Financial Reporting Analysis of The Star Ent Group (ACCT20074)

VerifiedAdded on 2023/04/04

|29

|5339

|272

Report

AI Summary

This report provides an in-depth analysis of The Star Ent Group's corporate external reporting practices, focusing on its use of the Conceptual Framework for Financial Reporting. The report begins with a review of the framework's history and development, highlighting the concerns of the Australian accounting profession regarding its application, and discusses the potential benefits and limitations. The report then examines the financial statements prepared by The Star Ent Group, including the consolidated income statement, balance sheet, cash flow statement, statement of equity changes and segment information, and the application of recognition principles and measurement bases for revenue, assets, and liabilities. The report references the conceptual framework and its application within the company's financial reporting practices. The report also compares the company's approach to that of another company in South Africa. The report covers the financial statements prepared by the company and how the conceptual framework is used to achieve the objective of financial reporting.

Running head: THE STAR ENT GROUP 1

The Star Ent Group

Student’s Name

Affiliation

Date

The Star Ent Group

Student’s Name

Affiliation

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE STAR ENT GROUP 2

The Star Ent Group

Executive summary

This research is a report conducted on the Star Ent Group Company. The aspects of

discussion in this report are the Star Ent Group's corporate external reporting practices. This

research report is divided into two major parts including the company's use of the conceptual

framework and its sustainability report. The IASC Board approved the Conceptual Framework

for Financial Reporting. IASB adopted such a conceptual framework in the year 2001.The works

of IASB extend to various states across the world including Australia, the United States of

America, and the United Kingdom. Various concerns have been raised as far as the application

of the Conceptual Framework for Financial Reporting is concerned. This research report will

highlight different concerns as far as such a conceptual framework is concerned. More so, this

research report will provide detailed information concerning the potential benefits and

limitations of the application of the conceptual framework for financial accounting. Different

reports have been prepared by different companies as per this conceptual framework is

concerned. This report reveals that the Star Group Company has so far prepared ten statements in

accordance to such a conceptual framework.

Introduction

In financial reporting, a conceptual framework refers to an accounting theory laid by a

body that sets standards against which the objectivity of practical problems are tested. The

purpose and objectives of financial reporting, the accounting information's quality-features, as

well as the financial statements make up a conceptual framework. Therefore, the first part of this

The Star Ent Group

Executive summary

This research is a report conducted on the Star Ent Group Company. The aspects of

discussion in this report are the Star Ent Group's corporate external reporting practices. This

research report is divided into two major parts including the company's use of the conceptual

framework and its sustainability report. The IASC Board approved the Conceptual Framework

for Financial Reporting. IASB adopted such a conceptual framework in the year 2001.The works

of IASB extend to various states across the world including Australia, the United States of

America, and the United Kingdom. Various concerns have been raised as far as the application

of the Conceptual Framework for Financial Reporting is concerned. This research report will

highlight different concerns as far as such a conceptual framework is concerned. More so, this

research report will provide detailed information concerning the potential benefits and

limitations of the application of the conceptual framework for financial accounting. Different

reports have been prepared by different companies as per this conceptual framework is

concerned. This report reveals that the Star Group Company has so far prepared ten statements in

accordance to such a conceptual framework.

Introduction

In financial reporting, a conceptual framework refers to an accounting theory laid by a

body that sets standards against which the objectivity of practical problems are tested. The

purpose and objectives of financial reporting, the accounting information's quality-features, as

well as the financial statements make up a conceptual framework. Therefore, the first part of this

THE STAR ENT GROUP 3

paper focuses on the applicability of the IFRS' conceptual framework in a selected Australian

company known as The Star Ent Group. Part B of the paper conducts an evaluation of the

sustainability as well as the applicability of integrated financial reports in a selected company in

South Africa Italtile ltd in comparison with the Australian company.

Part A: Conceptual framework

(a) Review of the history and development of the Conceptual Framework for Financial

Reporting

The IASC Board first approved the Conceptual Framework for Financial Reporting deals with

the preparation and presentation of different financial statements and it was developed in the year

1989. In July 1989, the conceptual framework was first published for use (Silvia, 2018). The

International Accounting Standards Board adopted this conceptual framework in April 2001

(IAS PLUS, 2013).In addition to the above, the framework's main purpose was to help the IASB

in the development and revision of IFRSs, which depended on different highly consistent study

concepts (Australian Accounting Standards Board, 2015). Therefore, the purpose of the

framework was to assist different preparers in the development of highly consistent policies of

accounting for fields that the standard did not cover at all or where individuals can make

decisions concerning the policy of accounting hence helping in the understanding of IFRS

(Sottoriva, 2018).

Currently, the conceptual framework is currently being adopted by different accounting

standard agencies in order to improve the standards of accounting in their respective countries.

