Statistical Analysis of Stock Returns, Risk, and CAPM for Finance

VerifiedAdded on 2020/05/11

|13

|1681

|62

Homework Assignment

AI Summary

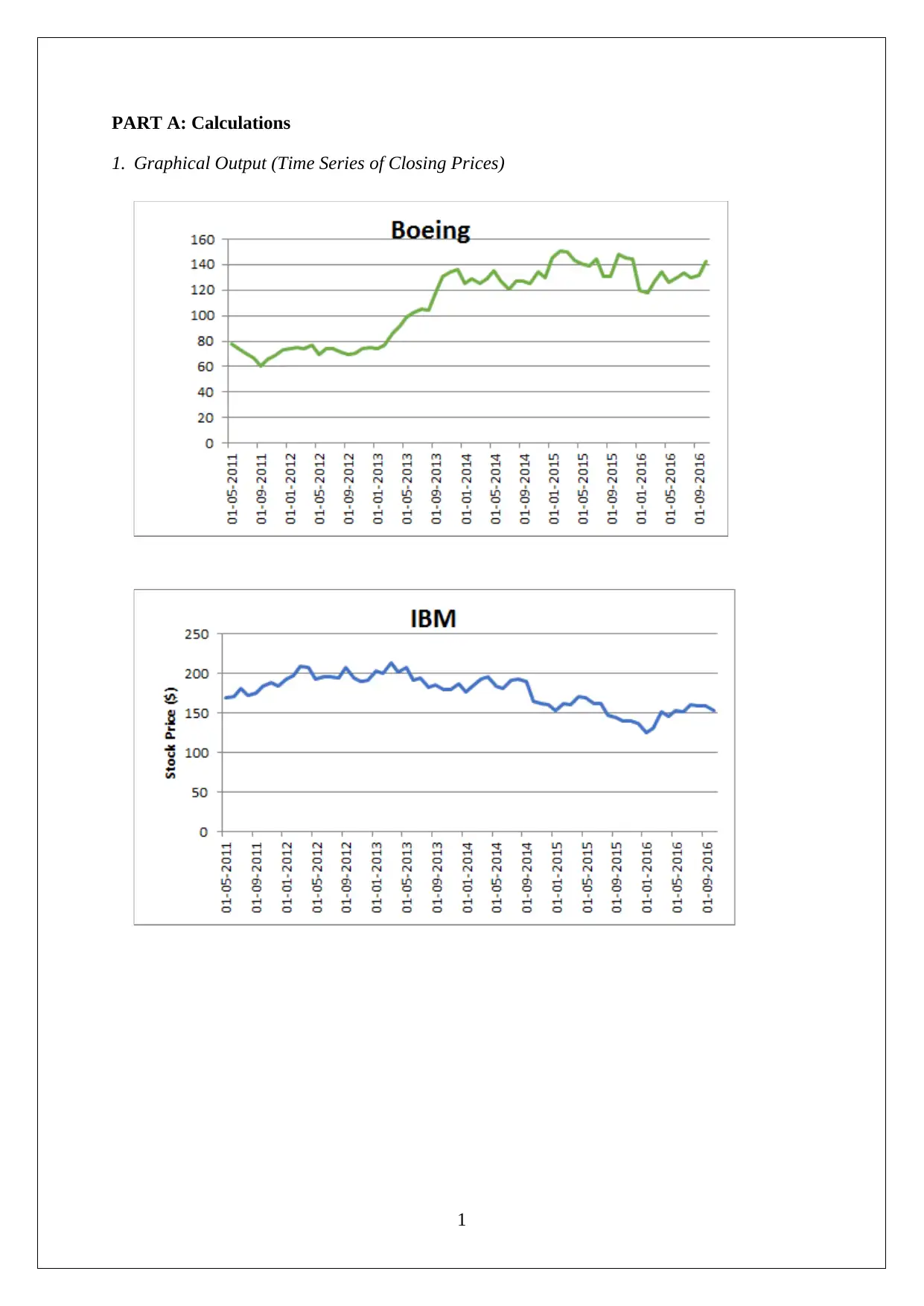

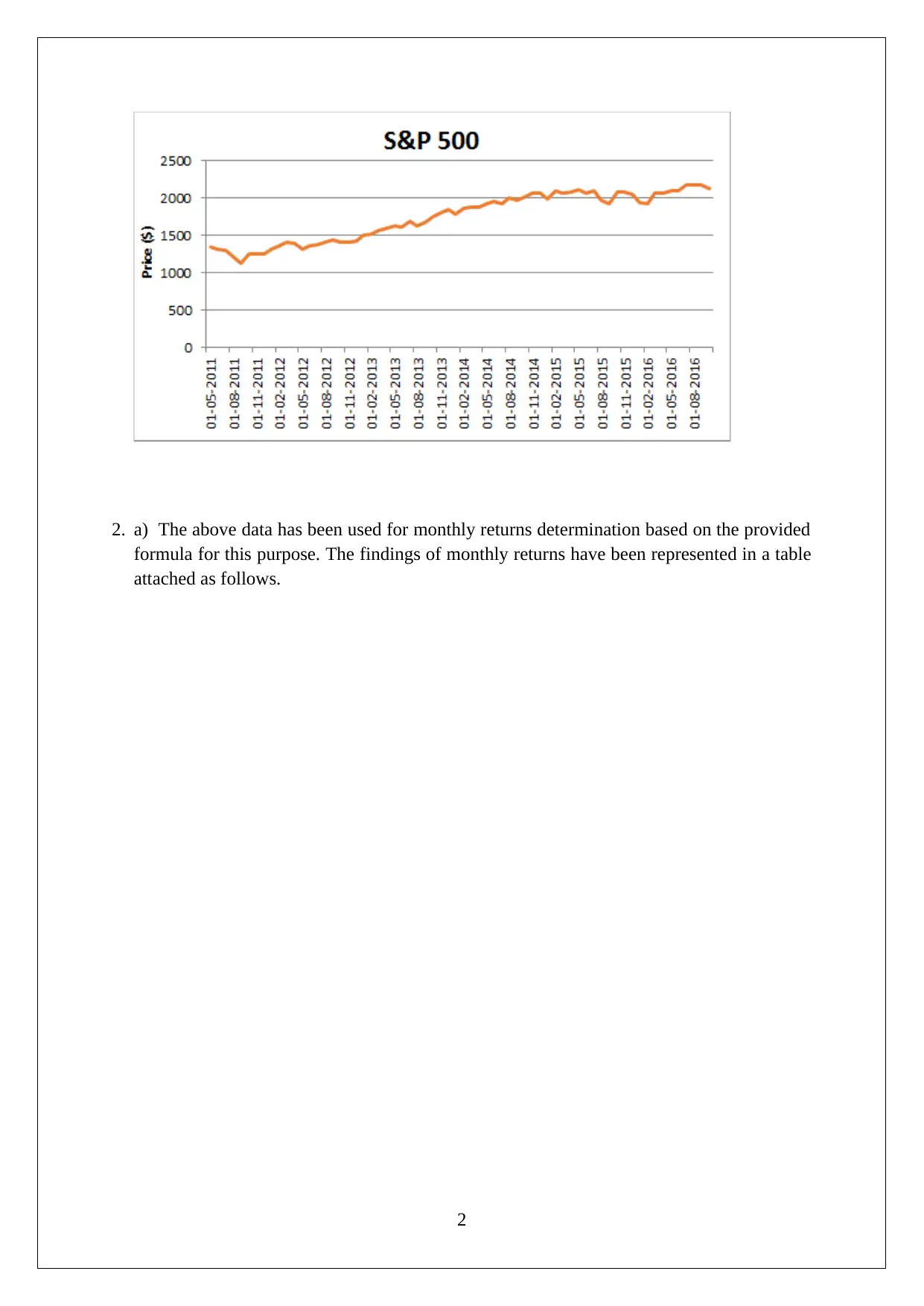

