Financial Performance Analysis: Starbucks' Acquisition of Roast Plc

VerifiedAdded on 2023/01/12

|14

|4390

|84

Report

AI Summary

This report analyzes the financial decision-making process of Starbucks in its planned acquisition of Roast Plc. It begins with an industry review of the coffee house sector in the UK, highlighting key players and market trends. The report then conducts a business performance analysis of Roast Plc, including a detailed examination of its statement of profit or loss, statement of financial position (balance sheet), and statement of cash flows for the years 2017 and 2018. Various financial ratios, such as gross profit ratio, operating profit ratio, net profit ratio, debt-equity ratio, return on capital employed, quick ratio, and current ratio, are calculated and interpreted to assess the company's profitability, liquidity, and financial health. Finally, the report delves into investment appraisal techniques, forecasting, and potential sources of finance relevant to the acquisition, providing a comprehensive financial assessment of the proposed merger.

Financial decision

making

making

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

PART 1: INDUSTRY REVIEW.....................................................................................................1

Review of coffee house industry.................................................................................................1

PART 2: BUSINESS PERFORMANCE ANALYSIS....................................................................2

2.1 Statement of profit or loss......................................................................................................2

2.2 Statement of financial position..............................................................................................3

2.3 Statement of cash flows.........................................................................................................6

PART 3: INVESTMENT APPRAISAL..........................................................................................9

3.1.a Management forecast..........................................................................................................9

3.1.b Investment appraisal techniques.........................................................................................9

3.2 Sources of finance................................................................................................................10

EXECUTIVE SUMMARY.............................................................................................................1

PART 1: INDUSTRY REVIEW.....................................................................................................1

Review of coffee house industry.................................................................................................1

PART 2: BUSINESS PERFORMANCE ANALYSIS....................................................................2

2.1 Statement of profit or loss......................................................................................................2

2.2 Statement of financial position..............................................................................................3

2.3 Statement of cash flows.........................................................................................................6

PART 3: INVESTMENT APPRAISAL..........................................................................................9

3.1.a Management forecast..........................................................................................................9

3.1.b Investment appraisal techniques.........................................................................................9

3.2 Sources of finance................................................................................................................10

EXECUTIVE SUMMARY

Present report is based upon financial decision making of Starbucks which is planning to

acquire Roast Plc. FDM can be defined as the procedure forming effective decisions for

betterment of business so that efficiency of business could be improved. Main purpose of it is to

grow the business and attain sustainability for long run in future. While planning to acquire a

new company then it is very important for the organisation to make sure that all the elements of

financial position of the other entity is analysed properly. If the decisions of acquisition are

formed without any appropriate analysis of financial position then it may result in failure of

whole project. While performing the assessment different statements are analysed by the finance

department of the enterprise. These are profit and loss account, balance sheet and cash flow

statement. In order to determine the growth level of sector analysis of industry is conducted.

Different types of investment appraisal techniques are used to determine the financial viability of

the company which will be acquired in future. The key elements that are also required to be

focused are sources of funds as they are used to fulfil all the monetary requirements.

PART 1: INDUSTRY REVIEW

Review of coffee house industry

The sector in which different coffee houses are operating business is considered very big

and it is analysed that it contributes in development of economy. In order to conduct the industry

review different elements regarding the whole sector are required to be determined. Some of the

key elements that are discovered while conducting industry review of coffee house sector of UK

(Barth, Papageorge and Thom, 2017). All of them are as follows:

Coffee house industry of UK have experienced the growth of 7.9% in year 2018 which

shows the development of it.

The key players in the industry are Soho Coffee, Coffee Republic, Café2U, Muffin

Break, AMT Coffee, Starbucks, Roast Ltd., Costa Coffee etc.

The GDP contribution of coffee industry for year 2017 was around 3.7 billion pounds. It

shows that the level of growth of the industry is very high.

The major challenge which is faced by the sector is increasing number of fitness freak

individuals. They do not consume coffee because of higher level of sugar in it. They

avoid all the drinks that are affecting their health.

1

Present report is based upon financial decision making of Starbucks which is planning to

acquire Roast Plc. FDM can be defined as the procedure forming effective decisions for

betterment of business so that efficiency of business could be improved. Main purpose of it is to

grow the business and attain sustainability for long run in future. While planning to acquire a

new company then it is very important for the organisation to make sure that all the elements of

financial position of the other entity is analysed properly. If the decisions of acquisition are

formed without any appropriate analysis of financial position then it may result in failure of

whole project. While performing the assessment different statements are analysed by the finance

department of the enterprise. These are profit and loss account, balance sheet and cash flow

statement. In order to determine the growth level of sector analysis of industry is conducted.

Different types of investment appraisal techniques are used to determine the financial viability of

the company which will be acquired in future. The key elements that are also required to be

focused are sources of funds as they are used to fulfil all the monetary requirements.

PART 1: INDUSTRY REVIEW

Review of coffee house industry

The sector in which different coffee houses are operating business is considered very big

and it is analysed that it contributes in development of economy. In order to conduct the industry

review different elements regarding the whole sector are required to be determined. Some of the

key elements that are discovered while conducting industry review of coffee house sector of UK

(Barth, Papageorge and Thom, 2017). All of them are as follows:

Coffee house industry of UK have experienced the growth of 7.9% in year 2018 which

shows the development of it.

The key players in the industry are Soho Coffee, Coffee Republic, Café2U, Muffin

Break, AMT Coffee, Starbucks, Roast Ltd., Costa Coffee etc.

The GDP contribution of coffee industry for year 2017 was around 3.7 billion pounds. It

shows that the level of growth of the industry is very high.

The major challenge which is faced by the sector is increasing number of fitness freak

individuals. They do not consume coffee because of higher level of sugar in it. They

avoid all the drinks that are affecting their health.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The opportunity for the coffee house industry is to expand the business in those countries

where it is not operating. Another opportunity for the sector is to make sure that it

introduces such drinks in the market which are specially for fitness freak people. It will

help to retain the customers and grow the business.