This framework helps IASB in different countries to develop and further revise the International

paper focuses on the applicability of the IFRS' conceptual framework in a selected Australian

company known as The Star Ent Group. Part B of the paper conducts an evaluation of the

sustainability as well as the applicability of integrated financial reports in a selected company in

South Africa Italtile ltd in comparison with the Australian company.

Part A: Conceptual framework

(a) Review of the history and development of the Conceptual Framework for Financial

Reporting

The IASC Board first approved the Conceptual Framework for Financial Reporting deals with

the preparation and presentation of different financial statements and it was developed in the year

1989. In July 1989, the conceptual framework was first published for use (Silvia, 2018). The

International Accounting Standards Board adopted this conceptual framework in April 2001

(IAS PLUS, 2013).In addition to the above, the framework's main purpose was to help the IASB

in the development and revision of IFRSs, which depended on different highly consistent study

concepts (Australian Accounting Standards Board, 2015). Therefore, the purpose of the

framework was to assist different preparers in the development of highly consistent policies of

accounting for fields that the standard did not cover at all or where individuals can make

decisions concerning the policy of accounting hence helping in the understanding of IFRS

(Sottoriva, 2018).

Currently, the conceptual framework is currently being adopted by different accounting

standard agencies in order to improve the standards of accounting in their respective countries.

This framework helps IASB in different countries to develop and further revise the International

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

THE STAR ENT GROUP 4

Financial Reporting Standards among these different countries (AASB, 2015). Under the IASB,

the conceptual framework is constantly being revised in different countries with an intention of

ensuring that it serves its purpose effectively. More so, it currently operates as a layout that

guides in the formation of different standards of accounting, which apply, to various accounting

companies and individuals in the accounting profession among different countries (AASB,

2015).

(b) Accounting profession’s concerns regarding the application of the (IASB/IFRS)

Conceptual Framework for Financial Reporting

There are various Australian Accounting professions’ concerns as far as the application

of the Conceptual Framework for Financial Reporting is concerned. The Conceptual framework

was adopted with an intention of ensuring that Australia's Accounting standards are based on

highly consistent concepts. The conceptual framework was therefore intended to help the IASB

come up with concepts that are more consistent as far as the different accounting principles are

concerned. More so, the Australian Accounting professional standards were unclear to different

people. The conceptual framework was therefore developed or applied with an intention of

helping different individuals to understand easily different accounting standards (AASB, 2015).

In the time when the IASB came into effect, there were various accounting profession's

concerns that were raised. During such years, various concerns were raised particularly in

Australia in relation to the application of the conceptual; framework. Wayne, who is a one of the

professors in the University of Sydney and in the field of Business and Economics, the

introduction of Australia's international standards of accounting was associated with numerous

outcomes in respect to the entire economy of Australian (Humayun and Asheq, 2018).

Financial Reporting Standards among these different countries (AASB, 2015). Under the IASB,

the conceptual framework is constantly being revised in different countries with an intention of

ensuring that it serves its purpose effectively. More so, it currently operates as a layout that

guides in the formation of different standards of accounting, which apply, to various accounting

companies and individuals in the accounting profession among different countries (AASB,

2015).

(b) Accounting profession’s concerns regarding the application of the (IASB/IFRS)

Conceptual Framework for Financial Reporting

There are various Australian Accounting professions’ concerns as far as the application

of the Conceptual Framework for Financial Reporting is concerned. The Conceptual framework

was adopted with an intention of ensuring that Australia's Accounting standards are based on

highly consistent concepts. The conceptual framework was therefore intended to help the IASB

come up with concepts that are more consistent as far as the different accounting principles are

concerned. More so, the Australian Accounting professional standards were unclear to different

people. The conceptual framework was therefore developed or applied with an intention of

helping different individuals to understand easily different accounting standards (AASB, 2015).

In the time when the IASB came into effect, there were various accounting profession's

concerns that were raised. During such years, various concerns were raised particularly in

Australia in relation to the application of the conceptual; framework. Wayne, who is a one of the

professors in the University of Sydney and in the field of Business and Economics, the

introduction of Australia's international standards of accounting was associated with numerous

outcomes in respect to the entire economy of Australian (Humayun and Asheq, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE STAR ENT GROUP 5

