Introduction to Management Accounting: Product Costing System Report

VerifiedAdded on 2019/09/22

|10

|1460

|324

Report

AI Summary

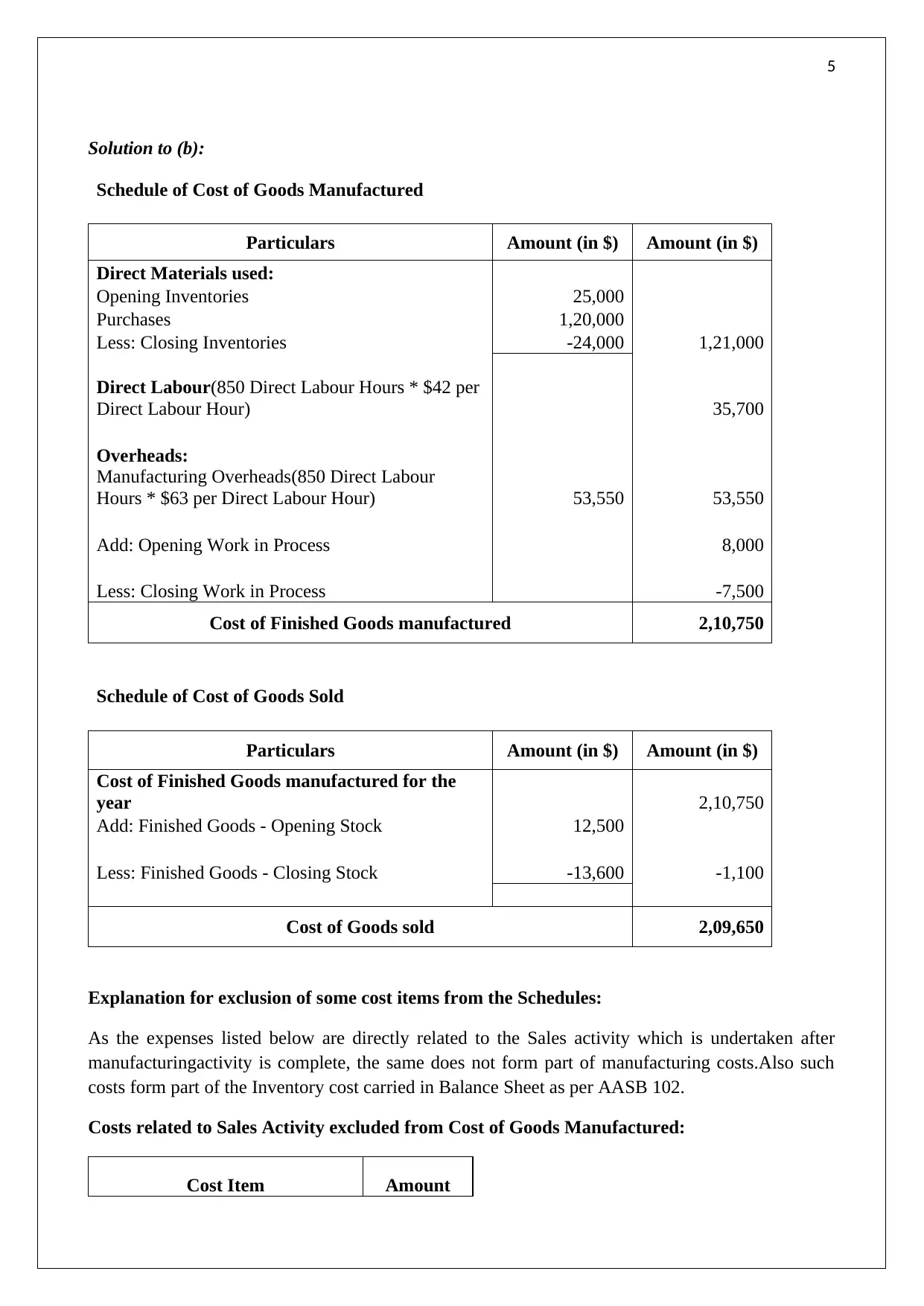

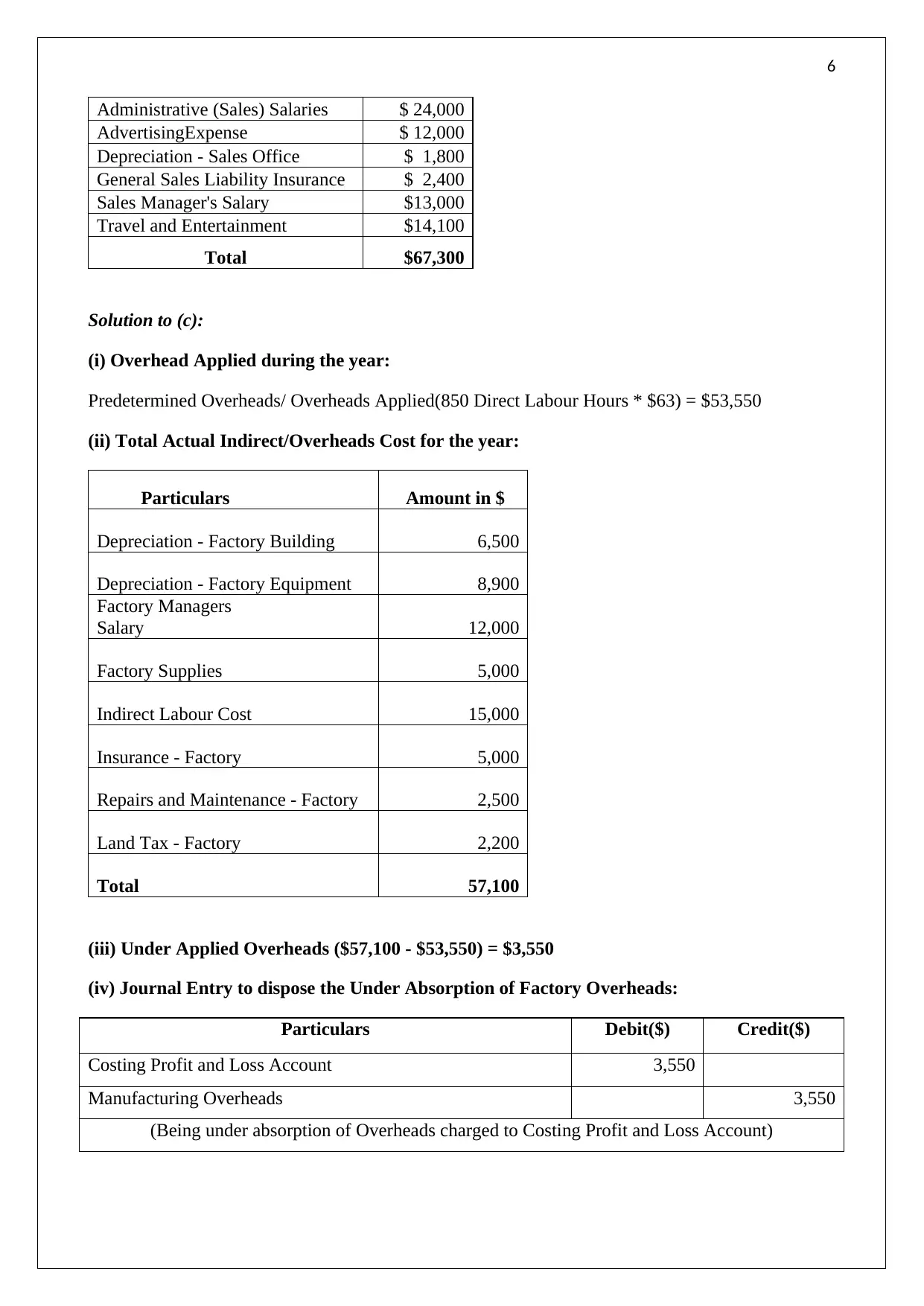

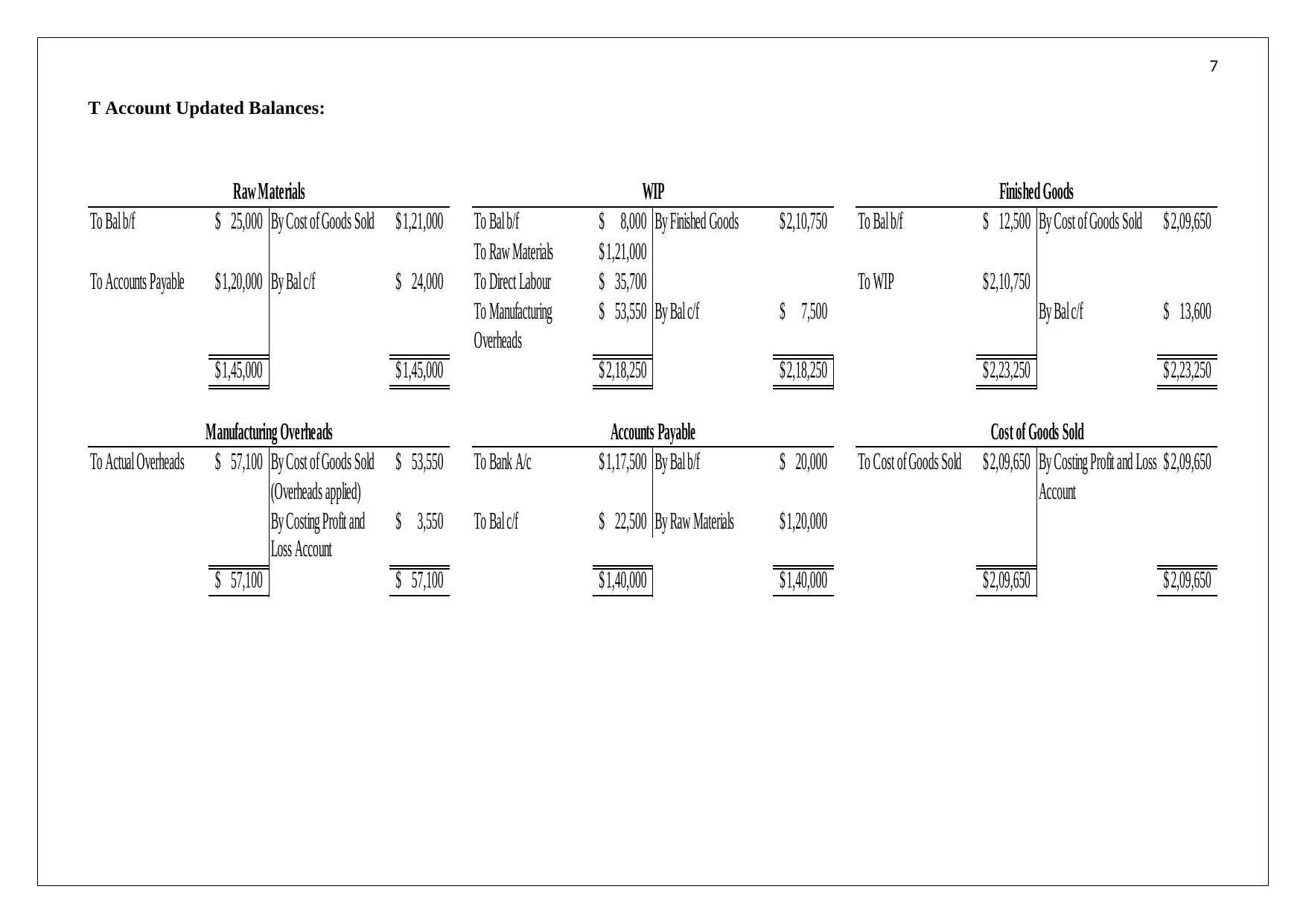

This report, prepared for Seafarer Kayaks, delves into the significance of product costing systems and standard costing within a manufacturing context. It begins by elucidating the fundamental purpose of product costing, emphasizing its role in allocating costs to specific products and its necessity for informed decision-making regarding pricing, expansion, and product mix. The report details the creation of a Schedule of Cost of Goods Manufactured and a Schedule of Cost of Goods Sold, along with an explanation of cost exclusions. It then analyzes overhead application, calculates under-applied overhead, and provides the relevant journal entry. Furthermore, it explains the benefits of a standard costing system as a control tool, particularly its value in identifying variances and facilitating corrective actions. The report highlights the importance of accurate budgeting in standard costing and concludes by referencing relevant accounting resources.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.