PART 2: BUSINESS PERFORMANCE ANALYSIS

2.1 Statement of profit or loss

The statement which is formed by business entities for the purpose of keeping detailed

information of all the incomes and expenses is known as statement of profit and loss. With the

help of it, the stakeholders can analyse that business is able to generate appropriate amount of

profits or not to meet all the future goals. It is mainly used for the purpose of determining

profitability of the company. As Starbucks is planning to acquire Roast Ltd., therefore it is very

important for it to analyse its profit and loss account properly. The exhibit 1 is showing that for

year 2017 revenues of Roast Ltd were around 2022 and in year 2018 these are increased up to

2534. On the other hand, due to increment in revenues cost of sales is also increased from 1505

to 1990. Gross profit of the company is also showing positive changes in 2018 as it is inclined

from 517 to 544. In year 2017 the entity did not have any operating incomes but in 2018 the

operating income earned by the company was around 60 (Consigli, Kuhn and Brandimarte,

2017). The elements that are included in operating expenses of the company are director’s

remuneration, bad debts, depreciation, utility cost, store maintenance, distribution cost,

marketing and advertising, legal and professional fees etc. At the end of 2017 and 2018 the

profits of the company were 36 and 81 respectively.

In order to analyse the statement of profit and loss different ratios are calculated which

are as follows:

Gross profit ratio: While analysing the percentage of direct profits this ratio is

calculated. With the help of it, the managers of a company can determine the operational

performance of the company. It guides to analyse the relationship between revenues and gross

profits of the company.

Operating profit ratio: When an organisation is willing to assess the ability to create

profits in the accounting period this ratio is calculated. In order to calculate it the profits that are

used for the calculations should be before interest and taxes.

2

where it is not operating. Another opportunity for the sector is to make sure that it

introduces such drinks in the market which are specially for fitness freak people. It will

help to retain the customers and grow the business.

PART 2: BUSINESS PERFORMANCE ANALYSIS

2.1 Statement of profit or loss

The statement which is formed by business entities for the purpose of keeping detailed

information of all the incomes and expenses is known as statement of profit and loss. With the

help of it, the stakeholders can analyse that business is able to generate appropriate amount of

profits or not to meet all the future goals. It is mainly used for the purpose of determining

profitability of the company. As Starbucks is planning to acquire Roast Ltd., therefore it is very

important for it to analyse its profit and loss account properly. The exhibit 1 is showing that for

year 2017 revenues of Roast Ltd were around 2022 and in year 2018 these are increased up to

2534. On the other hand, due to increment in revenues cost of sales is also increased from 1505

to 1990. Gross profit of the company is also showing positive changes in 2018 as it is inclined

from 517 to 544. In year 2017 the entity did not have any operating incomes but in 2018 the

operating income earned by the company was around 60 (Consigli, Kuhn and Brandimarte,

2017). The elements that are included in operating expenses of the company are director’s

remuneration, bad debts, depreciation, utility cost, store maintenance, distribution cost,

marketing and advertising, legal and professional fees etc. At the end of 2017 and 2018 the

profits of the company were 36 and 81 respectively.

In order to analyse the statement of profit and loss different ratios are calculated which

are as follows:

Gross profit ratio: While analysing the percentage of direct profits this ratio is

calculated. With the help of it, the managers of a company can determine the operational

performance of the company. It guides to analyse the relationship between revenues and gross

profits of the company.

Operating profit ratio: When an organisation is willing to assess the ability to create

profits in the accounting period this ratio is calculated. In order to calculate it the profits that are

used for the calculations should be before interest and taxes.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

