Analysis of Enterprise Risk Management at Standard Chartered PLC

VerifiedAdded on 2019/12/03

|22

|4203

|130

Report

AI Summary

This report provides a comprehensive analysis of Enterprise Risk Management (ERM) at Standard Chartered PLC. It begins with an introduction to ERM, highlighting its significance in achieving corporate objectives and managing various business risks. The report then delves into the background of Standard Chartered, emphasizing its focus on Asia, Africa, and the Middle East. It addresses key questions regarding the bank's aims and objectives, past problems like credit and market risks, and problems faced by other companies in the banking sector. The report also covers relevant rules and regulations, potential opportunities such as mobile banking and globalization, and the concept of the threshold of acceptable risk. A risk register is prepared to identify and mitigate risks. The report concludes with a summary of findings and references.

ENTERPRISE RISK

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Background of the organization...................................................................................................1

QUESTIONS...................................................................................................................................1

Aims & Objectives of the Standard Chartered PLC....................................................................1

Problems that have been encountered in the past........................................................................1

Problems faced by the other companies:.....................................................................................3

Rules and regulations...................................................................................................................3

The potential opportunities that could enhance company performance......................................4

Threshold of acceptable Risk.......................................................................................................6

Risk Committee Structure............................................................................................................7

RISK REGISTER............................................................................................................................7

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................1

Background of the organization...................................................................................................1

QUESTIONS...................................................................................................................................1

Aims & Objectives of the Standard Chartered PLC....................................................................1

Problems that have been encountered in the past........................................................................1

Problems faced by the other companies:.....................................................................................3

Rules and regulations...................................................................................................................3

The potential opportunities that could enhance company performance......................................4

Threshold of acceptable Risk.......................................................................................................6

Risk Committee Structure............................................................................................................7

RISK REGISTER............................................................................................................................7

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

Enterprise Risk Management is the process of managing different types of risks which

can have an impact on the organizational strategies which are implemented to achieve corporate

objectives. All the business activities involves a certain level of risks and these are managed

through anticipating, understanding and deciding what can be done. The purpose of this report is

to examine the risk management within an organization named Standard Chartered PLC. It will

recognise the issues which could threaten or enhance the achievement of the aim of the company.

The study will also find out the mitigation actions which can be adopted by the company in

response to these issues. At last the report will end in preparing a risk mitigation register for The

Standard Chartered Group.

Background of the organization

The Standard Chartered Group is a leading international banking and financial services

group, specifically focused on the markets of Asia, Africa and the Middle East. The bank is

regulated by the Financial Conduct Authority and Prudential Regulation Authority in the UK

(Standard chartered plc, 2014). The ultimate parent company of the bank is Standard Chartered

PLC which is listed on the London Stock Exchange and also on various other stock exchanges of

other nations.

QUESTIONS

Aims & Objectives of the Standard Chartered PLC

Following are the objectives of the study:

To achieve accurate level of security at the global level

To prepare remediation and responsive plans in order to meet the strict financial

compliance requirements

To maintain a robust and disciplined approach towards the risk management

Problems that have been encountered in the past

Standard Chartered has faced different kinds of risks in the past. These are as follows:

Providing credit to clients – Bank always carries a risk from the client side related to default of

loan and payments. In the first resort it is a loss to the lender as it creates disruption in the cash

flows and increases the collection costs for the company (Dikmen and Birgonul, 2004). This type

1

Enterprise Risk Management is the process of managing different types of risks which

can have an impact on the organizational strategies which are implemented to achieve corporate

objectives. All the business activities involves a certain level of risks and these are managed

through anticipating, understanding and deciding what can be done. The purpose of this report is

to examine the risk management within an organization named Standard Chartered PLC. It will

recognise the issues which could threaten or enhance the achievement of the aim of the company.

The study will also find out the mitigation actions which can be adopted by the company in

response to these issues. At last the report will end in preparing a risk mitigation register for The

Standard Chartered Group.

Background of the organization

The Standard Chartered Group is a leading international banking and financial services

group, specifically focused on the markets of Asia, Africa and the Middle East. The bank is

regulated by the Financial Conduct Authority and Prudential Regulation Authority in the UK

(Standard chartered plc, 2014). The ultimate parent company of the bank is Standard Chartered

PLC which is listed on the London Stock Exchange and also on various other stock exchanges of

other nations.

QUESTIONS

Aims & Objectives of the Standard Chartered PLC

Following are the objectives of the study:

To achieve accurate level of security at the global level

To prepare remediation and responsive plans in order to meet the strict financial

compliance requirements

To maintain a robust and disciplined approach towards the risk management

Problems that have been encountered in the past

Standard Chartered has faced different kinds of risks in the past. These are as follows:

Providing credit to clients – Bank always carries a risk from the client side related to default of

loan and payments. In the first resort it is a loss to the lender as it creates disruption in the cash

flows and increases the collection costs for the company (Dikmen and Birgonul, 2004). This type

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of risk also puts an impact on the business of the company as it becomes difficult to increase the

revenue and profits.

Country cross border – Under this risk, the bank does not able to obtain payments from its

global customers or third parties due to contractual obligations. These types of risks have

emerged in past few years because company’s exposure to China, Hong Kong, India, Singapore,

Korea and Indonesia has also increased significantly (Emblemsvag and Kjolstad, 2006).