Australia’s process of developing standard in accounting was weakened by the State's policy of

using the International standards of accounting. Such an International system not only

emasculated Australia's process of setting accounting standards but further weakened the State's

capacity of setting its own standards including its role as far as the accounting excellence is

concerned. Different professionals discuss that different companies in Australia produced

financial reports of very poor quality at a time due to the use of IAS (Gordon et al, 2015). A

group of Australia's accounting professionals discussed that IAS led to financial stability as far

as Australia's corporate government is concerned. Today, many efforts that the corporate

government adopts have their main concentration on ensuring that best guidelines are adopted,

and that disclosure and independence among different accounting companies increase. More so,

such companies further need to be able to provide full disclosures of their failure to comply with

such standards in their respective annual financial reports (Aasb.gov.au, 2015). The corporate

government’s main objective is to ensure that there is a development of a culture of integrity and

trust between different stakeholders and other parties involved in the accounting processes such

as the company directors, the fund managers, and auditors. The currently adopted reforms as far

as the conceptual framework are concerned are putting their main emphasis on correcting the

symptoms observed in the accounting field instead of fully solving the different main causes of

the problems observes (Aasb.gov.au, 2015). Accounting standards are viewed as the backbone as

far as the concept of financial reporting is concerned. Until today, Australia’s financial reporting

system is still associated with various limitations and deficiencies. Australia's former accounting

system was associated with very poor financial and auditing practices, which affected both the

financial organizations and the different end users. The International Accounting standards,

which were earlier adopted in Australia largely, overshadowed the AASB policies irrespective of

Australia’s process of developing standard in accounting was weakened by the State's policy of

using the International standards of accounting. Such an International system not only

emasculated Australia's process of setting accounting standards but further weakened the State's

capacity of setting its own standards including its role as far as the accounting excellence is

concerned. Different professionals discuss that different companies in Australia produced

financial reports of very poor quality at a time due to the use of IAS (Gordon et al, 2015). A

group of Australia's accounting professionals discussed that IAS led to financial stability as far

as Australia's corporate government is concerned. Today, many efforts that the corporate

government adopts have their main concentration on ensuring that best guidelines are adopted,

and that disclosure and independence among different accounting companies increase. More so,

such companies further need to be able to provide full disclosures of their failure to comply with

such standards in their respective annual financial reports (Aasb.gov.au, 2015). The corporate

government’s main objective is to ensure that there is a development of a culture of integrity and

trust between different stakeholders and other parties involved in the accounting processes such

as the company directors, the fund managers, and auditors. The currently adopted reforms as far

as the conceptual framework are concerned are putting their main emphasis on correcting the

symptoms observed in the accounting field instead of fully solving the different main causes of

the problems observes (Aasb.gov.au, 2015). Accounting standards are viewed as the backbone as

far as the concept of financial reporting is concerned. Until today, Australia’s financial reporting

system is still associated with various limitations and deficiencies. Australia's former accounting

system was associated with very poor financial and auditing practices, which affected both the

financial organizations and the different end users. The International Accounting standards,

which were earlier adopted in Australia largely, overshadowed the AASB policies irrespective of

THE STAR ENT GROUP 6

the fact that the organization had its own areas of significant interest. Moreover, AASB was left

irrelevant more especially in relation to the private sector since AASB no longer issued the

accounting standards bur rather by the IASB and therefore its need was eliminated (Gordon et al,

2015).

(c) Potential (benefits and limitations) of the Conceptual Framework for Financial

Reporting

Benefits

The Conceptual Framework for Financial Reporting is associated with a number of benefits.

Among these includes the fact that it helps in the clarification of the different conceptual

underpinnings as far as different accounting standards are concerned (Aluchna et al., 2019). Such

a conceptual framework therefore allows different standards setters such as IASB to come up

with highly consistent standards of accounting (Armstrong, 2013). Besides, the Conceptual

Framework helps different auditors, preparers, and users of different financial statements

including different accountants to had better understand the required standards setting approach

and the function and nature of the type of financial information, which they report (Kieso and

Warfield, 2011; Bjørn et-al, 2016; Omanessay.com, 2018)

Limitations

The conceptual framework is associated with a number of limitations. Among these includes the

fact that it is strongly rigid and therefore such rigidity is further extended to the different

standardized practices of accounting after the framework implementation. Such a framework

therefore makes it extremely difficult for different new ideas to be introduced into the accounting

system since the framework has a lot of inflexibility (Barker& Teixeira, 2018). Moreover, some

the fact that the organization had its own areas of significant interest. Moreover, AASB was left

irrelevant more especially in relation to the private sector since AASB no longer issued the

accounting standards bur rather by the IASB and therefore its need was eliminated (Gordon et al,

2015).

(c) Potential (benefits and limitations) of the Conceptual Framework for Financial

Reporting

Benefits

The Conceptual Framework for Financial Reporting is associated with a number of benefits.

