Comprehensive Enterprise Risk Management Analysis: Standard Chartered

VerifiedAdded on 2019/12/03

|19

|3794

|72

Report

AI Summary

This report provides a comprehensive analysis of Enterprise Risk Management (ERM) at Standard Chartered Bank. It begins with an introduction to the bank's aims and objectives, followed by an examination of major problems encountered in the past, including credit, market, and legal risks, and how these compare to challenges faced by other organizations in the same sector. The report then explores the applicable regulations and potential opportunities for enhancing company performance, such as expansion in developing countries and technology infrastructure setup. A detailed risk assessment is presented, identifying and scoring risks like technical, market, credit, legal, strategic implementation, and wealth management, along with proposed mitigation actions. The report concludes with a summary of findings and references.

Enterprise risk management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

The aims and objectives of the organization...............................................................................1

Major problems which enterprise has encountered in past..........................................................1

Problems have other organizations in the same sector encountered in the past..........................2

Regulation is applicable to the organization/sector.....................................................................3

Potential opportunities that could enhance company performance.............................................3

Identification of risks and scoring each risk................................................................................6

Concept of the acceptable risk threshold...................................................................................11

Mitigation actions for risks that are above the stated threshold................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

APPENDIX 1.................................................................................................................................18

INTRODUCTION...........................................................................................................................1

The aims and objectives of the organization...............................................................................1

Major problems which enterprise has encountered in past..........................................................1

Problems have other organizations in the same sector encountered in the past..........................2

Regulation is applicable to the organization/sector.....................................................................3

Potential opportunities that could enhance company performance.............................................3

Identification of risks and scoring each risk................................................................................6

Concept of the acceptable risk threshold...................................................................................11

Mitigation actions for risks that are above the stated threshold................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................16

APPENDIX 1.................................................................................................................................18

LIST OF TABLE

Table 1: Opportunities.....................................................................................................................4

Table 2: Threats for bank.................................................................................................................6

LIST OF FIGURE

Figure 1: Quantitative method for risk measuring.........................................................................12

Table 1: Opportunities.....................................................................................................................4

Table 2: Threats for bank.................................................................................................................6

LIST OF FIGURE

Figure 1: Quantitative method for risk measuring.........................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Standard charted bank is UK base banking group and it provides variety of financial

services to its customers throughout the world. In addition, firm have more than 500 offices in

more than fifty countries in order to deliver consumer banking and institutional banking services

in a significant manner. However, enterprise is facing several risks or issues including legal and

reputational, risks-credit, foreign exchange, business and regulatory that affects business of

enterprise. The main purpose behind choosing Standard charted bank is to explore various risks

associated with the banking operations of company and strategies taken by management to

control over risks in the modern arena. By conducting research, investigator would be able to

understand the role of Risk Management System and its applicability in managing risks and

baking operations effectively.

The aims and objectives of the organization

Aim: The main aim of Standard charted bank is to provide banking and investment related

services to high net worth clients by managing risks in dynamic changing era.

Objectives of bank

To build a sustainable business and become a leading international leading group over the

long term with managing risks

To offer variety of products and services to personal and business customers across

different countries (Standard Chartered Annual Report, 2015)

To perform significant private banking and international banking operations to magnetize

customers by effective use of Enterprise Risk Management tactics in business functions.

Major problems which enterprise has encountered in past

Over the past few years, several changes arise in international financial market and these

changes negatively influence baking operation of banks such as corporate losses and imprudent

business etc. Earlier, Standard charted bank was faced several challenges related to its corporate

strategy including legal and reputational, wealth management liquidity and operational risks. As

per the standard charted report (2004), it is clear that firm has encountered credit, market,

liquidity, operation and other kinds of risks in their business operations. Credit risk was occurred

in case of individual borrower and portfolios on the banking and trading books functions no

execute in a proper way. Besides that, due to potential changes in market prices and rates,

customer retention and magnetizes new customer’s kinds of issues are also faced by organization

1

Standard charted bank is UK base banking group and it provides variety of financial

services to its customers throughout the world. In addition, firm have more than 500 offices in

more than fifty countries in order to deliver consumer banking and institutional banking services

in a significant manner. However, enterprise is facing several risks or issues including legal and

reputational, risks-credit, foreign exchange, business and regulatory that affects business of

enterprise. The main purpose behind choosing Standard charted bank is to explore various risks

associated with the banking operations of company and strategies taken by management to

control over risks in the modern arena. By conducting research, investigator would be able to

understand the role of Risk Management System and its applicability in managing risks and

baking operations effectively.

The aims and objectives of the organization

Aim: The main aim of Standard charted bank is to provide banking and investment related

services to high net worth clients by managing risks in dynamic changing era.

Objectives of bank

To build a sustainable business and become a leading international leading group over the

long term with managing risks

To offer variety of products and services to personal and business customers across

different countries (Standard Chartered Annual Report, 2015)

To perform significant private banking and international banking operations to magnetize

customers by effective use of Enterprise Risk Management tactics in business functions.

