Case Study: Starbucks' Response to New Lease Accounting Standards

VerifiedAdded on 2022/02/07

|13

|2725

|45

Case Study

AI Summary

This case study examines Starbucks' concerns regarding new lease accounting standards proposed by IASB and FASB, focusing on the impact on their financial statements. Starbucks' worries center around lease terms, expense recognition patterns, and contingent rentals. The report outlines the journal entries required if Starbucks adopts the new standards, explores alternative approaches, and weighs the pros and cons of each. Alternatives discussed include maintaining the current practices, accepting the proposed changes, and adopting Starbucks' own suggestions. Ultimately, the report provides a recommendation based on a thorough analysis of these alternatives, considering the financial implications and operational challenges for Starbucks.

Business Case Study – STARBUCKS: VENTI

LEASES

Group #5

Prepared for:

Professor Ramesh Saxena

ACCT 4000 RLA

Humber college

Prepared by:

Mohit Gadwal(N01332620)

Urvil Pravinbhai Patel (N01332646)

Aliza Tharani(N01349821)

Matthew Johnson(N01268714)

Denvis Tabod (N01250378)

LEASES

Group #5

Prepared for:

Professor Ramesh Saxena

ACCT 4000 RLA

Humber college

Prepared by:

Mohit Gadwal(N01332620)

Urvil Pravinbhai Patel (N01332646)

Aliza Tharani(N01349821)

Matthew Johnson(N01268714)

Denvis Tabod (N01250378)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

TOC \h \u \z HYPERLINK \l "_l2z9bukj5tw5" \h EXECUTIVE SUMMARY PAGEREF

_l2z9bukj5tw5 \h 3

INTRODUCTION: 4

PROBLEM STATEMENT 4

ANALYSIS OF ISSUES 4

ALTERNATIVES 9

ALTERNATIVES COMPARED 10

RECOMMENDATION 11

APPENDIX 12

TOC \h \u \z HYPERLINK \l "_l2z9bukj5tw5" \h EXECUTIVE SUMMARY PAGEREF

_l2z9bukj5tw5 \h 3

INTRODUCTION: 4

PROBLEM STATEMENT 4

ANALYSIS OF ISSUES 4

ALTERNATIVES 9

ALTERNATIVES COMPARED 10

RECOMMENDATION 11

APPENDIX 12

EXECUTIVE SUMMARY

The case tells us about the new accounting standards related to leases proposed by IASB and

FASB together and how these new standards will affect Starbucks. Starbucks has also shown

their concern related to the new accounting standards and how these standards can affect their

financial statements. Their major concerns were related to Lease term, Expense recognition

pattern, Contingent rentals. This report provides what journal entries are required if Starbucks

decides to accept the new standards proposed by IASB and FASB. This report also provides

different alternatives and shows the pros and cons of each alternative. After analyzing all the

pros and cons of each alternative we have provided the recommendation.

The case tells us about the new accounting standards related to leases proposed by IASB and

FASB together and how these new standards will affect Starbucks. Starbucks has also shown

their concern related to the new accounting standards and how these standards can affect their

financial statements. Their major concerns were related to Lease term, Expense recognition

pattern, Contingent rentals. This report provides what journal entries are required if Starbucks

decides to accept the new standards proposed by IASB and FASB. This report also provides

different alternatives and shows the pros and cons of each alternative. After analyzing all the

pros and cons of each alternative we have provided the recommendation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION:

The first Starbucks store was opened in Seattle on March 30, 1971 by three partners named Jerry

Baldwin, Gordon Bowker and Zev Siegl. The main product of Starbucks was selling fresh

roasted coffee beans. In 1982, an entrepreneur called Howard Schultz was hired as the director of

retail operation and marketing. After a trip to Italy in 1983, Howard Schultz, urged the Starbucks

owners to adopt their Italian coffee taste, however, they rejected the offer. He thus started his

own business called II Giornale which was his vision for Starbucks. Later in 1987, Starbucks

was then sold to II Giornale which was owned by Schultz which he later named as Starbucks.

Starbucks had 11,000 locations in the USA and 1000 locations in canada. Starbucks now has

32,646 stores worldwide.

PROBLEM STATEMENT

The Vice president and controller of starbuck have concerns about the new accounting standards

proposed by IASB and FASB in regards to lease accounting and how it will affect the companies

financial statements.