Market – This risk is regarded as the potential for loss of economic value or earnings due to

hostile changes in the financial market rates or prices. Company’s exposure to market risk

generates principally from customer driven transactions. The primary categories of market risks

faced by the company are:

Interest rate risk

Currency exchange rate risk

Equity price risk

Commodity price risk (Rasid and et.al., 2011)

Liquidity – It is another major risk which has been faced by the company many times. It creates

an unusual situation as company either do not have the sufficient financial resources to meet its

obligations or can only access these financial resources at high costs (Frenkel, Dufey and

Hommel. 2005)

Operational – It is the possibility for loss resulting from failure of manpower, process and

technology. It can arise from day to day operations carried out by the group. These issues can

take in several forms and are very important to deal with (Hall and Duperouzel, 2011)

Pension - It is another very unusual issue faced by the company. It is a potential loss arising

due to incapability in meeting the assessed shortfall in the Group’s pension schemes. Pension

risk is not related with the financial performance of this scheme but it is focused on the threat to

company’s position arising from the need to fulfil the obligations of pension scheme.

Reputational – This kind of threat is related with damage to the goodwill, loss of earnings and

contrary impact on the market capitalization of the company (Hartford, 2004). The stakeholders

also starts perceiving negative of the group and its actions.

2

revenue and profits.

Country cross border – Under this risk, the bank does not able to obtain payments from its

global customers or third parties due to contractual obligations. These types of risks have

emerged in past few years because company’s exposure to China, Hong Kong, India, Singapore,

Korea and Indonesia has also increased significantly (Emblemsvag and Kjolstad, 2006).

Market – This risk is regarded as the potential for loss of economic value or earnings due to

hostile changes in the financial market rates or prices. Company’s exposure to market risk

generates principally from customer driven transactions. The primary categories of market risks

faced by the company are:

Interest rate risk

Currency exchange rate risk

Equity price risk

Commodity price risk (Rasid and et.al., 2011)

Liquidity – It is another major risk which has been faced by the company many times. It creates

an unusual situation as company either do not have the sufficient financial resources to meet its

obligations or can only access these financial resources at high costs (Frenkel, Dufey and

Hommel. 2005)

Operational – It is the possibility for loss resulting from failure of manpower, process and

technology. It can arise from day to day operations carried out by the group. These issues can

take in several forms and are very important to deal with (Hall and Duperouzel, 2011)

Pension - It is another very unusual issue faced by the company. It is a potential loss arising

due to incapability in meeting the assessed shortfall in the Group’s pension schemes. Pension

risk is not related with the financial performance of this scheme but it is focused on the threat to

company’s position arising from the need to fulfil the obligations of pension scheme.

Reputational – This kind of threat is related with damage to the goodwill, loss of earnings and

contrary impact on the market capitalization of the company (Hartford, 2004). The stakeholders

also starts perceiving negative of the group and its actions.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Problems faced by the other companies:

There are many other companies in the banking sector which are facing many other types

of risks. These can be explained as follows:

Compliance risk – It is the risk related to breaching legal enactments, statutory

regulations, official provisions and internal regulations (Hoag, 2011). It involves the

issues related to official sanctions, financial loss and loss of reputation.

Foreign exchange – It is a potential loss which is arising due to change in the value of the

bank’s assets or liabilities. It arises due to fluctuations within the exchange rate. The

banks performs transactions related to foreign exchange for their customers and for the

bank’s own accounts (Hoekman, 2004). The value of foreign currency can diminish due

to adverse movement and it causes huge losses for the firms.

Business Risks – This type of threat emerges from the bank’s long term business strategy.

Under this phase, firms are not been able to provide response to the changing market

conditions, loss of market share, etc (Khatta, 2008). It mainly happens due to selection of

a wrong business strategy. This might lead to the failure of the business.

Commodity risk – This kind of threat mainly arises due to adverse impact on the

commodity prices. The commodities include agriculture products (wheat, corn, live-

stock), industrial commodities (iron, copper and zinc) and energy commodities (crude oil,

gas). Change in the value is seen due to change in the demand and supply of services

(Klemetti, 2006). Any of the bank holding these products as part of investment is

subjected to this kind of risks.

Rules and regulations

Standard Chartered Bank is authorized by the Prudential Regulation Authority and it is

regulated by the Financial Conduct Authority and Prudential Regulation Authority. The terms

and conditions of the bank are governed by the English Law and any kind of disputes related to

organization shall be covered under the non-exclusive jurisdiction of the English Courts. All the

transactions of the group banks in UK are protected by the country’s regulatory regime for the

conduct of the business (Knight, 2012).

3

There are many other companies in the banking sector which are facing many other types

of risks. These can be explained as follows:

Compliance risk – It is the risk related to breaching legal enactments, statutory

regulations, official provisions and internal regulations (Hoag, 2011). It involves the

issues related to official sanctions, financial loss and loss of reputation.

Foreign exchange – It is a potential loss which is arising due to change in the value of the

bank’s assets or liabilities. It arises due to fluctuations within the exchange rate. The

banks performs transactions related to foreign exchange for their customers and for the

bank’s own accounts (Hoekman, 2004). The value of foreign currency can diminish due

to adverse movement and it causes huge losses for the firms.

Business Risks – This type of threat emerges from the bank’s long term business strategy.

Under this phase, firms are not been able to provide response to the changing market

conditions, loss of market share, etc (Khatta, 2008). It mainly happens due to selection of

a wrong business strategy. This might lead to the failure of the business.