Major problems which enterprise has encountered in past

Over the past few years, several changes arise in international financial market and these

changes negatively influence baking operation of banks such as corporate losses and imprudent

business etc. Earlier, Standard charted bank was faced several challenges related to its corporate

strategy including legal and reputational, wealth management liquidity and operational risks. As

per the standard charted report (2004), it is clear that firm has encountered credit, market,

liquidity, operation and other kinds of risks in their business operations. Credit risk was occurred

in case of individual borrower and portfolios on the banking and trading books functions no

execute in a proper way. Besides that, due to potential changes in market prices and rates,

customer retention and magnetizes new customer’s kinds of issues are also faced by organization

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Standard charted report, 2004). Despite of that, operation and liquidity kinds of problems were

also encountered in firm and affects direct or indirect loss on business operations of bank such as

processes, infrastructure and personnel failure. Apart from this, due to inappropriate strategies

and inadequate allocation of resources, management of bank was failing to achieve business

targets and gain competitive advantages (Akatova and Curran, 2013). As per the report of Atos

consulting (2007), standard charted bank is struggling to understand the market sentiments and

changes occur in financial markets. The adverse impact of these kinds of risks can be seen in

forms of huge corporate losses and declined margin of international bank.

According to Davies (2015), from past couple of years, enterprise is facing rising bad

loans and commodity management related risks. In addition, share price of bank is very low and

it dilutes investors to invest money in international bank. However, on the other hand,

shareholders of bank are also throwing good money after bad situation raised. These kinds of

strategic issues create questions about its capital strength and creates negative image in the

canvas of the minds of customers. From the study, it is found that enterprise is still facing

different legal issues such as sanctions breaches and fines. On the other side, cut back on low-

returning, banking exposures and wealth management strategies kinds of risks and forced firm to

cut $20 billion of risk weighted assets and invest $1 billion to refocus on wealthy clients (Davies,

2015).

Weinland (2015) stated that Standard charted bank is facing technology related risks

including fail to set-up adequate financial infrastructure; manage database and the regulatory

issues associated with the appropriate use of technology in banking functions. Furthermore,

enterprise is also concentrating on credit modelling systems and SWIFT techniques to overcome

issues and takes financial decisions effectively (Weinland, 2015).

Problems have other organizations in the same sector encountered in the past

In the same financial sector, other organizations including Wellfleet, Barclays Plc and

HSBC banks were also created same kinds of business issues. In the time period of 2007-2010,

management of firm was faced credit risk and performance measurement kinds of problems in

their banking operations (Borghesi and Gaudenzi, 2013). Due to this kind of risk, profit and

customer base of company were also affected. Besides that, soggy commodity markets, changing

needs of customers and fluctuation come in market are also created problems for Barclays

2

also encountered in firm and affects direct or indirect loss on business operations of bank such as

processes, infrastructure and personnel failure. Apart from this, due to inappropriate strategies

and inadequate allocation of resources, management of bank was failing to achieve business

targets and gain competitive advantages (Akatova and Curran, 2013). As per the report of Atos

consulting (2007), standard charted bank is struggling to understand the market sentiments and

changes occur in financial markets. The adverse impact of these kinds of risks can be seen in

forms of huge corporate losses and declined margin of international bank.

According to Davies (2015), from past couple of years, enterprise is facing rising bad

loans and commodity management related risks. In addition, share price of bank is very low and

it dilutes investors to invest money in international bank. However, on the other hand,

shareholders of bank are also throwing good money after bad situation raised. These kinds of

strategic issues create questions about its capital strength and creates negative image in the

canvas of the minds of customers. From the study, it is found that enterprise is still facing

different legal issues such as sanctions breaches and fines. On the other side, cut back on low-

returning, banking exposures and wealth management strategies kinds of risks and forced firm to

cut $20 billion of risk weighted assets and invest $1 billion to refocus on wealthy clients (Davies,

2015).

Weinland (2015) stated that Standard charted bank is facing technology related risks

including fail to set-up adequate financial infrastructure; manage database and the regulatory

issues associated with the appropriate use of technology in banking functions. Furthermore,

enterprise is also concentrating on credit modelling systems and SWIFT techniques to overcome

issues and takes financial decisions effectively (Weinland, 2015).

Problems have other organizations in the same sector encountered in the past

In the same financial sector, other organizations including Wellfleet, Barclays Plc and

HSBC banks were also created same kinds of business issues. In the time period of 2007-2010,

management of firm was faced credit risk and performance measurement kinds of problems in

their banking operations (Borghesi and Gaudenzi, 2013). Due to this kind of risk, profit and

customer base of company were also affected. Besides that, soggy commodity markets, changing

needs of customers and fluctuation come in market are also created problems for Barclays

2

Plc and other banks also created challenges for banks to meet personal and business customers

needs in a significant manner.

Regulation is applicable to the organization/sector

In the context of meeting regulatory standards and requirements, government,

international regulatory developments have developed different codes and regulations. For risk

management, managing and supervising the company, Norway’s Public Limited Liability

Companies Act was framed. In addition, to address sustainability issues and manage capital

adequacy in the banking sector, firm was developed Asset and Liability Committee (ALCO). In

addition, for capital adequacy, Group Capital Management Committee (GCMC) and Group

Treasury (GT) committee have been prepared by Standard charted bank. Capital Planning

Framework has been framed to ensure that each entity of bank have sufficient capital or funds to

meet local regulatory capital requirements in a significant manner (Standard Chartered Annual

Report, 2015).