ANALYSIS OF ISSUES

Type of Business: The case focuses on a coffee retailing company (Starbucks) which belongs in

the food production industry. Starbucks is noted for their sale of high quality fresh roasted whole

coffee beans in locations where friends can meet for conversations away from their homes and

place of work.

Environment: Starbucks operates in leased identical locations which serves as a third place from

home and work where friends could meet for conservations and enjoy their high quality

products, great service and relax. Their identical environments are community friendly.

Originally, Starbucks operated only as Italian coffee bars in Italy, until the coffee experience in

those bars captured Schultz who adopted the idea in America and then it spread all over the

The first Starbucks store was opened in Seattle on March 30, 1971 by three partners named Jerry

Baldwin, Gordon Bowker and Zev Siegl. The main product of Starbucks was selling fresh

roasted coffee beans. In 1982, an entrepreneur called Howard Schultz was hired as the director of

retail operation and marketing. After a trip to Italy in 1983, Howard Schultz, urged the Starbucks

owners to adopt their Italian coffee taste, however, they rejected the offer. He thus started his

own business called II Giornale which was his vision for Starbucks. Later in 1987, Starbucks

was then sold to II Giornale which was owned by Schultz which he later named as Starbucks.

Starbucks had 11,000 locations in the USA and 1000 locations in canada. Starbucks now has

32,646 stores worldwide.

PROBLEM STATEMENT

The Vice president and controller of starbuck have concerns about the new accounting standards

proposed by IASB and FASB in regards to lease accounting and how it will affect the companies

financial statements.

ANALYSIS OF ISSUES

Type of Business: The case focuses on a coffee retailing company (Starbucks) which belongs in

the food production industry. Starbucks is noted for their sale of high quality fresh roasted whole

coffee beans in locations where friends can meet for conversations away from their homes and

place of work.

Environment: Starbucks operates in leased identical locations which serves as a third place from

home and work where friends could meet for conservations and enjoy their high quality

products, great service and relax. Their identical environments are community friendly.

Originally, Starbucks operated only as Italian coffee bars in Italy, until the coffee experience in

those bars captured Schultz who adopted the idea in America and then it spread all over the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

world.

Stakeholders: Starbucks company has many stakeholders who are interested in the company and

can either affect the business or can be affected by the business. Some of starbuck’s stakeholders

are;

● Customers - they are the key stakeholders in the starbucks company, this is because the

entire business only exists because of them. Starbucks depends on the loyalty of the

customers to survive.

● Investors - they are also very beneficial to the company through their investments, even

though they are liable to lose money through their investments.

● Employees are also stakeholders, as they contribute to the company’s growth by offering

their exceptional services to customers.

● Suppliers - they are important stakeholders because they provide raw material and

supplies for the business to run, for example: Coffee farmers.

According to the case, Starbucks needs to adapt to the new changes in the lease accounting

standards. Before the IASB and FASB jointly issued new accounting standards for all off-

balance sheet leases over 1 year to be reported on a company’s balance sheet as a right to use

assets with a corresponding liability, Starbucks was able to reduce her expenditure and debt by

using off-balance sheet leasing.

So, the new accounting standards are making things difficult for Starbucks, since they have to

stop their off-balance sheet lease practice.

Starbucks is a global retailer with approximately 9,000 company-operated retail locations under

operating leases in the U.S, and across the borders. Accounting standards related to Leases are

important for Starbucks because the stores are the most important asset of the company, and they

lease the stores. Changes in Accounting standards related to the leases would greatly affect the

company. Before August 2010, there were Various classification for leases from both the

International Accounting Standards Board (IASB) and the Financial Accounting Standard Board

(FASB). Both the boards have different approaches, but they established similar categories and

treatment of capital and operating leases.

Stakeholders: Starbucks company has many stakeholders who are interested in the company and

can either affect the business or can be affected by the business. Some of starbuck’s stakeholders

are;

● Customers - they are the key stakeholders in the starbucks company, this is because the

entire business only exists because of them. Starbucks depends on the loyalty of the

customers to survive.

● Investors - they are also very beneficial to the company through their investments, even

though they are liable to lose money through their investments.

