

on accurate integration of project information, resources, and con-

trolover projectimplementation (Baloiand Price 2003).Factors

influencing cost performance based on initial estimates have been

widely published and primarily concern project complexity,tech-

nology requirements,vagueness in scope,and the projectteam

requirements (Mansfield etal. 1994;Akintoye 2000;Frimpong

et al. 2003; Love et al. 2005). Empirical evidence suggests that con-

tractors’ efficiency in the estimating process and appropriate tender

pricing depictsthe cost performancein construction projects

(Skitmore and Wilcock 1994). Therefore, contractors’ ability in us-

ing sophisticated methods and their rationalizations atthe tender

development stage are considered crucial in achieving cost success

in mostprojects (Green 1989).In many instances,all of these

factorsidentified atan early stage ofthe construction process

are described as uncontrollable risks (Akinciand Fischer 1998).

Appropriate consideration ofthese uncontrollable risksduring

the initialstage ofthe estimating phase significantly increases

the chance ofminimizing any mistakes overthe course ofthe

construction phase. However, some of the key questions regar

responsibility,deliberation,and managementof such risks in the

construction supply chain remain unclear in the discipline dom

Identification ofthe cost-related risks,underlying drivers,and

impediments foreffective managementmustbe assessed in the

contextsof threekey stakeholders:clients,contractors,and

consultants.

This research is intended to investigate the perceived unde

standing and importance of the key attributes among these th

key stakeholders’ groups with respect to achieving the target

performance in projects.Estimation of projectcosts atthe early

stages of the design process and the ability to manage these c

throughout the construction phase is paramount to a project’s

all success. Past research illustrates that construction cost ove

and the subsequent poor cost performance are the attributes

lack of understanding among allparticipating teams across the

construction industry (Akintoye 2000;Frimpong etal. 2003).

However,an accurate understanding ofthe key attributes in the

context of the responsibility and management ability among c

and consultantcontractors has notbeen explored.By identifying

the factors affecting costoverruns,this research highlights the

criticality fortheireffective managementwithin the rolesand

responsibilitiesamong clients,consultants,and contractorsin

construction projects.

1Senior Lecturer, Faculty of Architecture, Building and Planning, Univ.

of Melbourne,Victoria 3010,Australia.E-mail:hdoloi@unimelb.edu.au

Note. This manuscript was submitted on November 13, 2009; approved

on June 6, 2012; published online on July 25, 2012. Discussion period open

until August 1, 2013; separate discussions must be submitted for individual

papers. This paper is part of the Journal of Construction Engineering and

Management, Vol. 139, No. 3, March 1, 2013. © ASCE, ISSN 0733-9364/

2013/3-267-279/$25.00.

JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013 /267

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Literature Review

Over the last few decades,there has been much research into the

factors thataffectcostperformance in the construction phase of

projects.Usually the vastmajority of costoverruns occur during

the construction phase, in which many unforeseen factors are con-

ceived over the conception/design stages (Chan and Kumaraswamy

1997).Attributes such as poor site management and supervision,

low speed of decision-making and client-initiated variations have

reportedly been some of the most significant causes of cost over-

runs in the construction phase of projects (Trostand Oberlender

2003;Iyer and Jha 2005).These factors primarily relate to the

project manager, given that project management involves managing

resources such as workers,machine,money, materials,and meth-

ods during this period (Frimpong etal. 2003).However,precise

understanding of these factors and protocols of responsibility shar-

ing for effective managementamong the key stakeholders is not

widespread. Although tools and techniques implemented to control

these factors is perceived to play an important role, understanding

the root cause of these factors and their potential impacts in man-

aging them from the perspectives of clients, consultants, and con-

tractors is the key for achieving success in costperformance.

Despite the factthatfactors associated with costmanagement

are reasonably understood,improvementof construction industry

practices in terms of responsibility sharing and deliberations among

the project’s participants is not particularly evident.In the United

Kingdom,Green (1989) conducted six case studies of tendering

practices for establishing the reasons for disregarding the best prac-

tices among the industry. Green (1989) concluded that whereas the

rationality for estimating is justified across the firms,a range of

uncertainties associated with the wider environmental issues prevail

over the tendering process. In an attempt to understand the rationale

of estimating indirect costs for construction work, Tah et al. (1994)

investigated the currentpractices towards quantification and allo-

cation of general overheads, risk contingencies, and profit margin

across seven firms. The research revealed that the approach for such

estimation is ad-hoc and based on past experience alone (Tah et al.

1994).Whereas more sophisticated and reflective approaches to-

wards subjective practices were suggested in published research,

the relationshipsbetween subjective practicesand overallcost

performance were notclearly highlighted (Enshassiet al. 2009;

Akintoye 2000).In the United Kingdom,Skitmore and Wilcock

(1994) surveyed nine smaller builders involved in all types of build-

ing projects to ascertain the pricing mechanism in preparing a bill

of quantities for competitive tender.The bulk of the items were

priced by experience,excepta smallpercentage ofspecialized

items,which were priced by the prescribed detailed methods.

However,the research asserted thatthe combination of both the

subjective and prescribed methods is the mostefficientmanner

in which achieving accurate tenderpricesfor estimatorsin a

time-constrained environmentcan be achieved.Incorporating the

statistically significant variability of the estimates in the program

evaluation and review technique (PERT) can enhance the reliability

of the subjective estimates.However,exclusion ofcostperfor-

mance in relation to such assertions rendered this research insuffi-

ciently comprehensive.

Chan and Kumaraswamy (1997) reported five principal causes

of time overruns perceived among clients, contractors, and consul-

tants in Hong Kong construction projects. A questionnaire survey

was designed comprising 83 delay factors across eight categories

and distributed to 400 localfirms involved in construction activ-

ities.Based on a 37% response,the five most significant sources

of delay were poor site management and supervision,unforeseen

ground conditions,low speed in decision-making,client-initiated

variations,and design change.Whereas a reasonable agreement

among three groups was reported on these time related factor

and theirlinks to overallprojectsuccess,the findings failed to

establish any meaningful insights into the roles and responsib

of the three groups and their underlying impacts on the overa

performance of the project.

Based on data collected from 84 contractors firms in the Un

Kingdom, Akintoye (2000) reported the primary factors releva

cost estimating practice as project complexity,scale and scope of

construction, market conditions, methods of construction, site

straints, client’s financial position, buildability, and location of

project.However,an investigation on how such factors would be

perceived by clients and consultants, and their potential impa

overall cost performance of projects,was not performed.This re-

search was therefore insufficiently comprehensive.Investigating

the causes of substantial cost variations relative to the initial c

tract and excessive cost overruns in Nigerian construction pro

Mansfield etal. (1994)revealed thatpoorprojectmanagement

during the construction phase produces notonly the deficiencies

in the projects’ plan and cost control, but also jeopardizes the

outcomes expected by clients,contractors,and consultants in the

overalldevelopmentprocess.Although the technicalability of

project managers is an important element to the project’s suc

the contribution of contractors and consultants in the process

cost monitoring and controlling is equally important in achievi

overallsuccess in projects (Iyer and Jha 2005).

In an attemptto establishing a predictive modelfor early cost

estimation, Trost and Oberlender (2003) collected quantitative

across 45 potential drivers on 67 completed construction proje

across the world. Based on factor analysis and regression mod

basic process design and site requirement was concluded to b

mostsignificantfactor thatimpacts estimate accuracy.Although

this finding is an important first step in that it reveals the sign

cance of early cost estimation, the exclusion of building and in

structure sector in the data collection process rendered the re

constrictive in the context of cost performance across constru

projects. Addressing the risk issues that affect cost performan

a project level, Baloi and Price (2003) examined the normative

behavioral perspectives based on an existing literature search

discussion with construction contractors.A lack of mechanized

support, such as a decision support system and contractors’ e

rience,were reported to be the key causes for failure in cost pe

formance in mostprojects.However,the rolesof clientsand

consultants were notincluded in the costperformance analysis,

and thus such findings are notbroadly useful.

