Statistical Analysis of Credit Card Spending and Family Size

VerifiedAdded on 2019/12/28

|30

|2296

|259

Report

AI Summary

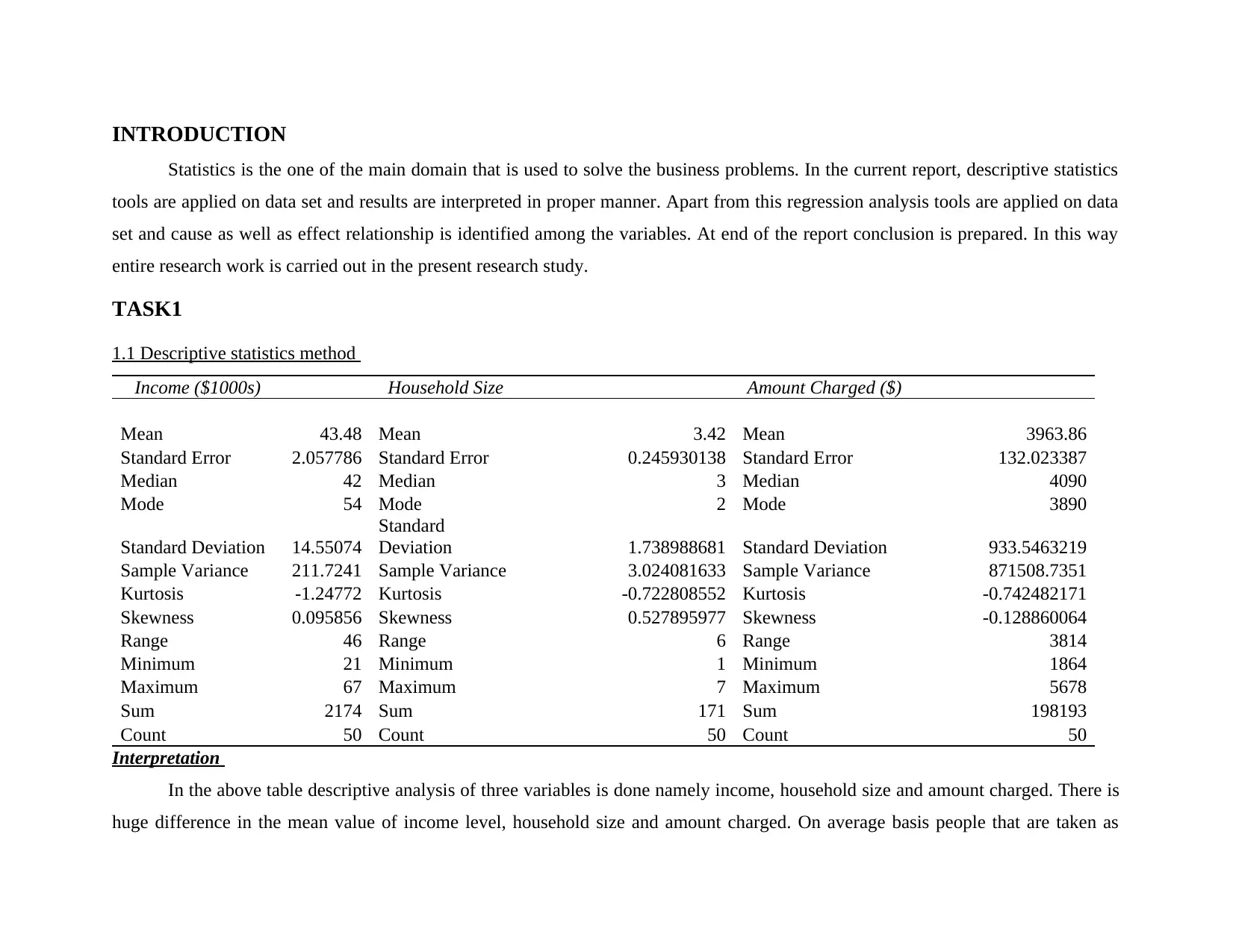