● Employees are also stakeholders, as they contribute to the company’s growth by offering

their exceptional services to customers.

● Suppliers - they are important stakeholders because they provide raw material and

supplies for the business to run, for example: Coffee farmers.

According to the case, Starbucks needs to adapt to the new changes in the lease accounting

standards. Before the IASB and FASB jointly issued new accounting standards for all off-

balance sheet leases over 1 year to be reported on a company’s balance sheet as a right to use

assets with a corresponding liability, Starbucks was able to reduce her expenditure and debt by

using off-balance sheet leasing.

So, the new accounting standards are making things difficult for Starbucks, since they have to

stop their off-balance sheet lease practice.

Starbucks is a global retailer with approximately 9,000 company-operated retail locations under

operating leases in the U.S, and across the borders. Accounting standards related to Leases are

important for Starbucks because the stores are the most important asset of the company, and they

lease the stores. Changes in Accounting standards related to the leases would greatly affect the

company. Before August 2010, there were Various classification for leases from both the

International Accounting Standards Board (IASB) and the Financial Accounting Standard Board

(FASB). Both the boards have different approaches, but they established similar categories and

treatment of capital and operating leases.

Operating Leases were shown as an operating expense in the income statement in the period in

which the lease payments were made. The operating leases don't affect the balance sheet of the

company and disclosures were made only in the notes to the financial statements. Capital Leases

were treated differently from the operating Leases. Capital leases were classified as both as an

asset and as a liability on the balance sheet. Sir David Tweedie (Chairman of the IASB) also

commented that the lease accounting standards fell significantly short.

In August 2010, IASB and FASB jointly proposed to standardize the recognition of assets and

liabilities under leases. The proposal was intended to help the financial users of financial

statements to avoid uncertainties that were faced in the existing standards. The new leasing

standards define a lease as a contract that gives the lessee the right to control the use of an asset

for a period in exchange for consideration (lease payments). This will result in that all off-

balance sheet leases must be reported on a company's balance sheet as an asset with a

corresponding liability. IASB and FASB also proposed that assets and liabilities recognized by

lessees and lessors would be measured on basis that-

A. Assumes the longest conceivable rent term that is almost certain to happen, considering

the effects of any other options to extend or end the lease.

B. Uses a normal result procedure to mirror the rent installments, including unexpected

rentals and anticipated installments under term option penalties and residual value

guarantees, indicated by the lease.

C. Is updated when changes in realities or conditions show that there would be a critical

change in those assets or liabilities since the past reporting period.

Starbuck would have been greatly affected by applying these new standards. so they discussed

their concerns about the new standard and they were not following the new standards from IASB

and FASB, The summary of the concerns are as follows-

The lease term

IASB and FASB proposed that the lease term should be determined as the longest term that is

more likely than not to occur, but Starbuck didn't agree with that and argued that the lessee does

which the lease payments were made. The operating leases don't affect the balance sheet of the

company and disclosures were made only in the notes to the financial statements. Capital Leases

were treated differently from the operating Leases. Capital leases were classified as both as an

asset and as a liability on the balance sheet. Sir David Tweedie (Chairman of the IASB) also

commented that the lease accounting standards fell significantly short.

In August 2010, IASB and FASB jointly proposed to standardize the recognition of assets and

liabilities under leases. The proposal was intended to help the financial users of financial

statements to avoid uncertainties that were faced in the existing standards. The new leasing

standards define a lease as a contract that gives the lessee the right to control the use of an asset

for a period in exchange for consideration (lease payments). This will result in that all off-

balance sheet leases must be reported on a company's balance sheet as an asset with a

corresponding liability. IASB and FASB also proposed that assets and liabilities recognized by

lessees and lessors would be measured on basis that-

A. Assumes the longest conceivable rent term that is almost certain to happen, considering

the effects of any other options to extend or end the lease.

B. Uses a normal result procedure to mirror the rent installments, including unexpected

rentals and anticipated installments under term option penalties and residual value

guarantees, indicated by the lease.

C. Is updated when changes in realities or conditions show that there would be a critical

change in those assets or liabilities since the past reporting period.