Among these includes the fact that it helps in the clarification of the different conceptual

underpinnings as far as different accounting standards are concerned (Aluchna et al., 2019). Such

a conceptual framework therefore allows different standards setters such as IASB to come up

with highly consistent standards of accounting (Armstrong, 2013). Besides, the Conceptual

Framework helps different auditors, preparers, and users of different financial statements

including different accountants to had better understand the required standards setting approach

and the function and nature of the type of financial information, which they report (Kieso and

Warfield, 2011; Bjørn et-al, 2016; Omanessay.com, 2018)

Limitations

The conceptual framework is associated with a number of limitations. Among these includes the

fact that it is strongly rigid and therefore such rigidity is further extended to the different

standardized practices of accounting after the framework implementation. Such a framework

therefore makes it extremely difficult for different new ideas to be introduced into the accounting

system since the framework has a lot of inflexibility (Barker& Teixeira, 2018). Moreover, some

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

THE STAR ENT GROUP 7

aspects embedded in the conceptual framework are unable to provide important insights as far as

the field of accounting is concerned (Armstrong, 2013). Such a rigid design makes the

incorporation of new ideas a very difficult process for different implementers. Another major

limitation as far as the conceptual framework is concerned is that is that different conflicts have

risen as far as the different standards of accounting, which were already in place and the

conceptual framework, are concerned (Sukhral, 2015). Such conflicts in most cases result from

the various differences that exist in the practices presented by the preceding standards of

accounting and conceptual framework for financial reporting. The main conflict therefore arises

from the fact that the standards that are already in existence have significant differences with the

conceptual framework's fundamental principles (Ngeno, 2018)

d: i) how many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

The Star Ent Group has so far prepared numerous reports as per the Conceptual Framework for

financial reporting is concerned. According to the data obtained. The Star group prepared four

financial statements in the year 2018 in accordance to this conceptual Framework for Financial

Accounting (Barker & Teixeira, 2018). The main components of such statements or reports

include the company's consolidated income statement, balance sheet, cash flow statements,

statement of equity changes and different notes in regards to the company's financial statements.

As far as the notes are concerned, the main components put into consideration include the

company's disclosures concerning income statements, disclosures concerning its balance sheet,

contingencies and commitments, risk management, group structure and many others (The Star

Entertainment Group, 2018).

aspects embedded in the conceptual framework are unable to provide important insights as far as

the field of accounting is concerned (Armstrong, 2013). Such a rigid design makes the

incorporation of new ideas a very difficult process for different implementers. Another major

limitation as far as the conceptual framework is concerned is that is that different conflicts have

risen as far as the different standards of accounting, which were already in place and the

conceptual framework, are concerned (Sukhral, 2015). Such conflicts in most cases result from

the various differences that exist in the practices presented by the preceding standards of

accounting and conceptual framework for financial reporting. The main conflict therefore arises

from the fact that the standards that are already in existence have significant differences with the

conceptual framework's fundamental principles (Ngeno, 2018)

d: i) how many statements/reports have been prepared as per the Conceptual Framework

and what are their major components

The Star Ent Group has so far prepared numerous reports as per the Conceptual Framework for

financial reporting is concerned. According to the data obtained. The Star group prepared four

financial statements in the year 2018 in accordance to this conceptual Framework for Financial

Accounting (Barker & Teixeira, 2018). The main components of such statements or reports

include the company's consolidated income statement, balance sheet, cash flow statements,

statement of equity changes and different notes in regards to the company's financial statements.

As far as the notes are concerned, the main components put into consideration include the

company's disclosures concerning income statements, disclosures concerning its balance sheet,

contingencies and commitments, risk management, group structure and many others (The Star

Entertainment Group, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE STAR ENT GROUP 8

The star group Company applies the conceptual framework for financial accounting in the

preparation of its financial report in many different ways. First, the company always

communicates the main objectives associated with their preparation of their financial reports at

the start of their respective reports (The Star Entertainment Group, 2018). Through

communication of the different objectives, the company in this way fulfills the main objective

communicated in the conceptual framework for financial accounting, which specifies that

financial reports have a general purpose of providing different financial information concerning

the reporting entity, which is of great use to potential and existence. Through communication of

their financial data to different parties after a specified period, the Star Group Company fulfills

the financial reporting objectives specified in the conceptual framework for all financial

documents (AASB, 2015).

Star Group's financial reports cover the company's assets, equity, liabilities, expenses and

income. More so, it further covers both the company's recognized and unrecognized assets, the

company's cash flows, the distributions and contributions of the company's equity holders and

the assumptions, methods and judgments employed including their respective changes. Through

providing all such information in their respective financial reports, the company is able to ensure

that all the useful information as far as the reporting entity is concerned is provided in their

report. Therefore, the company is able to apply chapter three of conceptual framework for

financial reporting which emphasizes the inclusion of all useful information as far as a specific

reporting entity is concerned (Sottoriva, 2018).