Commodity risk – This kind of threat mainly arises due to adverse impact on the

commodity prices. The commodities include agriculture products (wheat, corn, live-

stock), industrial commodities (iron, copper and zinc) and energy commodities (crude oil,

gas). Change in the value is seen due to change in the demand and supply of services

(Klemetti, 2006). Any of the bank holding these products as part of investment is

subjected to this kind of risks.

Rules and regulations

Standard Chartered Bank is authorized by the Prudential Regulation Authority and it is

regulated by the Financial Conduct Authority and Prudential Regulation Authority. The terms

and conditions of the bank are governed by the English Law and any kind of disputes related to

organization shall be covered under the non-exclusive jurisdiction of the English Courts. All the

transactions of the group banks in UK are protected by the country’s regulatory regime for the

conduct of the business (Knight, 2012).

3

The potential opportunities that could enhance company performance

There are many opportunities which are knocking on the door of Standard Chartered Plc:

Mobile banking – The trend of mobile banking is increasing very significantly and it can be

seen that people these days prefer to do all their transactions in a relaxed manner. Through

mobile banking, they can manage their cash very easily sitting in any part of the world (Lee,

Yeung, and Hong, 2012). This gives them the comfort and easiness. The trend of mobile banking

is increasing because number of smartphones are also increasing. In this way bank can connect

with its customers in very effective manner. Standard Chartered can also develop its mobile app

which can make the banking very easier for them as well their customers (Manelele and Muya,

2008.). Different type of apps can be introduced with more advanced and user-friendly features.

Hence in this manner company’s performance can be enhanced.

Imparting banking knowledge to customers – Many of the customers wants assistance in

financial planning and framing of financial goals. The banks which can impart correct advice and

knowledge to the customers are expected to grow their businesses (Minelli, Rebora, and Turri,

2008). Many people are of the belief that they are ready to increase business with their service

provider of advisory services are offered to them. Companies in the banking sector has the

opportunity to develop a mutual exchange of value through personalising their experience. For

that purpose it is essential to understand the client’s needs and expectations. This can be done by

leveraging both internal and external resources (Pellegrino, Vajdic and Carbonara, 2013).

Continuous innovation – It is evident that banking sector has seen great transformation in the

recent years. The functioning patter of the companies has changed completely as compared to the

traditional methods (Randall, 2008). It has become essential for the banks to respond effectively

to the changing market conditions. Continuous innovation is the key to success. Without

innovation, it is difficult to cope up with the increasing complexities of the business world. Path

of innovation can be very effective and resourceful for the companies and their business. In this

way the performance can be enhanced (Samson, Reneke, and Wiecek, 2009).

Improved economic conditions – It is another very big opportunity for the organization.

Improved conditions can increase the demand for products and services of the bank. It also

increases the spending power of the individuals as more and more money starts coming into the

economy (Valsamakis, Vivian, and DuToit, 2004). There is an availability of capital and

4

There are many opportunities which are knocking on the door of Standard Chartered Plc:

Mobile banking – The trend of mobile banking is increasing very significantly and it can be

seen that people these days prefer to do all their transactions in a relaxed manner. Through

mobile banking, they can manage their cash very easily sitting in any part of the world (Lee,

Yeung, and Hong, 2012). This gives them the comfort and easiness. The trend of mobile banking

is increasing because number of smartphones are also increasing. In this way bank can connect

with its customers in very effective manner. Standard Chartered can also develop its mobile app

which can make the banking very easier for them as well their customers (Manelele and Muya,

2008.). Different type of apps can be introduced with more advanced and user-friendly features.

Hence in this manner company’s performance can be enhanced.

Imparting banking knowledge to customers – Many of the customers wants assistance in

financial planning and framing of financial goals. The banks which can impart correct advice and

knowledge to the customers are expected to grow their businesses (Minelli, Rebora, and Turri,

2008). Many people are of the belief that they are ready to increase business with their service

provider of advisory services are offered to them. Companies in the banking sector has the

opportunity to develop a mutual exchange of value through personalising their experience. For

that purpose it is essential to understand the client’s needs and expectations. This can be done by

leveraging both internal and external resources (Pellegrino, Vajdic and Carbonara, 2013).

Continuous innovation – It is evident that banking sector has seen great transformation in the

recent years. The functioning patter of the companies has changed completely as compared to the

traditional methods (Randall, 2008). It has become essential for the banks to respond effectively

to the changing market conditions. Continuous innovation is the key to success. Without

innovation, it is difficult to cope up with the increasing complexities of the business world. Path

of innovation can be very effective and resourceful for the companies and their business. In this

way the performance can be enhanced (Samson, Reneke, and Wiecek, 2009).

Improved economic conditions – It is another very big opportunity for the organization.

Improved conditions can increase the demand for products and services of the bank. It also

increases the spending power of the individuals as more and more money starts coming into the

economy (Valsamakis, Vivian, and DuToit, 2004). There is an availability of capital and

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

liquidity funding for the business. Through this company can move on to the path of expansion

and success. It can open the gates of many opportunities and can also increase the rate of

customers for the business. The personal expenditure and consumption pattern of the people

passes in smooth manner (Woods, 2011). It is all reflected in high profitability and high turnover

at the end of the financial period.

Globalization - Globalization has rendered great opportunities for the company not only in one

sector but also in several other sectors also including the banking. Due to globalization, banks

are taking their business beyond the boundaries of the nations (Zou, Zhang and Wang, 2007). It

is being done to grab more value, to intake innovation and to reach towards high segment of

customers. At the global level banks are getting more customers and this is contributing in

enhancing the value of their business. Hence this offers great opportunity for the organization.