Starbuck would have been greatly affected by applying these new standards. so they discussed

their concerns about the new standard and they were not following the new standards from IASB

and FASB, The summary of the concerns are as follows-

The lease term

IASB and FASB proposed that the lease term should be determined as the longest term that is

more likely than not to occur, but Starbuck didn't agree with that and argued that the lessee does

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

not have an unconditional obligation to pay rentals in optional renewal periods until the lessee

has exercised the renewal option. Including not -yet -exercised option period for calculating lease

liability would create inconsistency and would lead to inflated balance. Donna Brooks (Vice

president and controller of Starbucks) also added that it would reduce the reliability and

comparability of financial statements.

Expense Recognition Pattern

IASB and FASB proposed the amortization cost method for the leases. Starbucks argued that the

linked approach would be a better approach for the expense recognition purpose. The company

believed it would accommodate the move away from off-balance-sheet financing and will also

preserve current straight-line rent expense recognition.

Contingent Rentals

Both the boards proposed that Contingent rent should be included in the determination of the

right-of-use asset and related liability. Starbucks stated that the Contingent rent should not be

included unless there is a primary obligation under the lease. Starbucks said the contingent rent

should be considered only when future events occur and trigger liability.

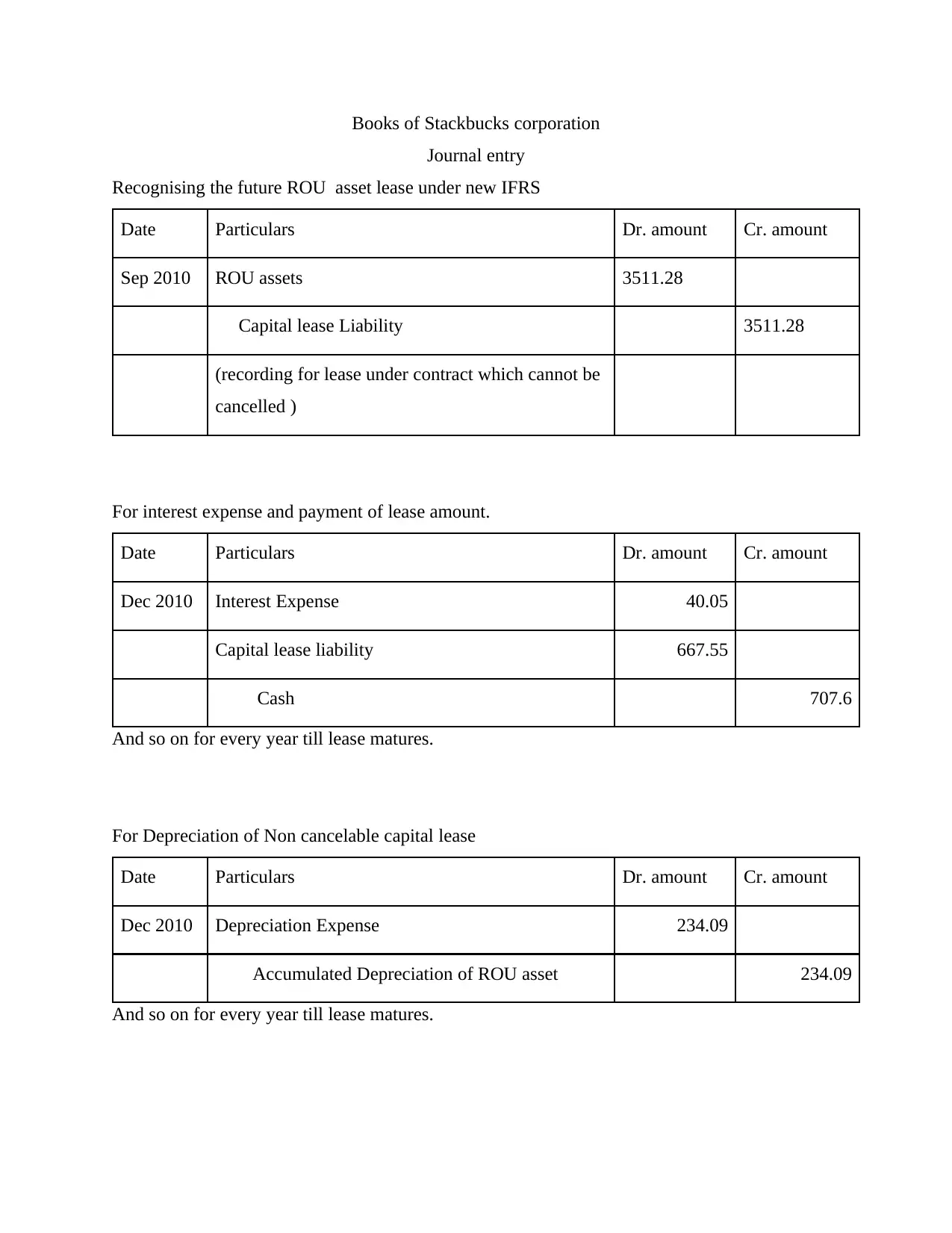

If Starbucks accepts the new standards proposed by IASB and FASB these entries are

required to be done.

If Starbucks accepts the proposal it means that the company needs to classify their lease both as

an asset and as a liability on the balance sheet. The company needs to do journal entry to record

lease as an asset and a corresponding entry for lease liability. We also need to do an entry for

depreciation each year.

To reach the present value of the lease we assumed that the cost of the capital is 6%.

(calculations are shown in the appendix)

has exercised the renewal option. Including not -yet -exercised option period for calculating lease

liability would create inconsistency and would lead to inflated balance. Donna Brooks (Vice

president and controller of Starbucks) also added that it would reduce the reliability and

comparability of financial statements.

Expense Recognition Pattern

IASB and FASB proposed the amortization cost method for the leases. Starbucks argued that the

linked approach would be a better approach for the expense recognition purpose. The company

believed it would accommodate the move away from off-balance-sheet financing and will also