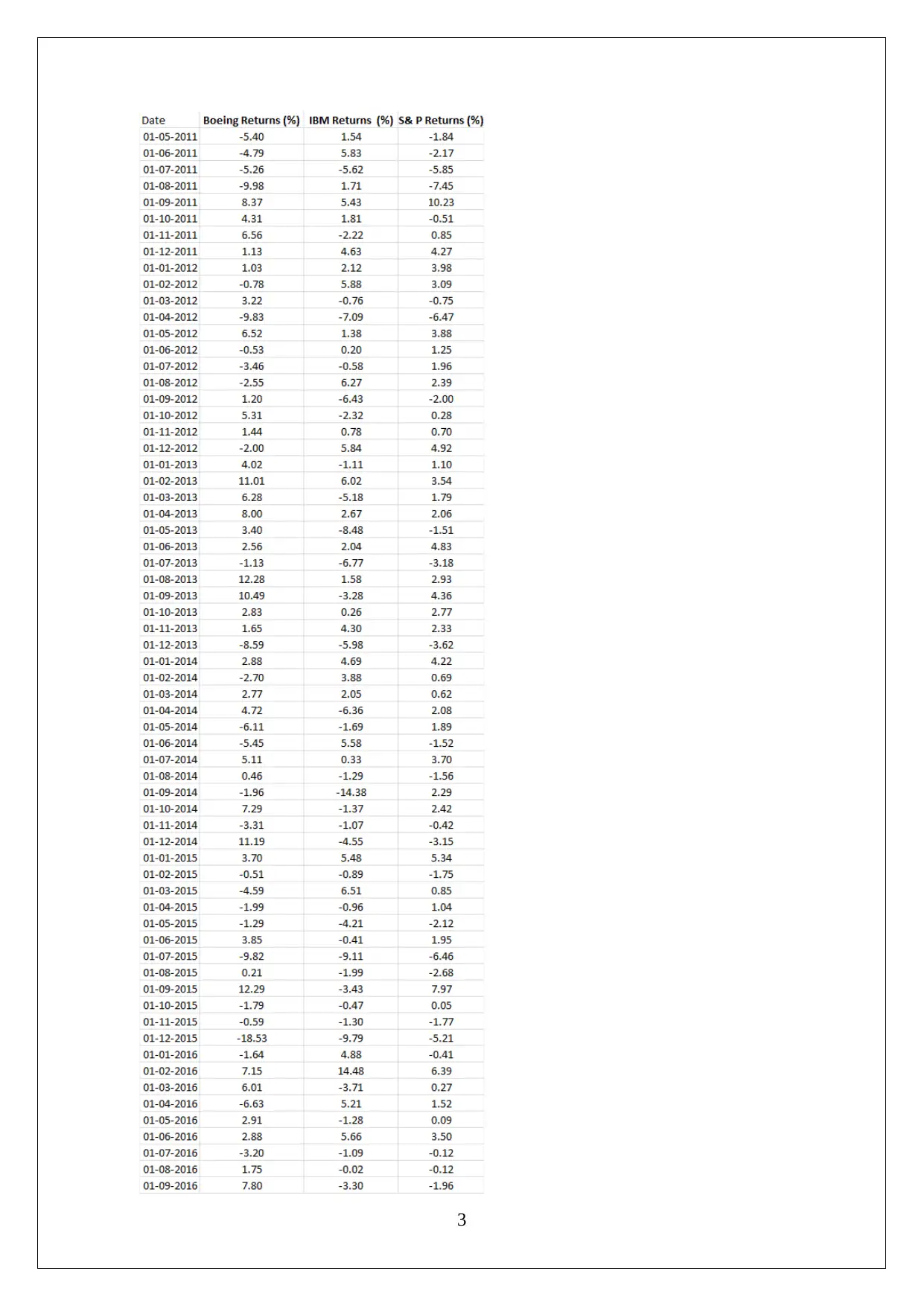

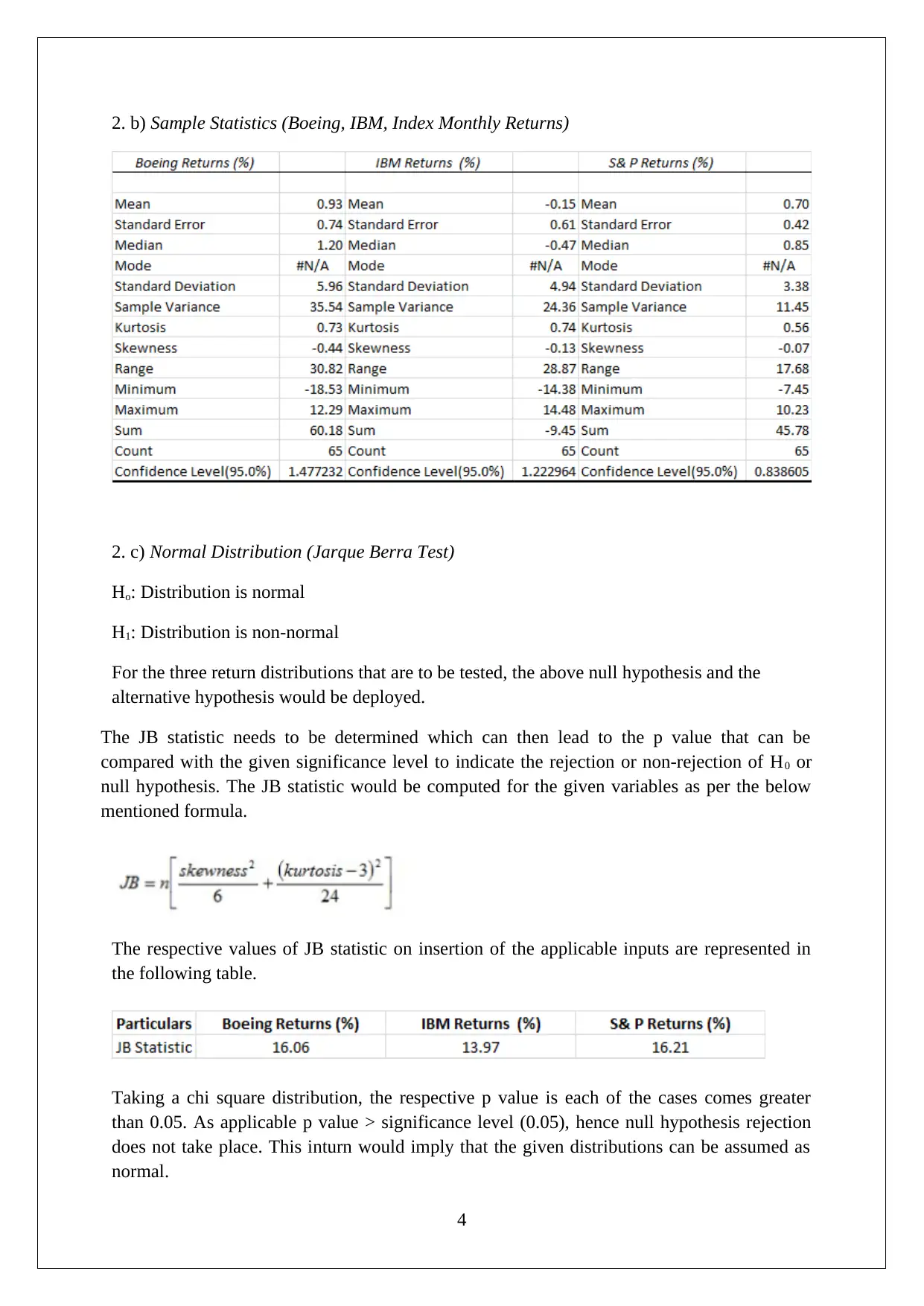

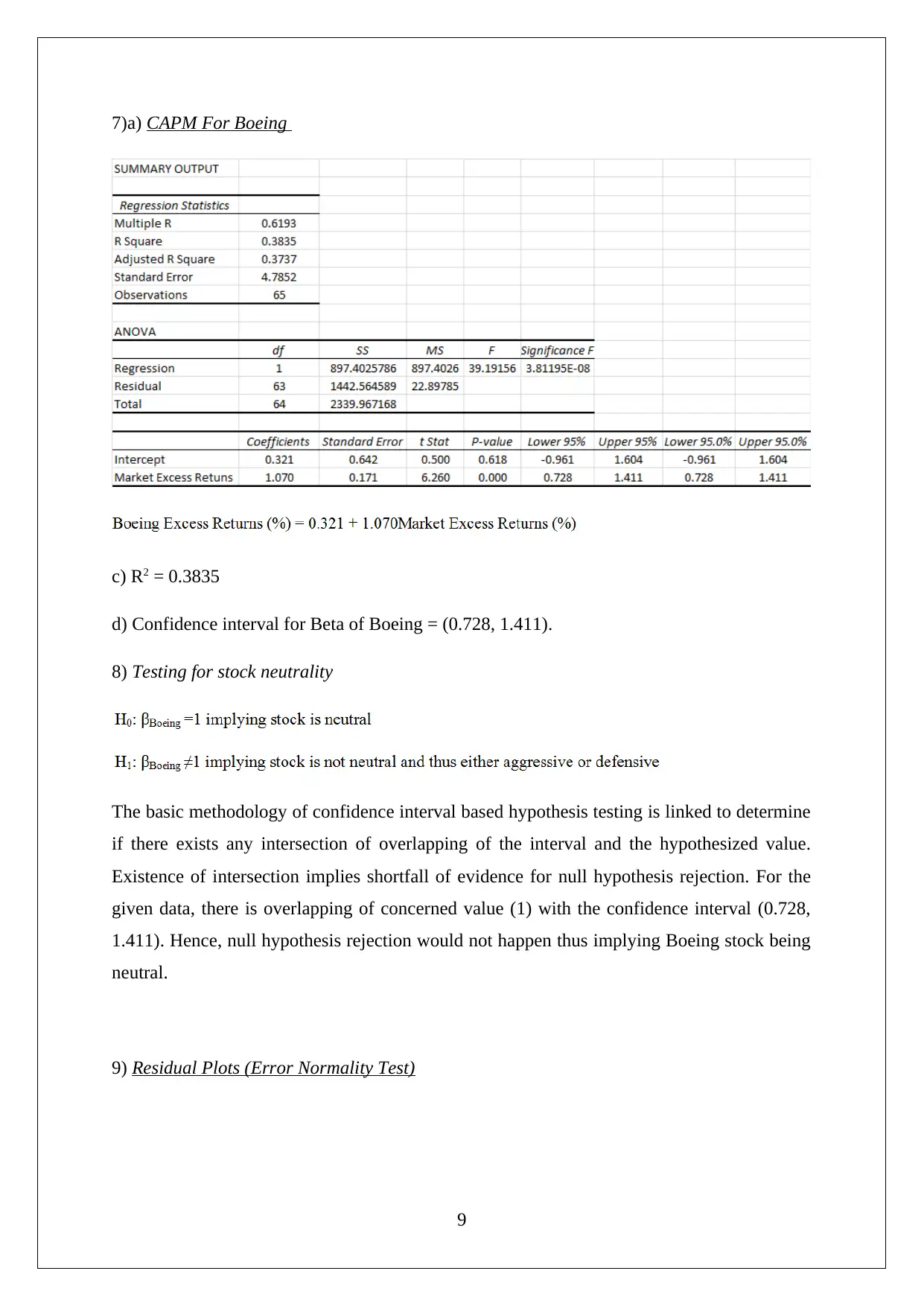

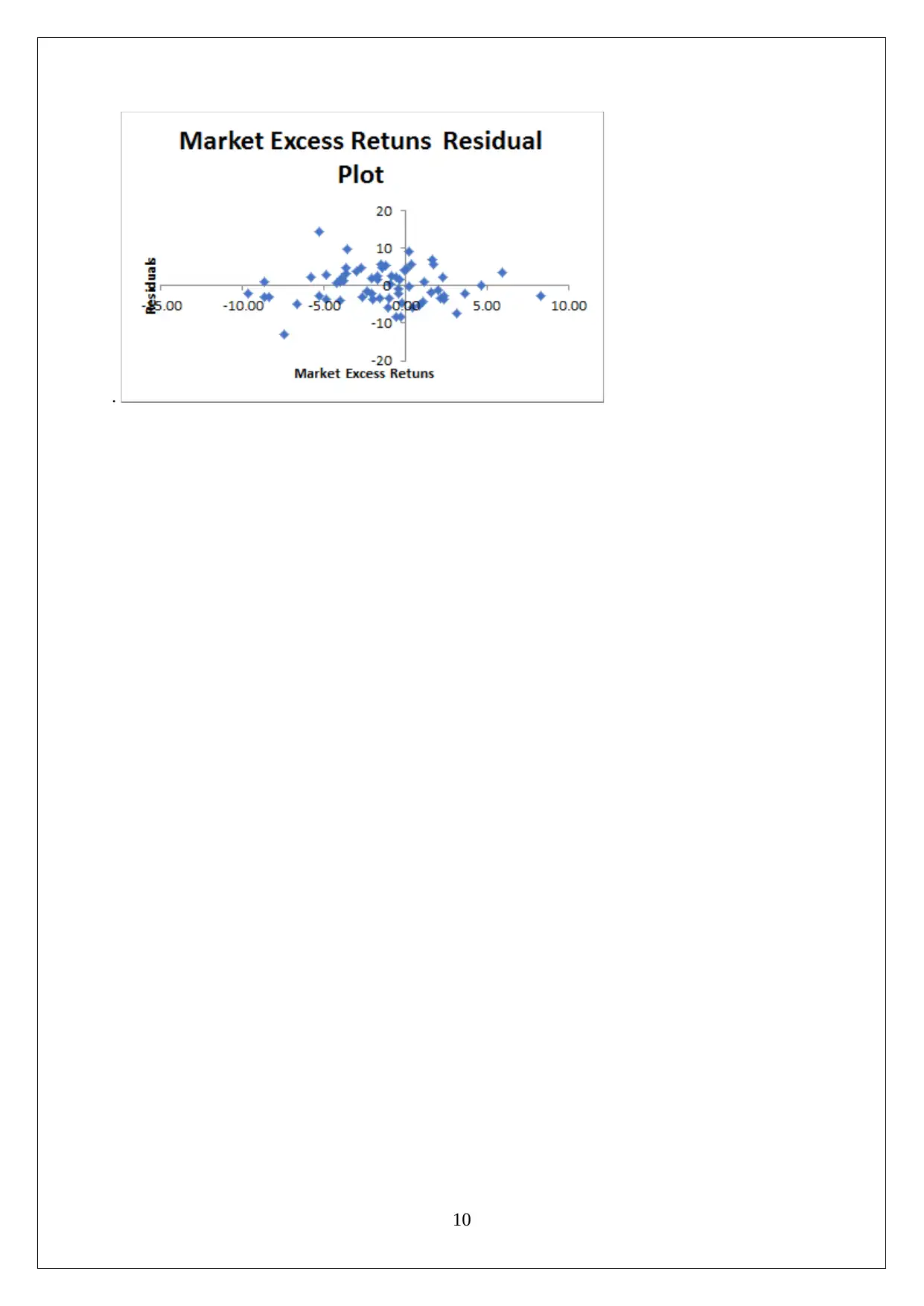

This assignment delves into the statistical analysis of stock data, focusing on the performance of Boeing and IBM. It begins with calculations of monthly returns and sample statistics, followed by an examination of normal distribution using the Jarque-Bera test. The assignment then applies hypothesis testing to evaluate Boeing's stock returns, compare risk levels using the F-test, and compare return levels using the t-test. The analysis extends to determining the superior stock based on return per unit of risk. Further, the Capital Asset Pricing Model (CAPM) is applied to Boeing, calculating the slope coefficient, R-squared value, and confidence interval for beta, followed by testing for stock neutrality. The assignment concludes with an interpretation of Boeing and IBM stock trends and a residual plot to test for error normality. The document provides a comprehensive statistical evaluation of the stocks, covering various financial metrics and testing methodologies.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.