Mergers and acquisitions – It is also a widely seen trend within the banking industry. In order

to increase the scale and size of the business, companies are entering into things like joint

venture, mergers, acquisitions etc (Randall, 2008). It is gives them more power and offer more

strength to their business operations. It also helps in increasing the market share of the company

within the industry. The large size holdings can acquire the small size holdings. In this way the

capitalization of the business also gets stronger and the financial performances also enhances

Pellegrino, Vajdic and Carbonara, 2013).

Micro-finance – This trend was restricted to small size financial institutions only. But slowly

and slowly this trend has been taken into consideration by big organizations also (Minelli,

Rebora, and Turri, 2008). Many large size banks have also implemented the micro-finance

services in their business operations.

5

and success. It can open the gates of many opportunities and can also increase the rate of

customers for the business. The personal expenditure and consumption pattern of the people

passes in smooth manner (Woods, 2011). It is all reflected in high profitability and high turnover

at the end of the financial period.

Globalization - Globalization has rendered great opportunities for the company not only in one

sector but also in several other sectors also including the banking. Due to globalization, banks

are taking their business beyond the boundaries of the nations (Zou, Zhang and Wang, 2007). It

is being done to grab more value, to intake innovation and to reach towards high segment of

customers. At the global level banks are getting more customers and this is contributing in

enhancing the value of their business. Hence this offers great opportunity for the organization.

Mergers and acquisitions – It is also a widely seen trend within the banking industry. In order

to increase the scale and size of the business, companies are entering into things like joint

venture, mergers, acquisitions etc (Randall, 2008). It is gives them more power and offer more

strength to their business operations. It also helps in increasing the market share of the company

within the industry. The large size holdings can acquire the small size holdings. In this way the

capitalization of the business also gets stronger and the financial performances also enhances

Pellegrino, Vajdic and Carbonara, 2013).

Micro-finance – This trend was restricted to small size financial institutions only. But slowly

and slowly this trend has been taken into consideration by big organizations also (Minelli,

Rebora, and Turri, 2008). Many large size banks have also implemented the micro-finance

services in their business operations.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