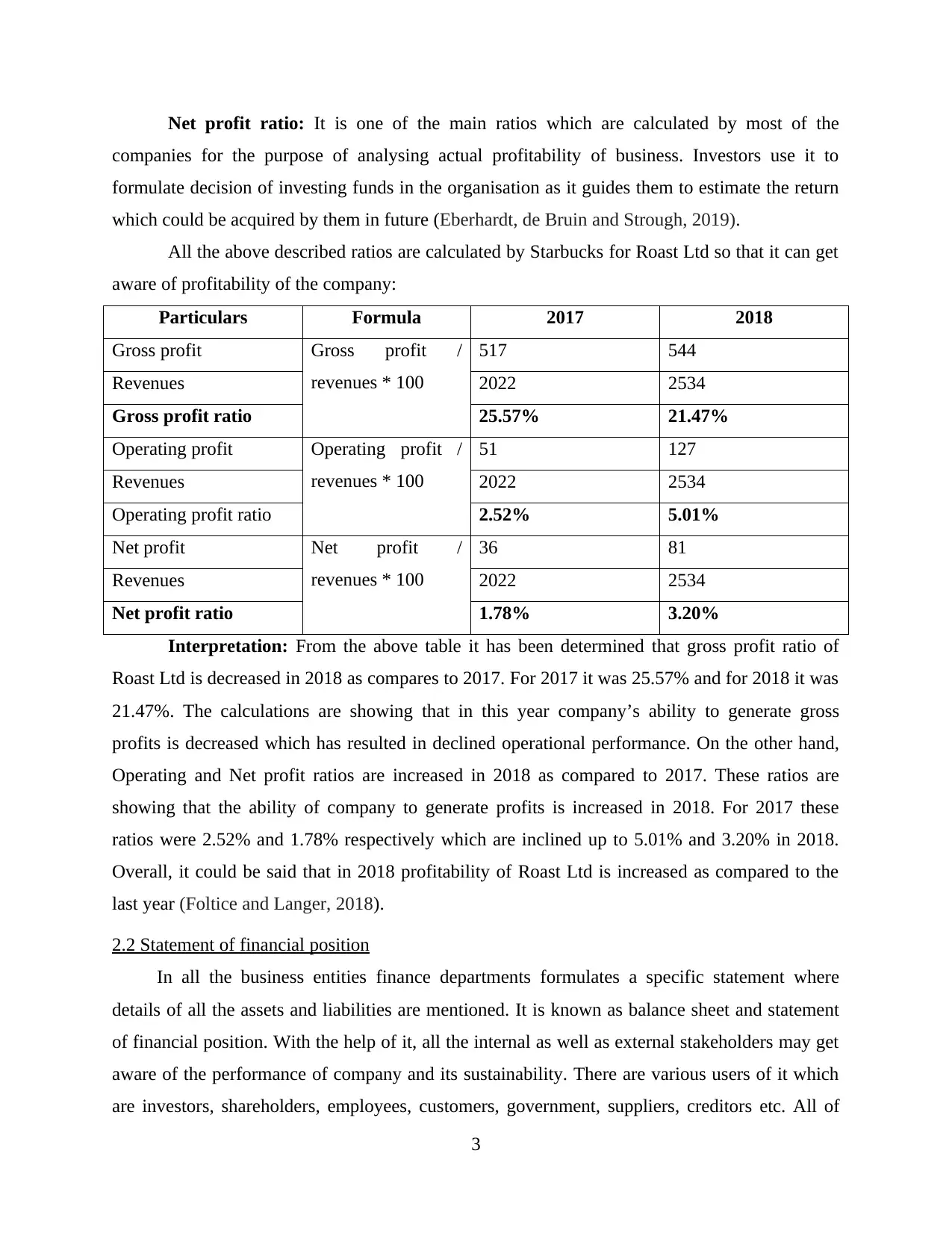

Net profit ratio: It is one of the main ratios which are calculated by most of the

companies for the purpose of analysing actual profitability of business. Investors use it to

formulate decision of investing funds in the organisation as it guides them to estimate the return

which could be acquired by them in future (Eberhardt, de Bruin and Strough, 2019).

All the above described ratios are calculated by Starbucks for Roast Ltd so that it can get

aware of profitability of the company:

Particulars Formula 2017 2018

Gross profit Gross profit /

revenues * 100

517 544

Revenues 2022 2534

Gross profit ratio 25.57% 21.47%

Operating profit Operating profit /

revenues * 100

51 127

Revenues 2022 2534

Operating profit ratio 2.52% 5.01%

Net profit Net profit /

revenues * 100

36 81

Revenues 2022 2534

Net profit ratio 1.78% 3.20%

Interpretation: From the above table it has been determined that gross profit ratio of

Roast Ltd is decreased in 2018 as compares to 2017. For 2017 it was 25.57% and for 2018 it was

21.47%. The calculations are showing that in this year company’s ability to generate gross

profits is decreased which has resulted in declined operational performance. On the other hand,

Operating and Net profit ratios are increased in 2018 as compared to 2017. These ratios are

showing that the ability of company to generate profits is increased in 2018. For 2017 these

ratios were 2.52% and 1.78% respectively which are inclined up to 5.01% and 3.20% in 2018.

Overall, it could be said that in 2018 profitability of Roast Ltd is increased as compared to the

last year (Foltice and Langer, 2018).

2.2 Statement of financial position

In all the business entities finance departments formulates a specific statement where

details of all the assets and liabilities are mentioned. It is known as balance sheet and statement

of financial position. With the help of it, all the internal as well as external stakeholders may get

aware of the performance of company and its sustainability. There are various users of it which

are investors, shareholders, employees, customers, government, suppliers, creditors etc. All of

3

companies for the purpose of analysing actual profitability of business. Investors use it to

formulate decision of investing funds in the organisation as it guides them to estimate the return

which could be acquired by them in future (Eberhardt, de Bruin and Strough, 2019).

All the above described ratios are calculated by Starbucks for Roast Ltd so that it can get

aware of profitability of the company:

Particulars Formula 2017 2018

Gross profit Gross profit /

revenues * 100

517 544

Revenues 2022 2534

Gross profit ratio 25.57% 21.47%

Operating profit Operating profit /

revenues * 100

51 127

Revenues 2022 2534

Operating profit ratio 2.52% 5.01%

Net profit Net profit /

revenues * 100

36 81

Revenues 2022 2534

Net profit ratio 1.78% 3.20%

Interpretation: From the above table it has been determined that gross profit ratio of

Roast Ltd is decreased in 2018 as compares to 2017. For 2017 it was 25.57% and for 2018 it was

21.47%. The calculations are showing that in this year company’s ability to generate gross

profits is decreased which has resulted in declined operational performance. On the other hand,

Operating and Net profit ratios are increased in 2018 as compared to 2017. These ratios are

showing that the ability of company to generate profits is increased in 2018. For 2017 these

ratios were 2.52% and 1.78% respectively which are inclined up to 5.01% and 3.20% in 2018.

Overall, it could be said that in 2018 profitability of Roast Ltd is increased as compared to the

last year (Foltice and Langer, 2018).

2.2 Statement of financial position

In all the business entities finance departments formulates a specific statement where

details of all the assets and liabilities are mentioned. It is known as balance sheet and statement

of financial position. With the help of it, all the internal as well as external stakeholders may get

aware of the performance of company and its sustainability. There are various users of it which

are investors, shareholders, employees, customers, government, suppliers, creditors etc. All of

3

them use it for different purposes. For example, investors use to it to determine financial position

of business, creditors use it to analyse credit ability of the company etc. Currently, Starbucks is

planning to acquire Roast Ltd therefore it is vital for it to make sure that it analyses actual

position of the company in the market. For this purpose, balance sheet is required to be assessed.

From the exhibit 2 which is statement of financial position of Roast Ltd it has been

determined that long-term borrowings which are part of non-current liabilities of the company

are increased in 2018 from 100 to 275 which shows that debts of the entity are increased in this

year. Current liabilities such as trade payables and bank overdraft are also increased in 2018. In

year 2017 there was no overdraft but in 2018 the company have took an overdraft from the bank

and its value is 73 (Hershfield, John and Reiff, 2018). Apart from this, trade payables were

increased from 138 to 235 in 2018. Share capital of the company remains the same for both the

years which is 200. Retained earnings for 2018 are increased from 579 to 660. It shows that

company have made reserves for future uncertainties.

