Financial Decision-Making: Starbucks and Roast Ltd Performance

VerifiedAdded on 2023/01/16

|16

|4606

|69

Report

AI Summary

This report provides a financial analysis of a potential acquisition scenario involving Starbucks and Roast Ltd. It begins with an executive summary, followed by an industry review of the coffee market in the UK, highlighting key players, challenges, and opportunities. The report then delves into the business performance analysis of Roast Ltd, examining statements of profit or loss, balance sheets, and cash flow statements. Key financial ratios such as ROCE, ROE, and profit margins are calculated and interpreted. The investment appraisal section includes management forecasts and explores various investment appraisal techniques. Finally, the report discusses potential sources of finance for the acquisition. The analysis concludes that Starbucks should acquire Roast Ltd due to its strong financial position, increasing profitability, and potential for global expansion.

FINANCIAL DECISION

MAKING

MAKING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

EXECUTIVE SUMMARY.............................................................................................................1

PART 1: INDUSTRY REVIEW.....................................................................................................1

PART 2 : BUSINESS PERFORMANCE ANALYSIS...................................................................3

2.1 Statements of Profit or loss....................................................................................................3

2.2 Balance Sheet Statement........................................................................................................6

2.3 Cash Flow Statement.............................................................................................................7

PART 3: INVESTMENT APPRAISAL..........................................................................................9

3.1.a Management Forecast ........................................................................................................9

3.1.b Investment Appraisal Techniques ....................................................................................10

3.2. Sources of Finance .............................................................................................................11

REFERENCES..............................................................................................................................13

EXECUTIVE SUMMARY.............................................................................................................1

PART 1: INDUSTRY REVIEW.....................................................................................................1

PART 2 : BUSINESS PERFORMANCE ANALYSIS...................................................................3

2.1 Statements of Profit or loss....................................................................................................3

2.2 Balance Sheet Statement........................................................................................................6

2.3 Cash Flow Statement.............................................................................................................7

PART 3: INVESTMENT APPRAISAL..........................................................................................9

3.1.a Management Forecast ........................................................................................................9

3.1.b Investment Appraisal Techniques ....................................................................................10

3.2. Sources of Finance .............................................................................................................11

REFERENCES..............................................................................................................................13

EXECUTIVE SUMMARY

Financial decision making is considered to be one of the most effective procedure which

is highly responsible for making strategic decision associated with the equities, liabilities and

stakeholders of the company. It s considered to be an effective tool in order to maximize the

profitability of the company (Lu, Won and Cheng, 2016). Financial decision making is

considered to be very useful in gaining relevant in formation by effectively analysing the

financial reports of the company. This in turn helps in making investment decision, determine

financial position which in turn helps in making strategic decision. Starbucks is an American

coffee company which is headquartered in Seattle, Washington. It was founded in the year 1971

and has approximately 988 stores in UK.

Roast Ltd. is considered to be in a very strong position because it has enough financial

capital. This in turn influences Starbucks to acquire Roast Ltd.

The net profit margin of the company is increasing exceptionally which in turn states

that, Starbucks must acquire Roast Ltd.

Roast Ltd expansion of business operations in Romania is considered to be an effective

opportunity for the Starbucks to carry out business across several parts of the globe.

The profit of the company has been increasing which is one of the key reason for the

Starbucks to effectively carry out business operations.

The return on equity of the company is increasing which in turn indicates the better

measure for the efficiency. This is one of the effective measure for Starbucks to acquire

Roast Ltd.

The return on capital employed of the Roast Ltd is increasing which states that the

profitability of the company is increasing. This is one of the effective aspect for

Starbucks to acquire Roast Ltd.

The current asset of the company is average which states company have enough cash to

mitigate its short term liabilities.

PART 1: INDUSTRY REVIEW

Roast Ltd is an independent chain which was established in UK, in the year 2008. It has

opened its first chain in Romania. They tend to focus on employing local people and also work

towards building a popular cafe culture which in turn leads to higher operational growth.

Britain is considered to be the nation of the coffee drinkers (Bradley and Botchway,

1

Financial decision making is considered to be one of the most effective procedure which

is highly responsible for making strategic decision associated with the equities, liabilities and

stakeholders of the company. It s considered to be an effective tool in order to maximize the

profitability of the company (Lu, Won and Cheng, 2016). Financial decision making is

considered to be very useful in gaining relevant in formation by effectively analysing the

financial reports of the company. This in turn helps in making investment decision, determine

financial position which in turn helps in making strategic decision. Starbucks is an American

coffee company which is headquartered in Seattle, Washington. It was founded in the year 1971

and has approximately 988 stores in UK.

Roast Ltd. is considered to be in a very strong position because it has enough financial

capital. This in turn influences Starbucks to acquire Roast Ltd.

The net profit margin of the company is increasing exceptionally which in turn states

that, Starbucks must acquire Roast Ltd.

Roast Ltd expansion of business operations in Romania is considered to be an effective

opportunity for the Starbucks to carry out business across several parts of the globe.

The profit of the company has been increasing which is one of the key reason for the

Starbucks to effectively carry out business operations.

The return on equity of the company is increasing which in turn indicates the better

measure for the efficiency. This is one of the effective measure for Starbucks to acquire

Roast Ltd.

The return on capital employed of the Roast Ltd is increasing which states that the

profitability of the company is increasing. This is one of the effective aspect for

Starbucks to acquire Roast Ltd.

The current asset of the company is average which states company have enough cash to

mitigate its short term liabilities.

PART 1: INDUSTRY REVIEW

Roast Ltd is an independent chain which was established in UK, in the year 2008. It has

opened its first chain in Romania. They tend to focus on employing local people and also work

towards building a popular cafe culture which in turn leads to higher operational growth.

Britain is considered to be the nation of the coffee drinkers (Bradley and Botchway,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2018). The coffee industry of the UK tends to be the fifth largest coffee consumer marketplace in

Europe. The British coffee market tends to grow at approximately 10% every year (The

Economic Impact of the Coffee Industry, 2019).

The expected retail sales of the coffee in UK is about to reach 69 million Kg in the year

2019.

The UK population consume around 70 million cups a day, around which 65% of which

is consumed at home, 10% at restaurants, bars and the remaining 25% at work.