Based on the case study data on completed projects in Gha

Frimpong etal. (2003)identified five key factorsthatimpact

projectcost performance.These factorsare monthly payment

difficulties from agencies,poor contractor management,material

procurement,poor technicalperformance,and escalationof

materials prices.Although a generalconsensus of the impacts of

these factors on cost performance was found among clients,con-

tractors,and clients,a significant contrast was highlighted on the

issues reported previously (Baloiand Price 2003;Skitmore and

Wilcock 1994).

Based on an investigation of the transport infrastructure acr

258 rail,bridge,tunnel,and road projects in Denmark,Flyvbjerg

et al. (2004) highlighted three key factors that affect cost over

Flyvbjerg etal. (2004)asserted thata longerprojectimple-

mentation phase, larger project size, and public ownership fac

are highly susceptible to costoverruns.However,relationships

between clients,contractors,and consultants in addressing these

factors and minimizing the impact of cost overruns were exclu

in the investigation. Cheung et al. (2008) investigated the atti

268 / JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

Over the last few decades,there has been much research into the

factors thataffectcostperformance in the construction phase of

projects.Usually the vastmajority of costoverruns occur during

the construction phase, in which many unforeseen factors are con-

ceived over the conception/design stages (Chan and Kumaraswamy

1997).Attributes such as poor site management and supervision,

low speed of decision-making and client-initiated variations have

reportedly been some of the most significant causes of cost over-

runs in the construction phase of projects (Trostand Oberlender

2003;Iyer and Jha 2005).These factors primarily relate to the

project manager, given that project management involves managing

resources such as workers,machine,money, materials,and meth-

ods during this period (Frimpong etal. 2003).However,precise

understanding of these factors and protocols of responsibility shar-

ing for effective managementamong the key stakeholders is not

widespread. Although tools and techniques implemented to control

these factors is perceived to play an important role, understanding

the root cause of these factors and their potential impacts in man-

aging them from the perspectives of clients, consultants, and con-

tractors is the key for achieving success in costperformance.

Despite the factthatfactors associated with costmanagement

are reasonably understood,improvementof construction industry

practices in terms of responsibility sharing and deliberations among

the project’s participants is not particularly evident.In the United

Kingdom,Green (1989) conducted six case studies of tendering

practices for establishing the reasons for disregarding the best prac-

tices among the industry. Green (1989) concluded that whereas the

rationality for estimating is justified across the firms,a range of

uncertainties associated with the wider environmental issues prevail

over the tendering process. In an attempt to understand the rationale

of estimating indirect costs for construction work, Tah et al. (1994)

investigated the currentpractices towards quantification and allo-

cation of general overheads, risk contingencies, and profit margin

across seven firms. The research revealed that the approach for such

estimation is ad-hoc and based on past experience alone (Tah et al.

1994).Whereas more sophisticated and reflective approaches to-

wards subjective practices were suggested in published research,

the relationshipsbetween subjective practicesand overallcost

performance were notclearly highlighted (Enshassiet al. 2009;

Akintoye 2000).In the United Kingdom,Skitmore and Wilcock

(1994) surveyed nine smaller builders involved in all types of build-

ing projects to ascertain the pricing mechanism in preparing a bill

of quantities for competitive tender.The bulk of the items were

priced by experience,excepta smallpercentage ofspecialized

items,which were priced by the prescribed detailed methods.

However,the research asserted thatthe combination of both the

subjective and prescribed methods is the mostefficientmanner

in which achieving accurate tenderpricesfor estimatorsin a

time-constrained environmentcan be achieved.Incorporating the

statistically significant variability of the estimates in the program

evaluation and review technique (PERT) can enhance the reliability

of the subjective estimates.However,exclusion ofcostperfor-

mance in relation to such assertions rendered this research insuffi-

ciently comprehensive.

Chan and Kumaraswamy (1997) reported five principal causes

of time overruns perceived among clients, contractors, and consul-

tants in Hong Kong construction projects. A questionnaire survey

was designed comprising 83 delay factors across eight categories

and distributed to 400 localfirms involved in construction activ-

ities.Based on a 37% response,the five most significant sources

of delay were poor site management and supervision,unforeseen

ground conditions,low speed in decision-making,client-initiated

variations,and design change.Whereas a reasonable agreement

among three groups was reported on these time related factor

and theirlinks to overallprojectsuccess,the findings failed to

establish any meaningful insights into the roles and responsib

of the three groups and their underlying impacts on the overa

performance of the project.

Based on data collected from 84 contractors firms in the Un

Kingdom, Akintoye (2000) reported the primary factors releva

cost estimating practice as project complexity,scale and scope of

construction, market conditions, methods of construction, site

straints, client’s financial position, buildability, and location of

project.However,an investigation on how such factors would be

perceived by clients and consultants, and their potential impa

overall cost performance of projects,was not performed.This re-

search was therefore insufficiently comprehensive.Investigating

the causes of substantial cost variations relative to the initial c

tract and excessive cost overruns in Nigerian construction pro

Mansfield etal. (1994)revealed thatpoorprojectmanagement

during the construction phase produces notonly the deficiencies

in the projects’ plan and cost control, but also jeopardizes the

outcomes expected by clients,contractors,and consultants in the

overalldevelopmentprocess.Although the technicalability of

project managers is an important element to the project’s suc

the contribution of contractors and consultants in the process

cost monitoring and controlling is equally important in achievi

overallsuccess in projects (Iyer and Jha 2005).

In an attemptto establishing a predictive modelfor early cost

estimation, Trost and Oberlender (2003) collected quantitative

across 45 potential drivers on 67 completed construction proje

across the world. Based on factor analysis and regression mod

basic process design and site requirement was concluded to b

mostsignificantfactor thatimpacts estimate accuracy.Although

this finding is an important first step in that it reveals the sign

cance of early cost estimation, the exclusion of building and in

structure sector in the data collection process rendered the re

constrictive in the context of cost performance across constru

projects. Addressing the risk issues that affect cost performan

a project level, Baloi and Price (2003) examined the normative

behavioral perspectives based on an existing literature search

discussion with construction contractors.A lack of mechanized

support, such as a decision support system and contractors’ e

rience,were reported to be the key causes for failure in cost pe

formance in mostprojects.However,the rolesof clientsand

consultants were notincluded in the costperformance analysis,

and thus such findings are notbroadly useful.

Based on the case study data on completed projects in Gha

Frimpong etal. (2003)identified five key factorsthatimpact

projectcost performance.These factorsare monthly payment

difficulties from agencies,poor contractor management,material

procurement,poor technicalperformance,and escalationof

materials prices.Although a generalconsensus of the impacts of

these factors on cost performance was found among clients,con-

tractors,and clients,a significant contrast was highlighted on the

issues reported previously (Baloiand Price 2003;Skitmore and

Wilcock 1994).

Based on an investigation of the transport infrastructure acr

258 rail,bridge,tunnel,and road projects in Denmark,Flyvbjerg

et al. (2004) highlighted three key factors that affect cost over

Flyvbjerg etal. (2004)asserted thata longerprojectimple-

mentation phase, larger project size, and public ownership fac

are highly susceptible to costoverruns.However,relationships

between clients,contractors,and consultants in addressing these

factors and minimizing the impact of cost overruns were exclu

in the investigation. Cheung et al. (2008) investigated the atti

268 / JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

clients and estimators towards estimating errors in the estimating

practice in the Hong Kong construction industry. Based on a ques-

tionnaire survey conducted among 45 estimators,33 clients,and

regression modeling,tolerances in overestimations among both

partieswere highlighted.Although both estimatorsand clients

are reasonablysatisfiedwith overestimations,the underlying

causes ofsuch practices and strategies formitigation were not

revealed.