In order to support its strategies, five years strategic, business and capital plans were

developed by international bank. In present arena, for risk management, enterprise has a strong

governance culture and framework. Despite of that, for managing and meeting the local

regulatory requirements, risk management principles were developed by bank (Garvey, 2008).

Risk management framework helps enterprise to better perform in risky business environment

such as market, operational, liquidity and credit risks etc. Besides that, functional and divisional

committees were established to monitor over risk issues and bringing alignment across the

business and the functions. Country Risk Committee (CRC) was framed within organization for

the effective management of risks and allocation of the roles and responsibilities of RCOs

locally. Regulatory requirements and policies of bank are varying as per different locations and

countries (Standard Chartered Annual Report, 2015). For example, in India, specific provisions

and guidelines of bank is framed under the RBI guidelines. On the other side, in Norway,

policies are framed under the Norway’s Public Limited Liability Companies Act. Due to

different locations and standard set by various banking institutions, policies and services offered

by bank to its customers also influence.

Potential opportunities that could enhance company performance

As a leading international bank, to retain its existing and attracting new customers, it is

essential for bank to adopt appropriate system and follow guidelines developed by government.

3

needs in a significant manner.

Regulation is applicable to the organization/sector

In the context of meeting regulatory standards and requirements, government,

international regulatory developments have developed different codes and regulations. For risk

management, managing and supervising the company, Norway’s Public Limited Liability

Companies Act was framed. In addition, to address sustainability issues and manage capital

adequacy in the banking sector, firm was developed Asset and Liability Committee (ALCO). In

addition, for capital adequacy, Group Capital Management Committee (GCMC) and Group

Treasury (GT) committee have been prepared by Standard charted bank. Capital Planning

Framework has been framed to ensure that each entity of bank have sufficient capital or funds to

meet local regulatory capital requirements in a significant manner (Standard Chartered Annual

Report, 2015).

In order to support its strategies, five years strategic, business and capital plans were

developed by international bank. In present arena, for risk management, enterprise has a strong

governance culture and framework. Despite of that, for managing and meeting the local

regulatory requirements, risk management principles were developed by bank (Garvey, 2008).

Risk management framework helps enterprise to better perform in risky business environment

such as market, operational, liquidity and credit risks etc. Besides that, functional and divisional

committees were established to monitor over risk issues and bringing alignment across the

business and the functions. Country Risk Committee (CRC) was framed within organization for

the effective management of risks and allocation of the roles and responsibilities of RCOs

locally. Regulatory requirements and policies of bank are varying as per different locations and

countries (Standard Chartered Annual Report, 2015). For example, in India, specific provisions

and guidelines of bank is framed under the RBI guidelines. On the other side, in Norway,

policies are framed under the Norway’s Public Limited Liability Companies Act. Due to

different locations and standard set by various banking institutions, policies and services offered

by bank to its customers also influence.

Potential opportunities that could enhance company performance

As a leading international bank, to retain its existing and attracting new customers, it is

essential for bank to adopt appropriate system and follow guidelines developed by government.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