Around £17.7 billion of the UK coffee market is contributed into the UK economy

(Morland, 2017).

The total turnover of the coffee products in the food industry is £3.2 billion in the year

2017.

The UK coffee market supports around 210,325 jobs which is very beneficial for the

growth of the economy (Ferreira, 2018).

Key players within coffee house industry

Costa Ltd: It is a British multinational coffee house company which was founded in 1971

and is headquartered in Dunstable, Bedfordshire. As per May 2018, Costa coffee tends to operate

high number of coffee outlets i.e., 2467 outlets in the UK. On the other hand overseas it tends to

operate 1412 stores in across 31 countries.

Starbucks: It is an American coffee company which was founded in the year 1971 and is

headquartered in Seattle, Washington. As per the year 2018, Starbucks tends to have a total of

around 988 stores in UK. The key opportunity associated with the Starbucks is that, it has the

possibility to expand its business operations across the globe in various diversified market.

Caffe Nero group: It is a European style private limited company which was founded in

the year 1997 and is headquartered in London, England. Caffe Nero group has around 566

outlets in the United Kingdom. It has business opeartions in acros s 11 vountries by running

around 1000 coffee houses in UK, Turkey, Ireland, Croatia, UAE, Oman, US, Cyprus, Poland

and Sweden (Bradley and Botchway, 2018).

Key challenges faced

The major challenge faced by the coffee industry is rise in the rents and cost of the

property which in turn has de-established several high street brands.

2

Europe. The British coffee market tends to grow at approximately 10% every year (The

Economic Impact of the Coffee Industry, 2019).

The expected retail sales of the coffee in UK is about to reach 69 million Kg in the year

2019.

The UK population consume around 70 million cups a day, around which 65% of which

is consumed at home, 10% at restaurants, bars and the remaining 25% at work.

Around £17.7 billion of the UK coffee market is contributed into the UK economy

(Morland, 2017).

The total turnover of the coffee products in the food industry is £3.2 billion in the year

2017.

The UK coffee market supports around 210,325 jobs which is very beneficial for the

growth of the economy (Ferreira, 2018).

Key players within coffee house industry

Costa Ltd: It is a British multinational coffee house company which was founded in 1971

and is headquartered in Dunstable, Bedfordshire. As per May 2018, Costa coffee tends to operate

high number of coffee outlets i.e., 2467 outlets in the UK. On the other hand overseas it tends to

operate 1412 stores in across 31 countries.

Starbucks: It is an American coffee company which was founded in the year 1971 and is

headquartered in Seattle, Washington. As per the year 2018, Starbucks tends to have a total of

around 988 stores in UK. The key opportunity associated with the Starbucks is that, it has the

possibility to expand its business operations across the globe in various diversified market.

Caffe Nero group: It is a European style private limited company which was founded in

the year 1997 and is headquartered in London, England. Caffe Nero group has around 566

outlets in the United Kingdom. It has business opeartions in acros s 11 vountries by running

around 1000 coffee houses in UK, Turkey, Ireland, Croatia, UAE, Oman, US, Cyprus, Poland

and Sweden (Bradley and Botchway, 2018).

Key challenges faced

The major challenge faced by the coffee industry is rise in the rents and cost of the

property which in turn has de-established several high street brands.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Strongly maintaining the customer footfall is considered to be vital for the boost in the

sales of the coffee house chain. Rise in the price of material associated with the coffee industry results in major challenge

for the business.

Key opportunities

The key opportunity with the coffee industry in UK is that, consumers tend to spend more

on food industry (Yang and et.al., 2016).

Higher growth in the coffee industry results in high degree of employment opportunities

for the individuals.

High degree of prominent rise in the UK coffee industry helps in expansion of business

operations within various developing countries.