As evident from the previously discussed research, the field of

costmanagementand underlying attributes in costestimation is

reasonably well developed (Bowen and Edwards 1998). However,

it is unclear how each of the attributes relate to the clients,con-

sultants,and contractors,and how the attributes effectsuccessful

costperformance.Currently,no research has been found in the

public domain thatfocuseson the entire projectdevelopment

phase,using the perceptions of clients,consultants,and contrac-

tors,and how itimpacts costperformance (Fortune 2006).There

is a need to re-think and re-engineer the existing or normalcost

estimating process, incorporating emergent diversity and complex-

ity,especially in the projectdelivery approach.The findings of

this research should benefit the construction community by high-

lighting thekey factorsthatimpactcostsand theassociated

responsibilities for effective managementamong the key project

participants.Additionally,the results willprovide guidance for

further research in developing practicalsteps thatcan be imple-

mented to reduce costoverrunsduring the entire development

process.

Methodology and Approach

Cost performance of projects and the management of cost overruns

is an ongoing topic of investigation in many countries.There has

been much research into the generic causes of costperformance

issuesover the designand constructionaspectsof projects

(Skitmore and Wilcock 1994;Cheung etal. 2008).However,no

or little research has been reported in the context of understanding

the rootcauses,tackling mechanisms,and stakeholders’ respon-

sibilities in addressing this chronic issue of costoverrun in most

projects.Furthermore,the area-specific study ofthe factors that

affectcostperformance in projects renders pastfindings insuffi-

ciently comprehensive in relation with Australian industry practice

(Love etal. 2005).Focusing on Australian construction projects,

this research istherefore intended to examine the rootcauses

behind the poorcostperformance from the perspectives ofthe

three key participants and management responsibilities commensu-

rate to the contractual roles of these participants across the entire

developmentprocess.

The research is intended to expand currentunderstanding of

cost performance issues and management methods through a ques-

tionnaire survey.The questionnaire was designed to capture the

currentconstruction industry experiences among clients,consul-

tants,and contractors.Over 160 construction clients,consultants,

and contractors were selected on the basis of their diverse back-

grounds,professionalexperiences,and currentparticipation in

the industry.

The objective ofthis research is to identify the mostcritical

factors that impact cost performance across the design consultants,

contactors,and clientperspectives by the following:

• Ranking the most critical attributes based on the relative impor-

tance weight(RIW),

• Reduce the influencing attributes into factor groups, identifying

the latent properties of each factor and their effective manage-

mentbased on factor analysis,

• Investigate the influencing factors on cost performance bas

multivariate regression analysis,and

• Analyze the management of the influencing factors in relati

with the roles and responsibilities of the consultants, contac

and clientin the project.

The first objective is important for clients, consultants, and

tractors to understand and attend to the underlying attributes

impactcostsuccess.By establishing the relative positioning of

the attributes in the order of their significance, the second obj

attempts to create a better understanding of the clustered eff

(e.g., factors) of these attributes on project cost performance.

factors are then analyzed in the context of effective managem

among the clients, consultants, and contractors in the optimal

delivery process.The second objective is particularly important

for allthree parties to prioritize,specifically,the factors in terms

of theircriticality fordeveloping contractualarrangements and

assume responsibilities, to obtain the desired outcomes.The third

objective is intended to validate the factors in terms of their re

and underlying influence on cost performance in projects. Fina

through the fourth objective, the resulting factors are analyzed

reference to the roles and responsibilities of all three key stak

ers with respect to cost management processes and their effe

development and implementation in the construction projectsBy

increasing the discipline-specific knowledge in meeting the req

ments and expectations of clients,consultants,and contractors,it

may be possible to accurately highlight the advantages and di

vantages of the cost management approach and clarify the pe

viewpoints within the construction industry.

The research uses a carefully designed questionnaire to col

the perceived opinions of the most possible causes of cost ove

among the three key stakeholder groups. To capture the most

evantattributes in the questionnaire thatimpactthe costperfor-

mance in projects,an extensive literature search was conducted.

A listing of the attributes that are directly or indirectly associa

with projectcostperformance was developed under seven broad

headings,as shown in Table 1.To validate the selected attributes

in an Australian context, a number of feedback sessions were

conducted among five senior industry professionals who repre

all three categories in the Australian construction industry.

The final questionnaire, consisting of 73 key attributes, was

distributed to over 160 selected professionals, targeting a goo

of construction contractors,consultants,and clients primarily in-

volved in medium- to large-scale construction projects. Of the

sible 73 attributes, 48 attributes had a sizeable correlation wit

another and were considered appropriate for further investiga

(Doloi 2008; Field 2005; Chan and Kumaraswamy 1997). The r

spondents were asked to provide their objective opinions on th

impacts of all the attributes on cost performance in one of the

or current projects on a five-point Likert scale (5 = strongly ag

4 = agree, 3 = neutral, 2 = disagree, and 1 = strongly disagre

measure the perceived agreement of the respondents’ groups

criticality of the attributes that impact project cost performanc

hypotheses were developed,as follows:

• Null hypothesis (H0): none of the groups are in agreement with

the ranking of any attribute,and

• Alternative hypothesis (H1): all three groups are in agreement

with the ranking of any attribute.

The previous hypotheses have been discussed in the contex

results and findings in the following sections. Given that there

tinues to be considerable cost overrun issues among a majorit

construction projects,the contributions made in this research are

highly relevantfor understanding the client’s,consultant’s,and

contractor’s roles in relation to achieving target cost performa

and overallprojectsuccess.

JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013 /269

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

practice in the Hong Kong construction industry. Based on a ques-

tionnaire survey conducted among 45 estimators,33 clients,and

regression modeling,tolerances in overestimations among both

partieswere highlighted.Although both estimatorsand clients

are reasonablysatisfiedwith overestimations,the underlying

causes ofsuch practices and strategies formitigation were not

revealed.

As evident from the previously discussed research, the field of

costmanagementand underlying attributes in costestimation is

reasonably well developed (Bowen and Edwards 1998). However,

it is unclear how each of the attributes relate to the clients,con-

sultants,and contractors,and how the attributes effectsuccessful

costperformance.Currently,no research has been found in the

public domain thatfocuseson the entire projectdevelopment

phase,using the perceptions of clients,consultants,and contrac-

tors,and how itimpacts costperformance (Fortune 2006).There

is a need to re-think and re-engineer the existing or normalcost

estimating process, incorporating emergent diversity and complex-

ity,especially in the projectdelivery approach.The findings of

this research should benefit the construction community by high-

lighting thekey factorsthatimpactcostsand theassociated

responsibilities for effective managementamong the key project

participants.Additionally,the results willprovide guidance for

further research in developing practicalsteps thatcan be imple-

mented to reduce costoverrunsduring the entire development

process.

Methodology and Approach

Cost performance of projects and the management of cost overruns

is an ongoing topic of investigation in many countries.There has

been much research into the generic causes of costperformance

issuesover the designand constructionaspectsof projects

(Skitmore and Wilcock 1994;Cheung etal. 2008).However,no

or little research has been reported in the context of understanding

the rootcauses,tackling mechanisms,and stakeholders’ respon-

sibilities in addressing this chronic issue of costoverrun in most

projects.Furthermore,the area-specific study ofthe factors that

affectcostperformance in projects renders pastfindings insuffi-

ciently comprehensive in relation with Australian industry practice

(Love etal. 2005).Focusing on Australian construction projects,

this research istherefore intended to examine the rootcauses

behind the poorcostperformance from the perspectives ofthe

three key participants and management responsibilities commensu-

rate to the contractual roles of these participants across the entire

developmentprocess.

