Statistical Analysis of Bitcoin and Stocks: ECON 1030

VerifiedAdded on 2023/03/20

|19

|2110

|73

Report

AI Summary

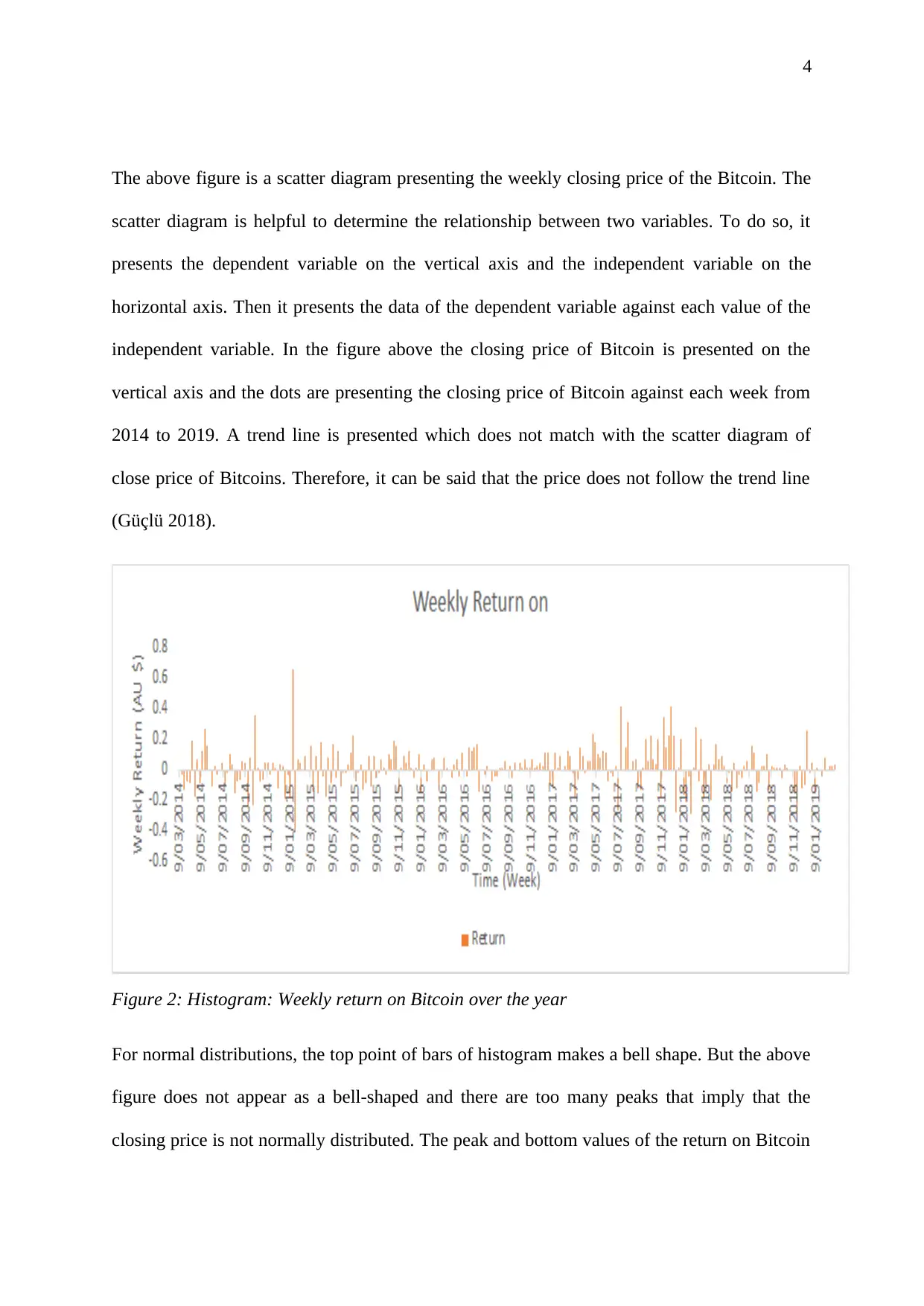

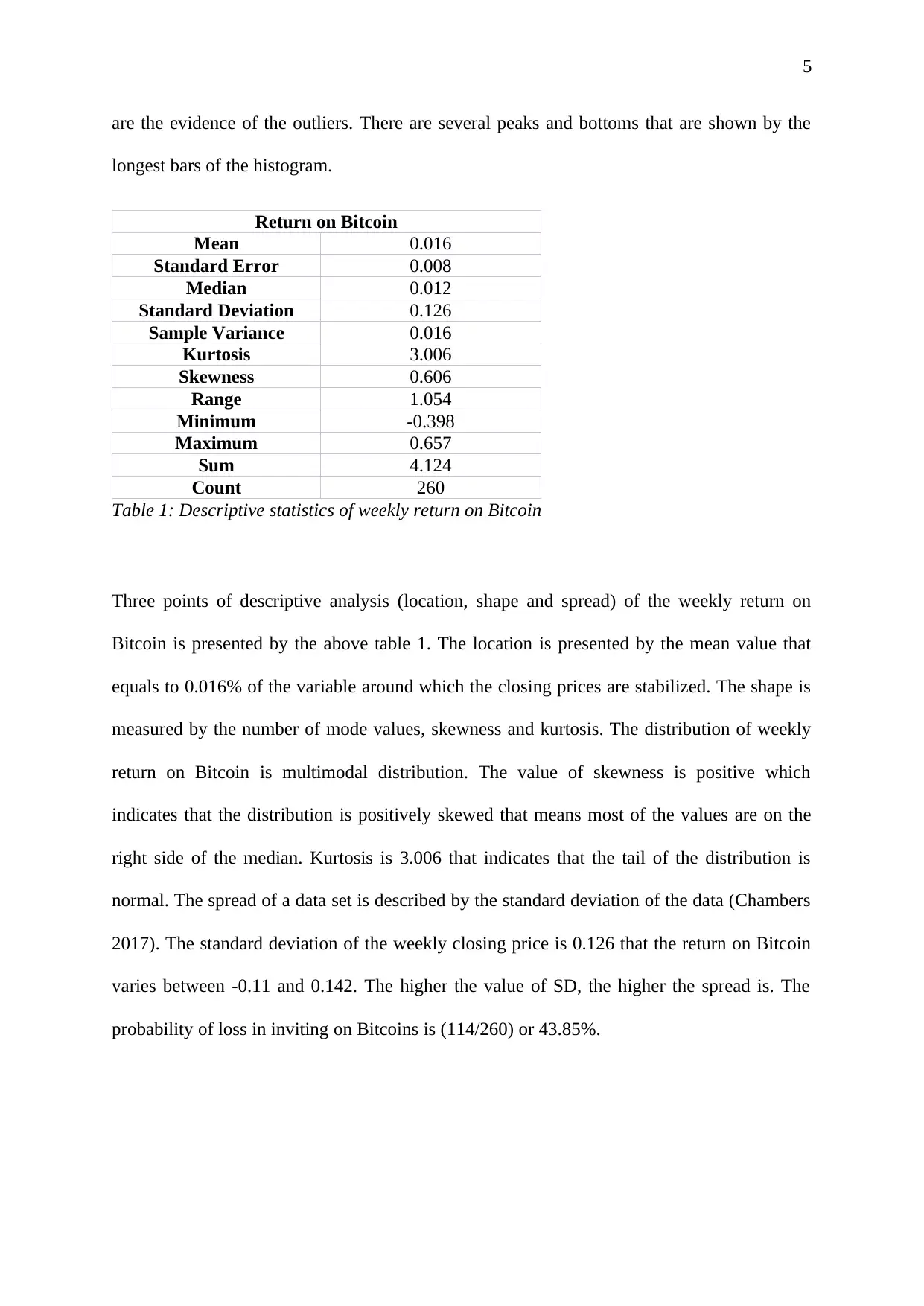

