Comprehensive Report on Statutory Requirements for Sports Businesses

VerifiedAdded on 2021/01/05

|8

|1848

|71

Report

AI Summary

This report delves into the statutory requirements imposed on sports businesses, examining various legal regulations and their impact on financial operations. It analyzes different taxation laws, including the mutuality concept and its implications on income assessment for sports clubs like the Maxwell Golf Club. The report further explores the tax implications of player contracts, such as those of Jamile Elias, considering match payments, bonuses, and lump-sum payments. Additionally, it addresses the deductibility of legal expenses and capital expenditures, using examples like Sydney Sports Ltd.'s expenses and Max Fit Gym's warehouse conversion. The conclusion emphasizes the importance of compliance with these regulations to avoid governmental interference and ensure appropriate tax payments.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Statutory Requirement

for Sports Business

for Sports Business

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Question 1:...................................................................................................................................1

Question 2:...................................................................................................................................2

Question 3:...................................................................................................................................3

Question 4:...................................................................................................................................3

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................5

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

Question 1:...................................................................................................................................1

Question 2:...................................................................................................................................2

Question 3:...................................................................................................................................3

Question 4:...................................................................................................................................3

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................5

INTRODUCTION

Statutory requirements are the set of governmental bodies that are imposed on the

organisations which are operating business under them. There are several types of legal

regulations that are implemented upon sports businesses and for all the firms that are part of such

type of business have to comply with them in order to reduce governmental interference in the

operational activities (Anagnostopoulos, Byers and Shilbury, 2014). Different types of taxation

laws are imposed on sports businesses and all the firms that are related to it have to follow all of

them. This report is based upon such type of regulations and their treatments by sport clubs. It

includes different taxation laws related to income of various sport clubs.

MAIN BODY

Question 1:

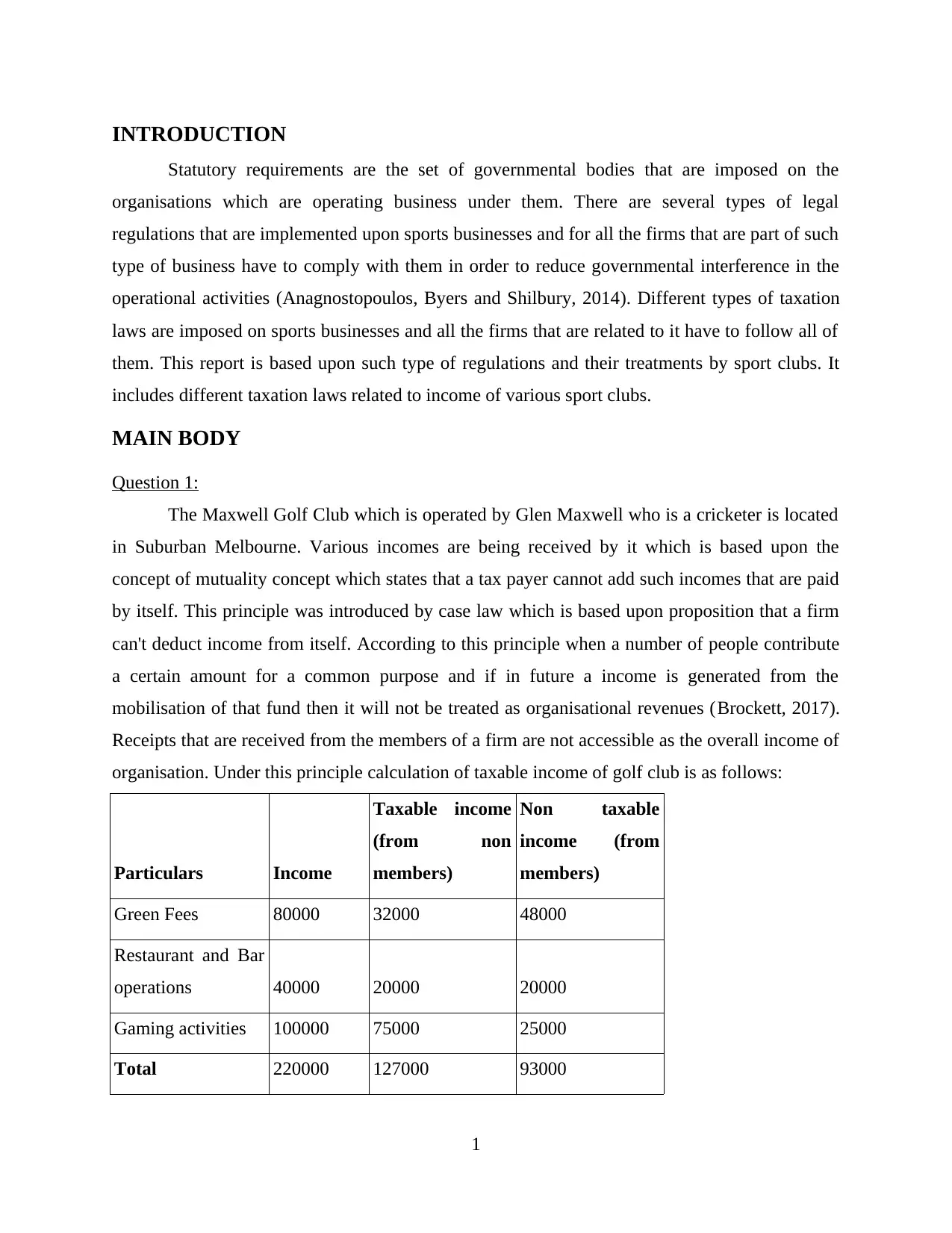

The Maxwell Golf Club which is operated by Glen Maxwell who is a cricketer is located

in Suburban Melbourne. Various incomes are being received by it which is based upon the

concept of mutuality concept which states that a tax payer cannot add such incomes that are paid

by itself. This principle was introduced by case law which is based upon proposition that a firm

can't deduct income from itself. According to this principle when a number of people contribute

a certain amount for a common purpose and if in future a income is generated from the

mobilisation of that fund then it will not be treated as organisational revenues (Brockett, 2017).

Receipts that are received from the members of a firm are not accessible as the overall income of

organisation. Under this principle calculation of taxable income of golf club is as follows:

Particulars Income

Taxable income

(from non

members)

Non taxable

income (from

members)

Green Fees 80000 32000 48000

Restaurant and Bar

operations 40000 20000 20000

Gaming activities 100000 75000 25000

Total 220000 127000 93000

1

Statutory requirements are the set of governmental bodies that are imposed on the

organisations which are operating business under them. There are several types of legal

regulations that are implemented upon sports businesses and for all the firms that are part of such

type of business have to comply with them in order to reduce governmental interference in the

operational activities (Anagnostopoulos, Byers and Shilbury, 2014). Different types of taxation

laws are imposed on sports businesses and all the firms that are related to it have to follow all of

them. This report is based upon such type of regulations and their treatments by sport clubs. It

includes different taxation laws related to income of various sport clubs.

MAIN BODY

Question 1:

The Maxwell Golf Club which is operated by Glen Maxwell who is a cricketer is located

in Suburban Melbourne. Various incomes are being received by it which is based upon the

concept of mutuality concept which states that a tax payer cannot add such incomes that are paid

by itself. This principle was introduced by case law which is based upon proposition that a firm

can't deduct income from itself. According to this principle when a number of people contribute

a certain amount for a common purpose and if in future a income is generated from the

mobilisation of that fund then it will not be treated as organisational revenues (Brockett, 2017).

Receipts that are received from the members of a firm are not accessible as the overall income of

organisation. Under this principle calculation of taxable income of golf club is as follows:

Particulars Income

Taxable income

(from non

members)

Non taxable

income (from

members)

Green Fees 80000 32000 48000

Restaurant and Bar

operations 40000 20000 20000

Gaming activities 100000 75000 25000

Total 220000 127000 93000

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

From the above table it has been analysed that total taxable income of The Maxwell Golf

Club is 127000 Dollar which is received from non members. Income tax assessment tax act 1997

section 75 states that income which is received from members of a firm is not treated as receipts

from members are not revenues these are monetary resources raised by using contribution of

internal persons (Taxation rules for Mutuality concept, 2018). Total income which will added to

the assessable income of The Maxwell Golf Club is 127000 dollars in which 40% of total green

fees, 50% of total restaurant and bar operations and 75% of Gaming activities. These are 32000,

20000 and 75000 dollar for all the activities.