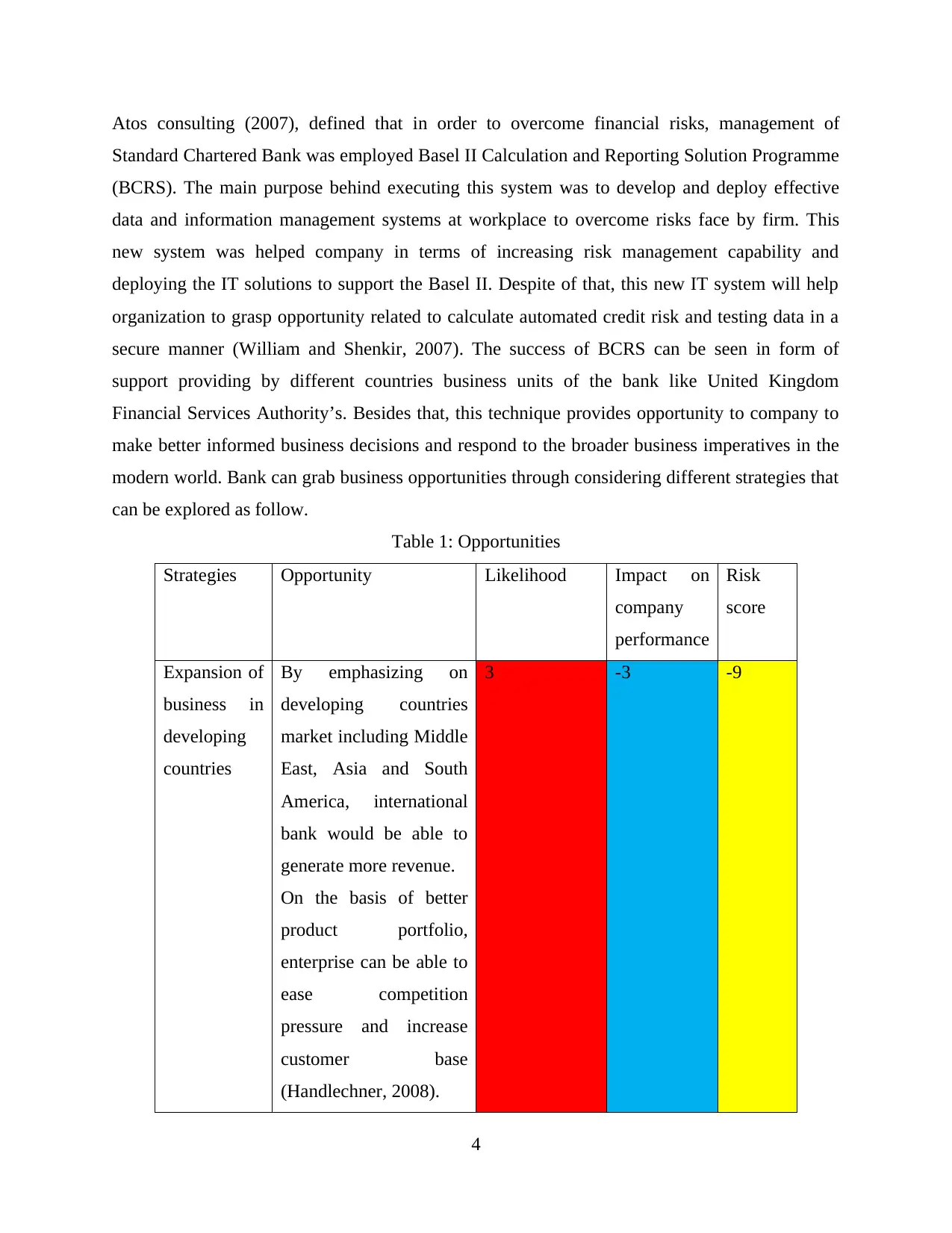

Atos consulting (2007), defined that in order to overcome financial risks, management of

Standard Chartered Bank was employed Basel II Calculation and Reporting Solution Programme

(BCRS). The main purpose behind executing this system was to develop and deploy effective

data and information management systems at workplace to overcome risks face by firm. This

new system was helped company in terms of increasing risk management capability and

deploying the IT solutions to support the Basel II. Despite of that, this new IT system will help

organization to grasp opportunity related to calculate automated credit risk and testing data in a

secure manner (William and Shenkir, 2007). The success of BCRS can be seen in form of

support providing by different countries business units of the bank like United Kingdom

Financial Services Authority’s. Besides that, this technique provides opportunity to company to

make better informed business decisions and respond to the broader business imperatives in the

modern world. Bank can grab business opportunities through considering different strategies that

can be explored as follow.

Table 1: Opportunities

Strategies Opportunity Likelihood Impact on

company

performance

Risk

score

Expansion of

business in

developing

countries

By emphasizing on

developing countries

market including Middle

East, Asia and South

America, international

bank would be able to

generate more revenue.

On the basis of better

product portfolio,

enterprise can be able to

ease competition

pressure and increase

customer base

(Handlechner, 2008).

3 -3 -9

4

Standard Chartered Bank was employed Basel II Calculation and Reporting Solution Programme

(BCRS). The main purpose behind executing this system was to develop and deploy effective

data and information management systems at workplace to overcome risks face by firm. This

new system was helped company in terms of increasing risk management capability and

deploying the IT solutions to support the Basel II. Despite of that, this new IT system will help

organization to grasp opportunity related to calculate automated credit risk and testing data in a

secure manner (William and Shenkir, 2007). The success of BCRS can be seen in form of

support providing by different countries business units of the bank like United Kingdom

Financial Services Authority’s. Besides that, this technique provides opportunity to company to

make better informed business decisions and respond to the broader business imperatives in the

modern world. Bank can grab business opportunities through considering different strategies that

can be explored as follow.

Table 1: Opportunities

Strategies Opportunity Likelihood Impact on

company

performance

Risk

score

Expansion of

business in

developing

countries

By emphasizing on

developing countries

market including Middle

East, Asia and South

America, international

bank would be able to

generate more revenue.

On the basis of better

product portfolio,

enterprise can be able to

ease competition

pressure and increase

customer base

(Handlechner, 2008).