The research is intended to expand currentunderstanding of

cost performance issues and management methods through a ques-

tionnaire survey.The questionnaire was designed to capture the

currentconstruction industry experiences among clients,consul-

tants,and contractors.Over 160 construction clients,consultants,

and contractors were selected on the basis of their diverse back-

grounds,professionalexperiences,and currentparticipation in

the industry.

The objective ofthis research is to identify the mostcritical

factors that impact cost performance across the design consultants,

contactors,and clientperspectives by the following:

• Ranking the most critical attributes based on the relative impor-

tance weight(RIW),

• Reduce the influencing attributes into factor groups, identifying

the latent properties of each factor and their effective manage-

mentbased on factor analysis,

• Investigate the influencing factors on cost performance bas

multivariate regression analysis,and

• Analyze the management of the influencing factors in relati

with the roles and responsibilities of the consultants, contac

and clientin the project.

The first objective is important for clients, consultants, and

tractors to understand and attend to the underlying attributes

impactcostsuccess.By establishing the relative positioning of

the attributes in the order of their significance, the second obj

attempts to create a better understanding of the clustered eff

(e.g., factors) of these attributes on project cost performance.

factors are then analyzed in the context of effective managem

among the clients, consultants, and contractors in the optimal

delivery process.The second objective is particularly important

for allthree parties to prioritize,specifically,the factors in terms

of theircriticality fordeveloping contractualarrangements and

assume responsibilities, to obtain the desired outcomes.The third

objective is intended to validate the factors in terms of their re

and underlying influence on cost performance in projects. Fina

through the fourth objective, the resulting factors are analyzed

reference to the roles and responsibilities of all three key stak

ers with respect to cost management processes and their effe

development and implementation in the construction projectsBy

increasing the discipline-specific knowledge in meeting the req

ments and expectations of clients,consultants,and contractors,it

may be possible to accurately highlight the advantages and di

vantages of the cost management approach and clarify the pe

viewpoints within the construction industry.

The research uses a carefully designed questionnaire to col

the perceived opinions of the most possible causes of cost ove

among the three key stakeholder groups. To capture the most

evantattributes in the questionnaire thatimpactthe costperfor-

mance in projects,an extensive literature search was conducted.

A listing of the attributes that are directly or indirectly associa

with projectcostperformance was developed under seven broad

headings,as shown in Table 1.To validate the selected attributes

in an Australian context, a number of feedback sessions were

conducted among five senior industry professionals who repre

all three categories in the Australian construction industry.

The final questionnaire, consisting of 73 key attributes, was

distributed to over 160 selected professionals, targeting a goo

of construction contractors,consultants,and clients primarily in-

volved in medium- to large-scale construction projects. Of the

sible 73 attributes, 48 attributes had a sizeable correlation wit

another and were considered appropriate for further investiga

(Doloi 2008; Field 2005; Chan and Kumaraswamy 1997). The r

spondents were asked to provide their objective opinions on th

impacts of all the attributes on cost performance in one of the

or current projects on a five-point Likert scale (5 = strongly ag

4 = agree, 3 = neutral, 2 = disagree, and 1 = strongly disagre

measure the perceived agreement of the respondents’ groups

criticality of the attributes that impact project cost performanc

hypotheses were developed,as follows:

• Null hypothesis (H0): none of the groups are in agreement with

the ranking of any attribute,and

• Alternative hypothesis (H1): all three groups are in agreement

with the ranking of any attribute.

The previous hypotheses have been discussed in the contex

results and findings in the following sections. Given that there

tinues to be considerable cost overrun issues among a majorit

construction projects,the contributions made in this research are

highly relevantfor understanding the client’s,consultant’s,and

contractor’s roles in relation to achieving target cost performa

and overallprojectsuccess.

JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013 /269

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Data Collection Process

A total of 160 questionnairesurveysweredistributed to the

selected clients, contractors, and consultants within the Australian

Construction Industry, comprising residential, commercial, and in-

dustrialbuildings.Selection of those firms and individuals from

the contractor, client, or consultant background was critical to the

success ofthis research.Given thatthe targetoutcome ofthis

research entirely relies on the representative population sample,

a simple random sampling was adopted to provide a broad spec-

trum of the three key groups in both governmentand private or-

ganizations within the industry (Akintoye 2003). The selection of

the firms/individuals had therefore been selected from industry

body websites.The contractorswereprimarily sourced from

the Master Builders of Australia (MBA) website.The consultants

were sourced from specific industry websites, which include quan-

tity surveyors from the Australian Institute of Quantity Surveyors

(AIQS) and architects from the Australian Institute of Architects

(AIA). The clients firms were identified primarily from property

development companies available from both contractors’ web

and the Australian Property Institute (API).

A totalof 94 responses were received,which consisted of 24

clients,29 consultants,and 41 contractors.The response rate of

approximately 25% of clients, 31% of consultants, and 44% of

tractors from the overallrespondents was deemed acceptable for

this study (Flyvbjerg et al.2004; Doloi 2008).Table 2 shows the

profile of the respondents in terms of their experience and the

of the projects.

As seen in Table 2,among 94 respondents across the clients,

contractors,and consultants,46% had a minimum of10 years

experiencein the construction industry.As seen in thelast

column,59% respondents were involved in projectin the range

of $75–$150 million, with 11% over $150 million. These statist

provide the basis thatthe research feedback has been based on

medium- to large-scale construction projects.