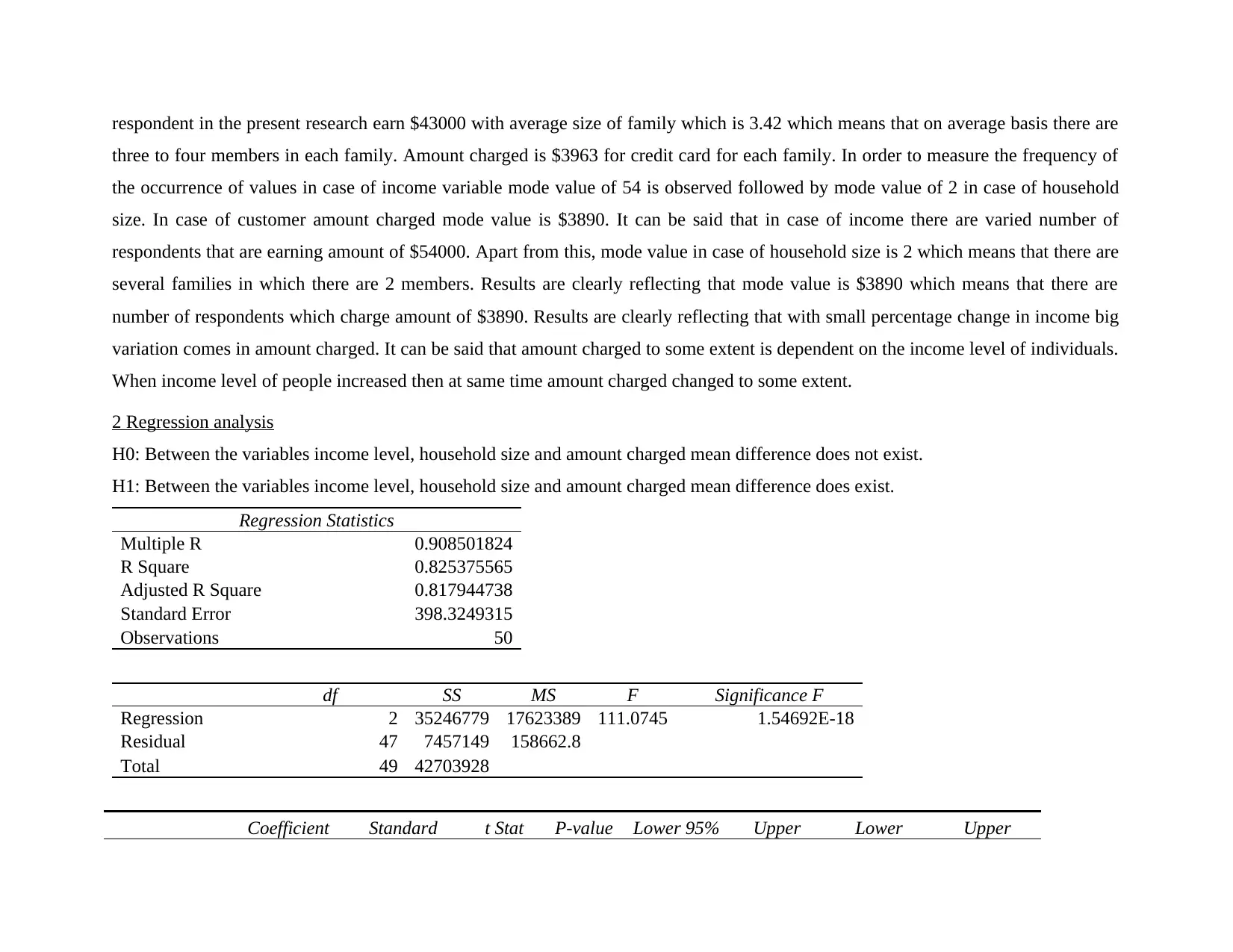

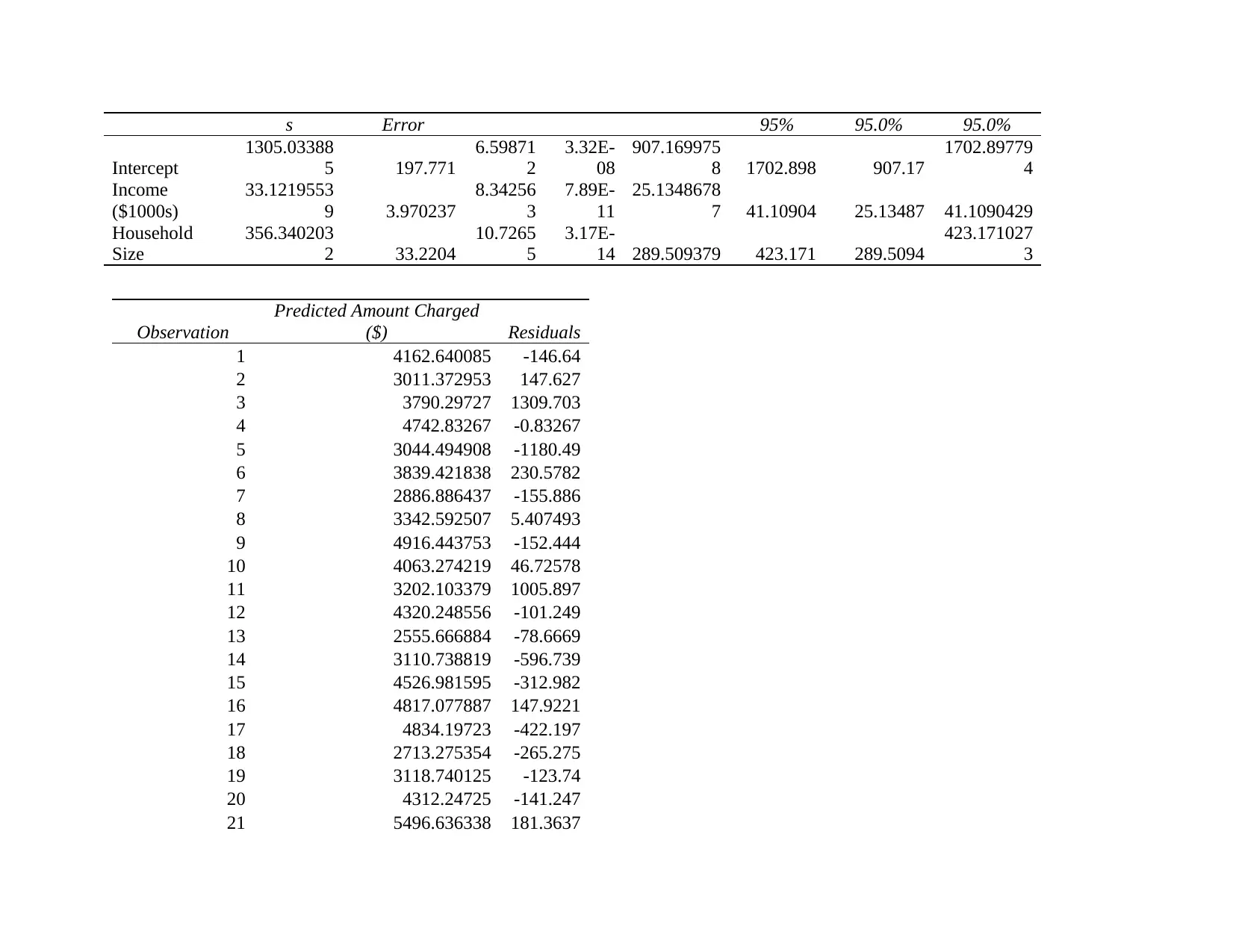

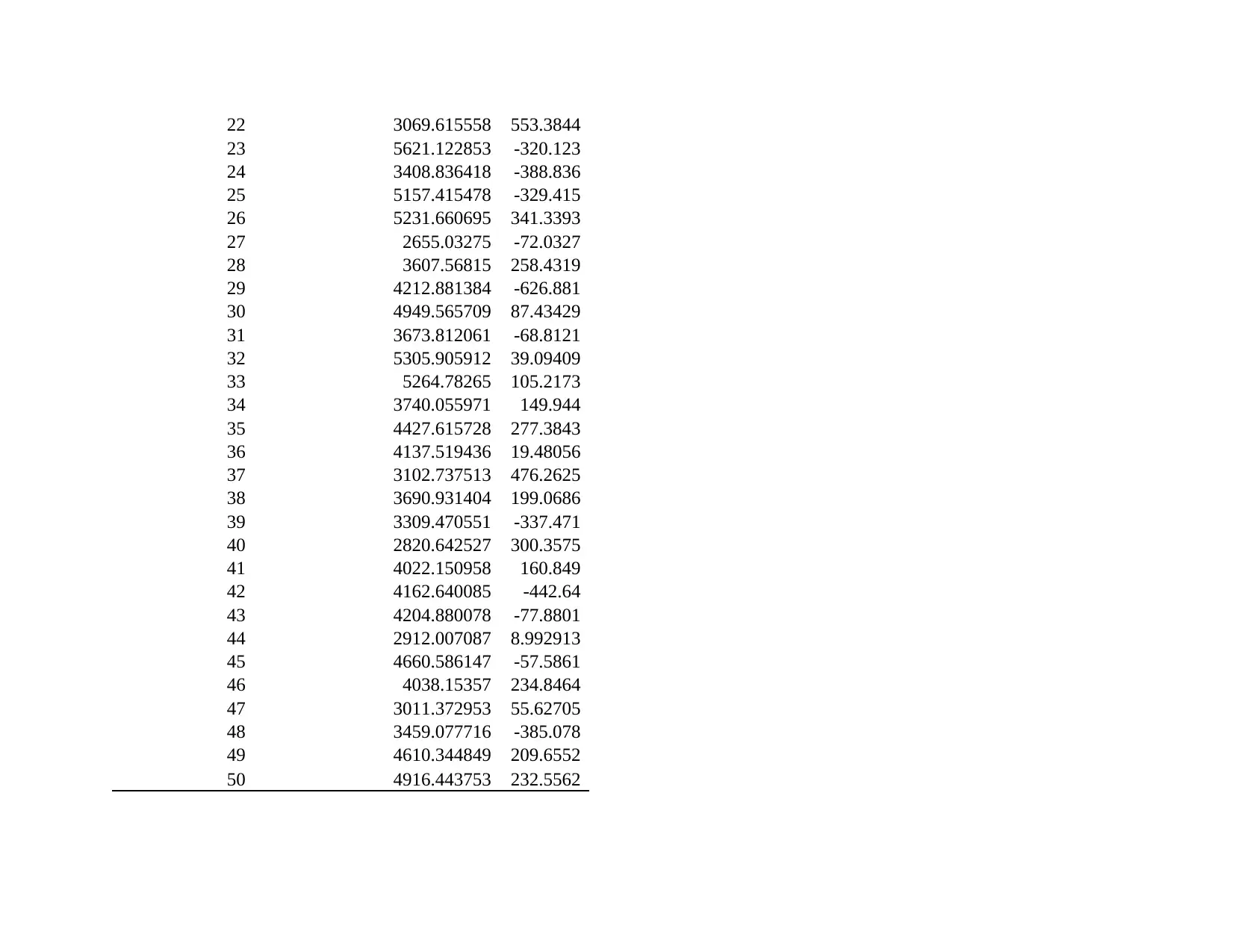

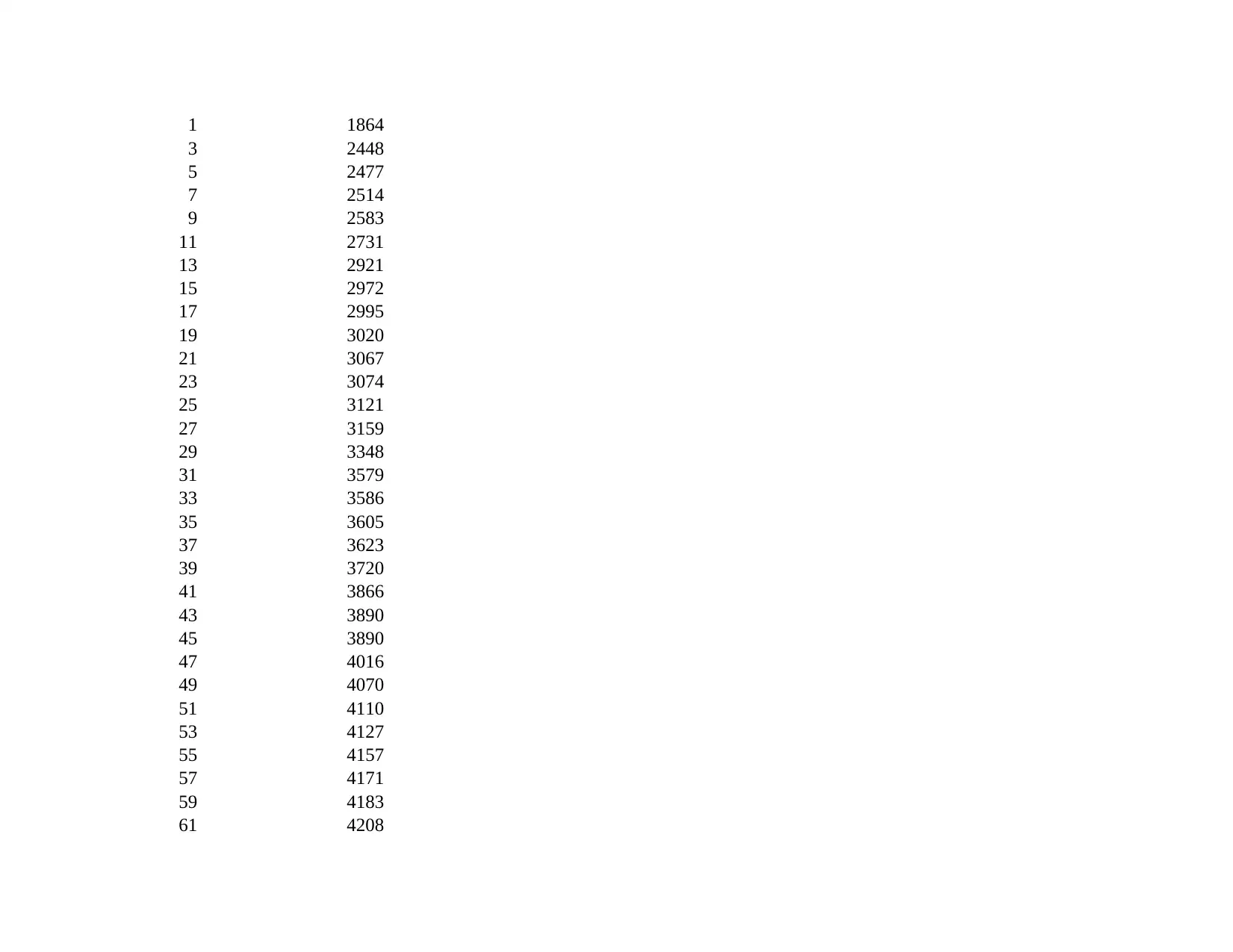