PART 2 : BUSINESS PERFORMANCE ANALYSIS

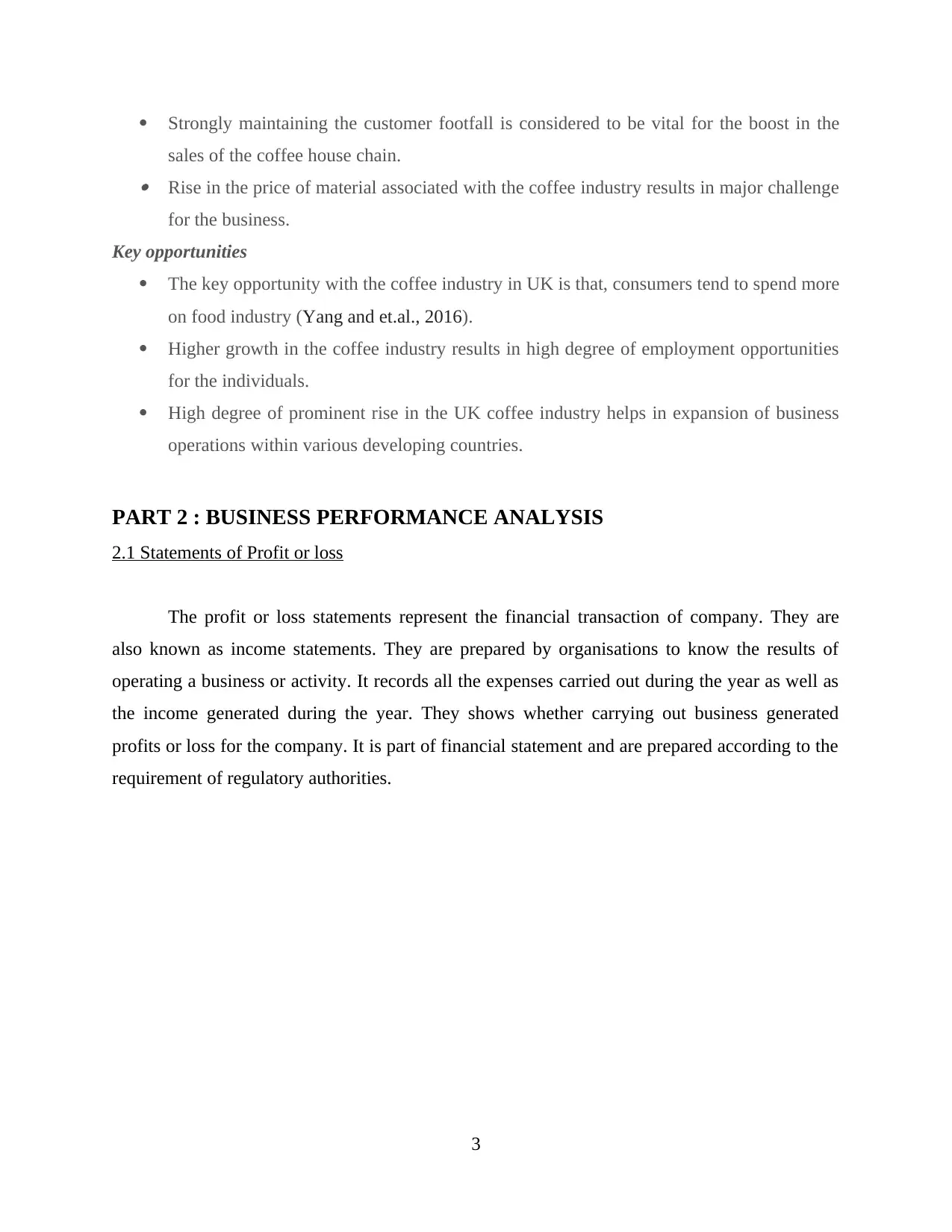

2.1 Statements of Profit or loss

The profit or loss statements represent the financial transaction of company. They are

also known as income statements. They are prepared by organisations to know the results of

operating a business or activity. It records all the expenses carried out during the year as well as

the income generated during the year. They shows whether carrying out business generated

profits or loss for the company. It is part of financial statement and are prepared according to the

requirement of regulatory authorities.

3

sales of the coffee house chain. Rise in the price of material associated with the coffee industry results in major challenge

for the business.

Key opportunities

The key opportunity with the coffee industry in UK is that, consumers tend to spend more

on food industry (Yang and et.al., 2016).

Higher growth in the coffee industry results in high degree of employment opportunities

for the individuals.

High degree of prominent rise in the UK coffee industry helps in expansion of business

operations within various developing countries.

PART 2 : BUSINESS PERFORMANCE ANALYSIS

2.1 Statements of Profit or loss

The profit or loss statements represent the financial transaction of company. They are

also known as income statements. They are prepared by organisations to know the results of

operating a business or activity. It records all the expenses carried out during the year as well as

the income generated during the year. They shows whether carrying out business generated

profits or loss for the company. It is part of financial statement and are prepared according to the

requirement of regulatory authorities.

3

The profit or loss statement of Harridge ltd represents significant profit for the current

year in comparison to last year. Company earned profit of £ 81 during current year that was £36

last year. This shows that business have made significant growth from last year. Company along

with profits should also have growth in the business. For attracting the new investors it is

important to show the growth in the business. There has been increase of 25% in its revenues

from last year. This is seen after the new strategies adopted by the company for promoting the

sales and revenues. Company this year has earned other operating income of £60 that was not

earned last year this has raised the profit levels for the year. Operating expenses have not

increased with the same proportion as that of revenues as it has saved the cost of remuneration of

directors. On of the director has left and its roles and responsibilities will be managed by the

chief executive director without any additional pay. Also the legal cost related to the purchase of

property were paid in last year therefore the company had reduced legal costs this year. Business

has shown improved performance which could be seen through its revenues and efficient control

over its operating expenses.

4

year in comparison to last year. Company earned profit of £ 81 during current year that was £36

last year. This shows that business have made significant growth from last year. Company along

with profits should also have growth in the business. For attracting the new investors it is

important to show the growth in the business. There has been increase of 25% in its revenues

from last year. This is seen after the new strategies adopted by the company for promoting the

sales and revenues. Company this year has earned other operating income of £60 that was not

earned last year this has raised the profit levels for the year. Operating expenses have not

increased with the same proportion as that of revenues as it has saved the cost of remuneration of

directors. On of the director has left and its roles and responsibilities will be managed by the

chief executive director without any additional pay. Also the legal cost related to the purchase of

property were paid in last year therefore the company had reduced legal costs this year. Business

has shown improved performance which could be seen through its revenues and efficient control

over its operating expenses.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