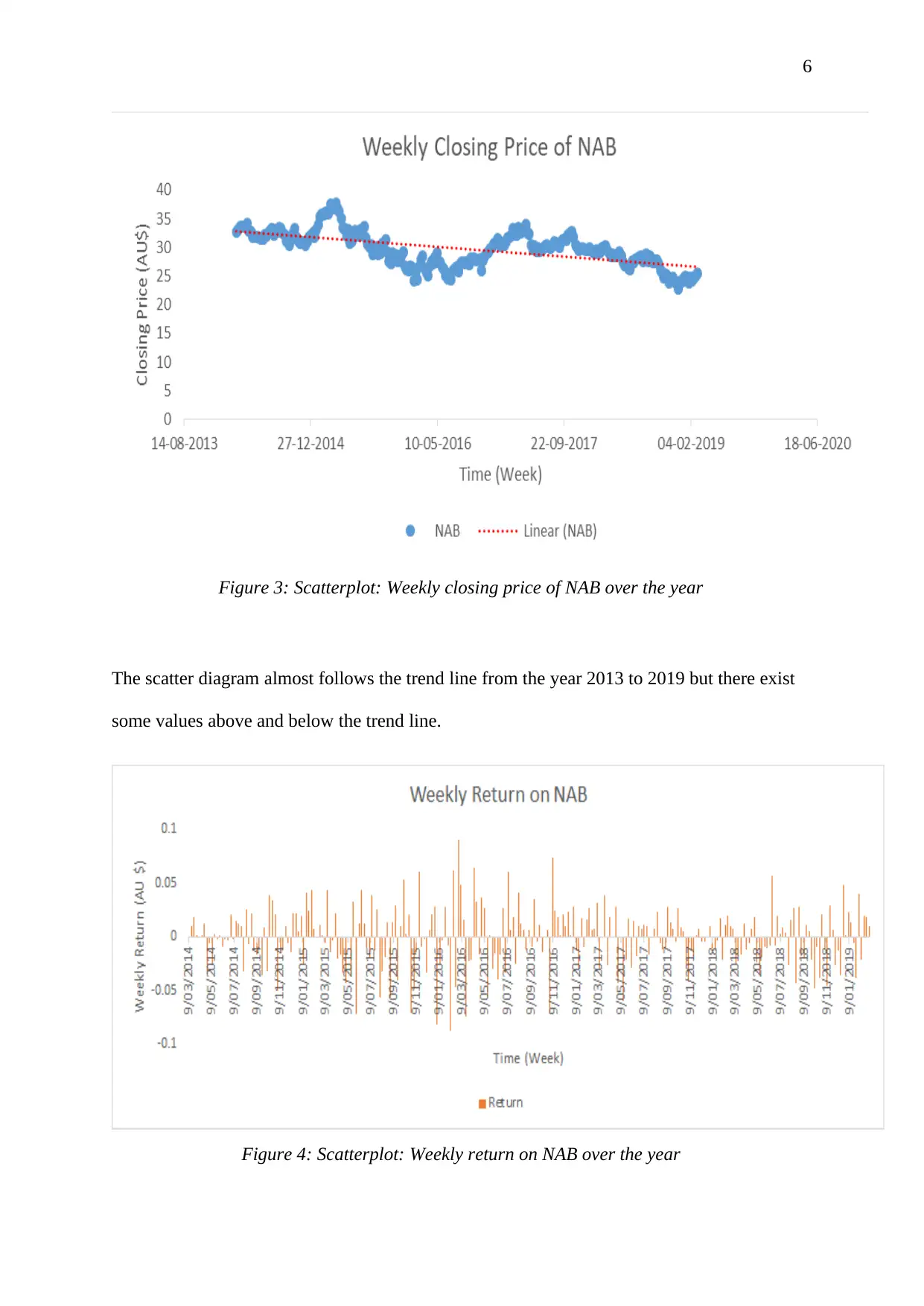

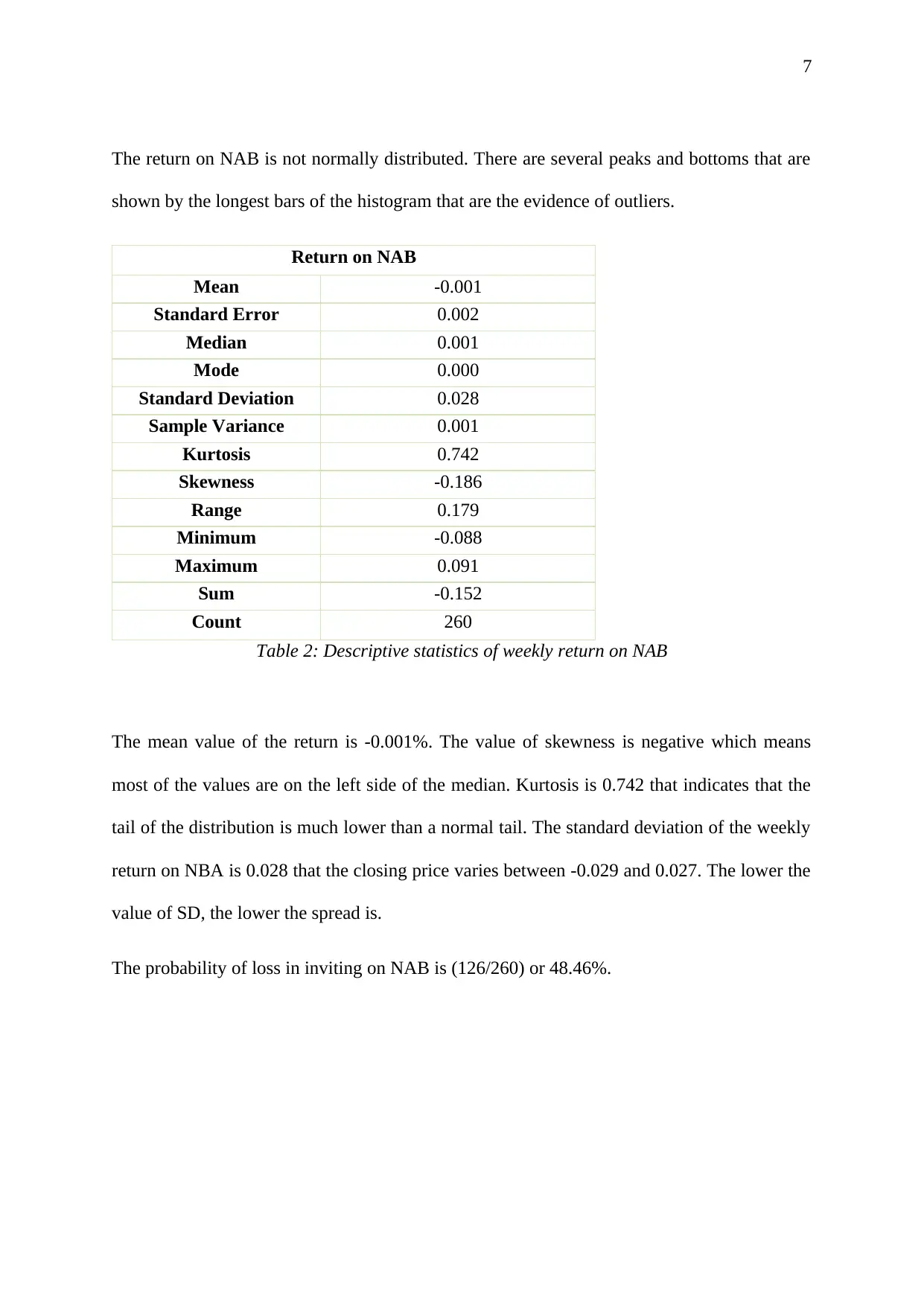

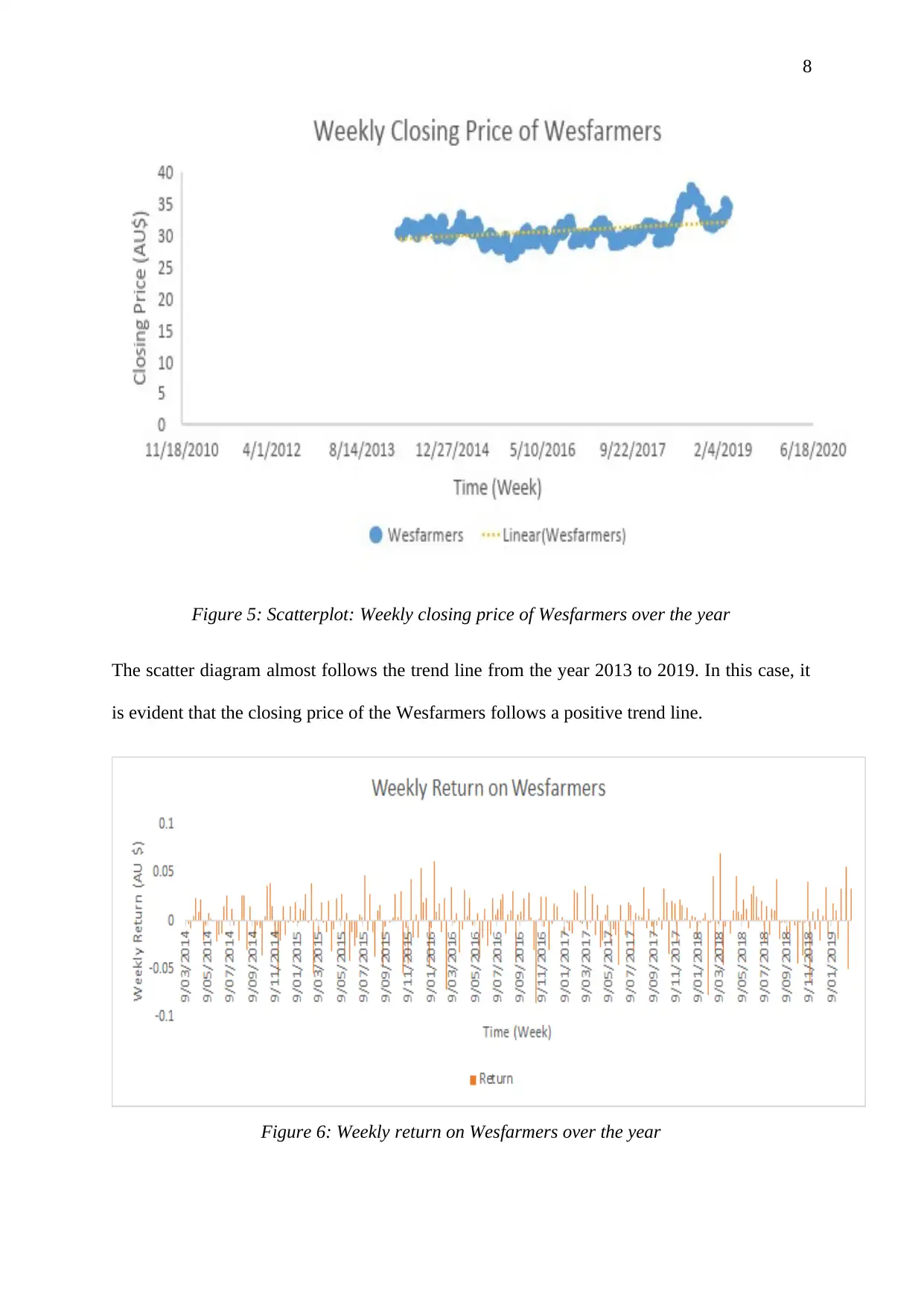

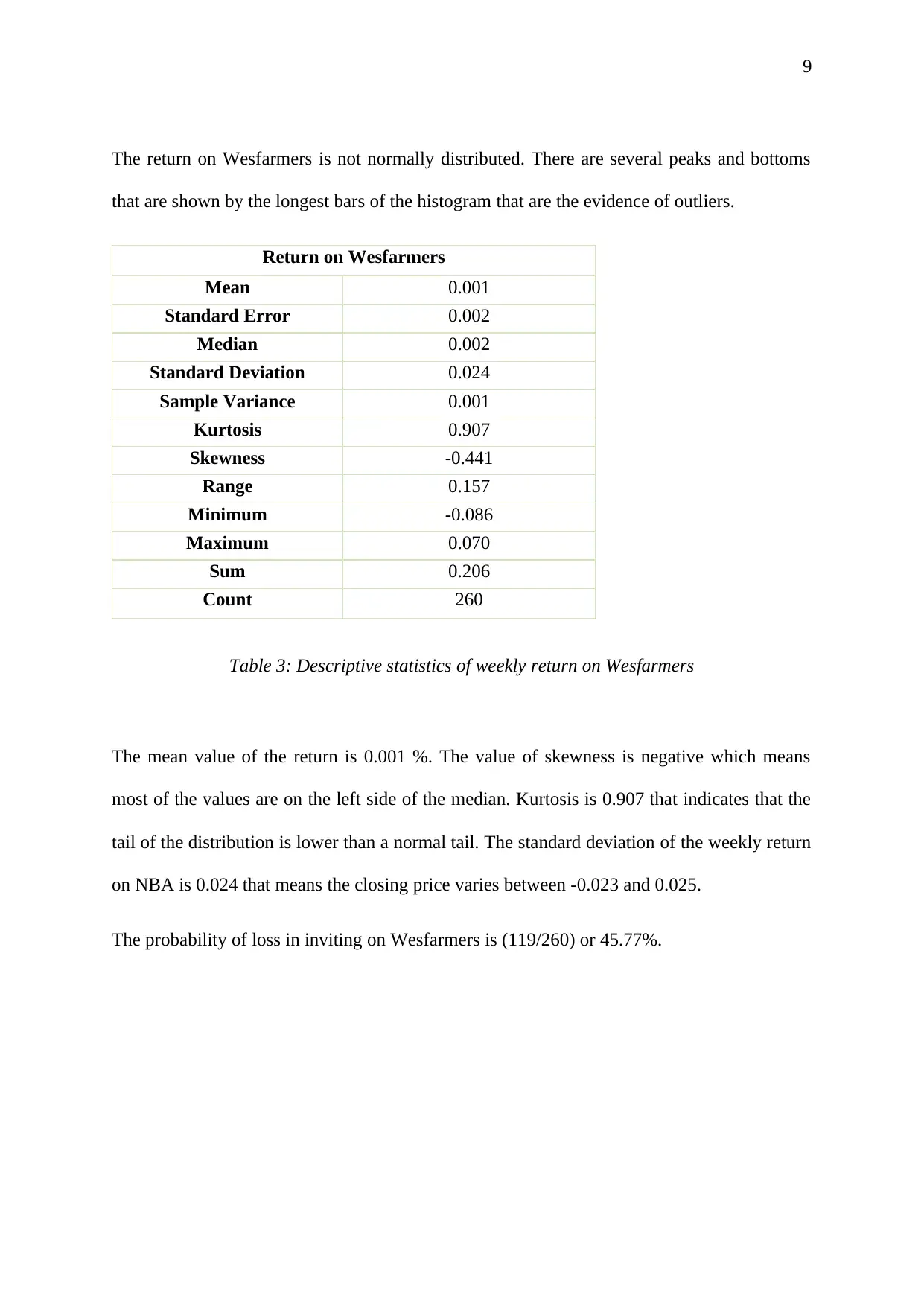

