Accounting Financial Analysis Report on Starbucks Corporation

VerifiedAdded on 2023/06/11

|5

|608

|223

Report

AI Summary

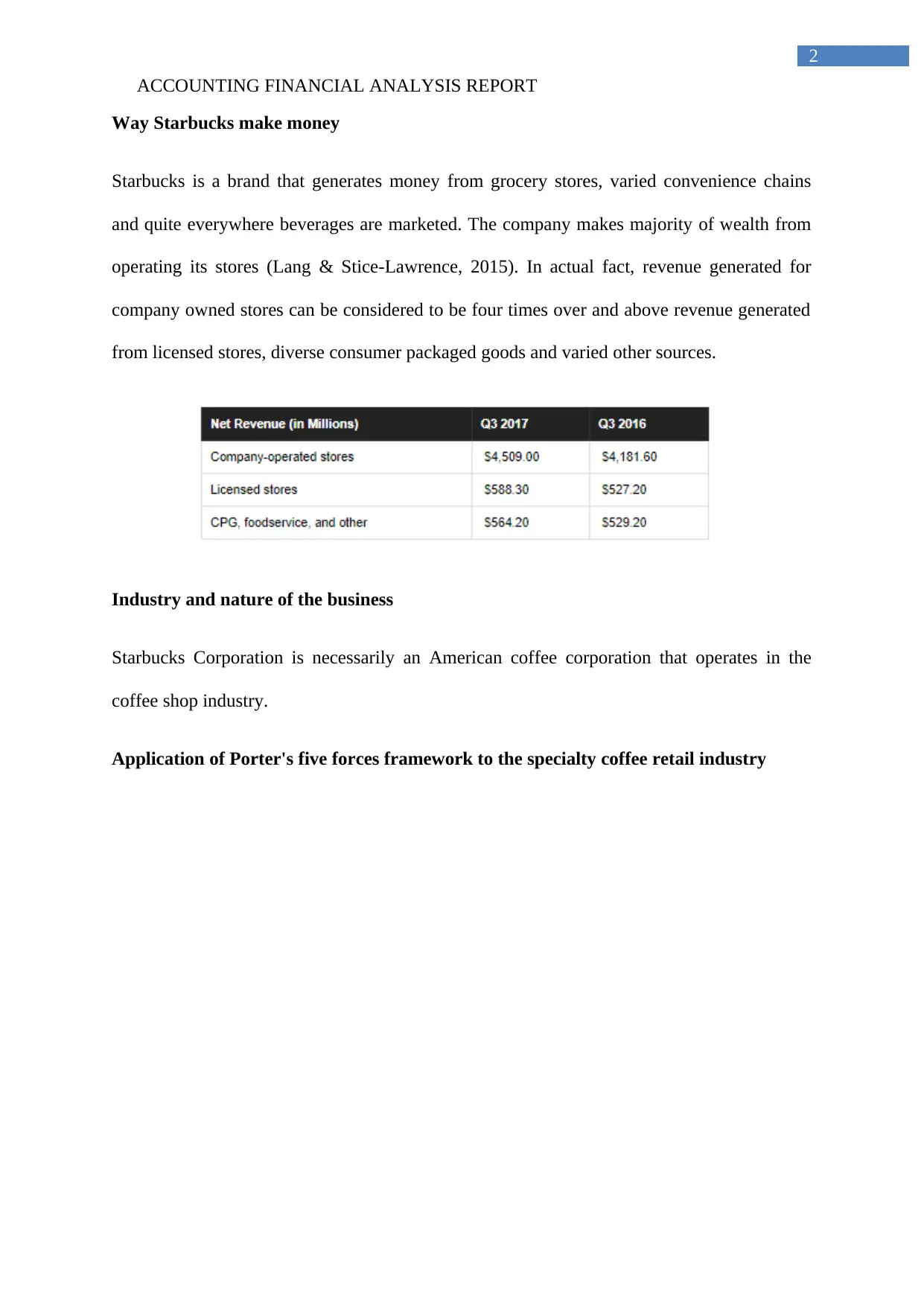

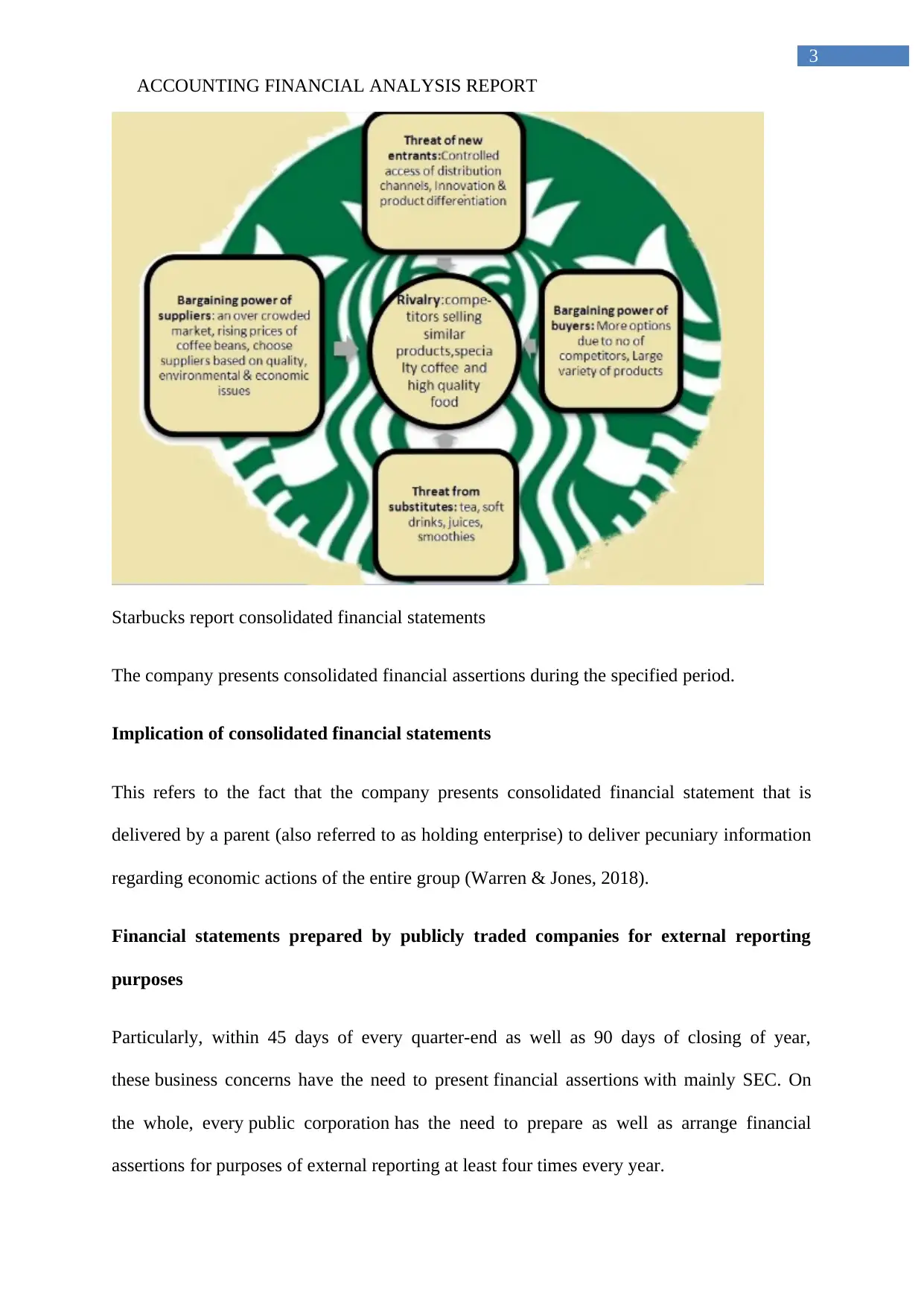

This report provides a financial analysis of Starbucks Corporation, examining the company's revenue generation from its stores and other sources. It discusses the industry and nature of Starbucks' business, applying Porter's five forces framework to the specialty coffee retail industry. The report highlights the presentation of consolidated financial statements and their implications, emphasizing the importance of external reporting to the SEC. It identifies potential users of Starbucks' financial statements, such as financiers and stakeholders, and their interests in financial performance and corporate governance. The report also mentions Deloitte & Touche LLP as the auditing company and explains the reason for the delay in the opinion letter after the fiscal year-end, attributing it to the extensive time required for assessments and evaluations to ensure the accuracy and reliability of financial reporting.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.