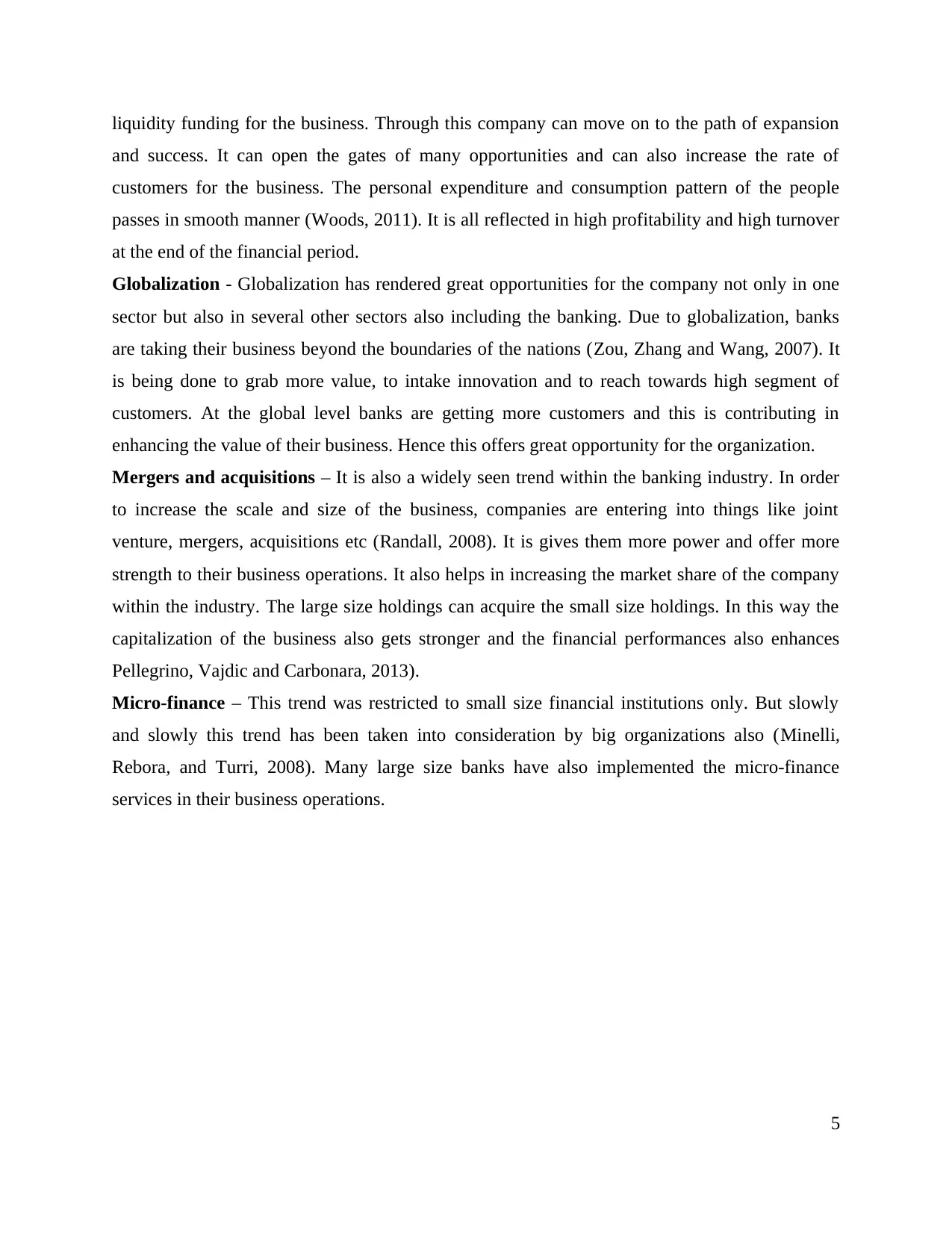

Threshold of acceptable Risk

Figure 1 Threshold of acceptable Risk

(Source Valsamakis, Vivian, and DuToit, 2004)

This process is regarded as the exercise which helps in exploring the risk and threats in an

in-depth manner. Further perceptions and impact related to those potential loses can be

identified. Concept of Threshold of acceptable Risk can be understood by the above diagram.

The risks which are mentioned in the figure are examples only (Samson, Reneke, and Wiecek,

2009). The level of the threats are measured at scales such as very low, low, medium, high etc. It

reflects the amount of risk which is acceptable to a company. For example an organization may

keep the policy that a risk that enhances the costs of a venture by not more than 10% is

acceptable but costs more than 10% is not acceptable. It is to be noted that in case of business,

the customers, sponsors and other stakeholders may have different opinions and different risk

thresholds. It becomes the responsibility of the risk controller to bring consensus on the

acceptable threshold (Hubbard, 2009).

6

Figure 1 Threshold of acceptable Risk

(Source Valsamakis, Vivian, and DuToit, 2004)

This process is regarded as the exercise which helps in exploring the risk and threats in an

in-depth manner. Further perceptions and impact related to those potential loses can be

identified. Concept of Threshold of acceptable Risk can be understood by the above diagram.

The risks which are mentioned in the figure are examples only (Samson, Reneke, and Wiecek,

2009). The level of the threats are measured at scales such as very low, low, medium, high etc. It

reflects the amount of risk which is acceptable to a company. For example an organization may

keep the policy that a risk that enhances the costs of a venture by not more than 10% is

acceptable but costs more than 10% is not acceptable. It is to be noted that in case of business,

the customers, sponsors and other stakeholders may have different opinions and different risk

thresholds. It becomes the responsibility of the risk controller to bring consensus on the

acceptable threshold (Hubbard, 2009).