From the assets side of balance sheet, it has been determined that in 2017 Roast Ltd was

having cash and cash equivalents of 134 and in 2018 it was not having any cash or bank balance.

Inventories for 2017 were 120 and in 2018 these were increased up to 299. Trade and other

receivables for 2017 were 93 and for 2018 the value of them was 148. Property, plant and

equipment which are fixed assets of the company were also increased in 2018 as compared to

2017. For 2018 these were 996 and for 2017 value of them was 670.

In order to make sure that Roast Ltd should be acquired by Starbucks or not different

ratios are calculated with the help of statement of financial position of the company. All of them

are as follows:

Debt equity: It is used by companies to analyse the use of internal liabilities against

external funds. In order to carry out operations in systematic manner it is essential for all the

organisations to utilise outsider’s finance more than internal funds because with the help of it

negative impact of uncertainties upon the business could be reduced.

Return on capital employed: While planning to analyse the ability of using profits and

capital to enhance efficiency of the company this ratio is calculated. It can guide the investors

and other top-level executives to determine that the business is performing well or not in the

market as compared to the competitors (Hirshleifer, Jian and Zhang, 2018).

4

of business, creditors use it to analyse credit ability of the company etc. Currently, Starbucks is

planning to acquire Roast Ltd therefore it is vital for it to make sure that it analyses actual

position of the company in the market. For this purpose, balance sheet is required to be assessed.

From the exhibit 2 which is statement of financial position of Roast Ltd it has been

determined that long-term borrowings which are part of non-current liabilities of the company

are increased in 2018 from 100 to 275 which shows that debts of the entity are increased in this

year. Current liabilities such as trade payables and bank overdraft are also increased in 2018. In

year 2017 there was no overdraft but in 2018 the company have took an overdraft from the bank

and its value is 73 (Hershfield, John and Reiff, 2018). Apart from this, trade payables were

increased from 138 to 235 in 2018. Share capital of the company remains the same for both the

years which is 200. Retained earnings for 2018 are increased from 579 to 660. It shows that

company have made reserves for future uncertainties.

From the assets side of balance sheet, it has been determined that in 2017 Roast Ltd was

having cash and cash equivalents of 134 and in 2018 it was not having any cash or bank balance.

Inventories for 2017 were 120 and in 2018 these were increased up to 299. Trade and other

receivables for 2017 were 93 and for 2018 the value of them was 148. Property, plant and

equipment which are fixed assets of the company were also increased in 2018 as compared to

2017. For 2018 these were 996 and for 2017 value of them was 670.

In order to make sure that Roast Ltd should be acquired by Starbucks or not different

ratios are calculated with the help of statement of financial position of the company. All of them

are as follows:

Debt equity: It is used by companies to analyse the use of internal liabilities against

external funds. In order to carry out operations in systematic manner it is essential for all the

organisations to utilise outsider’s finance more than internal funds because with the help of it

negative impact of uncertainties upon the business could be reduced.

Return on capital employed: While planning to analyse the ability of using profits and

capital to enhance efficiency of the company this ratio is calculated. It can guide the investors

and other top-level executives to determine that the business is performing well or not in the

market as compared to the competitors (Hirshleifer, Jian and Zhang, 2018).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