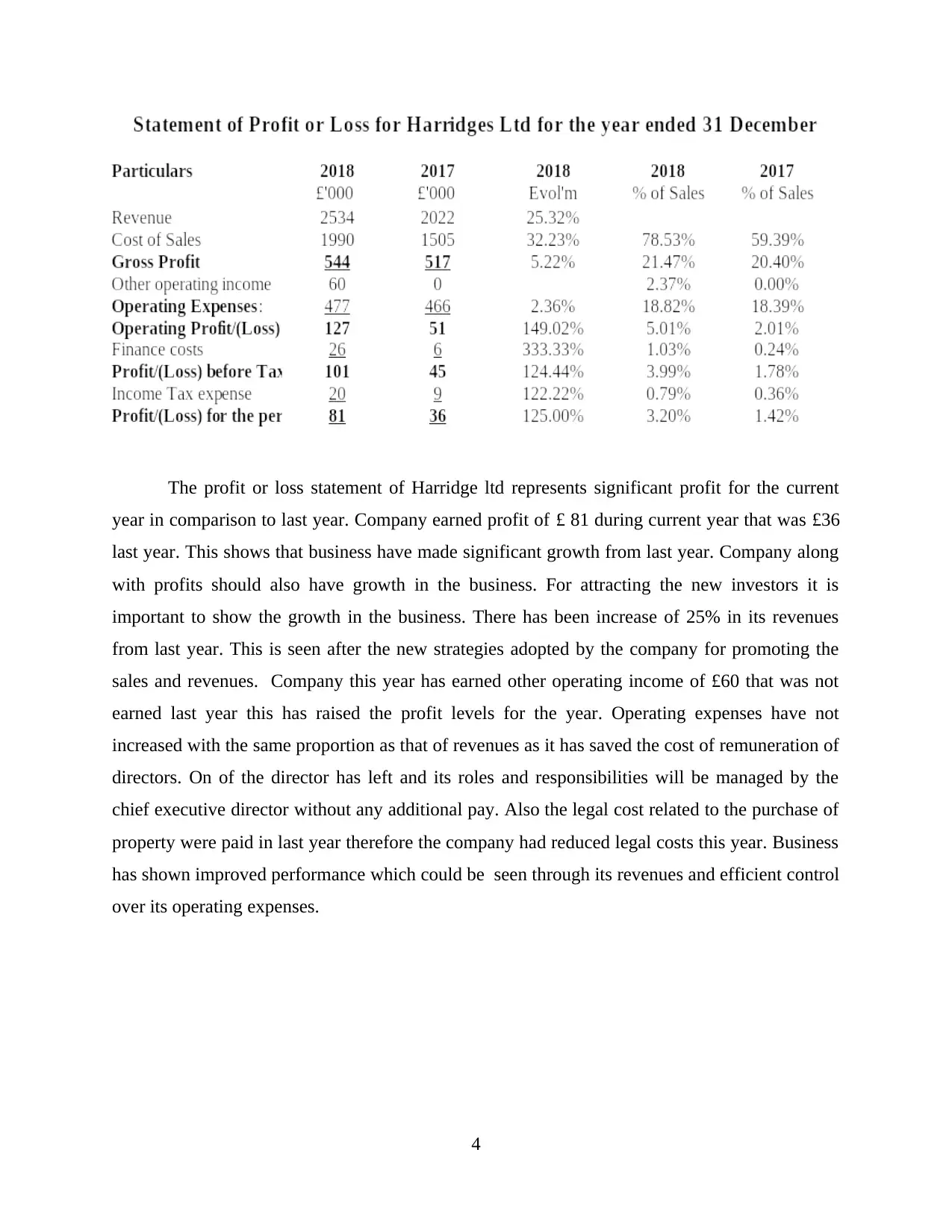

Ratio analysis is used for identifying the financial health of organisation. The financial

performance of the business can be analysed using profitability ratios. This ratio helps in

measuring the health and position of company. Theses ratios include ROCE, ROE, Gross profit

margin and net profit margins.

Return on capital employed is used for measuring the returns generated utilising the

resources of company. Capital is employed in the business for earning maximum possible

returns. ROCE of company is 8.80 and has shown a significant increase of 75.50%. Company

has not high returns over the capital employed as per the industry standards. Also the significant

cause of high return is other operating income (Hausmann, Kokkinaki and Leng, 2019). The

returns should be high as it shows the efficiency of company in managing its operations.

Return on equity is calculated for measuring the return that company is able to generate

over its equity. Equity refers to the investment in share capital and retained earnings. This ratio is

similar to ROCE as both measures the efficiency of company to to effectively utilise its

resources. Investments are made for earning reasonable rate of return therefore it is important for

company to earn reasonable rate of return over its equity. It has earned return of 9.42% for

present year which was 4.62%.

Gross profit and net profit margins are for assessing the efficiency of business in

managing its operating costs. Gross profit margin of company is 21.47% which was 25.42% last

year. The scale of gross margin has sloped downward despite of increase in revenues and

incomes (Kogadeeva and Zamboni, 2016). The reason behind decrease is increase in cost of

imported raw material. There has been rise in prices of raw material and the labour charges. The

5

performance of the business can be analysed using profitability ratios. This ratio helps in

measuring the health and position of company. Theses ratios include ROCE, ROE, Gross profit

margin and net profit margins.

Return on capital employed is used for measuring the returns generated utilising the

resources of company. Capital is employed in the business for earning maximum possible

returns. ROCE of company is 8.80 and has shown a significant increase of 75.50%. Company

has not high returns over the capital employed as per the industry standards. Also the significant

cause of high return is other operating income (Hausmann, Kokkinaki and Leng, 2019). The

returns should be high as it shows the efficiency of company in managing its operations.

Return on equity is calculated for measuring the return that company is able to generate

over its equity. Equity refers to the investment in share capital and retained earnings. This ratio is

similar to ROCE as both measures the efficiency of company to to effectively utilise its

resources. Investments are made for earning reasonable rate of return therefore it is important for

company to earn reasonable rate of return over its equity. It has earned return of 9.42% for

present year which was 4.62%.

Gross profit and net profit margins are for assessing the efficiency of business in

managing its operating costs. Gross profit margin of company is 21.47% which was 25.42% last

year. The scale of gross margin has sloped downward despite of increase in revenues and

incomes (Kogadeeva and Zamboni, 2016). The reason behind decrease is increase in cost of

imported raw material. There has been rise in prices of raw material and the labour charges. The

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increase was higher than the proportionate increase in revenues that let the gross profit to move

downwards.

Net profit margin of company has increased from last year to 5.02% from last year. This

also shows the significant increase in the profits. Net profits is arrived after the other operations

that are essential for running the business are met like salaries, administration and selling

expenses. Companies must use adequate measures for controlling the costs so that net profits of

company are high. Also the revenues should be given focus using appropriate promotional

strategies for boosting the sales (Zavadskas and et.al., 2018).

2.2 Balance Sheet Statement

Balance is prepared for presenting all the assets and liabilities of business. It is prepared

for presenting the wealth and financial position of the business. Company is required to include

all the items of assets and liabilities under their respective heads. All the contingent liabilities are

required to be shown in the notes and provisions should be made for material amount. Investors

use balance sheet for assessing the financial health of business and the risks associated before

investing in the company.