3 -3 -9

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

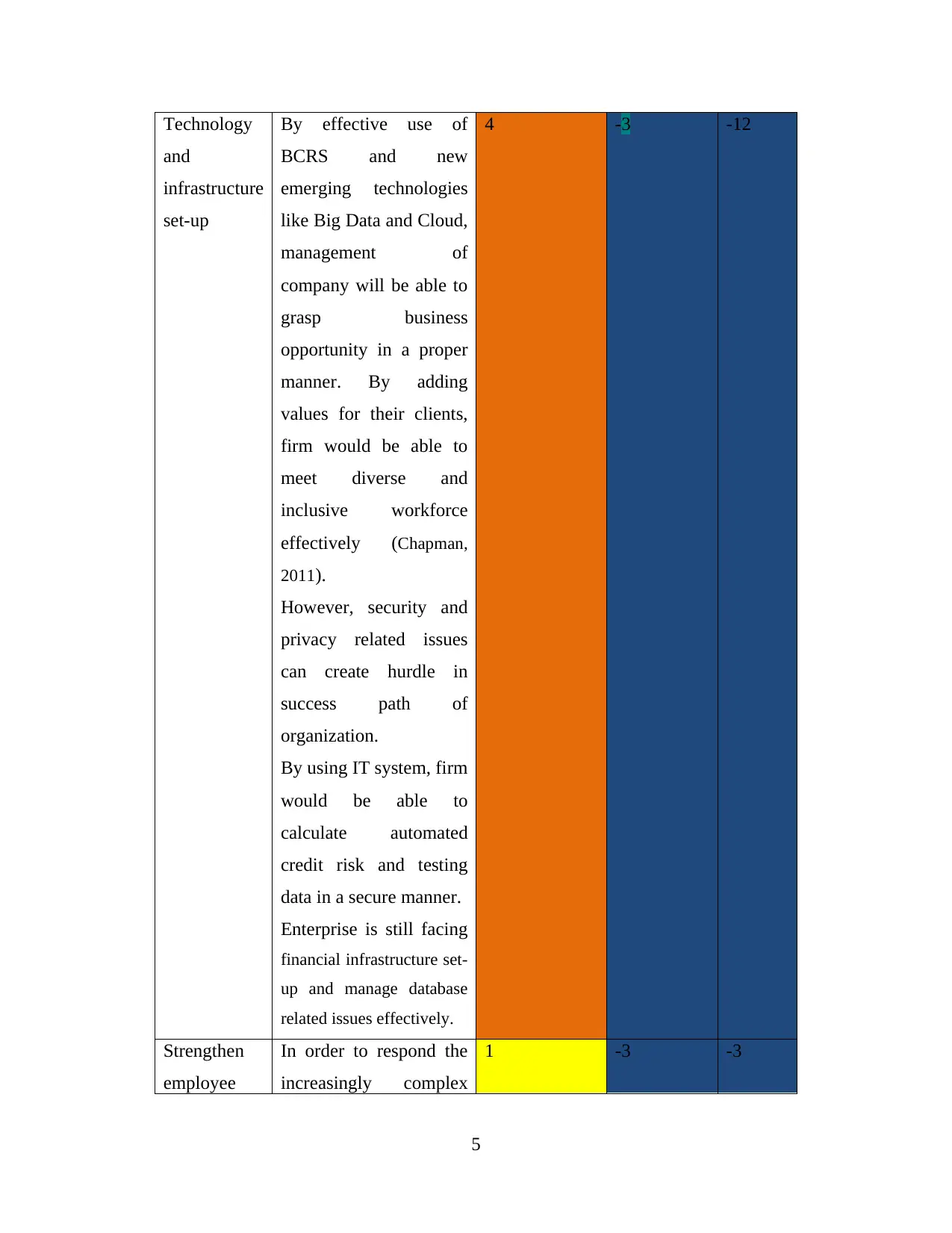

Technology

and

infrastructure

set-up

By effective use of

BCRS and new

emerging technologies

like Big Data and Cloud,

management of

company will be able to

grasp business

opportunity in a proper

manner. By adding

values for their clients,

firm would be able to

meet diverse and

inclusive workforce

effectively (Chapman,

2011).

However, security and

privacy related issues

can create hurdle in

success path of

organization.

By using IT system, firm

would be able to

calculate automated

credit risk and testing

data in a secure manner.

Enterprise is still facing

financial infrastructure set-

up and manage database

related issues effectively.

4 -3 -12

Strengthen

employee

In order to respond the

increasingly complex

1 -3 -3

5

and

infrastructure

set-up

By effective use of

BCRS and new

emerging technologies

like Big Data and Cloud,

management of

company will be able to

grasp business

opportunity in a proper

manner. By adding

values for their clients,

firm would be able to

meet diverse and

inclusive workforce

effectively (Chapman,

2011).

However, security and

privacy related issues

can create hurdle in

success path of

organization.

By using IT system, firm

would be able to

calculate automated

credit risk and testing

data in a secure manner.

Enterprise is still facing

financial infrastructure set-

up and manage database

related issues effectively.