6

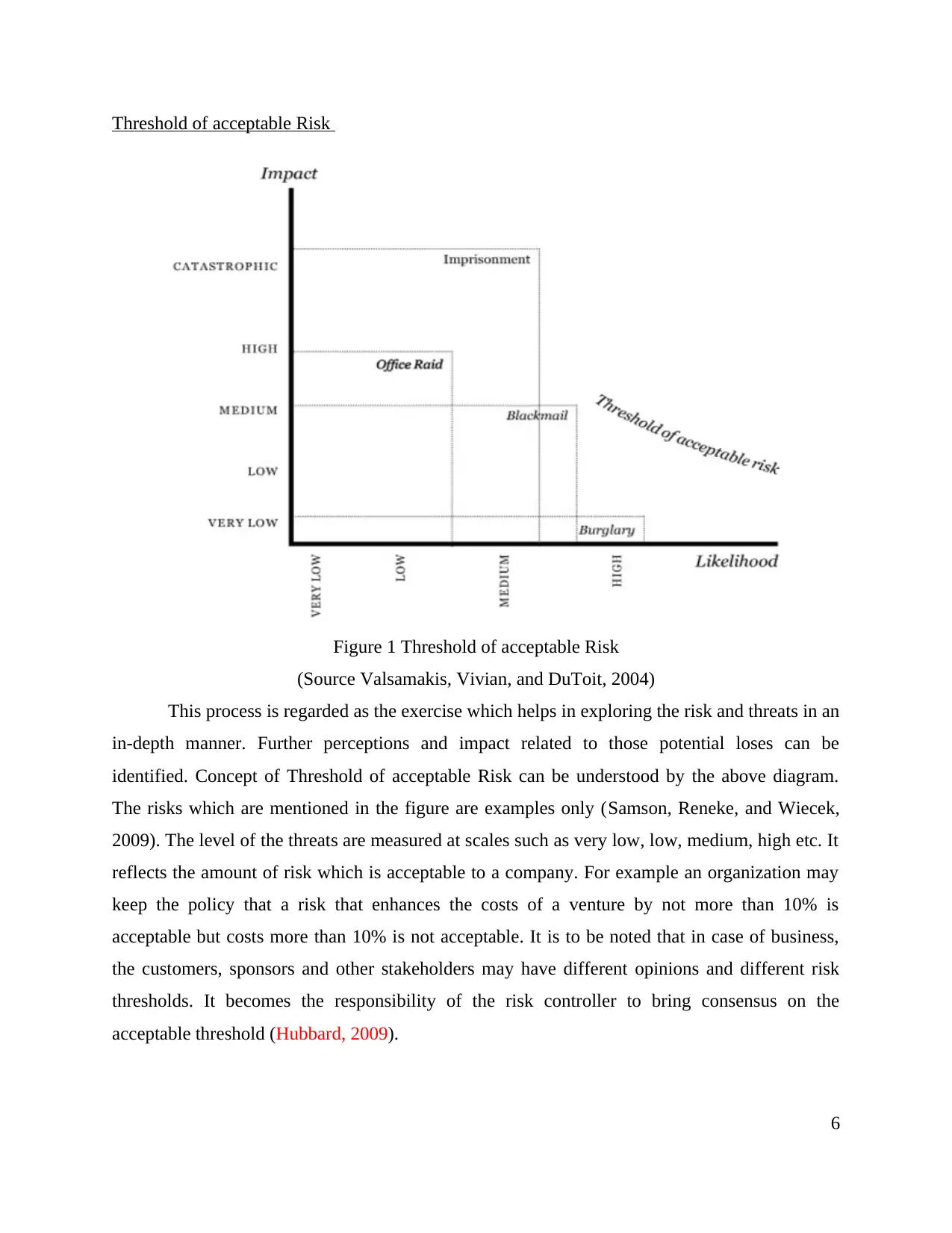

Risk Committee Structure

Figure 2 Group Risk Committee Structure

(Source: Standard chartered, 2015)

The above figure shows the Risk Committee Structure of the Standard Chartered Plc. The

whole structure is segmented into different committees. Each of them is responsible for handling

the risk related to their domain.

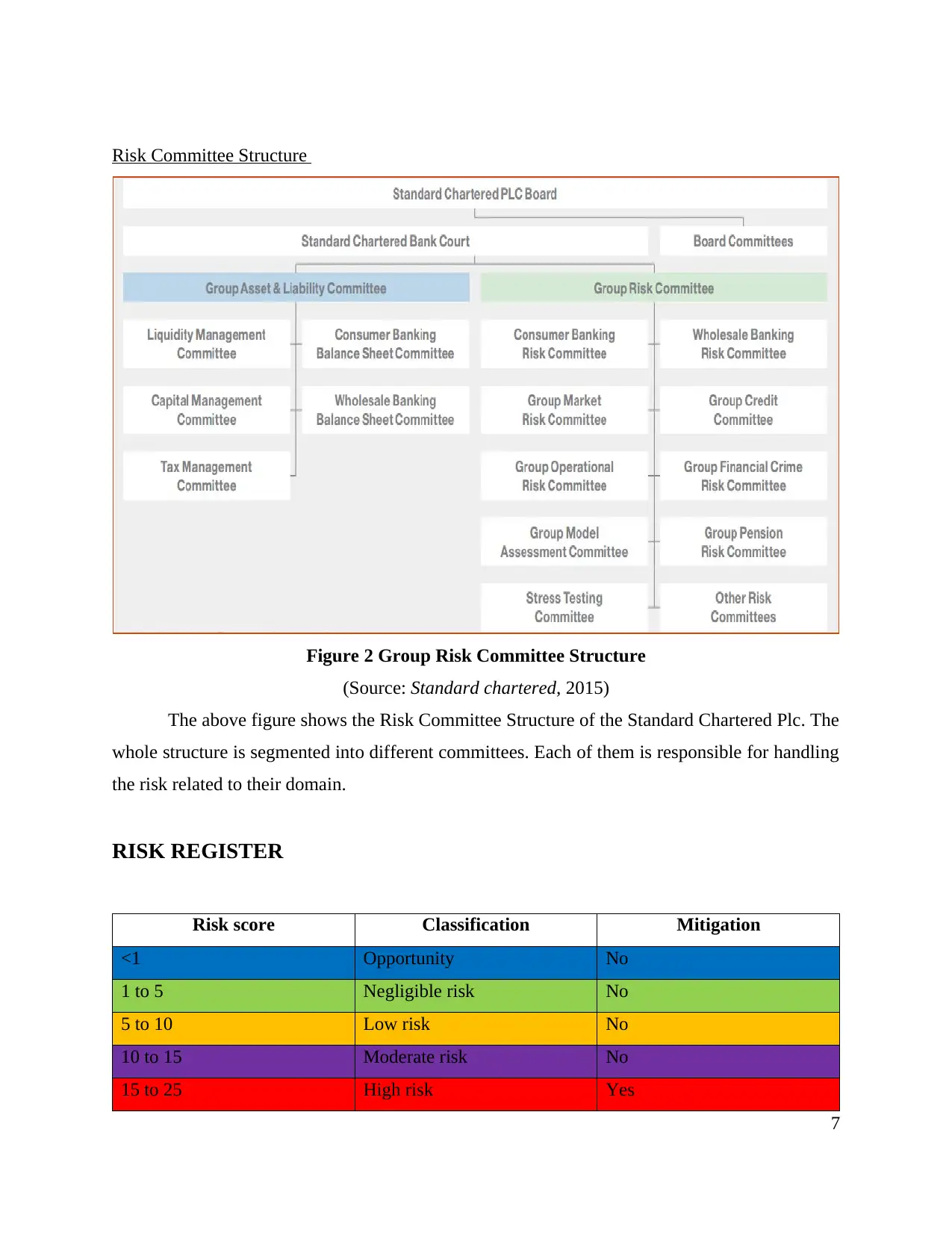

RISK REGISTER

Risk score Classification Mitigation

<1 Opportunity No

1 to 5 Negligible risk No

5 to 10 Low risk No

10 to 15 Moderate risk No

15 to 25 High risk Yes

7

Figure 2 Group Risk Committee Structure

(Source: Standard chartered, 2015)

The above figure shows the Risk Committee Structure of the Standard Chartered Plc. The

whole structure is segmented into different committees. Each of them is responsible for handling

the risk related to their domain.