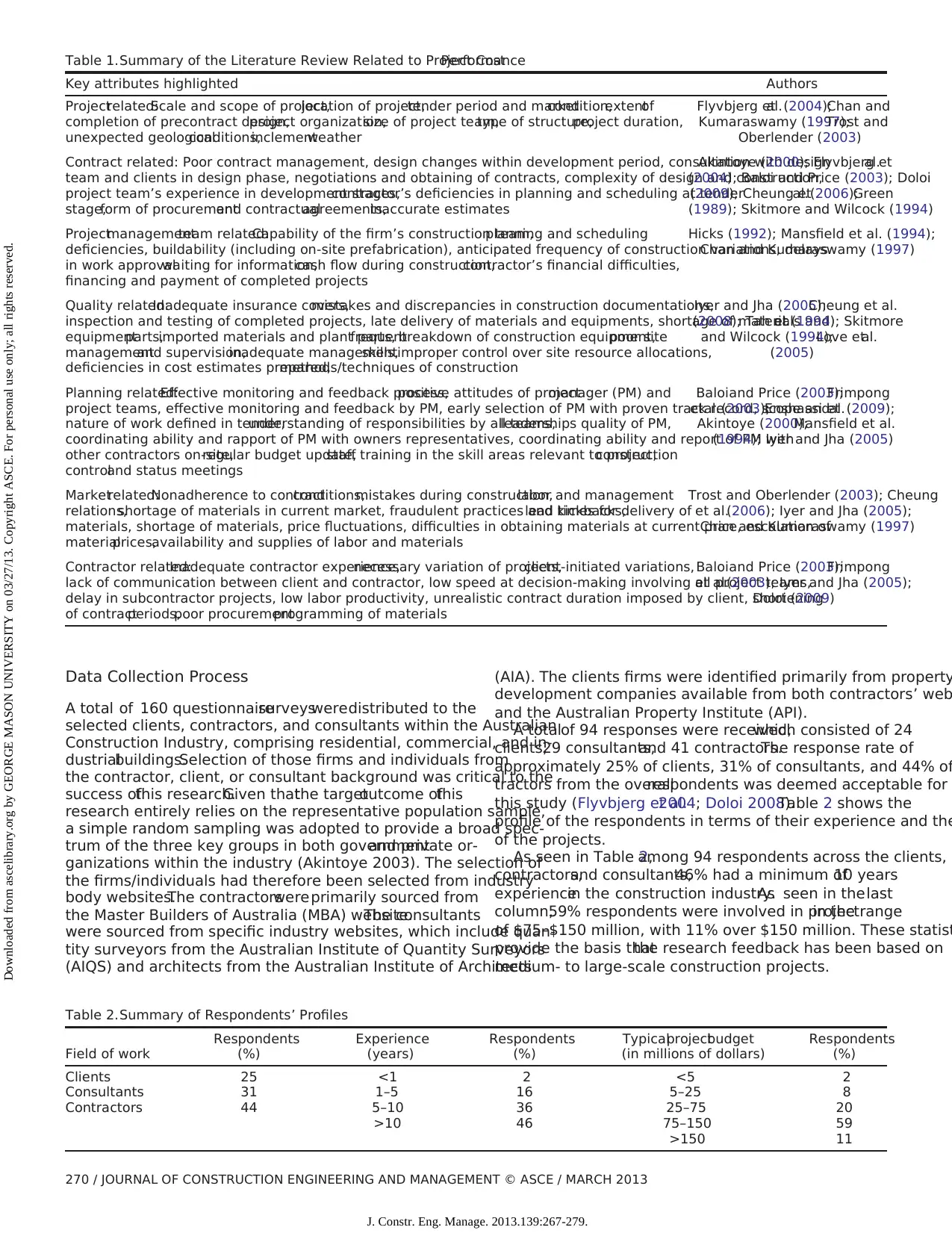

Table 1.Summary of the Literature Review Related to Project CostPerformance

Key attributes highlighted Authors

Projectrelated:Scale and scope of project,location of project,tender period and marketcondition,extentof

completion of precontract design,project organization,size of project team,type of structure,project duration,

unexpected geologicalconditions,inclementweather

Flyvbjerg etal.(2004);Chan and

Kumaraswamy (1997);Trost and

Oberlender (2003)

Contract related: Poor contract management, design changes within development period, consultation with design

team and clients in design phase, negotiations and obtaining of contracts, complexity of design and construction,

project team’s experience in development stages,contractor’s deficiencies in planning and scheduling at tender

stage,form of procurementand contractualagreements,inaccurate estimates

Akintoye (2000); Flyvbjerg etal.

(2004); Baloi and Price (2003); Doloi

(2009); Cheung etal.(2006);Green

(1989); Skitmore and Wilcock (1994)

Projectmanagementteam related:Capability of the firm’s construction team,planning and scheduling

deficiencies, buildability (including on-site prefabrication), anticipated frequency of construction variations, delays

in work approvalwaiting for information,cash flow during construction,contractor’s financial difficulties,

financing and payment of completed projects

Hicks (1992); Mansfield et al. (1994);

Chan and Kumaraswamy (1997)

Quality related:Inadequate insurance covers,mistakes and discrepancies in construction documentations,

inspection and testing of completed projects, late delivery of materials and equipments, shortage of materials and

equipmentparts,imported materials and plant parts,frequentbreakdown of construction equipment,poor site

managementand supervision,inadequate managementskills,improper control over site resource allocations,

deficiencies in cost estimates prepared,methods/techniques of construction

Iyer and Jha (2005);Cheung et al.

(2008); Tah etal.(1994); Skitmore

and Wilcock (1994);Love etal.

(2005)

Planning related:Effective monitoring and feedback process,positive attitudes of projectmanager (PM) and

project teams, effective monitoring and feedback by PM, early selection of PM with proven track record, scope and

nature of work defined in tender,understanding of responsibilities by all teams,leaderships quality of PM,

coordinating ability and rapport of PM with owners representatives, coordinating ability and report of PM with

other contractors on-site,regular budget update,staff training in the skill areas relevant to project,construction

controland status meetings

Baloiand Price (2003);Frimpong

etal.(2003);Enshassi etal.(2009);

Akintoye (2000);Mansfield et al.

(1994); Iyer and Jha (2005)

Marketrelated:Nonadherence to contractconditions,mistakes during construction,labor and management

relations,shortage of materials in current market, fraudulent practices and kickbacks,lead times for delivery of

materials, shortage of materials, price fluctuations, difficulties in obtaining materials at current price, escalation of

materialprices,availability and supplies of labor and materials

Trost and Oberlender (2003); Cheung

et al.(2006); Iyer and Jha (2005);

Chan and Kumaraswamy (1997)

Contractor related:Inadequate contractor experience,necessary variation of projects,client-initiated variations,

lack of communication between client and contractor, low speed at decision-making involving all project teams,

delay in subcontractor projects, low labor productivity, unrealistic contract duration imposed by client, shortening

of contractperiods,poor procurementprogramming of materials

Baloiand Price (2003);Frimpong

et al.(2003); Iyer and Jha (2005);

Doloi (2009)

Table 2.Summary of Respondents’ Profiles

Field of work

Respondents

(%)

Experience

(years)

Respondents

(%)

Typicalprojectbudget

(in millions of dollars)

Respondents

(%)

Clients 25 <1 2 <5 2

Consultants 31 1–5 16 5–25 8

Contractors 44 5–10 36 25–75 20

>10 46 75–150 59

>150 11

270 / JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

A total of 160 questionnairesurveysweredistributed to the

selected clients, contractors, and consultants within the Australian

Construction Industry, comprising residential, commercial, and in-

dustrialbuildings.Selection of those firms and individuals from

the contractor, client, or consultant background was critical to the

success ofthis research.Given thatthe targetoutcome ofthis

research entirely relies on the representative population sample,

a simple random sampling was adopted to provide a broad spec-

trum of the three key groups in both governmentand private or-

ganizations within the industry (Akintoye 2003). The selection of

the firms/individuals had therefore been selected from industry

body websites.The contractorswereprimarily sourced from

the Master Builders of Australia (MBA) website.The consultants

were sourced from specific industry websites, which include quan-

tity surveyors from the Australian Institute of Quantity Surveyors

(AIQS) and architects from the Australian Institute of Architects

(AIA). The clients firms were identified primarily from property

development companies available from both contractors’ web

and the Australian Property Institute (API).

A totalof 94 responses were received,which consisted of 24

clients,29 consultants,and 41 contractors.The response rate of

approximately 25% of clients, 31% of consultants, and 44% of

tractors from the overallrespondents was deemed acceptable for

this study (Flyvbjerg et al.2004; Doloi 2008).Table 2 shows the

profile of the respondents in terms of their experience and the

of the projects.

As seen in Table 2,among 94 respondents across the clients,

contractors,and consultants,46% had a minimum of10 years

experiencein the construction industry.As seen in thelast

column,59% respondents were involved in projectin the range

of $75–$150 million, with 11% over $150 million. These statist

provide the basis thatthe research feedback has been based on

medium- to large-scale construction projects.

Table 1.Summary of the Literature Review Related to Project CostPerformance

Key attributes highlighted Authors

Projectrelated:Scale and scope of project,location of project,tender period and marketcondition,extentof

completion of precontract design,project organization,size of project team,type of structure,project duration,

unexpected geologicalconditions,inclementweather

Flyvbjerg etal.(2004);Chan and

Kumaraswamy (1997);Trost and

Oberlender (2003)

Contract related: Poor contract management, design changes within development period, consultation with design

team and clients in design phase, negotiations and obtaining of contracts, complexity of design and construction,

project team’s experience in development stages,contractor’s deficiencies in planning and scheduling at tender

stage,form of procurementand contractualagreements,inaccurate estimates

Akintoye (2000); Flyvbjerg etal.