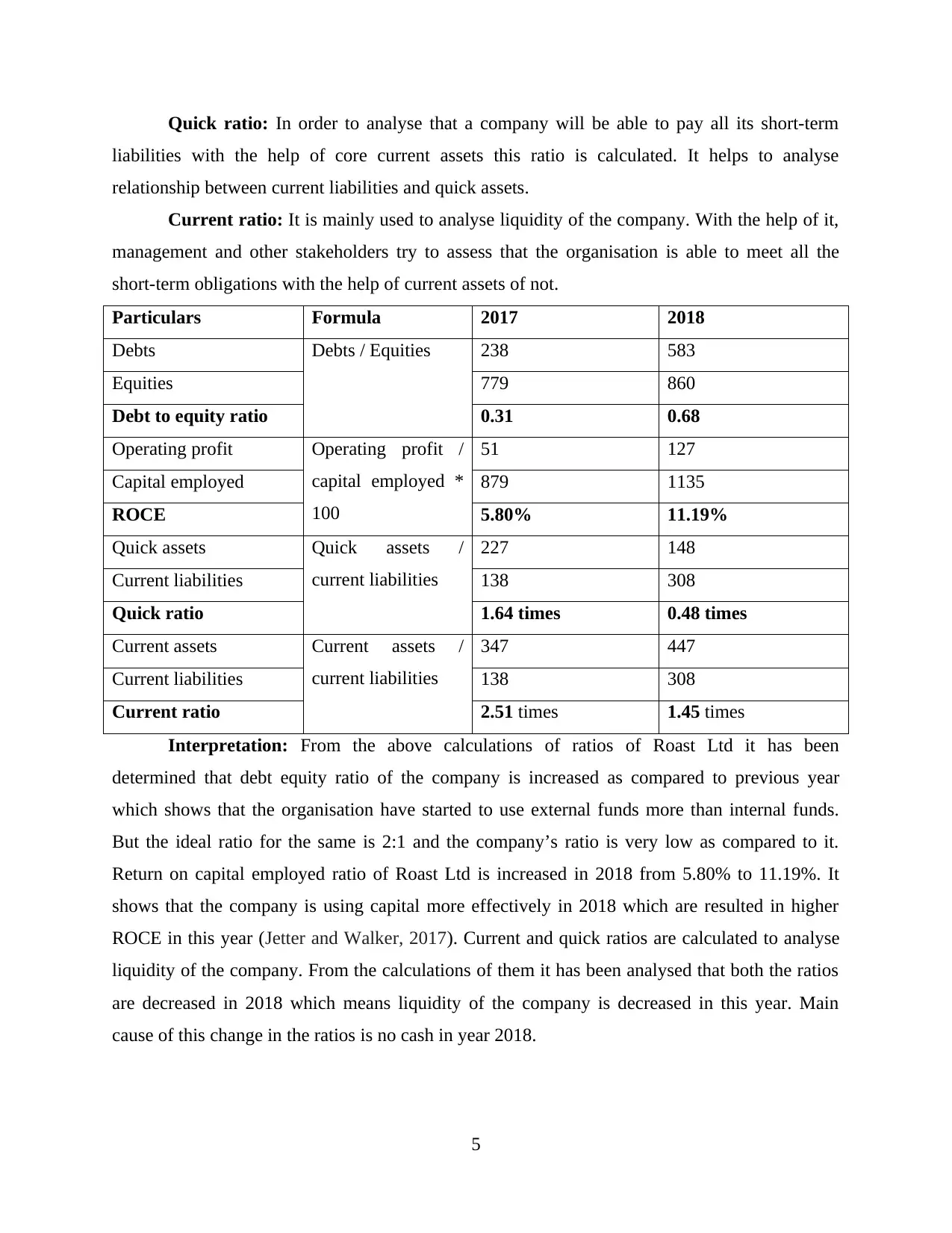

Quick ratio: In order to analyse that a company will be able to pay all its short-term

liabilities with the help of core current assets this ratio is calculated. It helps to analyse

relationship between current liabilities and quick assets.

Current ratio: It is mainly used to analyse liquidity of the company. With the help of it,

management and other stakeholders try to assess that the organisation is able to meet all the

short-term obligations with the help of current assets of not.

Particulars Formula 2017 2018

Debts Debts / Equities 238 583

Equities 779 860

Debt to equity ratio 0.31 0.68

Operating profit Operating profit /

capital employed *

100

51 127

Capital employed 879 1135

ROCE 5.80% 11.19%

Quick assets Quick assets /

current liabilities

227 148

Current liabilities 138 308

Quick ratio 1.64 times 0.48 times

Current assets Current assets /

current liabilities

347 447

Current liabilities 138 308

Current ratio 2.51 times 1.45 times

Interpretation: From the above calculations of ratios of Roast Ltd it has been

determined that debt equity ratio of the company is increased as compared to previous year

which shows that the organisation have started to use external funds more than internal funds.

But the ideal ratio for the same is 2:1 and the company’s ratio is very low as compared to it.

Return on capital employed ratio of Roast Ltd is increased in 2018 from 5.80% to 11.19%. It

shows that the company is using capital more effectively in 2018 which are resulted in higher

ROCE in this year (Jetter and Walker, 2017). Current and quick ratios are calculated to analyse

liquidity of the company. From the calculations of them it has been analysed that both the ratios

are decreased in 2018 which means liquidity of the company is decreased in this year. Main

cause of this change in the ratios is no cash in year 2018.

5

liabilities with the help of core current assets this ratio is calculated. It helps to analyse

relationship between current liabilities and quick assets.

Current ratio: It is mainly used to analyse liquidity of the company. With the help of it,

management and other stakeholders try to assess that the organisation is able to meet all the

short-term obligations with the help of current assets of not.

Particulars Formula 2017 2018

Debts Debts / Equities 238 583

Equities 779 860

Debt to equity ratio 0.31 0.68

Operating profit Operating profit /

capital employed *

100

51 127

Capital employed 879 1135

ROCE 5.80% 11.19%

Quick assets Quick assets /

current liabilities

227 148

Current liabilities 138 308

Quick ratio 1.64 times 0.48 times

Current assets Current assets /

current liabilities

347 447

Current liabilities 138 308

Current ratio 2.51 times 1.45 times

Interpretation: From the above calculations of ratios of Roast Ltd it has been

determined that debt equity ratio of the company is increased as compared to previous year

which shows that the organisation have started to use external funds more than internal funds.

But the ideal ratio for the same is 2:1 and the company’s ratio is very low as compared to it.

Return on capital employed ratio of Roast Ltd is increased in 2018 from 5.80% to 11.19%. It

shows that the company is using capital more effectively in 2018 which are resulted in higher

ROCE in this year (Jetter and Walker, 2017). Current and quick ratios are calculated to analyse

liquidity of the company. From the calculations of them it has been analysed that both the ratios

are decreased in 2018 which means liquidity of the company is decreased in this year. Main

cause of this change in the ratios is no cash in year 2018.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 Statement of cash flows

All the organisations formulate a specific statement so that information of cash transactions

could be recorded in it. It is known as statement of cash flows in which data of cash inflow and

outflow is reported. With the help of it, all the managers and other internal as well as external

stakeholders can analyse that company is having any cash balance at the end of the year or not.

For Starbucks it is essential to analyse the cash flow statement of Roast Ltd before acquiring it.

From the exhibit 2 it has been analysed that for year 2018 operating profit for the company was

around 127. The cash outflow from the operating activities was 24 and the investing activities are

also showing a negative balance which is 358. Financing activities are showing inflow of 175. At

the end of 2018 the organisation was having total outflow of 73 and it is the main reason why

there is an overdraft of 73 in the balance sheet of the company (Kim, Gutter and Spangler, 2017).

Operating cash cycle: In all the companies it is calculated to determine the time period

which is required by all them to covert the inventory in the funds. It can help the management to

determine that the in future the business will be able to sustain in the market or not. While

formulating the decision of acquiring Roast Ltd it will be calculated by Starbucks so that right

decision could be formed. The calculation of it is as follows:

Formula:

Days inventory outstanding XXX

Add: Days sales outstanding XXX

Less: Days payable outstanding XXX

Operating Cycle = XXX

Particulars 2017 2018

6

All the organisations formulate a specific statement so that information of cash transactions

could be recorded in it. It is known as statement of cash flows in which data of cash inflow and

outflow is reported. With the help of it, all the managers and other internal as well as external

stakeholders can analyse that company is having any cash balance at the end of the year or not.