RISK REGISTER

Risk score Classification Mitigation

<1 Opportunity No

1 to 5 Negligible risk No

5 to 10 Low risk No

10 to 15 Moderate risk No

15 to 25 High risk Yes

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Key register

Likelihood Impact

1 Very unlikely 1 Negligible impact

2 Unlikely 2 Low impact

3 Likely 3 Moderate impact

4 Very likely 4 High impact

5 Almost certain 5 Catastrophic impact

8

Likelihood Impact

1 Very unlikely 1 Negligible impact

2 Unlikely 2 Low impact

3 Likely 3 Moderate impact

4 Very likely 4 High impact

5 Almost certain 5 Catastrophic impact

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

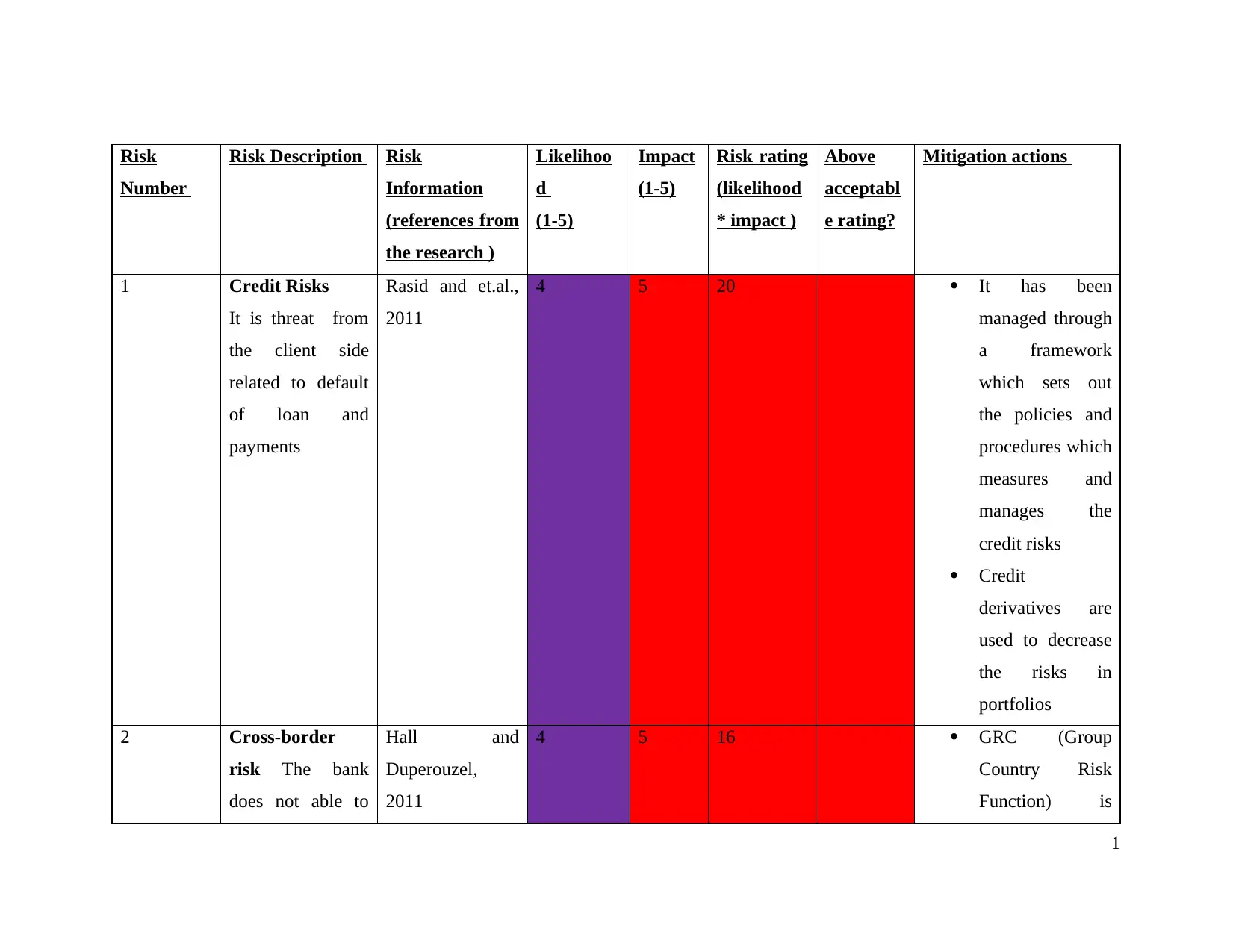

Risk

Number

Risk Description Risk

Information

(references from

the research )

Likelihoo

d

(1-5)

Impact

(1-5)

Risk rating

(likelihood

* impact )

Above

acceptabl

e rating?

Mitigation actions

1 Credit Risks

It is threat from

the client side

related to default

of loan and

payments

Rasid and et.al.,

2011

4 5 20 It has been

managed through

a framework

which sets out

the policies and

procedures which

measures and

manages the

credit risks

Credit

derivatives are

used to decrease

the risks in

portfolios

2 Cross-border

risk The bank

does not able to

Hall and

Duperouzel,

2011

4 5 16 GRC (Group

Country Risk

Function) is

1

Number

Risk Description Risk

Information

(references from

the research )

Likelihoo

d

(1-5)

Impact

(1-5)

Risk rating

(likelihood

* impact )

Above

acceptabl

e rating?