preserve current straight-line rent expense recognition.

Contingent Rentals

Both the boards proposed that Contingent rent should be included in the determination of the

right-of-use asset and related liability. Starbucks stated that the Contingent rent should not be

included unless there is a primary obligation under the lease. Starbucks said the contingent rent

should be considered only when future events occur and trigger liability.

If Starbucks accepts the new standards proposed by IASB and FASB these entries are

required to be done.

If Starbucks accepts the proposal it means that the company needs to classify their lease both as

an asset and as a liability on the balance sheet. The company needs to do journal entry to record

lease as an asset and a corresponding entry for lease liability. We also need to do an entry for

depreciation each year.

To reach the present value of the lease we assumed that the cost of the capital is 6%.

(calculations are shown in the appendix)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Books of Stackbucks corporation

Journal entry

Recognising the future ROU asset lease under new IFRS

Date Particulars Dr. amount Cr. amount

Sep 2010 ROU assets 3511.28

Capital lease Liability 3511.28

(recording for lease under contract which cannot be

cancelled )

For interest expense and payment of lease amount.

Date Particulars Dr. amount Cr. amount

Dec 2010 Interest Expense 40.05

Capital lease liability 667.55

Cash 707.6

And so on for every year till lease matures.

For Depreciation of Non cancelable capital lease

Date Particulars Dr. amount Cr. amount

Dec 2010 Depreciation Expense 234.09

Accumulated Depreciation of ROU asset 234.09

And so on for every year till lease matures.

Journal entry

Recognising the future ROU asset lease under new IFRS

Date Particulars Dr. amount Cr. amount

Sep 2010 ROU assets 3511.28

Capital lease Liability 3511.28

(recording for lease under contract which cannot be

cancelled )

For interest expense and payment of lease amount.

Date Particulars Dr. amount Cr. amount

Dec 2010 Interest Expense 40.05

Capital lease liability 667.55

Cash 707.6

And so on for every year till lease matures.

For Depreciation of Non cancelable capital lease

Date Particulars Dr. amount Cr. amount

Dec 2010 Depreciation Expense 234.09

Accumulated Depreciation of ROU asset 234.09

And so on for every year till lease matures.

ALTERNATIVES

Do nothing: The first alternative for Starbucks is to do nothing. They may decide to continue

with their current practices of classifying leases by the contractually obligated term they have

agreed to. This will result in no changes for the business’ current or future operations but leaves

them vulnerable to litigation if the proposed changes take effect. Starbucks was not in a position

to begin listing all of the off-balance sheet leases as assets with a corresponding liability.

