Statistical Report: Analysis of Insurance Fraud for IFBA Finance Team

VerifiedAdded on 2022/10/17

|11

|1457

|9

Report

AI Summary

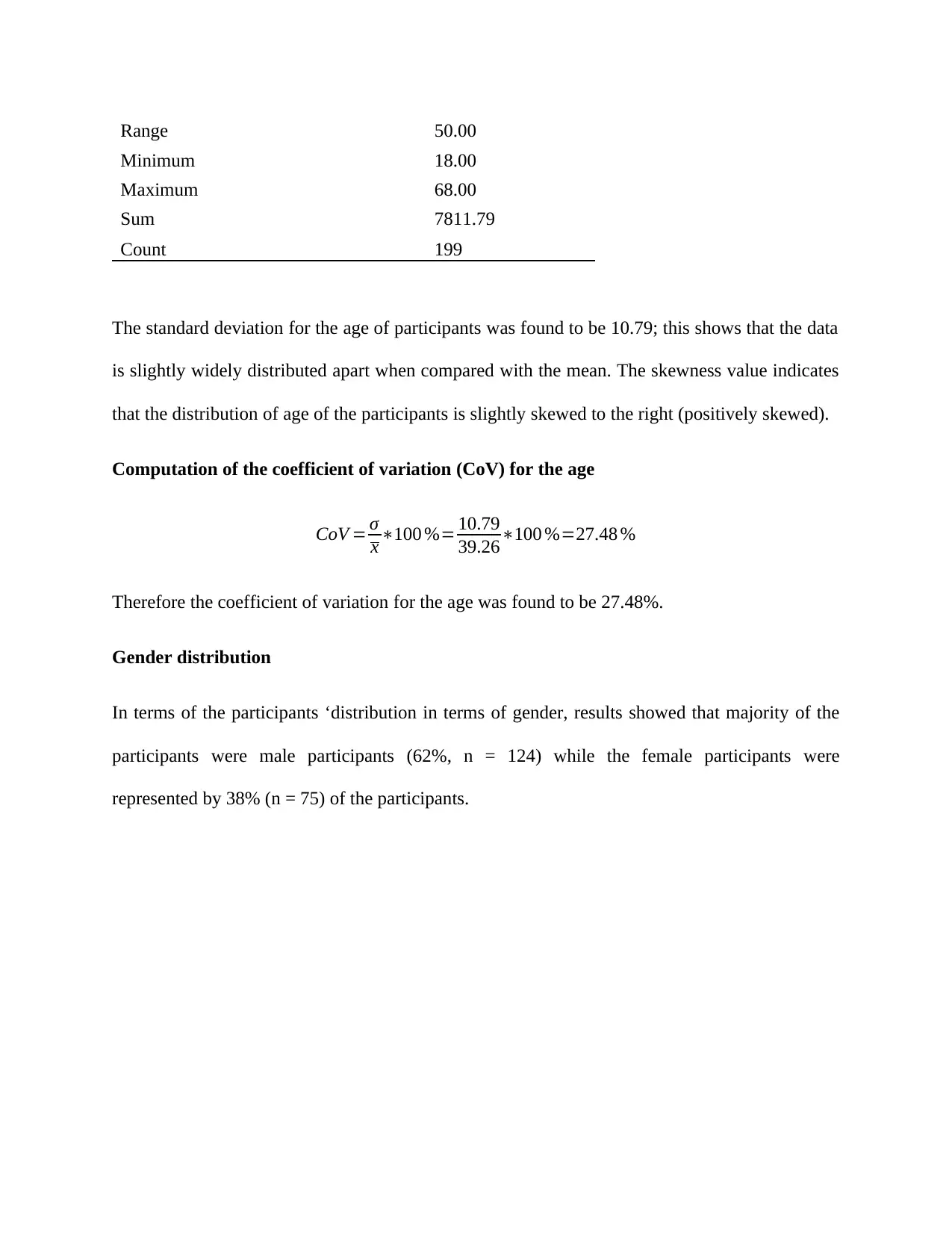

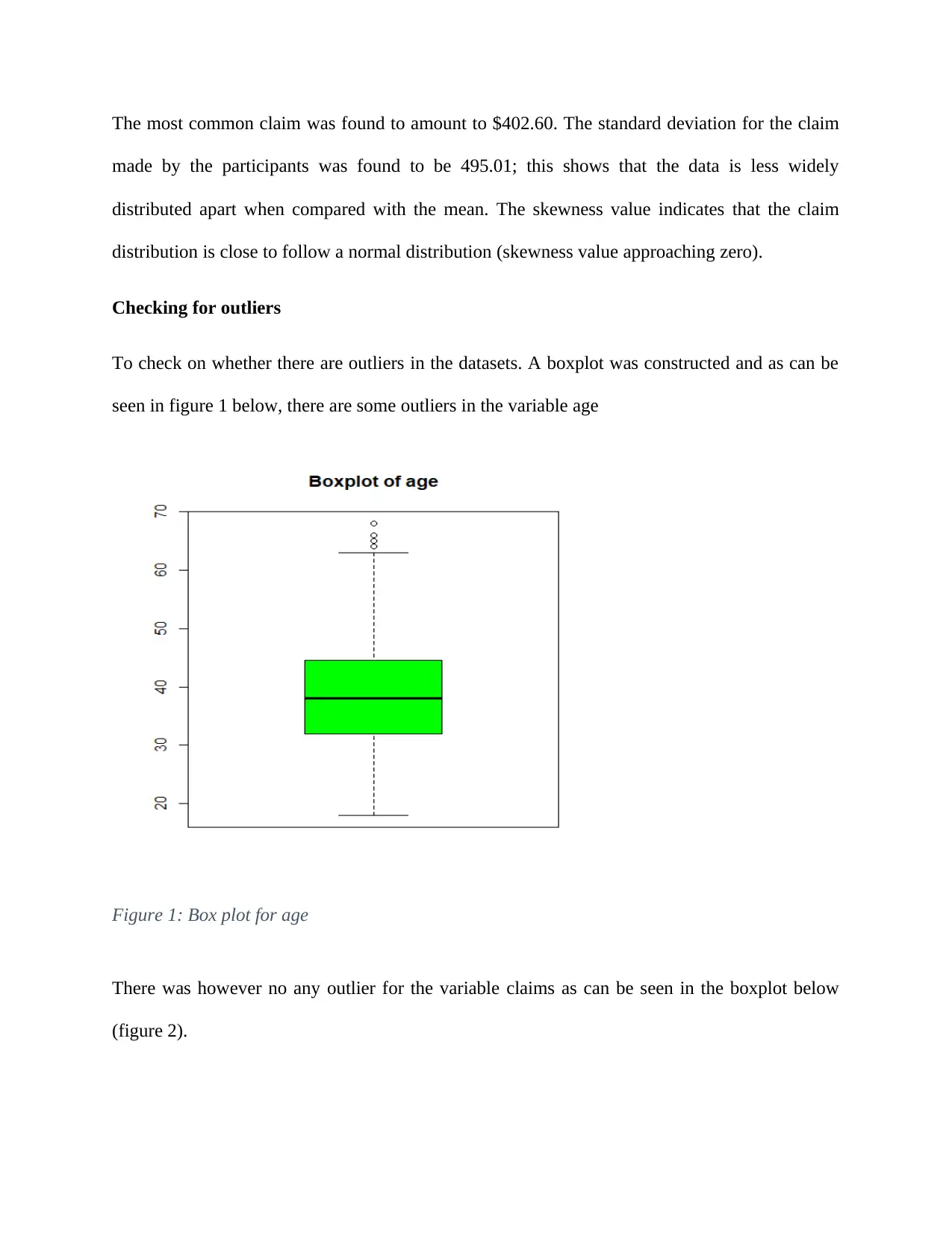

