Assignment 2: Statistical Inference and Simple Regression Analysis

VerifiedAdded on 2021/06/15

|9

|1862

|39

Homework Assignment

AI Summary

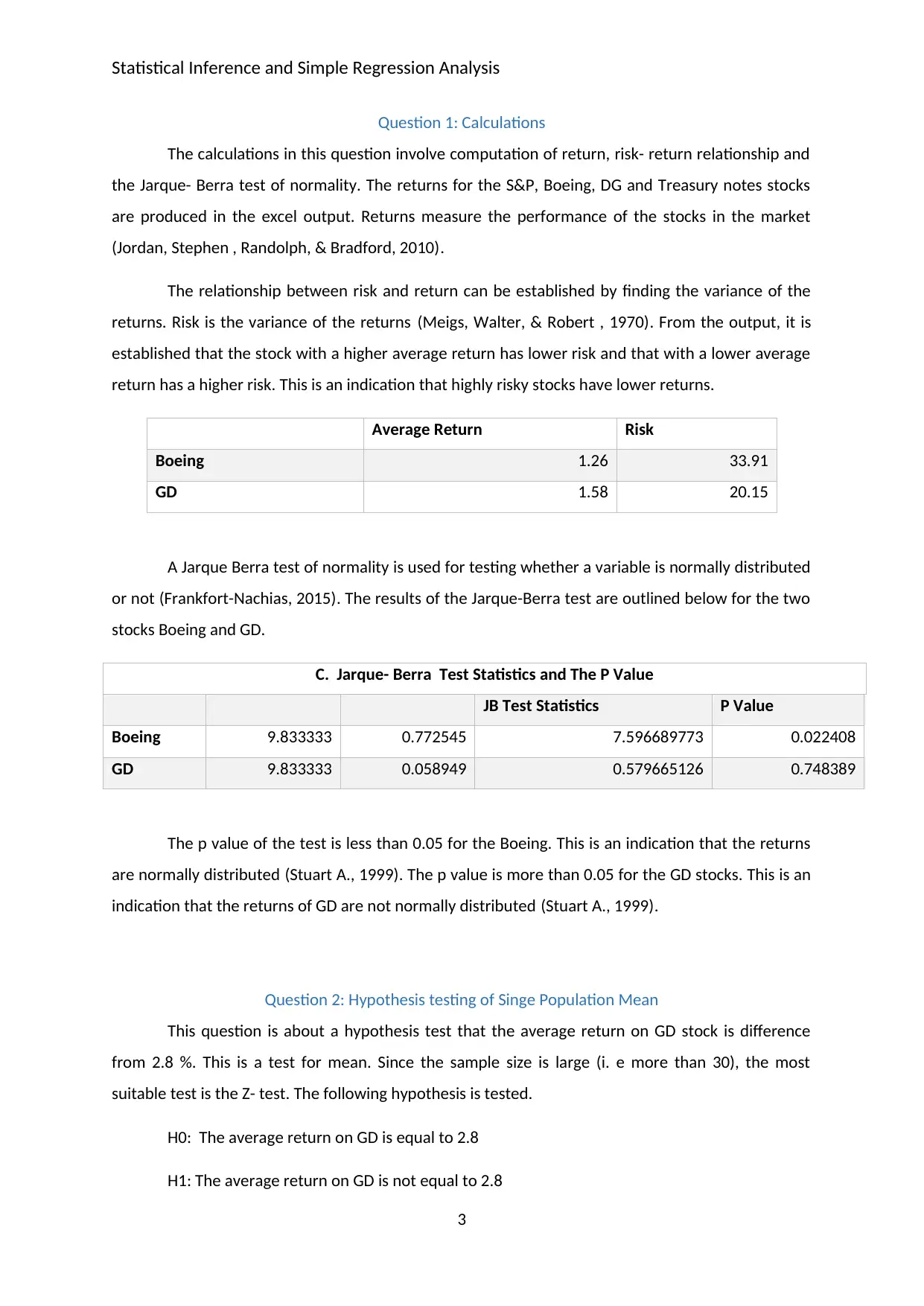

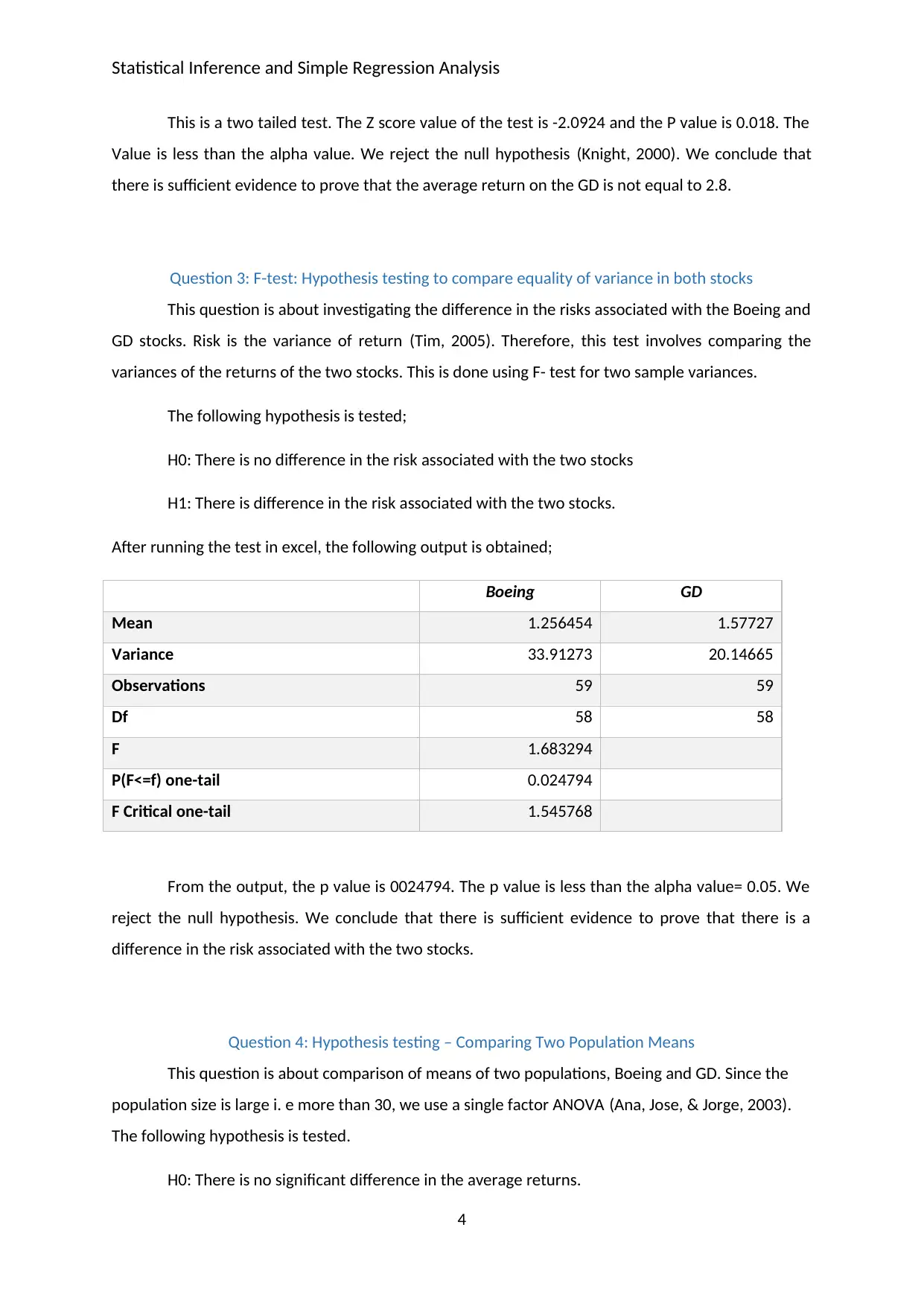