Question 2:

Jamile Elias is a player who is playing Rugby from the side of Oberon Tigers in the

Group 10 and winning the best and fairest award since last two years. In summer Sydney

Thunder is also represented by him in the Big Bash League and most probably he will be

selected for Australian T-20 Side. Several negotiations are made by Canterbury Bulldogs Rugby

Club and Jamile Elias has signed a contract with this club (Cox, 2015). The proposal which was

made by the club are match payments of 2000 dollar per match, 10000 dollar as bonus if the

team is able to be the part of top 8 teams at the ned of the season. They have also proposed a

clause regarding lump sum payment of 150000 dollar in which Jamile Elias is agreeing to play

rugby league exclusively and give up the cricket.

According to Income tax assessment act 1997, Section 15-2 (1) incomes which is

received as compensation, allowances, gratitudes, premiums and bonuses that are received by an

individuals in relation directly or indirectly to any employment or service rendered by that

person will be treated as taxable income. Under Income tax assessment act 1997, Section 15-2

(3) any lump sum payment, employment termination payment, dividend etc. included in

assessable income of individual (Taxation rules regarding allowances and other benefits, 2019).

If Elias signs the contract then tax implications will be as follows:

According to the Income tax assessment act 1997, 2000 dollar per game and 10000 dollar

of bonus will be added to the assessable income of Elias if the agreements is being

accepted by him as it is allowable expense under this act.

Taxation rule Income tax assessment act 1997, states that lump sum payments are not

added to the taxable income so the payment of 150000 dollar will not be considered as

the taxable amount. Nature of this money is capital because it will be received as a lump

2

Club is 127000 Dollar which is received from non members. Income tax assessment tax act 1997

section 75 states that income which is received from members of a firm is not treated as receipts

from members are not revenues these are monetary resources raised by using contribution of

internal persons (Taxation rules for Mutuality concept, 2018). Total income which will added to

the assessable income of The Maxwell Golf Club is 127000 dollars in which 40% of total green

fees, 50% of total restaurant and bar operations and 75% of Gaming activities. These are 32000,

20000 and 75000 dollar for all the activities.

Question 2:

Jamile Elias is a player who is playing Rugby from the side of Oberon Tigers in the

Group 10 and winning the best and fairest award since last two years. In summer Sydney

Thunder is also represented by him in the Big Bash League and most probably he will be

selected for Australian T-20 Side. Several negotiations are made by Canterbury Bulldogs Rugby

Club and Jamile Elias has signed a contract with this club (Cox, 2015). The proposal which was

made by the club are match payments of 2000 dollar per match, 10000 dollar as bonus if the

team is able to be the part of top 8 teams at the ned of the season. They have also proposed a

clause regarding lump sum payment of 150000 dollar in which Jamile Elias is agreeing to play

rugby league exclusively and give up the cricket.

According to Income tax assessment act 1997, Section 15-2 (1) incomes which is

received as compensation, allowances, gratitudes, premiums and bonuses that are received by an

individuals in relation directly or indirectly to any employment or service rendered by that

person will be treated as taxable income. Under Income tax assessment act 1997, Section 15-2

(3) any lump sum payment, employment termination payment, dividend etc. included in

assessable income of individual (Taxation rules regarding allowances and other benefits, 2019).

If Elias signs the contract then tax implications will be as follows:

According to the Income tax assessment act 1997, 2000 dollar per game and 10000 dollar

of bonus will be added to the assessable income of Elias if the agreements is being

accepted by him as it is allowable expense under this act.

Taxation rule Income tax assessment act 1997, states that lump sum payments are not

added to the taxable income so the payment of 150000 dollar will not be considered as

the taxable amount. Nature of this money is capital because it will be received as a lump

2

sum payment to Jamile Elias. It is not allowed under this act because it is considered as

capital expenditure and all of them are not considered as the part of assessable incomes

(Dabscheck, 2015).

Question 3:

Legal expenses around 500000 dollars are made by Sydney Sports Ltd. in order to protect

its exclusive rights agreement with Sydney Rugby Union for the purpose of televising all major

club rugby fixtures in Sydney (Hills and Walker, 2017). It is considered as the sole asset of the

club. According to income tax assessment act 1922- 1934 sec 23 (1) the expenses that are made

for the purpose of gaining or producing assessable income can be deducted from taxable income

for the year. According to this rule of taxation the amount which has been spent by Sydney

Sports Ltd. in October 2018 to protect its exclusive rights agreement is deductible for the year

ending 2018-19 from the income. While calculating assessable income the taxpayer is required to

deduct all outgoings and losses which are actually incurred in the process of producing or

gaining (Tax deduction regarding expenditure, 2019). Hence, 150000 dollars can be deducted by

Sydney Sports Club from its total incomes at the end of the year. Deduction of 150000 will be

allowed to Sydney Sports Club as the expenditure made by the organisation not Super Sports

club. According to this act all the expenses that are made for business purpose are allowed to be

deducted from assessable income but the expenditures that are made for personal issues are not

allowed to be deducted from assessable income.