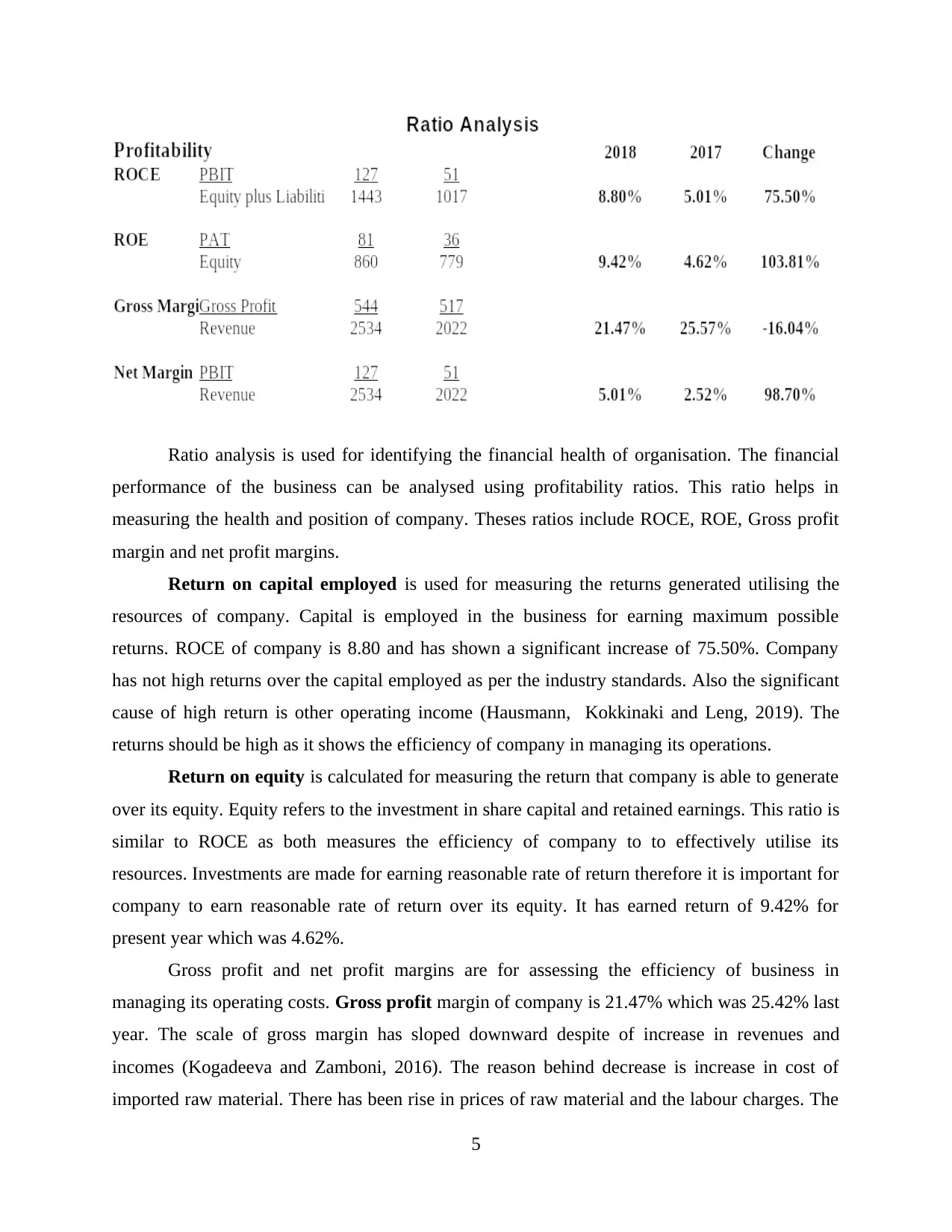

The liquidity ratios measures the liquidity of company whether company is able to meet

its obligations using the available resources. It is essential for the enterprises to have strong

liquidity position for running the business smoothly without interruptions.

Current ratio of company is 1.45 for the year that has declined from 2.51. current ratio

represents the ability of company to meet its shot term obligations using the current assets. If the

company is not able to meet its short term obligation than the business operations will be

affected. It is essential to have enough assets so that current liabilities do not affect the position

of company (Choi and et.al., 2018). Company can improve the current ratio by using the long

tern debts instead of short term borrowings for meeting the capital requirements. Ration has

6

downwards.

Net profit margin of company has increased from last year to 5.02% from last year. This

also shows the significant increase in the profits. Net profits is arrived after the other operations

that are essential for running the business are met like salaries, administration and selling

expenses. Companies must use adequate measures for controlling the costs so that net profits of

company are high. Also the revenues should be given focus using appropriate promotional

strategies for boosting the sales (Zavadskas and et.al., 2018).

2.2 Balance Sheet Statement

Balance is prepared for presenting all the assets and liabilities of business. It is prepared

for presenting the wealth and financial position of the business. Company is required to include

all the items of assets and liabilities under their respective heads. All the contingent liabilities are

required to be shown in the notes and provisions should be made for material amount. Investors

use balance sheet for assessing the financial health of business and the risks associated before

investing in the company.

The liquidity ratios measures the liquidity of company whether company is able to meet

its obligations using the available resources. It is essential for the enterprises to have strong

liquidity position for running the business smoothly without interruptions.

Current ratio of company is 1.45 for the year that has declined from 2.51. current ratio

represents the ability of company to meet its shot term obligations using the current assets. If the

company is not able to meet its short term obligation than the business operations will be

affected. It is essential to have enough assets so that current liabilities do not affect the position

of company (Choi and et.al., 2018). Company can improve the current ratio by using the long

tern debts instead of short term borrowings for meeting the capital requirements. Ration has

6

declined as cash position of the company is negative and has given rise to bank overdraft

increasing the short term liability.

Quick Ratios measures the liquidity without including inventory in its current assets. As

the inventory cannot realise immediate cash when sold in market. The Quick ratio of company is

0.48 decrease is high due to the inventory levels and bank overdraft in current year. These should

be improved as early as possible as the stakeholders are influenced because of these ratios.