(2004); Baloi and Price (2003); Doloi

(2009); Cheung etal.(2006);Green

(1989); Skitmore and Wilcock (1994)

Projectmanagementteam related:Capability of the firm’s construction team,planning and scheduling

deficiencies, buildability (including on-site prefabrication), anticipated frequency of construction variations, delays

in work approvalwaiting for information,cash flow during construction,contractor’s financial difficulties,

financing and payment of completed projects

Hicks (1992); Mansfield et al. (1994);

Chan and Kumaraswamy (1997)

Quality related:Inadequate insurance covers,mistakes and discrepancies in construction documentations,

inspection and testing of completed projects, late delivery of materials and equipments, shortage of materials and

equipmentparts,imported materials and plant parts,frequentbreakdown of construction equipment,poor site

managementand supervision,inadequate managementskills,improper control over site resource allocations,

deficiencies in cost estimates prepared,methods/techniques of construction

Iyer and Jha (2005);Cheung et al.

(2008); Tah etal.(1994); Skitmore

and Wilcock (1994);Love etal.

(2005)

Planning related:Effective monitoring and feedback process,positive attitudes of projectmanager (PM) and

project teams, effective monitoring and feedback by PM, early selection of PM with proven track record, scope and

nature of work defined in tender,understanding of responsibilities by all teams,leaderships quality of PM,

coordinating ability and rapport of PM with owners representatives, coordinating ability and report of PM with

other contractors on-site,regular budget update,staff training in the skill areas relevant to project,construction

controland status meetings

Baloiand Price (2003);Frimpong

etal.(2003);Enshassi etal.(2009);

Akintoye (2000);Mansfield et al.

(1994); Iyer and Jha (2005)

Marketrelated:Nonadherence to contractconditions,mistakes during construction,labor and management

relations,shortage of materials in current market, fraudulent practices and kickbacks,lead times for delivery of

materials, shortage of materials, price fluctuations, difficulties in obtaining materials at current price, escalation of

materialprices,availability and supplies of labor and materials

Trost and Oberlender (2003); Cheung

et al.(2006); Iyer and Jha (2005);

Chan and Kumaraswamy (1997)

Contractor related:Inadequate contractor experience,necessary variation of projects,client-initiated variations,

lack of communication between client and contractor, low speed at decision-making involving all project teams,

delay in subcontractor projects, low labor productivity, unrealistic contract duration imposed by client, shortening

of contractperiods,poor procurementprogramming of materials

Baloiand Price (2003);Frimpong

et al.(2003); Iyer and Jha (2005);

Doloi (2009)

Table 2.Summary of Respondents’ Profiles

Field of work

Respondents

(%)

Experience

(years)

Respondents

(%)

Typicalprojectbudget

(in millions of dollars)

Respondents

(%)

Clients 25 <1 2 <5 2

Consultants 31 1–5 16 5–25 8

Contractors 44 5–10 36 25–75 20

>10 46 75–150 59

>150 11

270 / JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

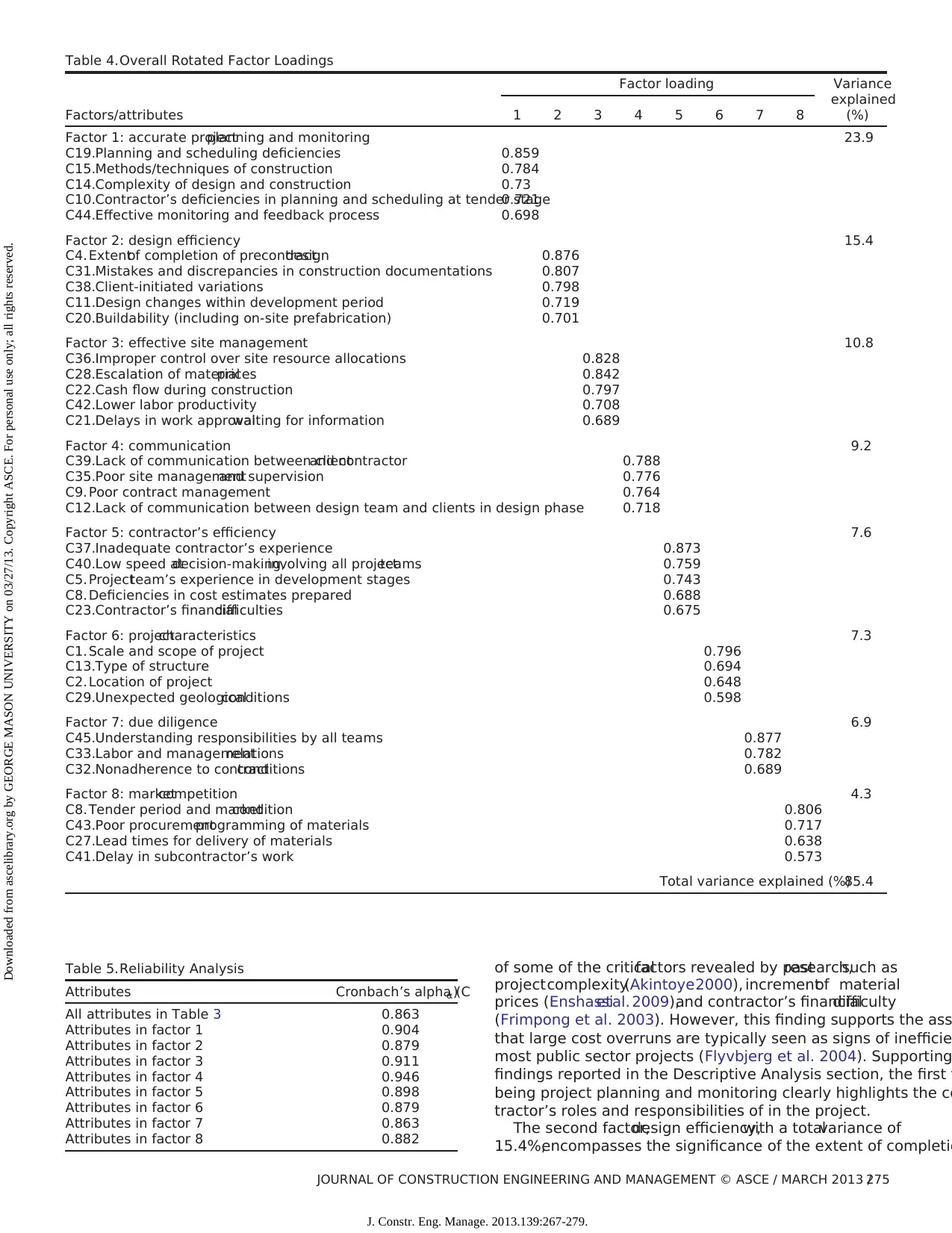

Data Analysis and Results

The author’s research primarily utilized two separate methods to

analyze the respondents’data to identify the criticalattributes

among allthree categories thataffectcostperformance.The first

is a descriptive approach with directinterpretation of the survey

results to identify the mostcriticalattribute based on the RIW

(Frimpong etal. 2003).The RIW score is a usefulmeasure of

the relative positioning of a particular attribute perceived by the

respondents on the raw dataset(Chan and Kumaraswamy 1997).

The RIW for each attribute is calculated by summing the weights

assigned to it by each respondent. Although the RIW score does not

represent the statistically significant measurement of any instance,

the score provides a good indication on the relative meritof an

attribute based on the frequency of occurrence within the independ-

ently collected sample.

The second method, the factor analysis technique, was used to

reduce the attributes in the raw dataset into the meaningful groups

known as factors. By reducing a dataset from a group of interrelated

variables into a smaller set of factors, the factor analysis allows one

to explain the maximum amountof common variance with the

smallestnumber of explanatory concepts (Field 2005).Thus,the

factors are useful explanatory concepts for analyzing the clustered

effectson costperformance and understanding the appropriate

managementfor ensuring targetoutcomes in the projects (Iyer

and Jha 2005;Trostand Oberlender2003).In addition,linear

regression analysis based on the factor scores was performed to

investigate the collective strengths ofthe factors thatinfluence

costperformance in a project.The StatisticalPackage for Social

Sciences (SPSS) software package was used for both factor analy-

sis and regression analysis.