4 -3 -12

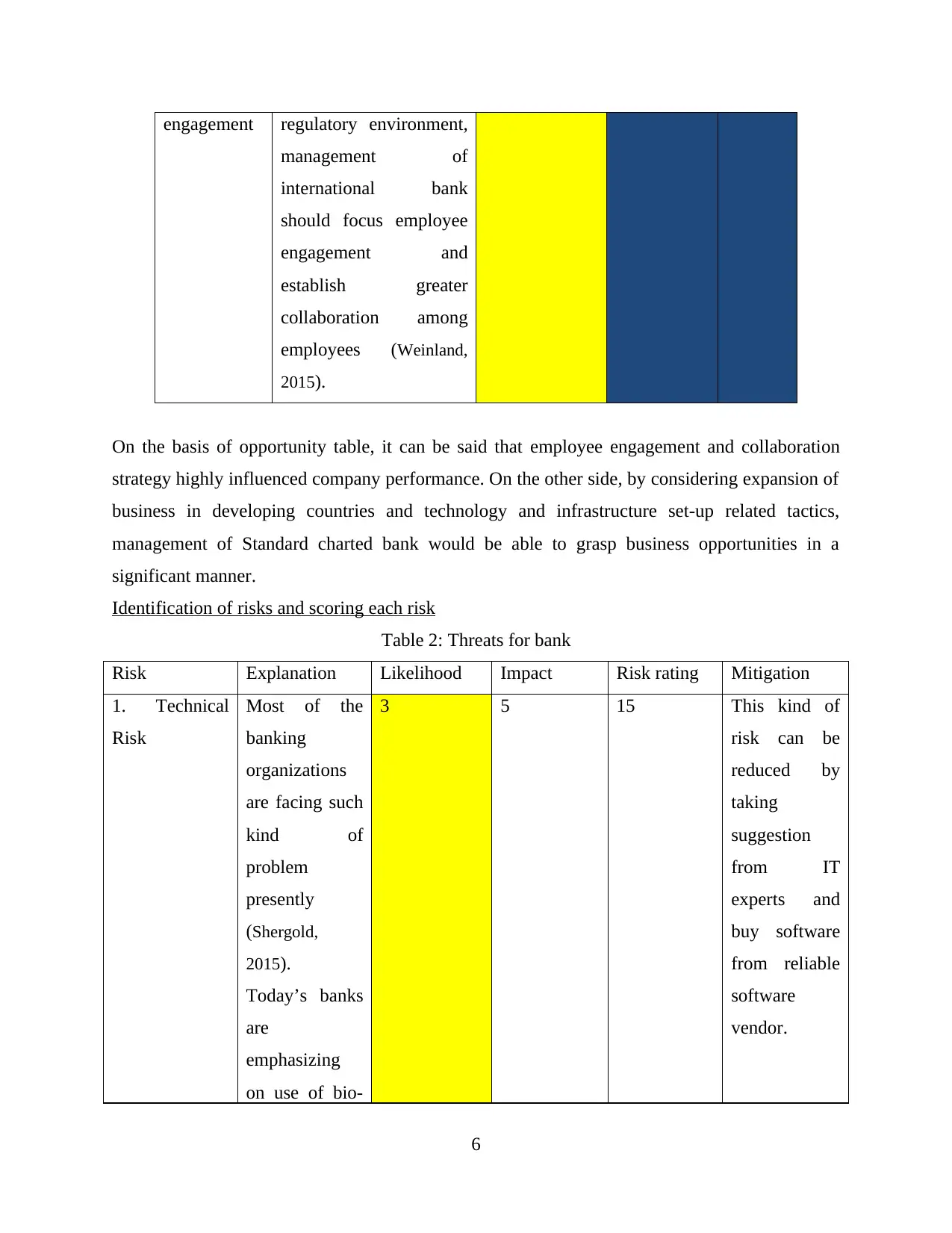

Strengthen

employee

In order to respond the

increasingly complex

1 -3 -3

5

engagement regulatory environment,

management of

international bank

should focus employee

engagement and

establish greater

collaboration among

employees (Weinland,

2015).

On the basis of opportunity table, it can be said that employee engagement and collaboration

strategy highly influenced company performance. On the other side, by considering expansion of

business in developing countries and technology and infrastructure set-up related tactics,

management of Standard charted bank would be able to grasp business opportunities in a

significant manner.