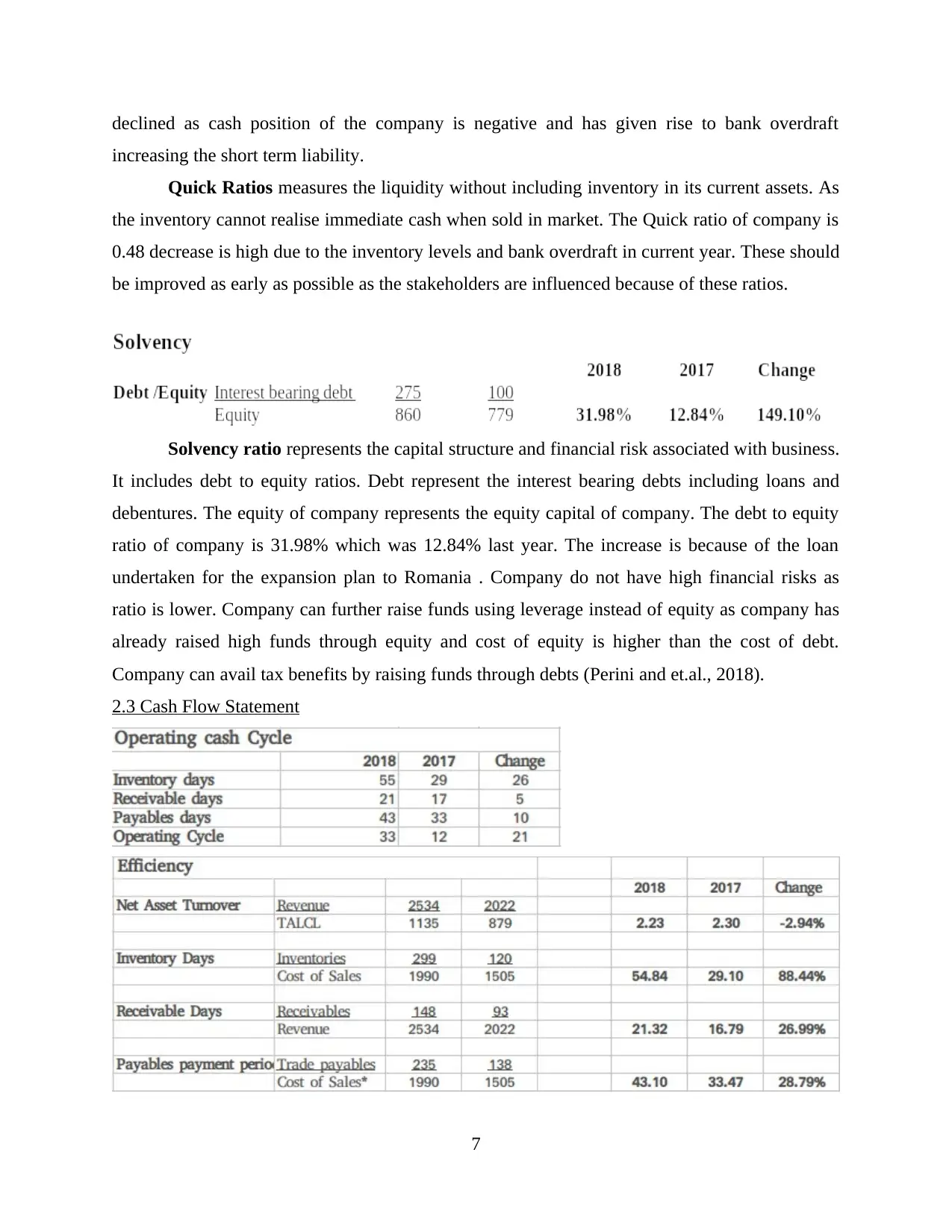

Solvency ratio represents the capital structure and financial risk associated with business.

It includes debt to equity ratios. Debt represent the interest bearing debts including loans and

debentures. The equity of company represents the equity capital of company. The debt to equity

ratio of company is 31.98% which was 12.84% last year. The increase is because of the loan

undertaken for the expansion plan to Romania . Company do not have high financial risks as

ratio is lower. Company can further raise funds using leverage instead of equity as company has

already raised high funds through equity and cost of equity is higher than the cost of debt.

Company can avail tax benefits by raising funds through debts (Perini and et.al., 2018).

2.3 Cash Flow Statement

7

increasing the short term liability.

Quick Ratios measures the liquidity without including inventory in its current assets. As

the inventory cannot realise immediate cash when sold in market. The Quick ratio of company is

0.48 decrease is high due to the inventory levels and bank overdraft in current year. These should

be improved as early as possible as the stakeholders are influenced because of these ratios.

Solvency ratio represents the capital structure and financial risk associated with business.

It includes debt to equity ratios. Debt represent the interest bearing debts including loans and

debentures. The equity of company represents the equity capital of company. The debt to equity

ratio of company is 31.98% which was 12.84% last year. The increase is because of the loan

undertaken for the expansion plan to Romania . Company do not have high financial risks as

ratio is lower. Company can further raise funds using leverage instead of equity as company has

already raised high funds through equity and cost of equity is higher than the cost of debt.

Company can avail tax benefits by raising funds through debts (Perini and et.al., 2018).

2.3 Cash Flow Statement

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: Cash flow statement is referred to as a financial report which is very

useful in managing the cash flows of the company. It tends to state the fiscal position of the

organisation. The net operating cash flow from the operating activity for the year ended 2018 is

-£24,000. A negative cash flow from operating activities tend to state that, the company is not in

a good position to pay off its bills without raising any additional capital. Negative cash flow

from operating activity tends to reflect, poor management of the income and expenses (Lu, Won

and Cheng, 2016). The net investing cash flow from the for the year ended 2018 is -£358'000. A

negative cash flow from investing activities tend to state that, significant amount of money of the

business has been invested in the long term plans of the organization. The net cash flow from the

financing activity for the year ended 2018 is £175'000. A positive cash flow from financing

activities tend to state that, large amount of money has been flowing into the business (Knežević

and Mitrović, 2018). This in turn largely increases the assets of the company. It has been

interpreted that, the net decrease in the cash and cash equivalents of the company is -£207,000.

The negative cash and cash equivalent states that, more money is flowing out of the business

than into the business.