Mitigation actions

1 Credit Risks

It is threat from

the client side

related to default

of loan and

payments

Rasid and et.al.,

2011

4 5 20 It has been

managed through

a framework

which sets out

the policies and

procedures which

measures and

manages the

credit risks

Credit

derivatives are

used to decrease

the risks in

portfolios

2 Cross-border

risk The bank

does not able to

Hall and

Duperouzel,

2011

4 5 16 GRC (Group

Country Risk

Function) is

1

obtain payments

from its global

customers or third

parties due to

contractual

obligations

responsible for

the nations cross

border risk limits

Countries which

are identified as

higher risks are

subjected to

central

monitoring

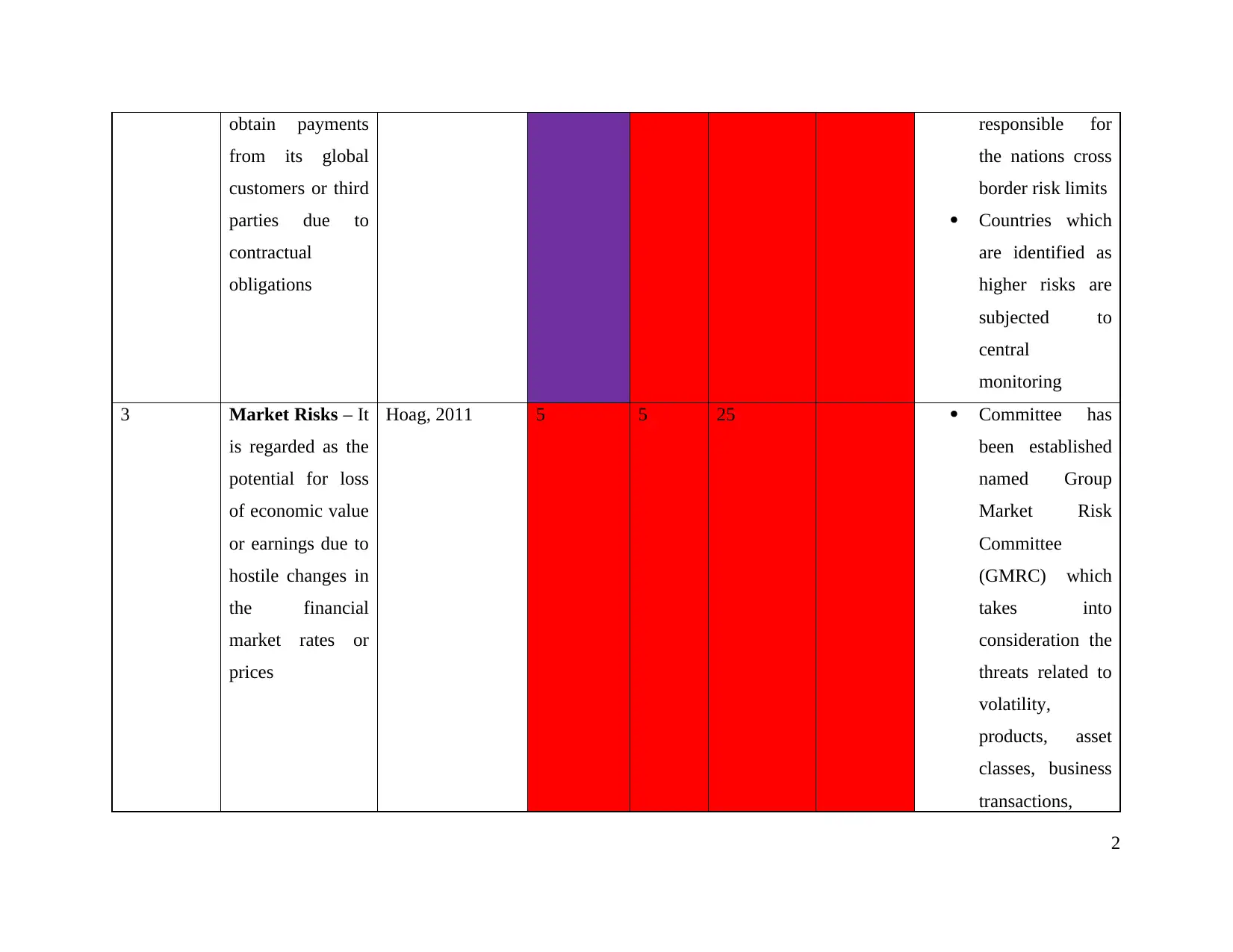

3 Market Risks – It

is regarded as the

potential for loss

of economic value

or earnings due to

hostile changes in

the financial

market rates or

prices

Hoag, 2011 5 5 25 Committee has

been established

named Group

Market Risk

Committee

(GMRC) which

takes into

consideration the

threats related to

volatility,

products, asset

classes, business

transactions,

2

from its global

customers or third

parties due to

contractual

obligations

responsible for

the nations cross

border risk limits

Countries which

are identified as

higher risks are

subjected to

central

monitoring

3 Market Risks – It

is regarded as the

potential for loss

of economic value

or earnings due to

hostile changes in

the financial

market rates or

prices

Hoag, 2011 5 5 25 Committee has

been established

named Group

Market Risk

Committee

(GMRC) which

takes into

consideration the

threats related to

volatility,

products, asset

classes, business

transactions,

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.