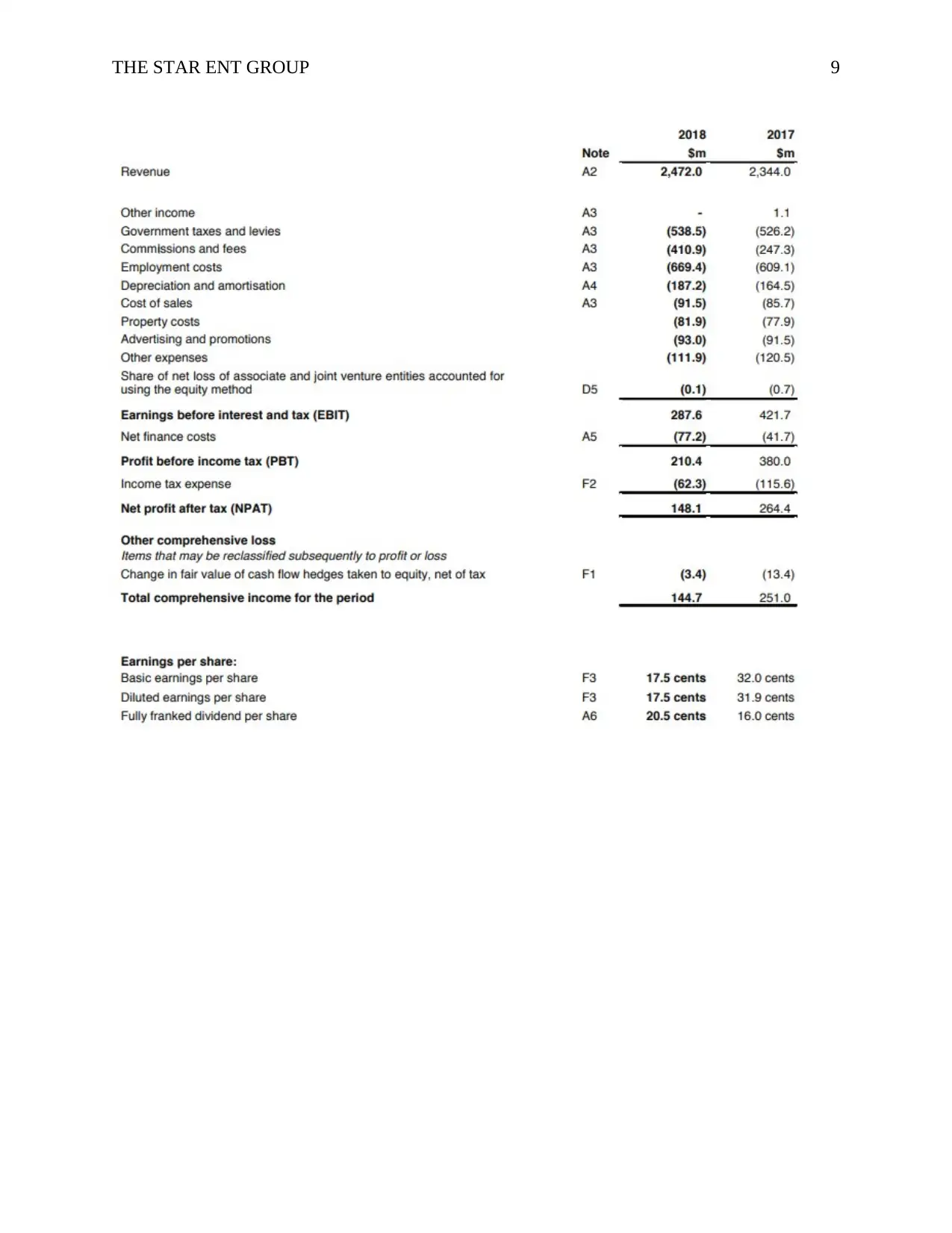

Star Group's consolidated income statement

The star group Company applies the conceptual framework for financial accounting in the

preparation of its financial report in many different ways. First, the company always

communicates the main objectives associated with their preparation of their financial reports at

the start of their respective reports (The Star Entertainment Group, 2018). Through

communication of the different objectives, the company in this way fulfills the main objective

communicated in the conceptual framework for financial accounting, which specifies that

financial reports have a general purpose of providing different financial information concerning

the reporting entity, which is of great use to potential and existence. Through communication of

their financial data to different parties after a specified period, the Star Group Company fulfills

the financial reporting objectives specified in the conceptual framework for all financial

documents (AASB, 2015).

Star Group's financial reports cover the company's assets, equity, liabilities, expenses and

income. More so, it further covers both the company's recognized and unrecognized assets, the

company's cash flows, the distributions and contributions of the company's equity holders and

the assumptions, methods and judgments employed including their respective changes. Through

providing all such information in their respective financial reports, the company is able to ensure

that all the useful information as far as the reporting entity is concerned is provided in their

report. Therefore, the company is able to apply chapter three of conceptual framework for

financial reporting which emphasizes the inclusion of all useful information as far as a specific

reporting entity is concerned (Sottoriva, 2018).