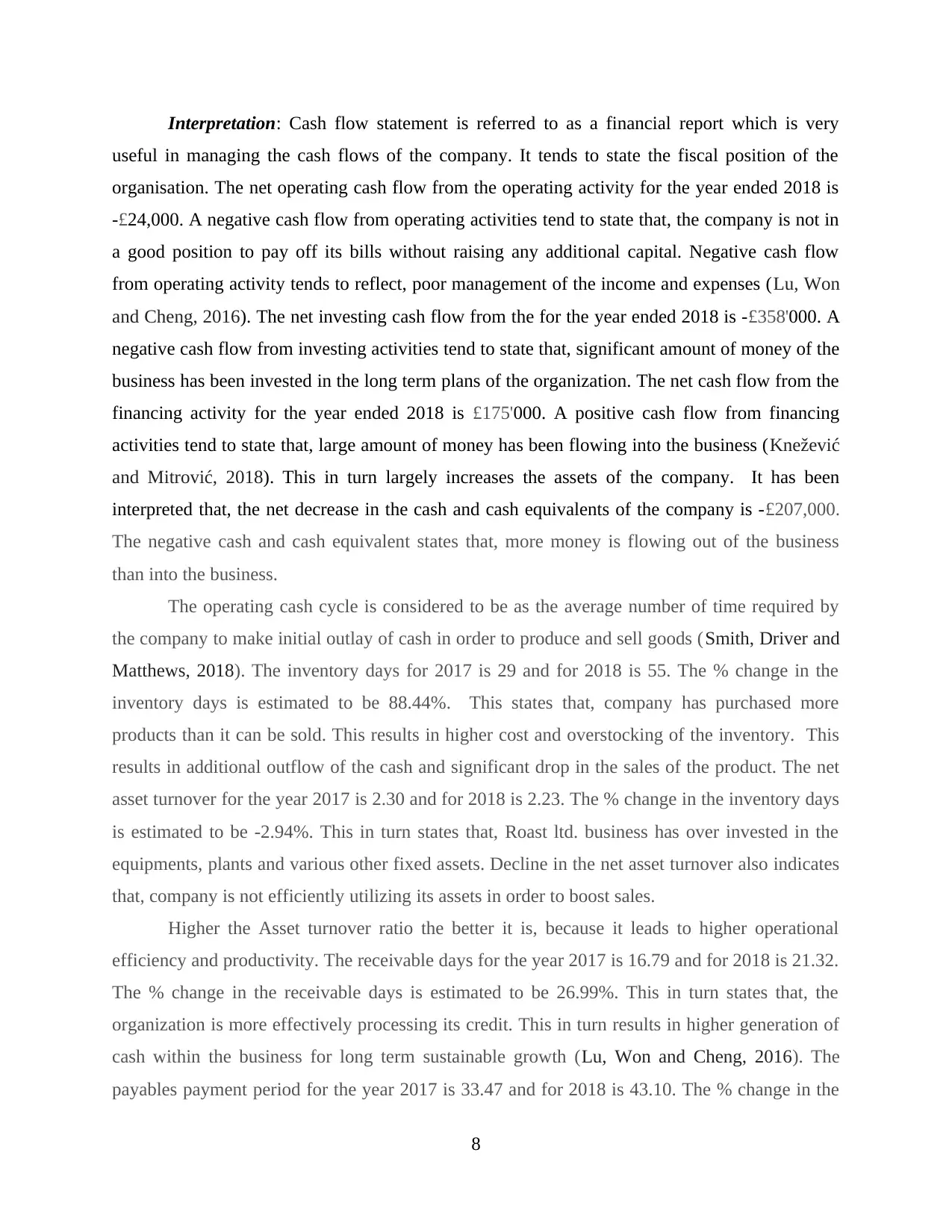

The operating cash cycle is considered to be as the average number of time required by

the company to make initial outlay of cash in order to produce and sell goods (Smith, Driver and

Matthews, 2018). The inventory days for 2017 is 29 and for 2018 is 55. The % change in the

inventory days is estimated to be 88.44%. This states that, company has purchased more

products than it can be sold. This results in higher cost and overstocking of the inventory. This

results in additional outflow of the cash and significant drop in the sales of the product. The net

asset turnover for the year 2017 is 2.30 and for 2018 is 2.23. The % change in the inventory days

is estimated to be -2.94%. This in turn states that, Roast ltd. business has over invested in the

equipments, plants and various other fixed assets. Decline in the net asset turnover also indicates

that, company is not efficiently utilizing its assets in order to boost sales.

Higher the Asset turnover ratio the better it is, because it leads to higher operational

efficiency and productivity. The receivable days for the year 2017 is 16.79 and for 2018 is 21.32.

The % change in the receivable days is estimated to be 26.99%. This in turn states that, the

organization is more effectively processing its credit. This in turn results in higher generation of

cash within the business for long term sustainable growth (Lu, Won and Cheng, 2016). The

payables payment period for the year 2017 is 33.47 and for 2018 is 43.10. The % change in the

8

useful in managing the cash flows of the company. It tends to state the fiscal position of the

organisation. The net operating cash flow from the operating activity for the year ended 2018 is

-£24,000. A negative cash flow from operating activities tend to state that, the company is not in

a good position to pay off its bills without raising any additional capital. Negative cash flow

from operating activity tends to reflect, poor management of the income and expenses (Lu, Won

and Cheng, 2016). The net investing cash flow from the for the year ended 2018 is -£358'000. A

negative cash flow from investing activities tend to state that, significant amount of money of the

business has been invested in the long term plans of the organization. The net cash flow from the

financing activity for the year ended 2018 is £175'000. A positive cash flow from financing

activities tend to state that, large amount of money has been flowing into the business (Knežević

and Mitrović, 2018). This in turn largely increases the assets of the company. It has been

interpreted that, the net decrease in the cash and cash equivalents of the company is -£207,000.

The negative cash and cash equivalent states that, more money is flowing out of the business

than into the business.

The operating cash cycle is considered to be as the average number of time required by

the company to make initial outlay of cash in order to produce and sell goods (Smith, Driver and

Matthews, 2018). The inventory days for 2017 is 29 and for 2018 is 55. The % change in the

inventory days is estimated to be 88.44%. This states that, company has purchased more

products than it can be sold. This results in higher cost and overstocking of the inventory. This

results in additional outflow of the cash and significant drop in the sales of the product. The net

asset turnover for the year 2017 is 2.30 and for 2018 is 2.23. The % change in the inventory days

is estimated to be -2.94%. This in turn states that, Roast ltd. business has over invested in the

equipments, plants and various other fixed assets. Decline in the net asset turnover also indicates

that, company is not efficiently utilizing its assets in order to boost sales.

Higher the Asset turnover ratio the better it is, because it leads to higher operational

efficiency and productivity. The receivable days for the year 2017 is 16.79 and for 2018 is 21.32.

The % change in the receivable days is estimated to be 26.99%. This in turn states that, the

organization is more effectively processing its credit. This in turn results in higher generation of

cash within the business for long term sustainable growth (Lu, Won and Cheng, 2016). The

payables payment period for the year 2017 is 33.47 and for 2018 is 43.10. The % change in the

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

payables payment period is estimated to be 28.79%. This in turn states that, company is taking

longer time to pay off the debts. This in turn results in higher interest payment and liabilities for

the company.