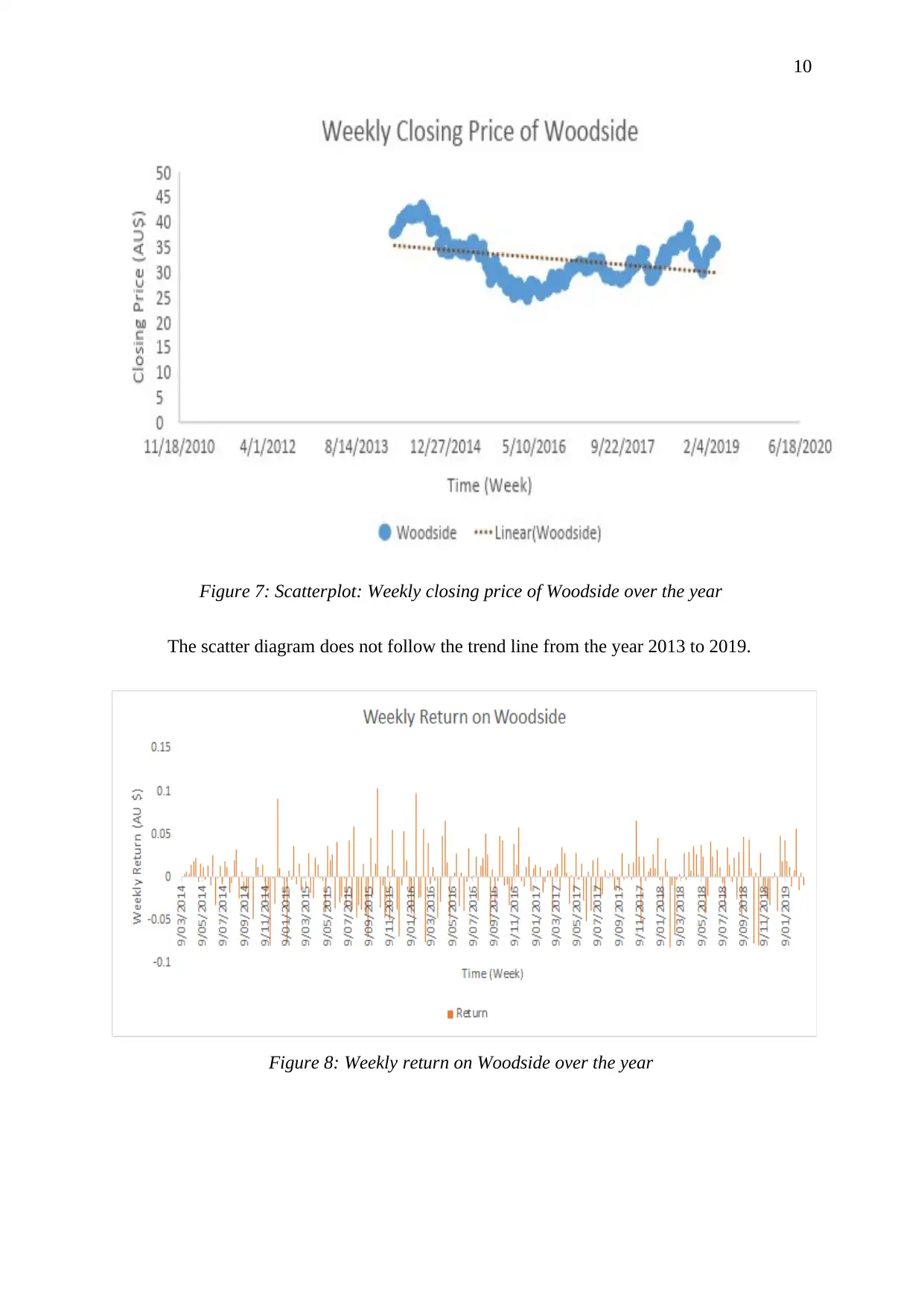

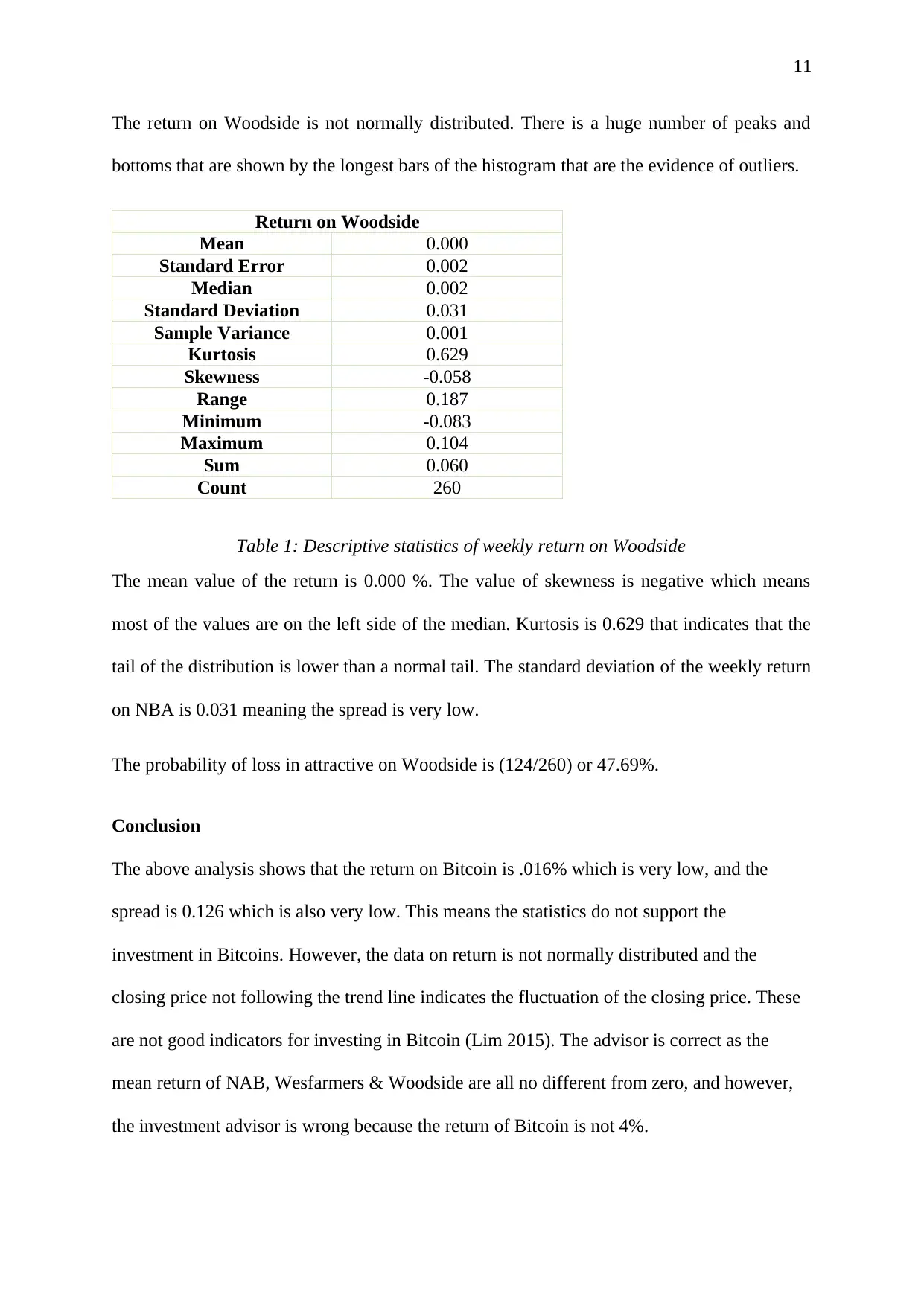

This report provides a comprehensive statistical analysis of Bitcoin as an investment, comparing its performance with other stocks like NAB, Wesfarmers, and Woodside. The analysis includes scatterplots and histograms to visualize weekly closing prices and returns, alongside descriptive statistics such as mean, standard deviation, skewness, and kurtosis. The report calculates confidence intervals for returns and conducts hypothesis tests to assess the validity of an investment advisor's claims regarding Bitcoin's return and the returns of other shares. The findings suggest that the statistical data does not support investment in Bitcoins due to low returns and high volatility, while the analysis of other stocks provides contrasting insights. The report also addresses the limitations of the data, such as non-normal distributions and trend deviations, which may impact the investment decisions. The appendices include detailed calculations of confidence intervals and interpretations of the results.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.