Star Group's consolidated income statement

THE STAR ENT GROUP 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

THE STAR ENT GROUP 10

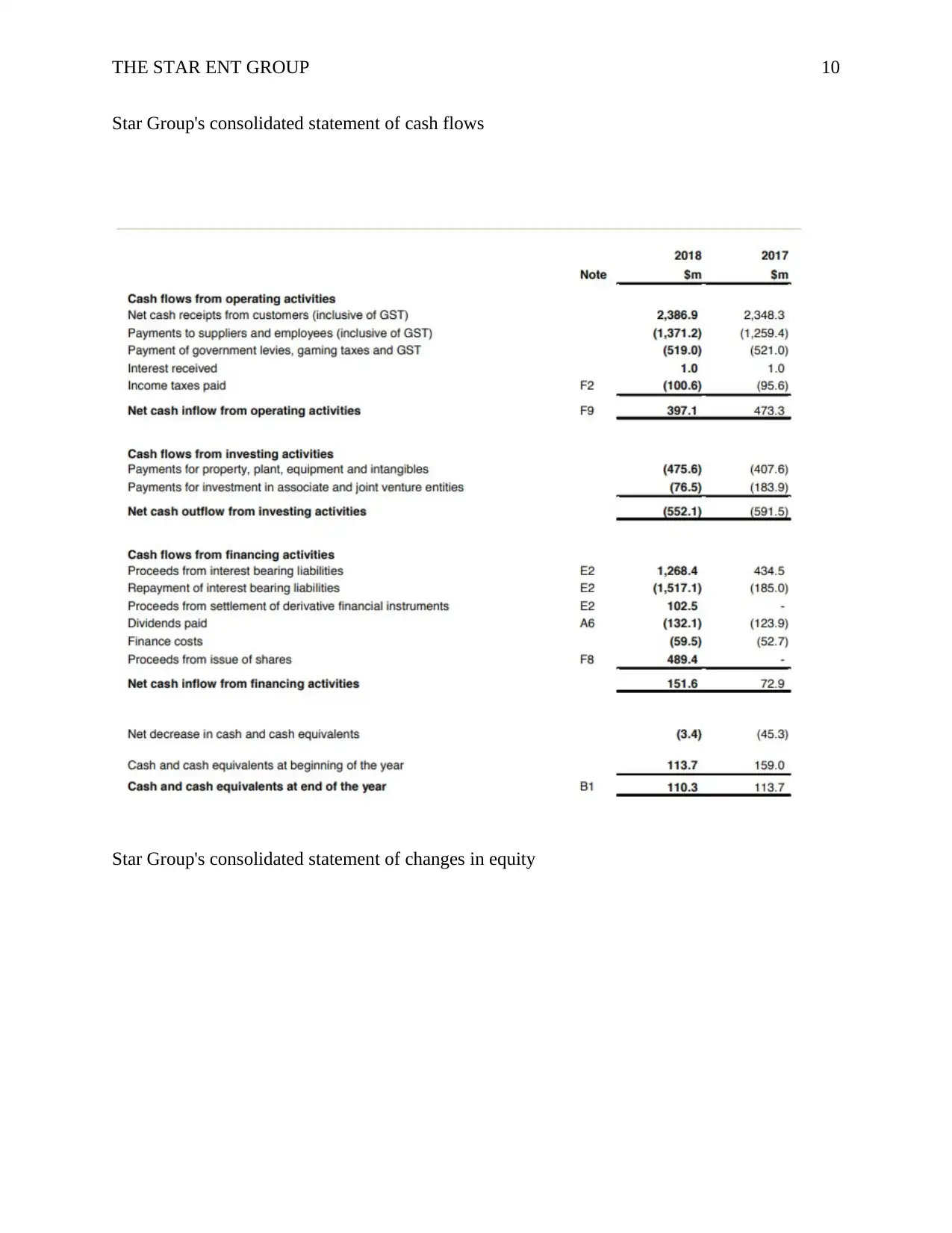

Star Group's consolidated statement of cash flows

Star Group's consolidated statement of changes in equity

Star Group's consolidated statement of cash flows

Star Group's consolidated statement of changes in equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