Question 4:

A warehouse is being acquired by Max Fit Gym on 1 July 2017 in order to convert it into

24 hour Gym. Almost 750000 dollars are being spent by the Gym to covert or upgrade the

warehouse in a reasonable working condition (Sawyer, 2014). According to Income tax

assessment act 1997 Sec T 25 (10) the amount of 750000 dollars is not deductible from the

assessable income of Max Fit Gym as its nature is capital. Under this act such types of

expenditures that are incurred for repairs of premises or a depreciating asset of the organisation.

If the property where repair is made is partially used for business purpose then partial amount of

expense will be deducted from annual income. Capital expenditures are not deducted under this

section of income tax. This same thing also happened to another case which is FCT V Western

Suburbs Cinemas Ltd (1952) 86 CLR 102 under which ceiling of a cinema hall is being replaced

by a tin ceiling which is having end number of benefits (Case related to repair, 2019). It is an

3

capital expenditure and all of them are not considered as the part of assessable incomes

(Dabscheck, 2015).

Question 3:

Legal expenses around 500000 dollars are made by Sydney Sports Ltd. in order to protect

its exclusive rights agreement with Sydney Rugby Union for the purpose of televising all major

club rugby fixtures in Sydney (Hills and Walker, 2017). It is considered as the sole asset of the

club. According to income tax assessment act 1922- 1934 sec 23 (1) the expenses that are made

for the purpose of gaining or producing assessable income can be deducted from taxable income

for the year. According to this rule of taxation the amount which has been spent by Sydney

Sports Ltd. in October 2018 to protect its exclusive rights agreement is deductible for the year

ending 2018-19 from the income. While calculating assessable income the taxpayer is required to

deduct all outgoings and losses which are actually incurred in the process of producing or

gaining (Tax deduction regarding expenditure, 2019). Hence, 150000 dollars can be deducted by

Sydney Sports Club from its total incomes at the end of the year. Deduction of 150000 will be

allowed to Sydney Sports Club as the expenditure made by the organisation not Super Sports

club. According to this act all the expenses that are made for business purpose are allowed to be

deducted from assessable income but the expenditures that are made for personal issues are not

allowed to be deducted from assessable income.

Question 4:

A warehouse is being acquired by Max Fit Gym on 1 July 2017 in order to convert it into

24 hour Gym. Almost 750000 dollars are being spent by the Gym to covert or upgrade the

warehouse in a reasonable working condition (Sawyer, 2014). According to Income tax

assessment act 1997 Sec T 25 (10) the amount of 750000 dollars is not deductible from the

assessable income of Max Fit Gym as its nature is capital. Under this act such types of

expenditures that are incurred for repairs of premises or a depreciating asset of the organisation.

If the property where repair is made is partially used for business purpose then partial amount of

expense will be deducted from annual income. Capital expenditures are not deducted under this

section of income tax. This same thing also happened to another case which is FCT V Western

Suburbs Cinemas Ltd (1952) 86 CLR 102 under which ceiling of a cinema hall is being replaced

by a tin ceiling which is having end number of benefits (Case related to repair, 2019). It is an

3

improvement which is made by the payer and he was not entitles for the deduction. According to

the taxation rules all the expenses that are made for long term business operation purposes are

not deductible under taxation laws as these are considered as capital expenditures (Tax deduction

regarding repair or up-gradation, 2019).

CONCLUSION

From the above project report it has been concluded that there are various types of

legislations that are imposed by governmental bodies on the business entities of different sectors.

These are related to taxation, business operations, policies and procedures that are used by

organisations. It is vital for sport businesses to comply with all of them so that operational

activities can be conducted without any governmental interference. While calculating taxable

income it is very important for enterprises to analyse all the rules and regulations and then apply

for deductions so that appropriate tax can be paid to the legal bodies.

4

the taxation rules all the expenses that are made for long term business operation purposes are

not deductible under taxation laws as these are considered as capital expenditures (Tax deduction

regarding repair or up-gradation, 2019).

CONCLUSION

From the above project report it has been concluded that there are various types of

legislations that are imposed by governmental bodies on the business entities of different sectors.