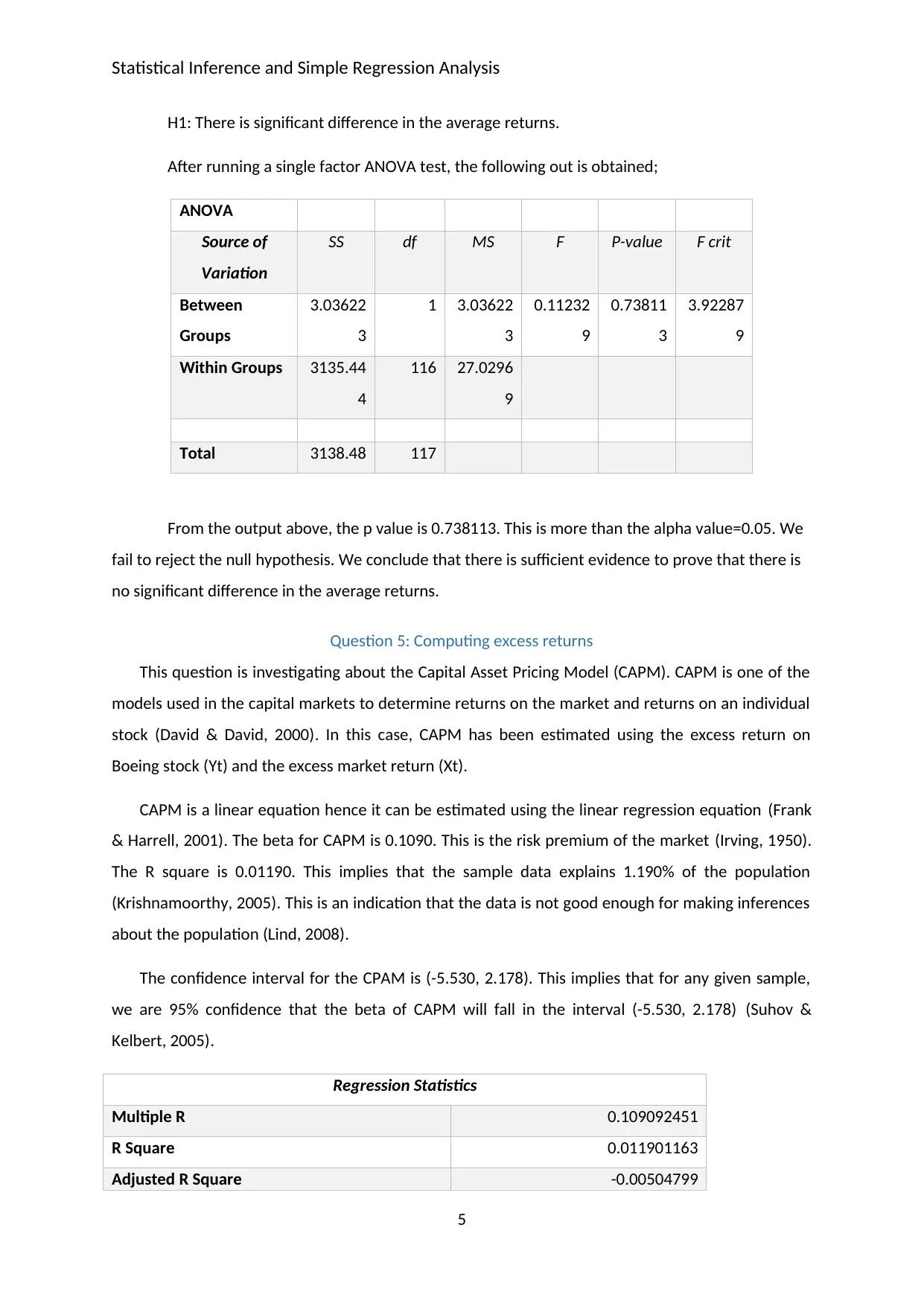

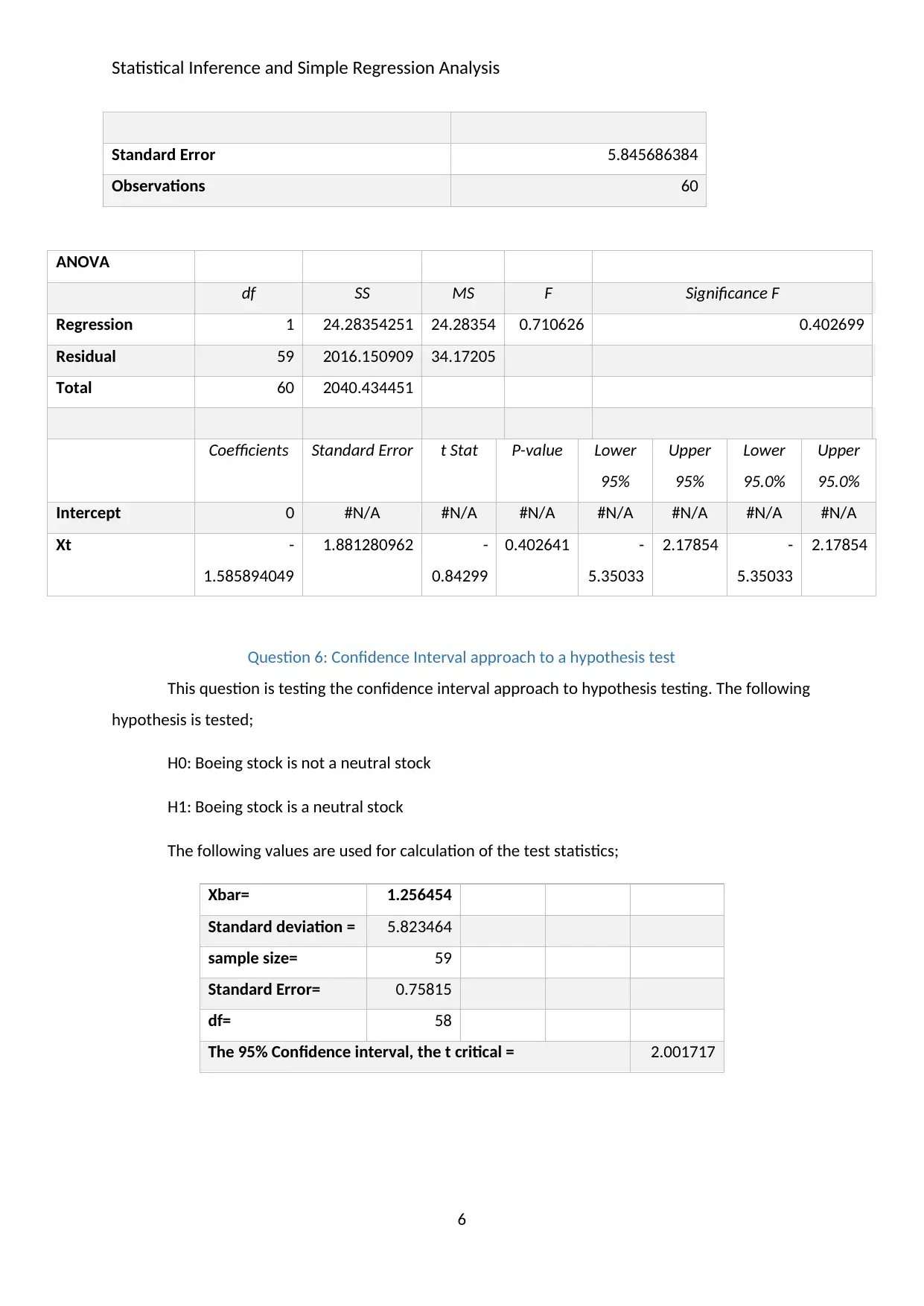

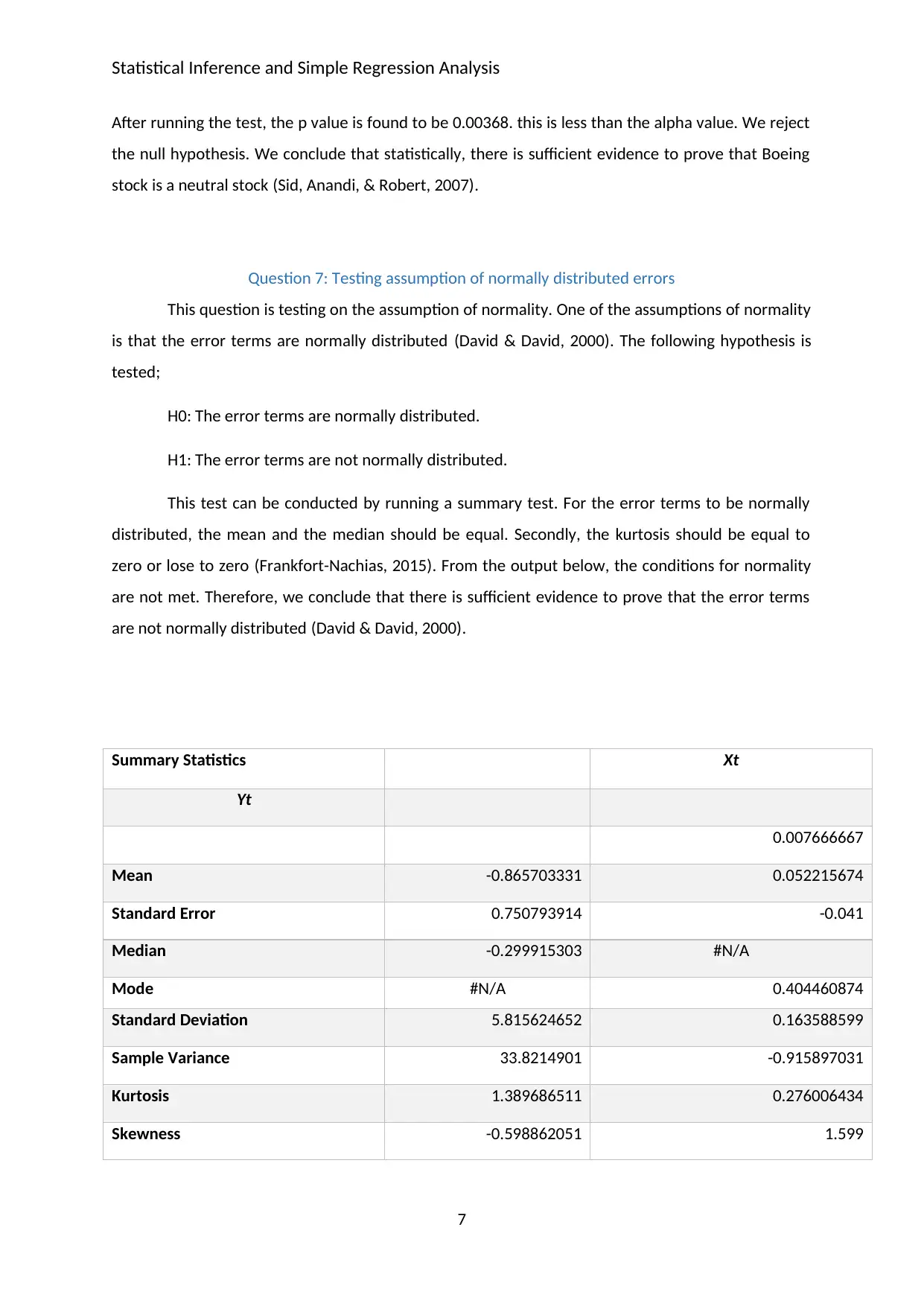

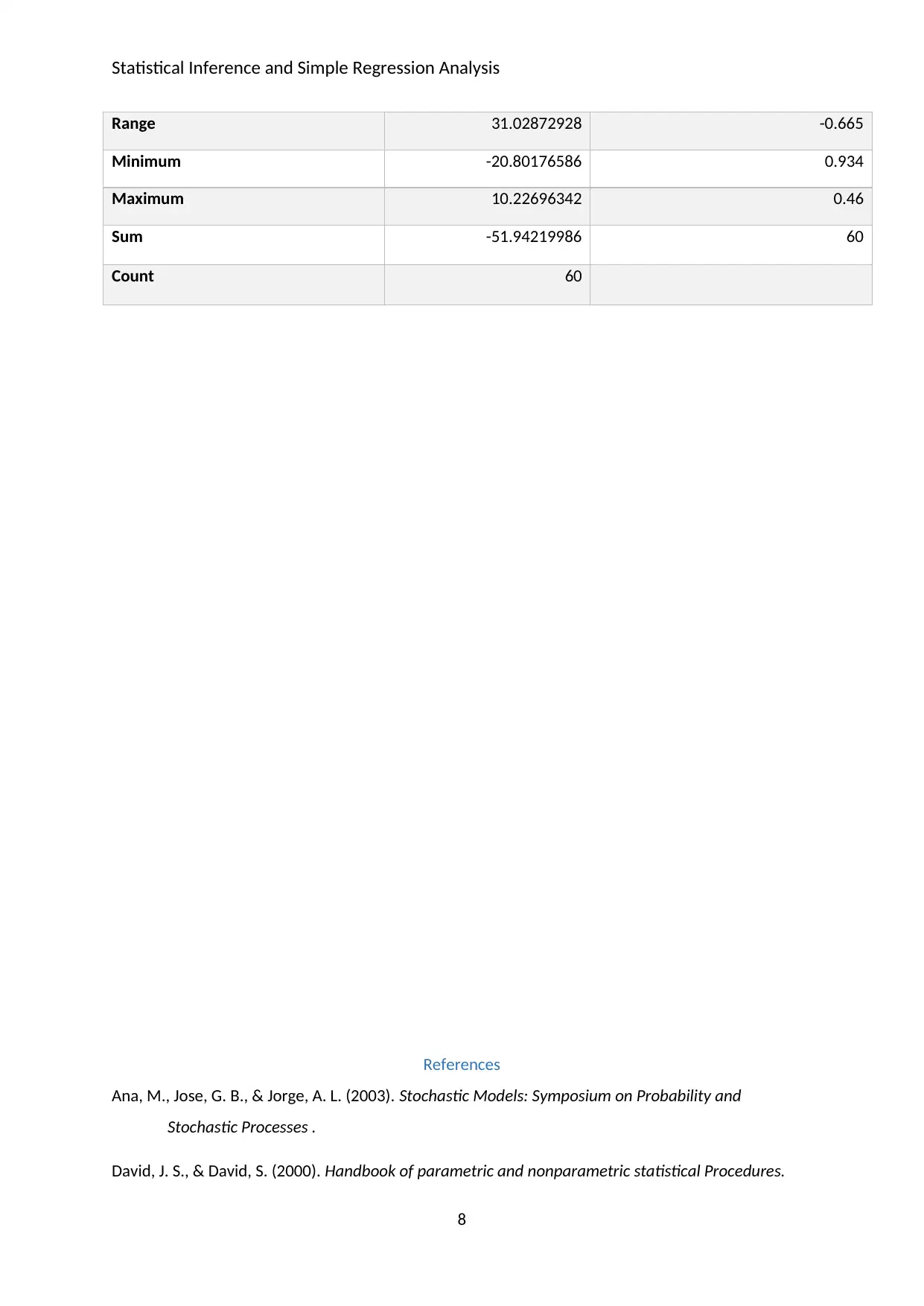

This assignment report provides a comprehensive analysis of statistical inference and simple regression techniques applied to financial data. It begins with calculations of returns, risk, and the Jarque-Bera test for normality on stock data. The report then delves into hypothesis testing for single population means, variance comparisons using the F-test, and comparing two population means using ANOVA. The Capital Asset Pricing Model (CAPM) is explored through regression analysis, including the interpretation of beta, R-squared, and confidence intervals. Additionally, the assignment covers the confidence interval approach to hypothesis testing and tests the assumption of normally distributed errors. The report provides detailed outputs, interpretations, and conclusions for each statistical test, demonstrating a solid understanding of the concepts and their practical application in finance.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.