Descriptive Analysis

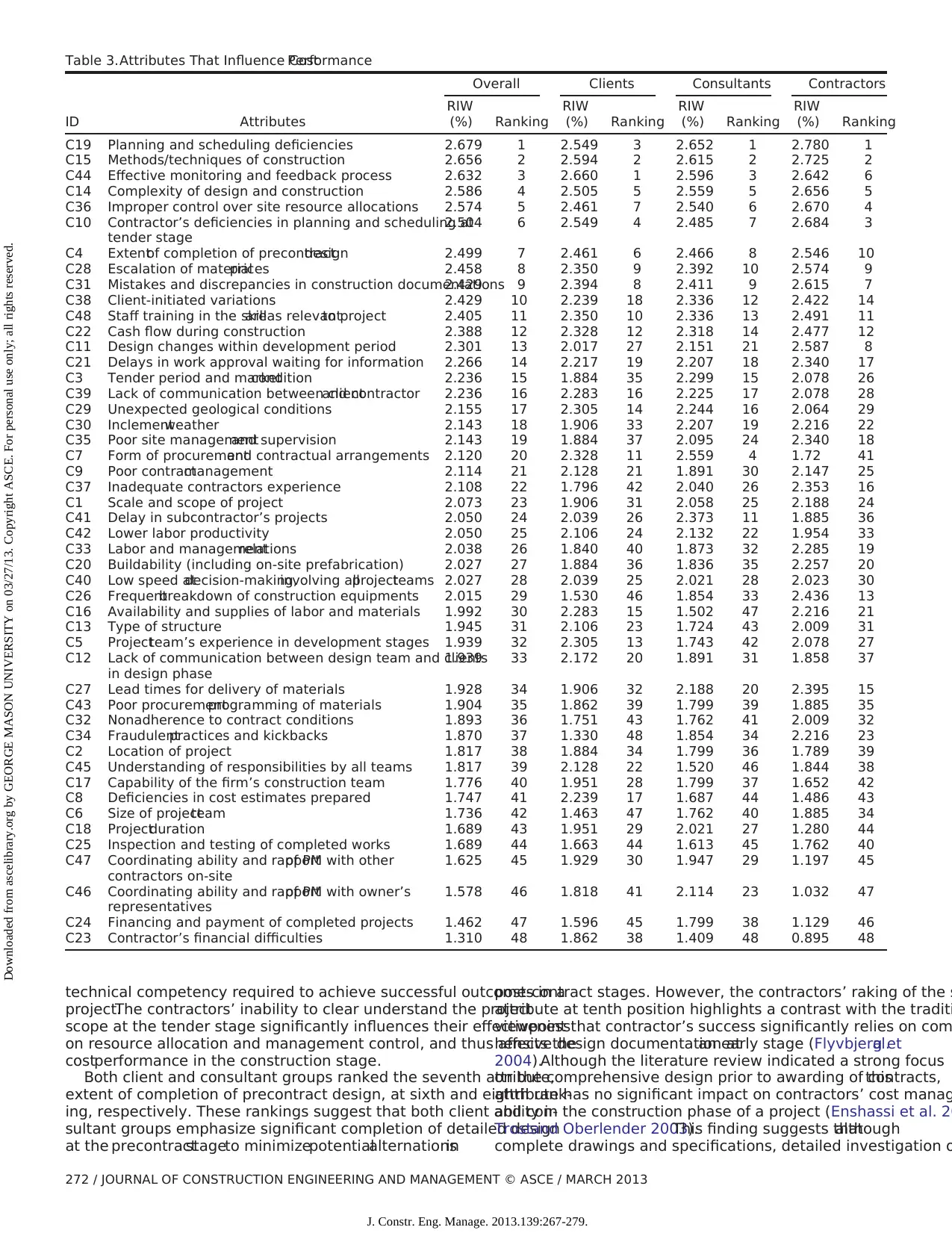

Various methods can be used to rank and subsequently identify the

relative critical attributes out of a raw data analysis. According to

numerous researchers,the mean and standard deviations are not

reliable statistics forassessing overallranking ofthe attributes.

However, RIW is one of the most widely used measures to deter-

mine the relative significance ofthe attributes (Frimpong etal.

2003).The RIW was evaluated using the following expression:

RIW ¼

P 5

i¼1ai ni

P N

j¼1xj

× 100 ð1Þ

in which xj = sum of the jth factor; j = factors 1, 2, 3, 4, : : : , N;

N = total number of attributes (48); ai is a constant that expresses

the weight given to the ith response: i ¼ 1 (very high), 2 (high), 3

(medium), 4 (low) and 5 (very low); and ni is the variable express-

ing the frequency of the ith response.

Based on Eq. (1), the RIW for all the attributes were determined

first for client, consultant, and contractor categories separately, and

then for overall samples.Table 3 shows the calculated RIWs and

rankings for 48 attributes in all four categories. The following sec-

tions discuss the significance of some of the key attributes across all

three categories with respect to the overall relative rankings shown

in the firstcolumn.

As seen in Table 3,the overallranking revealed that planning

and scheduling deficiencies is one of the most significant attributes

(RIW ¼ 2.679)that influencecost performancein projects.

Whereas both consultants and contractors share the same view-

point,clients ranked this attribute in third position.In contrast,

an effective monitoring and feedback process was perceived to

be the mostimportantfactor from the client’s perspective,which

was ranked in the third position in the overallcategory.The

third-rankedattribute,effectivemonitoringand feedbackin

overalland consultants’categories,postulatethe adequacy of

projectmanagementpractices forachieving costsuccess.Given

that the contractor’s motive is primarily driven by the earliest

pletion and site-levelmanagementof construction activities,the

monitoring and feedback process is neglected,and hence the jus-

tification for its listing at sixth position in the contractors’ cate

This is certainly the result of contractors being unaware about

roles and responsibilities in monitoring, controlling, and feedba

processes in the construction phase of the project.

Although pastresearch has reported many underlying factors

thatimpactcostperformance in projects,the revelation ofthe

impactsof planning and controlling isan importantshiftthat

has resulted from the author’s study.Whereas project planning is

a preconstruction activity in the planning phase,the bulk of the

controlling occurs in the construction phase of projects.Being a

key stakeholderin the construction phase,contractors mustbe

capable of devising an accurate time schedule such that the re

ant baseline assists in progress monitoring, reporting, and con

ling towards meeting the targets in the project. Accurate plann

requires accurate change controlprocesses to be adopted by the

contractor within the project. Thus, as far as responsibility is c

cerned, accurate planning and controlling clearly lies with the

tractors involved in the project.This finding demonstrates thata

lack of required technicalsupportand competency among the

key stakeholder(the contractors)potentially leads to failure in

delivering modern projects.

Construction methods or technique (RIW ¼ 2.656) was the s

ond most significant attribute across all three categories. Give

the complexity of modern construction projects increases acro

sectors,the requirement for the selection of appropriate constru

tion methods becomes critical for contractors. Both clients and

sultants have realized the benefits of using contemporary met

and techniques,in addition to appropriate exploitation of modern

equipmentin construction projects.