These are related to taxation, business operations, policies and procedures that are used by

organisations. It is vital for sport businesses to comply with all of them so that operational

activities can be conducted without any governmental interference. While calculating taxable

income it is very important for enterprises to analyse all the rules and regulations and then apply

for deductions so that appropriate tax can be paid to the legal bodies.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Anagnostopoulos, C., Byers, T., & Shilbury, D. (2014). Corporate social responsibility in

professional team sport organisations: Towards a theory of decision-making. European

Sport Management Quarterly. 14(3). 259-281.

Brockett, C. (2017). Australia: Evolution and Motivators of National Sport Policy. In Sport

Policy Systems and Sport Federations (pp. 19-40). Palgrave Macmillan, London.

Cox, J. (Ed.). (2015). Business Law. Oxford University Press, USA.

Dabscheck, B. (2015). Sweated labour, literally speaking: the case of australian jockeys. In The

Sports Business in The Pacific Rim (pp. 311-331). Springer, Cham.

Hills, S., & Walker, M. (2017). Sport and Social Development: Evaluating a Professional Sport

League’s Domestic Violence and Sexual Abuse Camp. Journal of Applied Sport

Management. 9(4).

Sawyer, C. (2014). Don't Dissolve the Nerve Center: A Status-Linked Citizenship Test for

Principal Place of Business. BCL Rev.. 55. 641.

Online

Taxation rules for Mutuality concept. 2018. [Online]. Available through:

<https://www.ato.gov.au/Non-profit/Your-organisation/In-detail/Income-tax/Mutuality-

and-taxable-income/?page=8>

Taxation rules regarding allowances and other benefits. 2019. [Online]. Available through:

<https://iknow.cch.com.au/document/atagUio838125sl36877295/section-15-2-

allowances-and-other-things-provided-in-respect-of-employment-or-services>

Tax deduction regarding expenditure. 2019. [Online]. Available through:

<https://www.ato.gov.au/law/view/document?DocID=JUD/61CLR337/00002>

Tax deduction regarding repair or up-gradation. 2019. [online]. Available through:

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s25.10.html>

Case related to repair. 2019. [Online]. Available through:

<https://www.coursehero.com/file/p48o931/FCT-v-Western-Suburbs-Cinemas-Ltd-

1952-86-CLR-102-The-ceiling-tin-sheeting-in-a/>

5

Books and Journals:

Anagnostopoulos, C., Byers, T., & Shilbury, D. (2014). Corporate social responsibility in

professional team sport organisations: Towards a theory of decision-making. European

Sport Management Quarterly. 14(3). 259-281.

Brockett, C. (2017). Australia: Evolution and Motivators of National Sport Policy. In Sport

Policy Systems and Sport Federations (pp. 19-40). Palgrave Macmillan, London.

Cox, J. (Ed.). (2015). Business Law. Oxford University Press, USA.

Dabscheck, B. (2015). Sweated labour, literally speaking: the case of australian jockeys. In The

Sports Business in The Pacific Rim (pp. 311-331). Springer, Cham.

Hills, S., & Walker, M. (2017). Sport and Social Development: Evaluating a Professional Sport

League’s Domestic Violence and Sexual Abuse Camp. Journal of Applied Sport

Management. 9(4).

Sawyer, C. (2014). Don't Dissolve the Nerve Center: A Status-Linked Citizenship Test for

Principal Place of Business. BCL Rev.. 55. 641.

Online

Taxation rules for Mutuality concept. 2018. [Online]. Available through:

<https://www.ato.gov.au/Non-profit/Your-organisation/In-detail/Income-tax/Mutuality-

and-taxable-income/?page=8>

Taxation rules regarding allowances and other benefits. 2019. [Online]. Available through:

<https://iknow.cch.com.au/document/atagUio838125sl36877295/section-15-2-

allowances-and-other-things-provided-in-respect-of-employment-or-services>

Tax deduction regarding expenditure. 2019. [Online]. Available through:

<https://www.ato.gov.au/law/view/document?DocID=JUD/61CLR337/00002>

Tax deduction regarding repair or up-gradation. 2019. [online]. Available through:

<http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s25.10.html>

Case related to repair. 2019. [Online]. Available through:

<https://www.coursehero.com/file/p48o931/FCT-v-Western-Suburbs-Cinemas-Ltd-

1952-86-CLR-102-The-ceiling-tin-sheeting-in-a/>

5

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.