For Starbucks it is essential to analyse the cash flow statement of Roast Ltd before acquiring it.

From the exhibit 2 it has been analysed that for year 2018 operating profit for the company was

around 127. The cash outflow from the operating activities was 24 and the investing activities are

also showing a negative balance which is 358. Financing activities are showing inflow of 175. At

the end of 2018 the organisation was having total outflow of 73 and it is the main reason why

there is an overdraft of 73 in the balance sheet of the company (Kim, Gutter and Spangler, 2017).

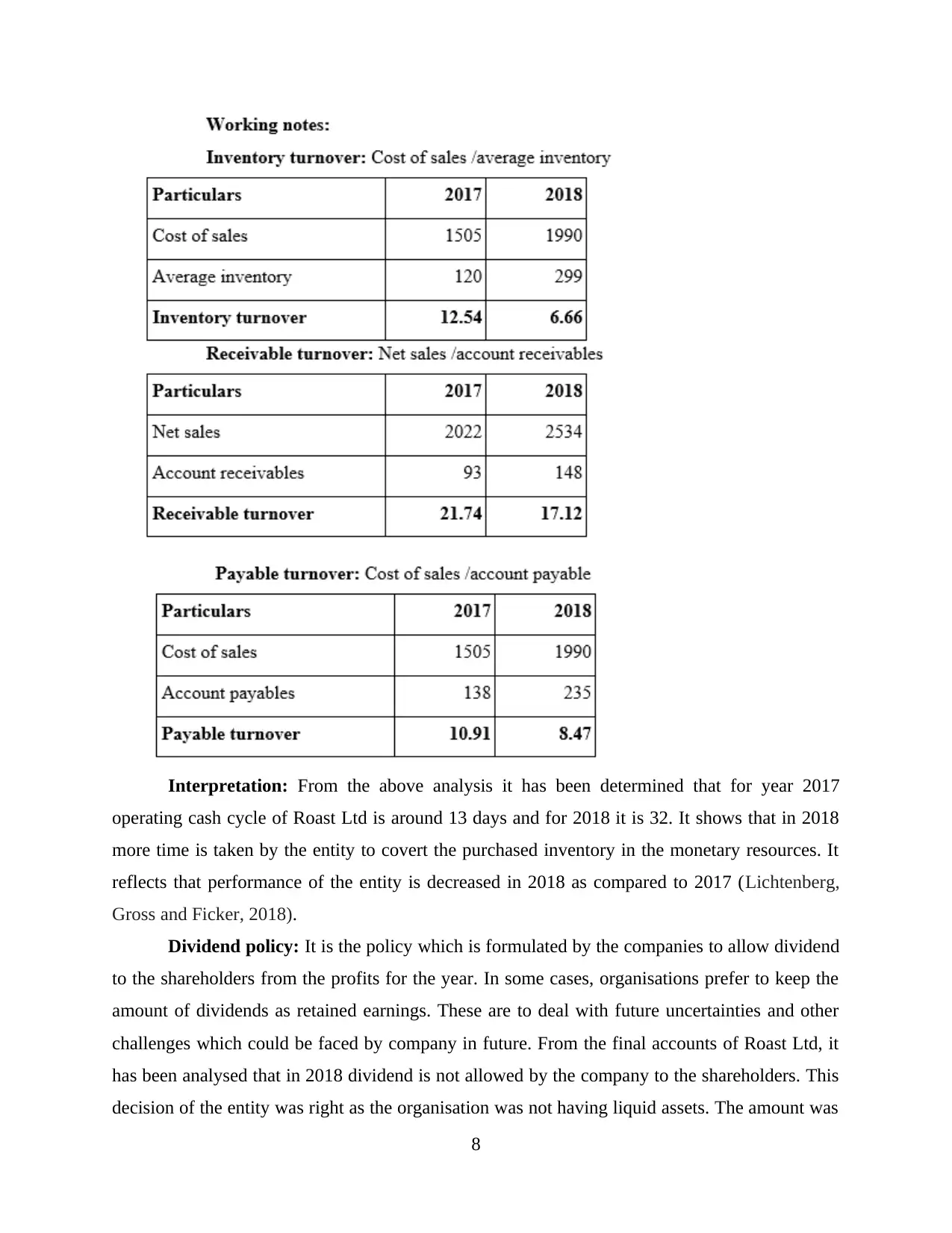

Operating cash cycle: In all the companies it is calculated to determine the time period

which is required by all them to covert the inventory in the funds. It can help the management to

determine that the in future the business will be able to sustain in the market or not. While

formulating the decision of acquiring Roast Ltd it will be calculated by Starbucks so that right

decision could be formed. The calculation of it is as follows:

Formula:

Days inventory outstanding XXX

Add: Days sales outstanding XXX

Less: Days payable outstanding XXX

Operating Cycle = XXX

Particulars 2017 2018

6

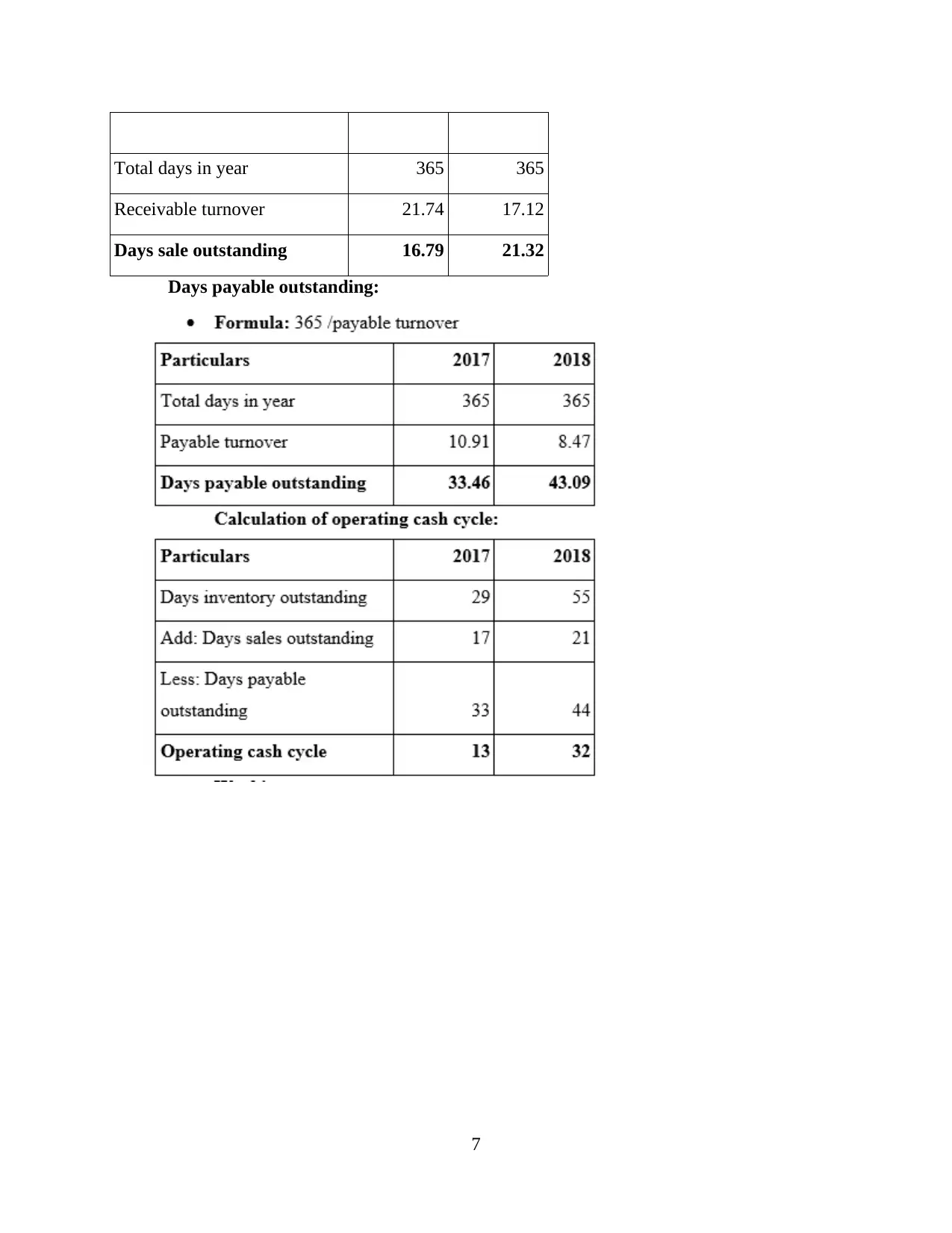

Total days in year 365 365

Receivable turnover 21.74 17.12

Days sale outstanding 16.79 21.32

Days payable outstanding:

7

Receivable turnover 21.74 17.12

Days sale outstanding 16.79 21.32

Days payable outstanding:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: From the above analysis it has been determined that for year 2017

operating cash cycle of Roast Ltd is around 13 days and for 2018 it is 32. It shows that in 2018

more time is taken by the entity to covert the purchased inventory in the monetary resources. It

reflects that performance of the entity is decreased in 2018 as compared to 2017 (Lichtenberg,

Gross and Ficker, 2018).

Dividend policy: It is the policy which is formulated by the companies to allow dividend

to the shareholders from the profits for the year. In some cases, organisations prefer to keep the

amount of dividends as retained earnings. These are to deal with future uncertainties and other

challenges which could be faced by company in future. From the final accounts of Roast Ltd, it

has been analysed that in 2018 dividend is not allowed by the company to the shareholders. This

decision of the entity was right as the organisation was not having liquid assets. The amount was

8

operating cash cycle of Roast Ltd is around 13 days and for 2018 it is 32. It shows that in 2018

more time is taken by the entity to covert the purchased inventory in the monetary resources. It

reflects that performance of the entity is decreased in 2018 as compared to 2017 (Lichtenberg,

Gross and Ficker, 2018).

Dividend policy: It is the policy which is formulated by the companies to allow dividend

to the shareholders from the profits for the year. In some cases, organisations prefer to keep the

amount of dividends as retained earnings. These are to deal with future uncertainties and other

challenges which could be faced by company in future. From the final accounts of Roast Ltd, it

has been analysed that in 2018 dividend is not allowed by the company to the shareholders. This

decision of the entity was right as the organisation was not having liquid assets. The amount was

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

kept by the enterprise as retained earnings so that it can respond to all the difficulties that may

take place in future.

PART 3: INVESTMENT APPRAISAL

3.1.a Management forecast

Roast Ltd is planning to invest 500 million pounds in upcoming years and the estimated

cash flow for the five year’s period is 60, 112, 148, 180 and 224. These are for the period of

2017 to 2021. It is reflecting that managers have planned that the cash inflow will be increased in

next five years. These estimations are made without proper basis so it is not possible to attain the

cash flow which is estimated by the company.

3.1.b Investment appraisal techniques

Investment appraisal: All the companies which are planning to make investment in a

future project then different techniques are used by them to analyse the viability of the project.

These are considered as the part of investment appraisal techniques. As Roast Ltd is planning to

invest 500 million pounds in a project therefore various types of techniques are being used by the

managers (Lieber and Skimmyhorn, 2018). All of them are as follows:

Payback period: It is used by companies to analyse the time which is required by an

investment to repay the actual value of investment. The Exhibit 3 is showing that if 500 million

pounds will be invested by Roast Ltd in the project then this value could be repaid by the

investment in 4 years.