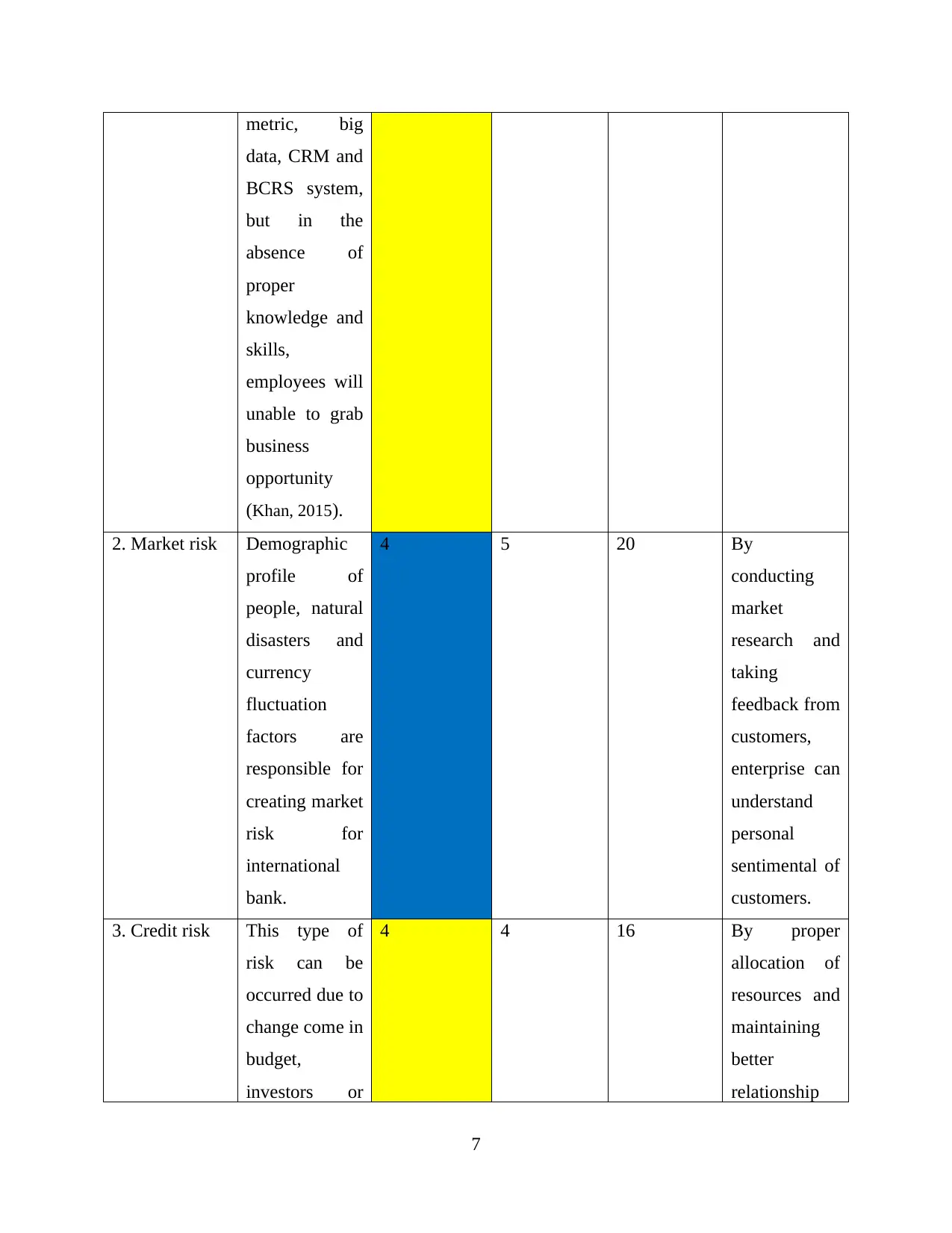

Identification of risks and scoring each risk

Table 2: Threats for bank

Risk Explanation Likelihood Impact Risk rating Mitigation

1. Technical

Risk

Most of the

banking

organizations

are facing such

kind of

problem

presently

(Shergold,

2015).

Today’s banks

are

emphasizing

on use of bio-

3 5 15 This kind of

risk can be

reduced by

taking

suggestion

from IT

experts and

buy software

from reliable

software

vendor.

6

management of

international bank

should focus employee

engagement and

establish greater

collaboration among

employees (Weinland,

2015).

On the basis of opportunity table, it can be said that employee engagement and collaboration

strategy highly influenced company performance. On the other side, by considering expansion of

business in developing countries and technology and infrastructure set-up related tactics,

management of Standard charted bank would be able to grasp business opportunities in a

significant manner.

Identification of risks and scoring each risk

Table 2: Threats for bank

Risk Explanation Likelihood Impact Risk rating Mitigation

1. Technical

Risk

Most of the

banking

organizations

are facing such

kind of

problem

presently

(Shergold,

2015).

Today’s banks

are

emphasizing

on use of bio-

3 5 15 This kind of

risk can be

reduced by

taking

suggestion

from IT

experts and

buy software

from reliable

software

vendor.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

metric, big

data, CRM and

BCRS system,

but in the

absence of

proper

knowledge and

skills,

employees will

unable to grab

business

opportunity

(Khan, 2015).

2. Market risk Demographic

profile of

people, natural

disasters and

currency

fluctuation

factors are

responsible for

creating market

risk for

international

bank.

4 5 20 By

conducting

market

research and

taking

feedback from

customers,

enterprise can

understand

personal

sentimental of

customers.

3. Credit risk This type of

risk can be

occurred due to

change come in

budget,

investors or

4 4 16 By proper

allocation of

resources and

maintaining

better

relationship

7

data, CRM and

BCRS system,

but in the

absence of

proper

knowledge and

skills,

employees will

unable to grab

business

opportunity

(Khan, 2015).

2. Market risk Demographic

profile of

people, natural

disasters and

currency

fluctuation

factors are

responsible for

creating market

risk for

international

bank.

4 5 20 By

conducting

market

research and

taking

feedback from

customers,

enterprise can

understand

personal

sentimental of

customers.

3. Credit risk This type of

risk can be

occurred due to

change come in

budget,

investors or

4 4 16 By proper

allocation of

resources and

maintaining

better

relationship

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

economic

conditions.

with

stakeholders,

company

would be able

to identify

credit risk. In

addition, by

managing

adequate

amount of

funds, firm

would be able

to overcome

negative

impact of

credit risk.

4. Legal and

reputational

risks

Government

and legal rules

®ulations

related factors

can create

hurdle in

successful

implementation

of

organizational

policies in a

significant

manner (Khan,

2015).

3 4 12 By

maintaining

transparency

and

confidentiality

in entire

transactions

and

information

sharing, firm

can enhance

integrity. By

following

regulations

developed by

8

conditions.

with

stakeholders,

company

would be able

to identify

credit risk. In

addition, by

managing

adequate

amount of

funds, firm

would be able

to overcome

negative

impact of

credit risk.