The fourth significant attribute, complexity of design and co

struction (RIW ¼ 2.586),clearly postulates the increasing com-

plexity ofdesign projectsand construction in modern projects

thatimpactcostperformance in overallprojects.The consistent

ranking ofthis attribute by clients,consultants,and contractors

attheir fifth positions asserts the underlying challenges faced

all three groups in successfuldelivery ofprojects.Whereas the

client’smotive ofvalue formoney exertssignificanttruston

consultant’s performance in most modern projects, the contra

performance is usually measured on the effectiveness ofon-site

construction with acceptable quality specification. However, a

of contractor’s in-depth understanding of the projectdesign and

specificationsoften leadsto inefficientconstruction and poor

on-site productivity in the project. This potentially triggers con

and disputes among all three parties, leading to additional cos

the project.Such conflicting requirements certainly contribute to

poorcontrolling ofcostaccounts and results in significantcost

overruns.

The fifth attribute,impropercontrolover site resources

(RIW value ¼ 2.574),clearly indicates the contractor’s inability

in handling construction resources and hence mismanagemenof

the scarce on-site resources in a project.In fact,the contractor

group has acknowledged itas a highly significantattribute by

assigning it as fourth ranking.The agreementof the level of sig-

nificance by both consultants and clients has been found at six

and seventh levels,respectively.The sixth attribute,contractors

deficiencies in realistic planning and scheduling at the tender

which has been ranked at the third position by the contractors

lights a significantconcern on contractors’prequalification and

JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013 /271

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

The author’s research primarily utilized two separate methods to

analyze the respondents’data to identify the criticalattributes

among allthree categories thataffectcostperformance.The first

is a descriptive approach with directinterpretation of the survey

results to identify the mostcriticalattribute based on the RIW

(Frimpong etal. 2003).The RIW score is a usefulmeasure of

the relative positioning of a particular attribute perceived by the

respondents on the raw dataset(Chan and Kumaraswamy 1997).

The RIW for each attribute is calculated by summing the weights

assigned to it by each respondent. Although the RIW score does not

represent the statistically significant measurement of any instance,

the score provides a good indication on the relative meritof an

attribute based on the frequency of occurrence within the independ-

ently collected sample.

The second method, the factor analysis technique, was used to

reduce the attributes in the raw dataset into the meaningful groups

known as factors. By reducing a dataset from a group of interrelated

variables into a smaller set of factors, the factor analysis allows one

to explain the maximum amountof common variance with the

smallestnumber of explanatory concepts (Field 2005).Thus,the

factors are useful explanatory concepts for analyzing the clustered

effectson costperformance and understanding the appropriate

managementfor ensuring targetoutcomes in the projects (Iyer

and Jha 2005;Trostand Oberlender2003).In addition,linear

regression analysis based on the factor scores was performed to

investigate the collective strengths ofthe factors thatinfluence

costperformance in a project.The StatisticalPackage for Social

Sciences (SPSS) software package was used for both factor analy-

sis and regression analysis.

Descriptive Analysis

Various methods can be used to rank and subsequently identify the

relative critical attributes out of a raw data analysis. According to

numerous researchers,the mean and standard deviations are not

reliable statistics forassessing overallranking ofthe attributes.

However, RIW is one of the most widely used measures to deter-

mine the relative significance ofthe attributes (Frimpong etal.

2003).The RIW was evaluated using the following expression:

RIW ¼

P 5

i¼1ai ni

P N

j¼1xj

× 100 ð1Þ

in which xj = sum of the jth factor; j = factors 1, 2, 3, 4, : : : , N;

N = total number of attributes (48); ai is a constant that expresses

the weight given to the ith response: i ¼ 1 (very high), 2 (high), 3

(medium), 4 (low) and 5 (very low); and ni is the variable express-

ing the frequency of the ith response.

Based on Eq. (1), the RIW for all the attributes were determined

first for client, consultant, and contractor categories separately, and

then for overall samples.Table 3 shows the calculated RIWs and

rankings for 48 attributes in all four categories. The following sec-

tions discuss the significance of some of the key attributes across all

three categories with respect to the overall relative rankings shown

in the firstcolumn.

As seen in Table 3,the overallranking revealed that planning

and scheduling deficiencies is one of the most significant attributes

(RIW ¼ 2.679)that influencecost performancein projects.

Whereas both consultants and contractors share the same view-

point,clients ranked this attribute in third position.In contrast,

an effective monitoring and feedback process was perceived to

be the mostimportantfactor from the client’s perspective,which

was ranked in the third position in the overallcategory.The

third-rankedattribute,effectivemonitoringand feedbackin

overalland consultants’categories,postulatethe adequacy of

projectmanagementpractices forachieving costsuccess.Given

that the contractor’s motive is primarily driven by the earliest

pletion and site-levelmanagementof construction activities,the

monitoring and feedback process is neglected,and hence the jus-

tification for its listing at sixth position in the contractors’ cate

This is certainly the result of contractors being unaware about

roles and responsibilities in monitoring, controlling, and feedba

processes in the construction phase of the project.

Although pastresearch has reported many underlying factors

thatimpactcostperformance in projects,the revelation ofthe

impactsof planning and controlling isan importantshiftthat

has resulted from the author’s study.Whereas project planning is

a preconstruction activity in the planning phase,the bulk of the

controlling occurs in the construction phase of projects.Being a

key stakeholderin the construction phase,contractors mustbe

capable of devising an accurate time schedule such that the re

ant baseline assists in progress monitoring, reporting, and con

ling towards meeting the targets in the project. Accurate plann

requires accurate change controlprocesses to be adopted by the

contractor within the project. Thus, as far as responsibility is c

cerned, accurate planning and controlling clearly lies with the

tractors involved in the project.This finding demonstrates thata

lack of required technicalsupportand competency among the

key stakeholder(the contractors)potentially leads to failure in

delivering modern projects.

Construction methods or technique (RIW ¼ 2.656) was the s

ond most significant attribute across all three categories. Give

the complexity of modern construction projects increases acro

sectors,the requirement for the selection of appropriate constru

tion methods becomes critical for contractors. Both clients and

sultants have realized the benefits of using contemporary met

and techniques,in addition to appropriate exploitation of modern

equipmentin construction projects.

The fourth significant attribute, complexity of design and co

struction (RIW ¼ 2.586),clearly postulates the increasing com-

plexity ofdesign projectsand construction in modern projects

thatimpactcostperformance in overallprojects.The consistent

ranking ofthis attribute by clients,consultants,and contractors

attheir fifth positions asserts the underlying challenges faced

all three groups in successfuldelivery ofprojects.Whereas the

client’smotive ofvalue formoney exertssignificanttruston

consultant’s performance in most modern projects, the contra

performance is usually measured on the effectiveness ofon-site

construction with acceptable quality specification. However, a

of contractor’s in-depth understanding of the projectdesign and

specificationsoften leadsto inefficientconstruction and poor

on-site productivity in the project. This potentially triggers con

and disputes among all three parties, leading to additional cos

the project.Such conflicting requirements certainly contribute to

poorcontrolling ofcostaccounts and results in significantcost

overruns.

The fifth attribute,impropercontrolover site resources

(RIW value ¼ 2.574),clearly indicates the contractor’s inability

in handling construction resources and hence mismanagemenof

the scarce on-site resources in a project.In fact,the contractor

group has acknowledged itas a highly significantattribute by

assigning it as fourth ranking.The agreementof the level of sig-

nificance by both consultants and clients has been found at six

and seventh levels,respectively.The sixth attribute,contractors

deficiencies in realistic planning and scheduling at the tender

which has been ranked at the third position by the contractors

lights a significantconcern on contractors’prequalification and

JOURNAL OF CONSTRUCTION ENGINEERING AND MANAGEMENT © ASCE / MARCH 2013 /271

J. Constr. Eng. Manage. 2013.139:267-279.

Downloaded from ascelibrary.org by GEORGE MASON UNIVERSITY on 03/27/13. Copyright ASCE. For personal use only; all rights reserved.

technical competency required to achieve successful outcomes in a

project.The contractors’ inability to clear understand the project

scope at the tender stage significantly influences their effectiveness

on resource allocation and management control, and thus affects the