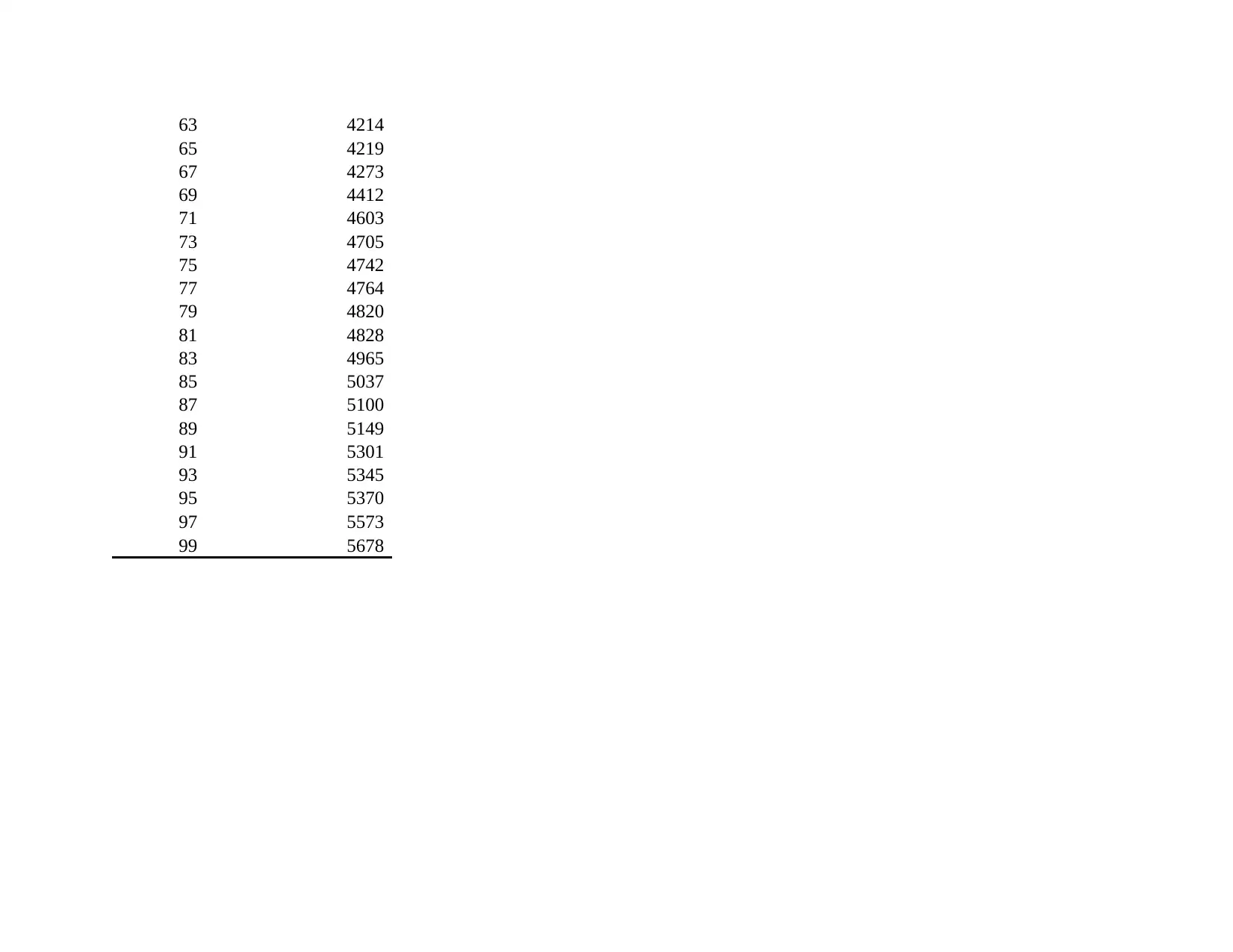

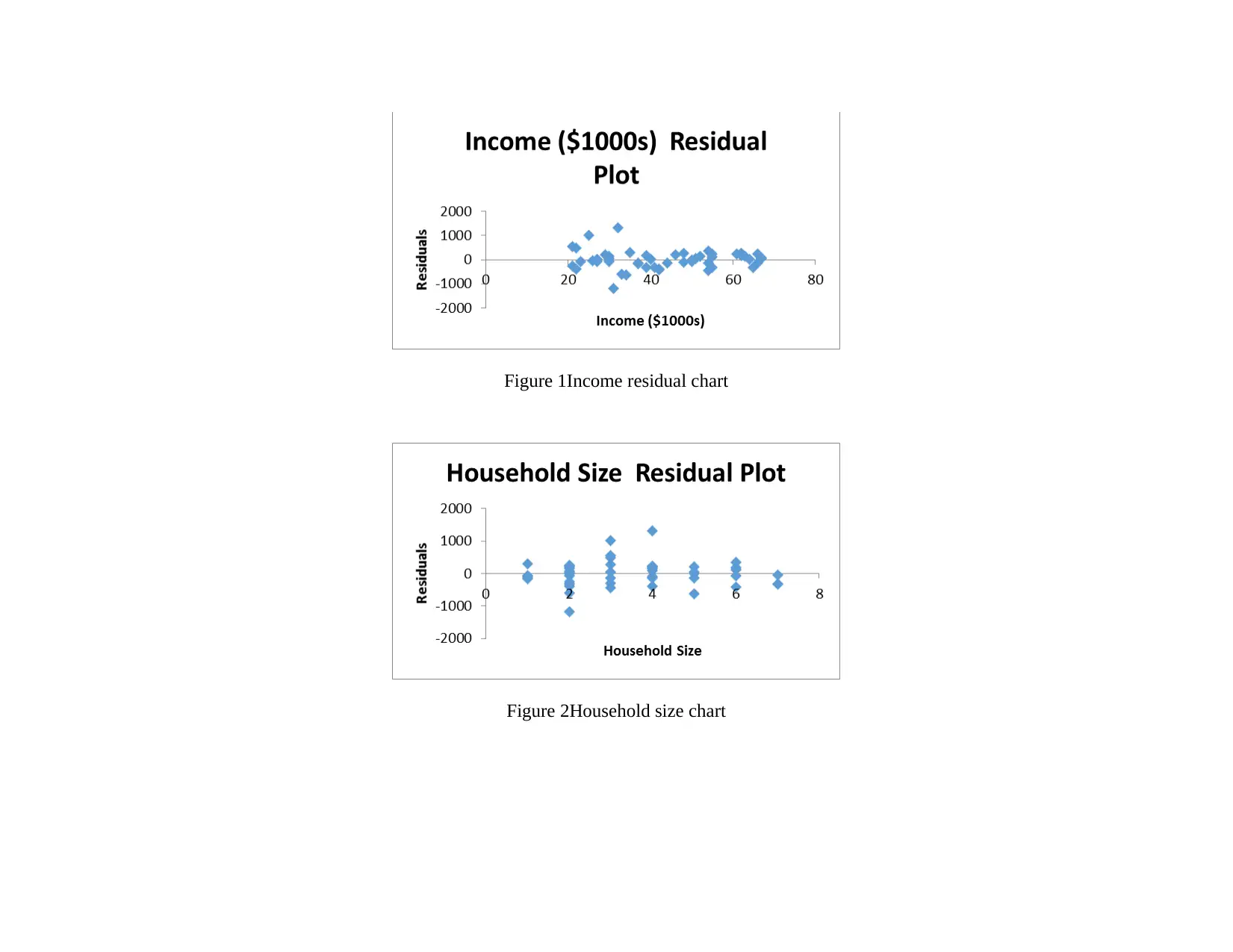

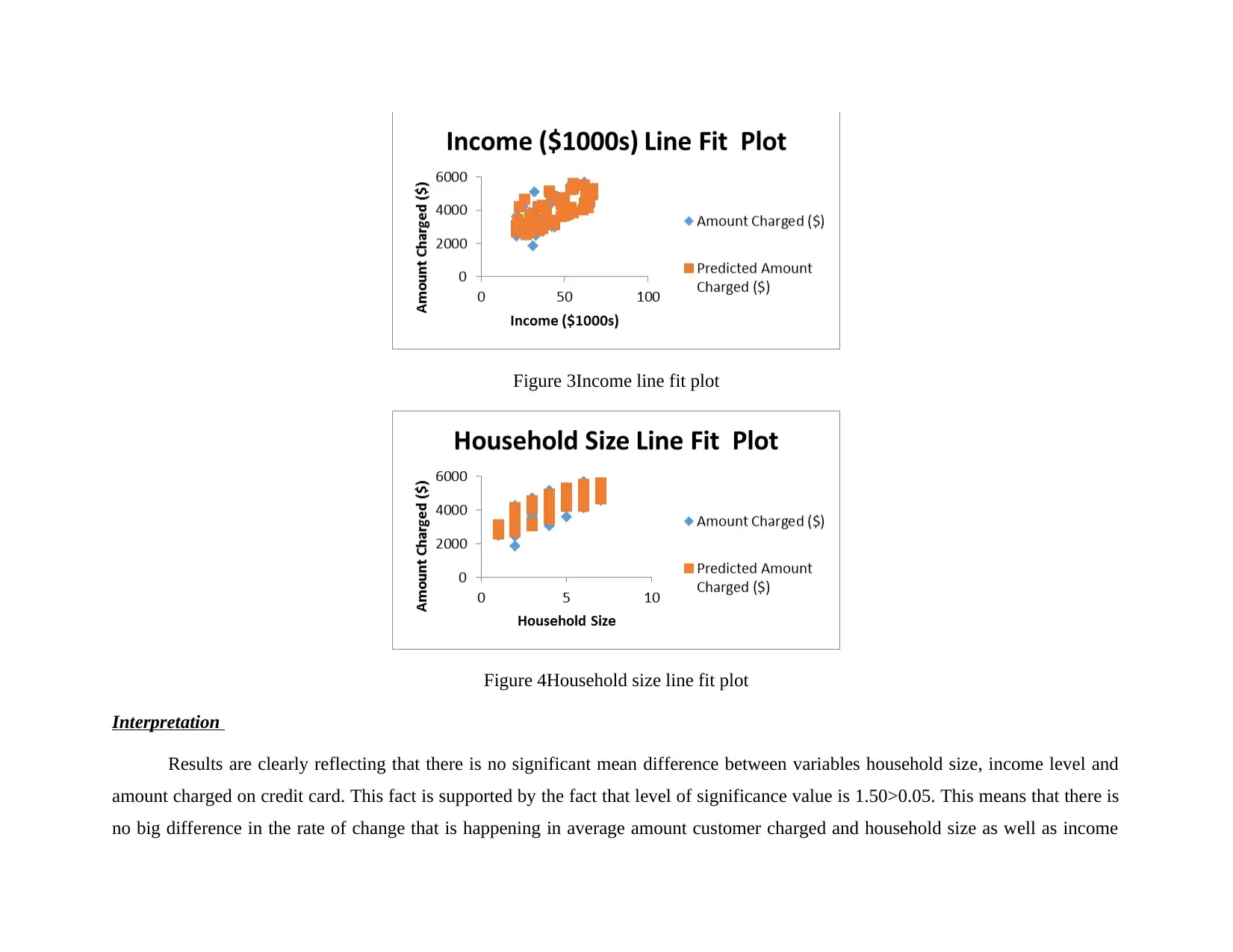

This report presents a comprehensive statistical analysis of credit card spending, household size, and income levels. The study begins with descriptive statistics, providing an overview of the mean, median, mode, and standard deviation for each variable. Regression analysis is then employed to identify the relationships between these variables, with a focus on how income and family size impact credit card charges. The report includes regression equations, interpretations of the results, and the addition of variables to refine the model. Further analysis includes histograms, descriptive statistics, and correlation analysis of exam and assignment scores. Finally, ANOVA is used to assess depression levels across different cities, with a discussion on the appropriateness of treatment methods. The findings provide valuable insights into consumer behavior and statistical methodologies.

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.