Accept the proposed changes: The second alternative for Starbucks is to accept the proposed

changes and begin to reclassify all existing leases they hold to appropriately match the new

standards. This would result in a large shift in their balance sheets as much of the leases are not

recorded as assets, and only the lease payments are recorded under liabilities. This represents a

significant burden to both the accounting and administrative departments as they will need to

make constant adjustments to accurately reflect and change the estimated contingent rental

payments that are made in advance of the actual activities having occurred. The net result of this

alternative should Starbucks choose to adopt this reform is an expensive and time-consuming

procedure that Starbucks sees as entirely unnecessary and too costly to provide any meaningful

changes.

Adopt their own suggestions: The third option for Starbucks is to adopt the recommendations

made in its letter to the Financial Accounting Standards board. In the letter Starbucks recognized

that there is likely a contingent of shareholders who may be interested in the inner workings of

the company’s lease agreements beyond what is already required by the current standards. The

company could choose to add ‘qualitative disclosures’ for these end-users to help explain the

practices and highlight meaningful metrics in the portfolio. Another recommendation for them to

adopt is a linked approach to recognizing expenses. They believe this is a valid method of

recording previously off-balance sheet financing while allowing them to preserve the straight-

line rental expense pattern currently in use. They also argued that in cases where base rent is

either below market rates or nil that contingent rents could be used in its place to effectively

report the lease’s economic substance.

Do nothing: The first alternative for Starbucks is to do nothing. They may decide to continue

with their current practices of classifying leases by the contractually obligated term they have

agreed to. This will result in no changes for the business’ current or future operations but leaves

them vulnerable to litigation if the proposed changes take effect. Starbucks was not in a position

to begin listing all of the off-balance sheet leases as assets with a corresponding liability.

Accept the proposed changes: The second alternative for Starbucks is to accept the proposed

changes and begin to reclassify all existing leases they hold to appropriately match the new

standards. This would result in a large shift in their balance sheets as much of the leases are not

recorded as assets, and only the lease payments are recorded under liabilities. This represents a

significant burden to both the accounting and administrative departments as they will need to

make constant adjustments to accurately reflect and change the estimated contingent rental

payments that are made in advance of the actual activities having occurred. The net result of this

alternative should Starbucks choose to adopt this reform is an expensive and time-consuming

procedure that Starbucks sees as entirely unnecessary and too costly to provide any meaningful

changes.

Adopt their own suggestions: The third option for Starbucks is to adopt the recommendations

made in its letter to the Financial Accounting Standards board. In the letter Starbucks recognized

that there is likely a contingent of shareholders who may be interested in the inner workings of

the company’s lease agreements beyond what is already required by the current standards. The

company could choose to add ‘qualitative disclosures’ for these end-users to help explain the

practices and highlight meaningful metrics in the portfolio. Another recommendation for them to

adopt is a linked approach to recognizing expenses. They believe this is a valid method of

recording previously off-balance sheet financing while allowing them to preserve the straight-

line rental expense pattern currently in use. They also argued that in cases where base rent is

either below market rates or nil that contingent rents could be used in its place to effectively

report the lease’s economic substance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ALTERNATIVES COMPARED

Do nothing

Pro:

· No additional expenses

· No changes made to current internal accounting and reporting procedures

· Consistency in year-to-year reports allows for financial statement users to easily

comprehend and identify trends, should they arise

Cons:

· Leaves the company open to litigation should they fail to adapt to changes

· Possibility of being isolated from other industry leaders should those companies

choose to adopt these rules

Accept Proposed Changes

Pros:

· Stay ahead of changing trends in financial reporting

· Get a head start on changing old lease classifications to reduce reporting delays

Cons:

· Time consuming- beyond a reasonable amount of time would be needed to accurately

account for all contingent rentals

· Constant need for changes to accurately reflect real costs associated with contingent

rent

Do nothing

Pro:

· No additional expenses

· No changes made to current internal accounting and reporting procedures

· Consistency in year-to-year reports allows for financial statement users to easily

comprehend and identify trends, should they arise

Cons:

· Leaves the company open to litigation should they fail to adapt to changes

· Possibility of being isolated from other industry leaders should those companies

choose to adopt these rules

Accept Proposed Changes

Pros:

· Stay ahead of changing trends in financial reporting

· Get a head start on changing old lease classifications to reduce reporting delays

Cons:

