Analyzing Starbucks' Financial Health: A Case Study Using Ratios

VerifiedAdded on 2023/06/11

|4

|541

|286

Case Study

AI Summary

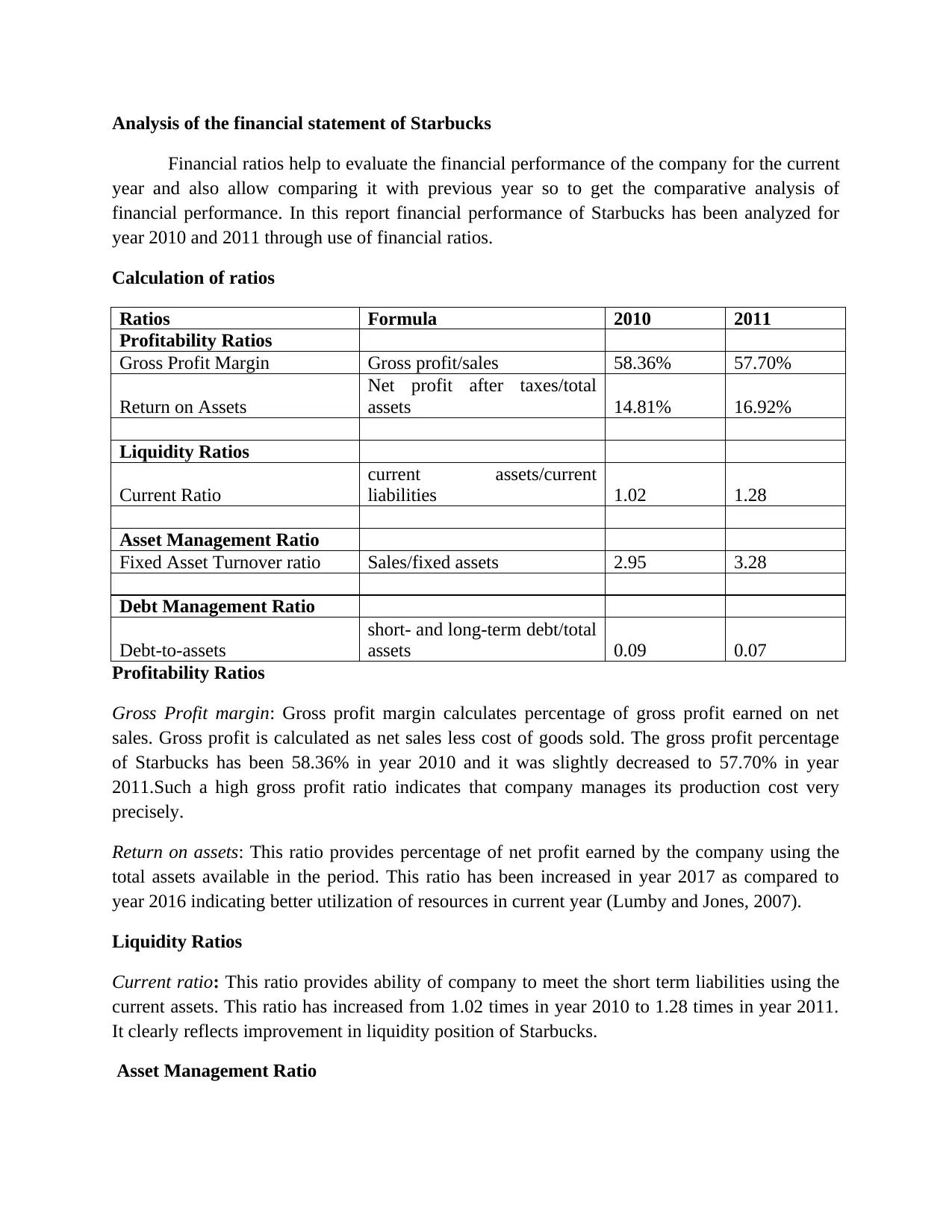

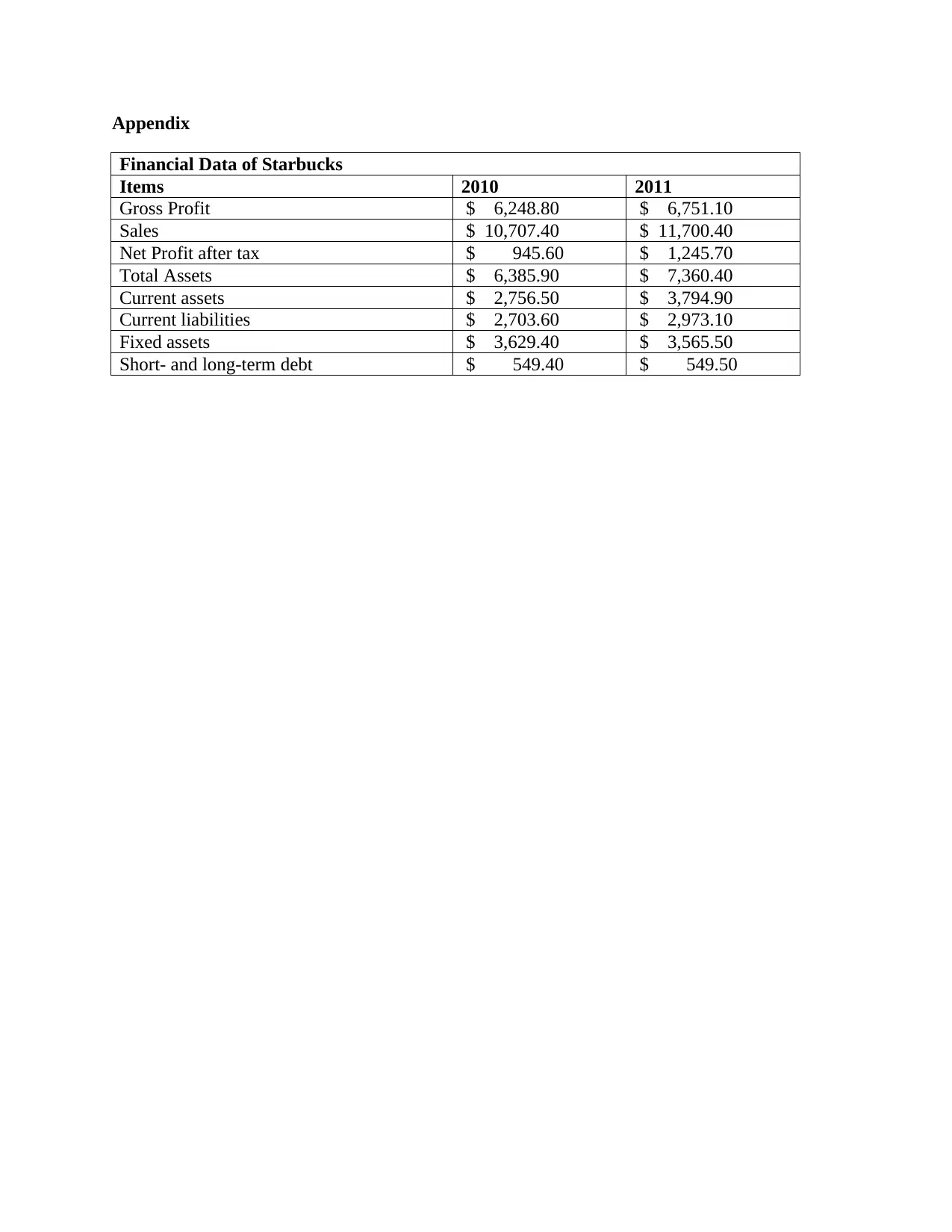

This case study provides a financial analysis of Starbucks, focusing on key financial ratios for the years 2010 and 2011. It examines profitability ratios such as gross profit margin and return on assets, liquidity ratios like the current ratio, asset management ratios including fixed asset turnover, and debt management ratios such as debt-to-assets. The analysis indicates that while Starbucks maintained a high gross profit margin, its return on assets improved from 2010 to 2011. The current ratio also showed improvement in liquidity. Furthermore, the efficiency of utilizing fixed assets to generate revenue increased, and there was a positive shift in the capital structure with a decrease in the debt-to-assets ratio, suggesting a stronger financial position in 2011 compared to 2010.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.