Benefits: It can help to analyse different projects in less time period so that best suitable

decision in less time could be formulated.

Drawbacks: It does not take time value of money in to consideration therefore the results

of it are not accurate.

Accounting rate of return: This investment appraisal technique is used by organisations

to assess the rate of return which could be attained by an entity on the investment which will be

made in the project. Exhibit 3 is showing that is 500 million pounds will be invested by Roast

Ltd then it can provide returns on 18% to the organisation (Lu, Won and Cheng, 2016).

Benefits: It is beneficial for all the companies which are planning to invest in future

projects as it can guide them to assess the possible rate of return which could be acquired

by them in future.

9

take place in future.

PART 3: INVESTMENT APPRAISAL

3.1.a Management forecast

Roast Ltd is planning to invest 500 million pounds in upcoming years and the estimated

cash flow for the five year’s period is 60, 112, 148, 180 and 224. These are for the period of

2017 to 2021. It is reflecting that managers have planned that the cash inflow will be increased in

next five years. These estimations are made without proper basis so it is not possible to attain the

cash flow which is estimated by the company.

3.1.b Investment appraisal techniques

Investment appraisal: All the companies which are planning to make investment in a

future project then different techniques are used by them to analyse the viability of the project.

These are considered as the part of investment appraisal techniques. As Roast Ltd is planning to

invest 500 million pounds in a project therefore various types of techniques are being used by the

managers (Lieber and Skimmyhorn, 2018). All of them are as follows:

Payback period: It is used by companies to analyse the time which is required by an

investment to repay the actual value of investment. The Exhibit 3 is showing that if 500 million

pounds will be invested by Roast Ltd in the project then this value could be repaid by the

investment in 4 years.

Benefits: It can help to analyse different projects in less time period so that best suitable

decision in less time could be formulated.

Drawbacks: It does not take time value of money in to consideration therefore the results

of it are not accurate.

Accounting rate of return: This investment appraisal technique is used by organisations

to assess the rate of return which could be attained by an entity on the investment which will be

made in the project. Exhibit 3 is showing that is 500 million pounds will be invested by Roast

Ltd then it can provide returns on 18% to the organisation (Lu, Won and Cheng, 2016).

Benefits: It is beneficial for all the companies which are planning to invest in future

projects as it can guide them to assess the possible rate of return which could be acquired

by them in future.

9

Drawbacks: Just like pay back period time factor is also not focused in this technique of

investment appraisal which may result in inaccurate results.

Net present value: This technique of investment appraisal is used by companies to

analyse difference between initial investment and present value of cash flows. From the Exhibit

3 it has been analysed that if the project for investing 500 million pound will be selected by

Roast Ltd then it will result in NPV of 110 for the entity (Mitchell, Hammond and Utkus, 2017).

Benefits: With the help of it, effective and right decisions for future could be formulated

because it is highly focused with time factor.

Drawbacks: While planning to compare different sizes of projects it cannot be used by

companies.

The above discussion is showing that Roast Ltd should invest in the project of 500 million

pounds as it can help the company to generate higher returns. Its NPV and pay back period is

also very good which will help the enterprise to attain success in future.

3.2 Sources of finance

Finance is considered most vital and important part of any business that is required to meet

day to day expenses together with meeting long term investment. Sources of fimacee mainly

refer to the different ways and options from which money can be obtain by an organisation to

meet its expenses and other costs (Nofsinger, Patterson and Shank, 2018). The Roast Ltd is

currently planning to invest around 500 million pounds in a new project therefore it is looking

for most suitable sources of finance from where it can manage monetary funds for its upcoming

project. The two best alternatives that can be used by Roast Ltd to get an investment of 500

million pounds in order to finance its new project are discussed below with their respective

benefits and drawbacks:

Bank Loan

It basically represents the amount of money that an organisation can borrow from a bank

or other financial institution for a set period of time and at an agreed rate of interest. Use of bank

loan could be Roast Ltd to get a borrowing of 500 million pounds as it facilitates most secured

from of investment and also no dilution is created on ownership. The main advantages and

drawbacks associated with ban loan that could be faced by Roast Ltd while opting finance from

this source is discussed below:

10

investment appraisal which may result in inaccurate results.

Net present value: This technique of investment appraisal is used by companies to

analyse difference between initial investment and present value of cash flows. From the Exhibit

3 it has been analysed that if the project for investing 500 million pound will be selected by

Roast Ltd then it will result in NPV of 110 for the entity (Mitchell, Hammond and Utkus, 2017).

Benefits: With the help of it, effective and right decisions for future could be formulated

because it is highly focused with time factor.

Drawbacks: While planning to compare different sizes of projects it cannot be used by

companies.

The above discussion is showing that Roast Ltd should invest in the project of 500 million

pounds as it can help the company to generate higher returns. Its NPV and pay back period is

also very good which will help the enterprise to attain success in future.

3.2 Sources of finance

Finance is considered most vital and important part of any business that is required to meet

day to day expenses together with meeting long term investment. Sources of fimacee mainly

refer to the different ways and options from which money can be obtain by an organisation to

meet its expenses and other costs (Nofsinger, Patterson and Shank, 2018). The Roast Ltd is

currently planning to invest around 500 million pounds in a new project therefore it is looking

for most suitable sources of finance from where it can manage monetary funds for its upcoming

project. The two best alternatives that can be used by Roast Ltd to get an investment of 500

million pounds in order to finance its new project are discussed below with their respective

benefits and drawbacks:

Bank Loan

It basically represents the amount of money that an organisation can borrow from a bank

or other financial institution for a set period of time and at an agreed rate of interest. Use of bank

loan could be Roast Ltd to get a borrowing of 500 million pounds as it facilitates most secured

from of investment and also no dilution is created on ownership. The main advantages and

drawbacks associated with ban loan that could be faced by Roast Ltd while opting finance from

this source is discussed below:

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.