THE STAR ENT GROUP 11

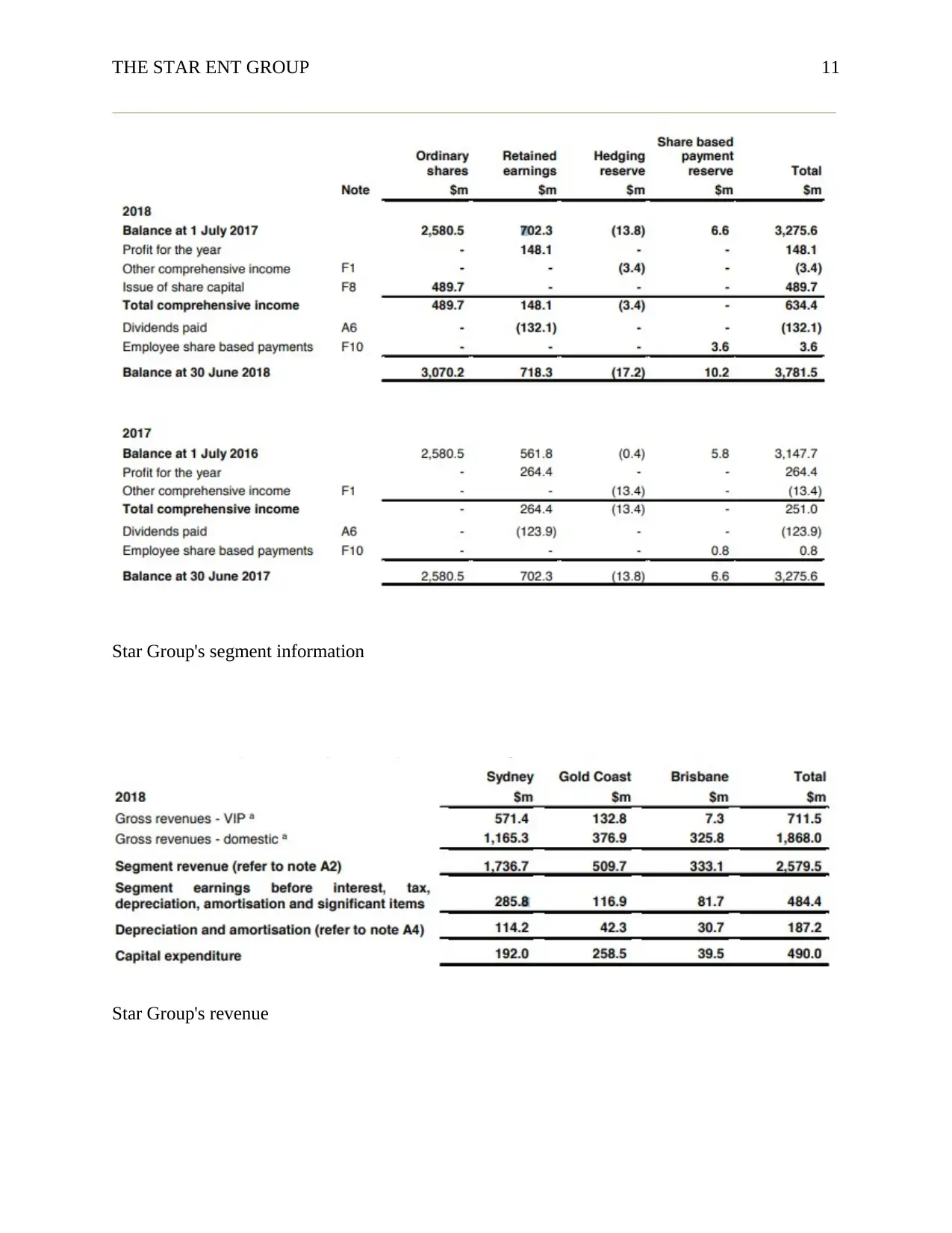

Star Group's segment information

Star Group's revenue

Star Group's segment information

Star Group's revenue

THE STAR ENT GROUP 12

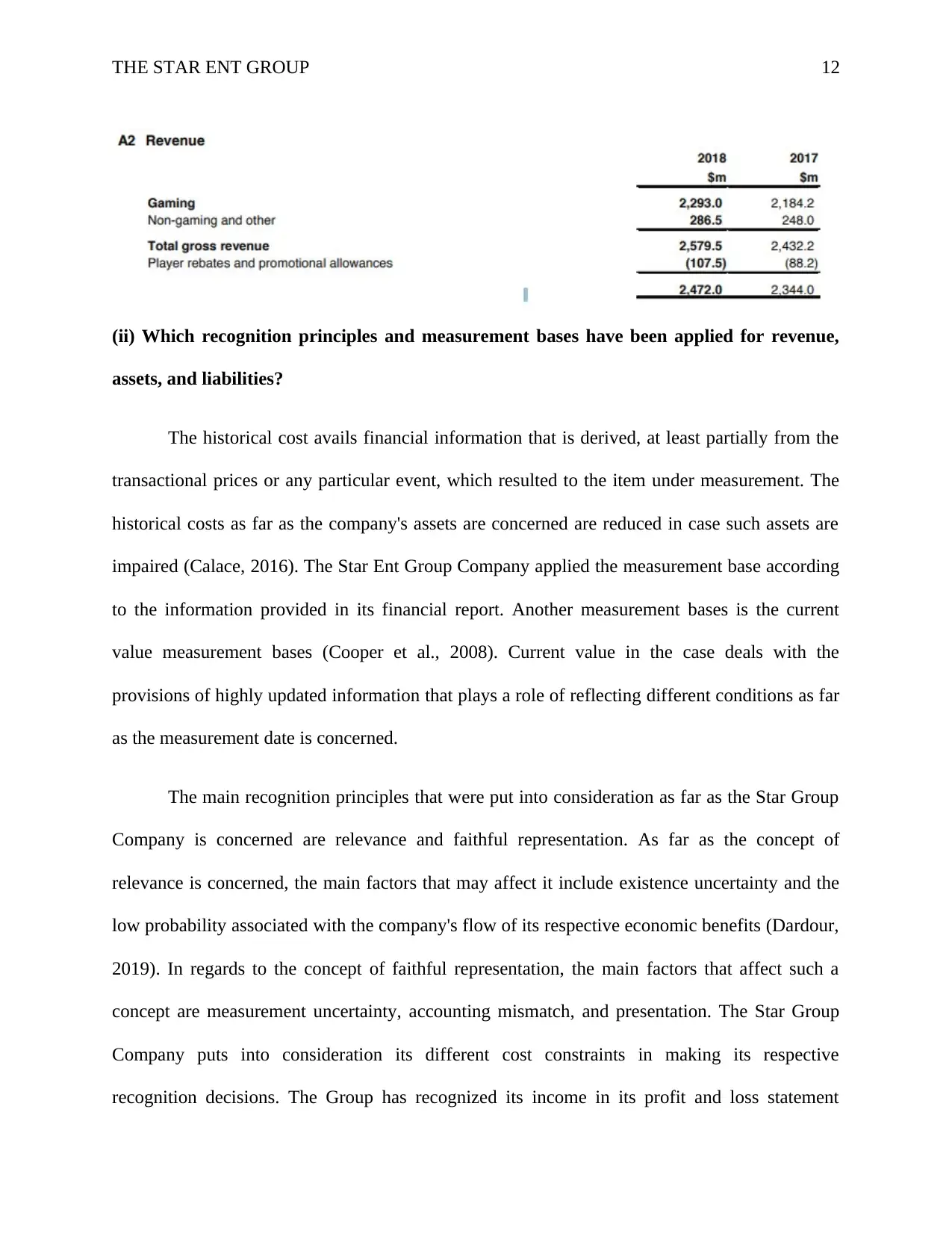

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets, and liabilities?

The historical cost avails financial information that is derived, at least partially from the

transactional prices or any particular event, which resulted to the item under measurement. The

historical costs as far as the company's assets are concerned are reduced in case such assets are

impaired (Calace, 2016). The Star Ent Group Company applied the measurement base according

to the information provided in its financial report. Another measurement bases is the current

value measurement bases (Cooper et al., 2008). Current value in the case deals with the

provisions of highly updated information that plays a role of reflecting different conditions as far

as the measurement date is concerned.

The main recognition principles that were put into consideration as far as the Star Group

Company is concerned are relevance and faithful representation. As far as the concept of

relevance is concerned, the main factors that may affect it include existence uncertainty and the

low probability associated with the company's flow of its respective economic benefits (Dardour,

2019). In regards to the concept of faithful representation, the main factors that affect such a

concept are measurement uncertainty, accounting mismatch, and presentation. The Star Group

Company puts into consideration its different cost constraints in making its respective

recognition decisions. The Group has recognized its income in its profit and loss statement

(ii) Which recognition principles and measurement bases have been applied for revenue,

assets, and liabilities?

The historical cost avails financial information that is derived, at least partially from the

transactional prices or any particular event, which resulted to the item under measurement. The

historical costs as far as the company's assets are concerned are reduced in case such assets are

impaired (Calace, 2016). The Star Ent Group Company applied the measurement base according

to the information provided in its financial report. Another measurement bases is the current

value measurement bases (Cooper et al., 2008). Current value in the case deals with the

provisions of highly updated information that plays a role of reflecting different conditions as far

as the measurement date is concerned.

The main recognition principles that were put into consideration as far as the Star Group

Company is concerned are relevance and faithful representation. As far as the concept of

relevance is concerned, the main factors that may affect it include existence uncertainty and the

low probability associated with the company's flow of its respective economic benefits (Dardour,

2019). In regards to the concept of faithful representation, the main factors that affect such a

concept are measurement uncertainty, accounting mismatch, and presentation. The Star Group

Company puts into consideration its different cost constraints in making its respective

recognition decisions. The Group has recognized its income in its profit and loss statement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.