The dividend paid by the Roast Ltd. in the year 2017 was £30 million. But no dividend

has been paid in the year 2018 by Roast Ltd. The company made the right choice by not paying

the dividend in the year 2018 because dividend are considered to be the corporate earnings which

the company tends to pass on to the shareholders of the organization (Knežević and Mitrović,

2018). Roast Ltd. Is still growing because it wants to invest in the different projects for higher

future growth perspective. The cash and cash equivalents for the year end 2018 is -£73,000

million. Hence, negative cash and cash equivalents is considered to be as the good sign to not

pay dividend for the year 2018.

PART 3: INVESTMENT APPRAISAL

3.1.a Management Forecast

The management can make forecast about the expansion projects to Romania using

appropriate capital budgeting techniques. They are used for identifying the viability of the

projects before making the investments. Company wants to spread its business over global scale

scale and it has planned to expand over Romania by opening new outlets. Company for

expansing its business will be requiring an initial investment of £ 500 million. Management

wants to raise the funds ff the expansion. It is involving significant amount therefore the capital

budgeting techniques are used before investing in the projects. It has used techniques like NPV,

IRR and payback period for identifying the returns from investment and its profitability.

As per the forecast of management it is identified that project is viable and should be

adopted. All the outcomes are positive and show that investment will be profitable for the

company. Project involves purchase of new coffee machines that are manufactured as per the

requirements of company (Alkaraan, 2017). This machine involves Italian process of preparing

the coffee. It will be completely new Italian taste and experience to its customers. Forecast is

based over the revenues generated by the coffee outlets established in other nation. People have

accepted the taste and cafe services that helped it to generate significant revenues. Adoptions of

new project will be contributing significantly in the growth of business in Romania. The

performance of the company is significant and will help the company in raising the funds for

investments. All the property and equipments for the expansion have already been purchased by

9

longer time to pay off the debts. This in turn results in higher interest payment and liabilities for

the company.

The dividend paid by the Roast Ltd. in the year 2017 was £30 million. But no dividend

has been paid in the year 2018 by Roast Ltd. The company made the right choice by not paying

the dividend in the year 2018 because dividend are considered to be the corporate earnings which

the company tends to pass on to the shareholders of the organization (Knežević and Mitrović,

2018). Roast Ltd. Is still growing because it wants to invest in the different projects for higher

future growth perspective. The cash and cash equivalents for the year end 2018 is -£73,000

million. Hence, negative cash and cash equivalents is considered to be as the good sign to not

pay dividend for the year 2018.

PART 3: INVESTMENT APPRAISAL

3.1.a Management Forecast

The management can make forecast about the expansion projects to Romania using

appropriate capital budgeting techniques. They are used for identifying the viability of the

projects before making the investments. Company wants to spread its business over global scale

scale and it has planned to expand over Romania by opening new outlets. Company for

expansing its business will be requiring an initial investment of £ 500 million. Management

wants to raise the funds ff the expansion. It is involving significant amount therefore the capital

budgeting techniques are used before investing in the projects. It has used techniques like NPV,

IRR and payback period for identifying the returns from investment and its profitability.

As per the forecast of management it is identified that project is viable and should be

adopted. All the outcomes are positive and show that investment will be profitable for the

company. Project involves purchase of new coffee machines that are manufactured as per the

requirements of company (Alkaraan, 2017). This machine involves Italian process of preparing

the coffee. It will be completely new Italian taste and experience to its customers. Forecast is

based over the revenues generated by the coffee outlets established in other nation. People have

accepted the taste and cafe services that helped it to generate significant revenues. Adoptions of

new project will be contributing significantly in the growth of business in Romania. The

performance of the company is significant and will help the company in raising the funds for

investments. All the property and equipments for the expansion have already been purchased by

9

the business. Expenditure is to be made only for the new project and company will show growth

of 20% by adopting this project.

3.1.b Investment Appraisal Techniques

Pay Back Period

Payback period is used in capital budgeting for identifying the viability of project. This is

calculated for knowing the time within which company will be able to recover its initial cost of

investment. This project will recover the cost of investment inn 4 years. The cost will be

recovered by the company within the time fame therefore the project is viable (Harris, 2017). If

the pay back period is higher than company may refuse the project.

Advantages

It is simple and easy to understand method and therefore used by number of investors and

business before investing the funds. The method is most beneficial in case of uncertainty and business is prone to uncertainty.

Disadvantages

This method also ignores time value of money.

The method do not covers all the cash flows and ignores profitability.

Net Present Value

NPV is used by business for identifying whether adopting any business enterprises. NPV

uses discounting factor for knowing whether the cash future ash flows from the project will be

adequate for covering the cost of project. Project should be adopted by the enterprise if the NPV

after discounting the cash flows is positive. Negative cash flow represents that project will not be

profitable for the company and therefore should not be adopted (Throsby, 2016). NPV in the

present case is positive and project should be accepted.

Advantages

It represents whether company will exceed the initial investment of cash or not at present. It takes into account time value of money and factors risks.

Disadvantages

There are not set guidelines for determining required rate of return.

It cannot be used to compare projects with different sizes.

10

of 20% by adopting this project.

3.1.b Investment Appraisal Techniques

Pay Back Period

Payback period is used in capital budgeting for identifying the viability of project. This is

calculated for knowing the time within which company will be able to recover its initial cost of

investment. This project will recover the cost of investment inn 4 years. The cost will be

recovered by the company within the time fame therefore the project is viable (Harris, 2017). If

the pay back period is higher than company may refuse the project.

Advantages

It is simple and easy to understand method and therefore used by number of investors and

business before investing the funds. The method is most beneficial in case of uncertainty and business is prone to uncertainty.

Disadvantages

This method also ignores time value of money.

The method do not covers all the cash flows and ignores profitability.

Net Present Value

NPV is used by business for identifying whether adopting any business enterprises. NPV

uses discounting factor for knowing whether the cash future ash flows from the project will be

adequate for covering the cost of project. Project should be adopted by the enterprise if the NPV

after discounting the cash flows is positive. Negative cash flow represents that project will not be

profitable for the company and therefore should not be adopted (Throsby, 2016). NPV in the

present case is positive and project should be accepted.

Advantages

It represents whether company will exceed the initial investment of cash or not at present. It takes into account time value of money and factors risks.

Disadvantages

There are not set guidelines for determining required rate of return.

It cannot be used to compare projects with different sizes.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.