· Time consuming- beyond a reasonable amount of time would be needed to accurately

account for all contingent rentals

· Constant need for changes to accurately reflect real costs associated with contingent

rent

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

· The high cost of implementing and carrying proposed changes would diminish the

usefulness of the new reporting standards

· Unnecessary changes could lead to confusion in all stakeholder parties as they adapt to

new reporting standards

Adopt Recommendations

Pros:

· Demonstrate responsible governance on behalf of the company’s board

· Easily understandable rental portfolio could entice future investments

· Demonstrate that proposed changes are unnecessary if recommendations become

industry standard

Cons:

· While not as expensive as a full implementation of the proposed changes this option

still carries high costs

· Adoption of unrequired standards of financial reporting could result in backlash from

shareholders unhappy with any additional unnecessary expenses

RECOMMENDATION

We identified 3 possible solutions in the issues relating to starbucks accounting treatment of

lease accounting and recommend them to go with the second option of accepting the proposed

standard. As it has been developed over time by professionals all over the world with expertise

and sound knowledge. It helps in the true presentation of liabilities and assets of the company

which has already occurred but loopholes are used to hide them. To say by definition Starbucks

already have signed non cancelable contracts of lease and obligation to pay in future have

usefulness of the new reporting standards

· Unnecessary changes could lead to confusion in all stakeholder parties as they adapt to

new reporting standards

Adopt Recommendations

Pros:

· Demonstrate responsible governance on behalf of the company’s board

· Easily understandable rental portfolio could entice future investments

· Demonstrate that proposed changes are unnecessary if recommendations become

industry standard

Cons:

· While not as expensive as a full implementation of the proposed changes this option

still carries high costs

· Adoption of unrequired standards of financial reporting could result in backlash from

shareholders unhappy with any additional unnecessary expenses

RECOMMENDATION

We identified 3 possible solutions in the issues relating to starbucks accounting treatment of

lease accounting and recommend them to go with the second option of accepting the proposed

standard. As it has been developed over time by professionals all over the world with expertise

and sound knowledge. It helps in the true presentation of liabilities and assets of the company

which has already occurred but loopholes are used to hide them. To say by definition Starbucks

already have signed non cancelable contracts of lease and obligation to pay in future have