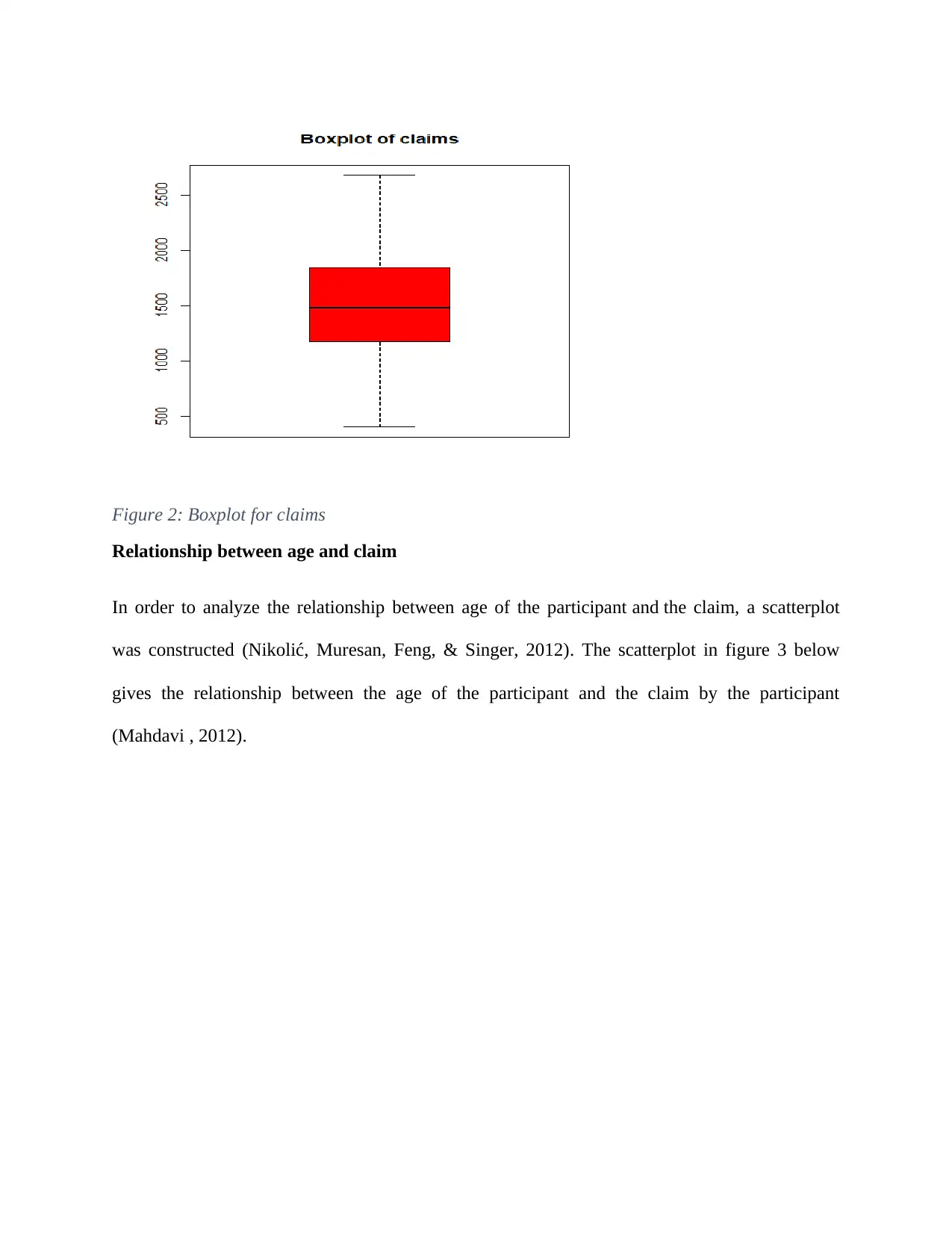

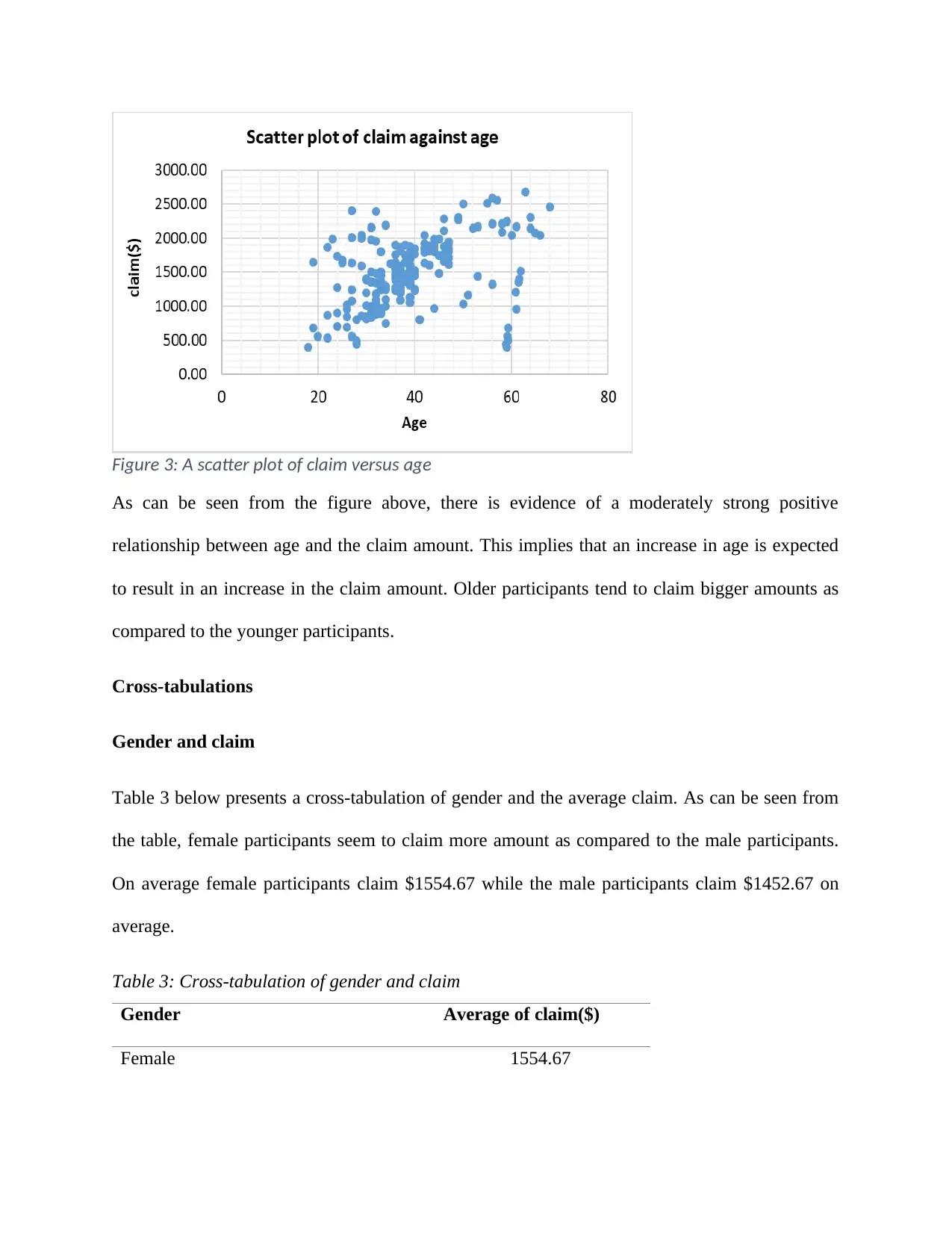

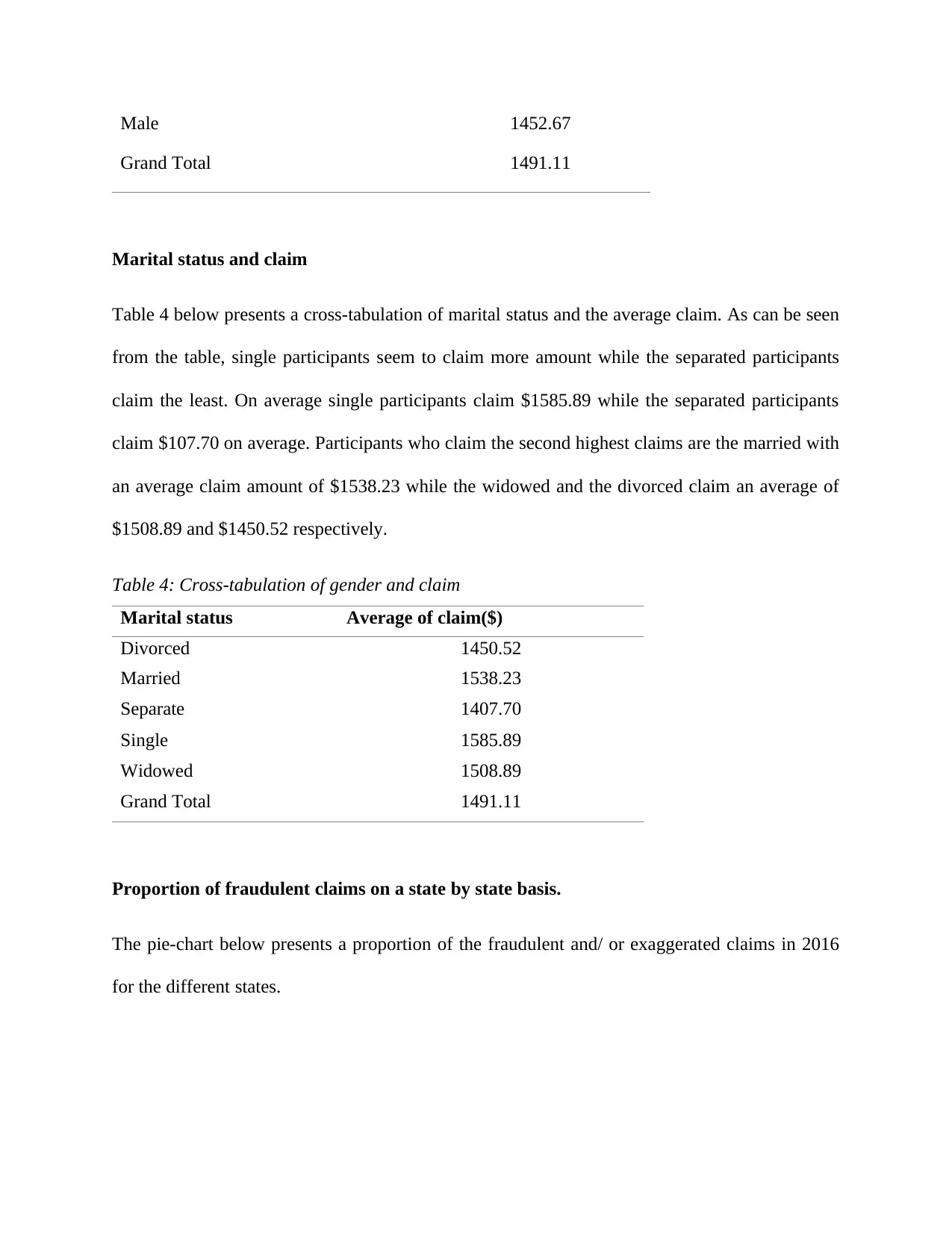

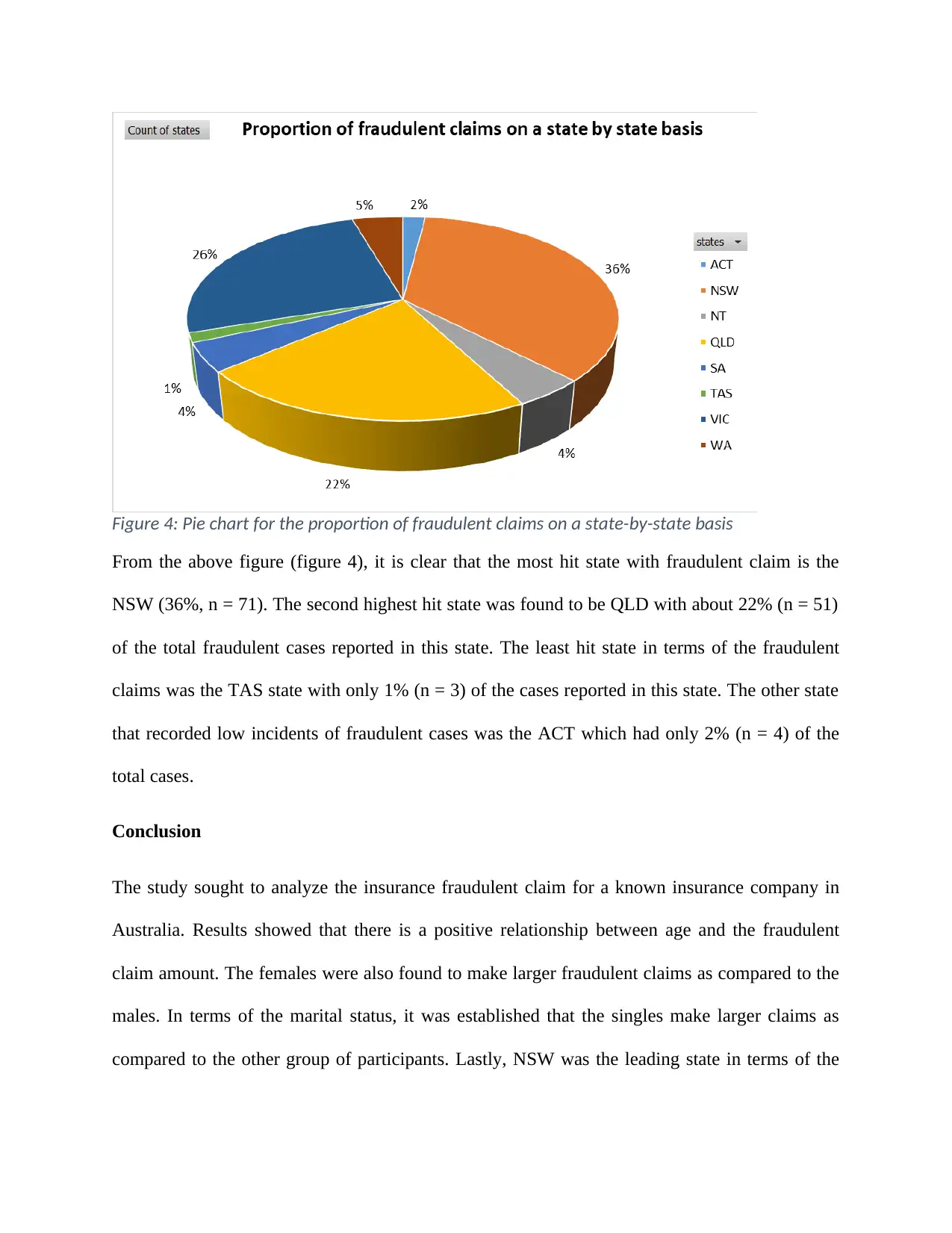

This report analyzes insurance fraud within a major Australian insurance company using 2016 data, addressing research questions on the relationship between gender, marital status, age, and fraudulent claim amounts. The study employs descriptive statistics, including mean, median, standard deviation, and boxplots, to identify trends and outliers. Findings reveal a positive correlation between age and claim amount, with females making larger claims on average. Single participants were found to have the highest average claim amounts. The report also examines the proportion of fraudulent claims by state, highlighting NSW as the most affected. The analysis concludes with key insights into the factors influencing insurance fraud and provides recommendations for fraud detection and prevention.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.