4. Legal and

reputational

risks

Government

and legal rules

®ulations

related factors

can create

hurdle in

successful

implementation

of

organizational

policies in a

significant

manner (Khan,

2015).

3 4 12 By

maintaining

transparency

and

confidentiality

in entire

transactions

and

information

sharing, firm

can enhance

integrity. By

following

regulations

developed by

8

government

and financial

institutions,

chances of

negative

implications

of law and

regulations

can be

reduced.

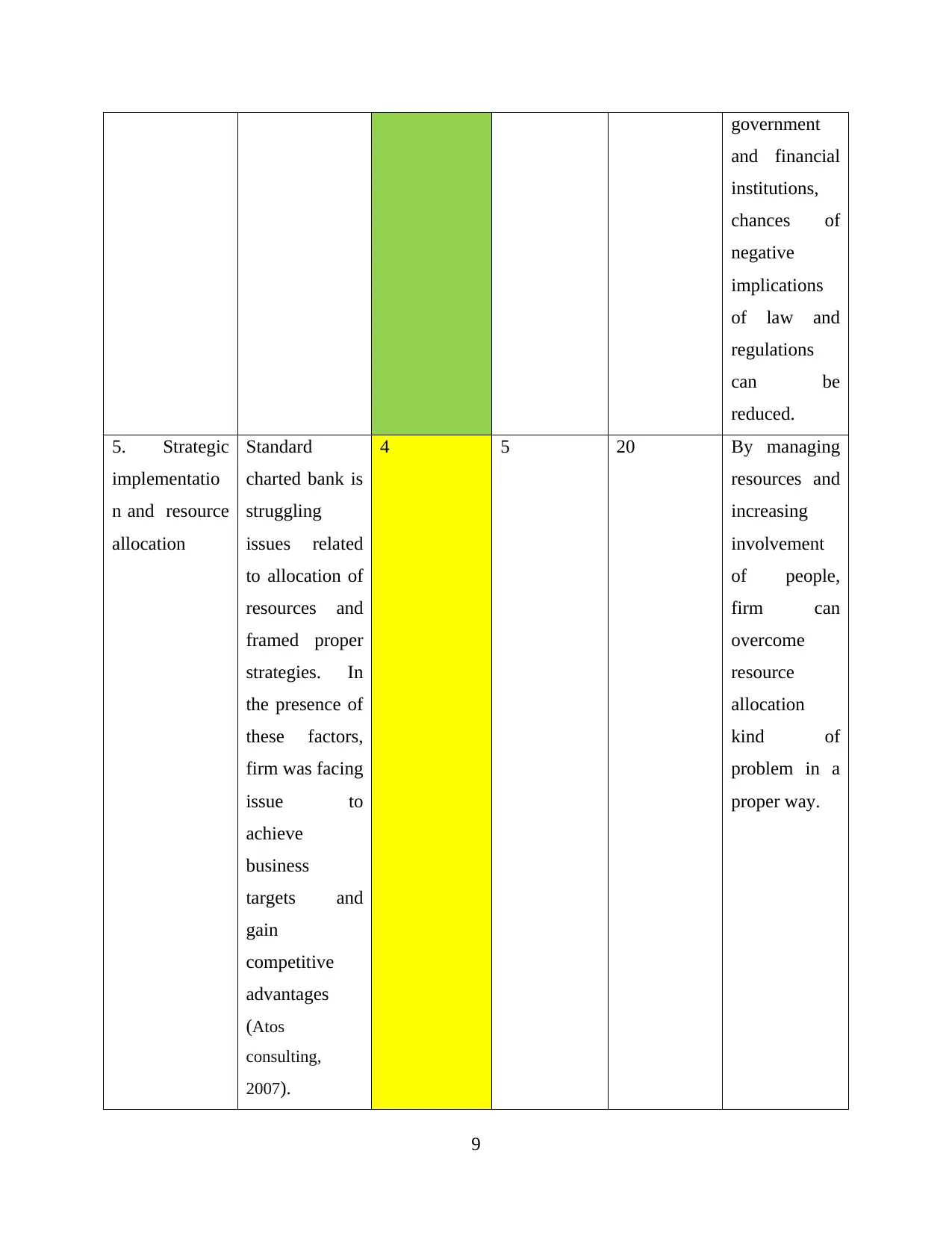

5. Strategic

implementatio

n and resource

allocation

Standard

charted bank is

struggling

issues related

to allocation of

resources and

framed proper

strategies. In

the presence of

these factors,

firm was facing

issue to

achieve

business

targets and

gain

competitive

advantages

(Atos

consulting,

2007).

4 5 20 By managing

resources and

increasing

involvement

of people,

firm can

overcome

resource

allocation

kind of

problem in a

proper way.

9

and financial

institutions,

chances of

negative

implications

of law and

regulations

can be

reduced.

5. Strategic

implementatio

n and resource

allocation

Standard

charted bank is

struggling

issues related

to allocation of

resources and

framed proper

strategies. In

the presence of

these factors,

firm was facing

issue to

achieve

business

targets and

gain

competitive

advantages

(Atos

consulting,

2007).

4 5 20 By managing

resources and

increasing

involvement

of people,

firm can

overcome

resource

allocation

kind of

problem in a

proper way.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.