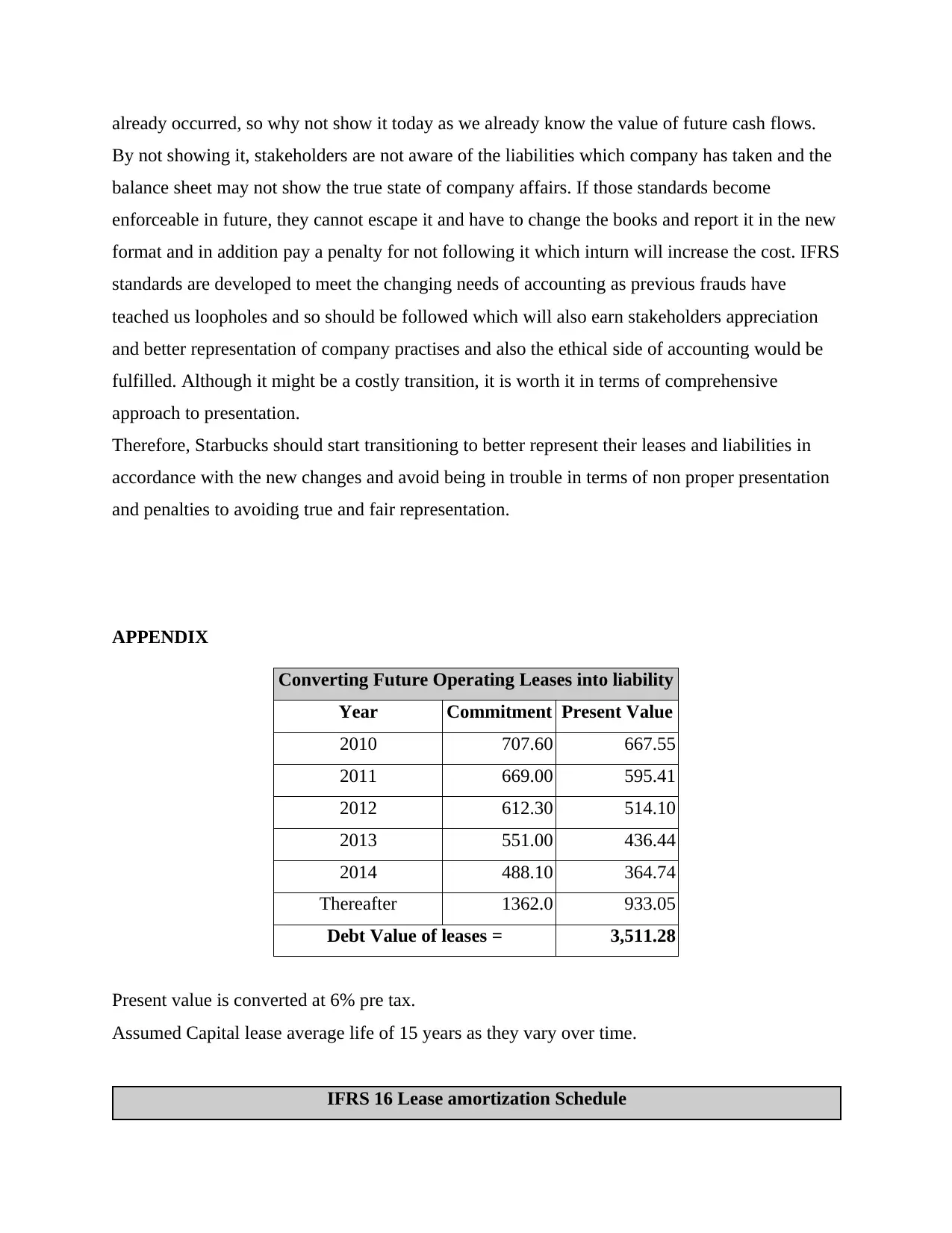

already occurred, so why not show it today as we already know the value of future cash flows.

By not showing it, stakeholders are not aware of the liabilities which company has taken and the

balance sheet may not show the true state of company affairs. If those standards become

enforceable in future, they cannot escape it and have to change the books and report it in the new

format and in addition pay a penalty for not following it which inturn will increase the cost. IFRS

standards are developed to meet the changing needs of accounting as previous frauds have

teached us loopholes and so should be followed which will also earn stakeholders appreciation

and better representation of company practises and also the ethical side of accounting would be

fulfilled. Although it might be a costly transition, it is worth it in terms of comprehensive

approach to presentation.

Therefore, Starbucks should start transitioning to better represent their leases and liabilities in

accordance with the new changes and avoid being in trouble in terms of non proper presentation

and penalties to avoiding true and fair representation.

APPENDIX

Converting Future Operating Leases into liability

Year Commitment Present Value

2010 707.60 667.55

2011 669.00 595.41

2012 612.30 514.10

2013 551.00 436.44

2014 488.10 364.74

Thereafter 1362.0 933.05

Debt Value of leases = 3,511.28

Present value is converted at 6% pre tax.

Assumed Capital lease average life of 15 years as they vary over time.

IFRS 16 Lease amortization Schedule

By not showing it, stakeholders are not aware of the liabilities which company has taken and the

balance sheet may not show the true state of company affairs. If those standards become

enforceable in future, they cannot escape it and have to change the books and report it in the new

format and in addition pay a penalty for not following it which inturn will increase the cost. IFRS

standards are developed to meet the changing needs of accounting as previous frauds have

teached us loopholes and so should be followed which will also earn stakeholders appreciation

and better representation of company practises and also the ethical side of accounting would be

fulfilled. Although it might be a costly transition, it is worth it in terms of comprehensive

approach to presentation.

Therefore, Starbucks should start transitioning to better represent their leases and liabilities in

accordance with the new changes and avoid being in trouble in terms of non proper presentation

and penalties to avoiding true and fair representation.

APPENDIX

Converting Future Operating Leases into liability

Year Commitment Present Value

2010 707.60 667.55

2011 669.00 595.41

2012 612.30 514.10

2013 551.00 436.44

2014 488.10 364.74

Thereafter 1362.0 933.05

Debt Value of leases = 3,511.28

Present value is converted at 6% pre tax.

Assumed Capital lease average life of 15 years as they vary over time.

IFRS 16 Lease amortization Schedule

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.